Management Accounting Report: Cost Analysis for Heatrod Element Ltd

VerifiedAdded on 2021/02/21

|14

|3885

|423

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Heatrod Element Ltd, a UK-based manufacturer of household heaters. The report explores various management accounting systems, including price optimization, cost accounting, job costing, and inventory management systems like LIFO, FIFO, and AVOC. It delves into the presentation of financial information through management accounting reports, such as performance reports, budget reports, and accounting receivable reports. The core of the report focuses on calculating costs using absorption costing and marginal costing techniques, comparing their impact on net profit, and analyzing the reasons for profit variations. Additionally, the report examines the use of budgets for planning and control, and the identification of financial problems within the company, offering insights into how these tools support effective decision-making and financial management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and several types of essential systems................................................1

TASK 2............................................................................................................................................3

Calculate cost using appropriate techniques...............................................................................3

(b) Reason for analysing variations in profit...............................................................................6

TASK 3............................................................................................................................................7

Using budgets for planning and control......................................................................................7

TASK 4............................................................................................................................................9

Identifying financial problem......................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and several types of essential systems................................................1

TASK 2............................................................................................................................................3

Calculate cost using appropriate techniques...............................................................................3

(b) Reason for analysing variations in profit...............................................................................6

TASK 3............................................................................................................................................7

Using budgets for planning and control......................................................................................7

TASK 4............................................................................................................................................9

Identifying financial problem......................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is the process of analysing business costs and operations to

prepare internal financial report, records and account for the managers (Arroyo, 2012). These

reports provide help to manager in decision making process to acquire business goals and

objectives. In general terms it is the act of making sense of financial and costing data and

interpreting that data into useful information for management and officers within an

organization. In this report, to better understand the topic of relevant topic manufacturing

Heatrod Element Ltd which based on UK and manufacturing household heaters at reasonable

prices. The overall report focus on the different types of management accounting system as well

as report. There are calculating net profit through marginal costing and absorption costing.

Additionally, determine several planning tools and accounting tools can help to face off various

financial problem.

TASK 1

Management accounting and several types of essential systems

In modern era, in every organisation required to systematic approaches through internal

manager that use to manage and control the basic needs of business. Management accounting is

systematic process which is used to collect, examine, measure and evaluate meaning financial

information and posting them in correct accounts so that valuable decision is made to improve

and increase profitability of business operations. Heatrod Element Ltd can use different types of

management accounting system these are -

Price optimisation system – The particular system based on the mathematical analysis

that carry out the information regarding to product and services by the fluctuation in price. It

records the information then applies it on cost and inventory to assistance and deciding price to

increase the profit. In Heatrod Elements Ltd, this system can help to set best prices as per the

requirement of customers and it will help to company to increase gross provide and production

(Chenhall and Moers, 2015) .

Cost accounting system – It is mostly applied by manufacturing company in order to

computation of valuation of inventory, profitability and cost control. Cost accounting system

tacking the process of inventory (i.e. raw material, work in process and finished goods) to

1

Management accounting is the process of analysing business costs and operations to

prepare internal financial report, records and account for the managers (Arroyo, 2012). These

reports provide help to manager in decision making process to acquire business goals and

objectives. In general terms it is the act of making sense of financial and costing data and

interpreting that data into useful information for management and officers within an

organization. In this report, to better understand the topic of relevant topic manufacturing

Heatrod Element Ltd which based on UK and manufacturing household heaters at reasonable

prices. The overall report focus on the different types of management accounting system as well

as report. There are calculating net profit through marginal costing and absorption costing.

Additionally, determine several planning tools and accounting tools can help to face off various

financial problem.

TASK 1

Management accounting and several types of essential systems

In modern era, in every organisation required to systematic approaches through internal

manager that use to manage and control the basic needs of business. Management accounting is

systematic process which is used to collect, examine, measure and evaluate meaning financial

information and posting them in correct accounts so that valuable decision is made to improve

and increase profitability of business operations. Heatrod Element Ltd can use different types of

management accounting system these are -

Price optimisation system – The particular system based on the mathematical analysis

that carry out the information regarding to product and services by the fluctuation in price. It

records the information then applies it on cost and inventory to assistance and deciding price to

increase the profit. In Heatrod Elements Ltd, this system can help to set best prices as per the

requirement of customers and it will help to company to increase gross provide and production

(Chenhall and Moers, 2015) .

Cost accounting system – It is mostly applied by manufacturing company in order to

computation of valuation of inventory, profitability and cost control. Cost accounting system

tacking the process of inventory (i.e. raw material, work in process and finished goods) to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysis actual cost of production. In the context to Heatrod Element Ltd used the system to

evaluate total cost involved while manufacturing valuable product.

Job costing system – It is kind of cost accounting system where cost of a single unit has

been calculated. The particular system can be used to calculate value of different types of

product and it is especially used by manufacturing industry. In reference to Heatrod Element Ltd

can use the system to analysis the total number of employees who can involve in production unit

as well as set prices of heater to focus on overall expenses.

