HI5002 Finance for Business: Analyzing Wesfarmers Ltd Performance

VerifiedAdded on 2023/03/30

|20

|4537

|154

Report

AI Summary

This report provides an in-depth financial analysis of Wesfarmers Ltd, an ASX-listed entity, using techniques like ratio analysis, cash management strategies, and sensitivity analysis. The evaluation covers the financial years 2016, 2017, and 2018, examining profitability, operating efficiency, systematic and unsystematic risks, and dividend policy. The analysis indicates Wesfarmers' strong future growth prospects and effective risk management, leading to a recommendation for investment by an institutional investor. The report also discusses the company's use of marketable securities for cash management and includes a capital budgeting scenario to illustrate sensitivity analysis.

HI5002: Group Assignment

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This report has been developed for the purpose of providing an insight into the financial

performance of an ASX listed entity, that is, Wesfarmers Ltd. The financial evaluation conducted

with the use of ratio analysis, systematic and unsystematic risks, dividend policy, cash

management and sensitivity analysis has revealed that Wesfarmers is having good future growth

prospects owing to its higher profitability position. It is also effectively managing its systematic

and unsystematic risks in an effective manner and providing good dividend to shareholders and

thus selected for an investment purpose by an institutional investor.

2

This report has been developed for the purpose of providing an insight into the financial

performance of an ASX listed entity, that is, Wesfarmers Ltd. The financial evaluation conducted

with the use of ratio analysis, systematic and unsystematic risks, dividend policy, cash

management and sensitivity analysis has revealed that Wesfarmers is having good future growth

prospects owing to its higher profitability position. It is also effectively managing its systematic

and unsystematic risks in an effective manner and providing good dividend to shareholders and

thus selected for an investment purpose by an institutional investor.

2

Contents

Abstract............................................................................................................................................2

Section I: Introduction to the report.................................................................................................4

Section II: Financial Analysis of Wesfarmers for last three years (2016, 2017 and 2018).............4

Section 2.1: Overview of the selected company..........................................................................4

Section 2.2: Ratio Analysis of Wesfarmers.................................................................................5

Profitability Analysis of Wesfarmers...........................................................................................5

Operating Efficiency Analysis of Wesfarmers............................................................................7

Section 2.3: Use of marketable securities by Wesfarmers for cash management purpose..........9

Section 2.4: Application of sensitivity analysis through using the capital budgeting scenario...9

Section 2.5: Information on systematic risks and unsystematic risks that impacts the

performance of Wesfarmers.......................................................................................................16

Systematic Risks........................................................................................................................16

Unsystematic Risks....................................................................................................................16

Section 2.6: Estimation of dividend payout ratio and identification of dividend policy used by

the management at Wesfarmers.................................................................................................17

Section III: Recommendation Letter.............................................................................................18

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

3

Abstract............................................................................................................................................2

Section I: Introduction to the report.................................................................................................4

Section II: Financial Analysis of Wesfarmers for last three years (2016, 2017 and 2018).............4

Section 2.1: Overview of the selected company..........................................................................4

Section 2.2: Ratio Analysis of Wesfarmers.................................................................................5

Profitability Analysis of Wesfarmers...........................................................................................5

Operating Efficiency Analysis of Wesfarmers............................................................................7

Section 2.3: Use of marketable securities by Wesfarmers for cash management purpose..........9

Section 2.4: Application of sensitivity analysis through using the capital budgeting scenario...9

Section 2.5: Information on systematic risks and unsystematic risks that impacts the

performance of Wesfarmers.......................................................................................................16

Systematic Risks........................................................................................................................16

Unsystematic Risks....................................................................................................................16

Section 2.6: Estimation of dividend payout ratio and identification of dividend policy used by

the management at Wesfarmers.................................................................................................17

Section III: Recommendation Letter.............................................................................................18

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section I: Introduction to the report

The business entities tend to disclose the information relating to their financial

performance through the help of developing the financial statements. The financial statements

are analyzed by the end-users such as investors for gaining an insight into the present and future

growth of a company. This is largely required to take correct investment decisions and ensuring

that the wealth of the investors’ remains protected. This report has been developed for providing

support to an institutional investor aiming to invest within the Australian market. In this context,

an ASX listed entity having a promising future for investment in Australia has been selected for

the purpose of financial evaluation. The financial evaluation has been done by the use of

examination of the financial statements of the selected company with the use of technique such

as ratio analysis, cash management, and sensitivity analysis, discussion of systematic and

unsystematic risks, analysis of dividend payout ratio and providing recommendation to the

investors on the basis of financial evaluation carried out. The ASX listed entity that has been

selected for the purpose of financial evaluation is Wesfarmers Limited, a supermarket giant in

Australia.

Section II: Financial Analysis of Wesfarmers for last three years (2016, 2017 and 2018)

Section 2.1: Overview of the selected company

Wesfarmers Limited is a supermarket giant of Australia whose headquarter is located

Perth. The company is regarded to be in a conglomerate business as it is involved in different

businesses such as retail, chemicals, fertilizers, home improvement, outdoor living, apparel,

general merchandise and industrial safety products. As such, the major business segments have

been divided into following categories:

Home Improvements

Department Stores

Industrial Safety Products

Office Works

The company since its establishment in the year 1914 has been recognized as one of the

major retailing company within Australia. It is regarded as one of the largest employer within the

country. It conducts its diverse business operations with the help of its many subsidiaries such as

Bunning’s Warehouse, Kmart, Officeworks and others across Australia. The primary objective of

the company is to promote sustainable growth of its business through long-term management.

