HI5017 Managerial Accounting: Budgeting, Approaches & Income Analysis

VerifiedAdded on 2023/04/25

|12

|3659

|81

Report

AI Summary

This report provides an in-depth analysis of the budgeting process, focusing on Ansell Limited. It begins by outlining the elements of a master budget, including income and expense budgets, sales budgets, production budgets, direct labor and materials budgets, and manufacturing overhead budgets. The report then compares top-down and bottom-up budgeting approaches, advocating for the bottom-up approach's suitability for Ansell Limited due to its inclusive nature and potential for improved employee motivation. Furthermore, the report constructs a budgeted income statement using Ansell Limited's 2018 financial data and compares it with the actual income statement, highlighting variations and offering insights into the company's financial performance. Desklib provides this and many other solved assignments for students.

HI5017 Managerial Accounting

Trimester 3 2018

Individual Assignment

1

Trimester 3 2018

Individual Assignment

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The underlying report is being prepared for developing an insight into the budgeting

process sued by business companies. It has been depicted with the report that master budget is

very important for determining the needs of individual department. Top-down and bottom-up

approach are the two major methods used by business companies to develop budget. Bottom-

up approach is regarded to be most suitable for business companies as it involve participation

from all employee level. In addition to this, the report provides a comparison of the budgeted

income statement with the actual income statement for the prepared for the selected

company, Ansell Limited. It has been depicted with the comparison that there are variations in

the amount of revenue to be realized as stated by the budgeted income statement and the

actual income statement.

2

The underlying report is being prepared for developing an insight into the budgeting

process sued by business companies. It has been depicted with the report that master budget is

very important for determining the needs of individual department. Top-down and bottom-up

approach are the two major methods used by business companies to develop budget. Bottom-

up approach is regarded to be most suitable for business companies as it involve participation

from all employee level. In addition to this, the report provides a comparison of the budgeted

income statement with the actual income statement for the prepared for the selected

company, Ansell Limited. It has been depicted with the comparison that there are variations in

the amount of revenue to be realized as stated by the budgeted income statement and the

actual income statement.

2

Contents

Executive Summary.........................................................................................................................2

Introduction.....................................................................................................................................4

Part A: Elements of Master Budget.................................................................................................4

Part B: Discussion & Comparison of the top-down and bottom-up approach to the budgeting

process and selecting the moist suitable for the company.............................................................6

Part C: Budgeted income statement through using financial data of year 2018 of company

Ansell Limited..................................................................................................................................7

Part D: Presentation of actual income statement of year 2018 and budgeted income statement

to make comparison and provide the opinion on the changes....................................................10

Conclusion......................................................................................................................................11

References.....................................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction.....................................................................................................................................4

Part A: Elements of Master Budget.................................................................................................4

Part B: Discussion & Comparison of the top-down and bottom-up approach to the budgeting

process and selecting the moist suitable for the company.............................................................6

Part C: Budgeted income statement through using financial data of year 2018 of company

Ansell Limited..................................................................................................................................7

Part D: Presentation of actual income statement of year 2018 and budgeted income statement

to make comparison and provide the opinion on the changes....................................................10

Conclusion......................................................................................................................................11

References.....................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The process of creating budgets can be regarded as very important for a company to

develop accurate spending plans. This would help in ensuring that a business always has

enough money for meeting its varying financial needs and requirements. It enables a company

to plan for its future financial needs and thus achieving its financial and operational goals. The

most significant benefit of budgeting for the business owners is that it helps in reducing costs

and increasing returns on investment. In this context the present report is being developed for

explaining the importance of developing budgets for business companies. This is carried out by

providing explanation of the different elements of the master budget and providing a discussion

and comparison of its top-down and bottom-up approach and recommending the bets suitable

approach for the selected company. The company selected for the purpose is an ASX listed

entity, that is, Ansell Limited. The report access the financial information from the annual

report of the selected company for developing its budgeted income statement with the use of

some projected targets to be achieved. The budgeted income statements are being compared

with the actual income statement for providing a comparison of the data and discussing the

changes identified.

Part A: Elements of Master Budget

Master budget can be regarded as the integration of all the various types of budgets

that are developed by different functional areas of a company. The budget is mainly presented

in monthly or quarterly format and may include explanation of text for describing the various

elements of the budget. It is usually referred to as central planning tool that is used by the

management in providing direction to carry out the different operational activities of a

company. The budget is largely used for projecting the income nod expenses of a company so

as to assist the management in taking long-term decisions relating to their overall growth and

development in the future context. The master budget created assists the individual

departments of a company to develop reports for achieving their goals (Meredith and Mantel,

2009). As such, the major elements of the master budget can be discussed as follows:

Income and Expense Budget

Income is regarded to be a major component of a master budget that provides a

depiction of the sales, dividends, royalties and capital gains earned by a company. The other

main components of a master budget are expenses that help the management in assessing the

areas of expenses that should be controlled for maximizing company profitability. The

production or overhead costs assesses with the use of this account will help the management in

identifying the variable expenses that can be eliminated (Blocher, 2009).

4

The process of creating budgets can be regarded as very important for a company to

develop accurate spending plans. This would help in ensuring that a business always has

enough money for meeting its varying financial needs and requirements. It enables a company

to plan for its future financial needs and thus achieving its financial and operational goals. The

most significant benefit of budgeting for the business owners is that it helps in reducing costs

and increasing returns on investment. In this context the present report is being developed for

explaining the importance of developing budgets for business companies. This is carried out by

providing explanation of the different elements of the master budget and providing a discussion

and comparison of its top-down and bottom-up approach and recommending the bets suitable

approach for the selected company. The company selected for the purpose is an ASX listed

entity, that is, Ansell Limited. The report access the financial information from the annual

report of the selected company for developing its budgeted income statement with the use of

some projected targets to be achieved. The budgeted income statements are being compared

with the actual income statement for providing a comparison of the data and discussing the

changes identified.