Inventory management system – It is a system that include of producing and oversees the

inventory of the firm. For each organisation inventory management system plays role of success

key because it can track a record of stock at each stage. As a result it can help to reduce wastage

and increase productivity. In context to Heatrod Element Ltd can apply the system in order to

know production units and aware for stocks.

LIFO – Last in first out is method of inventory which can defined that stock come in last

that was going first out.

FIFO – First in first out selling those stock which is come first in the company.

AVOC – In the method used material on average cost for the production.

Presenting financial information

Through management accounting provide financial information to top management

which is related to internal system and record into reports. These Information should be relevant

to the user, reliable, up to date and accurate because it can help to decision making process and

understand to actual position of the company (DRURY, 2013) .

Different types of managerial accounting reports

Management accounting reports are the important parts of the reports that can help to

understand business activities of different departments. The reports will be prepared by manager

of company and present into financial and statistical form. It is mainly prepare to take short term

decision on daily basis and provide way to business finance. A manager of the Heatrod Element

Ltd prepare different types of management accounting reports to present actual performance and

analysis future improvement and development -

Performance Report – The performance report present all detailed information of

company as well as employees. With the help of report analysis budgeted and actual variance

and take appropriate action if the variance is unfavourable. If variance is favourable that time

2

evaluate total cost involved while manufacturing valuable product.

Job costing system – It is kind of cost accounting system where cost of a single unit has

been calculated. The particular system can be used to calculate value of different types of

product and it is especially used by manufacturing industry. In reference to Heatrod Element Ltd

can use the system to analysis the total number of employees who can involve in production unit

as well as set prices of heater to focus on overall expenses.

Inventory management system – It is a system that include of producing and oversees the

inventory of the firm. For each organisation inventory management system plays role of success

key because it can track a record of stock at each stage. As a result it can help to reduce wastage

and increase productivity. In context to Heatrod Element Ltd can apply the system in order to

know production units and aware for stocks.

LIFO – Last in first out is method of inventory which can defined that stock come in last

that was going first out.

FIFO – First in first out selling those stock which is come first in the company.

AVOC – In the method used material on average cost for the production.

Presenting financial information

Through management accounting provide financial information to top management

which is related to internal system and record into reports. These Information should be relevant

to the user, reliable, up to date and accurate because it can help to decision making process and

understand to actual position of the company (DRURY, 2013) .

Different types of managerial accounting reports

Management accounting reports are the important parts of the reports that can help to

understand business activities of different departments. The reports will be prepared by manager

of company and present into financial and statistical form. It is mainly prepare to take short term

decision on daily basis and provide way to business finance. A manager of the Heatrod Element

Ltd prepare different types of management accounting reports to present actual performance and

analysis future improvement and development -

Performance Report – The performance report present all detailed information of

company as well as employees. With the help of report analysis budgeted and actual variance

and take appropriate action if the variance is unfavourable. If variance is favourable that time

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provide reward to those employees who contribute effectively. The internal manager of Heatrod

Element Ltd produce the report to compute and measure for better improvement.

Budget Report – Every organisation can prepare budget report to predict the cost and

expenses to analysing future situation. Through budget report examine all department to estimate

expenses then effectively prepare report. An ideal budget report help to user to make comparison

between estimated and actual results. The Heatrod Element Ltd can prepare report to prepare

plan for increase profitability and execute as per the plans (Hiebl, 2014).

Accounting Receivable Report – The particular report presents summary of the accounts

receivables. The report prepare by manager to define detail information to those person who can

take money from company and payment in future. A business can collect payments from their

customers and unused credit memos which are not collected yet. To increase sales volume

prepare report by Heatrod Element Ltd to sale out heater on credit basis and provide advantage to

create systematic list of customers.

TASK 2

Calculate cost using appropriate techniques

Cost – It is indicate the amount of the money which are spend by business in order to

create or manufacturing of goods or services. Cost contains of all required cost to get an asset in

place and ready to use. There are defined different types of cost - Direct & indirect cost – Direct cost can be described in accurately way and applied in

directly manner. It is typically provide advantage a single cost object therefore categorise

of any cost either as direct cost or indirect cost. Indirect cost are those expenses which

can apply to more than one business activity as well as can not assign indirect expenses

regarding to specific cost objects (Kokubu and Kitada, 2015). Fixed and variable cost – When a cost can not change after change in business activities

that are known as fixed cost. A variable cost will change as per the requirement and

affect by change in the level of activity to material cost. For example – direct cost

Product and non production cost – The production cost related to manufacturing of

products like material and labour cost on the other side non production cost are

considering as other cost of the business like administrative cost and selling costs.

3

Element Ltd produce the report to compute and measure for better improvement.

