Hewlett-Packard - Business Activity and Instalment Statement Tasks

VerifiedAdded on 2020/04/21

|27

|4722

|400

Homework Assignment

AI Summary

This assignment solution addresses business activity statement tasks, including GST implications, PAYG, and BAS reconciliation. The solution covers the three main categories of tax obligations: registration, lodgement, and reporting/payment. It explores the application of GST, reporting on payroll activities, other amounts withheld, PAYG installments, and taxes. The assignment also details the tasks for completing and lodging activity statements, including BAS reconciliation steps and calculations. Furthermore, it examines the advantages of using the activity statement functions in the portal, the use of accounting software for lodging, the purpose of the Tax Agent Services Act 2009, and what can be included in a BAS. The solution also clarifies the difference between cash and non-cash reporting options.

MOHSIN ALI SHAIKH

1321600

1321600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOHSIN ALI SHAIKH

1321600

NO INDEX PAGE

NO

1

ASSIGNMENT 1 (QUESTION/ANSWERE)

QUESTION 1 TO 2 3

2 QUESTION 3 TO 5 4

3 QUESTION 5 TO 6 5

4 QUESTION 6 TO 8 6

5 QUESTION 8 TO 12 7

6 QUESTION 12 TO 14 8

7 QUESTION 15 TO 18 9

8 QUESTION 18 10

9 ASSIGNMENT 2

TASK 1 11/16

10 TASK 1 REFERENCES 16

11 TASK 2 17/22

12 TASK 2 REFERENCES 23

2

1321600

NO INDEX PAGE

NO

1

ASSIGNMENT 1 (QUESTION/ANSWERE)

QUESTION 1 TO 2 3

2 QUESTION 3 TO 5 4

3 QUESTION 5 TO 6 5

4 QUESTION 6 TO 8 6

5 QUESTION 8 TO 12 7

6 QUESTION 12 TO 14 8

7 QUESTION 15 TO 18 9

8 QUESTION 18 10

9 ASSIGNMENT 2

TASK 1 11/16

10 TASK 1 REFERENCES 16

11 TASK 2 17/22

12 TASK 2 REFERENCES 23

2

MOHSIN ALI SHAIKH

1321600

ASSESSMENT 1: WRITTEN QUESTIONS

QUESTIONS

1. What are the three main categories of tax obligations?

Answer: The three main tax obligations for the taxpayer are as follows;

a. Registration

b. Lodgement

c. Reporting and Payment

Irrespective of the type of entity an individual, big organization or SMSF all the tax

payers are required to make an application for the TFN and a large number of them

are required to lodge a yearly tax return.

2. What do you need to do in order to identify individual compliance and other

requirements?

Answer: Obeying to the lawful requirements and obligations or systematically and

preventively protecting the individual taxpayer in the field of taxes is known as the

tax compliance. Government with the help of the tax administrations, usually seek to

reduce their own system of taxation operating cost whereas at the same time

keeping the compliance cost for taxpayers as minimum as possible. In order to attain

this, an equilibrium should be created between the cost borne by the individual in

complying with the regulations of tax and the cost that is shouldered by the revenue

authority in running the system. Enforcing compliance through constant checks,

substantial audits and prosecution is considered as an expensive method of making

3

1321600

ASSESSMENT 1: WRITTEN QUESTIONS

QUESTIONS

1. What are the three main categories of tax obligations?

Answer: The three main tax obligations for the taxpayer are as follows;

a. Registration

b. Lodgement

c. Reporting and Payment

Irrespective of the type of entity an individual, big organization or SMSF all the tax

payers are required to make an application for the TFN and a large number of them

are required to lodge a yearly tax return.

2. What do you need to do in order to identify individual compliance and other

requirements?

Answer: Obeying to the lawful requirements and obligations or systematically and

preventively protecting the individual taxpayer in the field of taxes is known as the

tax compliance. Government with the help of the tax administrations, usually seek to

reduce their own system of taxation operating cost whereas at the same time

keeping the compliance cost for taxpayers as minimum as possible. In order to attain

this, an equilibrium should be created between the cost borne by the individual in

complying with the regulations of tax and the cost that is shouldered by the revenue

authority in running the system. Enforcing compliance through constant checks,

substantial audits and prosecution is considered as an expensive method of making

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOHSIN ALI SHAIKH

1321600

sure that adequate compliance is attained where the taxpayer is stimulated to co-

operate and actively comply with the regulations of taxation.