The company since its establishment has prioritized to become a sustainable company by

conducts its business operations in a responsible and ethical manner. The high emphasis placed

on sustainability has enabled the company to promote its long-term growth and development by

achieving a distinctive position in the retailing sector of Australia. It strong commitment towards

4

The business entities tend to disclose the information relating to their financial

performance through the help of developing the financial statements. The financial statements

are analyzed by the end-users such as investors for gaining an insight into the present and future

growth of a company. This is largely required to take correct investment decisions and ensuring

that the wealth of the investors’ remains protected. This report has been developed for providing

support to an institutional investor aiming to invest within the Australian market. In this context,

an ASX listed entity having a promising future for investment in Australia has been selected for

the purpose of financial evaluation. The financial evaluation has been done by the use of

examination of the financial statements of the selected company with the use of technique such

as ratio analysis, cash management, and sensitivity analysis, discussion of systematic and

unsystematic risks, analysis of dividend payout ratio and providing recommendation to the

investors on the basis of financial evaluation carried out. The ASX listed entity that has been

selected for the purpose of financial evaluation is Wesfarmers Limited, a supermarket giant in

Australia.

Section II: Financial Analysis of Wesfarmers for last three years (2016, 2017 and 2018)

Section 2.1: Overview of the selected company

Wesfarmers Limited is a supermarket giant of Australia whose headquarter is located

Perth. The company is regarded to be in a conglomerate business as it is involved in different

businesses such as retail, chemicals, fertilizers, home improvement, outdoor living, apparel,

general merchandise and industrial safety products. As such, the major business segments have

been divided into following categories:

Home Improvements

Department Stores

Industrial Safety Products

Office Works

The company since its establishment in the year 1914 has been recognized as one of the

major retailing company within Australia. It is regarded as one of the largest employer within the

country. It conducts its diverse business operations with the help of its many subsidiaries such as

Bunning’s Warehouse, Kmart, Officeworks and others across Australia. The primary objective of

the company is to promote sustainable growth of its business through long-term management.

The company since its establishment has prioritized to become a sustainable company by

conducts its business operations in a responsible and ethical manner. The high emphasis placed

on sustainability has enabled the company to promote its long-term growth and development by

achieving a distinctive position in the retailing sector of Australia. It strong commitment towards

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

promoting the growth and development of local communities and reducing the environmental

impact has enabled it to create value over long-term (Wesfarmers Limited, 2019).

Section 2.2: Ratio Analysis of Wesfarmers

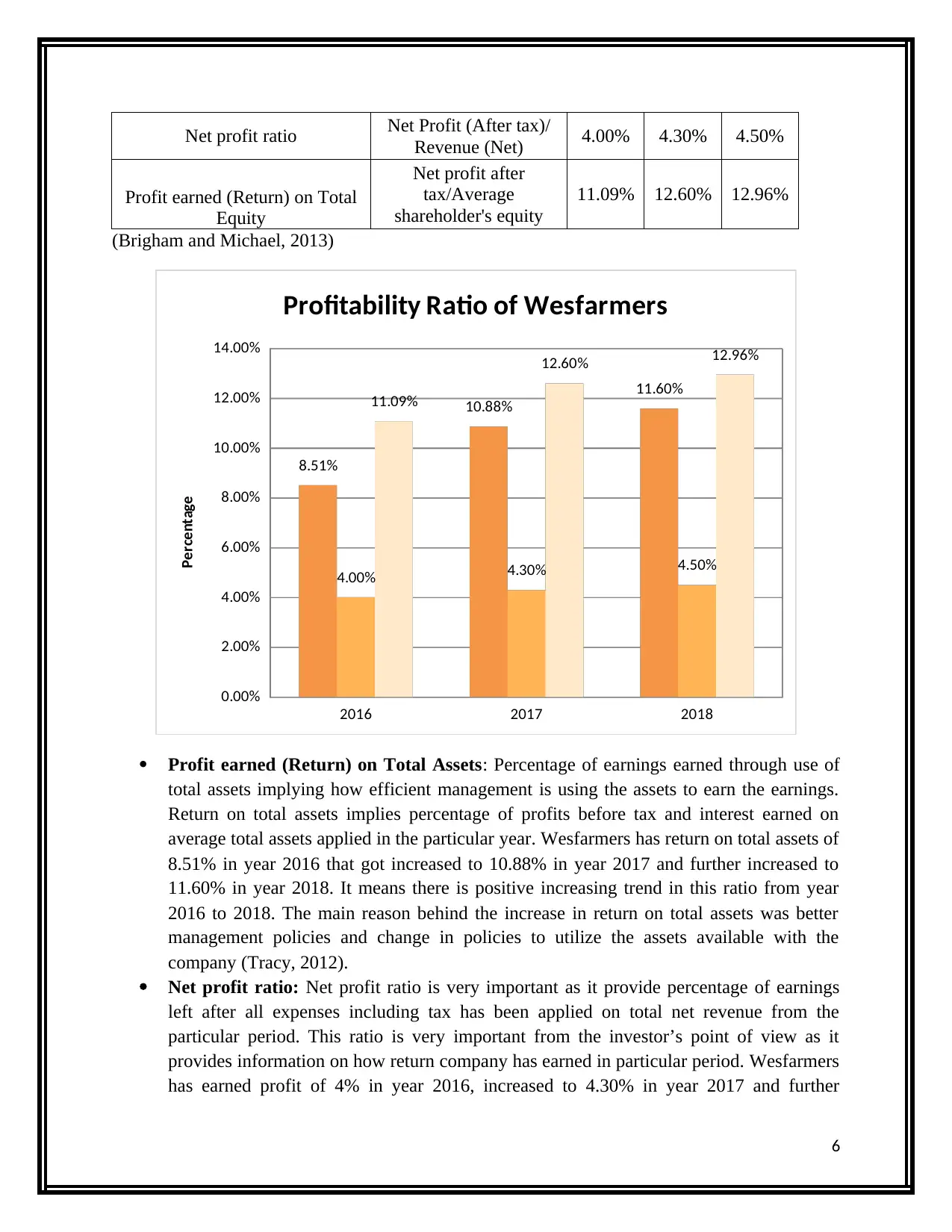

This section of the report will provide the detailed calculation of performance ratios

divided into two major categories profitability and operating efficiency. Firstly detailed

calculation has been made for ratios for last three years (2016, 2017 and 2018). All financial data

has been gathered from the annual reports available on company website under investor’s

relation section.

