HI5017 - Managerial Accounting: Master Budget, Approaches & Analysis

VerifiedAdded on 2023/05/26

|18

|4630

|99

Report

AI Summary

This report provides a comprehensive analysis of master budgeting in managerial accounting. It begins by describing the essential elements of a master budget, including the manufacturing overhead budget, production budget, sales budget, and cash budget, emphasizing their role in managing manufacturing, sales, profitability, and cash flow. The report then compares top-down and bottom-up budgeting approaches, relating them to ActivEX Limited, a Brisbane-based mining company, and discusses how these approaches impact budget projections. It also examines the differences between the budgeted income statement for 2019 and the actual income for 2018, offering assertions for these variances, highlighting increased expenses and cumulative losses. The report concludes that a top-down approach is suitable for ActivEX Limited due to its large aggregate estimations and the need for top management oversight in budgeting, while also noting the importance of considering day-to-day operational expenses.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary

The report has depicted several aspects of preparing a master budget. The initial discussions

include considering various elements in preparing master budget. This discourse is followed by

identifying the differences of top-down and bottom-up approach in the budget process and

relate the same with Brisbane-based mining and mineral resource explorer ActivEX Limited. The

overall discussions of the study will identify various types of changes pertaining to projections

within the budget of the company. The final section of the report has considered the

differences observed between the budgeted income statement prepared for the year 2019 and

actual budgeted income of 2018. The several types of assertions have stated about the

rationale for such difference. The findings show that the different elements in the master

budget is considered to be essential in managing the manufacturing and sales activities for

accompanying the profitability and cash flow goals. Moreover, as ActivEX Limited deals with

large aggregate while estimation of specific segments in a budget. It is essential that such a

nature of budgeting estimate is taken under the responsibility of the top management for

estimating the budget requirements in the necessary segments. The top-down budget

approach will be appropriate in knowing about the day to day expenses considered during the

mining operations. Additionally, the assertions made from table 2 the projected income is

identified with increasing amount of expenses leading to cumulative the loss before income tax

from $ -6,48,677 in 2018 to $ -6,61,529 in 2019.

Executive Summary

The report has depicted several aspects of preparing a master budget. The initial discussions

include considering various elements in preparing master budget. This discourse is followed by

identifying the differences of top-down and bottom-up approach in the budget process and

relate the same with Brisbane-based mining and mineral resource explorer ActivEX Limited. The

overall discussions of the study will identify various types of changes pertaining to projections

within the budget of the company. The final section of the report has considered the

differences observed between the budgeted income statement prepared for the year 2019 and

actual budgeted income of 2018. The several types of assertions have stated about the

rationale for such difference. The findings show that the different elements in the master

budget is considered to be essential in managing the manufacturing and sales activities for

accompanying the profitability and cash flow goals. Moreover, as ActivEX Limited deals with

large aggregate while estimation of specific segments in a budget. It is essential that such a

nature of budgeting estimate is taken under the responsibility of the top management for

estimating the budget requirements in the necessary segments. The top-down budget

approach will be appropriate in knowing about the day to day expenses considered during the

mining operations. Additionally, the assertions made from table 2 the projected income is

identified with increasing amount of expenses leading to cumulative the loss before income tax

from $ -6,48,677 in 2018 to $ -6,61,529 in 2019.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction.........................................................................................................................3

a. Description of the elements in the Master Budget.........................................................3

b. A discourse on comparison of top-down and bottom-up approach to the budget

process and reason for application of the same in chosen company.............................................8

c. Budgeted income statement 2019................................................................................10

d. Opinion on the comparison of Budgeted Income Statement and actual statement....11

Conclusion..........................................................................................................................14

References.........................................................................................................................15

Table of Contents

Introduction.........................................................................................................................3

a. Description of the elements in the Master Budget.........................................................3

b. A discourse on comparison of top-down and bottom-up approach to the budget

process and reason for application of the same in chosen company.............................................8

c. Budgeted income statement 2019................................................................................10

d. Opinion on the comparison of Budgeted Income Statement and actual statement....11

