Financial Decision Making: A Report on Hi-Tech PLC Analysis

VerifiedAdded on 2021/06/15

|22

|4867

|43

Report

AI Summary

This report presents a comprehensive financial analysis of Hi-Tech PLC, a UK-based company in the computer hardware and accessories industry. The analysis is divided into two parts: the first part focuses on the company's business performance, examining its income statement and balance sheet through various financial ratios such as profitability, efficiency, liquidity, and gearing ratios. Cash flow and product line analyses are also included. The second part delves into investment appraisal techniques used to evaluate Hi-Tech PLC's expansion project, including management forecasts and methods like payback period, accounting rate of return, and net present value. The report also discusses sources of finance and non-financial factors influencing the company's decisions. The analysis reveals insights into Hi-Tech PLC's financial health, operational efficiency, and investment strategies.

RUNNING HEAD: FINANCIAL DECISION MAKING

financial analysis

Hi-Tech PLC

financial analysis

Hi-Tech PLC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial decision making 1

Executive summary

This report contains a brief financial analysis of Hi-Tech PLC, a company that operates in United

Kingdom and deals with the manufacturing of computer hardware and accessories. It was

founded in 1980 and is now a multi-national company in UK. The first part of the report deals

with the analysis of company’s income statement and balance sheet with help of some specific

ratios. In addition to this, cash flow analysis and production analysis is also done which reflects

the financial position of Hi-Tech in the market.

The second part of the report contains investment appraisal techniques used for evaluating the

expansion project of Hi-Tech PLC. A management forecast is been done and various appraisal

methods are been used. The methods include payback, accounting rate of return and net present

value method. Along with this, various sources of finance and non financial factors are also

discussed in the later part of the report. Overall, the report presents the business analysis and

investment analysis of Hi-Tech PLC and its expansion strategy.

Executive summary

This report contains a brief financial analysis of Hi-Tech PLC, a company that operates in United

Kingdom and deals with the manufacturing of computer hardware and accessories. It was

founded in 1980 and is now a multi-national company in UK. The first part of the report deals

with the analysis of company’s income statement and balance sheet with help of some specific

ratios. In addition to this, cash flow analysis and production analysis is also done which reflects

the financial position of Hi-Tech in the market.

The second part of the report contains investment appraisal techniques used for evaluating the

expansion project of Hi-Tech PLC. A management forecast is been done and various appraisal

methods are been used. The methods include payback, accounting rate of return and net present

value method. Along with this, various sources of finance and non financial factors are also

discussed in the later part of the report. Overall, the report presents the business analysis and

investment analysis of Hi-Tech PLC and its expansion strategy.

Financial decision making 2

Contents

Part 1 Business Performance Analysis........................................................................................................4

Statement of profit and loss analysis...........................................................................................................4

Analysis of sales......................................................................................................................................4

Profitability ratios....................................................................................................................................4

Gross profit ratio..................................................................................................................................4

Net profit ratio.....................................................................................................................................5

Return on equity..................................................................................................................................6

Statement of financial position analysis......................................................................................................7

Efficiency ratios......................................................................................................................................7

Inventory turnover ratio.......................................................................................................................7

Inventory days.....................................................................................................................................7

Receivable turnover ratio.....................................................................................................................8

Receivable days...................................................................................................................................8

Creditor turnover ratio.........................................................................................................................9

Payables days....................................................................................................................................10

Asset turnover ratio...........................................................................................................................10

Liquidity ratios......................................................................................................................................11

Current ratio......................................................................................................................................11

Quick ratio.........................................................................................................................................12

Gearing ratios........................................................................................................................................12

Debt-to-equity ratio...........................................................................................................................12

Interest coverage ratio........................................................................................................................13

Statement of cash flow analysis.............................................................................................................14

Product Line Analysis...........................................................................................................................15

Part-2 Investment Appraisal......................................................................................................................16

Management forecast.............................................................................................................................16

Contents

Part 1 Business Performance Analysis........................................................................................................4

Statement of profit and loss analysis...........................................................................................................4

Analysis of sales......................................................................................................................................4

Profitability ratios....................................................................................................................................4

Gross profit ratio..................................................................................................................................4

Net profit ratio.....................................................................................................................................5

Return on equity..................................................................................................................................6

Statement of financial position analysis......................................................................................................7

Efficiency ratios......................................................................................................................................7

Inventory turnover ratio.......................................................................................................................7

Inventory days.....................................................................................................................................7

Receivable turnover ratio.....................................................................................................................8

Receivable days...................................................................................................................................8

Creditor turnover ratio.........................................................................................................................9

Payables days....................................................................................................................................10

Asset turnover ratio...........................................................................................................................10

Liquidity ratios......................................................................................................................................11

Current ratio......................................................................................................................................11

Quick ratio.........................................................................................................................................12

Gearing ratios........................................................................................................................................12

Debt-to-equity ratio...........................................................................................................................12

Interest coverage ratio........................................................................................................................13

Statement of cash flow analysis.............................................................................................................14

Product Line Analysis...........................................................................................................................15

Part-2 Investment Appraisal......................................................................................................................16

Management forecast.............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial decision making 3

Appraisal Techniques............................................................................................................................17

Payback period..................................................................................................................................17

Accounting rate of return...................................................................................................................17

Net Present Value..............................................................................................................................18

Sources of Finance................................................................................................................................18

Non-Financial factors............................................................................................................................19

References.................................................................................................................................................20

Appraisal Techniques............................................................................................................................17

Payback period..................................................................................................................................17

Accounting rate of return...................................................................................................................17

Net Present Value..............................................................................................................................18

Sources of Finance................................................................................................................................18

Non-Financial factors............................................................................................................................19

References.................................................................................................................................................20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial decision making 4