3. How would you recognise and apply GST implications and code transactions?

Answer: Recognizing and applying GST implications and code transactions are as

follows;

a. The fundamentals of GST are recognized, applied and recorded.

b. Purchases and payments are recorded, coded in accordance with the GST

classifications and they are split in capital and non-capital as considered

appropriate.

c. Sales and other receipts are recognized and coded according to the GST

classifications

d. Accounting data is processed to adhere with the reporting requirements of

taxation1.

4. What do you need to do to report on payroll activities?

Answer: Reporting on payroll activities are as follows;

a. An employer under the payroll activities is required to report to the ATO

regarding all the payments on or prior to the payday, through the payroll

event.

b. When the payment is made through electronic means, the day of payment is

either considered as the date that is stipulated in the electronic transactions or

else no date is specified, the data on which the payment is proposed to be

made in the employees bank account.

c. The report should take into the account the employee, with the amount that is

subjected to withholding in the regular cycle of pay.

1 Coleman, C, & K Sadiq, Principles of taxation law 2013. in

4

1321600

sure that adequate compliance is attained where the taxpayer is stimulated to co-

operate and actively comply with the regulations of taxation.

3. How would you recognise and apply GST implications and code transactions?

Answer: Recognizing and applying GST implications and code transactions are as

follows;

a. The fundamentals of GST are recognized, applied and recorded.

b. Purchases and payments are recorded, coded in accordance with the GST

classifications and they are split in capital and non-capital as considered

appropriate.

c. Sales and other receipts are recognized and coded according to the GST

classifications

d. Accounting data is processed to adhere with the reporting requirements of

taxation1.

4. What do you need to do to report on payroll activities?

Answer: Reporting on payroll activities are as follows;

a. An employer under the payroll activities is required to report to the ATO

regarding all the payments on or prior to the payday, through the payroll

event.

b. When the payment is made through electronic means, the day of payment is

either considered as the date that is stipulated in the electronic transactions or

else no date is specified, the data on which the payment is proposed to be

made in the employees bank account.

c. The report should take into the account the employee, with the amount that is

subjected to withholding in the regular cycle of pay.

1 Coleman, C, & K Sadiq, Principles of taxation law 2013. in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOHSIN ALI SHAIKH

1321600

d. Total amount of salaries and other types of payments during the period of

accounting are recognized and reconciled.

e. The sum that is to be withhold from the salaries, wages and other payments

during the period of accounting are recognized and reconciled in the

conjunctions with the department of payroll if it is applicable.

5. What do you need to do in order to report on other amounts withheld, PAYG

instalments and taxes?

Answer: The requirements of reporting on the other amount withheld, PAYG

instalments and taxes are as follows;

a. An employer having a branch for PAYG for withholding purpose, the employer

is required to report separately the payroll events for each of the PAYG

withholding branch that is established with the ATO.

b. Amounts that are withheld from other payments during the period of

accounting are recognized and identified and reconciled in accordance with

other subdivisions provided they are applicable.

c. The instalment amount of PAYG should be verified or wherever applicable

should be computed.

d. Instalments amounts must be verified wherever applicable and must be

computed for other taxes2.

6. What tasks must be performed when completing and reconciling the activity

statement?

2 Kenny, P, Australian tax 2013. in , Chatswood, N.S.W., LexisNexis

Butterworths, 2013.

5

1321600

d. Total amount of salaries and other types of payments during the period of

accounting are recognized and reconciled.

e. The sum that is to be withhold from the salaries, wages and other payments

during the period of accounting are recognized and reconciled in the

conjunctions with the department of payroll if it is applicable.

5. What do you need to do in order to report on other amounts withheld, PAYG

instalments and taxes?

Answer: The requirements of reporting on the other amount withheld, PAYG

instalments and taxes are as follows;

a. An employer having a branch for PAYG for withholding purpose, the employer

is required to report separately the payroll events for each of the PAYG

withholding branch that is established with the ATO.

b. Amounts that are withheld from other payments during the period of

accounting are recognized and identified and reconciled in accordance with

other subdivisions provided they are applicable.

c. The instalment amount of PAYG should be verified or wherever applicable

should be computed.

d. Instalments amounts must be verified wherever applicable and must be

computed for other taxes2.

