HI5017 Managerial Accounting: Activity-Based Costing Implementation

VerifiedAdded on 2023/06/04

|19

|3911

|392

Report

AI Summary

This report delves into activity-based costing (ABC) as a managerial accounting tool, analyzing its application in real-world scenarios. It examines two studies: one focusing on Nestle Bangladesh's implementation of ABC and another on its use in a Turkish private hospital's gynecology department. The report discusses the advantages of ABC, including accurate product costing, better cost behavior understanding, and improved cost information. It compares and contrasts the findings of the two studies, highlighting similarities in enhanced operational performance and cost-effective service delivery, while noting differences in geographical scope and product diversity. Ultimately, the report aims to provide insights for Australian companies considering implementing an ABC system, drawing lessons from both manufacturing and healthcare contexts. Desklib offers a wealth of similar assignments and study resources for students.

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 1

Executive Summary

The management accounting is the provision that is related to the financial data and advice to the

company for making use of accounting tools that mainly include budgeting, activity-based

costing and others. These tools are essential to be used in the organization for the development of

business. The rise in the competition is not allowing the company to conduct the business

activities without the activity-based costing method. The report includes the description related

to the two studies that is based on the real-life manufacturing and healthcare business. The

analysis of the selected studies has been done which include purpose, similarities and differences

with the outcomes. Further, the findings of the studies reflect the outcomes that help the

Australian companies in implementing an ABC system in their business organisation.

Executive Summary

The management accounting is the provision that is related to the financial data and advice to the

company for making use of accounting tools that mainly include budgeting, activity-based

costing and others. These tools are essential to be used in the organization for the development of

business. The rise in the competition is not allowing the company to conduct the business

activities without the activity-based costing method. The report includes the description related

to the two studies that is based on the real-life manufacturing and healthcare business. The

analysis of the selected studies has been done which include purpose, similarities and differences

with the outcomes. Further, the findings of the studies reflect the outcomes that help the

Australian companies in implementing an ABC system in their business organisation.

Managerial Accounting 2

Contents

Introduction......................................................................................................................................3

Explanation of activity-based costing..............................................................................................4

Advantages of Activity-based costing method............................................................................6

Accurate product cost..............................................................................................................6

Information for the cost behaviour..........................................................................................7

Cost information......................................................................................................................7

Explanation of the purpose of the two studies.................................................................................8

Similarities and differences in the findings of the two studies........................................................9

Similarities in findings of both the studies..................................................................................9

Differences in the findings of both the studies..........................................................................10

Outcomes from the two studies.....................................................................................................11

Article 1.....................................................................................................................................11

Article 2.....................................................................................................................................12

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Contents

Introduction......................................................................................................................................3

Explanation of activity-based costing..............................................................................................4

Advantages of Activity-based costing method............................................................................6

Accurate product cost..............................................................................................................6

Information for the cost behaviour..........................................................................................7

Cost information......................................................................................................................7

Explanation of the purpose of the two studies.................................................................................8

Similarities and differences in the findings of the two studies........................................................9

Similarities in findings of both the studies..................................................................................9

Differences in the findings of both the studies..........................................................................10

Outcomes from the two studies.....................................................................................................11

Article 1.....................................................................................................................................11

Article 2.....................................................................................................................................12

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 3

Introduction

The report is based on one of the topics of the management accounting. The management

accounting topics are activity-based costing (ABC), budgeting, standard costing and many

others. The topic that has been selected for this report is Activity-based costing. Activity-based

costing is one of the important tools that are used by the real-life organisations. The aim of the

report is to explore the findings from the literature research from the selected studies. The studies

that have been selected include Article 1- Activity-Based Costing (ABC) – An Effective Tool for

Better Management and Article 2- The Excellence of Activity-Based Costing in Cost

Calculation: Case Study of A Private Hospital in Turkey.

Further, the details related to the management accounting topic has been discussed. In addition,

the explanation of the two studies, the research question and the similarities and differences in

the findings of the two studies are discussed in the report. In the end, the specific outcomes or

lessons learned from the two studies are discussed. These findings will further provide the

benefits to the Australian companies who are making use of the Activity-based costing

management accounting tool in their business operations.