Part A: Elements of Master Budget

Master budget can be regarded as the integration of all the various types of budgets

that are developed by different functional areas of a company. The budget is mainly presented

in monthly or quarterly format and may include explanation of text for describing the various

elements of the budget. It is usually referred to as central planning tool that is used by the

management in providing direction to carry out the different operational activities of a

company. The budget is largely used for projecting the income nod expenses of a company so

as to assist the management in taking long-term decisions relating to their overall growth and

development in the future context. The master budget created assists the individual

departments of a company to develop reports for achieving their goals (Meredith and Mantel,

2009). As such, the major elements of the master budget can be discussed as follows:

Income and Expense Budget

Income is regarded to be a major component of a master budget that provides a

depiction of the sales, dividends, royalties and capital gains earned by a company. The other

main components of a master budget are expenses that help the management in assessing the

areas of expenses that should be controlled for maximizing company profitability. The

production or overhead costs assesses with the use of this account will help the management in

identifying the variable expenses that can be eliminated (Blocher, 2009).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales Budget

This is also an essential element of master budget that provides a depiction of its overall

sales that is an integration of its product of expected sales and price per unit. This budget

provides a depiction to the management regarding the estimated sales likely to be occurred

within future financial period. It is mainly used for determining the goals of different

departments by gaining the estimate of the future product requirements. This requires the

managers to gain an estimate of the factors such as economic conditions and business specific

factors to predict its future financial performance.

Production Budget

The production budget that is used for gaining an estimate of the number of units of

product that must be manufactured can also be regarded as an integral part of the master

budget. The production budget is mainly developed with the combination of sales forecast and

the inventory value and is mainly used for planning the requirements of the raw material that

would be required in the future direction. It helps the business owners in providing an estimate

of the units of the product that should be produced for meeting the sales needs (Albrecht,

2010).

Direct Labor Budget

The direct labor budget is used for estimating the number of labor hours that would be

required for producing the required items of product. This would helps in predicting the

employees required for meeting the production requirements and thus the management can

adequately plan for hiring the employees.

Direct Materials Budget

This type of budget is usually created for assessing the requirements of the materials

that should be purchased for meeting the requirements of the production budget. This provides

an estimate of the requirements of the cash that would be used for purchasing the raw

materials and thus depicts the majority of the costs to be incurred by a company on its

operational activities. The quantity of direct material that can be used for production and is

required to be purchased is estimated though the use of this budget (Brigham and Michael,

2013).

Manufacturing Overhead Budget

The budget is used for depiction of all the manufacturing costs that are incurred during

production and only excludes direct materials and direct labor cost. This budget usually

provides the value of cost of goods sold items within the master budget. It mainly includes the

5

This is also an essential element of master budget that provides a depiction of its overall

sales that is an integration of its product of expected sales and price per unit. This budget

provides a depiction to the management regarding the estimated sales likely to be occurred

within future financial period. It is mainly used for determining the goals of different

departments by gaining the estimate of the future product requirements. This requires the

managers to gain an estimate of the factors such as economic conditions and business specific

factors to predict its future financial performance.

Production Budget

The production budget that is used for gaining an estimate of the number of units of

product that must be manufactured can also be regarded as an integral part of the master

budget. The production budget is mainly developed with the combination of sales forecast and

the inventory value and is mainly used for planning the requirements of the raw material that

would be required in the future direction. It helps the business owners in providing an estimate

of the units of the product that should be produced for meeting the sales needs (Albrecht,

2010).

Direct Labor Budget

The direct labor budget is used for estimating the number of labor hours that would be

required for producing the required items of product. This would helps in predicting the

employees required for meeting the production requirements and thus the management can

adequately plan for hiring the employees.

Direct Materials Budget

This type of budget is usually created for assessing the requirements of the materials

that should be purchased for meeting the requirements of the production budget. This provides

an estimate of the requirements of the cash that would be used for purchasing the raw

materials and thus depicts the majority of the costs to be incurred by a company on its

operational activities. The quantity of direct material that can be used for production and is

required to be purchased is estimated though the use of this budget (Brigham and Michael,

2013).

Manufacturing Overhead Budget

The budget is used for depiction of all the manufacturing costs that are incurred during

production and only excludes direct materials and direct labor cost. This budget usually

provides the value of cost of goods sold items within the master budget. It mainly includes the

5

presentation of administrative expenses such as stationery, utilities, salaries, rent or other

facilities. This helps the management in reducing the production overhead and improving the

operational efficiency of a company (Butz, 2011).

Part B: Discussion & Comparison of the top-down and bottom-up approach to the budgeting

process and selecting the moist suitable for the company

Top-down and bottom-up are the two major approaches of budgeting used in the

corporate budgeting for creation of the budgets. A top-down approach of budgeting begins

with developing a high-level budget for the overall organization. The creation of a single budget

in this approach is followed by assigning the amounts to individual departments. The

departments then work in the direction of meeting the pre-determined goals that has been

provided to them by the higher management. Thus, it can be said that this type of budgeting

process begins with initially estimating the cost of the overall project and then dividing it into

the lower level tasks. Thus, it can be regarded as a planning strategy that estimates the cost of

the overall organizational activities by working from higher level towards the downwards

direction. The major benefit of this type of approach used by a company in creating the budgets

is that it is relatively time-consuming. This is because it involves only the higher management

and does not involve the participation from lower level of management for preparing the

budget. It facilitates in streamlining the business accounting process as upper level

management determines the goals to be achieved and lower-level management works in the

direction of meeting the determined targets to be achieved. On the other hand, the major

drawback associated with this method is that it does not involve participation from the lower-

level management people and therefore the budget created may suffer from a drawback of not

incorporating specific expenses that the higher management is not aware (Crosson and

Needles, 2010).