6. What tasks must be performed when completing and reconciling the activity

statement?

2 Kenny, P, Australian tax 2013. in , Chatswood, N.S.W., LexisNexis

Butterworths, 2013.

5

MOHSIN ALI SHAIKH

1321600

Answer: Tasks that needs to be executed at the time of completing and reconciling

the activity statement are as follows;

a. Activity statement report should be generated whenever required and should

be checked and validated.

b. Errors should be identified and correct bookkeeping entries must be

generated.

c. Adjustment for previous quarter should be made, or months or end of the year

whenever it is necessary.

d. BAS and IAS return must be completed in compliance with the up to date

statutory, regulatory and legislative organisational schedule.

e. Figures must be completed on the BAS and IAS form and must be reconciled

with the journal entries profit and loss statement, GST and other forms of

control accounts.

7. What tasks are required when lodging an activity statement?

Answer: Task required at the time of lodging activity statements are as follows;

a. Activity statement must be checked and signed off by an appropriate

individual as identified by the statutory legislation and regulations

requirements

b. Activity statements must be dispatched in compliance with the statutory

requirements, legislative and regulatory requirements.

c. Payment or any form of refund that is processed must be recorded.

8. What steps are involved in completing a BAS reconciliation?

6

1321600

Answer: Tasks that needs to be executed at the time of completing and reconciling

the activity statement are as follows;

a. Activity statement report should be generated whenever required and should

be checked and validated.

b. Errors should be identified and correct bookkeeping entries must be

generated.

c. Adjustment for previous quarter should be made, or months or end of the year

whenever it is necessary.

d. BAS and IAS return must be completed in compliance with the up to date

statutory, regulatory and legislative organisational schedule.

e. Figures must be completed on the BAS and IAS form and must be reconciled

with the journal entries profit and loss statement, GST and other forms of

control accounts.

7. What tasks are required when lodging an activity statement?

Answer: Task required at the time of lodging activity statements are as follows;

a. Activity statement must be checked and signed off by an appropriate

individual as identified by the statutory legislation and regulations

requirements

b. Activity statements must be dispatched in compliance with the statutory

requirements, legislative and regulatory requirements.

c. Payment or any form of refund that is processed must be recorded.

8. What steps are involved in completing a BAS reconciliation?

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOHSIN ALI SHAIKH

1321600

Answer: Steps involved in completed BAS reconciliation are as follows;

Step 1: Preparing the information: Under this step the taxpayer is required to

reconcile their books of accounts to make sure that all the information is correct and

up to date.

Step 2: Entering Missing Transactions: An individual is required to record any

missing transaction for which they have receipts and invoices. For each of the

missing transactions the taxpayer will be needing a date, total sum of the

transaction, amount of GST and description3.

Step 3: Totalling all records: Once the information is appropriately entered an

individual can either run the activity statement in their software or if an individual is

using a manual method then all the numbers must be added up to determine the

amount of GST that is owed during the period of tax.

Step 4: Updating the records and lodge: Once the taxpayer has completed the BAS,

they are required to update their records with new information and make the copies

of all the necessary documents. Then in the later stages either the taxpayer should

mail the hard copy of the BAS form to the ATO or they can file through electronic

means to the portal of ATO or have their agent to lodge the report on behalf of the

taxpayer.

9. How can you calculate the amount of GST that needs to be paid or will be

refunded?

Answer: GST is payable if an individual makes a taxable supply. A taxable supply is

the supply that an individual has paid for or receive considerations for in the course

of running their business. GST is computed as the 10 per cent of the amount of the

supply. The worth of the taxable supply represents the considerations that is payable

during the supply.

10. What is GST?

Answer: GST can be defined as the goods and service tax which represents a

broad based tax of 10 per cent on large number of goods, service and other items

that are sold and consumed in Australia. GST is applicable to most of the production

in Australia however it is refunded to all the parties that are involved in the chain of

production other than the final consumers. All the Australia business whose turnover

3 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson

Reuters, 2013.