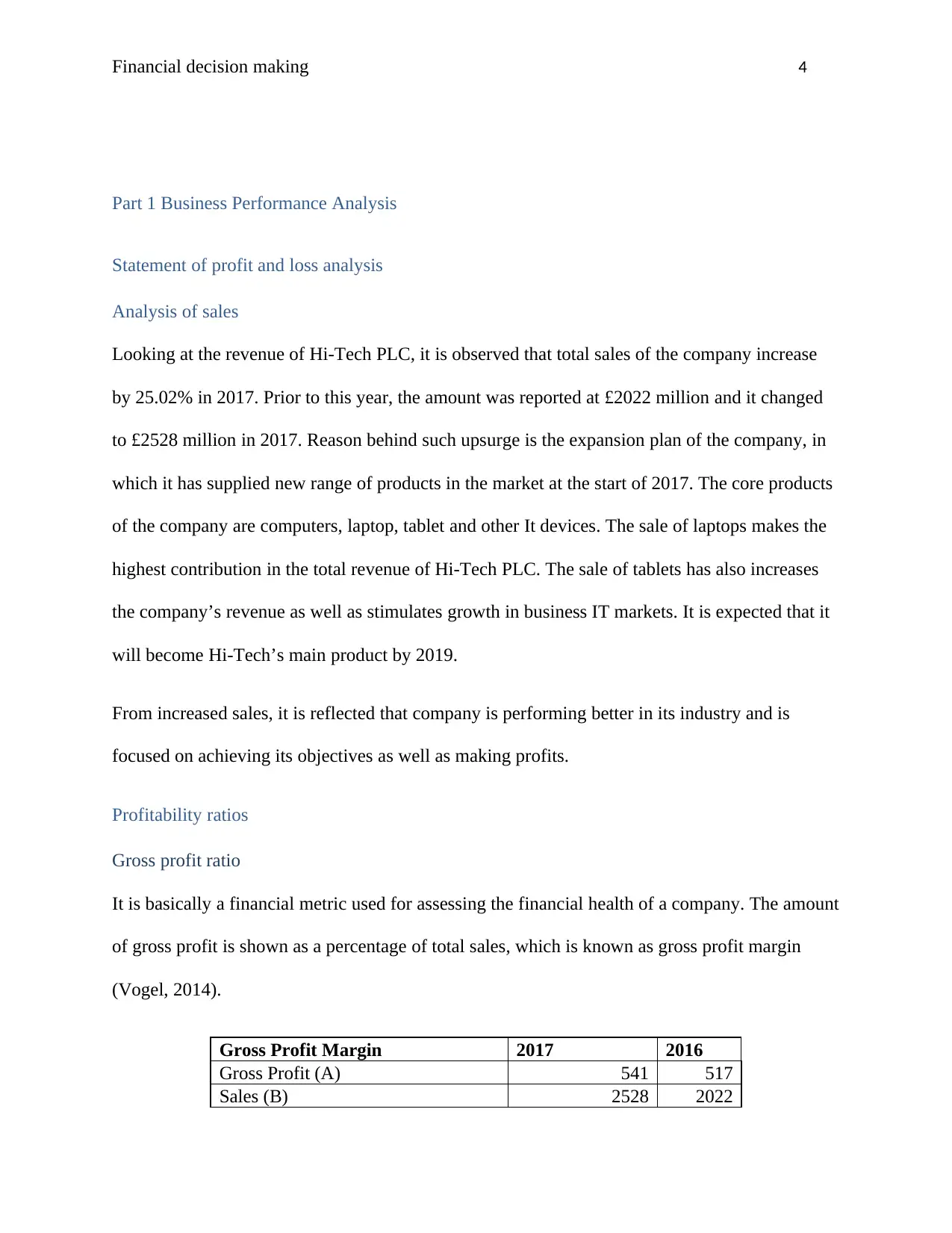

Part 1 Business Performance Analysis

Statement of profit and loss analysis

Analysis of sales

Looking at the revenue of Hi-Tech PLC, it is observed that total sales of the company increase

by 25.02% in 2017. Prior to this year, the amount was reported at £2022 million and it changed

to £2528 million in 2017. Reason behind such upsurge is the expansion plan of the company, in

which it has supplied new range of products in the market at the start of 2017. The core products

of the company are computers, laptop, tablet and other It devices. The sale of laptops makes the

highest contribution in the total revenue of Hi-Tech PLC. The sale of tablets has also increases

the company’s revenue as well as stimulates growth in business IT markets. It is expected that it

will become Hi-Tech’s main product by 2019.

From increased sales, it is reflected that company is performing better in its industry and is

focused on achieving its objectives as well as making profits.

Profitability ratios

Gross profit ratio

It is basically a financial metric used for assessing the financial health of a company. The amount

of gross profit is shown as a percentage of total sales, which is known as gross profit margin

(Vogel, 2014).

Gross Profit Margin 2017 2016

Gross Profit (A) 541 517

Sales (B) 2528 2022

Part 1 Business Performance Analysis

Statement of profit and loss analysis

Analysis of sales

Looking at the revenue of Hi-Tech PLC, it is observed that total sales of the company increase

by 25.02% in 2017. Prior to this year, the amount was reported at £2022 million and it changed

to £2528 million in 2017. Reason behind such upsurge is the expansion plan of the company, in

which it has supplied new range of products in the market at the start of 2017. The core products

of the company are computers, laptop, tablet and other It devices. The sale of laptops makes the

highest contribution in the total revenue of Hi-Tech PLC. The sale of tablets has also increases

the company’s revenue as well as stimulates growth in business IT markets. It is expected that it

will become Hi-Tech’s main product by 2019.

From increased sales, it is reflected that company is performing better in its industry and is

focused on achieving its objectives as well as making profits.

Profitability ratios

Gross profit ratio

It is basically a financial metric used for assessing the financial health of a company. The amount

of gross profit is shown as a percentage of total sales, which is known as gross profit margin

(Vogel, 2014).