Profitability Analysis of Wesfarmers

The purpose of profitability ratios is to evaluate the profitability performance of the

company during the specific period and it also allows the comparisons of profitability among

two. It means current profitability performance of Wesfarmers can be compared with previous

year in to order to evaluate the trend in performance. Profitability ratios measure the ability of

company to earn the sales revenue through use of resources available with the company. Some of

the important profitability ratios are net profit ratio, gross profit ratio, return on assets and return

on equity.

Data extracted from the financial report of Wesfarmers for last three years

Items of finance Year 2015 Year 2016 Year 2017 Year 2018

Amount in $ Million

Profit before Interest

and tax

$

3,454.00

$

4,400.00

$

4,468.00

Net profit after tax

$

2,646.00

$

2,955.00

$

3,025.00

Net Revenue

$

66,085.00

$

68,648.00

$

67,152.00

Equity Shareholders

value

$

24,781.00

$

22,949.00

$

23,941.00

$

22,754.00

Average shareholder's

equity

$

23,865.00

$

23,445.00

$

23,347.50

Assets (Total)

$

40,402.00

$

40,783.00

$

40,115.00

$

36,933.00

Average total assets

$

40,592.50

$

40,449.00

$

38,524.00

(Wesfarmers Limited, 2018; Wesfarmers Limited. 2017 and Wesfarmers Limited. 2016)

Profitability Ratio (Wesfarmers)

Ratios Formula 2016 2017 2018

Profit earned (Return) on Total

Assets

Profit before Interest

and tax/Average assets

(Total)

8.51% 10.88% 11.60%

5

impact has enabled it to create value over long-term (Wesfarmers Limited, 2019).

Section 2.2: Ratio Analysis of Wesfarmers

This section of the report will provide the detailed calculation of performance ratios

divided into two major categories profitability and operating efficiency. Firstly detailed

calculation has been made for ratios for last three years (2016, 2017 and 2018). All financial data

has been gathered from the annual reports available on company website under investor’s

relation section.

Profitability Analysis of Wesfarmers

The purpose of profitability ratios is to evaluate the profitability performance of the

company during the specific period and it also allows the comparisons of profitability among

two. It means current profitability performance of Wesfarmers can be compared with previous

year in to order to evaluate the trend in performance. Profitability ratios measure the ability of

company to earn the sales revenue through use of resources available with the company. Some of

the important profitability ratios are net profit ratio, gross profit ratio, return on assets and return

on equity.

Data extracted from the financial report of Wesfarmers for last three years

Items of finance Year 2015 Year 2016 Year 2017 Year 2018

Amount in $ Million

Profit before Interest

and tax

$

3,454.00

$

4,400.00

$

4,468.00

Net profit after tax

$

2,646.00

$

2,955.00

$

3,025.00

Net Revenue

$

66,085.00

$

68,648.00

$

67,152.00

Equity Shareholders

value

$

24,781.00

$

22,949.00

$

23,941.00

$

22,754.00

Average shareholder's

equity

$

23,865.00

$

23,445.00

$

23,347.50

Assets (Total)

$

40,402.00

$

40,783.00

$

40,115.00

$

36,933.00

Average total assets

$

40,592.50

$

40,449.00

$

38,524.00

(Wesfarmers Limited, 2018; Wesfarmers Limited. 2017 and Wesfarmers Limited. 2016)

Profitability Ratio (Wesfarmers)

Ratios Formula 2016 2017 2018

Profit earned (Return) on Total

Assets

Profit before Interest

and tax/Average assets

(Total)

8.51% 10.88% 11.60%

5

Net profit ratio Net Profit (After tax)/

Revenue (Net) 4.00% 4.30% 4.50%

Profit earned (Return) on Total

Equity

Net profit after

tax/Average

shareholder's equity

11.09% 12.60% 12.96%

(Brigham and Michael, 2013)

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

8.51%

10.88%

11.60%

4.00% 4.30% 4.50%

11.09%

12.60% 12.96%

Profitability Ratio of Wesfarmers

Percentage

Profit earned (Return) on Total Assets: Percentage of earnings earned through use of

total assets implying how efficient management is using the assets to earn the earnings.

Return on total assets implies percentage of profits before tax and interest earned on

average total assets applied in the particular year. Wesfarmers has return on total assets of

8.51% in year 2016 that got increased to 10.88% in year 2017 and further increased to

11.60% in year 2018. It means there is positive increasing trend in this ratio from year

2016 to 2018. The main reason behind the increase in return on total assets was better

management policies and change in policies to utilize the assets available with the

company (Tracy, 2012).

Net profit ratio: Net profit ratio is very important as it provide percentage of earnings

left after all expenses including tax has been applied on total net revenue from the

particular period. This ratio is very important from the investor’s point of view as it

provides information on how return company has earned in particular period. Wesfarmers

has earned profit of 4% in year 2016, increased to 4.30% in year 2017 and further

6

Revenue (Net) 4.00% 4.30% 4.50%

Profit earned (Return) on Total

Equity

Net profit after

tax/Average

shareholder's equity

11.09% 12.60% 12.96%

(Brigham and Michael, 2013)

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

8.51%

10.88%

11.60%

4.00% 4.30% 4.50%

11.09%

12.60% 12.96%

Profitability Ratio of Wesfarmers

Percentage

Profit earned (Return) on Total Assets: Percentage of earnings earned through use of

total assets implying how efficient management is using the assets to earn the earnings.

