Strategic Information Systems Case Study: Rainbow Illusion Analysis

VerifiedAdded on 2022/11/29

|13

|3151

|7

Case Study

AI Summary

This case study report provides an in-depth analysis of Rainbow Illusion's IT strategic information systems. It begins with an executive summary outlining financial reporting, transaction cycles, e-commerce, and management reporting, as well as the associated risks in internal control processes. The report then delves into the specific strengths of Rainbow Illusion's system, such as the use of a unified sales system across all stores, sequential numbering, separation of duties, commission-based pay for sales staff, salaried managers, and centralized invoice processing. It explores how these strengths help regulate sales transactions and mitigate potential issues. The report also examines situational pressures that can lead to employee fraud and discusses the benefits of a distributed computerized system. Furthermore, the study covers transaction processing systems, financial reporting systems, and management reporting systems, along with their roles within the accounting information system. It also explores the potential situational forces that can increase the likelihood of fraud within the company. The report concludes by highlighting the importance of robust internal controls and ethical considerations in preventing fraud and ensuring the integrity of the IT systems.

Running Head: IT 0

STRATEGIC INFORMATION SYSTEM

STRATEGIC INFORMATION SYSTEM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IT 1

Executive Summary

This report outlines various notions related to financial reporting, transaction cycles, e-

commerce, management reporting and the significant risks associated in internal control

process. The report is also connected to Rainbow Illusion situation in Australia trading read

to wear clothes for young women’s.

With depth analysis of Rainbow Illusion case, it also highlights six key strengths that can also

help in evading some of the specific problems. These respective strengths focused on all

stores using alike sales system, adopting of number sequencing, duties separation, sales

individual and young cashiers are paid wages plus commission relying on volumes of sale,

managers and associate manager are compensated on salary base and send all invoices related

to sales and other transactions to centralised processing division system.

It is also explained in the report that how strength has benefitted to Rainbow illusion in

effective regulating the transactions related to sales. Similarly, one of the key factor that force

any employee to indulge into fraud is situational pressure and thus it must be consider

primarily by any corporate. With regards to this, there is also a glimpse of distributed

computerised system as its functionality are considered by various companies as benefits.

Executive Summary

This report outlines various notions related to financial reporting, transaction cycles, e-

commerce, management reporting and the significant risks associated in internal control

process. The report is also connected to Rainbow Illusion situation in Australia trading read

to wear clothes for young women’s.

With depth analysis of Rainbow Illusion case, it also highlights six key strengths that can also

help in evading some of the specific problems. These respective strengths focused on all

stores using alike sales system, adopting of number sequencing, duties separation, sales

individual and young cashiers are paid wages plus commission relying on volumes of sale,

managers and associate manager are compensated on salary base and send all invoices related

to sales and other transactions to centralised processing division system.

It is also explained in the report that how strength has benefitted to Rainbow illusion in

effective regulating the transactions related to sales. Similarly, one of the key factor that force

any employee to indulge into fraud is situational pressure and thus it must be consider

primarily by any corporate. With regards to this, there is also a glimpse of distributed

computerised system as its functionality are considered by various companies as benefits.

IT 2

Table of Contents

Introduction................................................................................................................................3

Strengths in Rainbow illusion’s System....................................................................................4

Problems evaded by integrating strengths..................................................................................4

Situational force that would upsurge the possibility of fraud....................................................6

Reasons for companies to install a distributed computer system rather than centralised one. . .8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Strengths in Rainbow illusion’s System....................................................................................4

Problems evaded by integrating strengths..................................................................................4

Situational force that would upsurge the possibility of fraud....................................................6

Reasons for companies to install a distributed computer system rather than centralised one. . .8

Conclusion..................................................................................................................................9

References................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IT 3

Introduction

It is important to know various aspects before going into depth analysis of the case. It

includes system of accounting information, its subsystem and their linkage in the significant

case. Grabski et al (2011) defined accounting information system as collection of resources

like persons and equipment’s developed to convert financial and other sorts of data into

relevant information. It can renovate whether system is computerised or manual. The

computerised system has several benefits with making job easier with use of various

applications in the software and with performing other functions such as collection,

bookkeeping and operating of transaction data, spreading of financial data and so on.