On the contrary, the bottom-up approach of budgeting involves creating the budget by

the individual departments of an organization that is sent to the higher management for

gaining approval. The budget is either accepted or is sent back for some rectification and then a

master budget is created by integration of the budgets gained from various departments of a

company. It is also known as participative budgeting process as the budget holds have the

opportunity of participating in determining their own budgets. The process begins with the

identification of the different types of tasks that are involved within a department. The

expenses that are incurred in meeting the various operational activities of different tasks would

be determined to prepare the budget for the entire project. The expenses are added together

for preparation of the entire budget that can be done by the use of normal method of cost

estimation. The process is carried out for each organizational level and requires the manager’s

input at each and every step of the process. The annual budget is created after adding the

6

facilities. This helps the management in reducing the production overhead and improving the

operational efficiency of a company (Butz, 2011).

Part B: Discussion & Comparison of the top-down and bottom-up approach to the budgeting

process and selecting the moist suitable for the company

Top-down and bottom-up are the two major approaches of budgeting used in the

corporate budgeting for creation of the budgets. A top-down approach of budgeting begins

with developing a high-level budget for the overall organization. The creation of a single budget

in this approach is followed by assigning the amounts to individual departments. The

departments then work in the direction of meeting the pre-determined goals that has been

provided to them by the higher management. Thus, it can be said that this type of budgeting

process begins with initially estimating the cost of the overall project and then dividing it into

the lower level tasks. Thus, it can be regarded as a planning strategy that estimates the cost of

the overall organizational activities by working from higher level towards the downwards

direction. The major benefit of this type of approach used by a company in creating the budgets

is that it is relatively time-consuming. This is because it involves only the higher management

and does not involve the participation from lower level of management for preparing the

budget. It facilitates in streamlining the business accounting process as upper level

management determines the goals to be achieved and lower-level management works in the

direction of meeting the determined targets to be achieved. On the other hand, the major

drawback associated with this method is that it does not involve participation from the lower-

level management people and therefore the budget created may suffer from a drawback of not

incorporating specific expenses that the higher management is not aware (Crosson and

Needles, 2010).

On the contrary, the bottom-up approach of budgeting involves creating the budget by

the individual departments of an organization that is sent to the higher management for

gaining approval. The budget is either accepted or is sent back for some rectification and then a

master budget is created by integration of the budgets gained from various departments of a

company. It is also known as participative budgeting process as the budget holds have the

opportunity of participating in determining their own budgets. The process begins with the

identification of the different types of tasks that are involved within a department. The

expenses that are incurred in meeting the various operational activities of different tasks would

be determined to prepare the budget for the entire project. The expenses are added together

for preparation of the entire budget that can be done by the use of normal method of cost

estimation. The process is carried out for each organizational level and requires the manager’s

input at each and every step of the process. The annual budget is created after adding the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

monthly budgets for the overall financial year. The major advantage of this type of method is it

results in creation of accurate budget by gaining the participation from lower-level

management people as well.

Thus, it can result in developing the accurate budgets by incorporating all the

information from the lower level employees. In addition to this, it can also result in improving

the morale and involvement of employees and thus enhancing their commitment level. It

results in creating a sense of teamwork and cohesiveness as employees feel that their concerns

and issues are heard and respected. However, the major drawback associated with this type of

budgeting method is that it can result in loss of managerial control over the budgeting process.

It can result in adding the unnecessary expenses as a result of the feedback provided by the

lower level employees. As such, it could result in creating of high spending targets that are not

aligned with the corporate objectives. This is because the business managers can focus largely

on department rather than attaining the long-term goals and development of the organization.

It could result in the creation of a over-budget and thus the management could spend more

money in comparison to the actual cost to be incurred (Cunningham, Bazley and Simmons,

2018).

As such, it can be said by the discussion of both the budgeting process that bottom-up

budgeting is most suitable for the company selected, that is, Ansell Limited. This is because it

involves the participation from lower level management people as well and thus can create

accurate budget as well as result in improving the employee motivation level. This would result

in improving the depiction of the employees to achieve their long-term goals of growth and

development. The employees are familiar with each department and thus their involvement

within the process would result in developing a more précised budget (Cunningham, Nikolai,

Bazley and Slaughter, 2014).

Part C: Budgeted income statement through using financial data of year 2018 of company

Ansell Limited

Budgeted income statement is similar to the normal income statement but it does not

contain actual figures instead it has estimated figures that is calculated on the basis of previous

income statement and through using some important assumptions. Budgeted income

statement has all the line items as found in the normal financial statement of performance.

Budgeted income statement contains projection of the future years and it reflects the future

performance of the company. Budgeted income statement is subject to change in case if there

is change in output level in the particular period. Also the accuracy of the budgeted income

statement is critically based on various budgeted figures such as sales budget, finished goods

budget, expense budget, direct variable cost budget, cost of goods sold budget etc. So it can be

said that budgeted income statement is dependent upon various financial inputs that arise a

7

results in creation of accurate budget by gaining the participation from lower-level

management people as well.