Gross Profit Margin 2017 2016

Gross Profit (A) 541 517

Sales (B) 2528 2022

Financial decision making 5

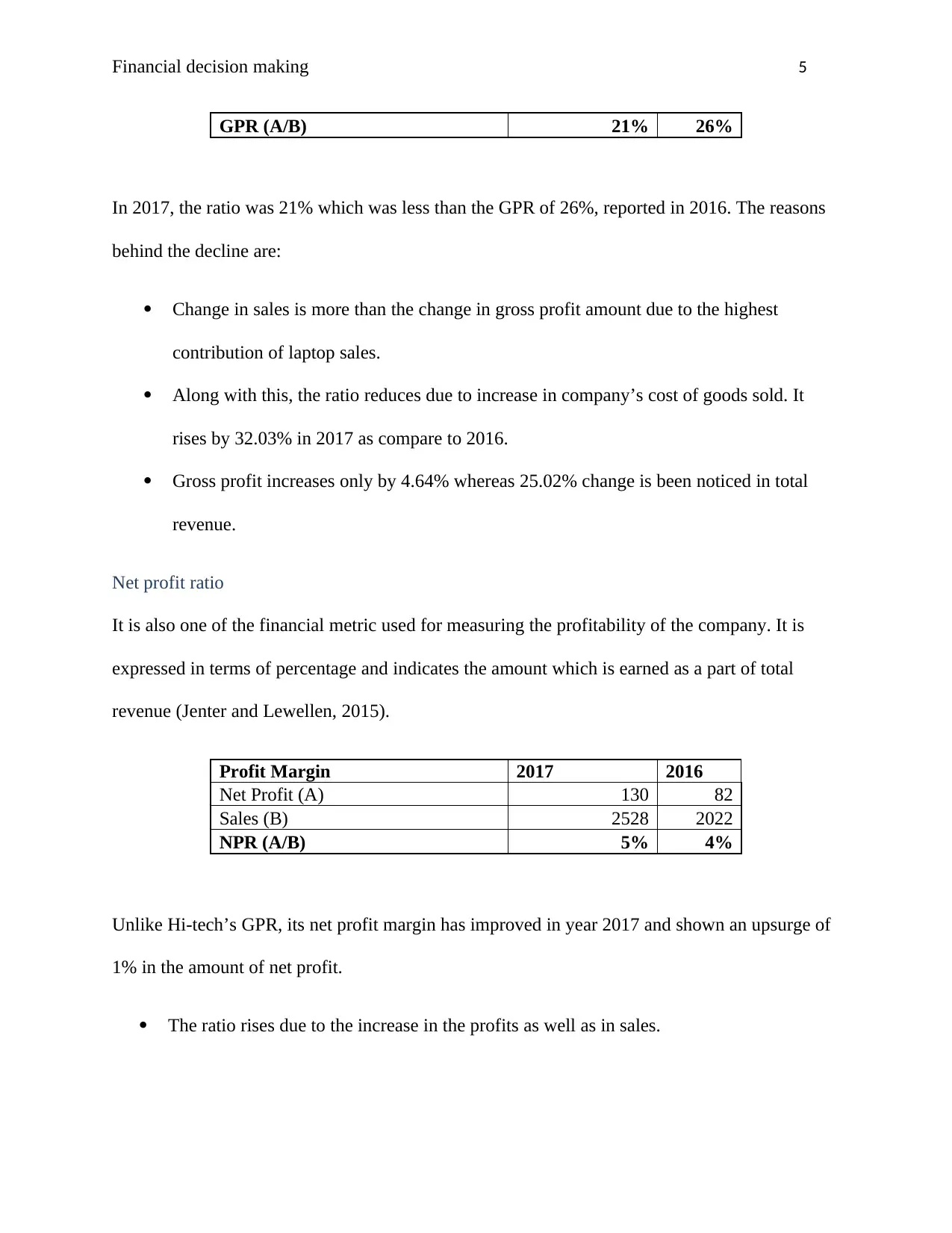

GPR (A/B) 21% 26%

In 2017, the ratio was 21% which was less than the GPR of 26%, reported in 2016. The reasons

behind the decline are:

Change in sales is more than the change in gross profit amount due to the highest

contribution of laptop sales.

Along with this, the ratio reduces due to increase in company’s cost of goods sold. It

rises by 32.03% in 2017 as compare to 2016.

Gross profit increases only by 4.64% whereas 25.02% change is been noticed in total

revenue.

Net profit ratio

It is also one of the financial metric used for measuring the profitability of the company. It is

expressed in terms of percentage and indicates the amount which is earned as a part of total

revenue (Jenter and Lewellen, 2015).

Profit Margin 2017 2016

Net Profit (A) 130 82

Sales (B) 2528 2022

NPR (A/B) 5% 4%

Unlike Hi-tech’s GPR, its net profit margin has improved in year 2017 and shown an upsurge of

1% in the amount of net profit.

The ratio rises due to the increase in the profits as well as in sales.

GPR (A/B) 21% 26%

In 2017, the ratio was 21% which was less than the GPR of 26%, reported in 2016. The reasons

behind the decline are:

Change in sales is more than the change in gross profit amount due to the highest

contribution of laptop sales.

Along with this, the ratio reduces due to increase in company’s cost of goods sold. It

rises by 32.03% in 2017 as compare to 2016.

Gross profit increases only by 4.64% whereas 25.02% change is been noticed in total

revenue.

Net profit ratio

It is also one of the financial metric used for measuring the profitability of the company. It is

expressed in terms of percentage and indicates the amount which is earned as a part of total

revenue (Jenter and Lewellen, 2015).

Profit Margin 2017 2016

Net Profit (A) 130 82

Sales (B) 2528 2022

NPR (A/B) 5% 4%

Unlike Hi-tech’s GPR, its net profit margin has improved in year 2017 and shown an upsurge of

1% in the amount of net profit.

The ratio rises due to the increase in the profits as well as in sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial decision making 6