Budget Report – Every organisation can prepare budget report to predict the cost and

expenses to analysing future situation. Through budget report examine all department to estimate

expenses then effectively prepare report. An ideal budget report help to user to make comparison

between estimated and actual results. The Heatrod Element Ltd can prepare report to prepare

plan for increase profitability and execute as per the plans (Hiebl, 2014).

Accounting Receivable Report – The particular report presents summary of the accounts

receivables. The report prepare by manager to define detail information to those person who can

take money from company and payment in future. A business can collect payments from their

customers and unused credit memos which are not collected yet. To increase sales volume

prepare report by Heatrod Element Ltd to sale out heater on credit basis and provide advantage to

create systematic list of customers.

TASK 2

Calculate cost using appropriate techniques

Cost – It is indicate the amount of the money which are spend by business in order to

create or manufacturing of goods or services. Cost contains of all required cost to get an asset in

place and ready to use. There are defined different types of cost - Direct & indirect cost – Direct cost can be described in accurately way and applied in

directly manner. It is typically provide advantage a single cost object therefore categorise

of any cost either as direct cost or indirect cost. Indirect cost are those expenses which

can apply to more than one business activity as well as can not assign indirect expenses

regarding to specific cost objects (Kokubu and Kitada, 2015). Fixed and variable cost – When a cost can not change after change in business activities

that are known as fixed cost. A variable cost will change as per the requirement and

affect by change in the level of activity to material cost. For example – direct cost

Product and non production cost – The production cost related to manufacturing of

products like material and labour cost on the other side non production cost are

considering as other cost of the business like administrative cost and selling costs.

3

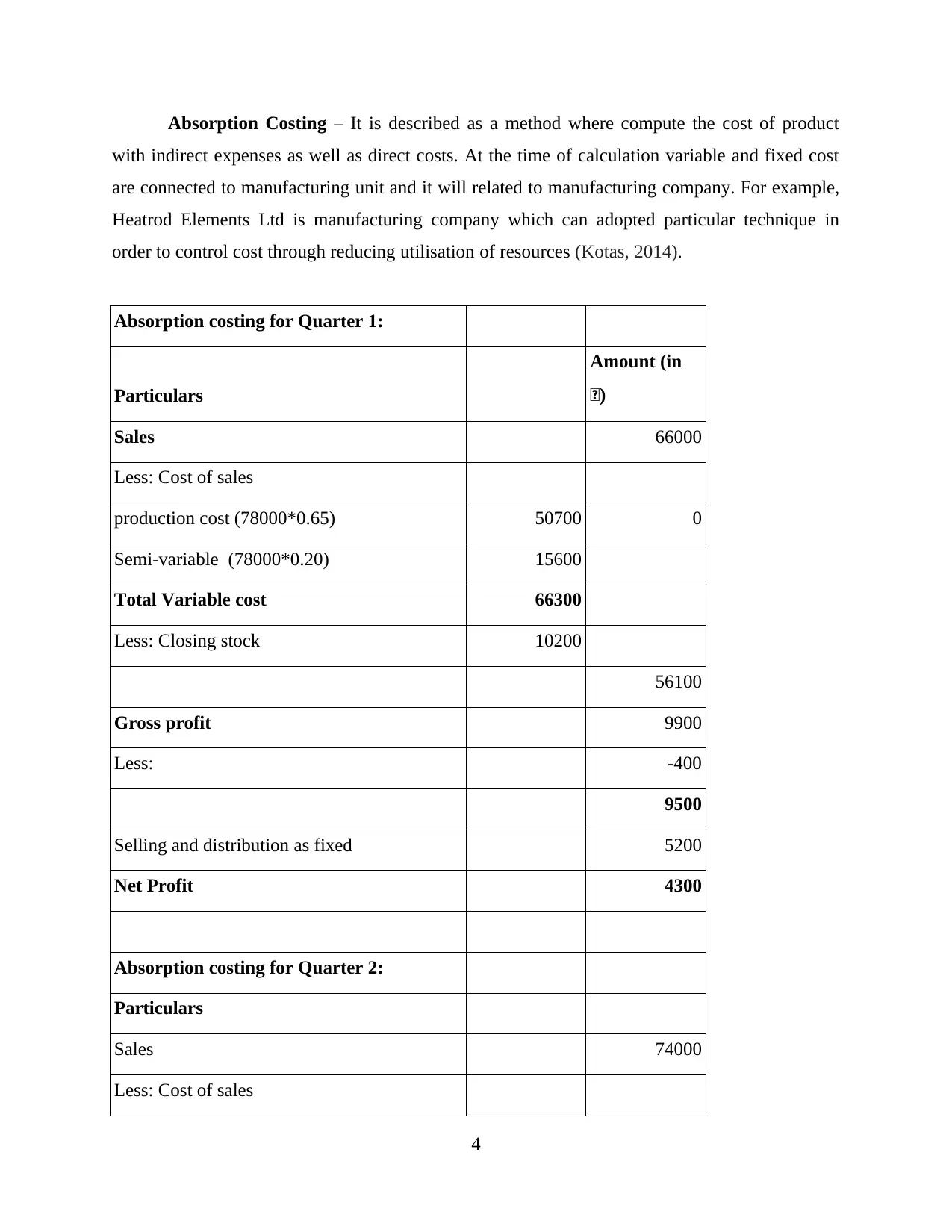

Absorption Costing – It is described as a method where compute the cost of product

with indirect expenses as well as direct costs. At the time of calculation variable and fixed cost

are connected to manufacturing unit and it will related to manufacturing company. For example,

Heatrod Elements Ltd is manufacturing company which can adopted particular technique in

order to control cost through reducing utilisation of resources (Kotas, 2014).

