BFW2751 - Derivatives 1 S1, 2021: Futures Hedging Strategies Analysis

VerifiedAdded on 2022/01/22

|32

|3543

|32

Report

AI Summary

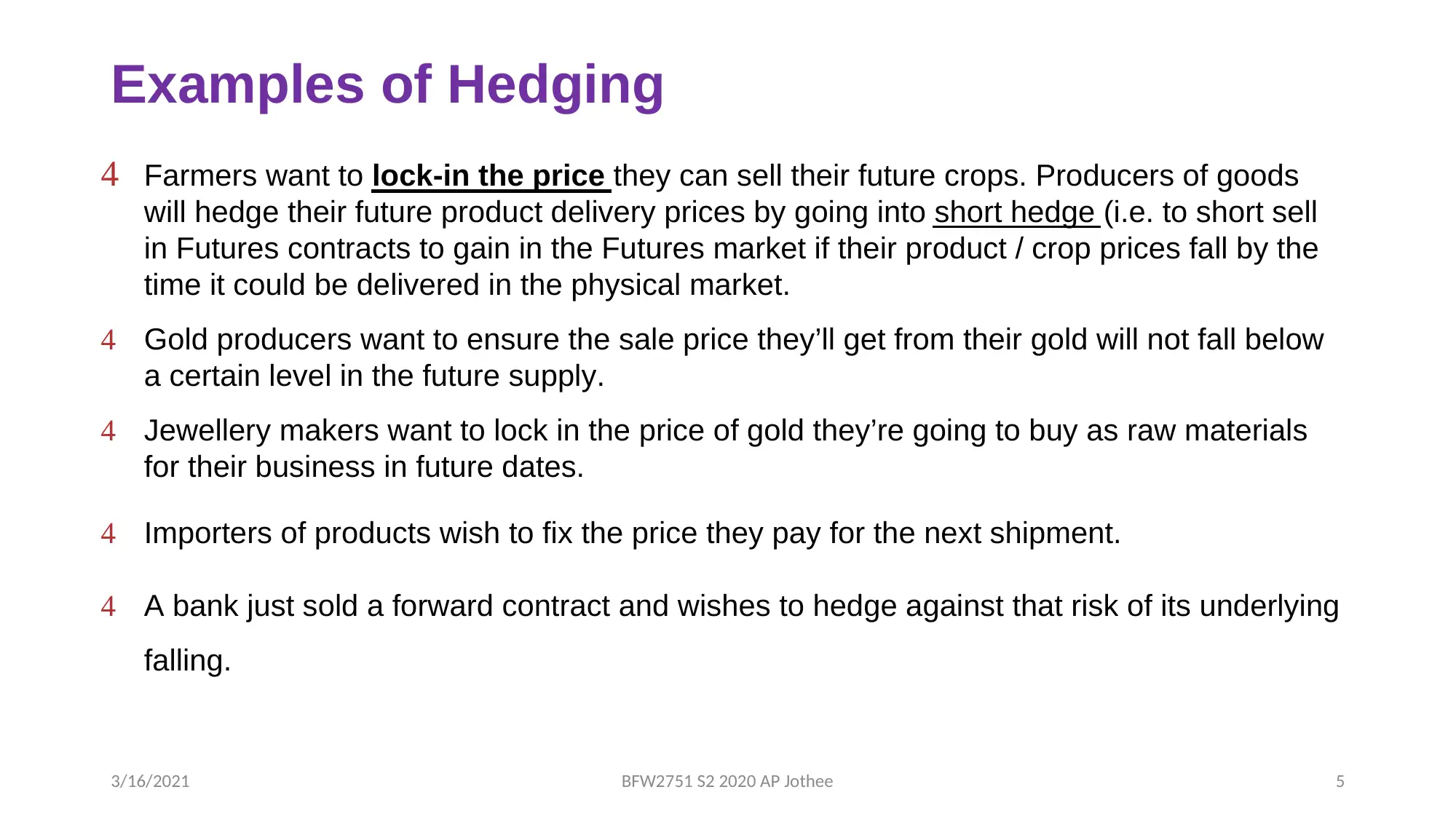

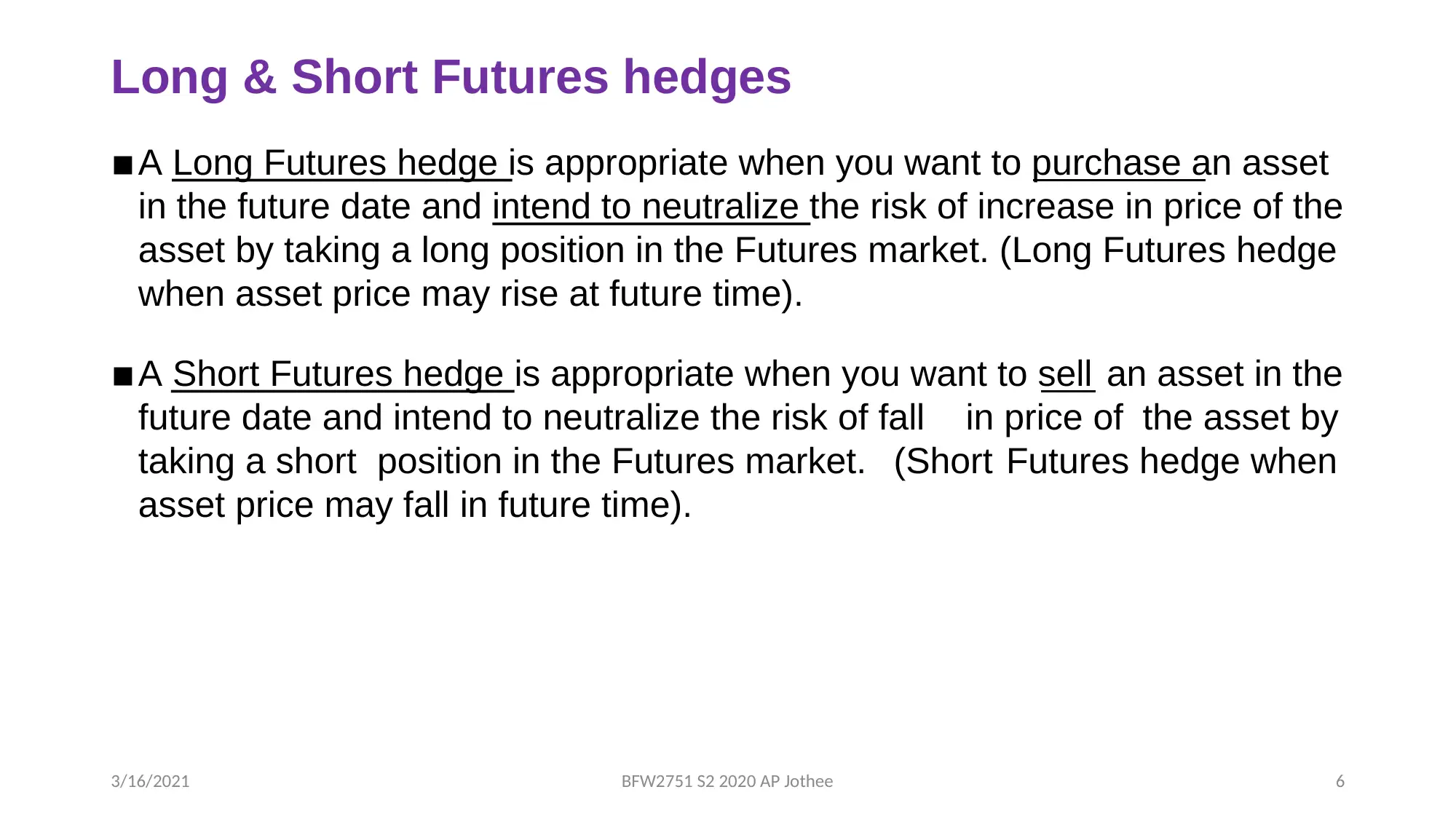

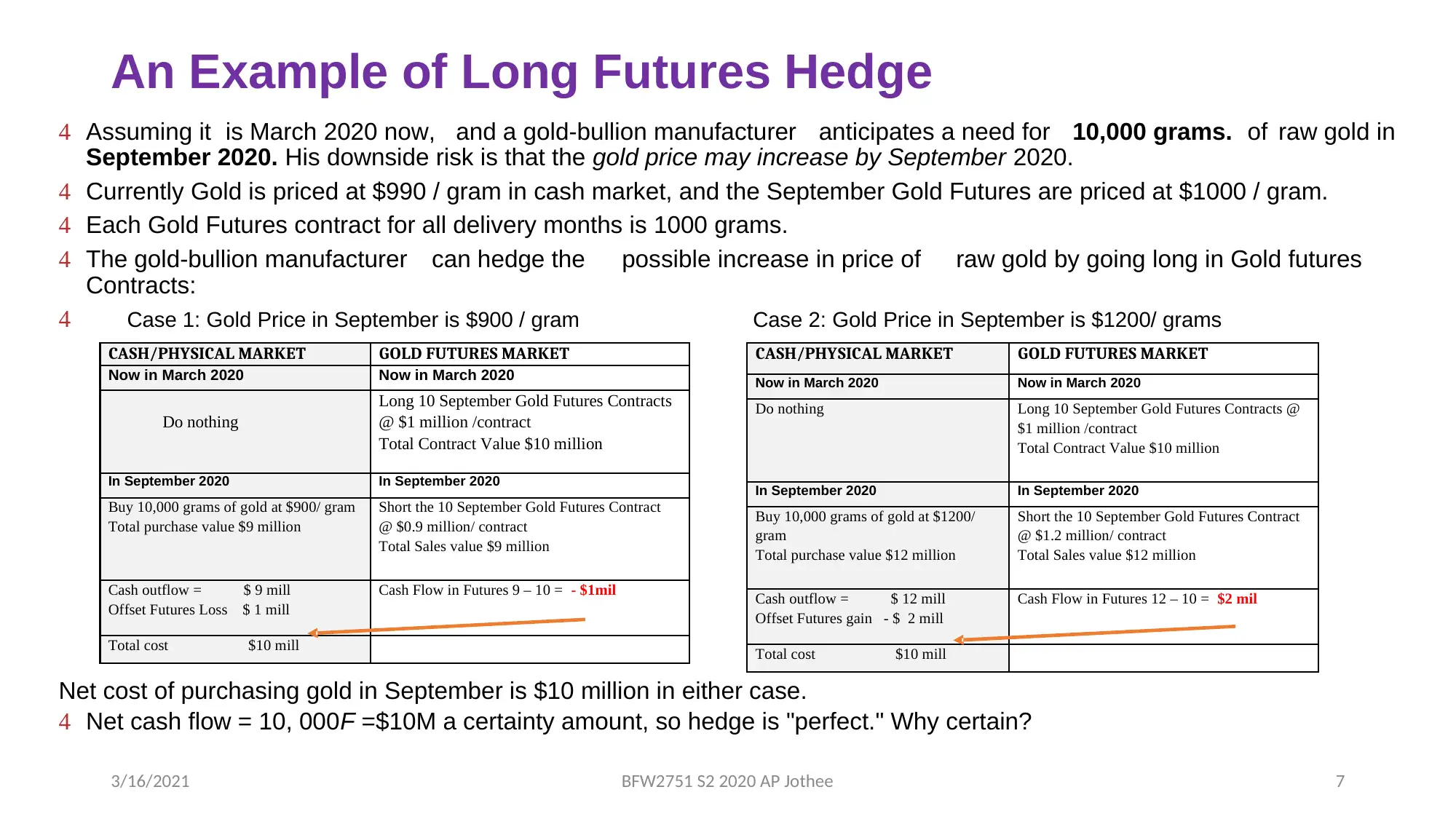