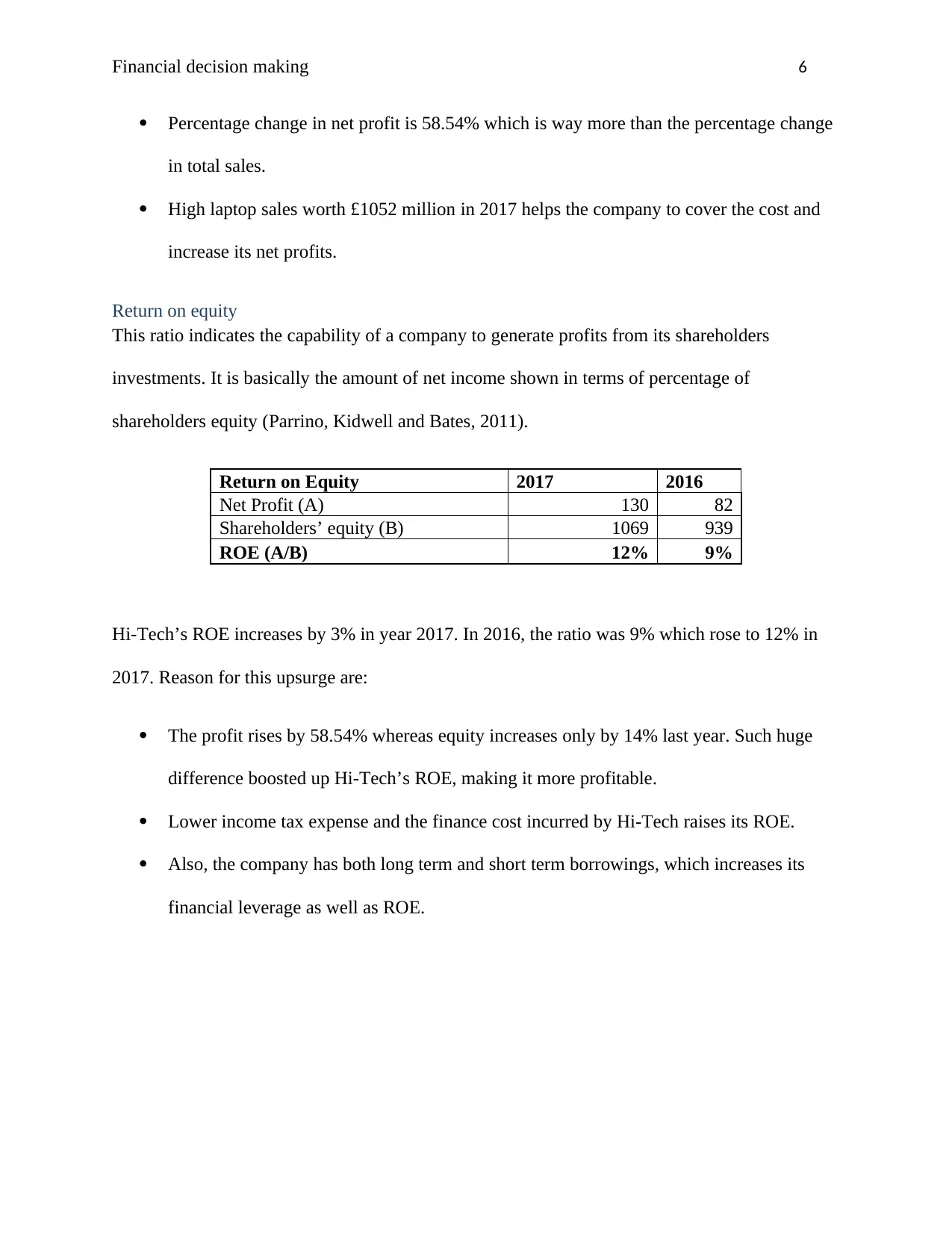

Percentage change in net profit is 58.54% which is way more than the percentage change

in total sales.

High laptop sales worth £1052 million in 2017 helps the company to cover the cost and

increase its net profits.

Return on equity

This ratio indicates the capability of a company to generate profits from its shareholders

investments. It is basically the amount of net income shown in terms of percentage of

shareholders equity (Parrino, Kidwell and Bates, 2011).

Return on Equity 2017 2016

Net Profit (A) 130 82

Shareholders’ equity (B) 1069 939

ROE (A/B) 12% 9%

Hi-Tech’s ROE increases by 3% in year 2017. In 2016, the ratio was 9% which rose to 12% in

2017. Reason for this upsurge are:

The profit rises by 58.54% whereas equity increases only by 14% last year. Such huge

difference boosted up Hi-Tech’s ROE, making it more profitable.

Lower income tax expense and the finance cost incurred by Hi-Tech raises its ROE.

Also, the company has both long term and short term borrowings, which increases its

financial leverage as well as ROE.

Percentage change in net profit is 58.54% which is way more than the percentage change

in total sales.

High laptop sales worth £1052 million in 2017 helps the company to cover the cost and

increase its net profits.

Return on equity

This ratio indicates the capability of a company to generate profits from its shareholders

investments. It is basically the amount of net income shown in terms of percentage of

shareholders equity (Parrino, Kidwell and Bates, 2011).

Return on Equity 2017 2016

Net Profit (A) 130 82

Shareholders’ equity (B) 1069 939

ROE (A/B) 12% 9%

Hi-Tech’s ROE increases by 3% in year 2017. In 2016, the ratio was 9% which rose to 12% in

2017. Reason for this upsurge are:

The profit rises by 58.54% whereas equity increases only by 14% last year. Such huge

difference boosted up Hi-Tech’s ROE, making it more profitable.

Lower income tax expense and the finance cost incurred by Hi-Tech raises its ROE.

Also, the company has both long term and short term borrowings, which increases its

financial leverage as well as ROE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial decision making 7

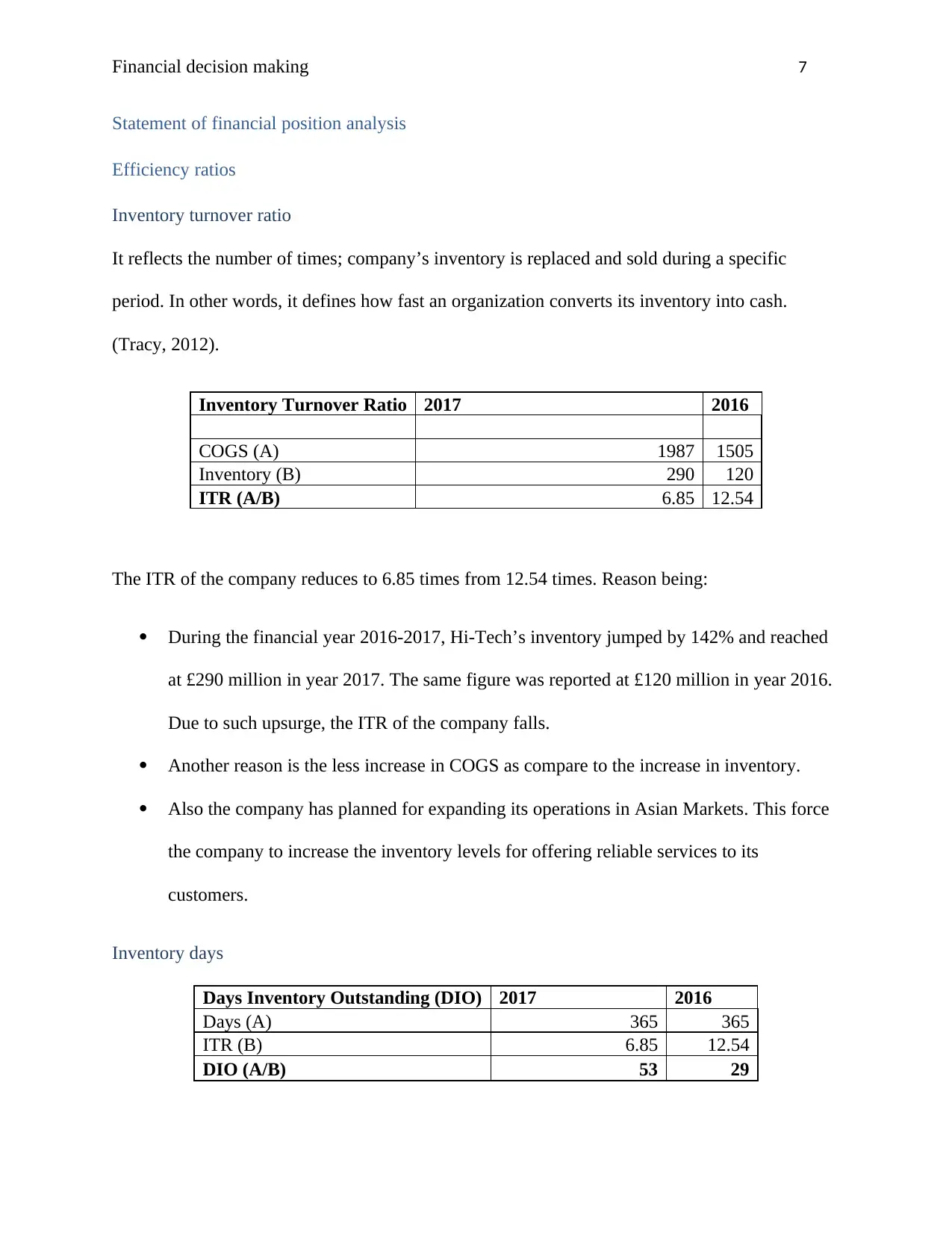

Statement of financial position analysis

Efficiency ratios

Inventory turnover ratio

It reflects the number of times; company’s inventory is replaced and sold during a specific

period. In other words, it defines how fast an organization converts its inventory into cash.