The accounting information system has three sub-systems also and they include –

Transaction Processing System (TPS) – There is five transaction cycle in TPS and

every cycle undertake the tasks in their own way with sharing of mutual attributes. In

addition, these cycles are also present in all sorts of businesses such as profit or non-

profit. One of the five cycles is revenue cycle defined as the repeated set of corporate

activities and associated information processing operations that are related with

offering products to consumers and pull payment from them. The key objective of this

cycle is to offer adequate product in right place at the right time for the right price.

Some of key basis revenue cycle activities include collection of cash, entry of sales

order, billing and shipping (Schroeder and Gibson, 2009).

The next cycle is expenditure cycle which aims to ensure that all products are ordered

as per the requirement and thus is related activities are associated with the purchasing

and payment of products. Payroll cycle in the system ensures with effective

management of the employee force and also considered as recurring set of business

activities. In the production cycle, raw materials and labour are transformed into

finished goods. At last, financial cycle involves interactions with creditors and

investors (Rimal et al, 2011).

Financial reporting system/ General ledger – In accounting information system, it

is another subsystem linked to all other systems by the transaction are firstly logged in

distinct journals and those transactions summary goes into financial reporting system

which goes to be the source of input to management reporting system. There is an

Introduction

It is important to know various aspects before going into depth analysis of the case. It

includes system of accounting information, its subsystem and their linkage in the significant

case. Grabski et al (2011) defined accounting information system as collection of resources

like persons and equipment’s developed to convert financial and other sorts of data into

relevant information. It can renovate whether system is computerised or manual. The

computerised system has several benefits with making job easier with use of various

applications in the software and with performing other functions such as collection,

bookkeeping and operating of transaction data, spreading of financial data and so on.

The accounting information system has three sub-systems also and they include –

Transaction Processing System (TPS) – There is five transaction cycle in TPS and

every cycle undertake the tasks in their own way with sharing of mutual attributes. In

addition, these cycles are also present in all sorts of businesses such as profit or non-

profit. One of the five cycles is revenue cycle defined as the repeated set of corporate

activities and associated information processing operations that are related with

offering products to consumers and pull payment from them. The key objective of this

cycle is to offer adequate product in right place at the right time for the right price.

Some of key basis revenue cycle activities include collection of cash, entry of sales

order, billing and shipping (Schroeder and Gibson, 2009).

The next cycle is expenditure cycle which aims to ensure that all products are ordered

as per the requirement and thus is related activities are associated with the purchasing

and payment of products. Payroll cycle in the system ensures with effective

management of the employee force and also considered as recurring set of business

activities. In the production cycle, raw materials and labour are transformed into

finished goods. At last, financial cycle involves interactions with creditors and

investors (Rimal et al, 2011).

Financial reporting system/ General ledger – In accounting information system, it

is another subsystem linked to all other systems by the transaction are firstly logged in

distinct journals and those transactions summary goes into financial reporting system

which goes to be the source of input to management reporting system. There is an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IT 4

assortment of broader information to fulfil the requirements of several external users

in any corporate enterprise (Gelinas, Dull and Wheeler, 2011).

Management reporting system (MRS) – It is known to be critical component of any

corporation inside control measures as it leads administration’s consideration to solve

several issues the business firm is facing in a timely manner. This encourages

effective management and benefits organisation in gaining its core purpose (Gelinas,

Dull and Wheeler, 2011).

Strengths in Rainbow illusion’s System

The six key strengths in Rainbow Illusion’s system includes –

The sales transaction is performed by all the 30 stores and with using the same

system.

On the basis of sales volume, sales personnel and young cashier are paid wages and

commission.

The job of manager and assistant are full time and they were paid on salary basis.

Duties separation.

To each transaction, cash register allocated consecutive number.

All sales invoices, tapes of cash register and return slips are gathered collectively to

central data processing division.

Problems evaded by integrating strengths

I. The sales transaction is performed by all the 30 stores and with using the same

system.

It implies that Rainbow illusion trails ERP system (Enterprise resource planning).