Conclusion..........................................................................................................................14

References.........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction

The learnings of the report have been seen with covering several aspects of preparing a

master budget. In the first section the discussions are relevant with considering various

elements of the master budget. The second segment of the study is evaluated on the

differences of top-down and bottom-up approach in the budget process and relate the same

with Brisbane-based mineral resource explorer ActivEX Limited. The overall discussions of the

study will identify various types of changes pertaining to projections within the budget of the

company. The initial study is considered the growth in sales projection with 10%. Subsequently,

the growth in cost of goods sold and be identified as 8%, along with growth in expenses of 2%.

The final section of the report has considered the differences observed between the budgeted

income statement prepared for the year 2019 and actual budgeted income of 2018. The several

types of assertions have stated about the rationale for such difference (Barr & McClellan, 2018).

a. Description of the elements in the Master Budget

The preparation of master budget begins with aggregating the budget produced in a

lower level hierarchy by consideration of various types of functional areas such as finance plan,

cash forecast and budgeted financial statement. The different elements in the master budget is

considered to be essential in managing the manufacturing and sales activities for accompanying

the profitability and cash flow goals. The preparation of a master budget should be based on a

careful coordination of smaller budgets thereby covering all segments of an organisation so

that it is able to provide a realistic information (Zietlow et al., 2018).

In general, the segregation of master budget can be done with either monthly or

quarterly basis in a financial year. The explanation of master budget can be identified with

Introduction

The learnings of the report have been seen with covering several aspects of preparing a

master budget. In the first section the discussions are relevant with considering various

elements of the master budget. The second segment of the study is evaluated on the

differences of top-down and bottom-up approach in the budget process and relate the same

with Brisbane-based mineral resource explorer ActivEX Limited. The overall discussions of the

study will identify various types of changes pertaining to projections within the budget of the

company. The initial study is considered the growth in sales projection with 10%. Subsequently,

the growth in cost of goods sold and be identified as 8%, along with growth in expenses of 2%.

The final section of the report has considered the differences observed between the budgeted

income statement prepared for the year 2019 and actual budgeted income of 2018. The several

types of assertions have stated about the rationale for such difference (Barr & McClellan, 2018).

a. Description of the elements in the Master Budget

The preparation of master budget begins with aggregating the budget produced in a

lower level hierarchy by consideration of various types of functional areas such as finance plan,

cash forecast and budgeted financial statement. The different elements in the master budget is

considered to be essential in managing the manufacturing and sales activities for accompanying

the profitability and cash flow goals. The preparation of a master budget should be based on a

careful coordination of smaller budgets thereby covering all segments of an organisation so

that it is able to provide a realistic information (Zietlow et al., 2018).

In general, the segregation of master budget can be done with either monthly or

quarterly basis in a financial year. The explanation of master budget can be identified with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

assisting necessary goals for achieving the management actions and also following up with the

strategy directions of the company. Moreover, the master budget is seen to include a

significant discussion about changes in activities for achieving a certain budgetary goal (Kaplan

& Atkinson, 2015).

Therefore, master budget is regarded as the primal tool for directing the activities and at

the same time identifying the performance responsibility factors of the corporation. It is

customary for the higher management for reviewing several types of iterations and

incorporation which is based on inferring a certain anticipated result. The companies seem to

use such a budget process to arrive at any decision as per consultation with the senior

management and taking reliable input from employees (Burtonshaw-Gunn, S2017). Some of the

main elements of the master budget are listed as follows:

1. “Manufacturing overhead budget”

2. “Production budget”

3. “Sales budget”

4. “Selling and administrative expense budget”

5. “Cash budget”

6. “Direct labour budget”

7. “Direct materials budget”

8. “Ending finished goods budget”

It can be said that cash budget is associated with identification of expected

disbursement related to cash receipt in a certain time period. The cash but it is inclusive of cash

outflows and cash inflows such as expenses, payments, receipts and revenue collected. In

assisting necessary goals for achieving the management actions and also following up with the

strategy directions of the company. Moreover, the master budget is seen to include a

significant discussion about changes in activities for achieving a certain budgetary goal (Kaplan

& Atkinson, 2015).