7

1321600

Answer: Steps involved in completed BAS reconciliation are as follows;

Step 1: Preparing the information: Under this step the taxpayer is required to

reconcile their books of accounts to make sure that all the information is correct and

up to date.

Step 2: Entering Missing Transactions: An individual is required to record any

missing transaction for which they have receipts and invoices. For each of the

missing transactions the taxpayer will be needing a date, total sum of the

transaction, amount of GST and description3.

Step 3: Totalling all records: Once the information is appropriately entered an

individual can either run the activity statement in their software or if an individual is

using a manual method then all the numbers must be added up to determine the

amount of GST that is owed during the period of tax.

Step 4: Updating the records and lodge: Once the taxpayer has completed the BAS,

they are required to update their records with new information and make the copies

of all the necessary documents. Then in the later stages either the taxpayer should

mail the hard copy of the BAS form to the ATO or they can file through electronic

means to the portal of ATO or have their agent to lodge the report on behalf of the

taxpayer.

9. How can you calculate the amount of GST that needs to be paid or will be

refunded?

Answer: GST is payable if an individual makes a taxable supply. A taxable supply is

the supply that an individual has paid for or receive considerations for in the course

of running their business. GST is computed as the 10 per cent of the amount of the

supply. The worth of the taxable supply represents the considerations that is payable

during the supply.

10. What is GST?

Answer: GST can be defined as the goods and service tax which represents a

broad based tax of 10 per cent on large number of goods, service and other items

that are sold and consumed in Australia. GST is applicable to most of the production

in Australia however it is refunded to all the parties that are involved in the chain of

production other than the final consumers. All the Australia business whose turnover

3 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson

Reuters, 2013.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOHSIN ALI SHAIKH

1321600

is beyond the minimum threshold limit of $75,000 per annum are required to get

registered for the purpose of GST.

11. When does PAYG apply?

Answer: When an individual makes payments to the employees and some

contractors they are required to withhold the amount and send it to the Australia

Taxation Office at the regular intervals. An individual has the withholding obligations

if any of the following is applicable;

a. If an individual has employees

b. An individual has other workers, such as contractors and they enter into

voluntary agreement to withholding amounts from their payment to them.

c. If an individual makes payment to the business that do not quote their

Australian business number.

12. What advantages are there in using the activity statement functions in the

portal?

Answer: The business portal is considered as the gateway to the Australian

government online service for business. It is regarded as the easy and convenient

method of accessing information and managing the business tax affairs. The benefits

of having activity statement portal on the portal are as follows;

a. An individual can view, prepare, lodge and revise their activity statements

b. An individual can update and view their details of the business registration

c. An individual can view their statement of account and options of payment

d. An individual can request for refunds and transfer credits

e. Send messages to the office of taxation on the selected matters4.

13. Can you use your accounting software package to lodge without having to

manually re-key the data on to the activity statement showing in the portal?

4 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation

law. in , North Ryde [N.S.W.], CCH Australia, 2013.

8

1321600

is beyond the minimum threshold limit of $75,000 per annum are required to get

registered for the purpose of GST.

11. When does PAYG apply?

Answer: When an individual makes payments to the employees and some

contractors they are required to withhold the amount and send it to the Australia

Taxation Office at the regular intervals. An individual has the withholding obligations

if any of the following is applicable;

a. If an individual has employees

b. An individual has other workers, such as contractors and they enter into

voluntary agreement to withholding amounts from their payment to them.

c. If an individual makes payment to the business that do not quote their

Australian business number.

12. What advantages are there in using the activity statement functions in the

portal?

Answer: The business portal is considered as the gateway to the Australian

government online service for business. It is regarded as the easy and convenient

method of accessing information and managing the business tax affairs. The benefits

of having activity statement portal on the portal are as follows;

a. An individual can view, prepare, lodge and revise their activity statements

b. An individual can update and view their details of the business registration

c. An individual can view their statement of account and options of payment

d. An individual can request for refunds and transfer credits

e. Send messages to the office of taxation on the selected matters4.

13. Can you use your accounting software package to lodge without having to

manually re-key the data on to the activity statement showing in the portal?

4 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation

law. in , North Ryde [N.S.W.], CCH Australia, 2013.

