Hewlett-Packard Financial Statement Analysis

VerifiedAdded on 2019/10/01

|14

|3235

|307

Report

AI Summary

This report provides a detailed financial analysis of Hewlett-Packard, encompassing sales analysis and an assessment of profitability. It explains key concepts like target profitability, lifetime value cash flow, variable costs, and fixed costs. The report includes calculations using sample and existing customer sales data to illustrate these concepts. Furthermore, it delves into the organization's management accounting procedures for handling various costs, evaluating their effectiveness, and providing a step-by-step analysis of customer account profitability for sustainable performance. The report also evaluates the value of each client, recommends strategies for client growth, assesses business and financial risks associated with each account, identifies key trends and variances, and discusses where to find relevant financial data both internally and externally. Finally, it outlines who within the organization has a stake in the financial performance of these accounts and how to ensure appropriate data access, provides proformas for capturing performance data, and develops contingency plans for potential financial problems.

Hewlett-Packard

Financial statement

Financial statement and sales analysis

Name of the author-

University Name-

[Type the abstract of the document here. The abstract is typically a short summary of the contents

of the document. Type the abstract of the document here. The abstract is typically a short

summary of the contents of the document.]

Financial statement

Financial statement and sales analysis

Name of the author-

University Name-

[Type the abstract of the document here. The abstract is typically a short summary of the contents

of the document. Type the abstract of the document here. The abstract is typically a short

summary of the contents of the document.]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1:...................................................................................................................................................3

Training Workbook for Sales Team........................................................................................................3

An explanation of the following concepts..................................................................................3

Using 2 made up sales volume numbers (simple) and 2 existing customers’ sales volume numbers

calculate;............................................................................................................................................3

The below given table shows the sales volume numbers and 2 existing client’s sales volume

numbers calculation...........................................................................................................................4

Assessment of the variable cost and cost which could impact the profitability..........................5

A description of your organisation’s management accounting procedures for dealing with the

following costs;.................................................................................................................................6

An evaluation of these costs and why these methods are used...................................................6

Example which shows the step by step analysis of the customer account for the profitability and how

it could be used for the sustainable customer performance.................................................................6

Task 2:...................................................................................................................................................9

Preparation of the financial analysis of company..................................................................................9

Evaluating the value of each clients towards.............................................................................9

Recommendation for growing the number of these clients in business..............................................9

An evaluation of the business and financial risks associated with each account.................................10

An identification of any key trends or variances......................................................................11

Where you would expect to look for financial data on these accounts (inside and outside your

organisation)....................................................................................................................................11

An identification of who else in your organisation would have a stake in the financial viability

and performance of these accounts and how you would ensure appropriate access to the data.......12

A provision of any proformas for capturing performance and financial data about these

accounts and the development of contingency plans for possible problems that may arise with the

financial performance of the accounts.............................................................................................12

REFERENCES....................................................................................................................................13

Task 1:...................................................................................................................................................3

Training Workbook for Sales Team........................................................................................................3

An explanation of the following concepts..................................................................................3

Using 2 made up sales volume numbers (simple) and 2 existing customers’ sales volume numbers

calculate;............................................................................................................................................3

The below given table shows the sales volume numbers and 2 existing client’s sales volume

numbers calculation...........................................................................................................................4

Assessment of the variable cost and cost which could impact the profitability..........................5

A description of your organisation’s management accounting procedures for dealing with the

following costs;.................................................................................................................................6

An evaluation of these costs and why these methods are used...................................................6

Example which shows the step by step analysis of the customer account for the profitability and how

it could be used for the sustainable customer performance.................................................................6

Task 2:...................................................................................................................................................9

Preparation of the financial analysis of company..................................................................................9

Evaluating the value of each clients towards.............................................................................9

Recommendation for growing the number of these clients in business..............................................9

An evaluation of the business and financial risks associated with each account.................................10

An identification of any key trends or variances......................................................................11

Where you would expect to look for financial data on these accounts (inside and outside your

organisation)....................................................................................................................................11

An identification of who else in your organisation would have a stake in the financial viability

and performance of these accounts and how you would ensure appropriate access to the data.......12

A provision of any proformas for capturing performance and financial data about these

accounts and the development of contingency plans for possible problems that may arise with the

financial performance of the accounts.............................................................................................12

REFERENCES....................................................................................................................................13

Task 1:

Training Workbook for Sales Team

An explanation of the following concepts

TARGET PROFITABILITY:

Target profitability could be defined as profit earned by company that managers and

directors of company anticipated to achieve in the given time frame. It is the part of the

budget which shows the expected earning of company. It is used to make comparison

between the actual and anticipated profit by the company so that proper variance issues and

challenges could be found (Mennen, & Storbacka, 2016).

LIFE TIME VALUE CASH FLOW:

This life time value cash flow shows present value of the cash inflow and outflow

generated by the company. It helps in evaluating the market price of company, identifying the

possible future cash value in present. It is further used in the marketing strategies and

preparing the budget for company. Life time value is computed by multiplying the average

order value with the number of the repeated sales and average retention time (Napoli, et, al.

2014).

VARIABLE COSTS:

The Variable cost is depicts the expenses incurred in busienss which changes with the

changes in the production level. It is based on the production level and changed accordingly.

The variable cost is associated with the packing cost, customer discount cost, delivery cost

and other related cost.

FIXED COSTS:

The Fixed cost is the amount of expenses which do not vary with the changes in the

production level. However, it helps in reduction in overall production cost if company

increases its production level. It is accompanied with the following cost such as wages, rent,

interest change of bank and electricity charges (Napoli, et, al. 2014).

Using 2 made up sales volume numbers (simple) and 2 existing customers’ sales volume

numbers calculate;

Training Workbook for Sales Team

An explanation of the following concepts

TARGET PROFITABILITY:

Target profitability could be defined as profit earned by company that managers and

directors of company anticipated to achieve in the given time frame. It is the part of the

budget which shows the expected earning of company. It is used to make comparison

between the actual and anticipated profit by the company so that proper variance issues and

challenges could be found (Mennen, & Storbacka, 2016).

LIFE TIME VALUE CASH FLOW:

This life time value cash flow shows present value of the cash inflow and outflow

generated by the company. It helps in evaluating the market price of company, identifying the

possible future cash value in present. It is further used in the marketing strategies and

preparing the budget for company. Life time value is computed by multiplying the average

order value with the number of the repeated sales and average retention time (Napoli, et, al.