Introduction

The report is based on one of the topics of the management accounting. The management

accounting topics are activity-based costing (ABC), budgeting, standard costing and many

others. The topic that has been selected for this report is Activity-based costing. Activity-based

costing is one of the important tools that are used by the real-life organisations. The aim of the

report is to explore the findings from the literature research from the selected studies. The studies

that have been selected include Article 1- Activity-Based Costing (ABC) – An Effective Tool for

Better Management and Article 2- The Excellence of Activity-Based Costing in Cost

Calculation: Case Study of A Private Hospital in Turkey.

Further, the details related to the management accounting topic has been discussed. In addition,

the explanation of the two studies, the research question and the similarities and differences in

the findings of the two studies are discussed in the report. In the end, the specific outcomes or

lessons learned from the two studies are discussed. These findings will further provide the

benefits to the Australian companies who are making use of the Activity-based costing

management accounting tool in their business operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 4

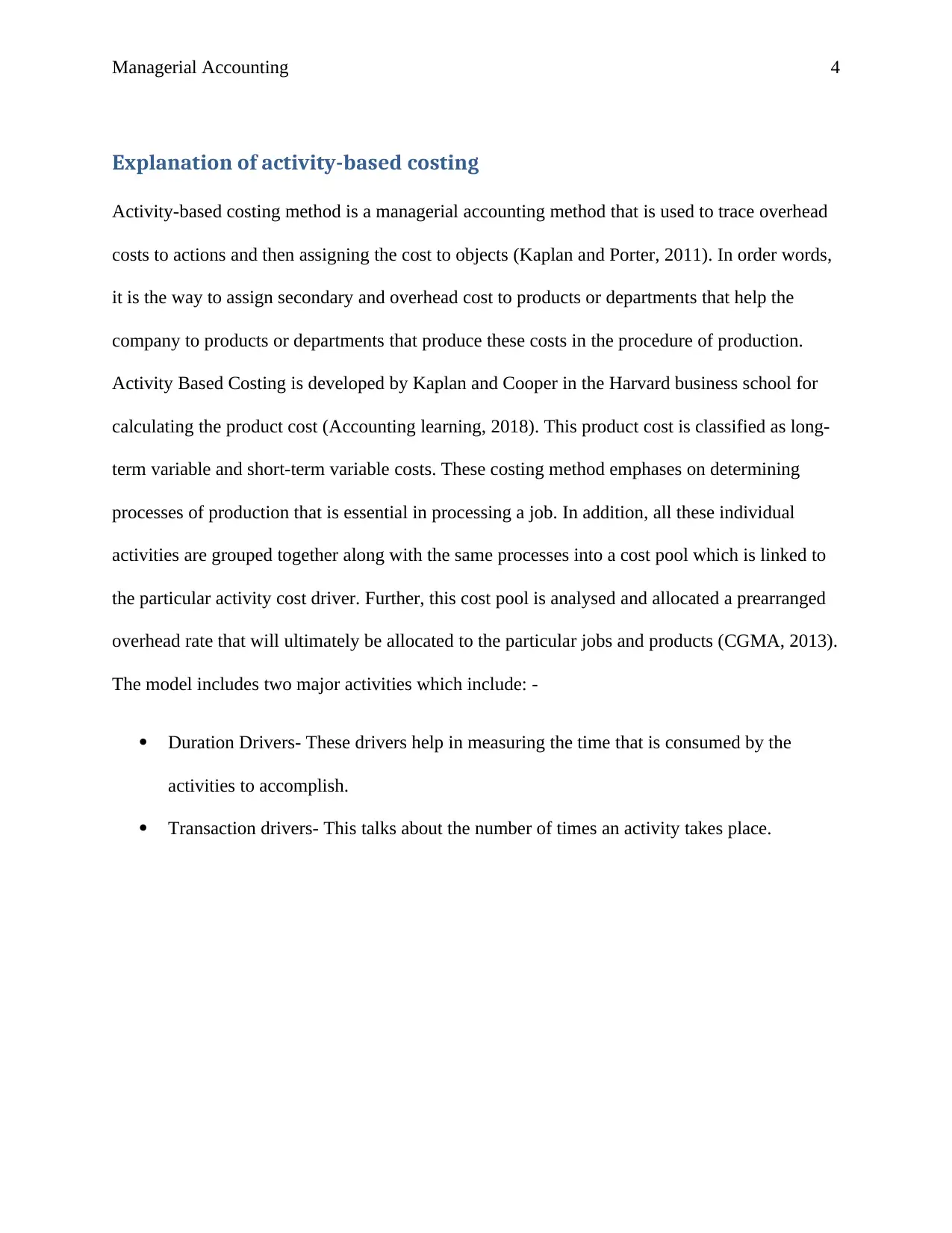

Explanation of activity-based costing

Activity-based costing method is a managerial accounting method that is used to trace overhead

costs to actions and then assigning the cost to objects (Kaplan and Porter, 2011). In order words,

it is the way to assign secondary and overhead cost to products or departments that help the

company to products or departments that produce these costs in the procedure of production.