Therefore, master budget is regarded as the primal tool for directing the activities and at

the same time identifying the performance responsibility factors of the corporation. It is

customary for the higher management for reviewing several types of iterations and

incorporation which is based on inferring a certain anticipated result. The companies seem to

use such a budget process to arrive at any decision as per consultation with the senior

management and taking reliable input from employees (Burtonshaw-Gunn, S2017). Some of the

main elements of the master budget are listed as follows:

1. “Manufacturing overhead budget”

2. “Production budget”

3. “Sales budget”

4. “Selling and administrative expense budget”

5. “Cash budget”

6. “Direct labour budget”

7. “Direct materials budget”

8. “Ending finished goods budget”

It can be said that cash budget is associated with identification of expected

disbursement related to cash receipt in a certain time period. The cash but it is inclusive of cash

outflows and cash inflows such as expenses, payments, receipts and revenue collected. In

5MANAGERIAL ACCOUNTING

addition to this, such a budget acts as the estimate of position of cash in the future for any

organisation. The management team is concerned to develop such a budgeting technique after

the purchases, sales and expenditures are already allocated. This type of budget is also

conducive in showing accurate information of how the cash may be affected in a certain

financial year. For example, cash budget can be used by the management for estimation of

overall cash pertaining to sail sales which can be collected in a particular year (Alviniussen &

Jankensgard, 2015).

Direct labour budget is an important estimation for direct labour hours which is

required for producing a particular item within the production budget. In several instances, the

direct labour budget is able to provide important information about segregation of each

category of the labour costs. Therefore, this type of budget is useful for estimating the total

number of employees essential for manufacturing a particular product along with the cost

segregation. Direct labour budget is also important for the management in evaluating the needs

related to hiring, scheduling and layoffs. Typically, this type of budget is able to provide an

aggregate level of information of cost which is essential for hiring and layoff requirements. This

type of budget information can be published both on quarterly and monthly basis (Dudin et al.,

2015).

Direct material budget acts as estimation of total materials which is to be purchased in

a given period of time for fulfilment of the necessary requirements of the production budget. In

general, this information can be produced in both monthly or quarterly format in the master

budget. A business which is involved in selling products, this type of budget may be conducive

for noting down all the costs which are incurred in a particular financial year. The basic

computation of such a budget includes summation of raw materials and planned ending

addition to this, such a budget acts as the estimate of position of cash in the future for any

organisation. The management team is concerned to develop such a budgeting technique after

the purchases, sales and expenditures are already allocated. This type of budget is also

conducive in showing accurate information of how the cash may be affected in a certain

financial year. For example, cash budget can be used by the management for estimation of

overall cash pertaining to sail sales which can be collected in a particular year (Alviniussen &

Jankensgard, 2015).

Direct labour budget is an important estimation for direct labour hours which is

required for producing a particular item within the production budget. In several instances, the

direct labour budget is able to provide important information about segregation of each

category of the labour costs. Therefore, this type of budget is useful for estimating the total

number of employees essential for manufacturing a particular product along with the cost

segregation. Direct labour budget is also important for the management in evaluating the needs

related to hiring, scheduling and layoffs. Typically, this type of budget is able to provide an

aggregate level of information of cost which is essential for hiring and layoff requirements. This

type of budget information can be published both on quarterly and monthly basis (Dudin et al.,

2015).

Direct material budget acts as estimation of total materials which is to be purchased in

a given period of time for fulfilment of the necessary requirements of the production budget. In

general, this information can be produced in both monthly or quarterly format in the master

budget. A business which is involved in selling products, this type of budget may be conducive

for noting down all the costs which are incurred in a particular financial year. The basic

computation of such a budget includes summation of raw materials and planned ending

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

inventory balance thereby subtracting the previous year’s raw material inventory (McKinney,

2015).

