Comparative Financial Analysis Report: Heineken and Farsons

VerifiedAdded on 2023/01/18

|36

|7301

|99

Report

AI Summary

This report conducts a comprehensive financial analysis comparing the performance of Heineken and Farsons, two prominent companies in the beverage industry. The analysis encompasses a detailed examination of their financial statements from 2015 to 2018, utilizing vertical, horizontal, and ratio analysis techniques to assess their financial health. The study evaluates key financial aspects such as profitability, liquidity, solvency, and working capital management. Vertical analysis assesses the proportional relationships within financial statements, while horizontal analysis examines trends over time. Ratio analysis provides insights into the companies' efficiency and solvency. The report also includes an evaluation of cash flow and working capital. The objective is to provide a comparative assessment to aid in decision-making regarding potential suppliers for beer manufacturers. The findings provide valuable insights into the financial strengths and weaknesses of both companies, supporting informed business decisions.

Financial Analysis

Management

&

Enterprise

Management

&

Enterprise

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Overview of Companies:........................................................................................................1

EVALUATION OF OVERALL FINANCIAL PERFORMANCE AND FINANCIAL

POSITION OF HEINIKEN AND FARSONS................................................................................2

Vertical analysis of the financial statements:.........................................................................2

Ratio analysis of the financial statements:.............................................................................6

EVALUATION OF THE WORKING CAPITAL .........................................................................8

EVALUATION OF THE CASH FLOW.......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

.......................................................................................................................................................24

INTRODUCTION...........................................................................................................................1

Overview of Companies:........................................................................................................1

EVALUATION OF OVERALL FINANCIAL PERFORMANCE AND FINANCIAL

POSITION OF HEINIKEN AND FARSONS................................................................................2

Vertical analysis of the financial statements:.........................................................................2

Ratio analysis of the financial statements:.............................................................................6

EVALUATION OF THE WORKING CAPITAL .........................................................................8

EVALUATION OF THE CASH FLOW.......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

.......................................................................................................................................................24

INTRODUCTION

Financial Analysis and management relates to procedures contributes in evaluation and

detailed assessment of fiscal and operating performance of a corporation take momentous and

reliable business or financial decisions. This system lets investors and shareholders to make

logical decisions related to investment made in securities and shares of a company. The study's

main goal is to provide an explanation about how financial data can be analysed through various

financial elements of company (Blum and Dacorogna, 2014). In this study, financial

recommendations are provided to beer-manufacturer company related to which corporation

either Farsons or Heineken is better, for supply of their beer and other beverage products. In this

study, a horizontal, vertical and ratio analysis is carried out against both firms. A cash flow

evaluation is also carried out in this study along with working capital to offer valid suggestions

for beer manufacturer.

Overview of Companies:

Simonds Farsons Cisk plc:

It is leading food and beverage corporation which is engaged in operations related to

brewing, producing or manufacturing, selling of beers brands and other beverages and soft-

drinks. Company is public limited corporation and company's securities are listed and trading in

Malta's stock and securities exchange. Corporation was formed in year 1928 and has grown

rapidly since then, due to which company has a trustworthy business image and unique brand

value (About Farsons. 2019).

Heineken

Company is beer manufacturer that operates throughout the globe and engaged in

operations like production, brewing, marketing, distribution and sale of beer and ciders.

Company has huge marketing-channel and network due to company's sales are much greater than

its core competitors. Company also launching innovative drinks and beer flavours time-to-time,

having a wider range of beer brands (About Heiniken. 2019).

1

Financial Analysis and management relates to procedures contributes in evaluation and

detailed assessment of fiscal and operating performance of a corporation take momentous and

reliable business or financial decisions. This system lets investors and shareholders to make

logical decisions related to investment made in securities and shares of a company. The study's

main goal is to provide an explanation about how financial data can be analysed through various

financial elements of company (Blum and Dacorogna, 2014). In this study, financial

recommendations are provided to beer-manufacturer company related to which corporation

either Farsons or Heineken is better, for supply of their beer and other beverage products. In this

study, a horizontal, vertical and ratio analysis is carried out against both firms. A cash flow

evaluation is also carried out in this study along with working capital to offer valid suggestions

for beer manufacturer.

Overview of Companies:

Simonds Farsons Cisk plc:

It is leading food and beverage corporation which is engaged in operations related to

brewing, producing or manufacturing, selling of beers brands and other beverages and soft-

drinks. Company is public limited corporation and company's securities are listed and trading in

Malta's stock and securities exchange. Corporation was formed in year 1928 and has grown

rapidly since then, due to which company has a trustworthy business image and unique brand

value (About Farsons. 2019).

Heineken

Company is beer manufacturer that operates throughout the globe and engaged in

operations like production, brewing, marketing, distribution and sale of beer and ciders.

Company has huge marketing-channel and network due to company's sales are much greater than

its core competitors. Company also launching innovative drinks and beer flavours time-to-time,

having a wider range of beer brands (About Heiniken. 2019).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EVALUATION OF OVERALL FINANCIAL PERFORMANCE AND

FINANCIAL POSITION OF HEINIKEN AND FARSONS

Vertical analysis of the financial statements:

Vertical analysis is a method of evaluating the financial reports by taking one component

of financial statement as a basic factor (generally total revenue) and then contrasting other

factors with this in order to determine how other factors influence an organization's revenues (El

Kasmioui and Ceulemans, 2012). In given case, vertical analysis has been done with respect to

both corporation's annual financial statements of 4years form year 2015 to year 2018 which are

attached in appendices, based on this data following is analysis of vertical FS of companies, as

follows:

Vertical analysis of Income Statement:

Simonds Farsons Cisk plc:

Sales figures are taken as base for whole analysis. It has been analysed from vertical P&L

of company that while sales of company Farsons is 100 percent then cost of sales are 63.29

percent in year2015, 61.18percent in year 2016, 61.36percent in year-2017 and 61.05percent in

year-2018. The purpose of such a vertical review is to decide whether Farsons Plc is able to pay-

off their distributors promptly to recommend the beer-manufacturer. Above decline in cost of

revenue percent indicates that company's operating effectiveness has been increased over this

period. Company's gross-margin percentages was 38.95 percent in 2018 which was 38.64percent,

38.82percent and 37.97percent respectively in year-2017, 2016 and 2015. While net-profit

margins were 10.13percent, 12.94percent, 13.64percent and 14.74percent continuously in year-

2015, 2016, 2017 and 2018 (Annual Report of Farsons. 2019). Overall trends shows that

company's gross-margin and net-profit margins have been increased over the period 2015 to

2018.