(Tracy, 2012).

Inventory Turnover Ratio 2017 2016

COGS (A) 1987 1505

Inventory (B) 290 120

ITR (A/B) 6.85 12.54

The ITR of the company reduces to 6.85 times from 12.54 times. Reason being:

During the financial year 2016-2017, Hi-Tech’s inventory jumped by 142% and reached

at £290 million in year 2017. The same figure was reported at £120 million in year 2016.

Due to such upsurge, the ITR of the company falls.

Another reason is the less increase in COGS as compare to the increase in inventory.

Also the company has planned for expanding its operations in Asian Markets. This force

the company to increase the inventory levels for offering reliable services to its

customers.

Inventory days

Days Inventory Outstanding (DIO) 2017 2016

Days (A) 365 365

ITR (B) 6.85 12.54

DIO (A/B) 53 29

Statement of financial position analysis

Efficiency ratios

Inventory turnover ratio

It reflects the number of times; company’s inventory is replaced and sold during a specific

period. In other words, it defines how fast an organization converts its inventory into cash.

(Tracy, 2012).

Inventory Turnover Ratio 2017 2016

COGS (A) 1987 1505

Inventory (B) 290 120

ITR (A/B) 6.85 12.54

The ITR of the company reduces to 6.85 times from 12.54 times. Reason being:

During the financial year 2016-2017, Hi-Tech’s inventory jumped by 142% and reached

at £290 million in year 2017. The same figure was reported at £120 million in year 2016.

Due to such upsurge, the ITR of the company falls.

Another reason is the less increase in COGS as compare to the increase in inventory.

Also the company has planned for expanding its operations in Asian Markets. This force

the company to increase the inventory levels for offering reliable services to its

customers.

Inventory days

Days Inventory Outstanding (DIO) 2017 2016

Days (A) 365 365

ITR (B) 6.85 12.54

DIO (A/B) 53 29

Financial decision making 8

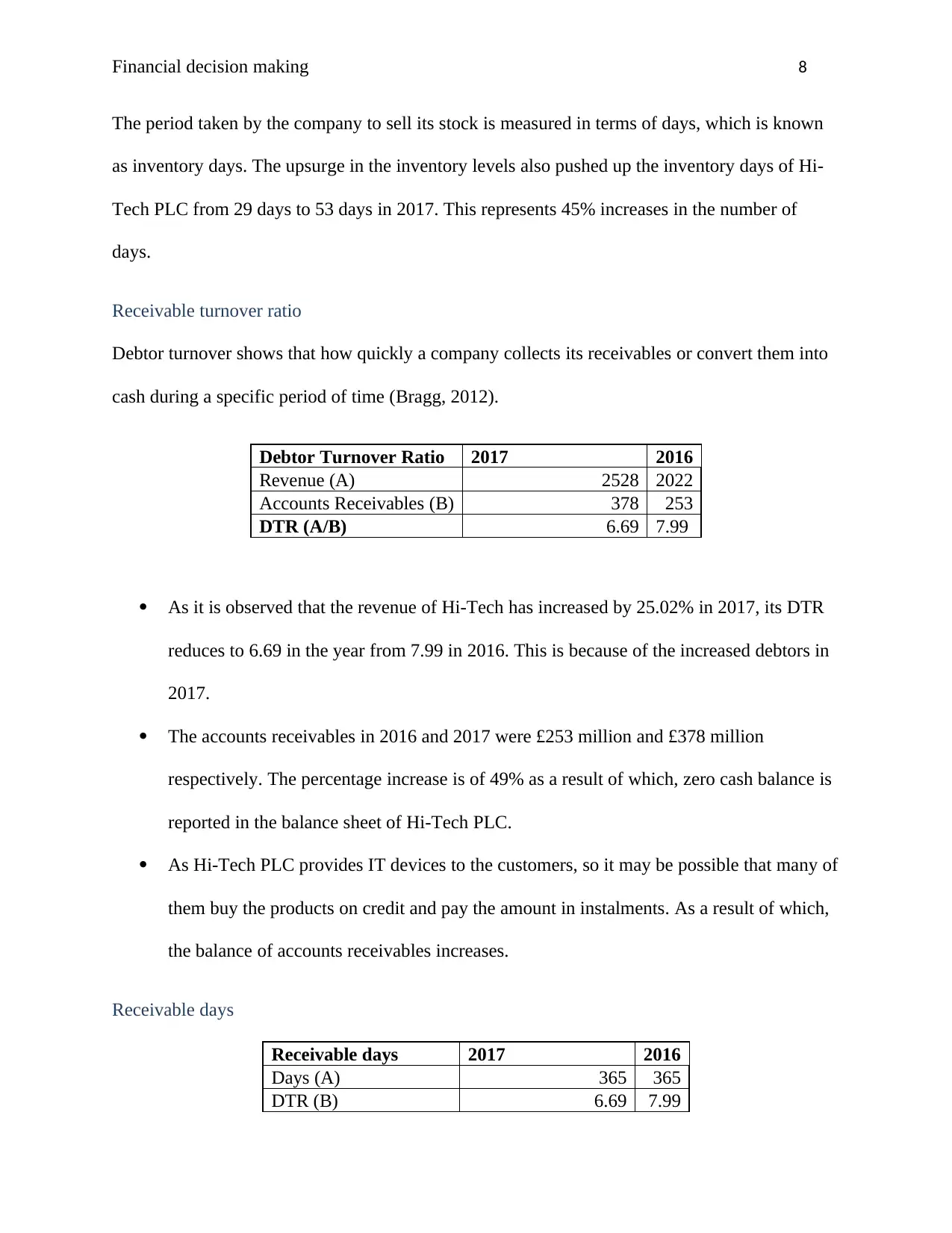

The period taken by the company to sell its stock is measured in terms of days, which is known

as inventory days. The upsurge in the inventory levels also pushed up the inventory days of Hi-

Tech PLC from 29 days to 53 days in 2017. This represents 45% increases in the number of

days.

Receivable turnover ratio

Debtor turnover shows that how quickly a company collects its receivables or convert them into

cash during a specific period of time (Bragg, 2012).