Return on total assets implies percentage of profits before tax and interest earned on

average total assets applied in the particular year. Wesfarmers has return on total assets of

8.51% in year 2016 that got increased to 10.88% in year 2017 and further increased to

11.60% in year 2018. It means there is positive increasing trend in this ratio from year

2016 to 2018. The main reason behind the increase in return on total assets was better

management policies and change in policies to utilize the assets available with the

company (Tracy, 2012).

Net profit ratio: Net profit ratio is very important as it provide percentage of earnings

left after all expenses including tax has been applied on total net revenue from the

particular period. This ratio is very important from the investor’s point of view as it

provides information on how return company has earned in particular period. Wesfarmers

has earned profit of 4% in year 2016, increased to 4.30% in year 2017 and further

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increased to 4.50% in year 2018 that implies positive increasing trend in net profit ratio in

last three years. The retail industry of Australia has faced tough times in last 5 years and

it is very hard to earn good net profit. This is the reason why profit is less as compared to

percentage of net profit in other industries. Wesfarmers has earned substantial net profit

during the past three years and there was increasing trend in this ratio.

Profit earned (Return) on Total Equity: The ratio denotes the profitability position of a

company by providing an assessment of the net income realized over the equity base of

its shareholders. The ROE of the company has depicted an increasing trend over the past

three years from 11.09% to 12.96% which means that it is generating increasing returns

over the equity resources of its shareholders (Arnold, 2013).

Operating Efficiency Analysis of Wesfarmers

Data extracted from the financial report of Wesfarmers for last three years

Items of finance Year 2015 Year 2016 Year 2017 Year 2018

Amount in $ Million

Net Revenue

$

66,085.00

$

68,648.00

$

67,152.00

Account Receivables

(Net)

$

1,463.00

$

1,628.00

$

1,633.00

$

1,657.00

Average account

receivable

$

1,545.50

$

1,630.50

$

1,645.00

Assets (Total)

$

40,402.00

$

40,783.00

$

40,115.00

$

36,933.00

Average total assets

$

40,592.50

$

40,449.00

$

38,524.00

Cost of Goods Sold

$

45,930.00

$

45,033.00

$

46,123.00

Inventory items

$

5,497.00

$

6,260.00

$

6,530.00

$

6,011.00

Average Inventory

$

5,878.50

$

6,395.00

$

6,270.50

(Wesfarmers Limited, 2018; Wesfarmers Limited. 2017 and Wesfarmers Limited. 2016)

Efficiency Ratio (Wesfarmers)

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

7.81 7.04 7.36

Account Receivable turnover ratio Net sales/Average

account receivables 42.76 42.10 40.82

7

last three years. The retail industry of Australia has faced tough times in last 5 years and

it is very hard to earn good net profit. This is the reason why profit is less as compared to

percentage of net profit in other industries. Wesfarmers has earned substantial net profit

during the past three years and there was increasing trend in this ratio.

Profit earned (Return) on Total Equity: The ratio denotes the profitability position of a

company by providing an assessment of the net income realized over the equity base of

its shareholders. The ROE of the company has depicted an increasing trend over the past

three years from 11.09% to 12.96% which means that it is generating increasing returns

over the equity resources of its shareholders (Arnold, 2013).

Operating Efficiency Analysis of Wesfarmers

Data extracted from the financial report of Wesfarmers for last three years

Items of finance Year 2015 Year 2016 Year 2017 Year 2018

Amount in $ Million

Net Revenue

$

66,085.00

$

68,648.00

$

67,152.00

Account Receivables

(Net)

$

1,463.00

$

1,628.00

$

1,633.00

$

1,657.00

Average account

receivable

$

1,545.50

$

1,630.50

$

1,645.00

Assets (Total)

$

40,402.00

$

40,783.00

$

40,115.00

$

36,933.00

Average total assets

$

40,592.50

$

40,449.00

$

38,524.00

Cost of Goods Sold

$

45,930.00

$

45,033.00

$

46,123.00

Inventory items

$

5,497.00

$

6,260.00

$

6,530.00

$

6,011.00

Average Inventory

$

5,878.50

$

6,395.00

$

6,270.50

(Wesfarmers Limited, 2018; Wesfarmers Limited. 2017 and Wesfarmers Limited. 2016)

Efficiency Ratio (Wesfarmers)

