HI5017 Managerial Accounting: ABC System Implementation at Integral

VerifiedAdded on 2023/06/11

|14

|2983

|257

Report

AI Summary

This report provides a comprehensive analysis of the Activity-Based Costing (ABC) system and its potential implementation within Integral Diagnostics Ltd, an ASX-listed healthcare service provider. It explores the characteristics of the ABC system, its alignment with the company's strategies and goals, and the challenges and benefits of its adoption in the healthcare sector. The report also considers alternative management accounting tools, such as budgetary control, and their potential advantages for Integral Diagnostics Ltd. The analysis includes a discussion of cost allocation, the role of cross-functional teams, and the importance of top management support for successful implementation. Ultimately, the report aims to provide valuable insights for improving cost management and operational efficiency within the company.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The study has included the important discourse associated to ABC system and its

enforcement from different perspective of company. The satisfactory criterion for this

system have been implemented in ASX listed company named Integral Diagnostics Ltd. The

existence of highly valuable and enhanced management accounting approach this company

is ideal for the assessment purposes. The main findings show that it particular reference to

the selected company, there is a system will be having a significant role in tracing the

business activities which need special attention and evaluation. Based on the analysis, it will

be conducive in adopting budgetary control as an alternative to ABC which will ensure

overall efficiency in terms of cost and process optimisation for the company.

Executive Summary:

The study has included the important discourse associated to ABC system and its

enforcement from different perspective of company. The satisfactory criterion for this

system have been implemented in ASX listed company named Integral Diagnostics Ltd. The

existence of highly valuable and enhanced management accounting approach this company

is ideal for the assessment purposes. The main findings show that it particular reference to

the selected company, there is a system will be having a significant role in tracing the

business activities which need special attention and evaluation. Based on the analysis, it will

be conducive in adopting budgetary control as an alternative to ABC which will ensure

overall efficiency in terms of cost and process optimisation for the company.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

Answer to Part a:........................................................................................................................3

Answer to Part b:.......................................................................................................................5

Requirement i:........................................................................................................................5

Requirement ii:.......................................................................................................................5

Requirement iii:......................................................................................................................6

Answer to Part c:........................................................................................................................8

Answer to Part d:.......................................................................................................................9

Conclusion:...............................................................................................................................10

References................................................................................................................................12

Table of Contents

Introduction:..............................................................................................................................3

Answer to Part a:........................................................................................................................3

Answer to Part b:.......................................................................................................................5

Requirement i:........................................................................................................................5

Requirement ii:.......................................................................................................................5

Requirement iii:......................................................................................................................6

Answer to Part c:........................................................................................................................8

Answer to Part d:.......................................................................................................................9

Conclusion:...............................................................................................................................10

References................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

Some of the important discourse in the report have comprised of relevant

information associated to ABC system and its enforcement from different perspective of

company. The satisfactory criterion for this system have been implemented in ASX listed

company named Integral Diagnostics Ltd. The existence of highly valuable and enhanced

management accounting approach this company is ideal for the assessment purposes. The

company is considered to be a healthcare service provider which is seen to specialise in

several areas of medical specialists, general practitioners and providing diagnostic imaging

services with the allied health professionals and patients across Australia. There have been

several efforts this company to align the ABC system with management’s goal and

strategies. The main form of recommendation has been seen to enforce suitable accounting

technique comprising of departmental needs (Weygandt, Kimmel and Kieso 2015).

Answer to Part a:

An important aspect of costing method under the basic concept is identified with

conducting the business operations in which the products are assigned in terms of indirect

costs. Additionally, the emphasis is placed on relating the activities for apportioning and

indirect costs with reduced subjectivity as compared to the conventional system. However,

managers find it intricate to apportion only few aspects of costs with the help of it is a

system. Due to this, the costing method has gained popularity among several industrial and

manufacturing sectors. Additionally, there is a possibility of using ABC system for product

costing, service pricing and target costing (Öker and Adıgüzel 2016).

Introduction:

Some of the important discourse in the report have comprised of relevant

information associated to ABC system and its enforcement from different perspective of

company. The satisfactory criterion for this system have been implemented in ASX listed

company named Integral Diagnostics Ltd. The existence of highly valuable and enhanced

management accounting approach this company is ideal for the assessment purposes. The

company is considered to be a healthcare service provider which is seen to specialise in

several areas of medical specialists, general practitioners and providing diagnostic imaging

services with the allied health professionals and patients across Australia. There have been

several efforts this company to align the ABC system with management’s goal and

strategies. The main form of recommendation has been seen to enforce suitable accounting

technique comprising of departmental needs (Weygandt, Kimmel and Kieso 2015).