2014).

VARIABLE COSTS:

The Variable cost is depicts the expenses incurred in busienss which changes with the

changes in the production level. It is based on the production level and changed accordingly.

The variable cost is associated with the packing cost, customer discount cost, delivery cost

and other related cost.

FIXED COSTS:

The Fixed cost is the amount of expenses which do not vary with the changes in the

production level. However, it helps in reduction in overall production cost if company

increases its production level. It is accompanied with the following cost such as wages, rent,

interest change of bank and electricity charges (Napoli, et, al. 2014).

Using 2 made up sales volume numbers (simple) and 2 existing customers’ sales volume

numbers calculate;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The below given table shows the sales volume numbers and 2 existing client’s sales volume

numbers calculation.

FIANNCIAL DATA

PARTICULARS sales

quantity

sales

price

variable

cost %

budgete

d fixed

cost

sampl

e

customer

1

30000 15 20% 30000

customer

2

25000 15 20%

actual customer

1

40000 15 20%

customer

2

20000 15 20%

TARGET PROFITABILITY

Revenue Budgeted

variable

cost

PROFIT

before

fixed

costs

Total

profit

before

variable

cost

Less:

fixed

cost

TARGET

PROFITABILIT

Y

Formula Sales

Volume *

sales price

Revenue *

15%

- - - -

Sampl

e

Custome

r 1

450000 67500 382500 146625

0

3000

0

1436250

Custome

r 2

375000 56250 318750

Actual Custome

r 1

600000 90000 510000

Custome

r 2

300000 45000 255000

numbers calculation.

FIANNCIAL DATA

PARTICULARS sales

quantity

sales

price

variable

cost %

budgete

d fixed

cost

sampl

e

customer

1

30000 15 20% 30000

customer

2

25000 15 20%

actual customer

1

40000 15 20%

customer

2

20000 15 20%

TARGET PROFITABILITY

Revenue Budgeted

variable

cost

PROFIT

before

fixed

costs

Total

profit

before

variable

cost

Less:

fixed

cost

TARGET

PROFITABILIT

Y

Formula Sales

Volume *

sales price

Revenue *

15%

- - - -

Sampl

e

Custome

r 1

450000 67500 382500 146625

0

3000

0

1436250

Custome

r 2

375000 56250 318750

Actual Custome

r 1

600000 90000 510000

Custome

r 2

300000 45000 255000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIFE VALUE CASH FLOW

LIFETIME VALUE CASH FLOW

acquisition

year

second

year

third

year

A CUSTOMER BASE 4 3.6 2.88

B retention 90% 80% 70%

C average sales (115000/4) 21250 21250 21250

D sales price per unit 20 20 20

E revenue (C X D) 425000 425000 425000

F total revenue (E X A) 1700000 1530000 1224000

G Variable cost (F X 20%) 340000 306000 244800

H fixed cost 30000 30000 30000

I net profit 1330000 1194000 949200

J discount factor @ 10% 1.0000 0.9091 0.8264

K net present value of net

profit

1330000 1085455 784463

L cumulative net present

value profit

1330000 2415455 3199917

customer lifetime value cash

flow (L/4)

332500 603864 799979

Assessment of the variable cost and cost which could impact the profitability

Variable cost varies with the changes in the production level. However, various

variable costs impact the earning capacity and profitability of company. All the variable costs

are the % of the total sales and the amount of variable cost increases with the increase in sales

and vice-versa. Therefore, variable cost is used to analyze the business cost and better

assessment of the financial performance of company. However, for this, we could use budget

analysis by comparing the actual variable cost with the estimated budget cost. This is the

variable cost such as special cost of customer delivery, management cost, packing cost and

marketing cost. The profitability of business could not impact if the % of the variable cost

does not change. However, marginal cost may decrease with the increase in the sales due to

the low impact of the fixed cost on the overall cost of production (Napoli, et, al. 2014).

A description of your organisation’s management accounting procedures for dealing

with the following costs;

FIXED OVERHEADS:

LIFETIME VALUE CASH FLOW

acquisition

year

second

year

third

year

A CUSTOMER BASE 4 3.6 2.88

B retention 90% 80% 70%

C average sales (115000/4) 21250 21250 21250

D sales price per unit 20 20 20

E revenue (C X D) 425000 425000 425000

F total revenue (E X A) 1700000 1530000 1224000

G Variable cost (F X 20%) 340000 306000 244800

H fixed cost 30000 30000 30000

I net profit 1330000 1194000 949200

J discount factor @ 10% 1.0000 0.9091 0.8264

K net present value of net

profit

1330000 1085455 784463

L cumulative net present

value profit

1330000 2415455 3199917

customer lifetime value cash

flow (L/4)

332500 603864 799979

Assessment of the variable cost and cost which could impact the profitability

Variable cost varies with the changes in the production level. However, various

variable costs impact the earning capacity and profitability of company. All the variable costs

are the % of the total sales and the amount of variable cost increases with the increase in sales

and vice-versa. Therefore, variable cost is used to analyze the business cost and better

assessment of the financial performance of company. However, for this, we could use budget

analysis by comparing the actual variable cost with the estimated budget cost. This is the

variable cost such as special cost of customer delivery, management cost, packing cost and

marketing cost. The profitability of business could not impact if the % of the variable cost

does not change. However, marginal cost may decrease with the increase in the sales due to

the low impact of the fixed cost on the overall cost of production (Napoli, et, al. 2014).