Thus, it can result in developing the accurate budgets by incorporating all the

information from the lower level employees. In addition to this, it can also result in improving

the morale and involvement of employees and thus enhancing their commitment level. It

results in creating a sense of teamwork and cohesiveness as employees feel that their concerns

and issues are heard and respected. However, the major drawback associated with this type of

budgeting method is that it can result in loss of managerial control over the budgeting process.

It can result in adding the unnecessary expenses as a result of the feedback provided by the

lower level employees. As such, it could result in creating of high spending targets that are not

aligned with the corporate objectives. This is because the business managers can focus largely

on department rather than attaining the long-term goals and development of the organization.

It could result in the creation of a over-budget and thus the management could spend more

money in comparison to the actual cost to be incurred (Cunningham, Bazley and Simmons,

2018).

As such, it can be said by the discussion of both the budgeting process that bottom-up

budgeting is most suitable for the company selected, that is, Ansell Limited. This is because it

involves the participation from lower level management people as well and thus can create

accurate budget as well as result in improving the employee motivation level. This would result

in improving the depiction of the employees to achieve their long-term goals of growth and

development. The employees are familiar with each department and thus their involvement

within the process would result in developing a more précised budget (Cunningham, Nikolai,

Bazley and Slaughter, 2014).

Part C: Budgeted income statement through using financial data of year 2018 of company

Ansell Limited

Budgeted income statement is similar to the normal income statement but it does not

contain actual figures instead it has estimated figures that is calculated on the basis of previous

income statement and through using some important assumptions. Budgeted income

statement has all the line items as found in the normal financial statement of performance.

Budgeted income statement contains projection of the future years and it reflects the future

performance of the company. Budgeted income statement is subject to change in case if there

is change in output level in the particular period. Also the accuracy of the budgeted income

statement is critically based on various budgeted figures such as sales budget, finished goods

budget, expense budget, direct variable cost budget, cost of goods sold budget etc. So it can be

said that budgeted income statement is dependent upon various financial inputs that arise a

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

question mark on the accuracy of the preparation of budgeted income statement. However,

proper planning, estimation and correct calculation will help to estimate highly accurate

budgeted income statement (Damodaran, 2011).

Budgeted income statement is very useful for the management as it helps in testing

whether company will profitable in near future and will company is successful to meet all the

expenses. It helps management to estimate whether company requires funds to manage the

working capital requirement or other important expenses during the budgeted year.

In order to formulate the budgeted income statement of Ansell Limited for year 2019 it

is important to look over the actual income statement of company for year 2018 as it will be

used as the base to prepare the budgeted income statement of year 2019. Below is the