Ending finished goods inventory budget is conducive in determining the cost which is

needed for manufacturing finished goods at the end of each budgeting period. However, it is

important to understand that ending finished goods inventory budget also includes necessary

estimation for total unit of the finished goods quantity which is displayed at the closing of each

budgeting period. The main source of information pertaining to this type of budget is seen with

production information. The use of such a budget is important for estimating the total amount

of cash which is to be invested in the assets. For instance, in estimation of cost of machine for

such a budget film include overallocation, direct material and direct labour as well (Martin,

2016).

The segregation of selling and administrative budget is seen with including the

expenses for the individual departments such as facilities, counting and engineering. It can be

said that this type of budget includes ending inventory for estimating the carrying value which

is referred as the closing balance of the finished goods which was used as the previous years

beginning inventory. This balance is used for the current year. The final value for such a budget

is arrived by subtracting the cost from the goods sold with total goods which is to be sold (Van

Dooren, Bouckaert & Halligan, 2015).

The manufacturing overhead budget considered the necessary cost for manufacturing

excluding the total cost for direct labour and direct material. This type of budget is essential in

fetching the necessary information about manufacturing items which is considered as a

essential part of cost of goods sold (Menifield, 2017).

inventory balance thereby subtracting the previous year’s raw material inventory (McKinney,

2015).

Ending finished goods inventory budget is conducive in determining the cost which is

needed for manufacturing finished goods at the end of each budgeting period. However, it is

important to understand that ending finished goods inventory budget also includes necessary

estimation for total unit of the finished goods quantity which is displayed at the closing of each

budgeting period. The main source of information pertaining to this type of budget is seen with

production information. The use of such a budget is important for estimating the total amount

of cash which is to be invested in the assets. For instance, in estimation of cost of machine for

such a budget film include overallocation, direct material and direct labour as well (Martin,

2016).

The segregation of selling and administrative budget is seen with including the

expenses for the individual departments such as facilities, counting and engineering. It can be

said that this type of budget includes ending inventory for estimating the carrying value which

is referred as the closing balance of the finished goods which was used as the previous years

beginning inventory. This balance is used for the current year. The final value for such a budget

is arrived by subtracting the cost from the goods sold with total goods which is to be sold (Van

Dooren, Bouckaert & Halligan, 2015).

The manufacturing overhead budget considered the necessary cost for manufacturing

excluding the total cost for direct labour and direct material. This type of budget is essential in

fetching the necessary information about manufacturing items which is considered as a

essential part of cost of goods sold (Menifield, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

The production budget is considered as conducive in estimating the total number of

units which are needed to be manufactured along with combination of sales forecast including

planning of finished goods inventory. The necessary considerations for production budget are

seen with including the necessary elements of push manufacturing system which are important

in depicting the necessary military requirement and planning environment. In general, the

production budget is produced both annually and quarterly. The management uses such

information for setting the corporate goals and predicting future production requirements

(Bryce, 2017).

After completion of preparing master budget, the details of individual budget

information are entered into the accounting software for the progression of final financial

reports and comparing the budgeted to do with actual results. After proceeding with creating

master budget, the accounting staff may consider to enter the relevant results into accounting

software for issuing an in-depth analysis of future budget predictions and comparing the same

with previous budget (Matthew, 2017). A significant nature of the smaller corporations often

considers preparing the master budget with use of accounting software such as electronic

spreadsheet. However, it needs to be noted that such a spreadsheet is also prone to consist of

errors in the formula which may result in giving inaccurate information in the budgeted report.

On the other hand, the big corporations are more likely to implement a budget specific solution

to not only avoid any hindrance in producing budgeted balance sheet but also obtain

continuous support from the software vendor (Maxwell et al., 2015).