Activity Based Costing is developed by Kaplan and Cooper in the Harvard business school for

calculating the product cost (Accounting learning, 2018). This product cost is classified as long-

term variable and short-term variable costs. These costing method emphases on determining

processes of production that is essential in processing a job. In addition, all these individual

activities are grouped together along with the same processes into a cost pool which is linked to

the particular activity cost driver. Further, this cost pool is analysed and allocated a prearranged

overhead rate that will ultimately be allocated to the particular jobs and products (CGMA, 2013).

The model includes two major activities which include: -

Duration Drivers- These drivers help in measuring the time that is consumed by the

activities to accomplish.

Transaction drivers- This talks about the number of times an activity takes place.

Explanation of activity-based costing

Activity-based costing method is a managerial accounting method that is used to trace overhead

costs to actions and then assigning the cost to objects (Kaplan and Porter, 2011). In order words,

it is the way to assign secondary and overhead cost to products or departments that help the

company to products or departments that produce these costs in the procedure of production.

Activity Based Costing is developed by Kaplan and Cooper in the Harvard business school for

calculating the product cost (Accounting learning, 2018). This product cost is classified as long-

term variable and short-term variable costs. These costing method emphases on determining

processes of production that is essential in processing a job. In addition, all these individual

activities are grouped together along with the same processes into a cost pool which is linked to

the particular activity cost driver. Further, this cost pool is analysed and allocated a prearranged

overhead rate that will ultimately be allocated to the particular jobs and products (CGMA, 2013).

The model includes two major activities which include: -

Duration Drivers- These drivers help in measuring the time that is consumed by the

activities to accomplish.

Transaction drivers- This talks about the number of times an activity takes place.

Managerial Accounting 5

(Source: CGMA, 2013)

In addition, activity based costing is an accounting technique that helps in determining assigned

cost to the overhead activities and then assigns a cost to the products. These management

accounting tools are used to determine the relationship between the cost, overhead activities and

manufacturing the products. The method follows the same relationship which is used by them to

assign the indirect cost to the products. Though, this is true that it has been found that there are

some costs in a business that is hard to be assigned with the help of the cost accounting

(Accounting tools, 2017). The indirect cost includes management and office staff salaries which

are hard to allocate to a product due to which this method has found its niche in the sector of

manufacturing.

This analysis shows that Activity-based costing is majorly used by the companies in the field of

manufacturing the products as it improves the reliability of cost data (Schulze, Seuring, and

Ewering, 2012). Thus, this contributes to produce true costs and better classifying cost of the

(Source: CGMA, 2013)

In addition, activity based costing is an accounting technique that helps in determining assigned

cost to the overhead activities and then assigns a cost to the products. These management

accounting tools are used to determine the relationship between the cost, overhead activities and

manufacturing the products. The method follows the same relationship which is used by them to

assign the indirect cost to the products. Though, this is true that it has been found that there are

some costs in a business that is hard to be assigned with the help of the cost accounting

(Accounting tools, 2017). The indirect cost includes management and office staff salaries which

are hard to allocate to a product due to which this method has found its niche in the sector of

manufacturing.

This analysis shows that Activity-based costing is majorly used by the companies in the field of

manufacturing the products as it improves the reliability of cost data (Schulze, Seuring, and

Ewering, 2012). Thus, this contributes to produce true costs and better classifying cost of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 6

company at the time of the production process. This is found that with the rise in the competition

the use of the activity-based costing method is used by the several companies that fall under the

different industries. These industries include hospitality, hospitals and healthcare, manufacturing,

consumer goods companies, and for many others (Randhawa and Sethi, 2017). All these

companies are getting numerous benefits of Activity-based Costing method due to which they

have started making use of this costing method in their organisation.

The reason behind the rise in the use of the Activity Based costing method is the objective of the

ABC method that provides the benefit to the companies. The objective includes rectifying the

inaccurate cost information, ABC also work to allocate the overheads on an activity basis, it

helps the management at making the decision on time with quality. All these objectives offer the

benefits to the company due to which they are able to compete in the market.