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

7.81 7.04 7.36

Account Receivable turnover ratio Net sales/Average

account receivables 42.76 42.10 40.82

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

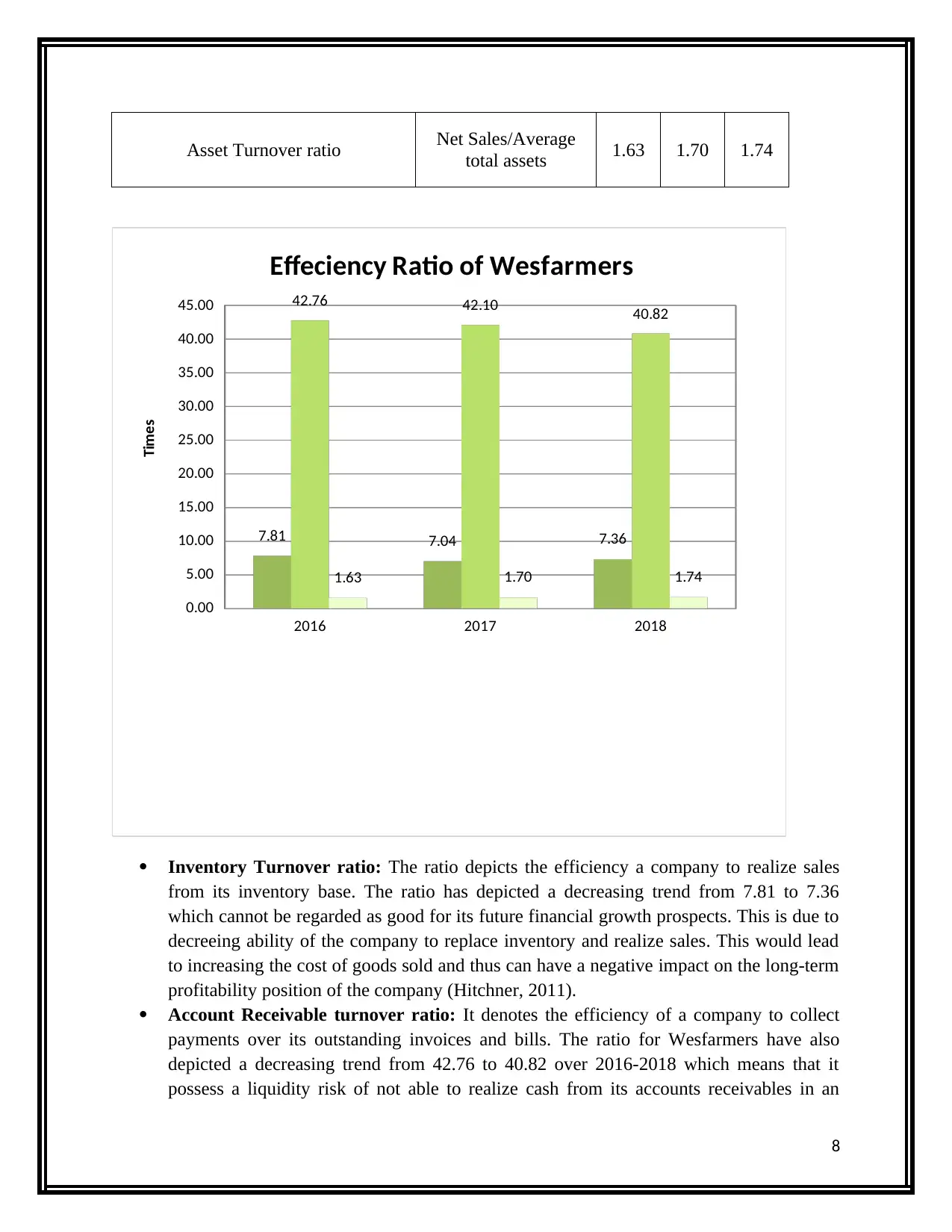

Asset Turnover ratio Net Sales/Average

total assets 1.63 1.70 1.74

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

7.81 7.04 7.36

42.76 42.10 40.82

1.63 1.70 1.74

Effeciency Ratio of Wesfarmers

Times

Inventory Turnover ratio: The ratio depicts the efficiency a company to realize sales

from its inventory base. The ratio has depicted a decreasing trend from 7.81 to 7.36

which cannot be regarded as good for its future financial growth prospects. This is due to

decreeing ability of the company to replace inventory and realize sales. This would lead

to increasing the cost of goods sold and thus can have a negative impact on the long-term

profitability position of the company (Hitchner, 2011).

Account Receivable turnover ratio: It denotes the efficiency of a company to collect

payments over its outstanding invoices and bills. The ratio for Wesfarmers have also

depicted a decreasing trend from 42.76 to 40.82 over 2016-2018 which means that it

possess a liquidity risk of not able to realize cash from its accounts receivables in an

8

total assets 1.63 1.70 1.74

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

7.81 7.04 7.36

42.76 42.10 40.82

1.63 1.70 1.74

Effeciency Ratio of Wesfarmers

Times

Inventory Turnover ratio: The ratio depicts the efficiency a company to realize sales

from its inventory base. The ratio has depicted a decreasing trend from 7.81 to 7.36

which cannot be regarded as good for its future financial growth prospects. This is due to

decreeing ability of the company to replace inventory and realize sales. This would lead

to increasing the cost of goods sold and thus can have a negative impact on the long-term

profitability position of the company (Hitchner, 2011).

Account Receivable turnover ratio: It denotes the efficiency of a company to collect

payments over its outstanding invoices and bills. The ratio for Wesfarmers have also

depicted a decreasing trend from 42.76 to 40.82 over 2016-2018 which means that it

possess a liquidity risk of not able to realize cash from its accounts receivables in an

8

effective manner which can lead to reduction in its operational efficiency and thus long-

term profits,.

Asset Turnover ratio: The asset turnover ratio for the company has depicted an

increasing trend over the past three financial years from 1.63 to 1.74. The ratio is also

higher than 1 over the selected time-period which means that it possess good efficiency to

realize sales from the asset base (Baker and Powell, 2009).

Section 2.3: Use of marketable securities by Wesfarmers for cash management purpose

Marketable securities refer to the short term financial instruments that are easily

redeemable in the market and they can be easily brought and sold in the market. It means

maturity period of the marketable securities is less than 1 year. The purpose of using the

marketable securities is to make sure enough liquidated cash is available with the company that

can be used in one year time period to pay the current liabilities. Marketable securities can be

both debt securities and equity securities dependent upon the securities chosen by the company.

Investment in shares, bonds, and debentures are some of examples of marketable securities

(Krantz, 2016).