Answer to Part a:

An important aspect of costing method under the basic concept is identified with

conducting the business operations in which the products are assigned in terms of indirect

costs. Additionally, the emphasis is placed on relating the activities for apportioning and

indirect costs with reduced subjectivity as compared to the conventional system. However,

managers find it intricate to apportion only few aspects of costs with the help of it is a

system. Due to this, the costing method has gained popularity among several industrial and

manufacturing sectors. Additionally, there is a possibility of using ABC system for product

costing, service pricing and target costing (Öker and Adıgüzel 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

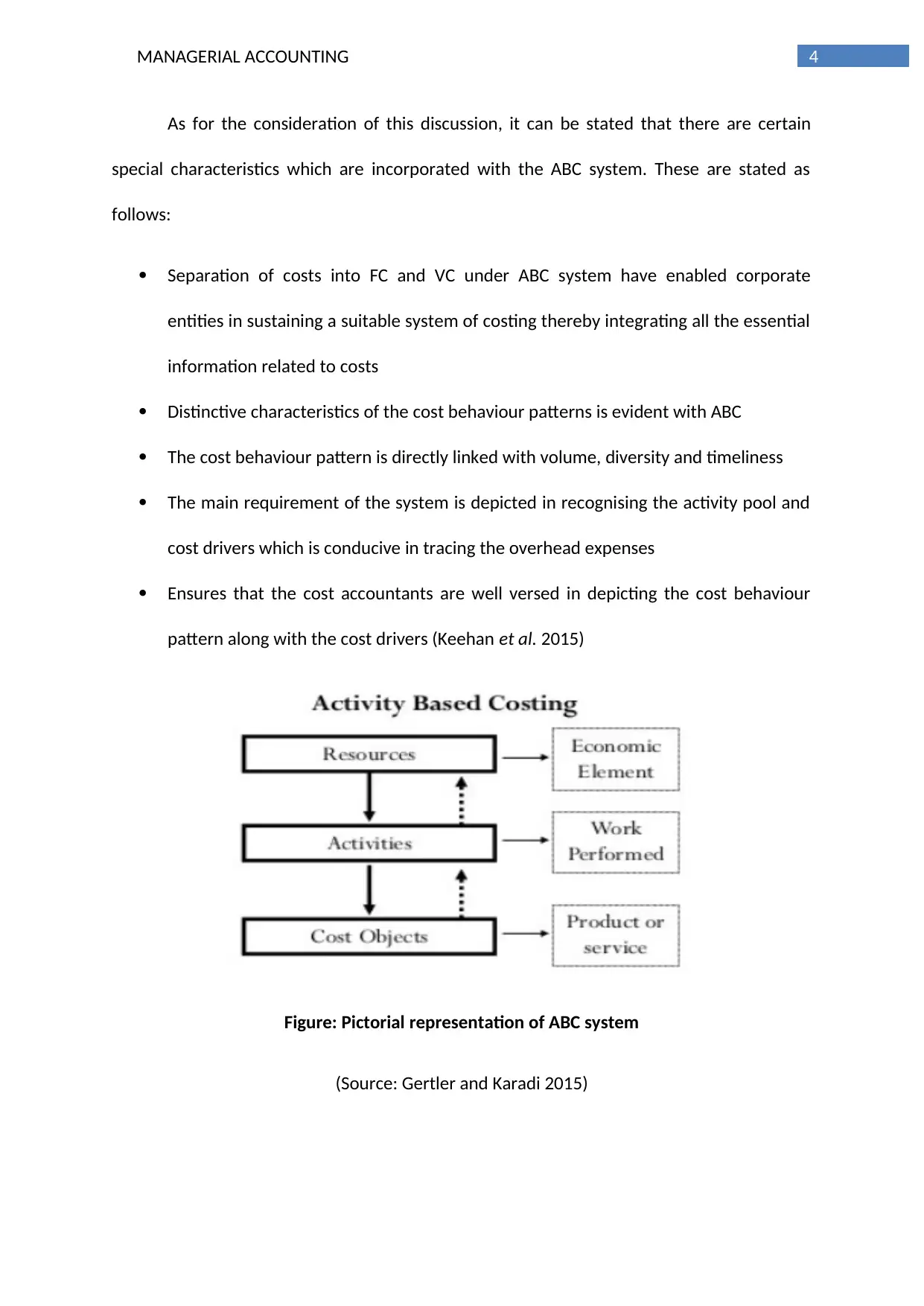

As for the consideration of this discussion, it can be stated that there are certain

special characteristics which are incorporated with the ABC system. These are stated as

follows:

Separation of costs into FC and VC under ABC system have enabled corporate

entities in sustaining a suitable system of costing thereby integrating all the essential

information related to costs

Distinctive characteristics of the cost behaviour patterns is evident with ABC

The cost behaviour pattern is directly linked with volume, diversity and timeliness

The main requirement of the system is depicted in recognising the activity pool and

cost drivers which is conducive in tracing the overhead expenses

Ensures that the cost accountants are well versed in depicting the cost behaviour

pattern along with the cost drivers (Keehan et al. 2015)

Figure: Pictorial representation of ABC system

(Source: Gertler and Karadi 2015)

As for the consideration of this discussion, it can be stated that there are certain

special characteristics which are incorporated with the ABC system. These are stated as

follows:

Separation of costs into FC and VC under ABC system have enabled corporate

entities in sustaining a suitable system of costing thereby integrating all the essential

information related to costs

Distinctive characteristics of the cost behaviour patterns is evident with ABC

The cost behaviour pattern is directly linked with volume, diversity and timeliness

The main requirement of the system is depicted in recognising the activity pool and

cost drivers which is conducive in tracing the overhead expenses

Ensures that the cost accountants are well versed in depicting the cost behaviour

pattern along with the cost drivers (Keehan et al. 2015)

Figure: Pictorial representation of ABC system

(Source: Gertler and Karadi 2015)

5MANAGERIAL ACCOUNTING

Answer to Part b:

It can be identified that with the assistance of ABC, the organisations are able to

better align their strategies and goals as per the costing impediments. For ensuring such

alignment, the basic needs are listed as follows:

Requirement i:

The main mission of the Internal Diagnostics Ltd has been depicted in assimilating

the main factors which work towards achievement of particular strategies and objectives.

Based on the company’s value and mission statement, it is depicted to provide inclusive

radiology services by referring from the allied health specialists and doctors. In order to

further ensure the use of such services the company uses several platforms such as clinical

outcomes, business efficacy and several other factors leading to patient care. Therefore, it

can be stated that mission statement of Integral Diagnostics Ltd have aimed at fulfilling the

needs of the customer by providing them superior services in the most cost-effective

manner. Additionally, profit is seen to be significant in terms of organisation for maintaining

the different aspects of sustainability. The main importance of improvement in the work

ambience is associated with raising the confidence and morale among the staff. This has

been taken into consideration as it leads to improved performance and attainment of

business goals and objectives (Mossialos et al. 2016).

Requirement ii:

The company’s descent to develop several corporate strategies and an innovative

manner which has adhered to all the business objectives as discussed below:

Answer to Part b:

It can be identified that with the assistance of ABC, the organisations are able to

better align their strategies and goals as per the costing impediments. For ensuring such

alignment, the basic needs are listed as follows:

Requirement i:

The main mission of the Internal Diagnostics Ltd has been depicted in assimilating

the main factors which work towards achievement of particular strategies and objectives.

Based on the company’s value and mission statement, it is depicted to provide inclusive

radiology services by referring from the allied health specialists and doctors. In order to

further ensure the use of such services the company uses several platforms such as clinical

outcomes, business efficacy and several other factors leading to patient care. Therefore, it

can be stated that mission statement of Integral Diagnostics Ltd have aimed at fulfilling the

needs of the customer by providing them superior services in the most cost-effective

manner. Additionally, profit is seen to be significant in terms of organisation for maintaining

the different aspects of sustainability. The main importance of improvement in the work

ambience is associated with raising the confidence and morale among the staff. This has

been taken into consideration as it leads to improved performance and attainment of

business goals and objectives (Mossialos et al. 2016).