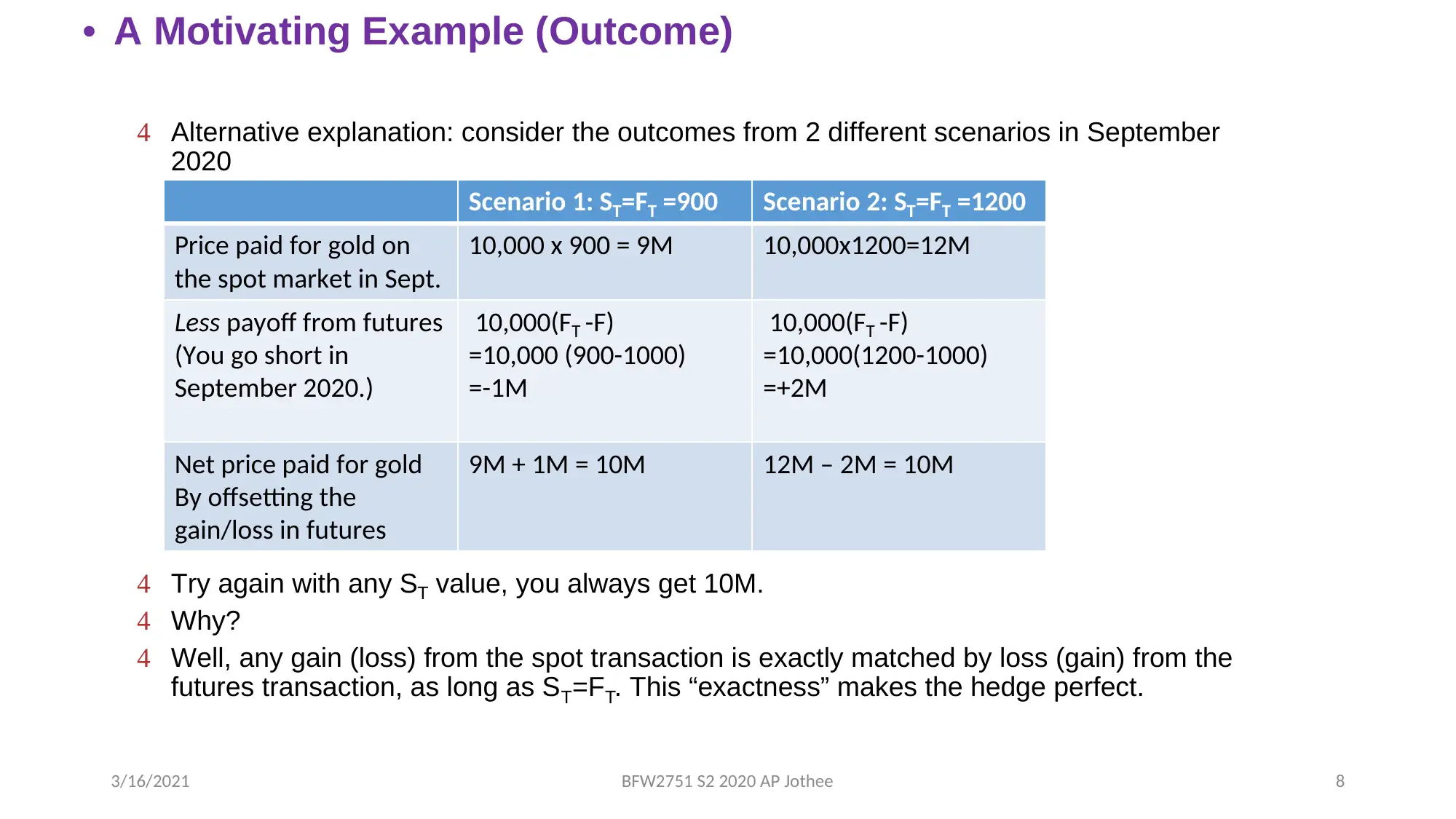

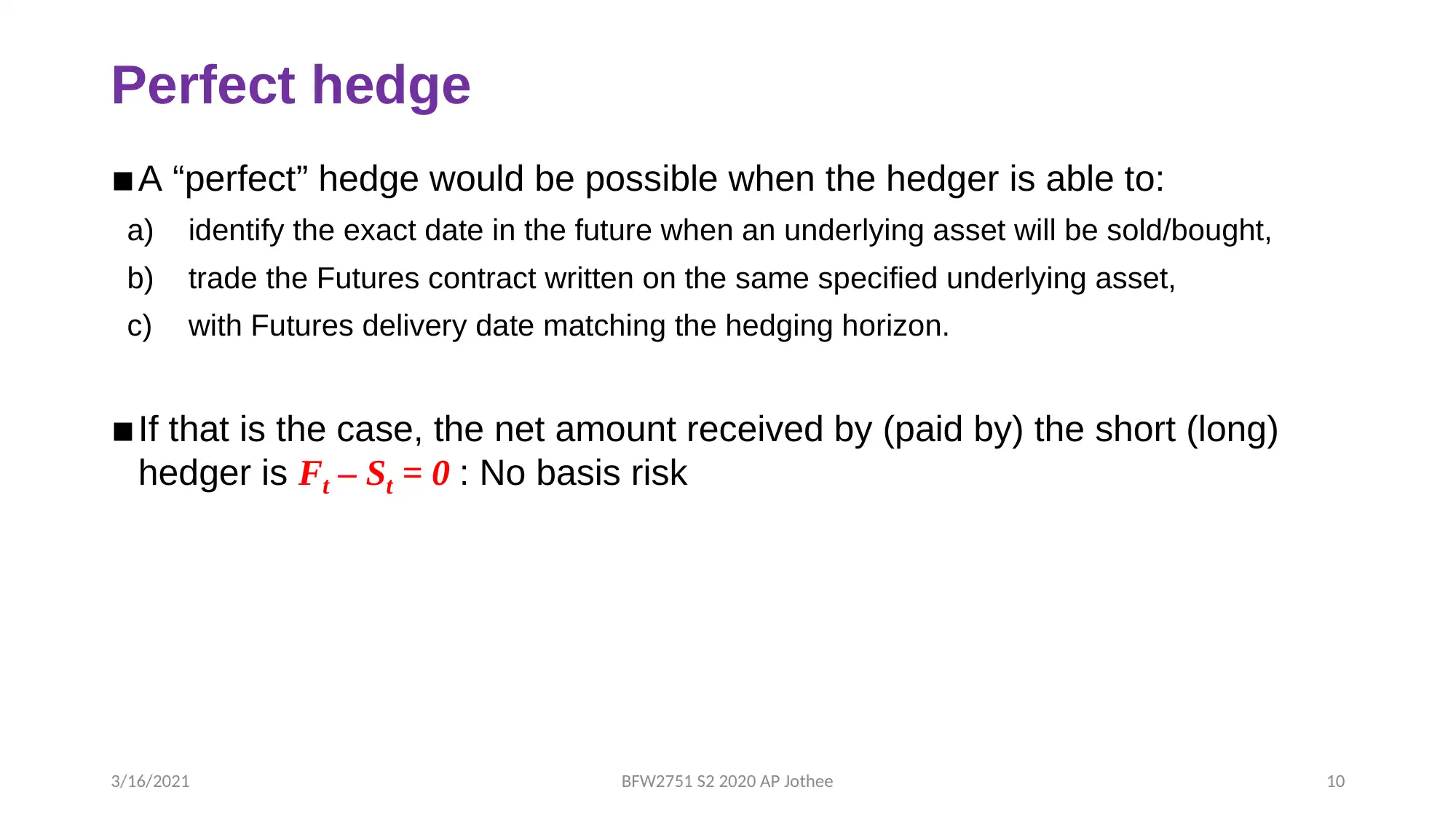

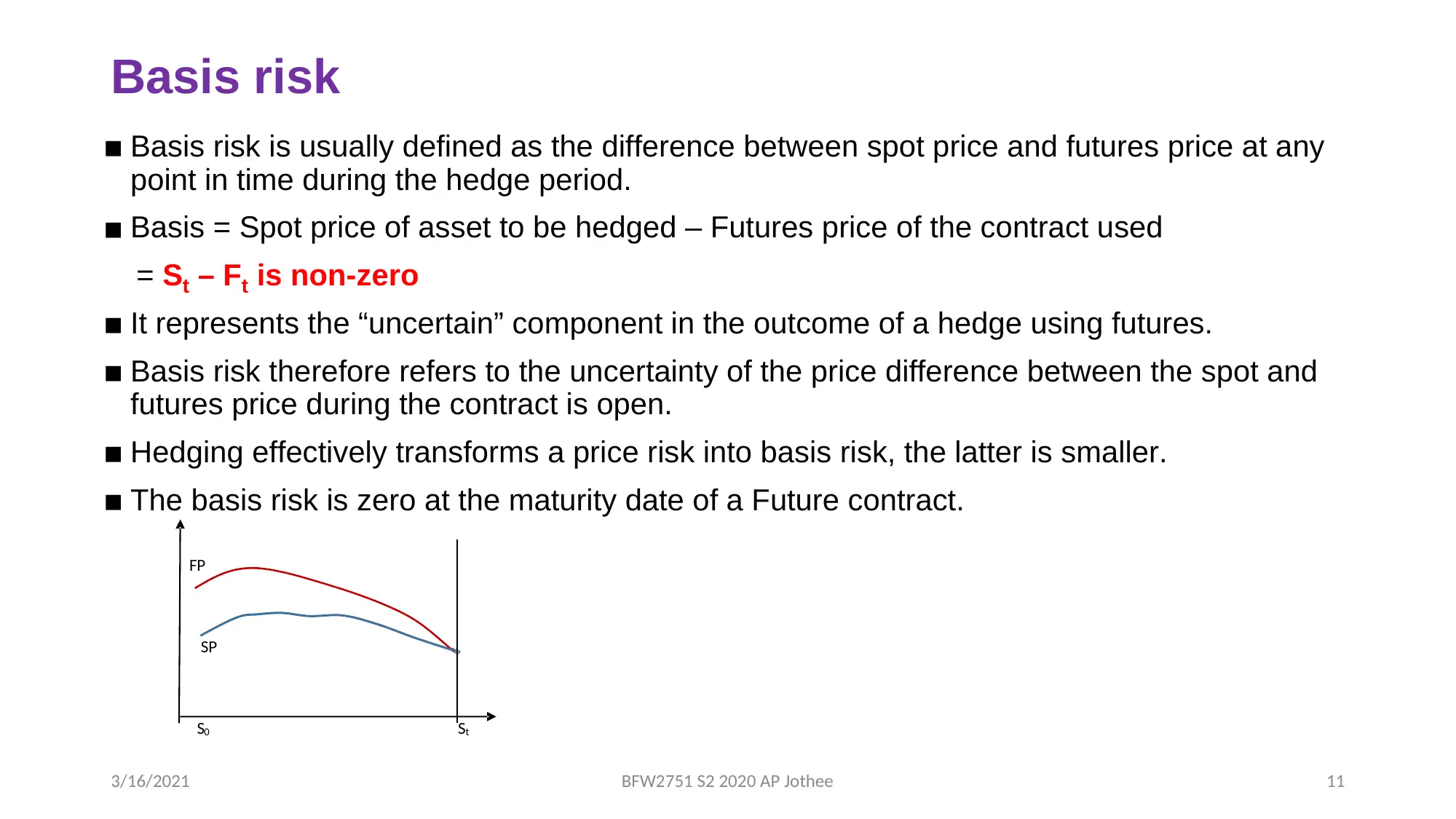

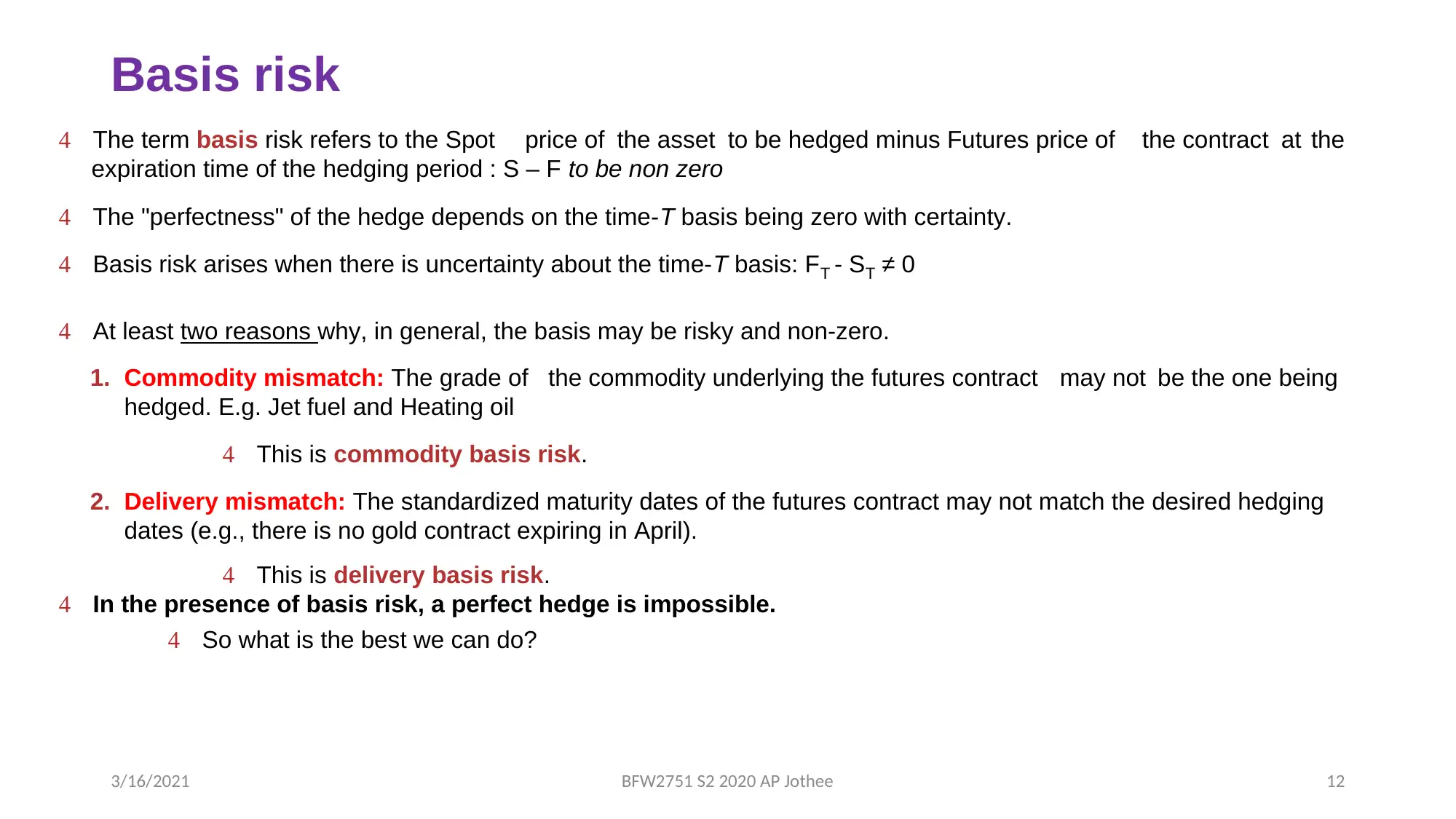

This report delves into the core concepts of hedging strategies using futures contracts, a critical component of risk management in finance. It differentiates between long and short futures hedges, elucidating their applications in mitigating price volatility for assets. The report explains the concept of basis risk, which arises from the difference between spot and futures prices, and discusses how it impacts the effectiveness of hedging. It further explores the optimal hedge ratio (OHR), a key metric for determining the ideal proportion of exposure to hedge, and the importance of cross-hedging when a direct futures contract is unavailable. Through practical examples, the report illustrates how companies can use futures contracts to lock in prices and reduce financial risk. The report also addresses the arguments for and against hedging, offering a balanced perspective on the benefits and drawbacks of these strategies. In addition, the report covers the choice of hedging contracts, the optimal number of contracts, and the impact of delivery month selection on basis risk. Overall, this report offers a comprehensive understanding of hedging techniques using futures contracts, providing valuable insights for students of finance and professionals in the field. This assignment is available on Desklib, which provides past papers and solved assignments for students.

1 out of 32

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.