Company Heineken:

Vertical P&L of company Heineken exhibits that cost of sales of company are

47.25percent, 46.61percent, 46.23percent and 48.71percent of aggregate sales amount

respectively in year-2015,2016,2017 and 2018. In year 2018, company's cost of revenue has been

improved which indicate that company's operating efficiency has been decreased. Gross profit

percentages are 52.75percent, 53.39percent, 53.77percent and 51.29percent respectively in year-

2015, 2016,2017 and 2018. Trends gross profit percent shows that also in year 2018 company's

2

FINANCIAL POSITION OF HEINIKEN AND FARSONS

Vertical analysis of the financial statements:

Vertical analysis is a method of evaluating the financial reports by taking one component

of financial statement as a basic factor (generally total revenue) and then contrasting other

factors with this in order to determine how other factors influence an organization's revenues (El

Kasmioui and Ceulemans, 2012). In given case, vertical analysis has been done with respect to

both corporation's annual financial statements of 4years form year 2015 to year 2018 which are

attached in appendices, based on this data following is analysis of vertical FS of companies, as

follows:

Vertical analysis of Income Statement:

Simonds Farsons Cisk plc:

Sales figures are taken as base for whole analysis. It has been analysed from vertical P&L

of company that while sales of company Farsons is 100 percent then cost of sales are 63.29

percent in year2015, 61.18percent in year 2016, 61.36percent in year-2017 and 61.05percent in

year-2018. The purpose of such a vertical review is to decide whether Farsons Plc is able to pay-

off their distributors promptly to recommend the beer-manufacturer. Above decline in cost of

revenue percent indicates that company's operating effectiveness has been increased over this

period. Company's gross-margin percentages was 38.95 percent in 2018 which was 38.64percent,

38.82percent and 37.97percent respectively in year-2017, 2016 and 2015. While net-profit

margins were 10.13percent, 12.94percent, 13.64percent and 14.74percent continuously in year-

2015, 2016, 2017 and 2018 (Annual Report of Farsons. 2019). Overall trends shows that

company's gross-margin and net-profit margins have been increased over the period 2015 to

2018.

Company Heineken:

Vertical P&L of company Heineken exhibits that cost of sales of company are

47.25percent, 46.61percent, 46.23percent and 48.71percent of aggregate sales amount

respectively in year-2015,2016,2017 and 2018. In year 2018, company's cost of revenue has been

improved which indicate that company's operating efficiency has been decreased. Gross profit

percentages are 52.75percent, 53.39percent, 53.77percent and 51.29percent respectively in year-

2015, 2016,2017 and 2018. Trends gross profit percent shows that also in year 2018 company's

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

gross-margin has been dropped due to increased cost of sales. While Net profit proportion

company was 4.67percent in year 2015 which was dropped to 4.28% with ups and down. In 2016

net-profit was 3.75% while in year 2017 it was reached to 4.46percent. Aggregate changes in NP

percentage shows that company after 2017, corporation's net-profit generation capacity has been

declined (Annual Report of Heiniken. 2019).

Vertical analysis of Balance Sheet:

Simonds Farsons-Cisk plc:

Simonds vertical BS's analysis reflects that company's overall long -term debts and

liabilities level in total assets terms has been reached to 77.16% in year-2018 with a decrease

from 81.42percent in year-2017. On other-side current-assets balances shown increase from

18.58percent in year-2017 to 22.22percent in year-2018 while in 2015-2016 it was 21.48percent

& 20.25percent.

Level of SH's equity funds was around 67.11-percent of assets in year-2015 that was

shifted to 66.87-percent, 67.21-percent and 59.88-percent correspondingly in year-2016,2017

and 2018. Whereas sum of all liabilities was just 20.37-percent in year-2018 that were 32.79-

percent, 32.52-percent and 32.89-percent respectively in year-2015,2016 and 2017 (Annual

Report of Farsons. 2019).

Company Heineken:

Taking total assets amount as baseline, vertical analysis of company's balance sheet

exhibits that aggregate non-current assets including tangible and intangible assets are 84.32

percent, 79.31 percent, 79.90 percent and 78.38 percent during period of year-2015 to year-2018

respectively reflecting a declining trend in figures. Cash and liquid funds of company are 6.92

percent of entire assets in year-2018 which was 5.95 percent, 7.72 percent and 2.23 percent in

year-2017, 2016 and 2015 correspondingly which points out that company's cash funds are

decreased after 2016. On other-hand current assets of corporation are 21.62 percent in year 2018,

20.10percent in year-2017, 20.69percent in year-2016 and 15.68percent in year-2015 indicating

overall improvement in current asset level in company.

Shareholder's equity funds has covered 17.06percent part in company's entire assets in

year-2018v while in year-2017, 2016 and 2015 it was 16.16 percent, 16.78 percent and 17.90

percent respectively. Enterprise's current liabilities level was drooped from 26.44-percent to

3

company was 4.67percent in year 2015 which was dropped to 4.28% with ups and down. In 2016

net-profit was 3.75% while in year 2017 it was reached to 4.46percent. Aggregate changes in NP

percentage shows that company after 2017, corporation's net-profit generation capacity has been

declined (Annual Report of Heiniken. 2019).

Vertical analysis of Balance Sheet:

Simonds Farsons-Cisk plc:

Simonds vertical BS's analysis reflects that company's overall long -term debts and

liabilities level in total assets terms has been reached to 77.16% in year-2018 with a decrease

from 81.42percent in year-2017. On other-side current-assets balances shown increase from

18.58percent in year-2017 to 22.22percent in year-2018 while in 2015-2016 it was 21.48percent

& 20.25percent.

Level of SH's equity funds was around 67.11-percent of assets in year-2015 that was

shifted to 66.87-percent, 67.21-percent and 59.88-percent correspondingly in year-2016,2017

and 2018. Whereas sum of all liabilities was just 20.37-percent in year-2018 that were 32.79-

percent, 32.52-percent and 32.89-percent respectively in year-2015,2016 and 2017 (Annual

Report of Farsons. 2019).

Company Heineken:

Taking total assets amount as baseline, vertical analysis of company's balance sheet

exhibits that aggregate non-current assets including tangible and intangible assets are 84.32

percent, 79.31 percent, 79.90 percent and 78.38 percent during period of year-2015 to year-2018

respectively reflecting a declining trend in figures. Cash and liquid funds of company are 6.92

percent of entire assets in year-2018 which was 5.95 percent, 7.72 percent and 2.23 percent in

year-2017, 2016 and 2015 correspondingly which points out that company's cash funds are

decreased after 2016. On other-hand current assets of corporation are 21.62 percent in year 2018,

20.10percent in year-2017, 20.69percent in year-2016 and 15.68percent in year-2015 indicating

overall improvement in current asset level in company.