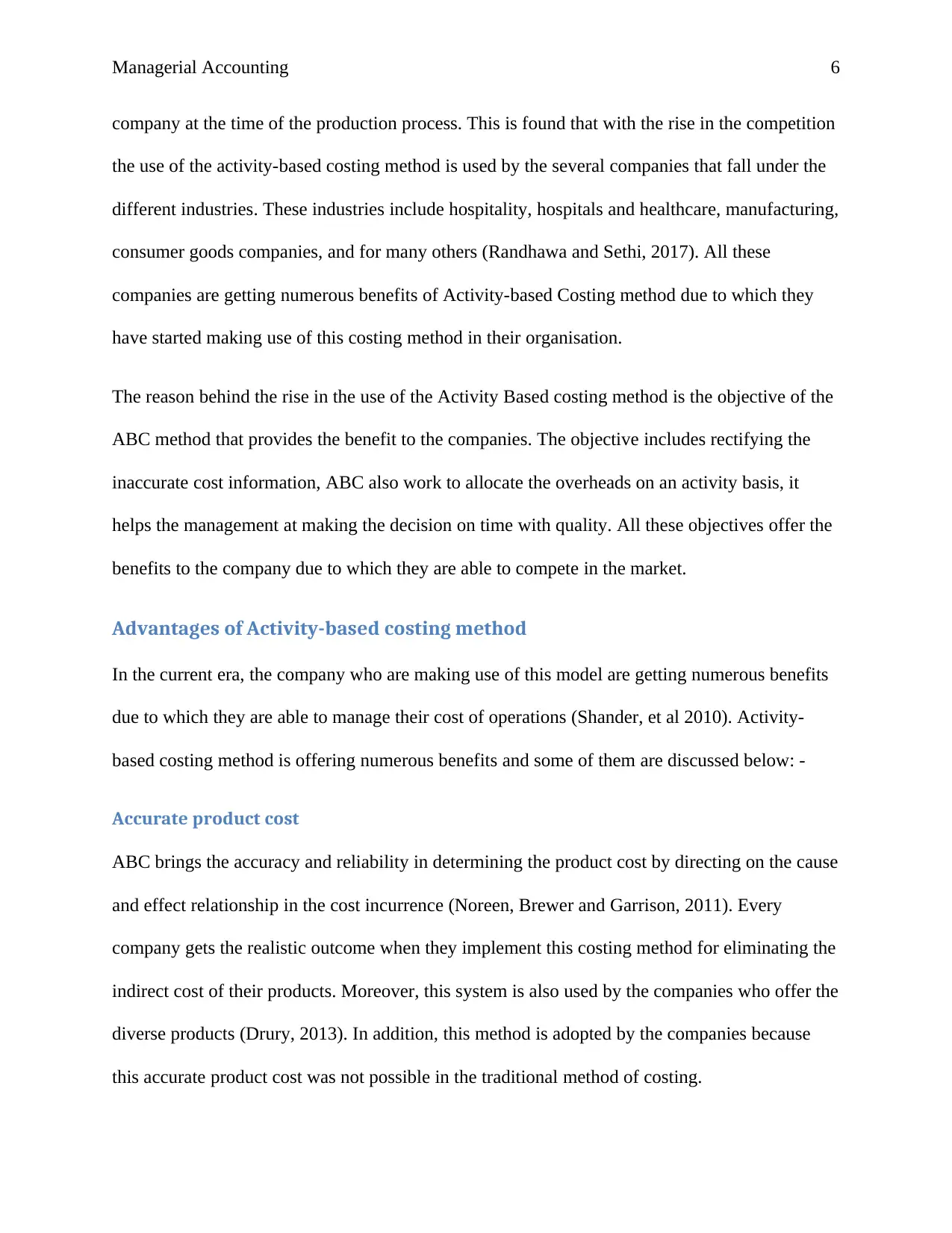

Advantages of Activity-based costing method

In the current era, the company who are making use of this model are getting numerous benefits

due to which they are able to manage their cost of operations (Shander, et al 2010). Activity-

based costing method is offering numerous benefits and some of them are discussed below: -

Accurate product cost

ABC brings the accuracy and reliability in determining the product cost by directing on the cause

and effect relationship in the cost incurrence (Noreen, Brewer and Garrison, 2011). Every

company gets the realistic outcome when they implement this costing method for eliminating the

indirect cost of their products. Moreover, this system is also used by the companies who offer the

diverse products (Drury, 2013). In addition, this method is adopted by the companies because

this accurate product cost was not possible in the traditional method of costing.

company at the time of the production process. This is found that with the rise in the competition

the use of the activity-based costing method is used by the several companies that fall under the

different industries. These industries include hospitality, hospitals and healthcare, manufacturing,

consumer goods companies, and for many others (Randhawa and Sethi, 2017). All these

companies are getting numerous benefits of Activity-based Costing method due to which they

have started making use of this costing method in their organisation.