Requirement ii:

The company’s descent to develop several corporate strategies and an innovative

manner which has adhered to all the business objectives as discussed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

The primary corporate strategy has been depicted in offering several types of quality

services to the rural patients across Australia in such a way that the profit can be

increased in these areas along with reducing business cost

The next important criterion has been depicted with providing necessary assistance

to the rural communities which will promote the development of a good brand

image for Integral Diagnostics Ltd

The third perspective needs to be further observed with initiating all the cost-

effective techniques and ensuring an increased profit margin

This stage is followed by taking the necessary measures for ensuring that the newly

opened centres helps in providing increased earnings and contribute to positive

future growth

The last outcome can be seen with valuing the evidence-based medicine is in the

best way possible (Foley and Manova 2015)

Requirement iii:

Based on the depiction of the ABC system, the model can be widely implemented in

the manufacturing area however there are certain features which cannot be left unnoticed

especially in the healthcare sector. It has been identified that the healthcare service

provider is not seen to possess any DC, as an alternative the costs are segregated with

overhead expenses. Therefore, the adoption of such a costing method will allow the

company to enjoy some benefits which will fulfil the business objectives and strategies

(Warren and Jones 2018).

There are several systems in ABC which deals with resources and cost object of

sections. With particular reference to Integral Diagnostics Ltd, the resource section has been

The primary corporate strategy has been depicted in offering several types of quality

services to the rural patients across Australia in such a way that the profit can be

increased in these areas along with reducing business cost

The next important criterion has been depicted with providing necessary assistance

to the rural communities which will promote the development of a good brand

image for Integral Diagnostics Ltd

The third perspective needs to be further observed with initiating all the cost-

effective techniques and ensuring an increased profit margin

This stage is followed by taking the necessary measures for ensuring that the newly

opened centres helps in providing increased earnings and contribute to positive

future growth

The last outcome can be seen with valuing the evidence-based medicine is in the

best way possible (Foley and Manova 2015)

Requirement iii:

Based on the depiction of the ABC system, the model can be widely implemented in

the manufacturing area however there are certain features which cannot be left unnoticed

especially in the healthcare sector. It has been identified that the healthcare service

provider is not seen to possess any DC, as an alternative the costs are segregated with

overhead expenses. Therefore, the adoption of such a costing method will allow the

company to enjoy some benefits which will fulfil the business objectives and strategies

(Warren and Jones 2018).

There are several systems in ABC which deals with resources and cost object of

sections. With particular reference to Integral Diagnostics Ltd, the resource section has been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

segregated several departments. Some of the most evident segmentations have been

shown as follows:

Selling channel like online portal and direct selling

Corporate office

Shared form of service departments like HR and IT

Call Centres

In order to compute the indirect cost, it is essential to explain the various dimensions of

shared services. It needs to be noted that the departmental service volumes are

considered with several departments. In addition to this, the varied nature of branches of

organisations is responsible for grouping the activities on which costs are dependent.

Henceforth, it can be stated that ABC is responsible for increasing overall scope for cost

assignment among all the branches due to which, the advertisement costs can be

predicted from beforehand (Edmonds et al. 2016).

The different types of cost object may be explained with business transactions and

operations which are relevant to the selected company in carrying out the selling

procedures. Due to this, the various perspective of organisation may be considered as

conducive in purchasing the wholesale equipment’s, service rendered to the customers

and order receipt. After the proper justification of transaction separation, ABC system is

duly implemented in the company’s accounting structure. After this stage, the naming of

the activities will be done by putting them against each other. This is considered with the

significant nature of that size and performing activities in batch mode. The several

considerations taken by ABC system as per departmental needs are based on group

activities. There is a system will be further conducive for the company in reducing the

segregated several departments. Some of the most evident segmentations have been

shown as follows:

Selling channel like online portal and direct selling

Corporate office

Shared form of service departments like HR and IT

Call Centres

In order to compute the indirect cost, it is essential to explain the various dimensions of

shared services. It needs to be noted that the departmental service volumes are

considered with several departments. In addition to this, the varied nature of branches of

organisations is responsible for grouping the activities on which costs are dependent.

Henceforth, it can be stated that ABC is responsible for increasing overall scope for cost

assignment among all the branches due to which, the advertisement costs can be

predicted from beforehand (Edmonds et al. 2016).