Debtor Turnover Ratio 2017 2016

Revenue (A) 2528 2022

Accounts Receivables (B) 378 253

DTR (A/B) 6.69 7.99

As it is observed that the revenue of Hi-Tech has increased by 25.02% in 2017, its DTR

reduces to 6.69 in the year from 7.99 in 2016. This is because of the increased debtors in

2017.

The accounts receivables in 2016 and 2017 were £253 million and £378 million

respectively. The percentage increase is of 49% as a result of which, zero cash balance is

reported in the balance sheet of Hi-Tech PLC.

As Hi-Tech PLC provides IT devices to the customers, so it may be possible that many of

them buy the products on credit and pay the amount in instalments. As a result of which,

the balance of accounts receivables increases.

Receivable days

Receivable days 2017 2016

Days (A) 365 365

DTR (B) 6.69 7.99

The period taken by the company to sell its stock is measured in terms of days, which is known

as inventory days. The upsurge in the inventory levels also pushed up the inventory days of Hi-

Tech PLC from 29 days to 53 days in 2017. This represents 45% increases in the number of

days.

Receivable turnover ratio

Debtor turnover shows that how quickly a company collects its receivables or convert them into

cash during a specific period of time (Bragg, 2012).

Debtor Turnover Ratio 2017 2016

Revenue (A) 2528 2022

Accounts Receivables (B) 378 253

DTR (A/B) 6.69 7.99

As it is observed that the revenue of Hi-Tech has increased by 25.02% in 2017, its DTR

reduces to 6.69 in the year from 7.99 in 2016. This is because of the increased debtors in

2017.

The accounts receivables in 2016 and 2017 were £253 million and £378 million

respectively. The percentage increase is of 49% as a result of which, zero cash balance is

reported in the balance sheet of Hi-Tech PLC.

As Hi-Tech PLC provides IT devices to the customers, so it may be possible that many of

them buy the products on credit and pay the amount in instalments. As a result of which,

the balance of accounts receivables increases.

Receivable days

Receivable days 2017 2016

Days (A) 365 365

DTR (B) 6.69 7.99

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial decision making 9

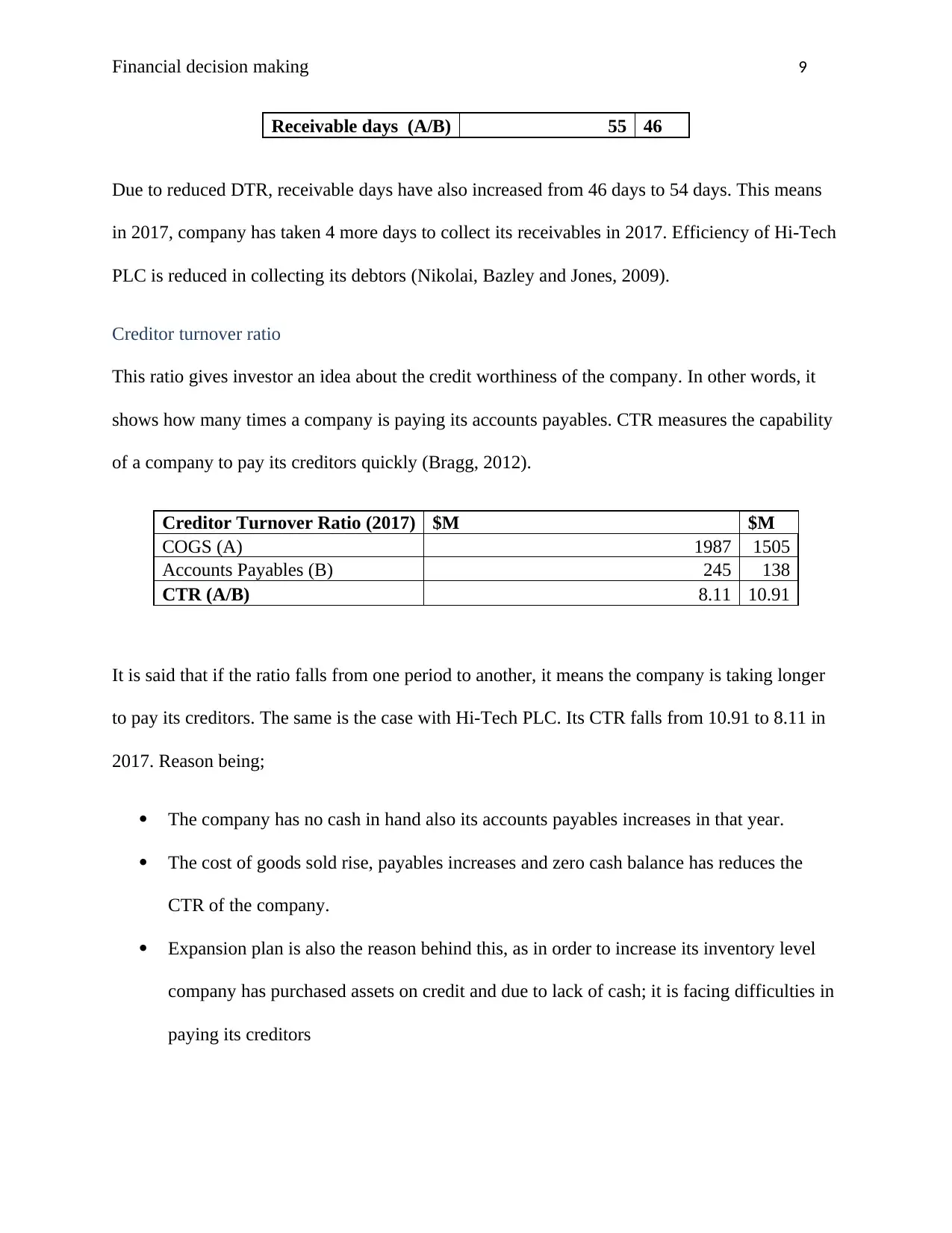

Receivable days (A/B) 55 46

Due to reduced DTR, receivable days have also increased from 46 days to 54 days. This means

in 2017, company has taken 4 more days to collect its receivables in 2017. Efficiency of Hi-Tech

PLC is reduced in collecting its debtors (Nikolai, Bazley and Jones, 2009).

Creditor turnover ratio

This ratio gives investor an idea about the credit worthiness of the company. In other words, it

shows how many times a company is paying its accounts payables. CTR measures the capability

of a company to pay its creditors quickly (Bragg, 2012).

Creditor Turnover Ratio (2017) $M $M

COGS (A) 1987 1505

Accounts Payables (B) 245 138

CTR (A/B) 8.11 10.91

It is said that if the ratio falls from one period to another, it means the company is taking longer

to pay its creditors. The same is the case with Hi-Tech PLC. Its CTR falls from 10.91 to 8.11 in

2017. Reason being;

The company has no cash in hand also its accounts payables increases in that year.