Wesfarmers Limited manages uses cash and cash equivalent such as capital market debt,

corporate bonds, financial instruments and other derivatives to manage their cash requirements.

All these marketable securities are being valued at fair value or carrying value depending upon

the value of marketable securities. So, it can be said that Wesfarmers make efficient use of

marketable securities to manage its cash requirements. Wesfarmers regularly trades in derivative

market and also in corporate bonds to get some benefit from the market. In addition to this

Wesfarmers have enough cash and cash equivalents to achieve the working capital requirements

(Wesfarmers Limited, 2018).

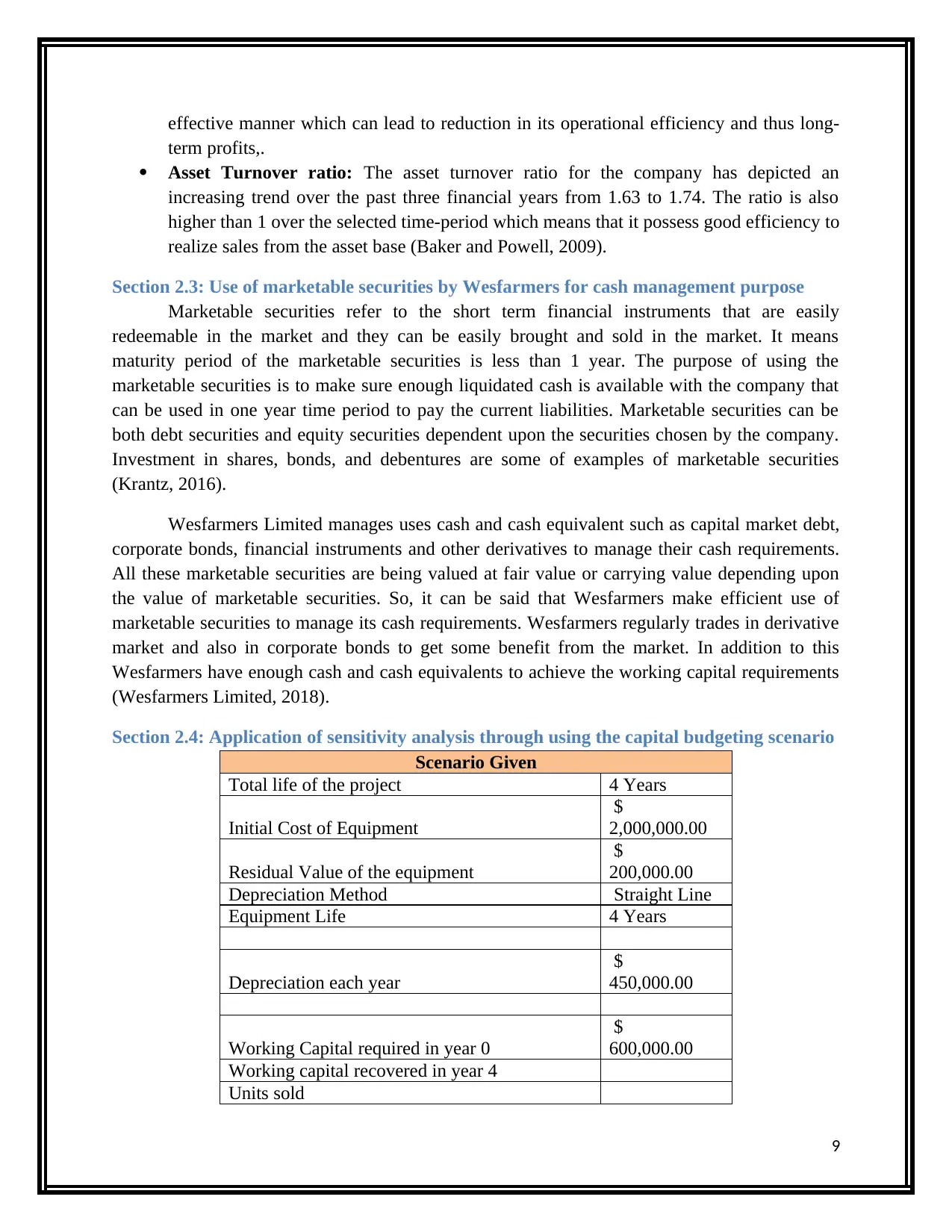

Section 2.4: Application of sensitivity analysis through using the capital budgeting scenario

Scenario Given

Total life of the project 4 Years

Initial Cost of Equipment

$

2,000,000.00

Residual Value of the equipment

$

200,000.00

Depreciation Method Straight Line

Equipment Life 4 Years

Depreciation each year

$

450,000.00

Working Capital required in year 0

$

600,000.00

Working capital recovered in year 4

Units sold

9

term profits,.

Asset Turnover ratio: The asset turnover ratio for the company has depicted an

increasing trend over the past three financial years from 1.63 to 1.74. The ratio is also

higher than 1 over the selected time-period which means that it possess good efficiency to

realize sales from the asset base (Baker and Powell, 2009).

Section 2.3: Use of marketable securities by Wesfarmers for cash management purpose

Marketable securities refer to the short term financial instruments that are easily

redeemable in the market and they can be easily brought and sold in the market. It means

maturity period of the marketable securities is less than 1 year. The purpose of using the

marketable securities is to make sure enough liquidated cash is available with the company that

can be used in one year time period to pay the current liabilities. Marketable securities can be

both debt securities and equity securities dependent upon the securities chosen by the company.

Investment in shares, bonds, and debentures are some of examples of marketable securities

(Krantz, 2016).