A description of your organisation’s management accounting procedures for dealing

with the following costs;

FIXED OVERHEADS:

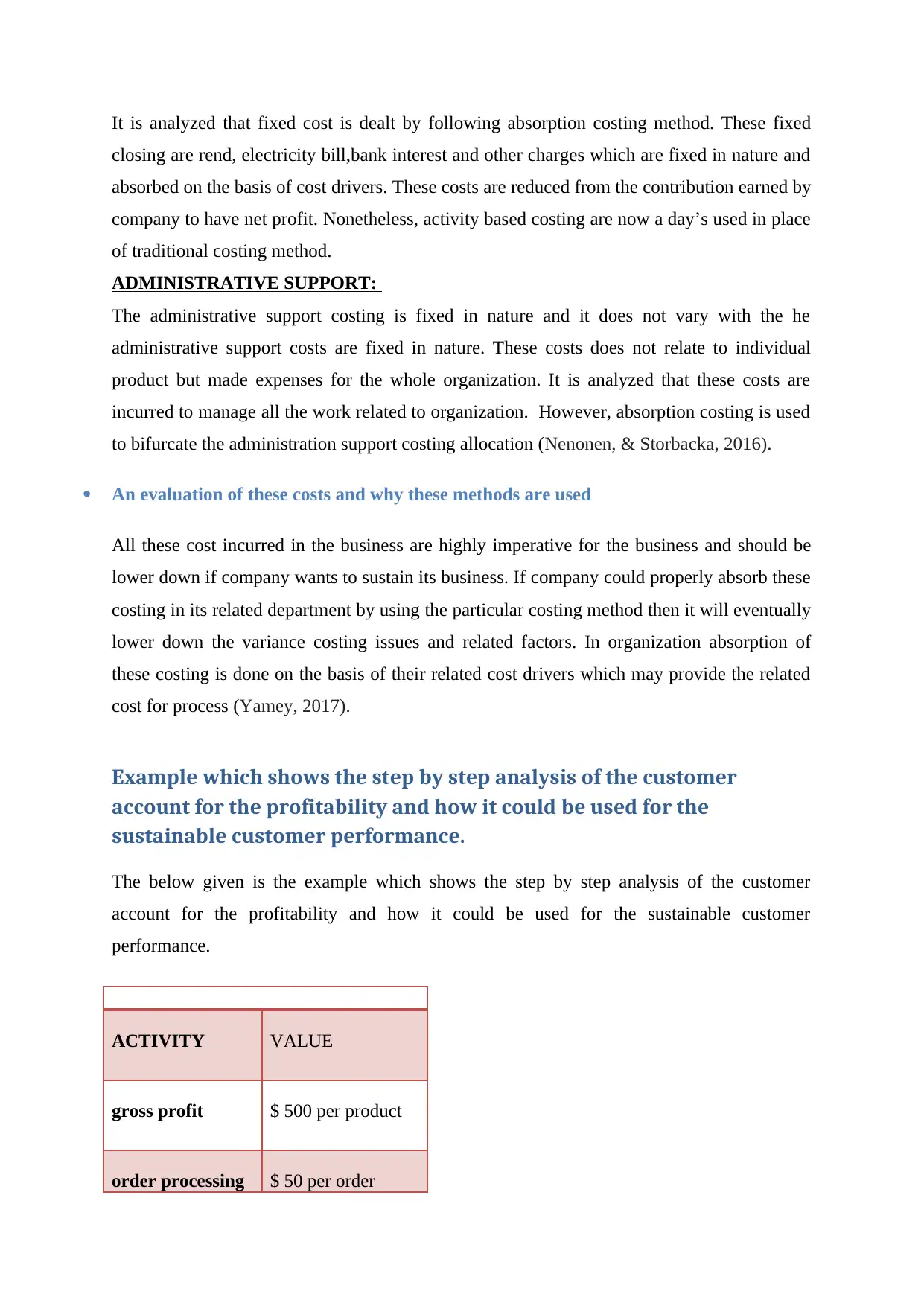

It is analyzed that fixed cost is dealt by following absorption costing method. These fixed

closing are rend, electricity bill,bank interest and other charges which are fixed in nature and

absorbed on the basis of cost drivers. These costs are reduced from the contribution earned by

company to have net profit. Nonetheless, activity based costing are now a day’s used in place

of traditional costing method.

ADMINISTRATIVE SUPPORT:

The administrative support costing is fixed in nature and it does not vary with the he

administrative support costs are fixed in nature. These costs does not relate to individual

product but made expenses for the whole organization. It is analyzed that these costs are

incurred to manage all the work related to organization. However, absorption costing is used

to bifurcate the administration support costing allocation (Nenonen, & Storbacka, 2016).

An evaluation of these costs and why these methods are used

All these cost incurred in the business are highly imperative for the business and should be

lower down if company wants to sustain its business. If company could properly absorb these

costing in its related department by using the particular costing method then it will eventually

lower down the variance costing issues and related factors. In organization absorption of

these costing is done on the basis of their related cost drivers which may provide the related

cost for process (Yamey, 2017).

Example which shows the step by step analysis of the customer

account for the profitability and how it could be used for the

sustainable customer performance.

The below given is the example which shows the step by step analysis of the customer

account for the profitability and how it could be used for the sustainable customer

performance.

ACTIVITY VALUE

gross profit $ 500 per product

order processing $ 50 per order

closing are rend, electricity bill,bank interest and other charges which are fixed in nature and

absorbed on the basis of cost drivers. These costs are reduced from the contribution earned by

company to have net profit. Nonetheless, activity based costing are now a day’s used in place

of traditional costing method.

ADMINISTRATIVE SUPPORT:

The administrative support costing is fixed in nature and it does not vary with the he

administrative support costs are fixed in nature. These costs does not relate to individual

product but made expenses for the whole organization. It is analyzed that these costs are

incurred to manage all the work related to organization. However, absorption costing is used

to bifurcate the administration support costing allocation (Nenonen, & Storbacka, 2016).

An evaluation of these costs and why these methods are used

All these cost incurred in the business are highly imperative for the business and should be

lower down if company wants to sustain its business. If company could properly absorb these

costing in its related department by using the particular costing method then it will eventually

lower down the variance costing issues and related factors. In organization absorption of

these costing is done on the basis of their related cost drivers which may provide the related

cost for process (Yamey, 2017).

Example which shows the step by step analysis of the customer

account for the profitability and how it could be used for the

sustainable customer performance.

The below given is the example which shows the step by step analysis of the customer

account for the profitability and how it could be used for the sustainable customer

performance.