The budgets prepared at the lower level needs to follow a relevant format for

consideration of a certain outcome which is associated to using apps of costing of finished

goods inventory and several numbers of other considerations related to preparing the final

The production budget is considered as conducive in estimating the total number of

units which are needed to be manufactured along with combination of sales forecast including

planning of finished goods inventory. The necessary considerations for production budget are

seen with including the necessary elements of push manufacturing system which are important

in depicting the necessary military requirement and planning environment. In general, the

production budget is produced both annually and quarterly. The management uses such

information for setting the corporate goals and predicting future production requirements

(Bryce, 2017).

After completion of preparing master budget, the details of individual budget

information are entered into the accounting software for the progression of final financial

reports and comparing the budgeted to do with actual results. After proceeding with creating

master budget, the accounting staff may consider to enter the relevant results into accounting

software for issuing an in-depth analysis of future budget predictions and comparing the same

with previous budget (Matthew, 2017). A significant nature of the smaller corporations often

considers preparing the master budget with use of accounting software such as electronic

spreadsheet. However, it needs to be noted that such a spreadsheet is also prone to consist of

errors in the formula which may result in giving inaccurate information in the budgeted report.

On the other hand, the big corporations are more likely to implement a budget specific solution

to not only avoid any hindrance in producing budgeted balance sheet but also obtain

continuous support from the software vendor (Maxwell et al., 2015).

The budgets prepared at the lower level needs to follow a relevant format for

consideration of a certain outcome which is associated to using apps of costing of finished

goods inventory and several numbers of other considerations related to preparing the final

8MANAGERIAL ACCOUNTING

budget. It is to be seen that the master budget consists of the income statement and balance

sheet as per the relevant accounting standard. The significant differences following the cash

budget can be inferred with standard format maintained under the statement of cash flows.

Despite of this, it is regarded to be a more practical decision for identifying specific inflows and

outflows of cash which is a result of the overall budgeted model (Bekaert & Hodrick, 2017).

b. A discourse on comparison of top-down and bottom-up approach to the budget process

and reason for application of the same in chosen company

The top-down budgeting approach is considered as setting the overall spending on the

higher side based on aggregate of the total cost which is spent by the company on individual

line items. On the contrary, the bottom-up approach is considered more with the contributions

made by the individual departments pertaining to reporting units for preparing personal

spending wish list and allocating the individual items of expenses. The general consideration of

bottom-up approach can be depicted with setting higher spending targets which is focused with

comparing the top-down approach. Henceforth, it is essential to use such an approach to

reconcile the process of production and company using this information to equal the entire

budget (Karadag, 2015).

The top-down budgeting approach is however considered with senior management to

develop a high-level budget pertaining to the entire entity. The completion of such a budget

shows that the individual amounts are depicted in relevant departments which are to be

considered with certain numbers and build the corresponding budgets confined within the

executive budget creation. In the bottom-up approach the process of budgeting starts when the

department individually create any budgeting information and forwards a same to the higher

budget. It is to be seen that the master budget consists of the income statement and balance

sheet as per the relevant accounting standard. The significant differences following the cash

budget can be inferred with standard format maintained under the statement of cash flows.

Despite of this, it is regarded to be a more practical decision for identifying specific inflows and

outflows of cash which is a result of the overall budgeted model (Bekaert & Hodrick, 2017).

b. A discourse on comparison of top-down and bottom-up approach to the budget process

and reason for application of the same in chosen company

The top-down budgeting approach is considered as setting the overall spending on the

higher side based on aggregate of the total cost which is spent by the company on individual

line items. On the contrary, the bottom-up approach is considered more with the contributions

made by the individual departments pertaining to reporting units for preparing personal

spending wish list and allocating the individual items of expenses. The general consideration of

bottom-up approach can be depicted with setting higher spending targets which is focused with

comparing the top-down approach. Henceforth, it is essential to use such an approach to

reconcile the process of production and company using this information to equal the entire

budget (Karadag, 2015).