8

MOHSIN ALI SHAIKH

1321600

Answer: Yes, an individual can make the use of the accounting software package to

lodge the tax return without entering manually the re-key on the business activity

statements that is showing in the portal.

14. State the purpose of the Tax Agent Services Act 2009.

Answer: The purpose of the tax agent service act 2009 are as follows;

a. The main purpose of the tax agent services act 2009 is to make sure that the

agent services are offered to the public in compliance with the correct

standards of professional and ethical code of conduct.

b. The purpose of this act is to establish a national board in order to register tax

agents and BAS agents

c. The purpose of tax agent service act 2009 is to introduce a code of

professional conduct for agents that are tax registered and BAS agents

d. Providing for a permission to self-control registered tax agents and BAS

agents5.

15. Under the TASA 2009, what is a BAS service?

Answer: A BAS service can be defined as the tax agent service which is related to

the ascertainment of the liabilities, obligations or entitlements of an entity which arise

or might arise under the provision of the BAS. It provides an advise to the entities

regarding the liabilities, obligations or entitlements of the entity or any other entity

that originate or might arise under the provision of the BAS.

16. Can you complete a BAS return using Xero?

Answer: Yes, an individual tax payer can complete the BAS by using the Xero. This

is because the activity statement that is generated by the Xero for the Australian

5 Woellner, R, Australian taxation law select 2013. in , North Ryde, N.S.W., CCH

Australia, 2013.

9

1321600

Answer: Yes, an individual can make the use of the accounting software package to

lodge the tax return without entering manually the re-key on the business activity

statements that is showing in the portal.

14. State the purpose of the Tax Agent Services Act 2009.

Answer: The purpose of the tax agent service act 2009 are as follows;

a. The main purpose of the tax agent services act 2009 is to make sure that the

agent services are offered to the public in compliance with the correct

standards of professional and ethical code of conduct.

b. The purpose of this act is to establish a national board in order to register tax

agents and BAS agents

c. The purpose of tax agent service act 2009 is to introduce a code of

professional conduct for agents that are tax registered and BAS agents

d. Providing for a permission to self-control registered tax agents and BAS

agents5.

15. Under the TASA 2009, what is a BAS service?

Answer: A BAS service can be defined as the tax agent service which is related to

the ascertainment of the liabilities, obligations or entitlements of an entity which arise

or might arise under the provision of the BAS. It provides an advise to the entities

regarding the liabilities, obligations or entitlements of the entity or any other entity

that originate or might arise under the provision of the BAS.

16. Can you complete a BAS return using Xero?

Answer: Yes, an individual tax payer can complete the BAS by using the Xero. This

is because the activity statement that is generated by the Xero for the Australian

5 Woellner, R, Australian taxation law select 2013. in , North Ryde, N.S.W., CCH

Australia, 2013.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOHSIN ALI SHAIKH

1321600

taxation office is based on the PAYG withholding and the frequency of GST

reporting. Therefore, using the BAS serves as the advantage for multiple users that

are working in the organization.

17. What can be included in a BAS?

Answer: Items that can be included in the BAS are as follows;

a. Gross fees for services

b. Gross amount of sales

c. Trade-in and barter transactions

d. Amount of interest earned

e. Rents

f. Overseas income

g. Commissions

h. Fees relating to membership and subscriptions

i. Grants received from government and specific grants from private sector

j. Amount derived from the sale of business assets namely office equipment’s.

18. What is the difference between Cash & Non-Cash reporting options?

Answer: The main difference between non-cash and cash basis of accounting

reporting lies during the time when the revenue and expenses are identified. Under

the cash method of reporting it is largely used by the small business and for personal

finance6. The cash method of accounts for revenue is considered when the amount

of money is received and for the expenditure when the money is paid out. In contrast

to this, the accrual method of accounts for revenue represents when the revenue is

earned and expenses for goods and services when they are incurred. The amount of

revenue is recorded even though the cash is not received or the expenditure have

been incurred but no cash has been paid. Non-cash method of reporting is the most

common method of reporting that is used by the business.

6 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson

Reuters, 2013.

10

1321600

taxation office is based on the PAYG withholding and the frequency of GST

reporting. Therefore, using the BAS serves as the advantage for multiple users that

are working in the organization.