The cost of goods sold rise, payables increases and zero cash balance has reduces the

CTR of the company.

Expansion plan is also the reason behind this, as in order to increase its inventory level

company has purchased assets on credit and due to lack of cash; it is facing difficulties in

paying its creditors

Receivable days (A/B) 55 46

Due to reduced DTR, receivable days have also increased from 46 days to 54 days. This means

in 2017, company has taken 4 more days to collect its receivables in 2017. Efficiency of Hi-Tech

PLC is reduced in collecting its debtors (Nikolai, Bazley and Jones, 2009).

Creditor turnover ratio

This ratio gives investor an idea about the credit worthiness of the company. In other words, it

shows how many times a company is paying its accounts payables. CTR measures the capability

of a company to pay its creditors quickly (Bragg, 2012).

Creditor Turnover Ratio (2017) $M $M

COGS (A) 1987 1505

Accounts Payables (B) 245 138

CTR (A/B) 8.11 10.91

It is said that if the ratio falls from one period to another, it means the company is taking longer

to pay its creditors. The same is the case with Hi-Tech PLC. Its CTR falls from 10.91 to 8.11 in

2017. Reason being;

The company has no cash in hand also its accounts payables increases in that year.

The cost of goods sold rise, payables increases and zero cash balance has reduces the

CTR of the company.

Expansion plan is also the reason behind this, as in order to increase its inventory level

company has purchased assets on credit and due to lack of cash; it is facing difficulties in

paying its creditors

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial decision making 10

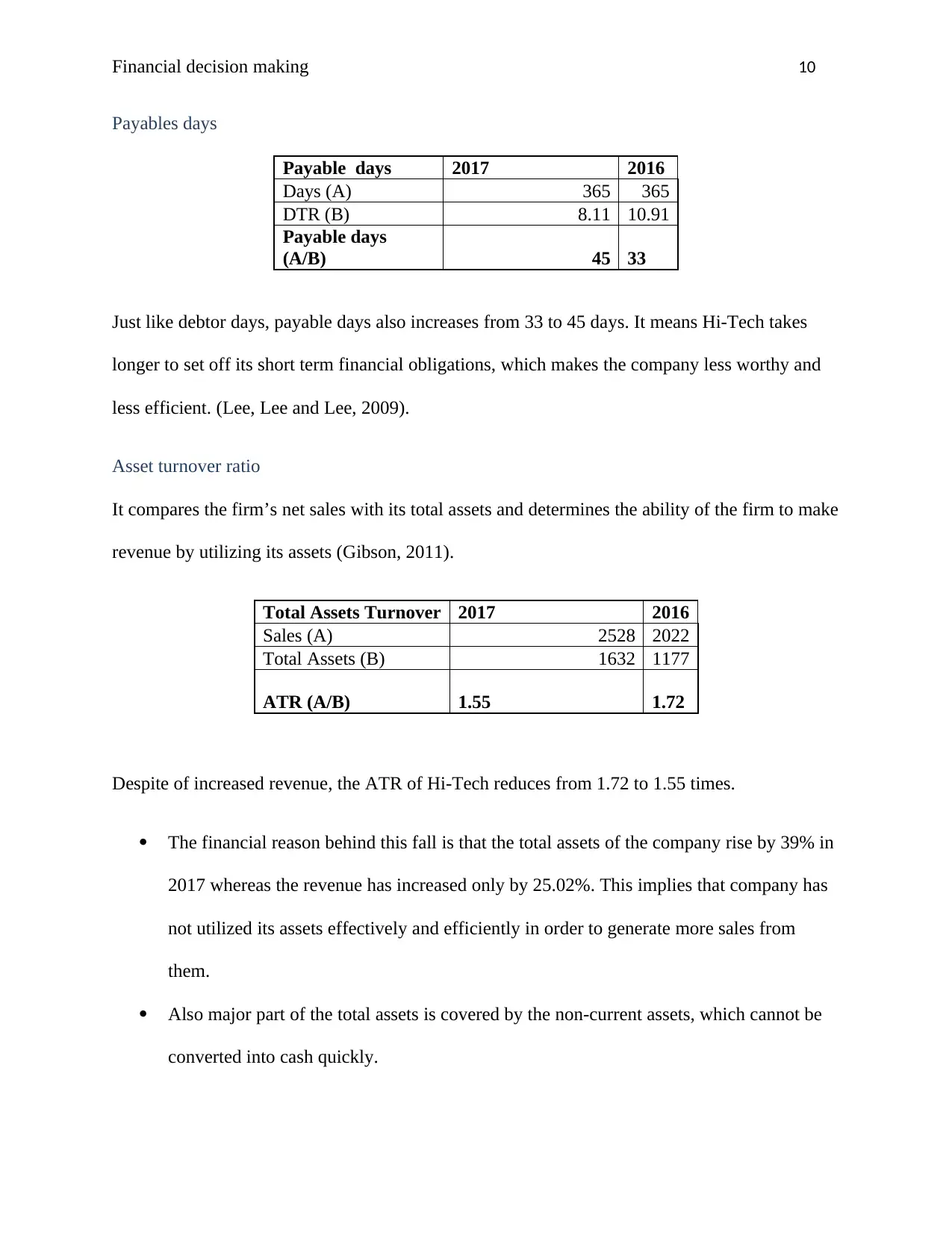

Payables days

Payable days 2017 2016

Days (A) 365 365

DTR (B) 8.11 10.91

Payable days

(A/B) 45 33

Just like debtor days, payable days also increases from 33 to 45 days. It means Hi-Tech takes

longer to set off its short term financial obligations, which makes the company less worthy and

less efficient. (Lee, Lee and Lee, 2009).

Asset turnover ratio

It compares the firm’s net sales with its total assets and determines the ability of the firm to make

revenue by utilizing its assets (Gibson, 2011).

Total Assets Turnover 2017 2016

Sales (A) 2528 2022

Total Assets (B) 1632 1177

ATR (A/B) 1.55 1.72

Despite of increased revenue, the ATR of Hi-Tech reduces from 1.72 to 1.55 times.

The financial reason behind this fall is that the total assets of the company rise by 39% in

2017 whereas the revenue has increased only by 25.02%. This implies that company has

not utilized its assets effectively and efficiently in order to generate more sales from

them.

Also major part of the total assets is covered by the non-current assets, which cannot be

converted into cash quickly.

Payables days

Payable days 2017 2016

Days (A) 365 365

DTR (B) 8.11 10.91

Payable days

(A/B) 45 33

Just like debtor days, payable days also increases from 33 to 45 days. It means Hi-Tech takes

longer to set off its short term financial obligations, which makes the company less worthy and

less efficient. (Lee, Lee and Lee, 2009).