The different types of cost object may be explained with business transactions and

operations which are relevant to the selected company in carrying out the selling

procedures. Due to this, the various perspective of organisation may be considered as

conducive in purchasing the wholesale equipment’s, service rendered to the customers

and order receipt. After the proper justification of transaction separation, ABC system is

duly implemented in the company’s accounting structure. After this stage, the naming of

the activities will be done by putting them against each other. This is considered with the

significant nature of that size and performing activities in batch mode. The several

considerations taken by ABC system as per departmental needs are based on group

activities. There is a system will be further conducive for the company in reducing the

8MANAGERIAL ACCOUNTING

additional cost burden pertaining to the patients and implementation of innovative

technologies (Lu, Won and Cheng 2016).

In this system, it is feasible to separate the cost objects into two sections. The first

division of the cost object is related to calculate the additional cost incurred by the

patients for providing different services thereby including channels of distribution. This is

depicted in form of sale of radiology services and diagnostic imaging services. The

evaluation of the patients need to be several additional costs for various services. Despite

of these factors the cost should not be computed as per combination of radiology services

as opposed to the diagnostic imaging services. In case, it is a system is adopted it will be

able to assist in rendering service across two activities. Therefore, the organisations need

to develop a considerable aspect of brand awareness for ensuring competitive advantage

and business sustainability (Yildiz 2014).

Answer to Part c:

The company’s top-level hierarchy needs to extend its support in this particular case.

This is important for overall implementation of ABC. Once the approval is made, it is the

obligation of cross functional team develop and implement the modern rather than relying

on accounting department. By referring to the particular case, the team needs to be framed

comprising of unifying members from individual departments and using the data derived for

ABC system. In addition to this, the external specialists can be appointed for ensuring

successful enforcement of this system (Chugh 2016).

There have been certain rational to include the viewpoint of top management in

supporting the system. This is mainly due to the fact that the subordinates and managers

additional cost burden pertaining to the patients and implementation of innovative

technologies (Lu, Won and Cheng 2016).

In this system, it is feasible to separate the cost objects into two sections. The first

division of the cost object is related to calculate the additional cost incurred by the

patients for providing different services thereby including channels of distribution. This is

depicted in form of sale of radiology services and diagnostic imaging services. The

evaluation of the patients need to be several additional costs for various services. Despite

of these factors the cost should not be computed as per combination of radiology services

as opposed to the diagnostic imaging services. In case, it is a system is adopted it will be

able to assist in rendering service across two activities. Therefore, the organisations need

to develop a considerable aspect of brand awareness for ensuring competitive advantage

and business sustainability (Yildiz 2014).

Answer to Part c:

The company’s top-level hierarchy needs to extend its support in this particular case.

This is important for overall implementation of ABC. Once the approval is made, it is the

obligation of cross functional team develop and implement the modern rather than relying

on accounting department. By referring to the particular case, the team needs to be framed

comprising of unifying members from individual departments and using the data derived for

ABC system. In addition to this, the external specialists can be appointed for ensuring

successful enforcement of this system (Chugh 2016).

There have been certain rational to include the viewpoint of top management in

supporting the system. This is mainly due to the fact that the subordinates and managers

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

may not demonstrate sufficient interest in accepting to the change. In case the top

management is not able to support the change with an augmented effort then the adoption

of such a system may be unsuccessful. The second important aspect is seen with the fact

that employers may not understand the value of this system if the top management does

not support. In order to make sure that there is successful implementation of this costing

method, the management of Integral Diagnostics Ltd should take into consideration the

development of an in-depth knowledge about the present costing system which are

inherent within the organisation. Moreover, the cost allocation needs to be done in a

suitable way which will ensure that the role of cross functional teams is also worth

mentioning as much as it is important to mention the success of top management (Maelah

and Yadzid 2018).

Answer to Part d:

The important evaluations made in the model would be conducive in providing

immense benefit for the selected company if it implements this costing method. Despite of

this, several other management accounting tools are available which will be able to meet

the interest of organisation. Some of these tools include budgetary control method. This is

important as it can be of use benefit in conducting the planning of business processes from

beforehand. In addition to this, the managers of Integral Diagnostics Ltd will be having the

scope of utilising such a budgetary measure for controlling, monitoring and planning of

several activities which take place during the normal business course (Mohamed, Kerosi and

Tirimba 2016). There are different types of other benefits depicted with the budgetary

control method which needs to be understood as follows:

may not demonstrate sufficient interest in accepting to the change. In case the top

management is not able to support the change with an augmented effort then the adoption

of such a system may be unsuccessful. The second important aspect is seen with the fact

that employers may not understand the value of this system if the top management does

not support. In order to make sure that there is successful implementation of this costing

method, the management of Integral Diagnostics Ltd should take into consideration the

development of an in-depth knowledge about the present costing system which are

inherent within the organisation. Moreover, the cost allocation needs to be done in a

suitable way which will ensure that the role of cross functional teams is also worth

mentioning as much as it is important to mention the success of top management (Maelah

and Yadzid 2018).