17. What can be included in a BAS?

Answer: Items that can be included in the BAS are as follows;

a. Gross fees for services

b. Gross amount of sales

c. Trade-in and barter transactions

d. Amount of interest earned

e. Rents

f. Overseas income

g. Commissions

h. Fees relating to membership and subscriptions

i. Grants received from government and specific grants from private sector

j. Amount derived from the sale of business assets namely office equipment’s.

18. What is the difference between Cash & Non-Cash reporting options?

Answer: The main difference between non-cash and cash basis of accounting

reporting lies during the time when the revenue and expenses are identified. Under

the cash method of reporting it is largely used by the small business and for personal

finance6. The cash method of accounts for revenue is considered when the amount

of money is received and for the expenditure when the money is paid out. In contrast

to this, the accrual method of accounts for revenue represents when the revenue is

earned and expenses for goods and services when they are incurred. The amount of

revenue is recorded even though the cash is not received or the expenditure have

been incurred but no cash has been paid. Non-cash method of reporting is the most

common method of reporting that is used by the business.

6 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson

Reuters, 2013.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOHSIN ALI SHAIKH

1321600

ASSESSMENT 2: SKILLS ASSESSMENT

Task 1 – Financial Activity Reporting #1

A. Using the accounts following, complete the GST Worksheet for BAS. Complete

the BAS Statement (copy may be downloaded from the Australian Taxation Office at

https://www.ato.gov.au/uploadedFiles/Content/CAS/downloads/BUS25199Nat4189s.

pdf).

Trial balance

Trial balance

11

1321600

ASSESSMENT 2: SKILLS ASSESSMENT

Task 1 – Financial Activity Reporting #1

A. Using the accounts following, complete the GST Worksheet for BAS. Complete

the BAS Statement (copy may be downloaded from the Australian Taxation Office at

https://www.ato.gov.au/uploadedFiles/Content/CAS/downloads/BUS25199Nat4189s.

pdf).