Shareholder's equity funds has covered 17.06percent part in company's entire assets in

year-2018v while in year-2017, 2016 and 2015 it was 16.16 percent, 16.78 percent and 17.90

percent respectively. Enterprise's current liabilities level was drooped from 26.44-percent to

3

24.91-percent in period 2016-2018. Further non-current liabilities level has been declined to

58.03% in year-2018 form 59.52percent in year-2015.

Horizontal Analysis of Financial Statements:

Horizontal analysis implies to systematic technique utilized for effective evaluation of

financial information where previous or just recent period is considered as base-line and

thereafter each element and item reported in financial-statements are compared with figures

stated in baseline period (Eng, Lea, and Cai, 2014). Core objective of a horizontal analysis is

assessment of true growth either negative or positive and variance in performance of corporation

based on each item's variance.

Horizontal analysis of Income-statements:

Simonds Farsons Cisk plc:

Company's horizontal income-statement shows that in 2018 increment in revenue was

7.95 percent while this increase in 2017 and 2016 was just 3.53% and 7.59% respectively. It

shows that company's sales generating efficiencies has been grown. Along with increase

company's cost of sales has been increase by almost same percentage of 7.41% in year 2018.

While company's gross-profits are reported an increment of 8.82% in year-2018 which was 10-

percent and 3.03-percent in year-2016 and 2017. Increment in Net-profits was 16.67% in year-

2018 which was 37.50-percent in year-2016 while in year-2017 it was only increased by 9.09-

percent which reflects that net-profitability position of corporation has been enhanced after year-

2017. Entire analysis represents that company's profitability position has been increased.

Company Heineken:

Horizontal analysis of Heinkeken shows that company's turnover has been grown by

2.66% in year 2018 while in year-2016 and 2017 such growth was around 1.37percent and

around 5.27-percent. Company's cost of sales has reported a growth of 0.01percent, 4.40-percent

and 8.18-percent during year-2016, 2017 and 2018. Growth in gross profits has been reached to

negative 2.08 percent in year-2018 while in 2016 and 2017 there was increase of 2.59-percent

and 6.04-percent. Company's net-income figures has shown a negative growth of 1.64 percent

and 18.60-percent in year-2018 and 2016 only a positive growth of 25.42-percent in year-2018.

Overall performance growth in term of profitability of company is not so much good as there are

negative growth in gross as well as net profits' figures.

Horizontal analysis of Balance Sheet:

4

58.03% in year-2018 form 59.52percent in year-2015.

Horizontal Analysis of Financial Statements:

Horizontal analysis implies to systematic technique utilized for effective evaluation of

financial information where previous or just recent period is considered as base-line and

thereafter each element and item reported in financial-statements are compared with figures

stated in baseline period (Eng, Lea, and Cai, 2014). Core objective of a horizontal analysis is

assessment of true growth either negative or positive and variance in performance of corporation

based on each item's variance.

Horizontal analysis of Income-statements:

Simonds Farsons Cisk plc:

Company's horizontal income-statement shows that in 2018 increment in revenue was

7.95 percent while this increase in 2017 and 2016 was just 3.53% and 7.59% respectively. It

shows that company's sales generating efficiencies has been grown. Along with increase

company's cost of sales has been increase by almost same percentage of 7.41% in year 2018.

While company's gross-profits are reported an increment of 8.82% in year-2018 which was 10-

percent and 3.03-percent in year-2016 and 2017. Increment in Net-profits was 16.67% in year-

2018 which was 37.50-percent in year-2016 while in year-2017 it was only increased by 9.09-

percent which reflects that net-profitability position of corporation has been enhanced after year-

2017. Entire analysis represents that company's profitability position has been increased.

Company Heineken:

Horizontal analysis of Heinkeken shows that company's turnover has been grown by

2.66% in year 2018 while in year-2016 and 2017 such growth was around 1.37percent and

around 5.27-percent. Company's cost of sales has reported a growth of 0.01percent, 4.40-percent

and 8.18-percent during year-2016, 2017 and 2018. Growth in gross profits has been reached to

negative 2.08 percent in year-2018 while in 2016 and 2017 there was increase of 2.59-percent

and 6.04-percent. Company's net-income figures has shown a negative growth of 1.64 percent

and 18.60-percent in year-2018 and 2016 only a positive growth of 25.42-percent in year-2018.

Overall performance growth in term of profitability of company is not so much good as there are

negative growth in gross as well as net profits' figures.

Horizontal analysis of Balance Sheet:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Simonds Farsons Cisk plc:

Horizontal BS of Simonds shows that shareholder's equity-funds balance has been

achieved a negative growth of 21.14% in year-2018 while increment in year-2017 and 2016 was

12.84-percent and 9-percent respectively reflecting a overall declining trend. While long-term

debts funds also declined by around 2.86-percent in year-2018 that was increased by 20.69-

percent in year-2017 and declined by 3.33% in year-2016. Current or short-run liabilities of

company has been grown by 33.33-percent in year-2018 and 2016 but in 2017 there was no

fluctuation.

Level of current assets has been achieved a 5.88-percent in year-2018, that growth in

2017 and 2016 was 3.03-percent and 3.13-percent, indicating a upward trend in current-assets'

level. Non-current assets reported negative growth of 77.16-percent in year-2018 while

increment in non-current assets in year-2016 and 2017 was 10.26-percent and 15.50-percent.

Cash balance of company has been attained 300% growth in year-2018 while there as negative

growth in cash-funds of 60 and 50 percent in year-2016 and 2017. Overall assets of Simonds

declined by around 11.48-percent in year-2018 while there was increase of 12.27-percent and

9.4percent in year-2016 and 2017.

Company Heineken:

Analyzing Horizontal BS of Heiniken provides that company's equity funds raised by

7.91-percent in year 2018 while changes in equity funds were -2.25 % and 0.53 % respectively in

year-2016 and 2017. Long-term debt funds just grown by around 1.69-percent during year-2018

that was reported increments of -0.54 percent and 7.24percent in year-2016 and 2017. Current

liabilities level in company has reported minor negative growth of 0.08-percent that was

enhanced by around 0.59-percent and 22.09-percent in year-2017 and 2016.