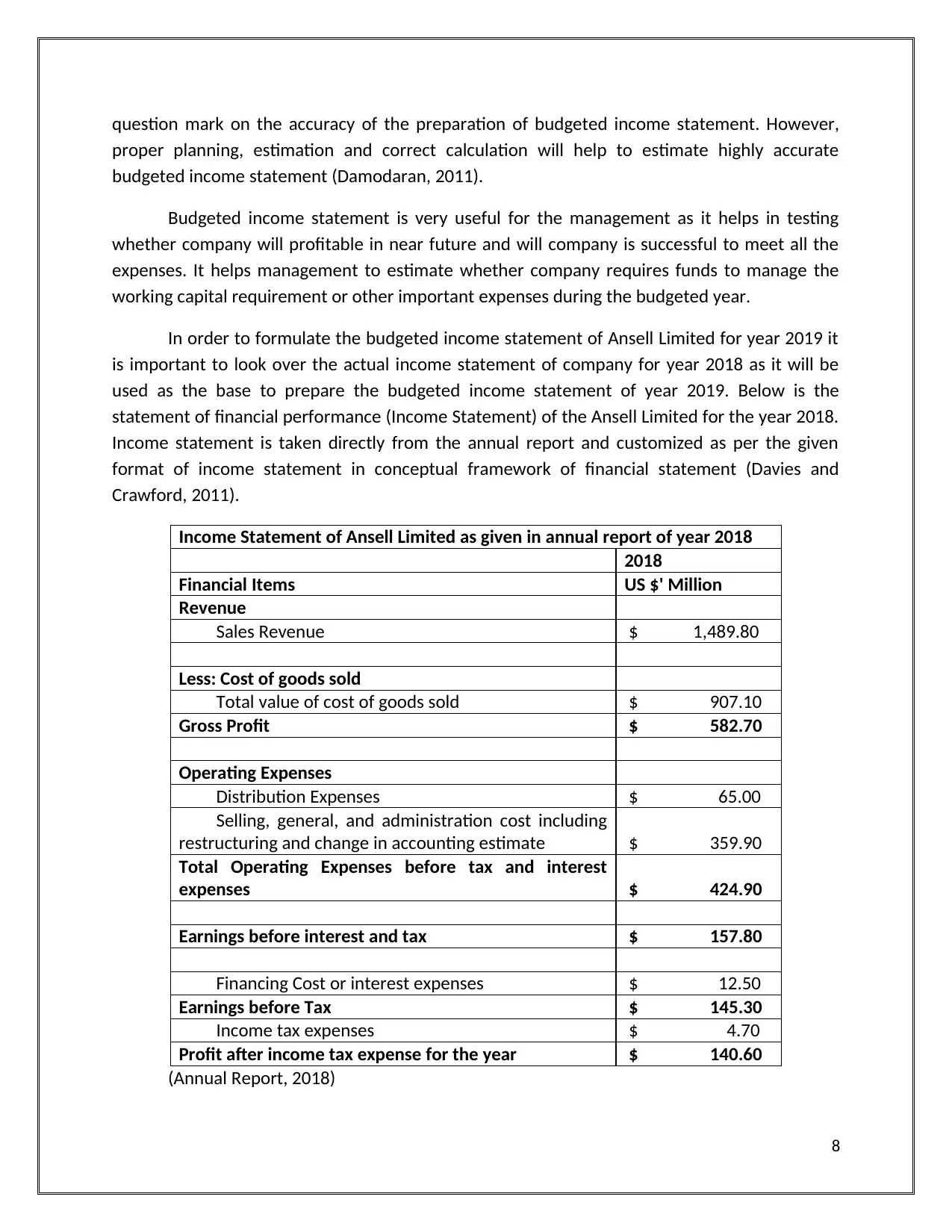

statement of financial performance (Income Statement) of the Ansell Limited for the year 2018.

Income statement is taken directly from the annual report and customized as per the given

format of income statement in conceptual framework of financial statement (Davies and

Crawford, 2011).

Income Statement of Ansell Limited as given in annual report of year 2018

2018

Financial Items US $' Million

Revenue

Sales Revenue $ 1,489.80

Less: Cost of goods sold

Total value of cost of goods sold $ 907.10

Gross Profit $ 582.70

Operating Expenses

Distribution Expenses $ 65.00

Selling, general, and administration cost including

restructuring and change in accounting estimate $ 359.90

Total Operating Expenses before tax and interest

expenses $ 424.90

Earnings before interest and tax $ 157.80

Financing Cost or interest expenses $ 12.50

Earnings before Tax $ 145.30

Income tax expenses $ 4.70

Profit after income tax expense for the year $ 140.60

(Annual Report, 2018)

8

proper planning, estimation and correct calculation will help to estimate highly accurate

budgeted income statement (Damodaran, 2011).

Budgeted income statement is very useful for the management as it helps in testing

whether company will profitable in near future and will company is successful to meet all the

expenses. It helps management to estimate whether company requires funds to manage the

working capital requirement or other important expenses during the budgeted year.

In order to formulate the budgeted income statement of Ansell Limited for year 2019 it

is important to look over the actual income statement of company for year 2018 as it will be

used as the base to prepare the budgeted income statement of year 2019. Below is the

statement of financial performance (Income Statement) of the Ansell Limited for the year 2018.

Income statement is taken directly from the annual report and customized as per the given

format of income statement in conceptual framework of financial statement (Davies and

Crawford, 2011).

Income Statement of Ansell Limited as given in annual report of year 2018

2018

Financial Items US $' Million

Revenue

Sales Revenue $ 1,489.80

Less: Cost of goods sold

Total value of cost of goods sold $ 907.10

Gross Profit $ 582.70

Operating Expenses

Distribution Expenses $ 65.00

Selling, general, and administration cost including

restructuring and change in accounting estimate $ 359.90

Total Operating Expenses before tax and interest

expenses $ 424.90

Earnings before interest and tax $ 157.80

Financing Cost or interest expenses $ 12.50

Earnings before Tax $ 145.30

Income tax expenses $ 4.70

Profit after income tax expense for the year $ 140.60

(Annual Report, 2018)

