Taxation Law HI3042 T2 2017: Individual Assignment Analysis

VerifiedAdded on 2020/03/16

|11

|1521

|33

Homework Assignment

AI Summary

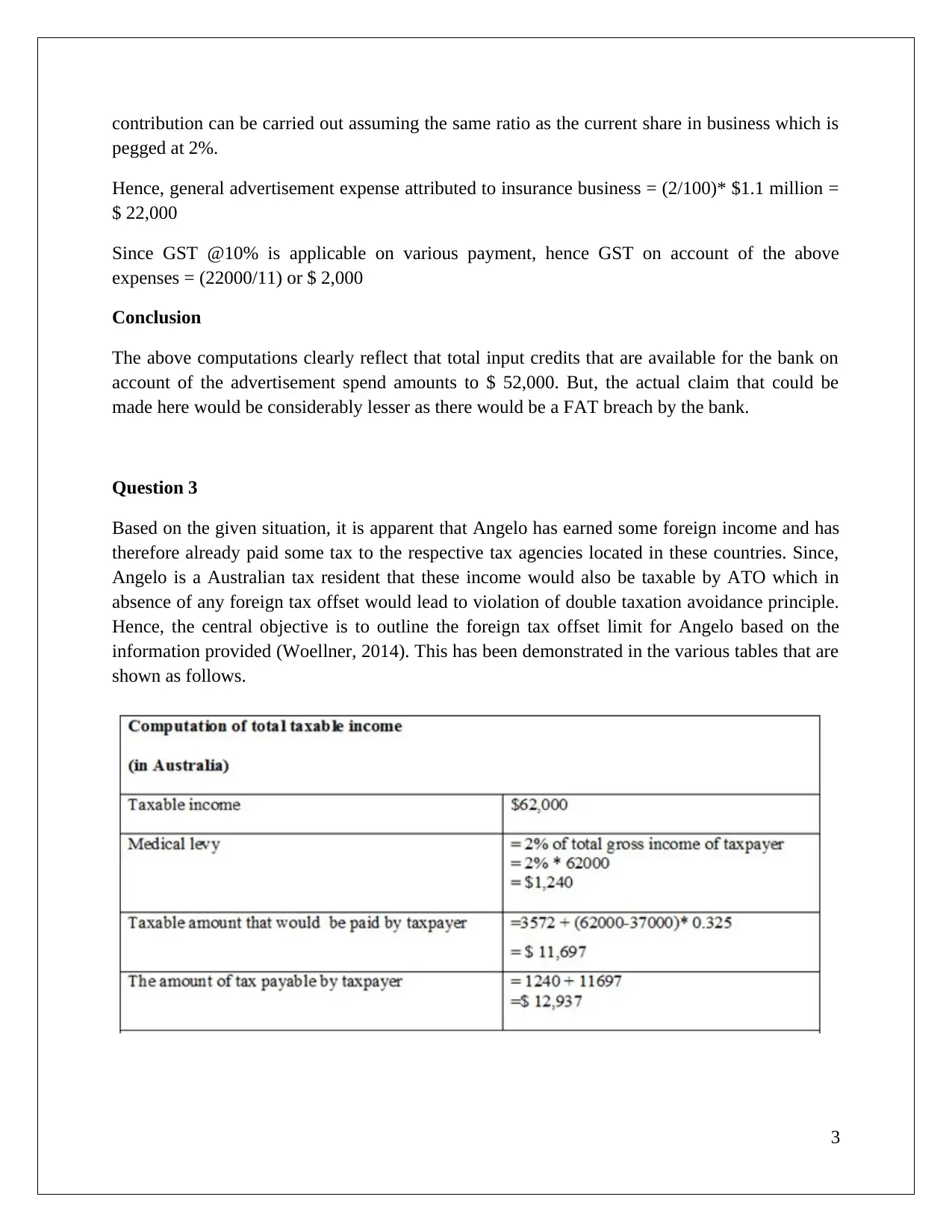

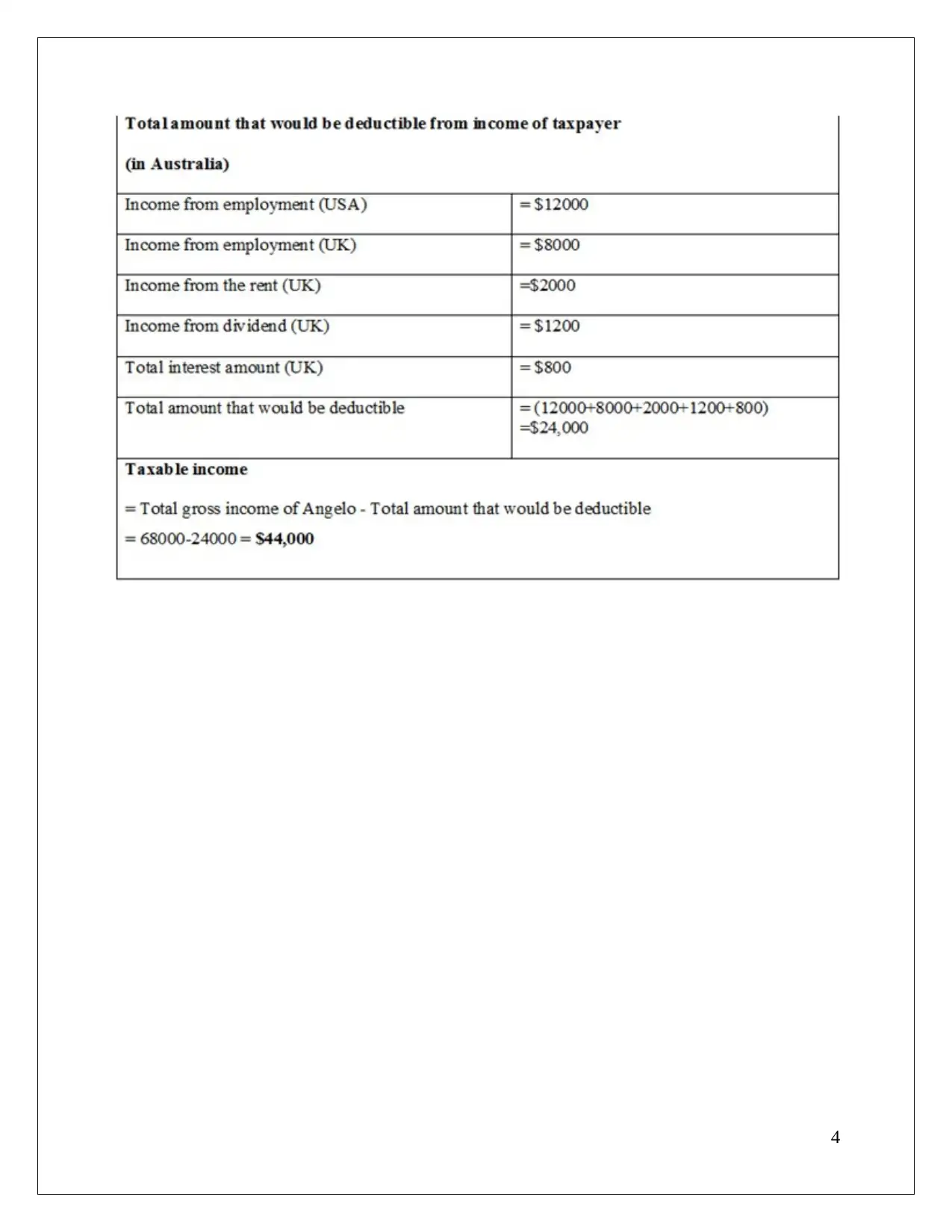