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

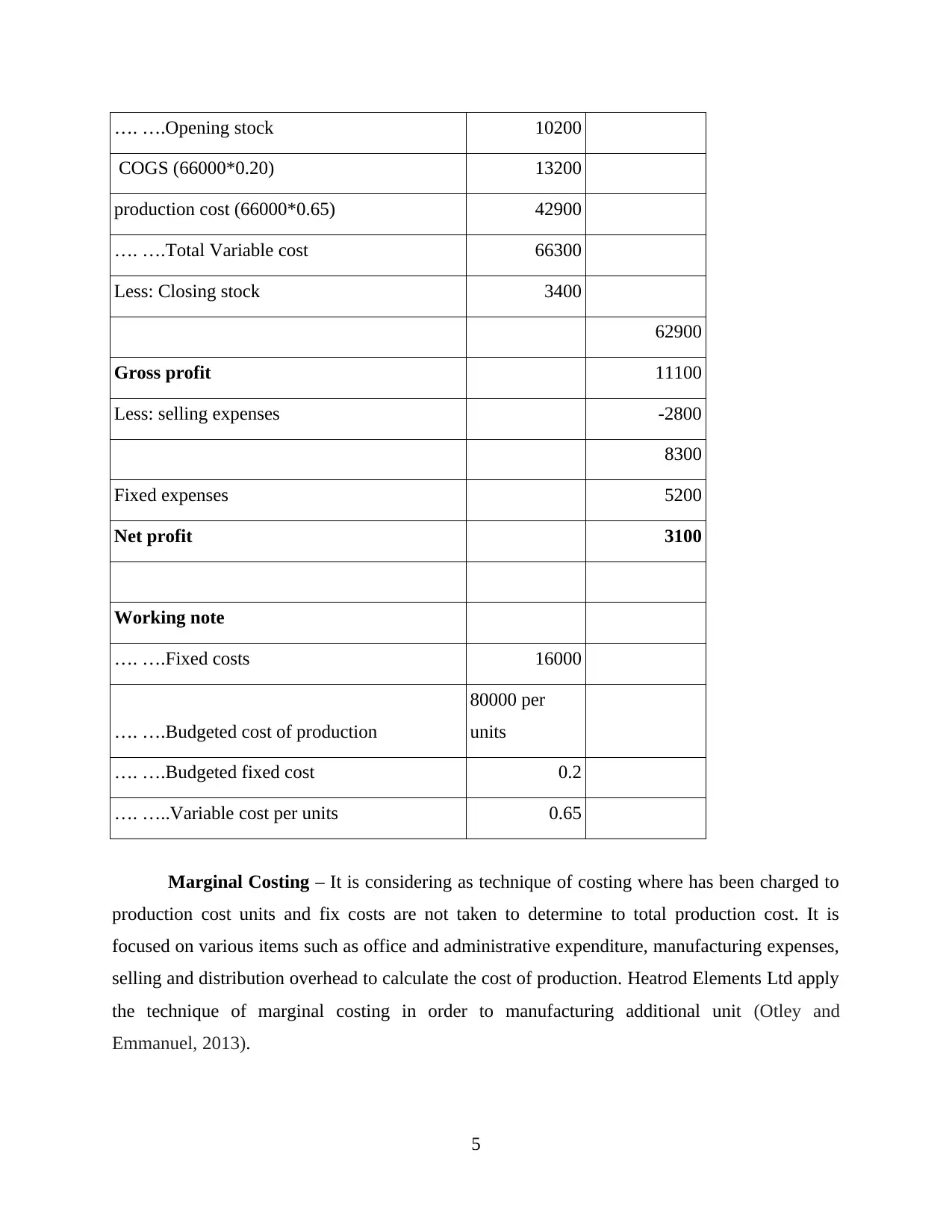

Particulars

Sales 74000

Less: Cost of sales

4

with indirect expenses as well as direct costs. At the time of calculation variable and fixed cost

are connected to manufacturing unit and it will related to manufacturing company. For example,

Heatrod Elements Ltd is manufacturing company which can adopted particular technique in

order to control cost through reducing utilisation of resources (Kotas, 2014).