ACTIVITY VALUE

gross profit $ 500 per product

order processing $ 50 per order

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

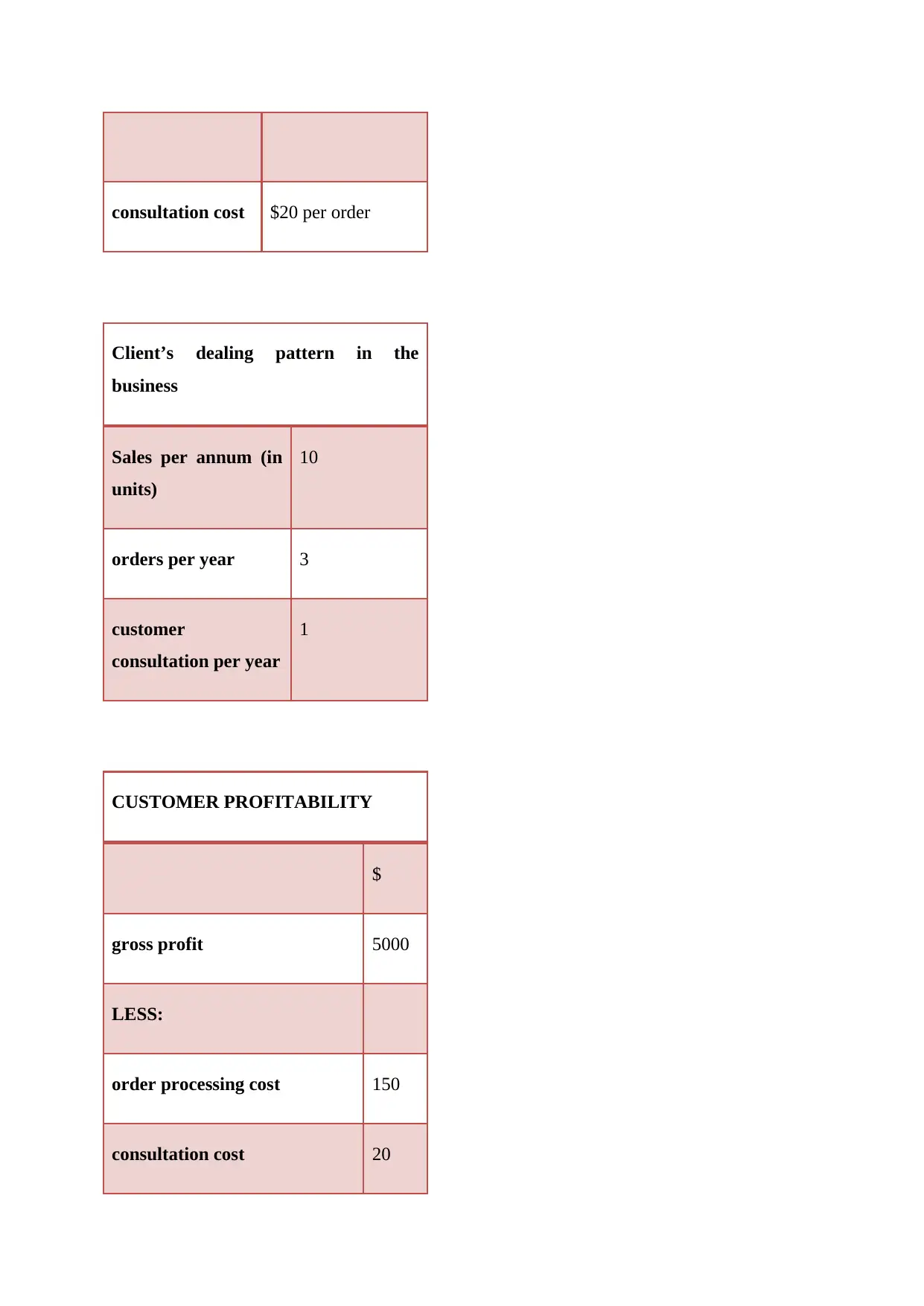

consultation cost $20 per order

Client’s dealing pattern in the

business

Sales per annum (in

units)

10

orders per year 3

customer

consultation per year

1

CUSTOMER PROFITABILITY

$

gross profit 5000

LESS:

order processing cost 150

consultation cost 20

Client’s dealing pattern in the

business

Sales per annum (in

units)

10

orders per year 3

customer

consultation per year

1

CUSTOMER PROFITABILITY

$

gross profit 5000

LESS:

order processing cost 150

consultation cost 20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

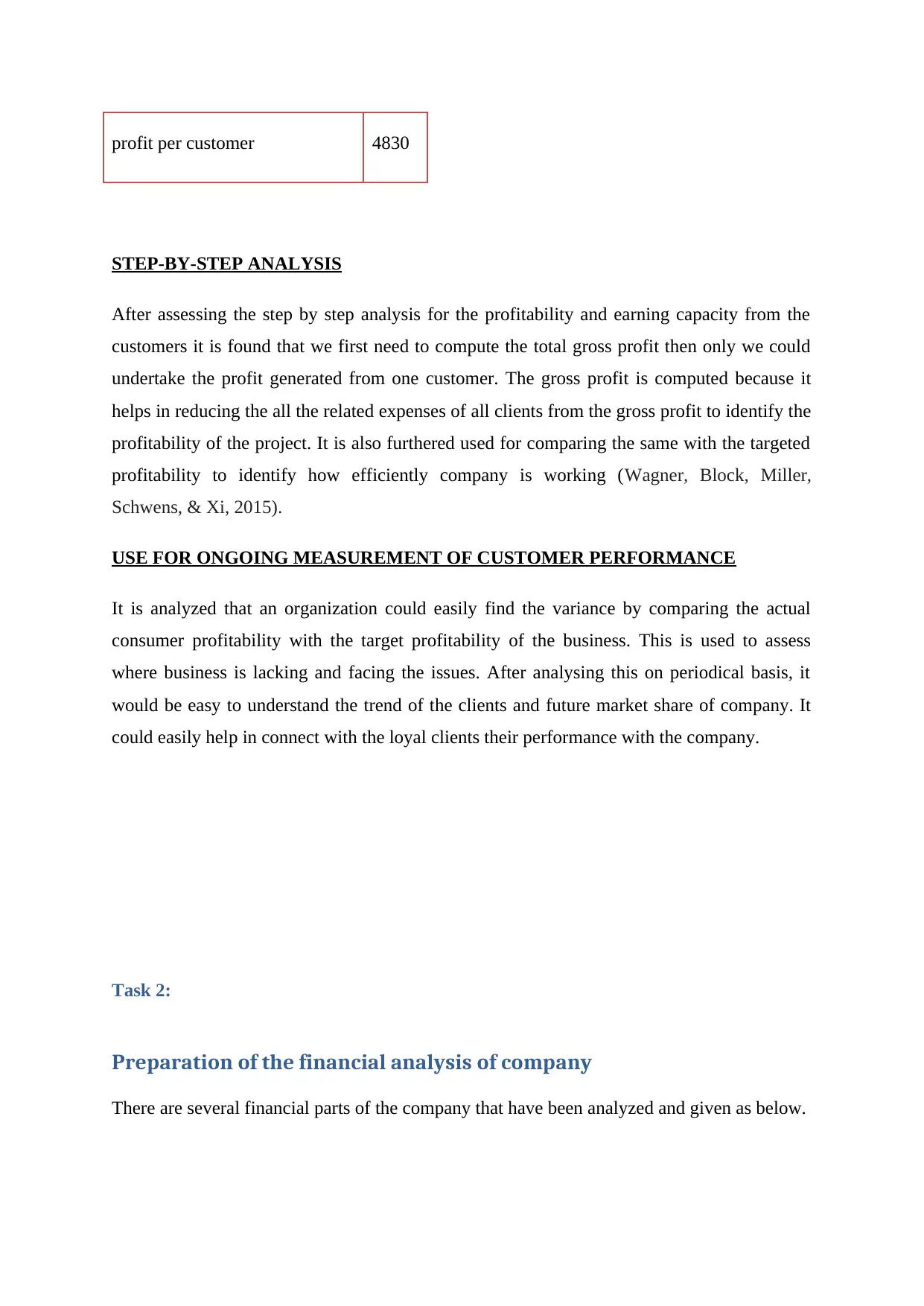

profit per customer 4830

STEP-BY-STEP ANALYSIS

After assessing the step by step analysis for the profitability and earning capacity from the

customers it is found that we first need to compute the total gross profit then only we could

undertake the profit generated from one customer. The gross profit is computed because it

helps in reducing the all the related expenses of all clients from the gross profit to identify the

profitability of the project. It is also furthered used for comparing the same with the targeted

profitability to identify how efficiently company is working (Wagner, Block, Miller,

Schwens, & Xi, 2015).

USE FOR ONGOING MEASUREMENT OF CUSTOMER PERFORMANCE

It is analyzed that an organization could easily find the variance by comparing the actual

consumer profitability with the target profitability of the business. This is used to assess

where business is lacking and facing the issues. After analysing this on periodical basis, it

would be easy to understand the trend of the clients and future market share of company. It

could easily help in connect with the loyal clients their performance with the company.

Task 2:

Preparation of the financial analysis of company

There are several financial parts of the company that have been analyzed and given as below.

STEP-BY-STEP ANALYSIS

After assessing the step by step analysis for the profitability and earning capacity from the

customers it is found that we first need to compute the total gross profit then only we could

undertake the profit generated from one customer. The gross profit is computed because it

helps in reducing the all the related expenses of all clients from the gross profit to identify the

profitability of the project. It is also furthered used for comparing the same with the targeted

profitability to identify how efficiently company is working (Wagner, Block, Miller,

Schwens, & Xi, 2015).

USE FOR ONGOING MEASUREMENT OF CUSTOMER PERFORMANCE

It is analyzed that an organization could easily find the variance by comparing the actual

consumer profitability with the target profitability of the business. This is used to assess

where business is lacking and facing the issues. After analysing this on periodical basis, it

would be easy to understand the trend of the clients and future market share of company. It

could easily help in connect with the loyal clients their performance with the company.

Task 2:

Preparation of the financial analysis of company

There are several financial parts of the company that have been analyzed and given as below.