8

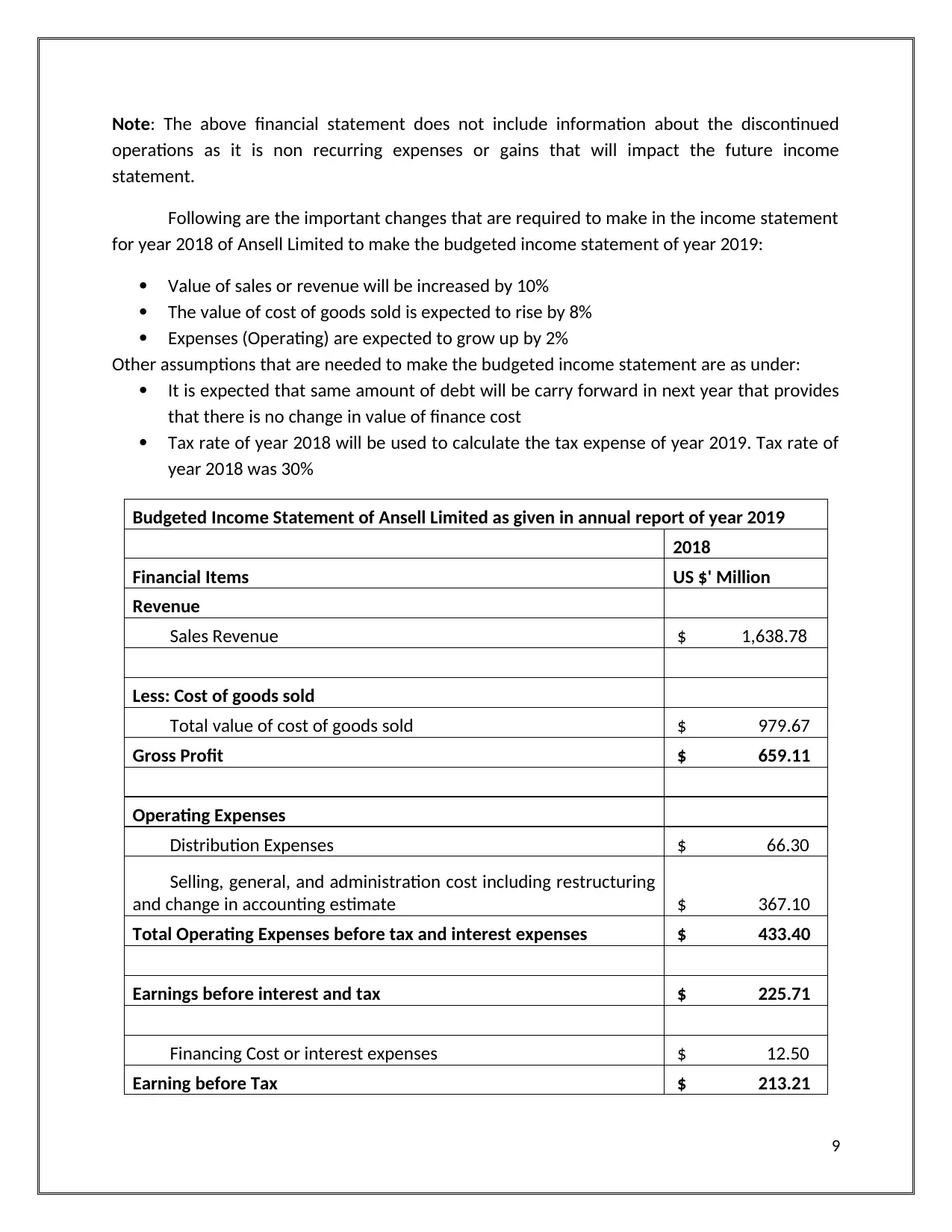

Note: The above financial statement does not include information about the discontinued

operations as it is non recurring expenses or gains that will impact the future income

statement.

Following are the important changes that are required to make in the income statement

for year 2018 of Ansell Limited to make the budgeted income statement of year 2019:

Value of sales or revenue will be increased by 10%

The value of cost of goods sold is expected to rise by 8%

Expenses (Operating) are expected to grow up by 2%

Other assumptions that are needed to make the budgeted income statement are as under:

It is expected that same amount of debt will be carry forward in next year that provides

that there is no change in value of finance cost

Tax rate of year 2018 will be used to calculate the tax expense of year 2019. Tax rate of

year 2018 was 30%

Budgeted Income Statement of Ansell Limited as given in annual report of year 2019

2018

Financial Items US $' Million

Revenue

Sales Revenue $ 1,638.78

Less: Cost of goods sold

Total value of cost of goods sold $ 979.67

Gross Profit $ 659.11

Operating Expenses

Distribution Expenses $ 66.30

Selling, general, and administration cost including restructuring

and change in accounting estimate $ 367.10

Total Operating Expenses before tax and interest expenses $ 433.40

Earnings before interest and tax $ 225.71

Financing Cost or interest expenses $ 12.50

Earning before Tax $ 213.21

9

operations as it is non recurring expenses or gains that will impact the future income

statement.

Following are the important changes that are required to make in the income statement

for year 2018 of Ansell Limited to make the budgeted income statement of year 2019:

Value of sales or revenue will be increased by 10%

The value of cost of goods sold is expected to rise by 8%

Expenses (Operating) are expected to grow up by 2%

Other assumptions that are needed to make the budgeted income statement are as under:

It is expected that same amount of debt will be carry forward in next year that provides

that there is no change in value of finance cost

Tax rate of year 2018 will be used to calculate the tax expense of year 2019. Tax rate of

year 2018 was 30%

Budgeted Income Statement of Ansell Limited as given in annual report of year 2019