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

…. ….Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

…. ….Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

…. ….Fixed costs 16000

…. ….Budgeted cost of production

80000 per

units

…. ….Budgeted fixed cost 0.2

…. …..Variable cost per units 0.65

Marginal Costing – It is considering as technique of costing where has been charged to

production cost units and fix costs are not taken to determine to total production cost. It is

focused on various items such as office and administrative expenditure, manufacturing expenses,

selling and distribution overhead to calculate the cost of production. Heatrod Elements Ltd apply

the technique of marginal costing in order to manufacturing additional unit (Otley and

Emmanuel, 2013).

5

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

…. ….Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

…. ….Fixed costs 16000

…. ….Budgeted cost of production

80000 per

units

…. ….Budgeted fixed cost 0.2

…. …..Variable cost per units 0.65

Marginal Costing – It is considering as technique of costing where has been charged to

production cost units and fix costs are not taken to determine to total production cost. It is

focused on various items such as office and administrative expenditure, manufacturing expenses,

selling and distribution overhead to calculate the cost of production. Heatrod Elements Ltd apply

the technique of marginal costing in order to manufacturing additional unit (Otley and

Emmanuel, 2013).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

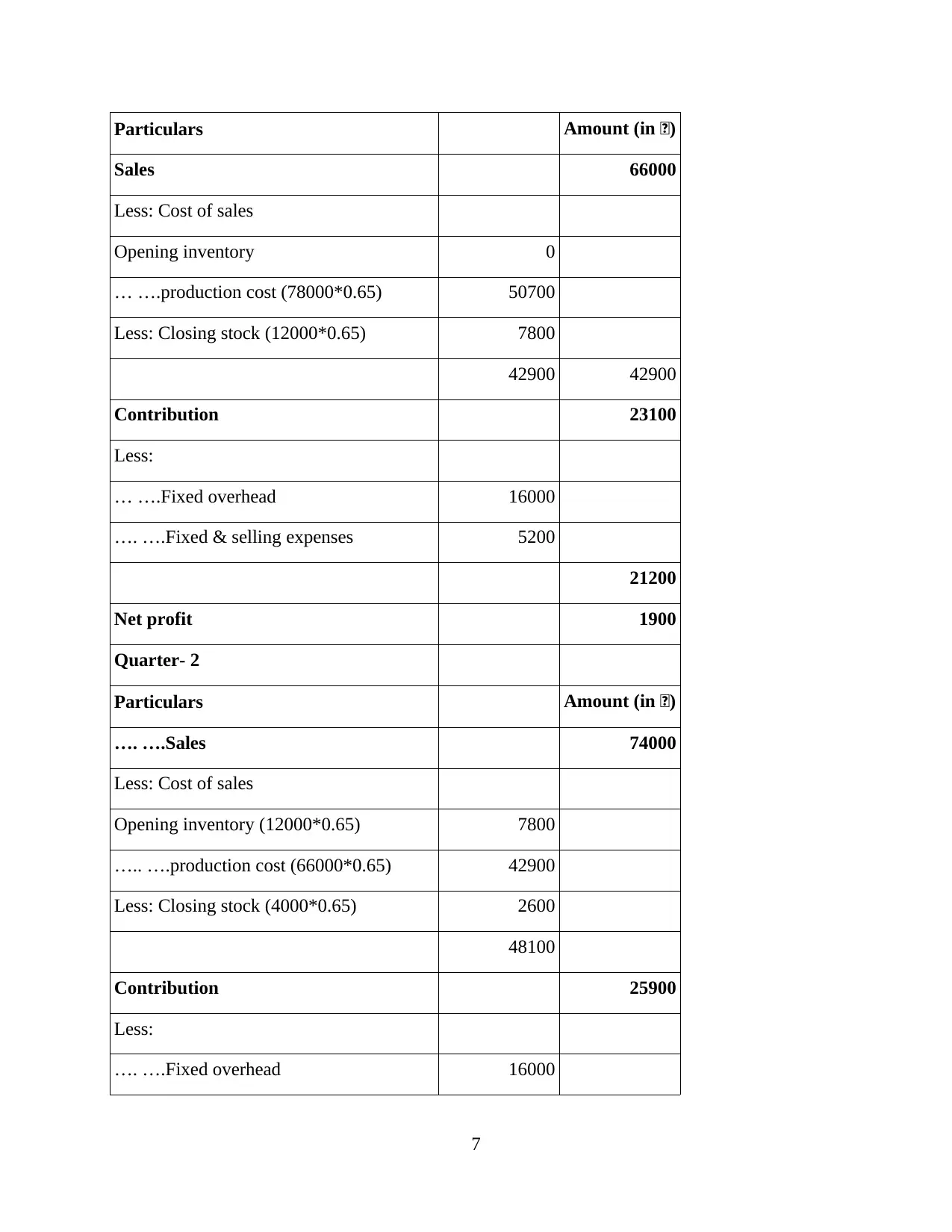

Quarter 1

6

6

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

… ….production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

… ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

…. ….Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

7

Sales 66000

Less: Cost of sales

Opening inventory 0