Cumulative cash and equivalent figures has been grown by around 268.33-percent in

year-2016 that was declined in year-2017 by 19.54-percent and ultimately increased by 18.88-

percent in year-2017. Current assets in company achieved a growth of 37.59-percent, 1.36-

percent and 9.97-percent correspondingly in year-2016, 2017 and 2018. On other-side non-

current ( both tangible and tangle) assets are shown a minor growth of around 0.31-percent in

year-2018, this growth rate in year-2017 was 5.14% and 1.94% in year-2016.

5

Horizontal BS of Simonds shows that shareholder's equity-funds balance has been

achieved a negative growth of 21.14% in year-2018 while increment in year-2017 and 2016 was

12.84-percent and 9-percent respectively reflecting a overall declining trend. While long-term

debts funds also declined by around 2.86-percent in year-2018 that was increased by 20.69-

percent in year-2017 and declined by 3.33% in year-2016. Current or short-run liabilities of

company has been grown by 33.33-percent in year-2018 and 2016 but in 2017 there was no

fluctuation.

Level of current assets has been achieved a 5.88-percent in year-2018, that growth in

2017 and 2016 was 3.03-percent and 3.13-percent, indicating a upward trend in current-assets'

level. Non-current assets reported negative growth of 77.16-percent in year-2018 while

increment in non-current assets in year-2016 and 2017 was 10.26-percent and 15.50-percent.

Cash balance of company has been attained 300% growth in year-2018 while there as negative

growth in cash-funds of 60 and 50 percent in year-2016 and 2017. Overall assets of Simonds

declined by around 11.48-percent in year-2018 while there was increase of 12.27-percent and

9.4percent in year-2016 and 2017.

Company Heineken:

Analyzing Horizontal BS of Heiniken provides that company's equity funds raised by

7.91-percent in year 2018 while changes in equity funds were -2.25 % and 0.53 % respectively in

year-2016 and 2017. Long-term debt funds just grown by around 1.69-percent during year-2018

that was reported increments of -0.54 percent and 7.24percent in year-2016 and 2017. Current

liabilities level in company has reported minor negative growth of 0.08-percent that was

enhanced by around 0.59-percent and 22.09-percent in year-2017 and 2016.

Cumulative cash and equivalent figures has been grown by around 268.33-percent in

year-2016 that was declined in year-2017 by 19.54-percent and ultimately increased by 18.88-

percent in year-2017. Current assets in company achieved a growth of 37.59-percent, 1.36-

percent and 9.97-percent correspondingly in year-2016, 2017 and 2018. On other-side non-

current ( both tangible and tangle) assets are shown a minor growth of around 0.31-percent in

year-2018, this growth rate in year-2017 was 5.14% and 1.94% in year-2016.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio analysis of the financial statements:

Ratio analysis is way to gain insight into the corporation's operating efficiency and

solvency. This helps in decision-making process so that the interested parties and prospective

customers can make a quantified financial decision. Even in this case, ratio analysis technique is

important as vertical analysis performed above represents company's efficiency outputs and

horizontal analysis suggests the performance effectiveness factors of both selected corporation

(Isberg and Pitta, 2013). In this situation, ratio analysis is conducted to examine both firms'

liquidity, profit making efficiency and solvency, so that a systematic decision can be made that

could support the beer's future potential suppliers.

Profitability Analysis: It simply reflects corporation's profitability making capacities. Through

gross-margin ratio and net-profit ratio of companies their profitability position can be easily

determined (Palepu and Healy, 2013). Following are the ratios of both respective corporation in

this context, as follows:

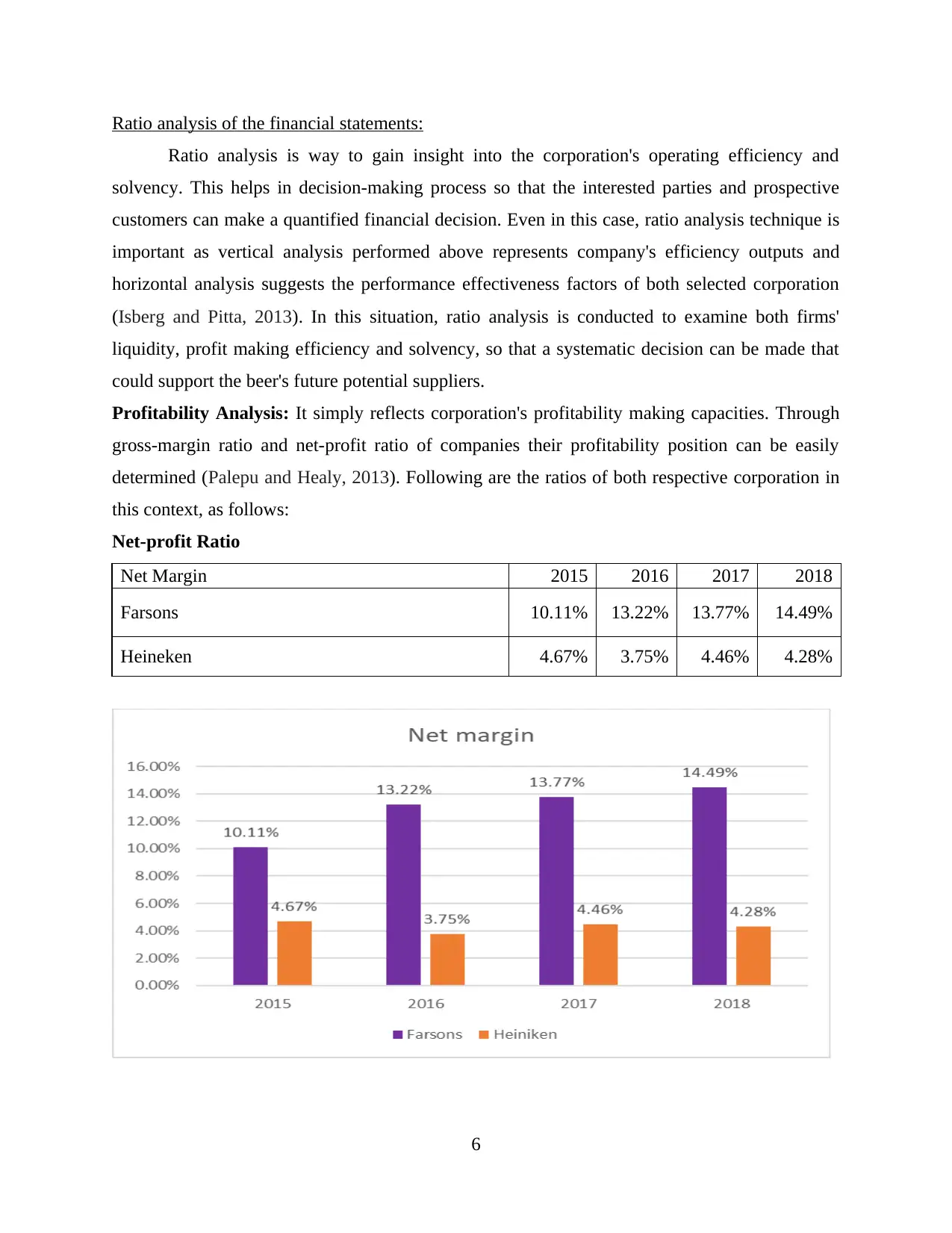

Net-profit Ratio

Net Margin 2015 2016 2017 2018

Farsons 10.11% 13.22% 13.77% 14.49%

Heineken 4.67% 3.75% 4.46% 4.28%

6

Ratio analysis is way to gain insight into the corporation's operating efficiency and

solvency. This helps in decision-making process so that the interested parties and prospective

customers can make a quantified financial decision. Even in this case, ratio analysis technique is

important as vertical analysis performed above represents company's efficiency outputs and

horizontal analysis suggests the performance effectiveness factors of both selected corporation

(Isberg and Pitta, 2013). In this situation, ratio analysis is conducted to examine both firms'

liquidity, profit making efficiency and solvency, so that a systematic decision can be made that

could support the beer's future potential suppliers.

Profitability Analysis: It simply reflects corporation's profitability making capacities. Through

gross-margin ratio and net-profit ratio of companies their profitability position can be easily

determined (Palepu and Healy, 2013). Following are the ratios of both respective corporation in

this context, as follows:

Net-profit Ratio

Net Margin 2015 2016 2017 2018

Farsons 10.11% 13.22% 13.77% 14.49%

Heineken 4.67% 3.75% 4.46% 4.28%

6

Net profit ratio is crucial profitability measure that represents enterprise's profit earning

capacity after providing overall expenses. Company Farsons reported net-profit ratio in percent

are 14.49, 13.77, 13.22 and 10.11 in year-2018,2017,2016 and 2015 reflecting a upward trend.

While Heiniken's net-profit ratio percent during the same years are 4.28, 4.46, 3.75 and 4.67

respectively which shows that in 2016 and 2018 net-profit rate has been dropped. It means that

company's net profitability level has been decreased. Farsons's profitability level and growth is

higher than Heineken.

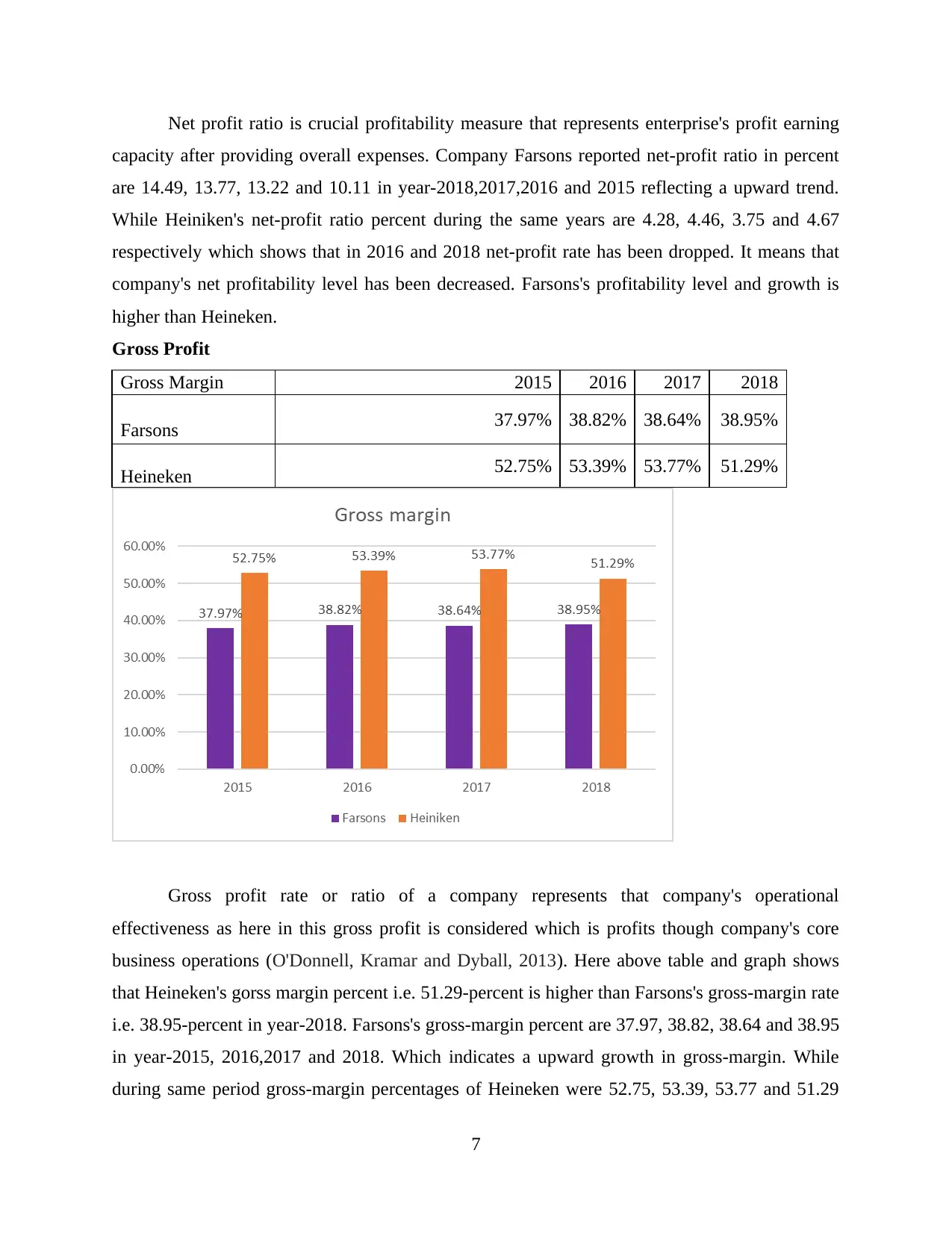

Gross Profit

Gross Margin 2015 2016 2017 2018

Farsons 37.97% 38.82% 38.64% 38.95%

Heineken 52.75% 53.39% 53.77% 51.29%

Gross profit rate or ratio of a company represents that company's operational

effectiveness as here in this gross profit is considered which is profits though company's core

business operations (O'Donnell, Kramar and Dyball, 2013). Here above table and graph shows

that Heineken's gorss margin percent i.e. 51.29-percent is higher than Farsons's gross-margin rate

i.e. 38.95-percent in year-2018. Farsons's gross-margin percent are 37.97, 38.82, 38.64 and 38.95

in year-2015, 2016,2017 and 2018. Which indicates a upward growth in gross-margin. While

during same period gross-margin percentages of Heineken were 52.75, 53.39, 53.77 and 51.29