2018

Financial Items US $' Million

Revenue

Sales Revenue $ 1,638.78

Less: Cost of goods sold

Total value of cost of goods sold $ 979.67

Gross Profit $ 659.11

Operating Expenses

Distribution Expenses $ 66.30

Selling, general, and administration cost including restructuring

and change in accounting estimate $ 367.10

Total Operating Expenses before tax and interest expenses $ 433.40

Earnings before interest and tax $ 225.71

Financing Cost or interest expenses $ 12.50

Earning before Tax $ 213.21

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

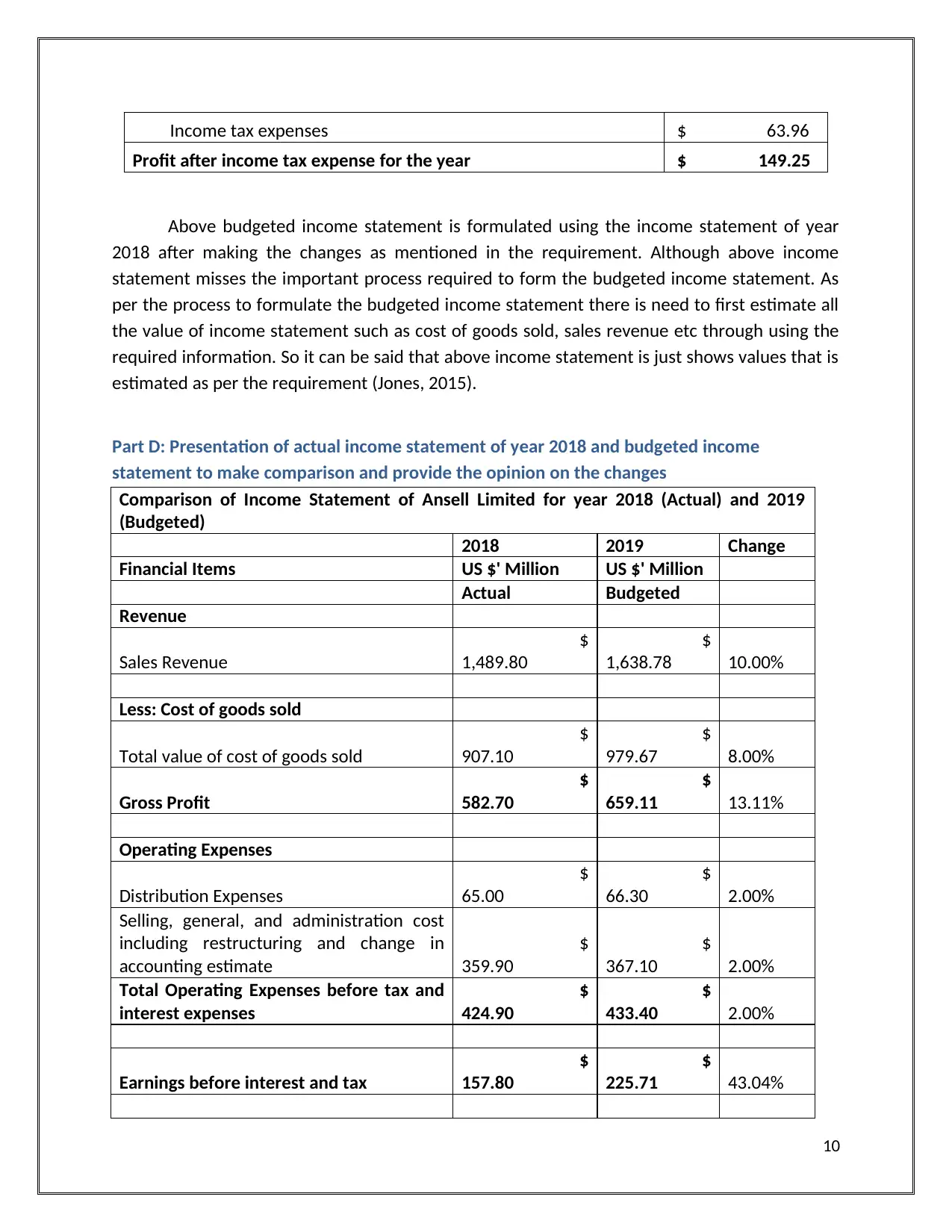

Income tax expenses $ 63.96

Profit after income tax expense for the year $ 149.25

Above budgeted income statement is formulated using the income statement of year

2018 after making the changes as mentioned in the requirement. Although above income

statement misses the important process required to form the budgeted income statement. As

per the process to formulate the budgeted income statement there is need to first estimate all

the value of income statement such as cost of goods sold, sales revenue etc through using the

required information. So it can be said that above income statement is just shows values that is

estimated as per the requirement (Jones, 2015).

Part D: Presentation of actual income statement of year 2018 and budgeted income

statement to make comparison and provide the opinion on the changes

Comparison of Income Statement of Ansell Limited for year 2018 (Actual) and 2019

(Budgeted)

2018 2019 Change

Financial Items US $' Million US $' Million

Actual Budgeted

Revenue

Sales Revenue

$

1,489.80

$

1,638.78 10.00%

Less: Cost of goods sold

Total value of cost of goods sold

$

907.10

$

979.67 8.00%

Gross Profit

$

582.70

$

659.11 13.11%

Operating Expenses

Distribution Expenses

$

65.00

$

66.30 2.00%

Selling, general, and administration cost

including restructuring and change in

accounting estimate

$

359.90

$

367.10 2.00%

Total Operating Expenses before tax and

interest expenses

$

424.90

$

433.40 2.00%

Earnings before interest and tax

$

157.80

$

225.71 43.04%

10

Profit after income tax expense for the year $ 149.25

Above budgeted income statement is formulated using the income statement of year

2018 after making the changes as mentioned in the requirement. Although above income

statement misses the important process required to form the budgeted income statement. As

per the process to formulate the budgeted income statement there is need to first estimate all

the value of income statement such as cost of goods sold, sales revenue etc through using the

required information. So it can be said that above income statement is just shows values that is

estimated as per the requirement (Jones, 2015).

Part D: Presentation of actual income statement of year 2018 and budgeted income

statement to make comparison and provide the opinion on the changes

Comparison of Income Statement of Ansell Limited for year 2018 (Actual) and 2019

(Budgeted)

2018 2019 Change

Financial Items US $' Million US $' Million

Actual Budgeted

Revenue

Sales Revenue

$

1,489.80

$

1,638.78 10.00%

Less: Cost of goods sold

Total value of cost of goods sold

$

907.10

$

979.67 8.00%

Gross Profit

$

582.70

$

659.11 13.11%

Operating Expenses

Distribution Expenses

$

65.00

$

66.30 2.00%

Selling, general, and administration cost

including restructuring and change in

accounting estimate

$

359.90

$

367.10 2.00%

Total Operating Expenses before tax and

interest expenses

$

424.90

$

433.40 2.00%

Earnings before interest and tax

$

157.80

$

225.71 43.04%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financing Cost or interest expenses

$

12.50

$

12.50 0.00%

Earnings before Tax

$

145.30

$

213.21 46.74%

Income tax expenses

$

4.70

$

63.96 1260.94%

Profit after income tax expense for the

year

$

140.60

$

149.25 6.15%

Comparison of both actual and budgeted income statement and opinion on the changes

Revenue: Revenue of Ansell Limited has been increased by 10% as required and change

in revenue over the year reflects company’s improved financial performance and

increase in output. The increase in revenue provides sufficient capacity to bear the

expenses and also to increase the profits in much greater proportion as compare to

sales revenue.