… ….production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

… ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

…. ….Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

…. ….Fixed & selling expenses 5200

21200

Net profit 4700

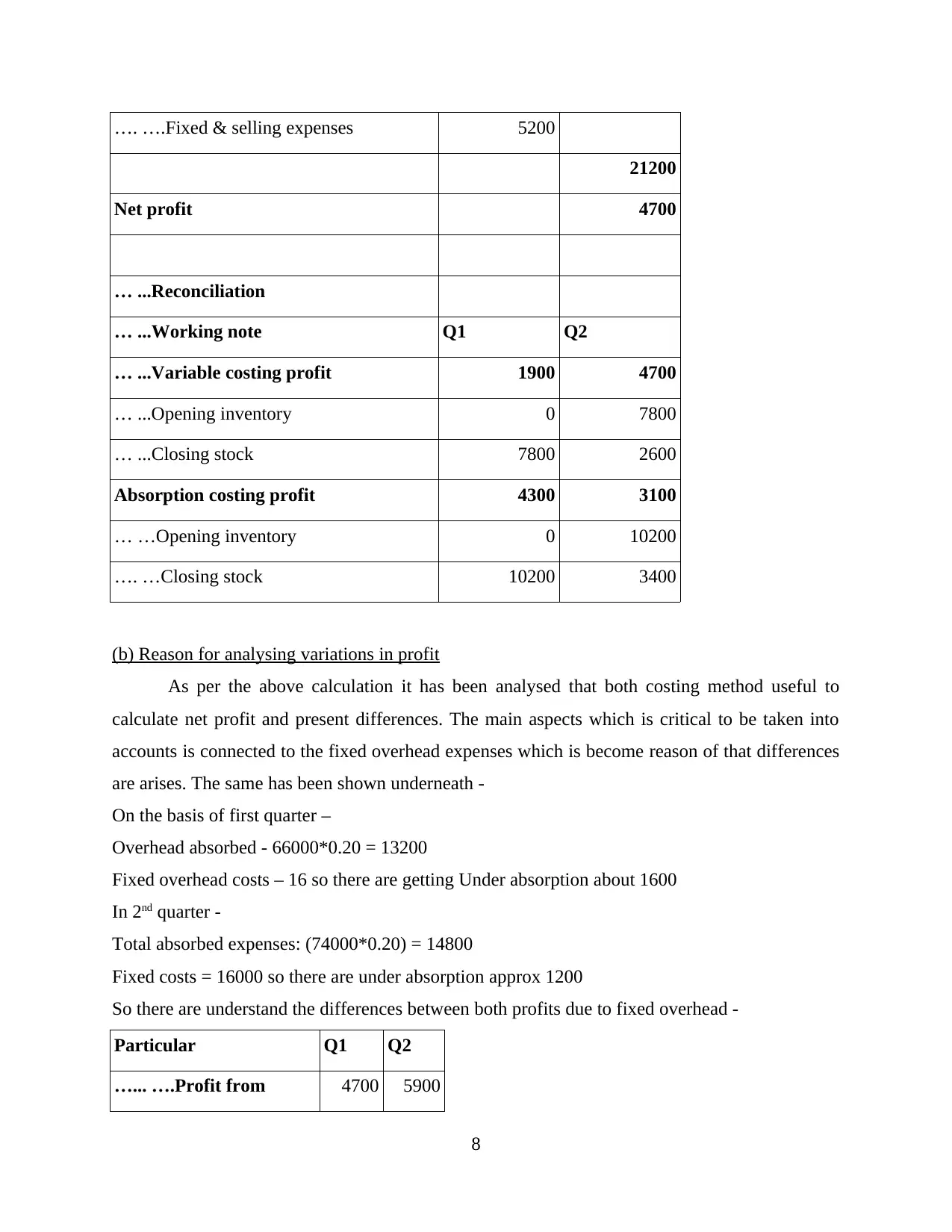

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

(b) Reason for analysing variations in profit

As per the above calculation it has been analysed that both costing method useful to

calculate net profit and present differences. The main aspects which is critical to be taken into

accounts is connected to the fixed overhead expenses which is become reason of that differences

are arises. The same has been shown underneath -

On the basis of first quarter –

Overhead absorbed - 66000*0.20 = 13200

Fixed overhead costs – 16 so there are getting Under absorption about 1600

In 2nd quarter -

Total absorbed expenses: (74000*0.20) = 14800

Fixed costs = 16000 so there are under absorption approx 1200

So there are understand the differences between both profits due to fixed overhead -

Particular Q1 Q2

…... ….Profit from 4700 5900

8

21200

Net profit 4700

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

(b) Reason for analysing variations in profit

As per the above calculation it has been analysed that both costing method useful to

calculate net profit and present differences. The main aspects which is critical to be taken into

accounts is connected to the fixed overhead expenses which is become reason of that differences

are arises. The same has been shown underneath -

On the basis of first quarter –

Overhead absorbed - 66000*0.20 = 13200

Fixed overhead costs – 16 so there are getting Under absorption about 1600

In 2nd quarter -

Total absorbed expenses: (74000*0.20) = 14800

Fixed costs = 16000 so there are under absorption approx 1200

So there are understand the differences between both profits due to fixed overhead -