The reason behind the rise in the use of the Activity Based costing method is the objective of the

ABC method that provides the benefit to the companies. The objective includes rectifying the

inaccurate cost information, ABC also work to allocate the overheads on an activity basis, it

helps the management at making the decision on time with quality. All these objectives offer the

benefits to the company due to which they are able to compete in the market.

Advantages of Activity-based costing method

In the current era, the company who are making use of this model are getting numerous benefits

due to which they are able to manage their cost of operations (Shander, et al 2010). Activity-

based costing method is offering numerous benefits and some of them are discussed below: -

Accurate product cost

ABC brings the accuracy and reliability in determining the product cost by directing on the cause

and effect relationship in the cost incurrence (Noreen, Brewer and Garrison, 2011). Every

company gets the realistic outcome when they implement this costing method for eliminating the

indirect cost of their products. Moreover, this system is also used by the companies who offer the

diverse products (Drury, 2013). In addition, this method is adopted by the companies because

this accurate product cost was not possible in the traditional method of costing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 7

(Source: Agarwal, 2018)

Information for the cost behaviour

Activity-based costing method is real in nature in terms of the cost behaviour and this is the

reason it helps in eliminating the cost and determining the activities which do not add value to

the products (Dale and Plunkett, 2017). This method allows the manager to control numerous

fixed overhead costs which are possible by exercising the control of the activities.

Cost information

Activity-based costing method offers the effective costing information that helps the managers to

manage the organisation and their working efficiently which is required to attain the better

understanding of the firm’s competitive advantage, strengths and weaknesses (Garrison, et al

2010). This is the effective way through which the company can earn the maximum of the profit

or can save the amount. This amount can further be used by the companies for making the right

decision for the products and services that they are offering to their customers (Weygandt,

Kimmel and Kieso, 2015).

(Source: Agarwal, 2018)

Information for the cost behaviour

Activity-based costing method is real in nature in terms of the cost behaviour and this is the

reason it helps in eliminating the cost and determining the activities which do not add value to

the products (Dale and Plunkett, 2017). This method allows the manager to control numerous

fixed overhead costs which are possible by exercising the control of the activities.

Cost information

Activity-based costing method offers the effective costing information that helps the managers to

manage the organisation and their working efficiently which is required to attain the better

understanding of the firm’s competitive advantage, strengths and weaknesses (Garrison, et al

2010). This is the effective way through which the company can earn the maximum of the profit

or can save the amount. This amount can further be used by the companies for making the right

decision for the products and services that they are offering to their customers (Weygandt,

Kimmel and Kieso, 2015).

Managerial Accounting 8

The above given are some of the benefits which the company is offering to the companies who

are implementing the Activity-based costing method. These benefits help the company in

generating the competitive advantage over their competitors (Pinto, 2010). ABC system is

effective that helps the company in managing the cost for the long run by controlling the

activities. The companies who are making use of the ABC not only get the cost-benefit but also

in managing the activities (Woodruff, 2018).

Explanation of the purpose of the two studies

The two Articles that have been selected for the analysis are selected with the purpose to learn

and to get the new research findings that will help the Australian companies in the near future

while implementing the activity-based costing system. The reason behind selecting the article 1

is to analyse how real life company – Nestle who is implementing Activity-based costing method

in Bangladesh. The article reflects that the data has been captured from both the primary and

secondary sources. Primary data has been captured by conducting the interview with the

employees of Nestle Bangladesh Ltd. and the secondary data has been collected from different

books. The purpose due to which the author conducted the research is to include the theories

related to the Activity-based costing and its application within the real-life organisation. The

author has conducted the research on the different cases of different cases but the major data has

been taken from the Nestle Bangladesh. The research question that has been included in the

article is; to identify the appropriate action based costing system that is used by the

manufacturing sector.