The top-down budgeting approach is however considered with senior management to

develop a high-level budget pertaining to the entire entity. The completion of such a budget

shows that the individual amounts are depicted in relevant departments which are to be

considered with certain numbers and build the corresponding budgets confined within the

executive budget creation. In the bottom-up approach the process of budgeting starts when the

department individually create any budgeting information and forwards a same to the higher

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

management. After this the budget is revised and approved with the relevant department

(Chohan & Jacobs, 2017).

A more vivid comparison of both top-down budget and bottom-up budget identifies that

there can be a greater potential for top-down budget for ensuring accuracy in the larger

organisations. On the contrary, bottom-up budget approach may involve several inaccuracies in

estimating results based on large totals. The analysis pertaining to both budgeting

consideration shows that ActivEX Limited is mainly focused to succeed as a profitable

exploration and mining entity. The extensive portfolio of the company includes granted mining

lease in Western Australia and granted exploration permits for minerals in Queensland. Can be

further saying that the company is successful in maintaining an advanced potash project in

Western Australia by investing in optimal methods for leaching and extraction of potash and by-

products. ActivEX Limited aims to pursue quality restoration development opportunities with

increasing up side values (Osadchy & Akhmetshin, 2015).

Therefore, it can be seen that the company deals with large aggregate while estimation

of specific segments in a budget. It is essential that such a nature of budgeting estimate is taken

under the responsibility of the top management for estimating the budget requirements in the

necessary segments. The top-down budget approach will be appropriate in knowing about the

day to day expenses considered during the mining operations. As a result of this, the top-down

approach of budgeting will be essential in improving the overall budget estimates as it will

require allocating higher cost for the individual segment which is essential for any mining

operation. Therefore, despite of involving large aggregate it can be seen that the company is

consistent with several segments such as mineral exploration, mining, extracting and producing.

management. After this the budget is revised and approved with the relevant department

(Chohan & Jacobs, 2017).

A more vivid comparison of both top-down budget and bottom-up budget identifies that

there can be a greater potential for top-down budget for ensuring accuracy in the larger

organisations. On the contrary, bottom-up budget approach may involve several inaccuracies in

estimating results based on large totals. The analysis pertaining to both budgeting

consideration shows that ActivEX Limited is mainly focused to succeed as a profitable

exploration and mining entity. The extensive portfolio of the company includes granted mining

lease in Western Australia and granted exploration permits for minerals in Queensland. Can be

further saying that the company is successful in maintaining an advanced potash project in

Western Australia by investing in optimal methods for leaching and extraction of potash and by-

products. ActivEX Limited aims to pursue quality restoration development opportunities with

increasing up side values (Osadchy & Akhmetshin, 2015).

Therefore, it can be seen that the company deals with large aggregate while estimation

of specific segments in a budget. It is essential that such a nature of budgeting estimate is taken

under the responsibility of the top management for estimating the budget requirements in the

necessary segments. The top-down budget approach will be appropriate in knowing about the

day to day expenses considered during the mining operations. As a result of this, the top-down

approach of budgeting will be essential in improving the overall budget estimates as it will

require allocating higher cost for the individual segment which is essential for any mining

operation. Therefore, despite of involving large aggregate it can be seen that the company is

consistent with several segments such as mineral exploration, mining, extracting and producing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Therefore, the individual costs are different for each segment. It top-down approach will be

conducive in ensuring the accuracy of such an estimate (Ahrens & Ferry, 2015).