Asset turnover ratio

It compares the firm’s net sales with its total assets and determines the ability of the firm to make

revenue by utilizing its assets (Gibson, 2011).

Total Assets Turnover 2017 2016

Sales (A) 2528 2022

Total Assets (B) 1632 1177

ATR (A/B) 1.55 1.72

Despite of increased revenue, the ATR of Hi-Tech reduces from 1.72 to 1.55 times.

The financial reason behind this fall is that the total assets of the company rise by 39% in

2017 whereas the revenue has increased only by 25.02%. This implies that company has

not utilized its assets effectively and efficiently in order to generate more sales from

them.

Also major part of the total assets is covered by the non-current assets, which cannot be

converted into cash quickly.

Financial decision making 11

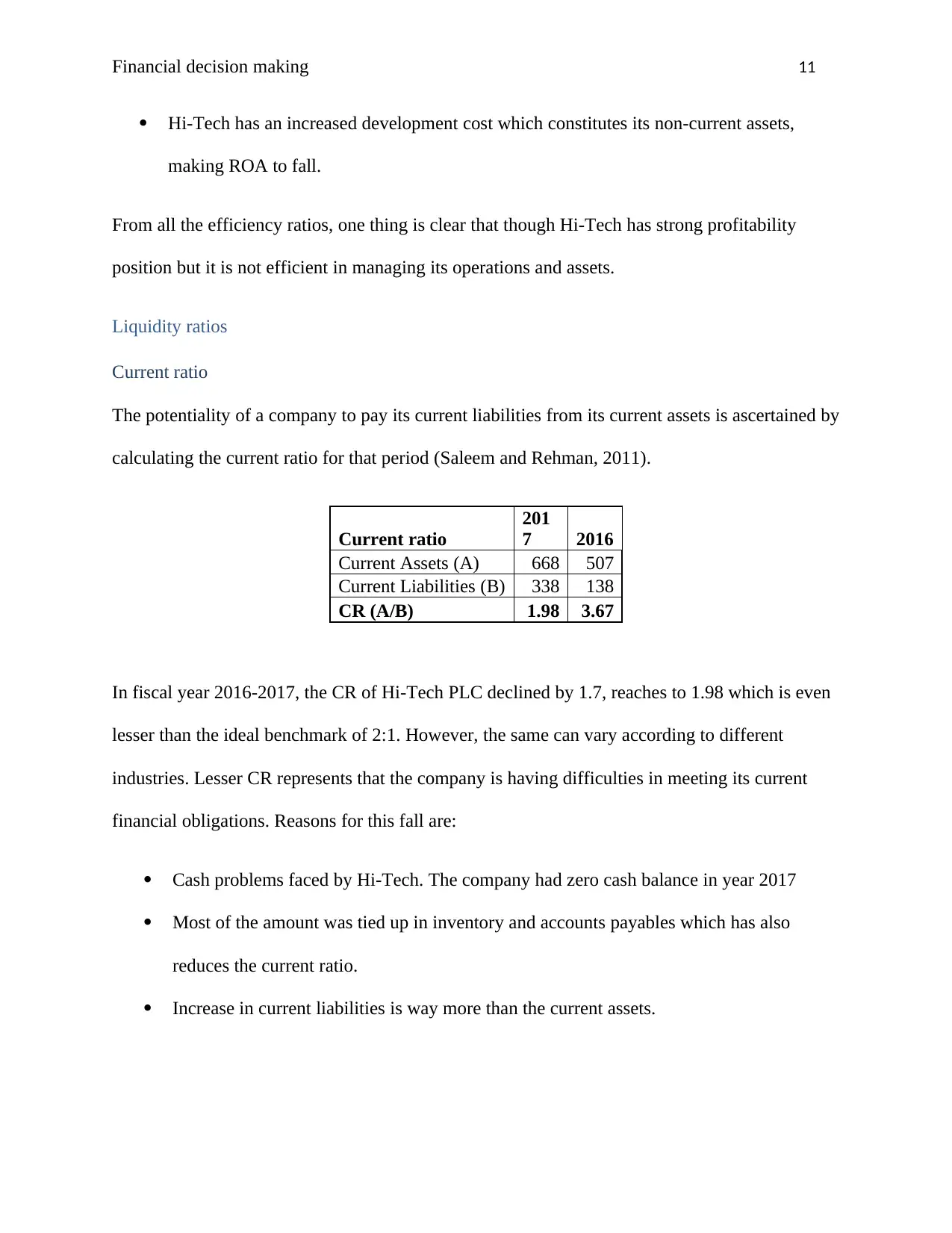

Hi-Tech has an increased development cost which constitutes its non-current assets,

making ROA to fall.

From all the efficiency ratios, one thing is clear that though Hi-Tech has strong profitability

position but it is not efficient in managing its operations and assets.

Liquidity ratios

Current ratio

The potentiality of a company to pay its current liabilities from its current assets is ascertained by

calculating the current ratio for that period (Saleem and Rehman, 2011).

Current ratio

201

7 2016

Current Assets (A) 668 507

Current Liabilities (B) 338 138

CR (A/B) 1.98 3.67

In fiscal year 2016-2017, the CR of Hi-Tech PLC declined by 1.7, reaches to 1.98 which is even

lesser than the ideal benchmark of 2:1. However, the same can vary according to different

industries. Lesser CR represents that the company is having difficulties in meeting its current

financial obligations. Reasons for this fall are:

Cash problems faced by Hi-Tech. The company had zero cash balance in year 2017

Most of the amount was tied up in inventory and accounts payables which has also

reduces the current ratio.

Increase in current liabilities is way more than the current assets.

Hi-Tech has an increased development cost which constitutes its non-current assets,

making ROA to fall.

From all the efficiency ratios, one thing is clear that though Hi-Tech has strong profitability

position but it is not efficient in managing its operations and assets.

Liquidity ratios

Current ratio

The potentiality of a company to pay its current liabilities from its current assets is ascertained by

calculating the current ratio for that period (Saleem and Rehman, 2011).

Current ratio

201

7 2016

Current Assets (A) 668 507

Current Liabilities (B) 338 138

CR (A/B) 1.98 3.67

In fiscal year 2016-2017, the CR of Hi-Tech PLC declined by 1.7, reaches to 1.98 which is even

lesser than the ideal benchmark of 2:1. However, the same can vary according to different

industries. Lesser CR represents that the company is having difficulties in meeting its current

financial obligations. Reasons for this fall are:

Cash problems faced by Hi-Tech. The company had zero cash balance in year 2017

Most of the amount was tied up in inventory and accounts payables which has also

reduces the current ratio.

Increase in current liabilities is way more than the current assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.