7

capacity after providing overall expenses. Company Farsons reported net-profit ratio in percent

are 14.49, 13.77, 13.22 and 10.11 in year-2018,2017,2016 and 2015 reflecting a upward trend.

While Heiniken's net-profit ratio percent during the same years are 4.28, 4.46, 3.75 and 4.67

respectively which shows that in 2016 and 2018 net-profit rate has been dropped. It means that

company's net profitability level has been decreased. Farsons's profitability level and growth is

higher than Heineken.

Gross Profit

Gross Margin 2015 2016 2017 2018

Farsons 37.97% 38.82% 38.64% 38.95%

Heineken 52.75% 53.39% 53.77% 51.29%

Gross profit rate or ratio of a company represents that company's operational

effectiveness as here in this gross profit is considered which is profits though company's core

business operations (O'Donnell, Kramar and Dyball, 2013). Here above table and graph shows

that Heineken's gorss margin percent i.e. 51.29-percent is higher than Farsons's gross-margin rate

i.e. 38.95-percent in year-2018. Farsons's gross-margin percent are 37.97, 38.82, 38.64 and 38.95

in year-2015, 2016,2017 and 2018. Which indicates a upward growth in gross-margin. While

during same period gross-margin percentages of Heineken were 52.75, 53.39, 53.77 and 51.29

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that shows decrement in gross-margin rate in year 2018. It implies that company's efficiencies to

generate profits form core operations has been declined.

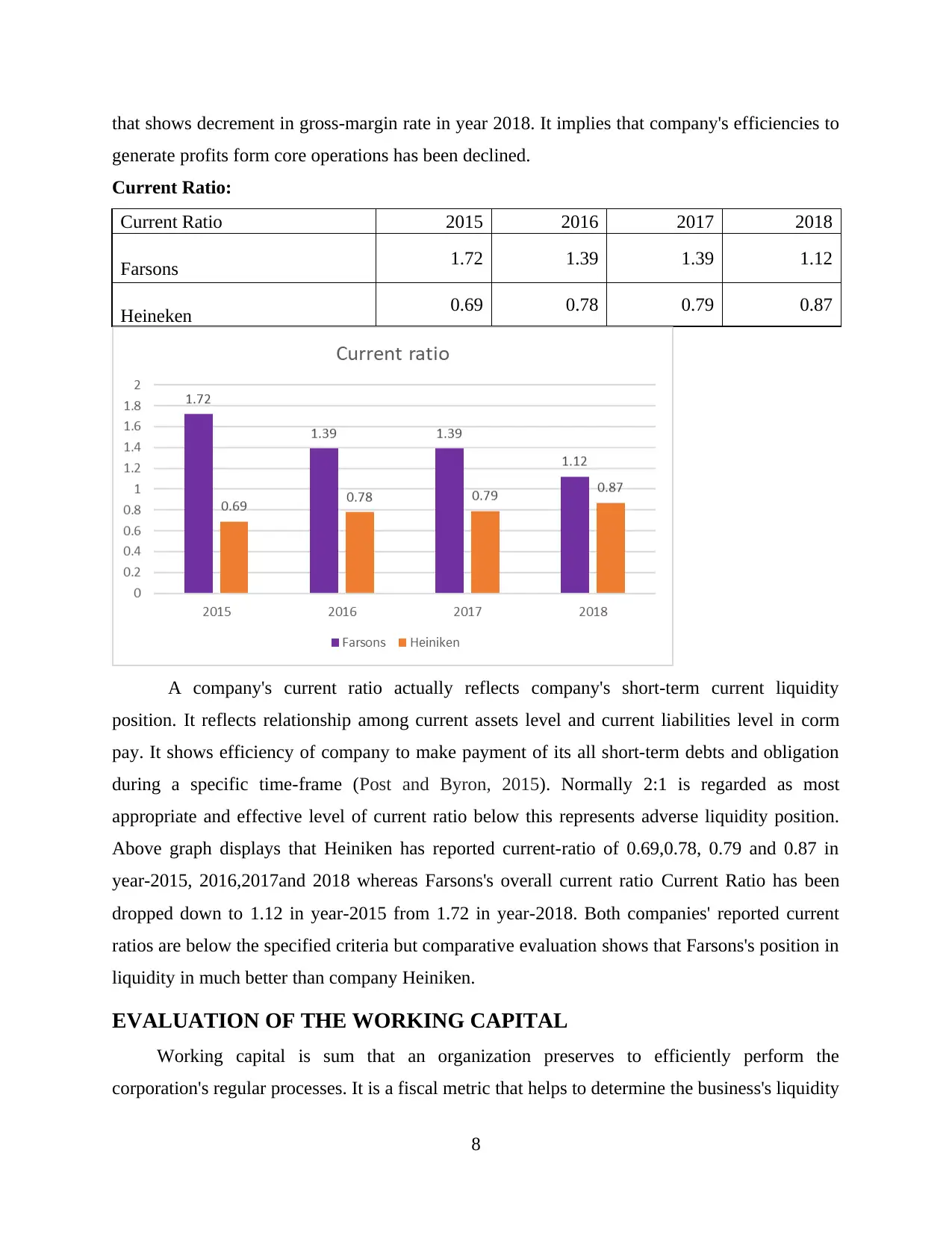

Current Ratio:

Current Ratio 2015 2016 2017 2018

Farsons 1.72 1.39 1.39 1.12

Heineken 0.69 0.78 0.79 0.87

A company's current ratio actually reflects company's short-term current liquidity

position. It reflects relationship among current assets level and current liabilities level in corm

pay. It shows efficiency of company to make payment of its all short-term debts and obligation

during a specific time-frame (Post and Byron, 2015). Normally 2:1 is regarded as most

appropriate and effective level of current ratio below this represents adverse liquidity position.