On the other hand, the second article that is selected as the study talks about the application of

ABC Systems to Health Care which is effective in the market of Turkey. The ABC system has

The above given are some of the benefits which the company is offering to the companies who

are implementing the Activity-based costing method. These benefits help the company in

generating the competitive advantage over their competitors (Pinto, 2010). ABC system is

effective that helps the company in managing the cost for the long run by controlling the

activities. The companies who are making use of the ABC not only get the cost-benefit but also

in managing the activities (Woodruff, 2018).

Explanation of the purpose of the two studies

The two Articles that have been selected for the analysis are selected with the purpose to learn

and to get the new research findings that will help the Australian companies in the near future

while implementing the activity-based costing system. The reason behind selecting the article 1

is to analyse how real life company – Nestle who is implementing Activity-based costing method

in Bangladesh. The article reflects that the data has been captured from both the primary and

secondary sources. Primary data has been captured by conducting the interview with the

employees of Nestle Bangladesh Ltd. and the secondary data has been collected from different

books. The purpose due to which the author conducted the research is to include the theories

related to the Activity-based costing and its application within the real-life organisation. The

author has conducted the research on the different cases of different cases but the major data has

been taken from the Nestle Bangladesh. The research question that has been included in the

article is; to identify the appropriate action based costing system that is used by the

manufacturing sector.

On the other hand, the second article that is selected as the study talks about the application of

ABC Systems to Health Care which is effective in the market of Turkey. The ABC system has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 9

been applied in the private hospital that is located in Istanbul, Turkey and it is one of the largest

private hospitals that are available in Turkey. The reason for selecting this article as a study that

this will provide the research findings related to the activity-based costing company in the

healthcare. This shows that apart from the manufacturing industry the Activity-based costing is

used in the other industries also which include health care. In this study, the author has selected

the Gynaecology department as the treatment unit for the particular hospital. The effectiveness

for implementing the Activity-based costing for the department is discussed in the report. The

major research question that has been answered in the research article is: The effective

implementation of ABC on health care sector.

Similarities and differences in the findings of the two studies

This section of the report includes the similarities and differences in the findings of the articles.

This is clear that both the selected articles are totally different from each other due to which

findings of the articles will show the more of different. Though, the method of Activity-based

costing remains the same with the same theories.

Similarities in findings of both the studies

In the article 1, this is clear that ABC implementation helped the managers of Nestle

Bangladesh in making their decision more quick and accurate by comparing the actual

performance with the budgeted estimation for improving their business operations (Mahal

and Hossain, 2015). On other hand, Article 2 shows that the ABC system has helped the

administration of the healthcare service providers to plan for the better services within the

organisation after knowing the accurate performance. This will ultimately help the

administration of to bring the improvement in their business operations.

been applied in the private hospital that is located in Istanbul, Turkey and it is one of the largest

private hospitals that are available in Turkey. The reason for selecting this article as a study that

this will provide the research findings related to the activity-based costing company in the

healthcare. This shows that apart from the manufacturing industry the Activity-based costing is

used in the other industries also which include health care. In this study, the author has selected

the Gynaecology department as the treatment unit for the particular hospital. The effectiveness

for implementing the Activity-based costing for the department is discussed in the report. The

major research question that has been answered in the research article is: The effective

implementation of ABC on health care sector.

Similarities and differences in the findings of the two studies

This section of the report includes the similarities and differences in the findings of the articles.

This is clear that both the selected articles are totally different from each other due to which

findings of the articles will show the more of different. Though, the method of Activity-based

costing remains the same with the same theories.

Similarities in findings of both the studies

In the article 1, this is clear that ABC implementation helped the managers of Nestle

Bangladesh in making their decision more quick and accurate by comparing the actual

performance with the budgeted estimation for improving their business operations (Mahal

and Hossain, 2015). On other hand, Article 2 shows that the ABC system has helped the

administration of the healthcare service providers to plan for the better services within the

organisation after knowing the accurate performance. This will ultimately help the

administration of to bring the improvement in their business operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 10

Article 1 findings reflect that the Nestle is able to enhance the operational performance

which is possible by allocating the overhead cost effectively. This shows that the

activities of the company get managed effectively with the low cost. Similarly, in the

article 2, the use of the ABC system offer the rise in the healthcare facilities cost

effectively without compromising the quality of service that they are offering to their

customers. The management of the healthcare in Turkey can easily control the cost

effectively with the use of ABC method (Aldogan, Austill and Kocakülâh, 2014).