Particular Q1 Q2

…... ….Profit from 4700 5900

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

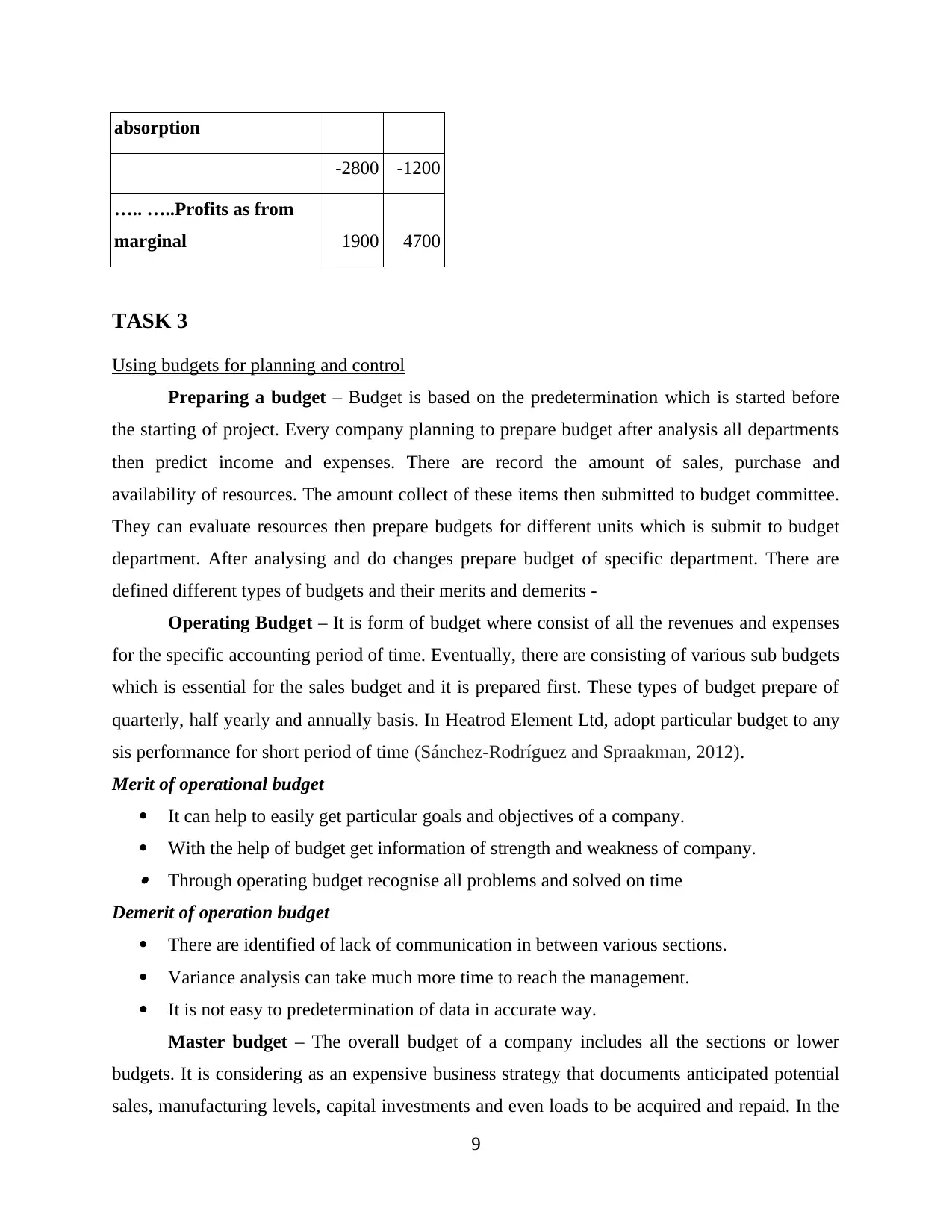

absorption

-2800 -1200

….. …..Profits as from

marginal 1900 4700

TASK 3

Using budgets for planning and control

Preparing a budget – Budget is based on the predetermination which is started before

the starting of project. Every company planning to prepare budget after analysis all departments

then predict income and expenses. There are record the amount of sales, purchase and

availability of resources. The amount collect of these items then submitted to budget committee.

They can evaluate resources then prepare budgets for different units which is submit to budget

department. After analysing and do changes prepare budget of specific department. There are

defined different types of budgets and their merits and demerits -

Operating Budget – It is form of budget where consist of all the revenues and expenses

for the specific accounting period of time. Eventually, there are consisting of various sub budgets

which is essential for the sales budget and it is prepared first. These types of budget prepare of

quarterly, half yearly and annually basis. In Heatrod Element Ltd, adopt particular budget to any

sis performance for short period of time (Sánchez-Rodríguez and Spraakman, 2012).