Above graph displays that Heiniken has reported current-ratio of 0.69,0.78, 0.79 and 0.87 in

year-2015, 2016,2017and 2018 whereas Farsons's overall current ratio Current Ratio has been

dropped down to 1.12 in year-2015 from 1.72 in year-2018. Both companies' reported current

ratios are below the specified criteria but comparative evaluation shows that Farsons's position in

liquidity in much better than company Heiniken.

EVALUATION OF THE WORKING CAPITAL

Working capital is sum that an organization preserves to efficiently perform the

corporation's regular processes. It is a fiscal metric that helps to determine the business's liquidity

8

generate profits form core operations has been declined.

Current Ratio:

Current Ratio 2015 2016 2017 2018

Farsons 1.72 1.39 1.39 1.12

Heineken 0.69 0.78 0.79 0.87

A company's current ratio actually reflects company's short-term current liquidity

position. It reflects relationship among current assets level and current liabilities level in corm

pay. It shows efficiency of company to make payment of its all short-term debts and obligation

during a specific time-frame (Post and Byron, 2015). Normally 2:1 is regarded as most

appropriate and effective level of current ratio below this represents adverse liquidity position.

Above graph displays that Heiniken has reported current-ratio of 0.69,0.78, 0.79 and 0.87 in

year-2015, 2016,2017and 2018 whereas Farsons's overall current ratio Current Ratio has been

dropped down to 1.12 in year-2015 from 1.72 in year-2018. Both companies' reported current

ratios are below the specified criteria but comparative evaluation shows that Farsons's position in

liquidity in much better than company Heiniken.

EVALUATION OF THE WORKING CAPITAL

Working capital is sum that an organization preserves to efficiently perform the

corporation's regular processes. It is a fiscal metric that helps to determine the business's liquidity

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stance. It is necessary to assess and evaluate both firms ' working capital because it can help the

beer producer recognize which corporation is more stable and able of sufficiently paying off the

provider's or supplies dues (Sheikhi, Ranjbar and Oraee, 2012). In this scenario, two beer

manufacturing firms, Heineken and Farsons Plc, are listed and their net-working capital figures

are carried out below:

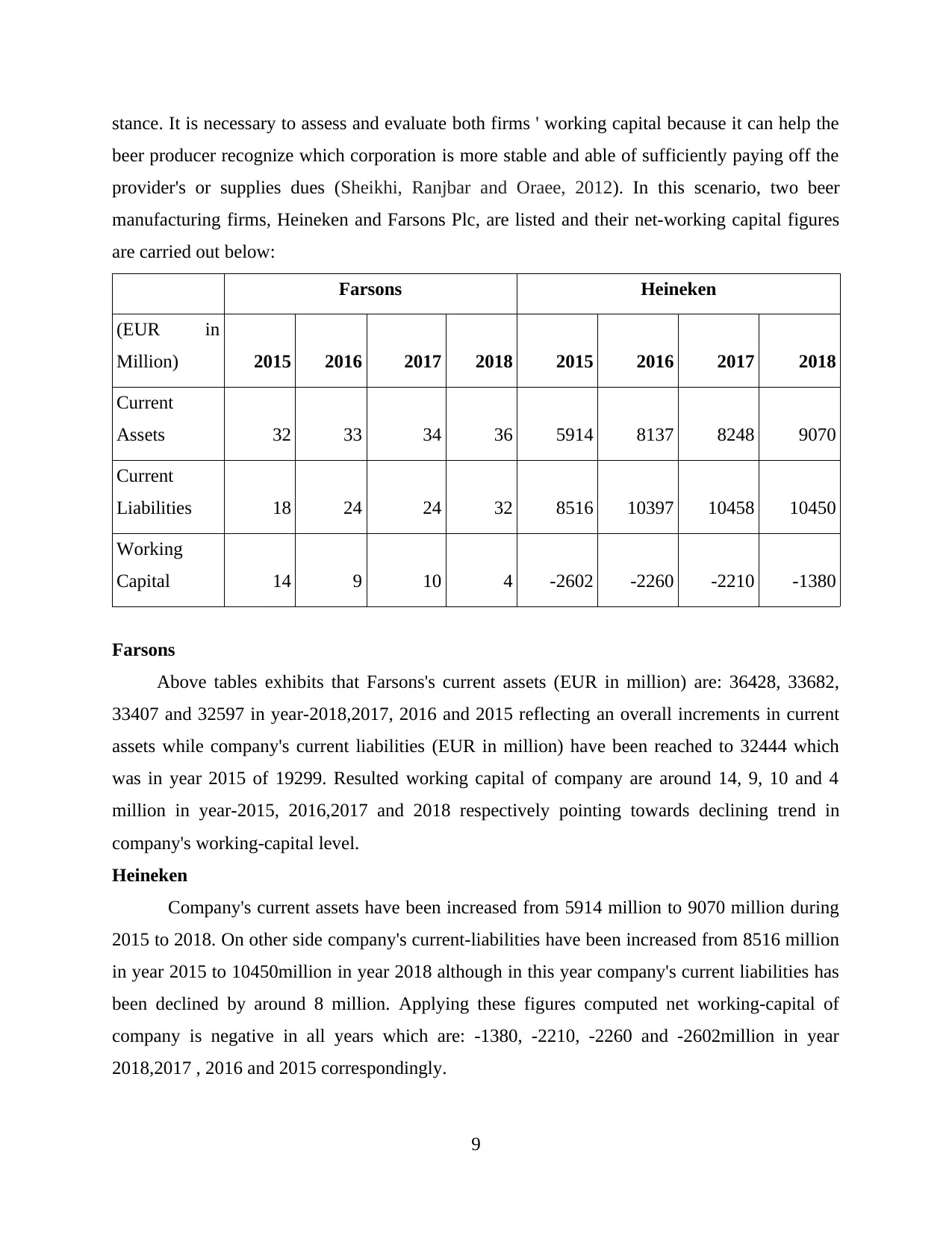

Farsons Heineken

(EUR in

Million) 2015 2016 2017 2018 2015 2016 2017 2018

Current

Assets 32 33 34 36 5914 8137 8248 9070

Current

Liabilities 18 24 24 32 8516 10397 10458 10450

Working

Capital 14 9 10 4 -2602 -2260 -2210 -1380

Farsons

Above tables exhibits that Farsons's current assets (EUR in million) are: 36428, 33682,

33407 and 32597 in year-2018,2017, 2016 and 2015 reflecting an overall increments in current

assets while company's current liabilities (EUR in million) have been reached to 32444 which

was in year 2015 of 19299. Resulted working capital of company are around 14, 9, 10 and 4

million in year-2015, 2016,2017 and 2018 respectively pointing towards declining trend in

company's working-capital level.