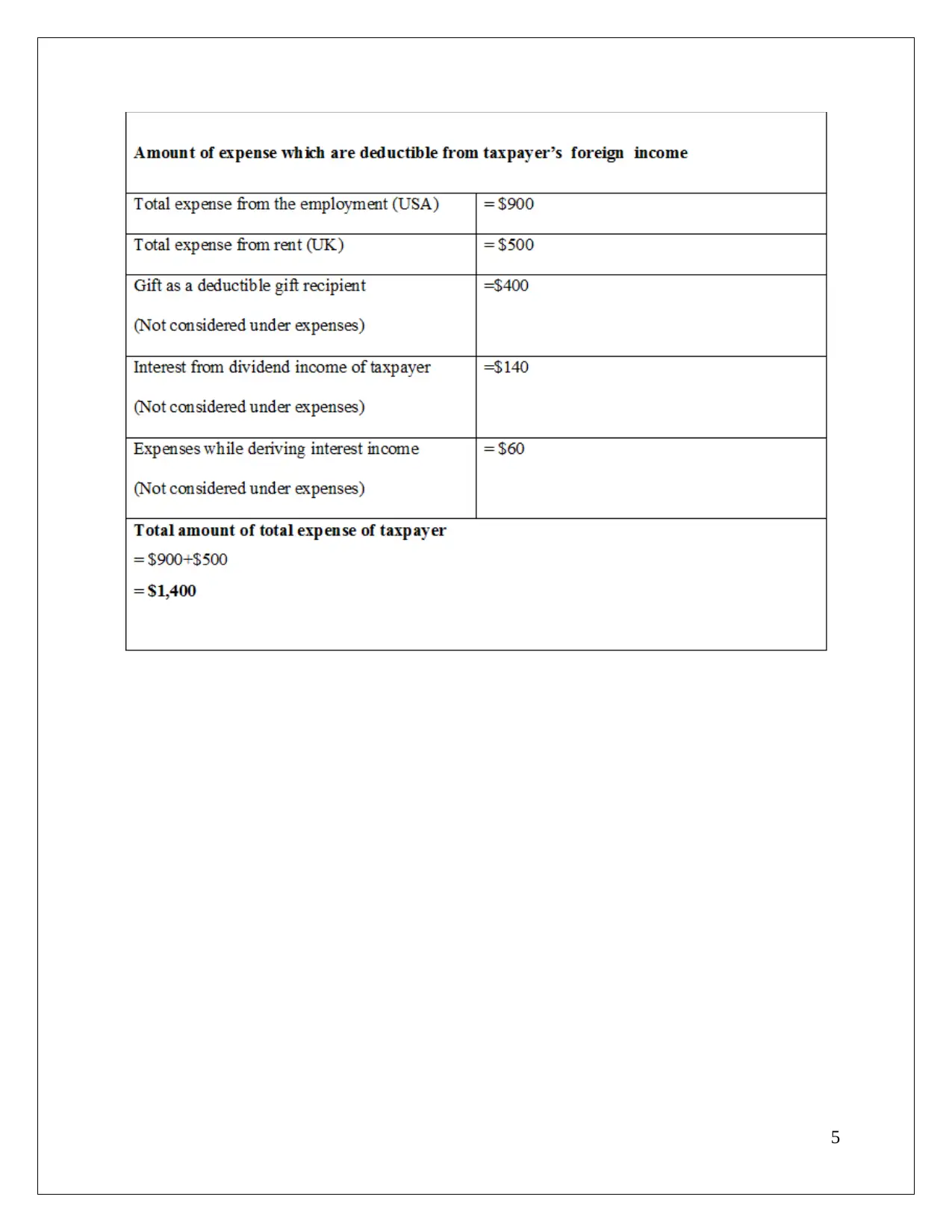

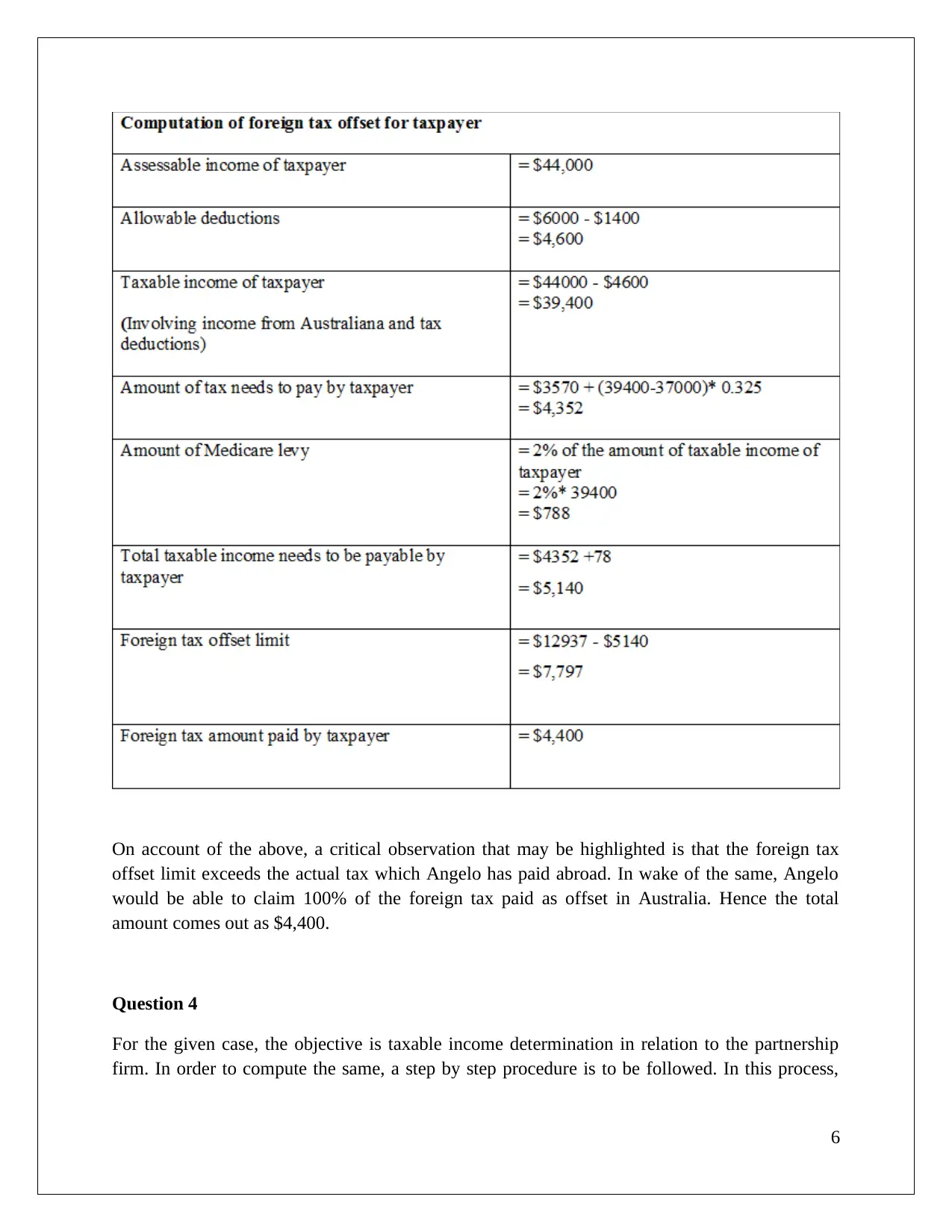

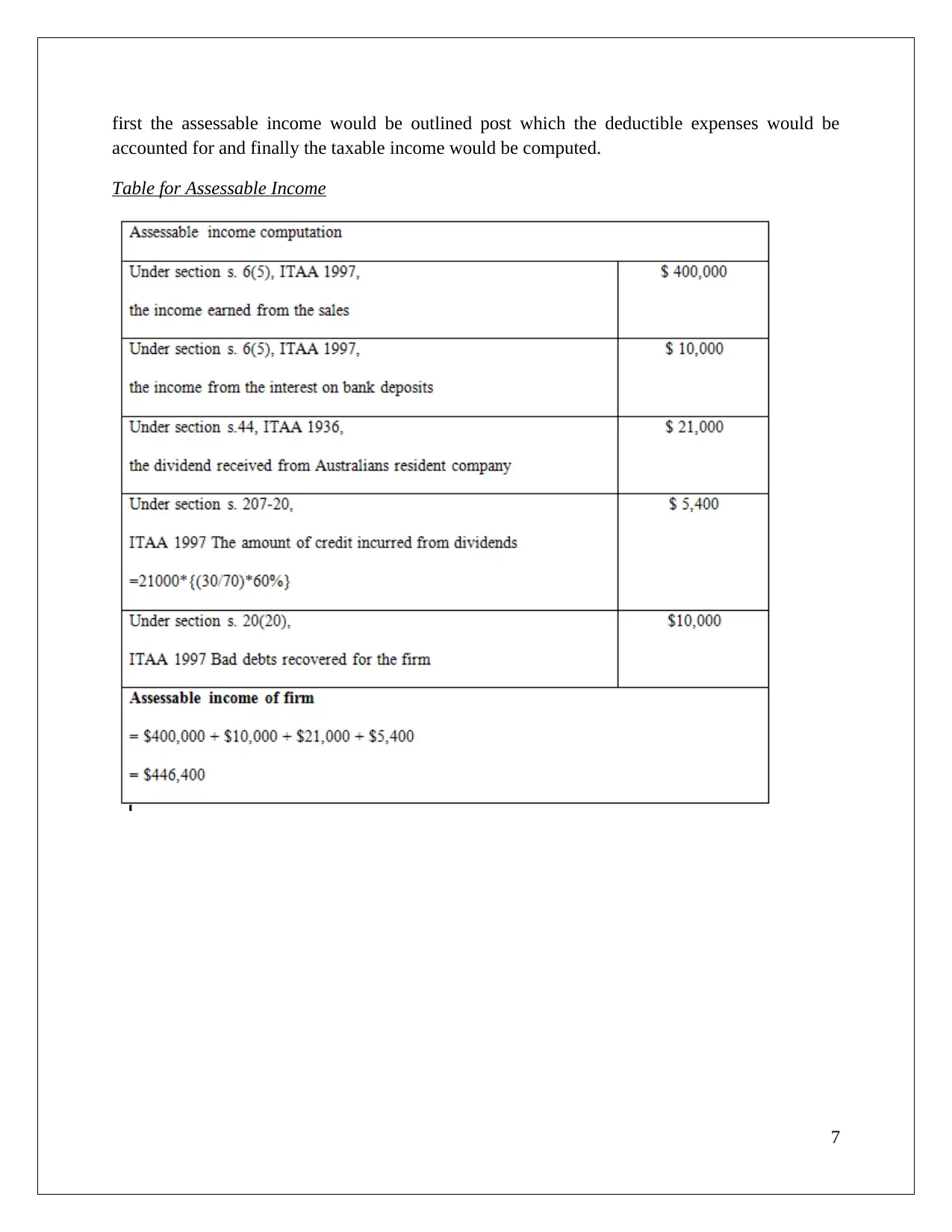

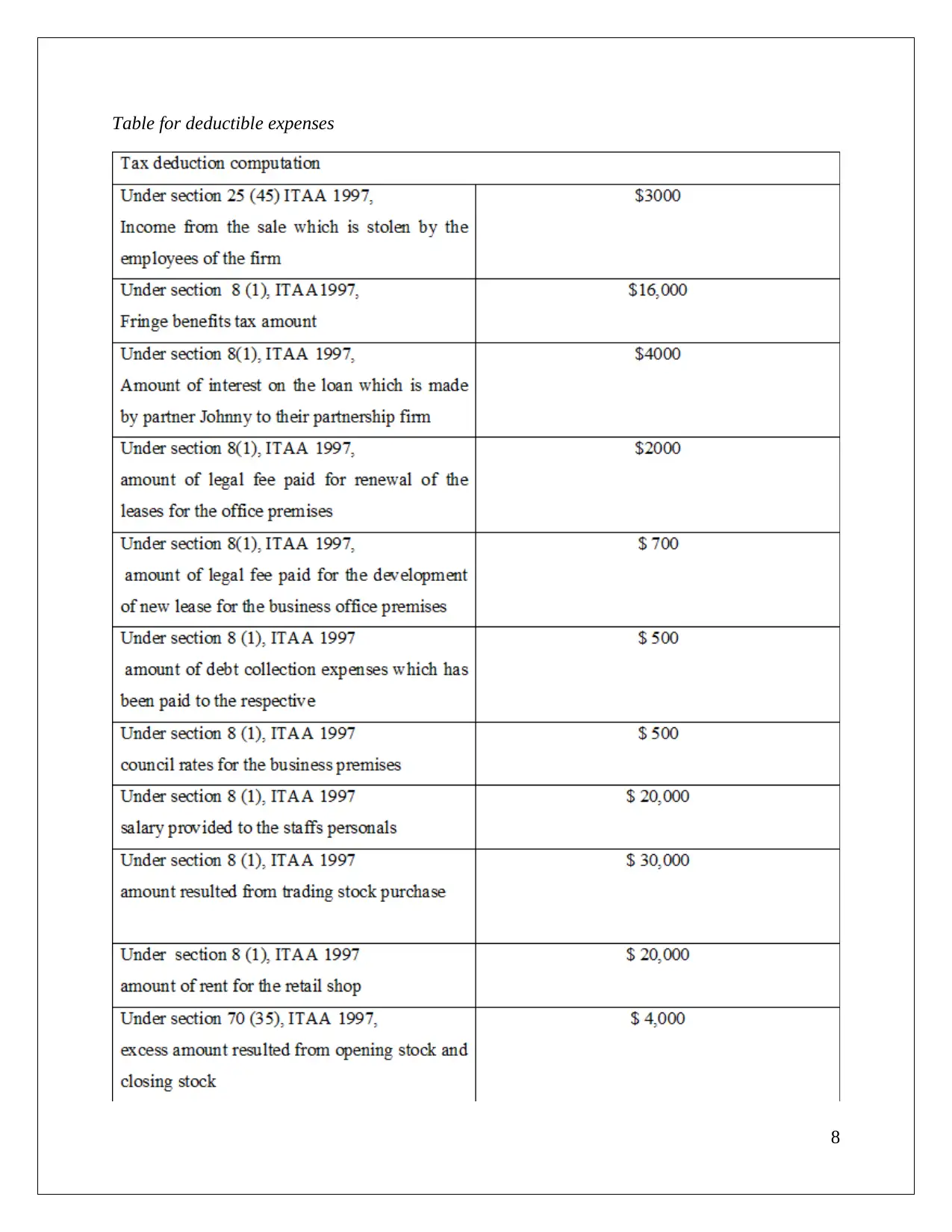

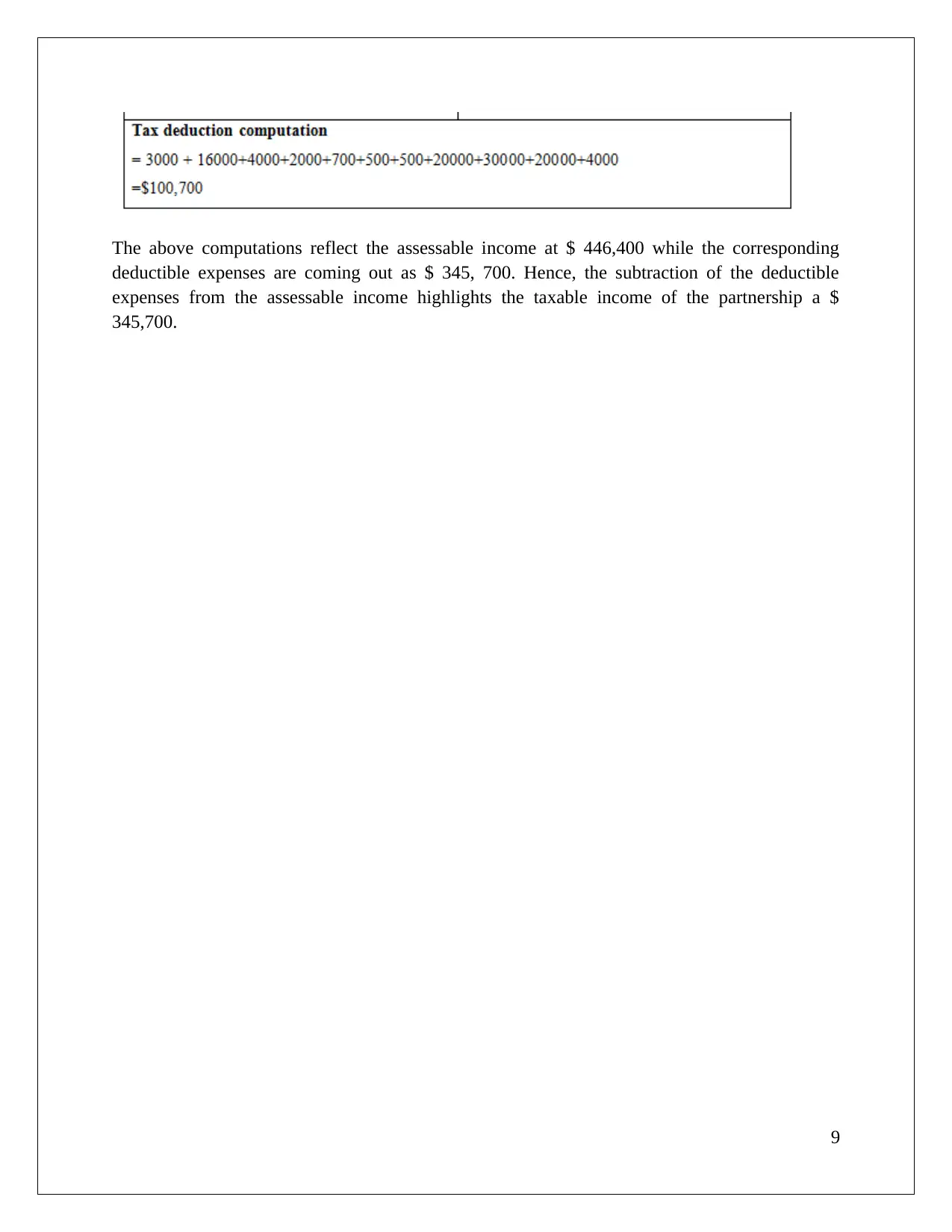

This document presents a comprehensive solution to a taxation law assignment (HI3042). It addresses several key areas of Australian taxation, including the deductibility of business expenses under s. 8(1) of the ITAA 1997, analyzing whether expenses related to asset relocation, legal fees for winding up, and solicitor services for business operations are deductible. The assignment also examines input tax credits, specifically focusing on GST implications for advertising expenses, and determines the extent to which Big Bank can claim input tax credits. Furthermore, the solution outlines the calculation of foreign tax offsets for an Australian tax resident (Angelo) who has earned foreign income and paid taxes abroad. Finally, the assignment concludes with the determination of taxable income for a partnership firm, detailing the calculation of assessable income, deductible expenses, and the resulting taxable income. References to relevant tax law and publications support the analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.