These systems help any business firm to synchronise all sides of organisation

operations with a traditional AIS (Chang et al, 2008). ERP system also facilitates the

information flow between all retail stores and all the functions are combined in a

single system which regulates to share sales information among themselves (Karsak

and Ozogul, 2009). This is regarded as strength in case of Rainbow illusion because it

assortment of broader information to fulfil the requirements of several external users

in any corporate enterprise (Gelinas, Dull and Wheeler, 2011).

Management reporting system (MRS) – It is known to be critical component of any

corporation inside control measures as it leads administration’s consideration to solve

several issues the business firm is facing in a timely manner. This encourages

effective management and benefits organisation in gaining its core purpose (Gelinas,

Dull and Wheeler, 2011).

Strengths in Rainbow illusion’s System

The six key strengths in Rainbow Illusion’s system includes –

The sales transaction is performed by all the 30 stores and with using the same

system.

On the basis of sales volume, sales personnel and young cashier are paid wages and

commission.

The job of manager and assistant are full time and they were paid on salary basis.

Duties separation.

To each transaction, cash register allocated consecutive number.

All sales invoices, tapes of cash register and return slips are gathered collectively to

central data processing division.

Problems evaded by integrating strengths

I. The sales transaction is performed by all the 30 stores and with using the same

system.

It implies that Rainbow illusion trails ERP system (Enterprise resource planning).

These systems help any business firm to synchronise all sides of organisation

operations with a traditional AIS (Chang et al, 2008). ERP system also facilitates the

information flow between all retail stores and all the functions are combined in a

single system which regulates to share sales information among themselves (Karsak

and Ozogul, 2009). This is regarded as strength in case of Rainbow illusion because it

IT 5

can control and regulate effective information flow required to each store related to

sales or others.

II. On the basis of sales volume, sales personnel and young cashier are paid wages

and commission.

When an employee receives income based in the percentage of the sales, it is termed

as a commission based pay system. Such system motivates employee to earn more

pay with increasing sales volume (Batt and Colvin, 2011). Considering Rainbow

illusion, sales individual and cashier can be encouraged with higher motivation to

gain high commission and there will not be any conflict among the sales personnel as

what would they get is related to their contribution to the firm.

III. The job of manager and assistant are full time and they were paid on salary

basis.

The managers and assistant managers are recruited based on their qualifications and

experience and therefore, it is their duty to accomplish the job for which they are

hired and no matter it takes 35 hours a week or 55 hours respectively. For their

particular performance, they are agreed to use their skills and their commitment

towards achieving organisation goal is a positive aspect for Rainbow Illusion.

The issues can effectively be avoided by Rainbow illusion as both assistant manager

and supervisor can offer their efforts constantly to the organisation and accomplish

their tasks in coordination with facilitation of sales transaction.

IV. Duties separation.

It is considered as one of the significant parts of control system and that is why

reflected as strength. Here, the three key objectives include –

Structured organisation.

There should be separation between transaction authorisation and transaction

processing.

Record keeping should be disjointed from responsibility of custody of assets

The division of sales should not make the bill as client may be charger higher they

support the less than they should be billed. Bills also should not be prepared by the

account receivable division because they have charge over the account receivables

assets (Gelinas, Dull and Wheeler, 2011).

There is a proper separation of duties in the Rainbow Illusion as processing of sales

are made by four individual in line. Initially, salesperson does his duty and provides

can control and regulate effective information flow required to each store related to

sales or others.

II. On the basis of sales volume, sales personnel and young cashier are paid wages

and commission.

When an employee receives income based in the percentage of the sales, it is termed

as a commission based pay system. Such system motivates employee to earn more

pay with increasing sales volume (Batt and Colvin, 2011). Considering Rainbow

illusion, sales individual and cashier can be encouraged with higher motivation to

gain high commission and there will not be any conflict among the sales personnel as

what would they get is related to their contribution to the firm.

III. The job of manager and assistant are full time and they were paid on salary

basis.

The managers and assistant managers are recruited based on their qualifications and

experience and therefore, it is their duty to accomplish the job for which they are

hired and no matter it takes 35 hours a week or 55 hours respectively. For their

particular performance, they are agreed to use their skills and their commitment

towards achieving organisation goal is a positive aspect for Rainbow Illusion.

The issues can effectively be avoided by Rainbow illusion as both assistant manager

and supervisor can offer their efforts constantly to the organisation and accomplish

their tasks in coordination with facilitation of sales transaction.