Trial balance

Trial balance

11

MOHSIN ALI SHAIKH

1321600

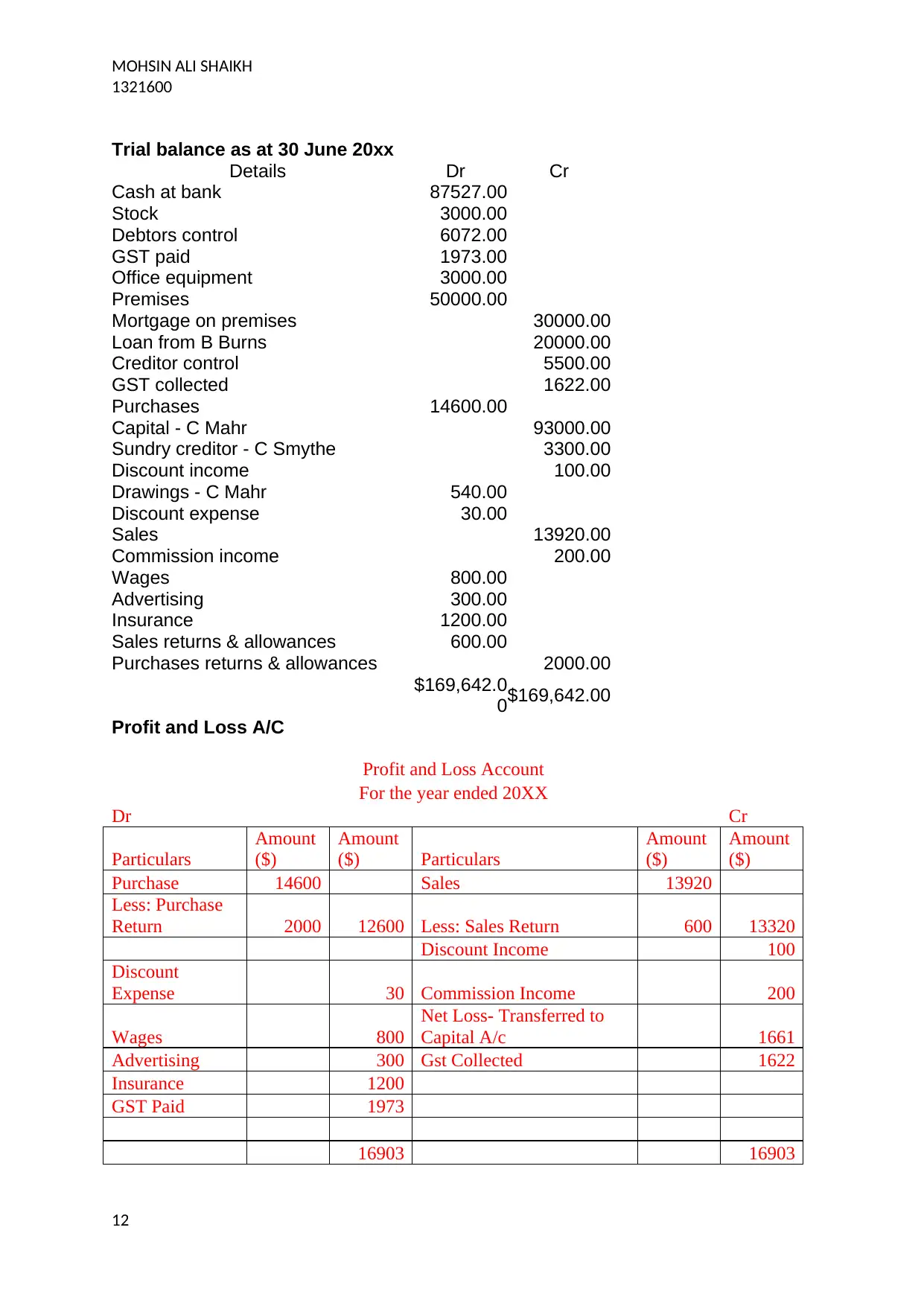

Trial balance as at 30 June 20xx

Details Dr Cr

Cash at bank 87527.00

Stock 3000.00

Debtors control 6072.00

GST paid 1973.00

Office equipment 3000.00

Premises 50000.00

Mortgage on premises 30000.00

Loan from B Burns 20000.00

Creditor control 5500.00

GST collected 1622.00

Purchases 14600.00

Capital - C Mahr 93000.00

Sundry creditor - C Smythe 3300.00

Discount income 100.00

Drawings - C Mahr 540.00

Discount expense 30.00

Sales 13920.00

Commission income 200.00

Wages 800.00

Advertising 300.00

Insurance 1200.00

Sales returns & allowances 600.00

Purchases returns & allowances 2000.00

$169,642.0

0$169,642.00

Profit and Loss A/C

Profit and Loss Account

For the year ended 20XX

Dr Cr

Particulars

Amount

($)

Amount

($) Particulars

Amount

($)

Amount

($)

Purchase 14600 Sales 13920

Less: Purchase

Return 2000 12600 Less: Sales Return 600 13320

Discount Income 100

Discount

Expense 30 Commission Income 200

Wages 800

Net Loss- Transferred to

Capital A/c 1661

Advertising 300 Gst Collected 1622

Insurance 1200

GST Paid 1973

16903 16903

12

1321600

Trial balance as at 30 June 20xx

Details Dr Cr

Cash at bank 87527.00

Stock 3000.00

Debtors control 6072.00

GST paid 1973.00

Office equipment 3000.00

Premises 50000.00

Mortgage on premises 30000.00

Loan from B Burns 20000.00

Creditor control 5500.00

GST collected 1622.00

Purchases 14600.00

Capital - C Mahr 93000.00

Sundry creditor - C Smythe 3300.00

Discount income 100.00

Drawings - C Mahr 540.00

Discount expense 30.00

Sales 13920.00

Commission income 200.00

Wages 800.00

Advertising 300.00

Insurance 1200.00

Sales returns & allowances 600.00

Purchases returns & allowances 2000.00

$169,642.0

0$169,642.00

Profit and Loss A/C

Profit and Loss Account

For the year ended 20XX

Dr Cr

Particulars

Amount

($)

Amount

($) Particulars

Amount

($)

Amount

($)

Purchase 14600 Sales 13920

Less: Purchase

Return 2000 12600 Less: Sales Return 600 13320

Discount Income 100

Discount

Expense 30 Commission Income 200

Wages 800

Net Loss- Transferred to

Capital A/c 1661

Advertising 300 Gst Collected 1622

Insurance 1200

GST Paid 1973

16903 16903

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.