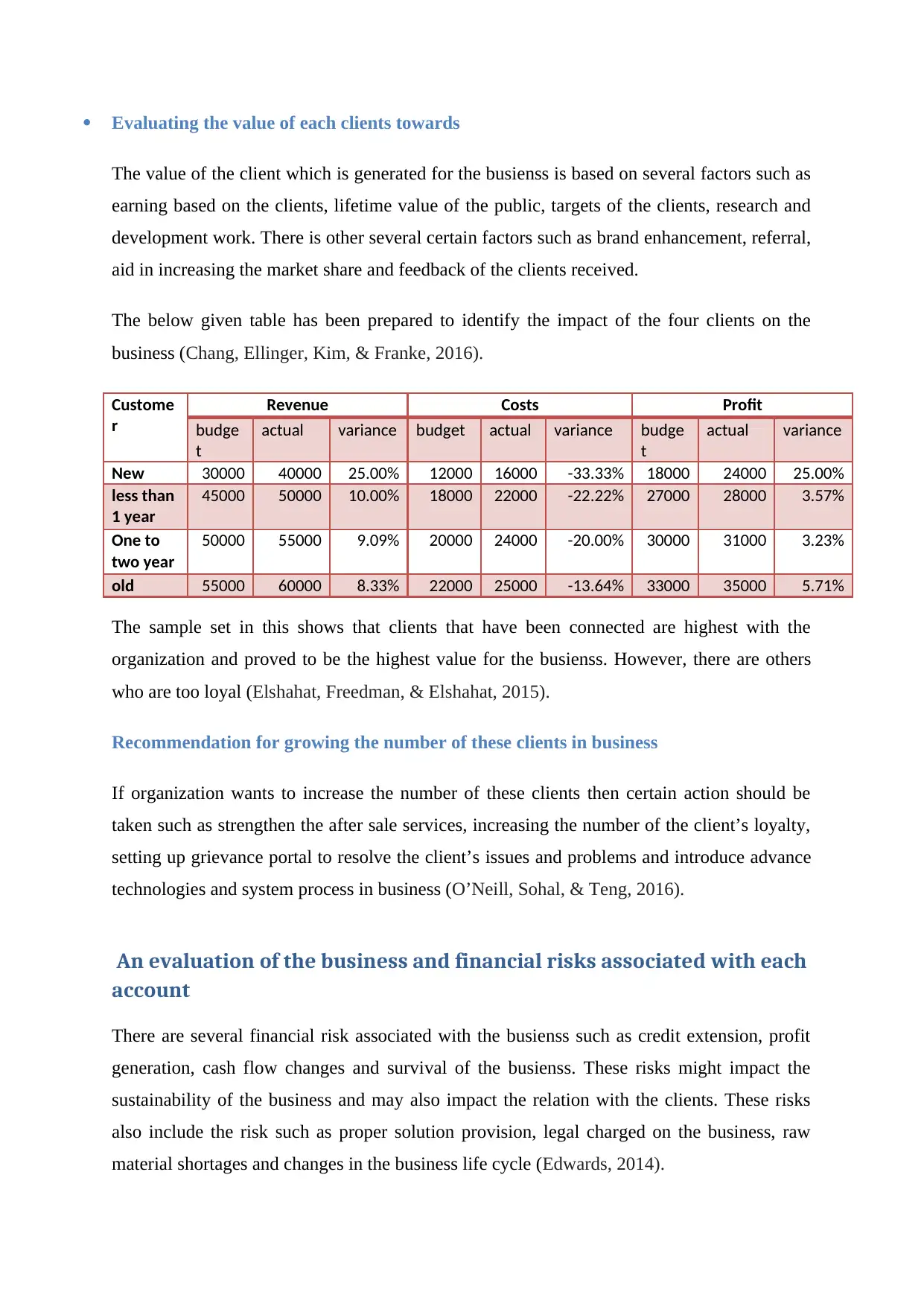

Evaluating the value of each clients towards

The value of the client which is generated for the busienss is based on several factors such as

earning based on the clients, lifetime value of the public, targets of the clients, research and

development work. There is other several certain factors such as brand enhancement, referral,

aid in increasing the market share and feedback of the clients received.

The below given table has been prepared to identify the impact of the four clients on the

business (Chang, Ellinger, Kim, & Franke, 2016).

Custome

r

Revenue Costs Profit

budge

t

actual variance budget actual variance budge

t

actual variance

New 30000 40000 25.00% 12000 16000 -33.33% 18000 24000 25.00%

less than

1 year

45000 50000 10.00% 18000 22000 -22.22% 27000 28000 3.57%

One to

two year

50000 55000 9.09% 20000 24000 -20.00% 30000 31000 3.23%

old 55000 60000 8.33% 22000 25000 -13.64% 33000 35000 5.71%

The sample set in this shows that clients that have been connected are highest with the

organization and proved to be the highest value for the busienss. However, there are others

who are too loyal (Elshahat, Freedman, & Elshahat, 2015).

Recommendation for growing the number of these clients in business

If organization wants to increase the number of these clients then certain action should be

taken such as strengthen the after sale services, increasing the number of the client’s loyalty,

setting up grievance portal to resolve the client’s issues and problems and introduce advance

technologies and system process in business (O’Neill, Sohal, & Teng, 2016).

An evaluation of the business and financial risks associated with each

account

There are several financial risk associated with the busienss such as credit extension, profit

generation, cash flow changes and survival of the busienss. These risks might impact the

sustainability of the business and may also impact the relation with the clients. These risks

also include the risk such as proper solution provision, legal charged on the business, raw

material shortages and changes in the business life cycle (Edwards, 2014).

The value of the client which is generated for the busienss is based on several factors such as

earning based on the clients, lifetime value of the public, targets of the clients, research and

development work. There is other several certain factors such as brand enhancement, referral,

aid in increasing the market share and feedback of the clients received.

The below given table has been prepared to identify the impact of the four clients on the

business (Chang, Ellinger, Kim, & Franke, 2016).

Custome

r

Revenue Costs Profit

budge

t

actual variance budget actual variance budge

t

actual variance

New 30000 40000 25.00% 12000 16000 -33.33% 18000 24000 25.00%

less than

1 year

45000 50000 10.00% 18000 22000 -22.22% 27000 28000 3.57%

One to

two year

50000 55000 9.09% 20000 24000 -20.00% 30000 31000 3.23%

old 55000 60000 8.33% 22000 25000 -13.64% 33000 35000 5.71%

The sample set in this shows that clients that have been connected are highest with the

organization and proved to be the highest value for the busienss. However, there are others

who are too loyal (Elshahat, Freedman, & Elshahat, 2015).

Recommendation for growing the number of these clients in business

If organization wants to increase the number of these clients then certain action should be

taken such as strengthen the after sale services, increasing the number of the client’s loyalty,

setting up grievance portal to resolve the client’s issues and problems and introduce advance

technologies and system process in business (O’Neill, Sohal, & Teng, 2016).

An evaluation of the business and financial risks associated with each

account

There are several financial risk associated with the busienss such as credit extension, profit

generation, cash flow changes and survival of the busienss. These risks might impact the

sustainability of the business and may also impact the relation with the clients. These risks

also include the risk such as proper solution provision, legal charged on the business, raw

material shortages and changes in the business life cycle (Edwards, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