Answer to Part d:

The important evaluations made in the model would be conducive in providing

immense benefit for the selected company if it implements this costing method. Despite of

this, several other management accounting tools are available which will be able to meet

the interest of organisation. Some of these tools include budgetary control method. This is

important as it can be of use benefit in conducting the planning of business processes from

beforehand. In addition to this, the managers of Integral Diagnostics Ltd will be having the

scope of utilising such a budgetary measure for controlling, monitoring and planning of

several activities which take place during the normal business course (Mohamed, Kerosi and

Tirimba 2016). There are different types of other benefits depicted with the budgetary

control method which needs to be understood as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

After the implementation of budgetary control, the management of the company is

more integrated in actions for fulfilment of common objectives. Furthermore, the

budgetary control ensures that synchronisation of activities will be conducive in

meeting the standards set along with the targets during the start of financial year.

The various types of budgetary control techniques are further conducive in

understanding the corrective actions in case the amount established for a particular

department during the beginning of the period is more than at the end of FY.

Some of the other help of budgetary control is depicted in terms of its easy knowing

about the previous events in which areas were committed. This allows information

to be re-evaluated and ensure that search stakes don’t reappear. Therefore, it needs

to be understood that the budgetary control is able to set for the appropriate

strategy for setting of the suitable strategy which will allow the company in dealing

with unexpected contingency and rectification of mistakes made in the past

(Gesimba, Alvar and Mante 2014)

Conclusion:

The study can be concluded by stating that the incorporation of ABC system

allows in terms of segregating the cost components in terms of variable cost and fixed cost.

In addition to this, based on this method, corporate entities are able to maintain a

sustaining a suitable system of costing thereby integrating all the essential information

related to costs. Distinctive characteristics of the cost behaviour patterns is evident with

ABC. The cost behaviour pattern is directly linked with volume, diversity and time. The main

requirement of the system is depicted in recognising the activity pool and cost drivers which

is conducive in tracing the overhead expenses. It can be further seen that the model can be

After the implementation of budgetary control, the management of the company is

more integrated in actions for fulfilment of common objectives. Furthermore, the

budgetary control ensures that synchronisation of activities will be conducive in

meeting the standards set along with the targets during the start of financial year.

The various types of budgetary control techniques are further conducive in

understanding the corrective actions in case the amount established for a particular

department during the beginning of the period is more than at the end of FY.

Some of the other help of budgetary control is depicted in terms of its easy knowing

about the previous events in which areas were committed. This allows information

to be re-evaluated and ensure that search stakes don’t reappear. Therefore, it needs

to be understood that the budgetary control is able to set for the appropriate

strategy for setting of the suitable strategy which will allow the company in dealing

with unexpected contingency and rectification of mistakes made in the past

(Gesimba, Alvar and Mante 2014)

Conclusion:

The study can be concluded by stating that the incorporation of ABC system

allows in terms of segregating the cost components in terms of variable cost and fixed cost.

In addition to this, based on this method, corporate entities are able to maintain a

sustaining a suitable system of costing thereby integrating all the essential information

related to costs. Distinctive characteristics of the cost behaviour patterns is evident with

ABC. The cost behaviour pattern is directly linked with volume, diversity and time. The main

requirement of the system is depicted in recognising the activity pool and cost drivers which

is conducive in tracing the overhead expenses. It can be further seen that the model can be

11MANAGERIAL ACCOUNTING

widely implemented in the manufacturing area however there are certain features which

cannot be left unnoticed especially in the healthcare sector. It has been identified that the

healthcare service provider is not seen to possess any DC, as an alternative the costs are

segregated with overhead expenses. Therefore, the adoption of such a costing method will

allow the company to enjoy some benefits which will fulfil the business objectives and

strategies.

widely implemented in the manufacturing area however there are certain features which

cannot be left unnoticed especially in the healthcare sector. It has been identified that the

healthcare service provider is not seen to possess any DC, as an alternative the costs are

segregated with overhead expenses. Therefore, the adoption of such a costing method will

allow the company to enjoy some benefits which will fulfil the business objectives and

strategies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.