Wesfarmers Limited manages uses cash and cash equivalent such as capital market debt,

corporate bonds, financial instruments and other derivatives to manage their cash requirements.

All these marketable securities are being valued at fair value or carrying value depending upon

the value of marketable securities. So, it can be said that Wesfarmers make efficient use of

marketable securities to manage its cash requirements. Wesfarmers regularly trades in derivative

market and also in corporate bonds to get some benefit from the market. In addition to this

Wesfarmers have enough cash and cash equivalents to achieve the working capital requirements

(Wesfarmers Limited, 2018).

Section 2.4: Application of sensitivity analysis through using the capital budgeting scenario

Scenario Given

Total life of the project 4 Years

Initial Cost of Equipment

$

2,000,000.00

Residual Value of the equipment

$

200,000.00

Depreciation Method Straight Line

Equipment Life 4 Years

Depreciation each year

$

450,000.00

Working Capital required in year 0

$

600,000.00

Working capital recovered in year 4

Units sold

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year 1 300000

Year 2 300000

Year 3 300000

Year 4 300000

Selling Price of product

$

20.00

Variable Cost of the product

$

12.00

Fixed Cost in each year

$

300,000.00

Discount Rate used to discount the cash flows 10%

Tax Rate 30%

Firstly there is need to calculate the cash flow without any change in value driver:

10

Year 2 300000

Year 3 300000

Year 4 300000

Selling Price of product

$

20.00

Variable Cost of the product

$

12.00

Fixed Cost in each year

$

300,000.00

Discount Rate used to discount the cash flows 10%

Tax Rate 30%

Firstly there is need to calculate the cash flow without any change in value driver:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0 1 2 3 4

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20$ 20$ 20$ 20$

Net Cash Inflows 6,000,000$ 6,000,000$ 6,000,000$ 6,000,000$

Cash Outflows

Variable Cost 3,600,000$ 3,600,000$ 3,600,000$ 3,600,000$

Fixed Cost 300,000$ 300,000$ 300,000$ 300,000$

Depreciation 450,000$ 450,000$ 450,000$ 450,000$

Total Cash outflows 4,350,000$ 4,350,000$ 4,350,000$ 4,350,000$

Cash flows before tax 1,650,000$ 1,650,000$ 1,650,000$ 1,650,000$

Less: Tax @ 30% 495,000$ 495,000$ 495,000$ 495,000$

Cash Flows after tax 1,155,000$ 1,155,000$ 1,155,000$ 1,155,000$

Add: Depreciation 450,000$ 450,000$ 450,000$ 450,000$

Cash Flows before

depreciation after tax 1,605,000$ 1,605,000$ 1,605,000$ 1,605,000$

Initial Equiment Cost (2,000,000)$

Salvage Value 200,000$

Working Capital

Initial Requirement (600,000)$

Recovery 600,000$

Net Cash Flows (2,600,000)$ 1,605,000$ 1,605,000$ 1,605,000$ 2,405,000$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000)$ 1,459,091$ 1,326,446$ 1,205,860$ 1,642,647$

Net Present Value 3,034,045$

Cash Flows during the life of the project in normal Case

Years

Particulars

11

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20$ 20$ 20$ 20$

Net Cash Inflows 6,000,000$ 6,000,000$ 6,000,000$ 6,000,000$

Cash Outflows

Variable Cost 3,600,000$ 3,600,000$ 3,600,000$ 3,600,000$

Fixed Cost 300,000$ 300,000$ 300,000$ 300,000$

Depreciation 450,000$ 450,000$ 450,000$ 450,000$

Total Cash outflows 4,350,000$ 4,350,000$ 4,350,000$ 4,350,000$

Cash flows before tax 1,650,000$ 1,650,000$ 1,650,000$ 1,650,000$

Less: Tax @ 30% 495,000$ 495,000$ 495,000$ 495,000$

Cash Flows after tax 1,155,000$ 1,155,000$ 1,155,000$ 1,155,000$

Add: Depreciation 450,000$ 450,000$ 450,000$ 450,000$

Cash Flows before

depreciation after tax 1,605,000$ 1,605,000$ 1,605,000$ 1,605,000$

Initial Equiment Cost (2,000,000)$

Salvage Value 200,000$

Working Capital

Initial Requirement (600,000)$

Recovery 600,000$

Net Cash Flows (2,600,000)$ 1,605,000$ 1,605,000$ 1,605,000$ 2,405,000$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000)$ 1,459,091$ 1,326,446$ 1,205,860$ 1,642,647$