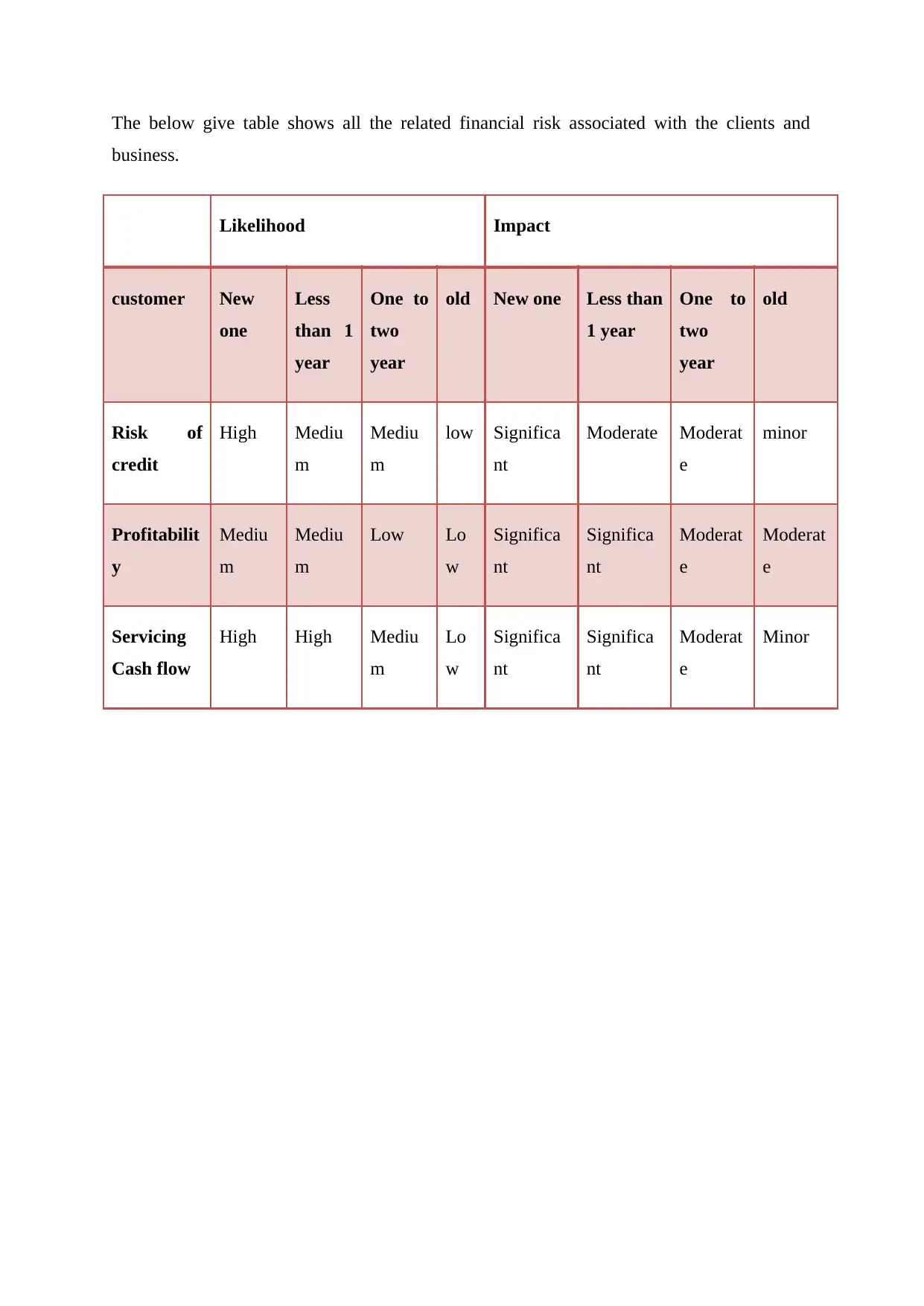

The below give table shows all the related financial risk associated with the clients and

business.

Likelihood Impact

customer New

one

Less

than 1

year

One to

two

year

old New one Less than

1 year

One to

two

year

old

Risk of

credit

High Mediu

m

Mediu

m

low Significa

nt

Moderate Moderat

e

minor

Profitabilit

y

Mediu

m

Mediu

m

Low Lo

w

Significa

nt

Significa

nt

Moderat

e

Moderat

e

Servicing

Cash flow

High High Mediu

m

Lo

w

Significa

nt

Significa

nt

Moderat

e

Minor

business.