Differences in the findings of both the studies

The article 1 reflects the analysis of Nestle Bangladesh, a company that desiin aa n wide

range of products with geographical presence. This is the reason due to which the

company needs to apply that activity-based costing system with the help of which they

can easily manage the activities or processes that are present (Mahal and Hossain, 2015).

In addition, this method is appropriate when the company deals in diverse service. On the

other hand, Healthcare service which has the service diversity to manage but over here

the focus has been done on the particular department of the private hospitals that merely

include 2 services in the Gynaecology Department.

The major difference lies in the findingofoe both the articles is related to the training to

the employees. In article 1, Nestle Bangladesh employees accepted the system of ABC

for their organisation and taken the training for the same. Though, on the other hand, in

the healthcare most of the employees are not able to understand the benefits of the ABC

system yet due to which they are not able to accept the system effectively (Aldogan,

Austill and Kocakülâh, 2014).

Article 1 findings reflect that the Nestle is able to enhance the operational performance

which is possible by allocating the overhead cost effectively. This shows that the

activities of the company get managed effectively with the low cost. Similarly, in the

article 2, the use of the ABC system offer the rise in the healthcare facilities cost

effectively without compromising the quality of service that they are offering to their

customers. The management of the healthcare in Turkey can easily control the cost

effectively with the use of ABC method (Aldogan, Austill and Kocakülâh, 2014).

Differences in the findings of both the studies

The article 1 reflects the analysis of Nestle Bangladesh, a company that desiin aa n wide

range of products with geographical presence. This is the reason due to which the

company needs to apply that activity-based costing system with the help of which they

can easily manage the activities or processes that are present (Mahal and Hossain, 2015).

In addition, this method is appropriate when the company deals in diverse service. On the

other hand, Healthcare service which has the service diversity to manage but over here

the focus has been done on the particular department of the private hospitals that merely

include 2 services in the Gynaecology Department.

The major difference lies in the findingofoe both the articles is related to the training to

the employees. In article 1, Nestle Bangladesh employees accepted the system of ABC

for their organisation and taken the training for the same. Though, on the other hand, in

the healthcare most of the employees are not able to understand the benefits of the ABC

system yet due to which they are not able to accept the system effectively (Aldogan,

Austill and Kocakülâh, 2014).

Managerial Accounting 11

This found that implementation of ABC syshave has been done in the private

organisation for only single department where they are facing the issues. This shthehthe n

aat application of the ABC system is limited in health care sector. Though, on the other

hand, the use of the ABC system in manufacturing industry is done in each and every

department and on the overall operations of the business that they are conducting in the

competitive environment.

Outcomes from the two studies

This section includes the outcomes from the two studies that will be considered as the useful

source for the management accountants in the companies of Australia.

Article 1

Knowledge of management supports in making decisions

The implementation of the ABC system supports the management of Nestle Bangladesh in

making the decisions by comparing the original performance with the budget estimation.

Moreover, the top management of Nestle Company make use of the ABC software that

simplified the system of costing. This software is imported by the company from India and

Switzerland which shows that they have the knowledge of the effective use of the ABC system to

their company (Mahal and Hossain, 2015). Through this, the company will be able to evaluate

the consumer profitability which is one of the good indicators of the performance of the firm.

This shows that decision making is linked with the knowledge of the top management of Nestle

Bangladesh for the products and services.

This found that implementation of ABC syshave has been done in the private

organisation for only single department where they are facing the issues. This shthehthe n

aat application of the ABC system is limited in health care sector. Though, on the other

hand, the use of the ABC system in manufacturing industry is done in each and every

department and on the overall operations of the business that they are conducting in the

competitive environment.

Outcomes from the two studies

This section includes the outcomes from the two studies that will be considered as the useful

source for the management accountants in the companies of Australia.

Article 1

Knowledge of management supports in making decisions

The implementation of the ABC system supports the management of Nestle Bangladesh in

making the decisions by comparing the original performance with the budget estimation.

Moreover, the top management of Nestle Company make use of the ABC software that

simplified the system of costing. This software is imported by the company from India and

Switzerland which shows that they have the knowledge of the effective use of the ABC system to

their company (Mahal and Hossain, 2015). Through this, the company will be able to evaluate

the consumer profitability which is one of the good indicators of the performance of the firm.

This shows that decision making is linked with the knowledge of the top management of Nestle

Bangladesh for the products and services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.