Net Present Value 3,034,045$

Cash Flows during the life of the project in normal Case

Years

Particulars

11

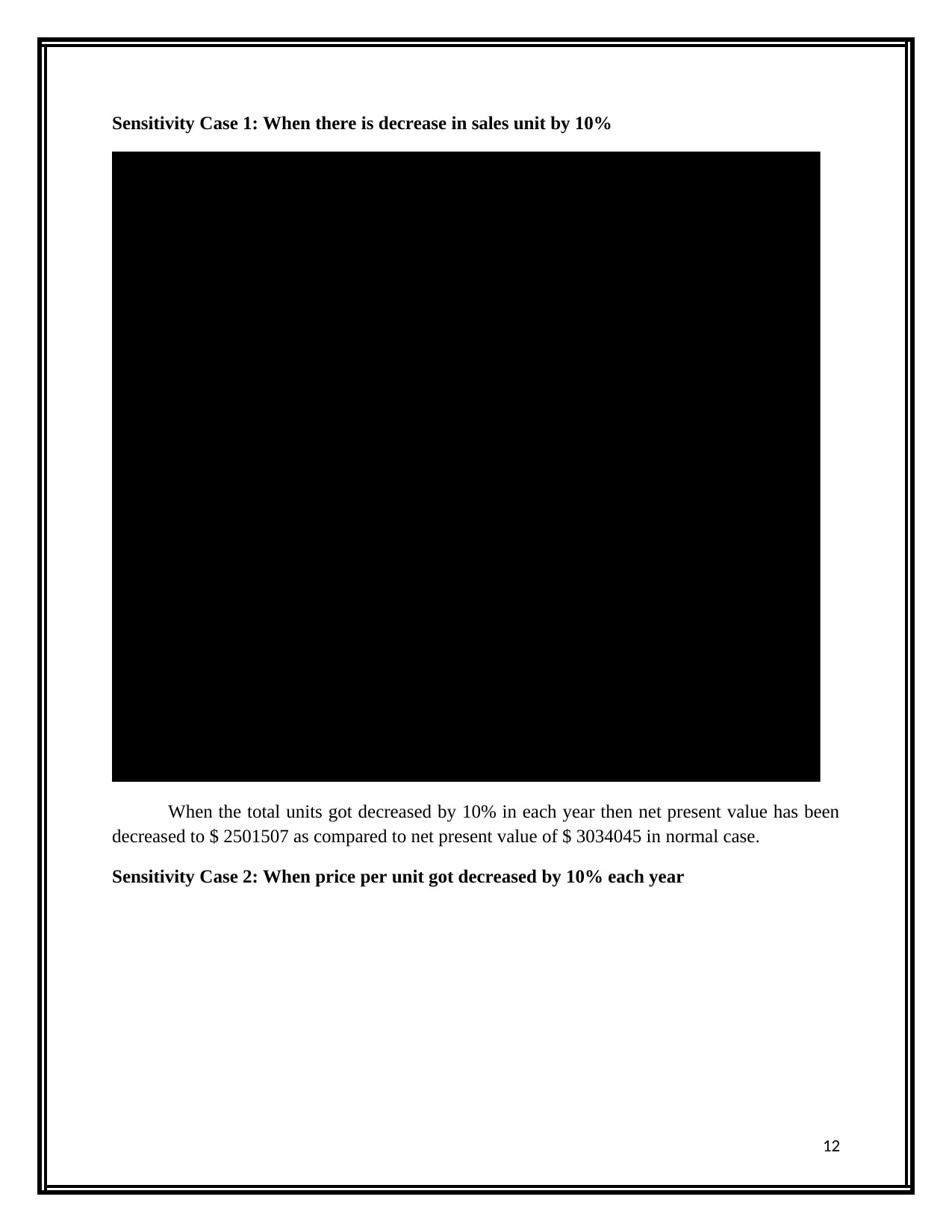

Sensitivity Case 1: When there is decrease in sales unit by 10%

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows $5,400,000 $5,400,000 $5,400,000 $5,400,000

Cash Outflows

Variable Cost $3,240,000 $3,240,000 $3,240,000 $3,240,000

Fixed Cost $300,000 $300,000 $300,000 $300,000

Depreciation $450,000 $450,000 $450,000 $450,000

Total Cash outflows $3,990,000 $3,990,000 $3,990,000 $3,990,000

Cash flows before tax $1,410,000 $1,410,000 $1,410,000 $1,410,000

Less: Tax @ 30% $423,000 $423,000 $423,000 $423,000

Cash Flows after tax $987,000 $987,000 $987,000 $987,000

Add: Depreciation $450,000 $450,000 $450,000 $450,000

Cash Flows before

depreciation after tax $1,437,000 $1,437,000 $1,437,000 $1,437,000

Initial Equiment Cost (2,000,000)$

Salvage Value 200,000$

Working Capital

Initial Requirement (600,000)$

Recovery 600,000$

Net Cash Flows -$2,600,000 $1,437,000 $1,437,000 $1,437,000 $2,237,000

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000)$ 1,306,364$ 1,187,603$ 1,079,639$ 1,527,901$

Net Present Value 2,501,507$

Statement of Cash flows when Unit sales decrease by 10%

Particulars Years

When the total units got decreased by 10% in each year then net present value has been

decreased to $ 2501507 as compared to net present value of $ 3034045 in normal case.

Sensitivity Case 2: When price per unit got decreased by 10% each year

12

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows $5,400,000 $5,400,000 $5,400,000 $5,400,000

Cash Outflows

Variable Cost $3,240,000 $3,240,000 $3,240,000 $3,240,000

Fixed Cost $300,000 $300,000 $300,000 $300,000

Depreciation $450,000 $450,000 $450,000 $450,000

Total Cash outflows $3,990,000 $3,990,000 $3,990,000 $3,990,000

Cash flows before tax $1,410,000 $1,410,000 $1,410,000 $1,410,000

Less: Tax @ 30% $423,000 $423,000 $423,000 $423,000

Cash Flows after tax $987,000 $987,000 $987,000 $987,000

Add: Depreciation $450,000 $450,000 $450,000 $450,000

Cash Flows before

depreciation after tax $1,437,000 $1,437,000 $1,437,000 $1,437,000

Initial Equiment Cost (2,000,000)$

Salvage Value 200,000$

Working Capital

Initial Requirement (600,000)$

Recovery 600,000$

Net Cash Flows -$2,600,000 $1,437,000 $1,437,000 $1,437,000 $2,237,000

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000)$ 1,306,364$ 1,187,603$ 1,079,639$ 1,527,901$

Net Present Value 2,501,507$

Statement of Cash flows when Unit sales decrease by 10%

Particulars Years

When the total units got decreased by 10% in each year then net present value has been

decreased to $ 2501507 as compared to net present value of $ 3034045 in normal case.

Sensitivity Case 2: When price per unit got decreased by 10% each year

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.