Likelihood Impact

customer New

one

Less

than 1

year

One to

two

year

old New one Less than

1 year

One to

two

year

old

Risk of

credit

High Mediu

m

Mediu

m

low Significa

nt

Moderate Moderat

e

minor

Profitabilit

y

Mediu

m

Mediu

m

Low Lo

w

Significa

nt

Significa

nt

Moderat

e

Moderat

e

Servicing

Cash flow

High High Mediu

m

Lo

w

Significa

nt

Significa

nt

Moderat

e

Minor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

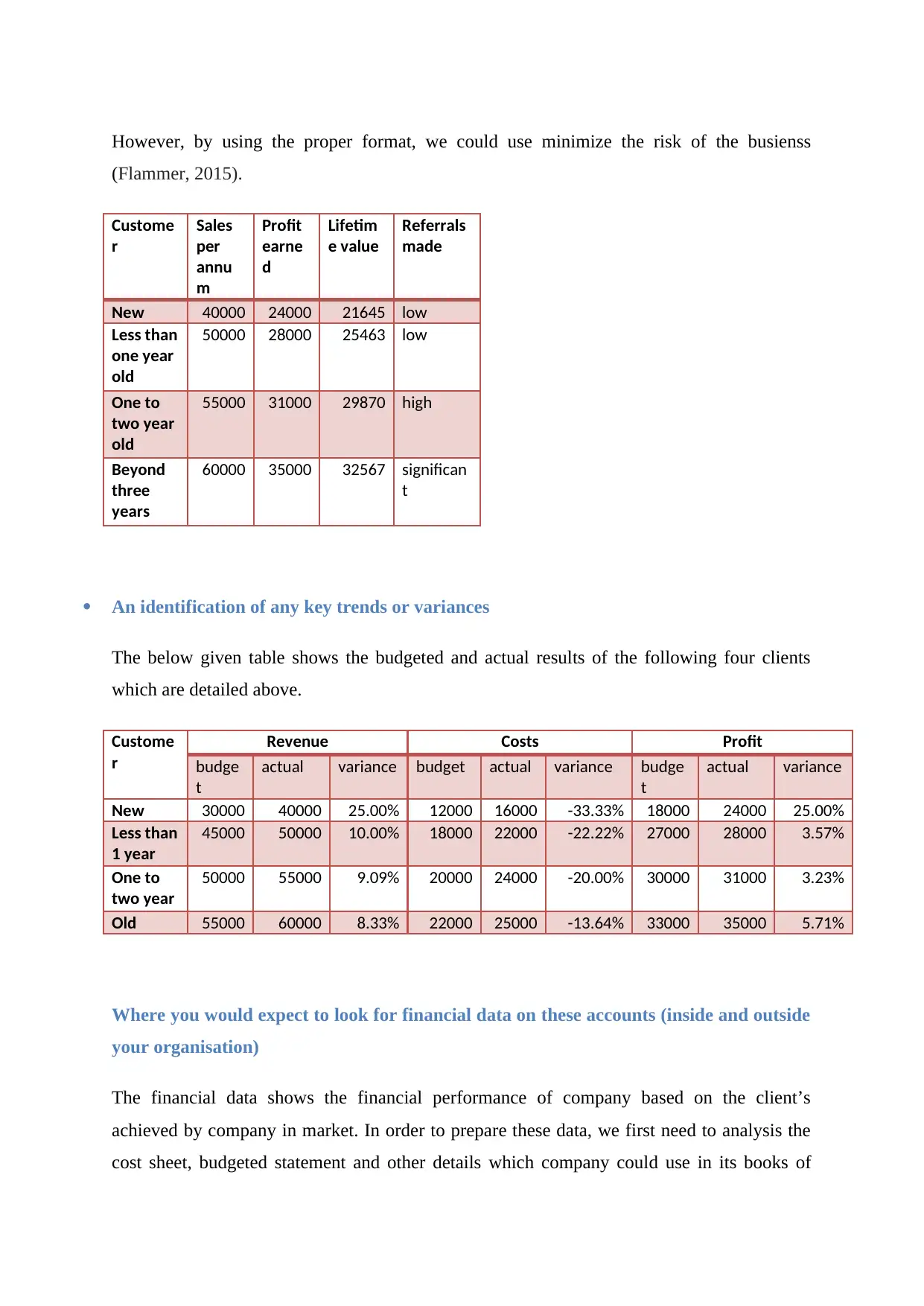

However, by using the proper format, we could use minimize the risk of the busienss

(Flammer, 2015).

Custome

r

Sales

per

annu

m

Profit

earne

d

Lifetim

e value

Referrals

made

New 40000 24000 21645 low

Less than

one year

old

50000 28000 25463 low

One to

two year

old

55000 31000 29870 high

Beyond

three

years

60000 35000 32567 significan

t

An identification of any key trends or variances

The below given table shows the budgeted and actual results of the following four clients

which are detailed above.

Custome

r

Revenue Costs Profit

budge

t

actual variance budget actual variance budge

t

actual variance

New 30000 40000 25.00% 12000 16000 -33.33% 18000 24000 25.00%

Less than

1 year

45000 50000 10.00% 18000 22000 -22.22% 27000 28000 3.57%

One to

two year

50000 55000 9.09% 20000 24000 -20.00% 30000 31000 3.23%

Old 55000 60000 8.33% 22000 25000 -13.64% 33000 35000 5.71%

Where you would expect to look for financial data on these accounts (inside and outside

your organisation)

The financial data shows the financial performance of company based on the client’s

achieved by company in market. In order to prepare these data, we first need to analysis the

cost sheet, budgeted statement and other details which company could use in its books of

(Flammer, 2015).

Custome

r

Sales

per

annu

m

Profit

earne

d

Lifetim

e value

Referrals

made

New 40000 24000 21645 low

Less than

one year

old

50000 28000 25463 low

One to

two year

old

55000 31000 29870 high

Beyond

three

years

60000 35000 32567 significan

t

An identification of any key trends or variances

The below given table shows the budgeted and actual results of the following four clients

which are detailed above.

Custome

r

Revenue Costs Profit

budge

t

actual variance budget actual variance budge

t

actual variance

New 30000 40000 25.00% 12000 16000 -33.33% 18000 24000 25.00%

Less than

1 year

45000 50000 10.00% 18000 22000 -22.22% 27000 28000 3.57%

One to

two year

50000 55000 9.09% 20000 24000 -20.00% 30000 31000 3.23%

Old 55000 60000 8.33% 22000 25000 -13.64% 33000 35000 5.71%

Where you would expect to look for financial data on these accounts (inside and outside

your organisation)

The financial data shows the financial performance of company based on the client’s

achieved by company in market. In order to prepare these data, we first need to analysis the

cost sheet, budgeted statement and other details which company could use in its books of

accounts. In addition to this, loyalty card approach could also be used to strengthen the

financial data performance of company (Lu, Chau, Wang, & Pan, 2014).

An identification of who else in your organisation would have a stake in the financial

viability and performance of these accounts and how you would ensure appropriate

access to the data

In organization there are several people who has stake in organization such as senior sales

manager, clients, financial managers, department head managers and other person who have

stake in the financial viability and performance of company. Company should keep its data

more revealed to its stakeholder by focusing on harmonized reporting frameworks. Every

interested stakeholder should be disclosed relevant information. Company will hold proper

meeting to disclose the required information and strengthen its financial reporting

frameworks. E-mail and direct communication should be properly followed by company to

strengthen the proper disclosing financial performance of company (Qiu, Shaukat, &

Tharyan, 2016).

A provision of any proformas for capturing performance and financial data about these

accounts and the development of contingency plans for possible problems that may

arise with the financial performance of the accounts

There should be proper format in which all the required data must be properly recorded as per

the applicable rules and regulation of the corporate governance mechanism. There should be

proper contingency plans which must be prepared before holding meeting so that possible

problems and issues could be mitigated. Proper plans must be prepared based on the market

internal and external factors which will helps in strategic implication.

For instance, if the employee’s turnover of the company increases then company should

strengthen its hiring process to maintain the effective management (Abdel-Maksoud,

Cerbioni, Omran, & Ricceri, 2015).

financial data performance of company (Lu, Chau, Wang, & Pan, 2014).

An identification of who else in your organisation would have a stake in the financial

viability and performance of these accounts and how you would ensure appropriate

access to the data

In organization there are several people who has stake in organization such as senior sales

manager, clients, financial managers, department head managers and other person who have

stake in the financial viability and performance of company. Company should keep its data

more revealed to its stakeholder by focusing on harmonized reporting frameworks. Every

interested stakeholder should be disclosed relevant information. Company will hold proper

meeting to disclose the required information and strengthen its financial reporting

frameworks. E-mail and direct communication should be properly followed by company to

strengthen the proper disclosing financial performance of company (Qiu, Shaukat, &

Tharyan, 2016).

A provision of any proformas for capturing performance and financial data about these

accounts and the development of contingency plans for possible problems that may

arise with the financial performance of the accounts

There should be proper format in which all the required data must be properly recorded as per

the applicable rules and regulation of the corporate governance mechanism. There should be

proper contingency plans which must be prepared before holding meeting so that possible

problems and issues could be mitigated. Proper plans must be prepared based on the market

internal and external factors which will helps in strategic implication.

For instance, if the employee’s turnover of the company increases then company should

strengthen its hiring process to maintain the effective management (Abdel-Maksoud,

Cerbioni, Omran, & Ricceri, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.