Cost of goods sold: Cost of goods sold represent expenses such as direct material, direct

labour and direct variable expenses. Overall cost of goods sold represents major

expenses and any unexpected increase in this cost will lead to decrease in profit and can

also leads to decrease in gross profit margin. In case of Ansell Limited cost of goods sold

is increased by 8% as required. It means management has been successful in saving

some percentage of cost in proportion to increase in sales revenue (Krantz, 2016).

Gross Profit: Gross profit has been increased by 13.11% in year 2019 (Budgeted) as

compare to actual gross profit in year 2018.

Net profit: Net profit is increased by 6.15% which is comparatively low in comparison to

increase in sales revenue by 10%.

Conclusion

On the basis of overall analysis of budgeted income statements of Ansell Limited it can

be said that there was improve in financial performance of the company in year 2019 as per the

information provided. It has been seen that budgeted income statement of Ansell Limited has

shown only an increase of 6.15% in net profit while there was increase in revenue by 10% that

indicates that company has failed to control the increase in expenses.

11

$

12.50

$

12.50 0.00%

Earnings before Tax

$

145.30

$

213.21 46.74%

Income tax expenses

$

4.70

$

63.96 1260.94%

Profit after income tax expense for the

year

$

140.60

$

149.25 6.15%

Comparison of both actual and budgeted income statement and opinion on the changes

Revenue: Revenue of Ansell Limited has been increased by 10% as required and change

in revenue over the year reflects company’s improved financial performance and

increase in output. The increase in revenue provides sufficient capacity to bear the

expenses and also to increase the profits in much greater proportion as compare to

sales revenue.

Cost of goods sold: Cost of goods sold represent expenses such as direct material, direct

labour and direct variable expenses. Overall cost of goods sold represents major

expenses and any unexpected increase in this cost will lead to decrease in profit and can

also leads to decrease in gross profit margin. In case of Ansell Limited cost of goods sold

is increased by 8% as required. It means management has been successful in saving

some percentage of cost in proportion to increase in sales revenue (Krantz, 2016).

Gross Profit: Gross profit has been increased by 13.11% in year 2019 (Budgeted) as

compare to actual gross profit in year 2018.

Net profit: Net profit is increased by 6.15% which is comparatively low in comparison to

increase in sales revenue by 10%.

Conclusion

On the basis of overall analysis of budgeted income statements of Ansell Limited it can

be said that there was improve in financial performance of the company in year 2019 as per the

information provided. It has been seen that budgeted income statement of Ansell Limited has

shown only an increase of 6.15% in net profit while there was increase in revenue by 10% that

indicates that company has failed to control the increase in expenses.

11

References

Albrecht, A. 2010. Accounting: Concepts and Applications. Cengage Learning.

Annual Report. 2018. Ansell Limited. [Online]. Available at:

https://www.ansell.com/-/media/projects/ansell/website/pdf/annual-reports/2018/2018-

annual-reports.ashx?

la=en&rev=e475cbd619de4c34af6a80d1373b988e&hash=DE939764F3477F6AA6BB1E89C6638

BD4 [Accessed on: 5 February 2019].

Blocher. 2009. Cost Management: A Strategic Emphasis. Tata McGraw-Hill Education.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Boston, USA:

Cengage Learning.

Butz, C. 2011. Role and Effects of Budgeting in Managerial Practice. Germany. GRIN Verlag.

Crosson, S.V. and Needles, B.E. 2010. Managerial Accounting. USA: Cengage Learning.

Cunningham, B., Bazley, J. and Simmons, S. 2018. Accounting: Information for Business

Decisions. USA: John Wiley & sons.

Cunningham, B., Nikolai, L.A., Bazley, J. and Slaughter, G. 2014. Accounting: Information for

Business Decisions. Australia: Cengage Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. London: Pearson.

Jones, S. 2015. The Routledge Companion to Financial Accounting Theory. London: Routledge.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Meredith, J. and Mantel, S. 2009. Project Management: A Managerial Approach. 6Th Ed. USA:

John Wiley & Sons.

12

Albrecht, A. 2010. Accounting: Concepts and Applications. Cengage Learning.

Annual Report. 2018. Ansell Limited. [Online]. Available at:

https://www.ansell.com/-/media/projects/ansell/website/pdf/annual-reports/2018/2018-

annual-reports.ashx?

la=en&rev=e475cbd619de4c34af6a80d1373b988e&hash=DE939764F3477F6AA6BB1E89C6638

BD4 [Accessed on: 5 February 2019].

Blocher. 2009. Cost Management: A Strategic Emphasis. Tata McGraw-Hill Education.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Boston, USA:

Cengage Learning.

Butz, C. 2011. Role and Effects of Budgeting in Managerial Practice. Germany. GRIN Verlag.

Crosson, S.V. and Needles, B.E. 2010. Managerial Accounting. USA: Cengage Learning.

Cunningham, B., Bazley, J. and Simmons, S. 2018. Accounting: Information for Business

Decisions. USA: John Wiley & sons.

Cunningham, B., Nikolai, L.A., Bazley, J. and Slaughter, G. 2014. Accounting: Information for

Business Decisions. Australia: Cengage Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. London: Pearson.

Jones, S. 2015. The Routledge Companion to Financial Accounting Theory. London: Routledge.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Meredith, J. and Mantel, S. 2009. Project Management: A Managerial Approach. 6Th Ed. USA:

John Wiley & Sons.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.