Heineken

Company's current assets have been increased from 5914 million to 9070 million during

2015 to 2018. On other side company's current-liabilities have been increased from 8516 million

in year 2015 to 10450million in year 2018 although in this year company's current liabilities has

been declined by around 8 million. Applying these figures computed net working-capital of

company is negative in all years which are: -1380, -2210, -2260 and -2602million in year

2018,2017 , 2016 and 2015 correspondingly.

9

beer producer recognize which corporation is more stable and able of sufficiently paying off the

provider's or supplies dues (Sheikhi, Ranjbar and Oraee, 2012). In this scenario, two beer

manufacturing firms, Heineken and Farsons Plc, are listed and their net-working capital figures

are carried out below:

Farsons Heineken

(EUR in

Million) 2015 2016 2017 2018 2015 2016 2017 2018

Current

Assets 32 33 34 36 5914 8137 8248 9070

Current

Liabilities 18 24 24 32 8516 10397 10458 10450

Working

Capital 14 9 10 4 -2602 -2260 -2210 -1380

Farsons

Above tables exhibits that Farsons's current assets (EUR in million) are: 36428, 33682,

33407 and 32597 in year-2018,2017, 2016 and 2015 reflecting an overall increments in current

assets while company's current liabilities (EUR in million) have been reached to 32444 which

was in year 2015 of 19299. Resulted working capital of company are around 14, 9, 10 and 4

million in year-2015, 2016,2017 and 2018 respectively pointing towards declining trend in

company's working-capital level.

Heineken

Company's current assets have been increased from 5914 million to 9070 million during

2015 to 2018. On other side company's current-liabilities have been increased from 8516 million

in year 2015 to 10450million in year 2018 although in this year company's current liabilities has

been declined by around 8 million. Applying these figures computed net working-capital of

company is negative in all years which are: -1380, -2210, -2260 and -2602million in year

2018,2017 , 2016 and 2015 correspondingly.

9

Both companies' comparison reflects that Farosns has reported positive and increased

working capital figures while Heineken has reported negative figures of working capital which

indicates that company has shortage of funds to operate routine business processes. Thus Farsons

is more efficient as per evaluation of working-capital position.

EVALUATION OF THE CASH FLOW

A cash flow report or statement is crucial document which provides details about net in

and out flow cash or monies in an enterprise. A cash-flow is prepared by companies by

classifying business tasks into financing, operating and investments (Vogel, 2014). Through

aggregation of these all activities' cash flows company's net free-cash-flows are determined.

Analysis of cash-flows is significant to assess adequacy of liquid cash-funds in company to

operate business activities. It also aid in controlling overall cash spending and receipts within

corporation.

Heiniken: Corporation's cash-flows generated by operational activities are 3489, 3718,

3882 and 4388 in 2015,2016,2017 and 2018 (figure are in million) respectively. While overall

net outflows of corporation by its all investment tasks from 2015 to 2018 are: 2064, 2,007, 2965

and 2355-million respectively. Through financing operations company's cash-flows are

1173million, 672, 966 and 967-million respectively during period 2015-2018. By summarizing

all cash in-out flows from different activities net-free cash-flows are: 1759, 1,852, 2,049and

2,333 million in year-2015,2016, 2017 and 2018 correspondingly and indicating up ward or

increasing trend. Throughout the entire period business has reported positive balance of free-

cash-flow it means company's liquidity situation in sound and efficient to pay all short-term

liabilities.

Farsons: Cash-flows generated by company Farsons are around 16, 16, 13 and 21million

during 2015 to 2018 respectively, reflecting increment in cash generation capacity of company.

Where as though investing task company has made outflows of 7, 18, 20 and 21 million during

2015,2016,2017 and 2018 year respectively. Corporation's financing operation have lead to cash-

flows of -4, -2, 4 and -1 millions through year-2015, 2016,2017 and 2018 respectively. Overall

net cash-flows in business after considering all activities are 9, -1, -6 and 7million during year-

2015,2016, 2017 and2018 respectively. These reported figures shows that during after period of

2016, in business cash-flows goes negative which are further improved in 2018. A negative cash-

10

working capital figures while Heineken has reported negative figures of working capital which

indicates that company has shortage of funds to operate routine business processes. Thus Farsons

is more efficient as per evaluation of working-capital position.

EVALUATION OF THE CASH FLOW

A cash flow report or statement is crucial document which provides details about net in

and out flow cash or monies in an enterprise. A cash-flow is prepared by companies by

classifying business tasks into financing, operating and investments (Vogel, 2014). Through

aggregation of these all activities' cash flows company's net free-cash-flows are determined.

Analysis of cash-flows is significant to assess adequacy of liquid cash-funds in company to

operate business activities. It also aid in controlling overall cash spending and receipts within

corporation.

Heiniken: Corporation's cash-flows generated by operational activities are 3489, 3718,

3882 and 4388 in 2015,2016,2017 and 2018 (figure are in million) respectively. While overall

net outflows of corporation by its all investment tasks from 2015 to 2018 are: 2064, 2,007, 2965

and 2355-million respectively. Through financing operations company's cash-flows are

1173million, 672, 966 and 967-million respectively during period 2015-2018. By summarizing

all cash in-out flows from different activities net-free cash-flows are: 1759, 1,852, 2,049and

2,333 million in year-2015,2016, 2017 and 2018 correspondingly and indicating up ward or

increasing trend. Throughout the entire period business has reported positive balance of free-

cash-flow it means company's liquidity situation in sound and efficient to pay all short-term

liabilities.

Farsons: Cash-flows generated by company Farsons are around 16, 16, 13 and 21million

during 2015 to 2018 respectively, reflecting increment in cash generation capacity of company.

Where as though investing task company has made outflows of 7, 18, 20 and 21 million during

2015,2016,2017 and 2018 year respectively. Corporation's financing operation have lead to cash-

flows of -4, -2, 4 and -1 millions through year-2015, 2016,2017 and 2018 respectively. Overall

net cash-flows in business after considering all activities are 9, -1, -6 and 7million during year-

2015,2016, 2017 and2018 respectively. These reported figures shows that during after period of

2016, in business cash-flows goes negative which are further improved in 2018. A negative cash-

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.