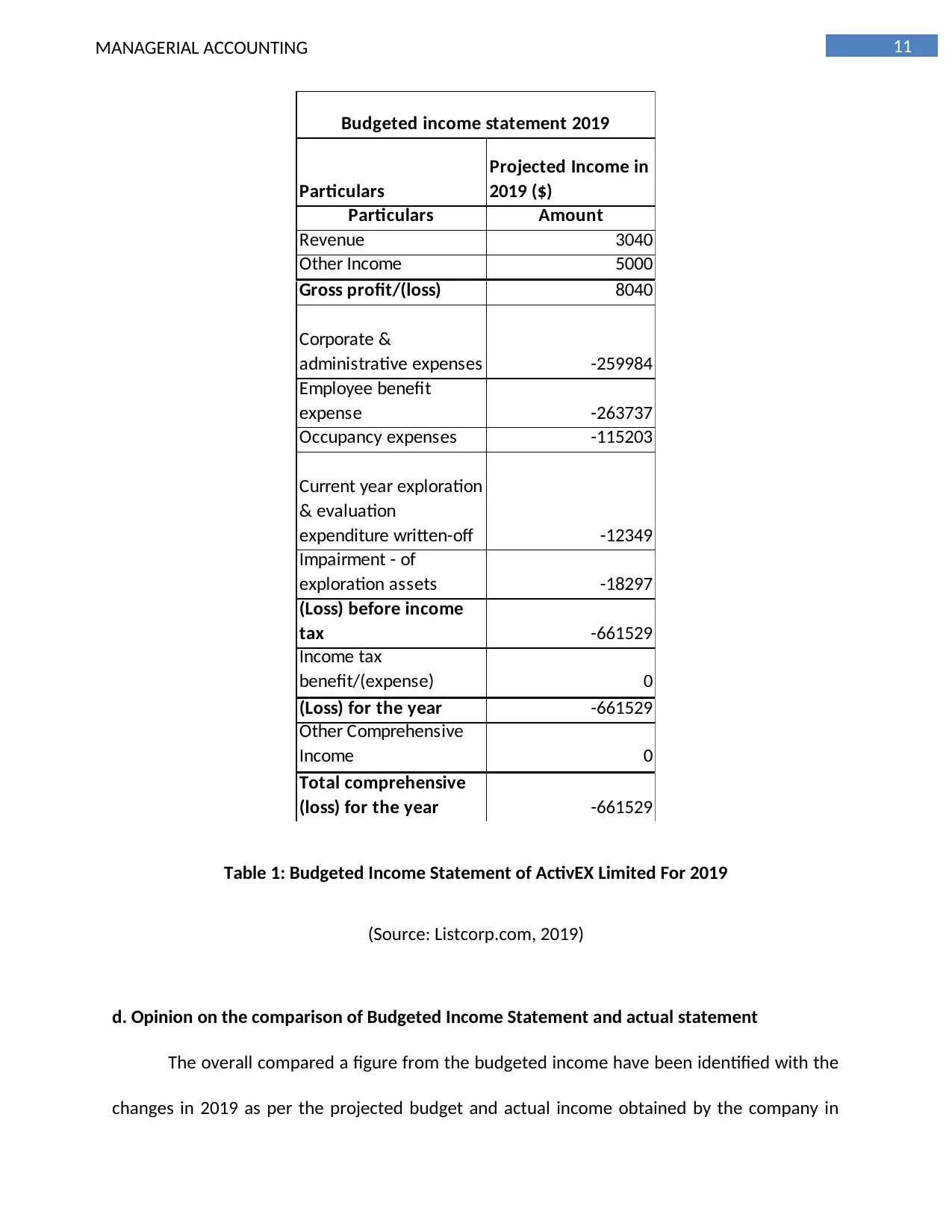

c. Budgeted income statement 2019

The necessary considerations in the budgeted income statement 2019 has been focused

with cost of goods sold, revenue and expenses. The alterations with the revenue are seen with

a projected change of 10% based on the actual income in 2018. In a similar manner the changes

pertaining to cost of goods sold is identified with 8% increase in the overall value in compared

to 2018. In a similar manner, the expenses are projected with an additional increase of 2%

based on the actual expenses incurred in 2018. As there has been no change in other income,

the gross profit in the projected income statement of the company increased from $ 7764 in

2018 to $ 8040 in 2019. It is to be also seen that as the company is based on exploration

projects it does not have any cost of goods sold or cost of sales. Therefore, it is excluded from

the master budget. The consideration of main expenses in the income statement can be

identified with items such as “Corporate & administrative expenses Employee benefit

expense”, “Occupancy expenses”, “Current year exploration & evaluation expenditure

written-off” and “Impairment - of exploration assets”. It can be clearly evident that as the

projected income is identified with increasing amount of expenses, the loss before income tax

has significantly increased from $ -6,48,677 in 2018 to $ -6,61,529 in 2019. In addition to this,

the overall comprehensive loss in the year has similarly increased. Based on the depictions

made in table 1 it can be stated that the change in budget projections have only contributed

positively towards Ross profit. However, due to increasing amount of expenses that of the

comprehensive loss for the year has increased (Ebdon & Franklin, 2015).