Merit of operational budget

It can help to easily get particular goals and objectives of a company.

With the help of budget get information of strength and weakness of company. Through operating budget recognise all problems and solved on time

Demerit of operation budget

There are identified of lack of communication in between various sections.

Variance analysis can take much more time to reach the management.

It is not easy to predetermination of data in accurate way.

Master budget – The overall budget of a company includes all the sections or lower

budgets. It is considering as an expensive business strategy that documents anticipated potential

sales, manufacturing levels, capital investments and even loads to be acquired and repaid. In the

9

-2800 -1200

….. …..Profits as from

marginal 1900 4700

TASK 3

Using budgets for planning and control

Preparing a budget – Budget is based on the predetermination which is started before

the starting of project. Every company planning to prepare budget after analysis all departments

then predict income and expenses. There are record the amount of sales, purchase and

availability of resources. The amount collect of these items then submitted to budget committee.

They can evaluate resources then prepare budgets for different units which is submit to budget

department. After analysing and do changes prepare budget of specific department. There are

defined different types of budgets and their merits and demerits -

Operating Budget – It is form of budget where consist of all the revenues and expenses

for the specific accounting period of time. Eventually, there are consisting of various sub budgets

which is essential for the sales budget and it is prepared first. These types of budget prepare of

quarterly, half yearly and annually basis. In Heatrod Element Ltd, adopt particular budget to any

sis performance for short period of time (Sánchez-Rodríguez and Spraakman, 2012).

Merit of operational budget

It can help to easily get particular goals and objectives of a company.

With the help of budget get information of strength and weakness of company. Through operating budget recognise all problems and solved on time

Demerit of operation budget

There are identified of lack of communication in between various sections.

Variance analysis can take much more time to reach the management.

It is not easy to predetermination of data in accurate way.

Master budget – The overall budget of a company includes all the sections or lower

budgets. It is considering as an expensive business strategy that documents anticipated potential

sales, manufacturing levels, capital investments and even loads to be acquired and repaid. In the

9

context of, Heatrod Element Ltd follow the budget calculate of balance sheet as well as income

statement.

Merit of master budget

Through particular budget analysis overview of the budget which define financial

position of Heatrod Element Ltd. It can help to supplying the resources to every sections fairly.

Demerit of master budget

It bring out short information of sectional budget as well as it can not provide minor data

of the lower budget.

It is not easy to update a master budget (Schaltegger and Burritt, 2017).

Cash budget - It is a statement that described about the all cash revenues and

expenditures which is based on assumptions for specific accounting period of time. The

particular budget has been produced after preparing of all budgets such as sales budget, master

budget, capital budget and purchase budget. There are recoded items of capital and revenue

receipts and payments. It is a document which is mainly prepare for external stakeholders and

after publishing can not change easily.

Merit of cash budget

The specific budget can help to minimise the cost and profit maximization. Cash budget influence to think critically and forecast to carefully of company's financial

situation.

Demerit of cash budget

It is difficult to analysis financial information through particular budget because in the

budget can not including non cash items.

Predicted and figures can easily be influenced by ulterior motives.

Pricing Strategies – In present time every business focus on their pricing strategies to attract

more customers. These pricing policies can help to determine the cost and expenses of the

company in effective manner. The Nero Ltd follow the two types of pricing policies in order to

provide support to products at the time of producing in the specific accounting year. It has been

analysed that after the valuation of competition of a commodity to support to customer and

change the business organization. There are defined two methods -

10

statement.

Merit of master budget

Through particular budget analysis overview of the budget which define financial

position of Heatrod Element Ltd. It can help to supplying the resources to every sections fairly.

Demerit of master budget

It bring out short information of sectional budget as well as it can not provide minor data

of the lower budget.

It is not easy to update a master budget (Schaltegger and Burritt, 2017).

Cash budget - It is a statement that described about the all cash revenues and

expenditures which is based on assumptions for specific accounting period of time. The

particular budget has been produced after preparing of all budgets such as sales budget, master

budget, capital budget and purchase budget. There are recoded items of capital and revenue

receipts and payments. It is a document which is mainly prepare for external stakeholders and

after publishing can not change easily.

Merit of cash budget

The specific budget can help to minimise the cost and profit maximization. Cash budget influence to think critically and forecast to carefully of company's financial

situation.

Demerit of cash budget

It is difficult to analysis financial information through particular budget because in the

budget can not including non cash items.

Predicted and figures can easily be influenced by ulterior motives.

Pricing Strategies – In present time every business focus on their pricing strategies to attract

more customers. These pricing policies can help to determine the cost and expenses of the

company in effective manner. The Nero Ltd follow the two types of pricing policies in order to

provide support to products at the time of producing in the specific accounting year. It has been

analysed that after the valuation of competition of a commodity to support to customer and

change the business organization. There are defined two methods -

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.