Therefore, the individual costs are different for each segment. It top-down approach will be

conducive in ensuring the accuracy of such an estimate (Ahrens & Ferry, 2015).

c. Budgeted income statement 2019

The necessary considerations in the budgeted income statement 2019 has been focused

with cost of goods sold, revenue and expenses. The alterations with the revenue are seen with

a projected change of 10% based on the actual income in 2018. In a similar manner the changes

pertaining to cost of goods sold is identified with 8% increase in the overall value in compared

to 2018. In a similar manner, the expenses are projected with an additional increase of 2%

based on the actual expenses incurred in 2018. As there has been no change in other income,

the gross profit in the projected income statement of the company increased from $ 7764 in

2018 to $ 8040 in 2019. It is to be also seen that as the company is based on exploration

projects it does not have any cost of goods sold or cost of sales. Therefore, it is excluded from

the master budget. The consideration of main expenses in the income statement can be

identified with items such as “Corporate & administrative expenses Employee benefit

expense”, “Occupancy expenses”, “Current year exploration & evaluation expenditure

written-off” and “Impairment - of exploration assets”. It can be clearly evident that as the

projected income is identified with increasing amount of expenses, the loss before income tax

has significantly increased from $ -6,48,677 in 2018 to $ -6,61,529 in 2019. In addition to this,

the overall comprehensive loss in the year has similarly increased. Based on the depictions

made in table 1 it can be stated that the change in budget projections have only contributed

positively towards Ross profit. However, due to increasing amount of expenses that of the

comprehensive loss for the year has increased (Ebdon & Franklin, 2015).

11MANAGERIAL ACCOUNTING

Particulars

Projected Income in

2019 ($)

Particulars Amount

Revenue 3040

Other Income 5000

Gross profit/(loss) 8040

Corporate &

administrative expenses -259984

Employee benefit

expense -263737

Occupancy expenses -115203

Current year exploration

& evaluation

expenditure written-off -12349

Impairment - of

exploration assets -18297

(Loss) before income

tax -661529

Income tax

benefit/(expense) 0

(Loss) for the year -661529

Other Comprehensive

Income 0

Total comprehensive

(loss) for the year -661529

Budgeted income statement 2019

Table 1: Budgeted Income Statement of ActivEX Limited For 2019

(Source: Listcorp.com, 2019)

d. Opinion on the comparison of Budgeted Income Statement and actual statement

The overall compared a figure from the budgeted income have been identified with the

changes in 2019 as per the projected budget and actual income obtained by the company in

Particulars

Projected Income in

2019 ($)

Particulars Amount

Revenue 3040

Other Income 5000

Gross profit/(loss) 8040

Corporate &

administrative expenses -259984

Employee benefit

expense -263737

Occupancy expenses -115203

Current year exploration

& evaluation

expenditure written-off -12349

Impairment - of

exploration assets -18297

(Loss) before income

tax -661529

Income tax

benefit/(expense) 0

(Loss) for the year -661529

Other Comprehensive

Income 0

Total comprehensive

(loss) for the year -661529

Budgeted income statement 2019

Table 1: Budgeted Income Statement of ActivEX Limited For 2019

(Source: Listcorp.com, 2019)

d. Opinion on the comparison of Budgeted Income Statement and actual statement

The overall compared a figure from the budgeted income have been identified with the

changes in 2019 as per the projected budget and actual income obtained by the company in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.