IV. Duties separation.

It is considered as one of the significant parts of control system and that is why

reflected as strength. Here, the three key objectives include –

Structured organisation.

There should be separation between transaction authorisation and transaction

processing.

Record keeping should be disjointed from responsibility of custody of assets

The division of sales should not make the bill as client may be charger higher they

support the less than they should be billed. Bills also should not be prepared by the

account receivable division because they have charge over the account receivables

assets (Gelinas, Dull and Wheeler, 2011).

There is a proper separation of duties in the Rainbow Illusion as processing of sales

are made by four individual in line. Initially, salesperson does his duty and provides

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IT 6

invoice to the cashier with retaining one copy in its sales book. Afterwards, the

invoice is assessed by the cashier and then finish its part for processing sales

transactions. Then the everyday settlement was performed by assistant manager

related to the assessment by store manager. Ultimately, the cash, cheque and sales

with credit card are reviewed by the manager with making of bank deposit regularly.

In this manner, responsibly of all employee are separated effectively which in turn

benefits to decrease any sorts of risk of deception in Rainbow Illusion.

V. To each transaction, cash register allocated consecutive number.

Considering sales transactions processing, developing numeric code can control

efficient and effective processing of data. If there is no code in the system, it can be

called as disadvantageous as corporate undertakes abundant transactions with

identical attributes and build challenges to differentiate one from the other (Putra and

Suryaputra, 2014).

The administration can be watchful with sequential coding related to any sort of

misdirected transaction deal if it discovers any gap when the processing of transaction

is going on. When there is consecutive number assigned, it would be easy to discover

the cause and effect of the error or it is difficult to solve the issue (Putra and

Suryaputra, 2014). With Rainbow Illusion, this mechanism has benefit the company

in regulating the transaction of sales efficiently.

VI. All sales invoices, tapes of cash register and return slips are gathered collectively

to central data processing division.

Batch processing system has been adopted by Rainbow illusion which allows the

administration efficiently undertaking the large transactions. When similar transaction

group are collected and carried together for the processing, it is termed as batch. It

benefits to evade the issue of inefficiency in operations and lack of control over

transactions processing (Gelinas, Dull and Wheeler, 2011).

All sales invoices, tapes of cash register and return slips are gathered collectively for

processing which also helps and benefits manager to assess of all at once. Hence, this

can solve the issue of system inconsistency.

Situational force that would upsurge the possibility of

fraud

invoice to the cashier with retaining one copy in its sales book. Afterwards, the

invoice is assessed by the cashier and then finish its part for processing sales

transactions. Then the everyday settlement was performed by assistant manager

related to the assessment by store manager. Ultimately, the cash, cheque and sales

with credit card are reviewed by the manager with making of bank deposit regularly.

In this manner, responsibly of all employee are separated effectively which in turn

benefits to decrease any sorts of risk of deception in Rainbow Illusion.

V. To each transaction, cash register allocated consecutive number.

Considering sales transactions processing, developing numeric code can control

efficient and effective processing of data. If there is no code in the system, it can be

called as disadvantageous as corporate undertakes abundant transactions with

identical attributes and build challenges to differentiate one from the other (Putra and

Suryaputra, 2014).

The administration can be watchful with sequential coding related to any sort of

misdirected transaction deal if it discovers any gap when the processing of transaction

is going on. When there is consecutive number assigned, it would be easy to discover

the cause and effect of the error or it is difficult to solve the issue (Putra and

Suryaputra, 2014). With Rainbow Illusion, this mechanism has benefit the company

in regulating the transaction of sales efficiently.

VI. All sales invoices, tapes of cash register and return slips are gathered collectively

to central data processing division.

Batch processing system has been adopted by Rainbow illusion which allows the

administration efficiently undertaking the large transactions. When similar transaction

group are collected and carried together for the processing, it is termed as batch. It

benefits to evade the issue of inefficiency in operations and lack of control over

transactions processing (Gelinas, Dull and Wheeler, 2011).

All sales invoices, tapes of cash register and return slips are gathered collectively for

processing which also helps and benefits manager to assess of all at once. Hence, this

can solve the issue of system inconsistency.

Situational force that would upsurge the possibility of

fraud

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IT 7

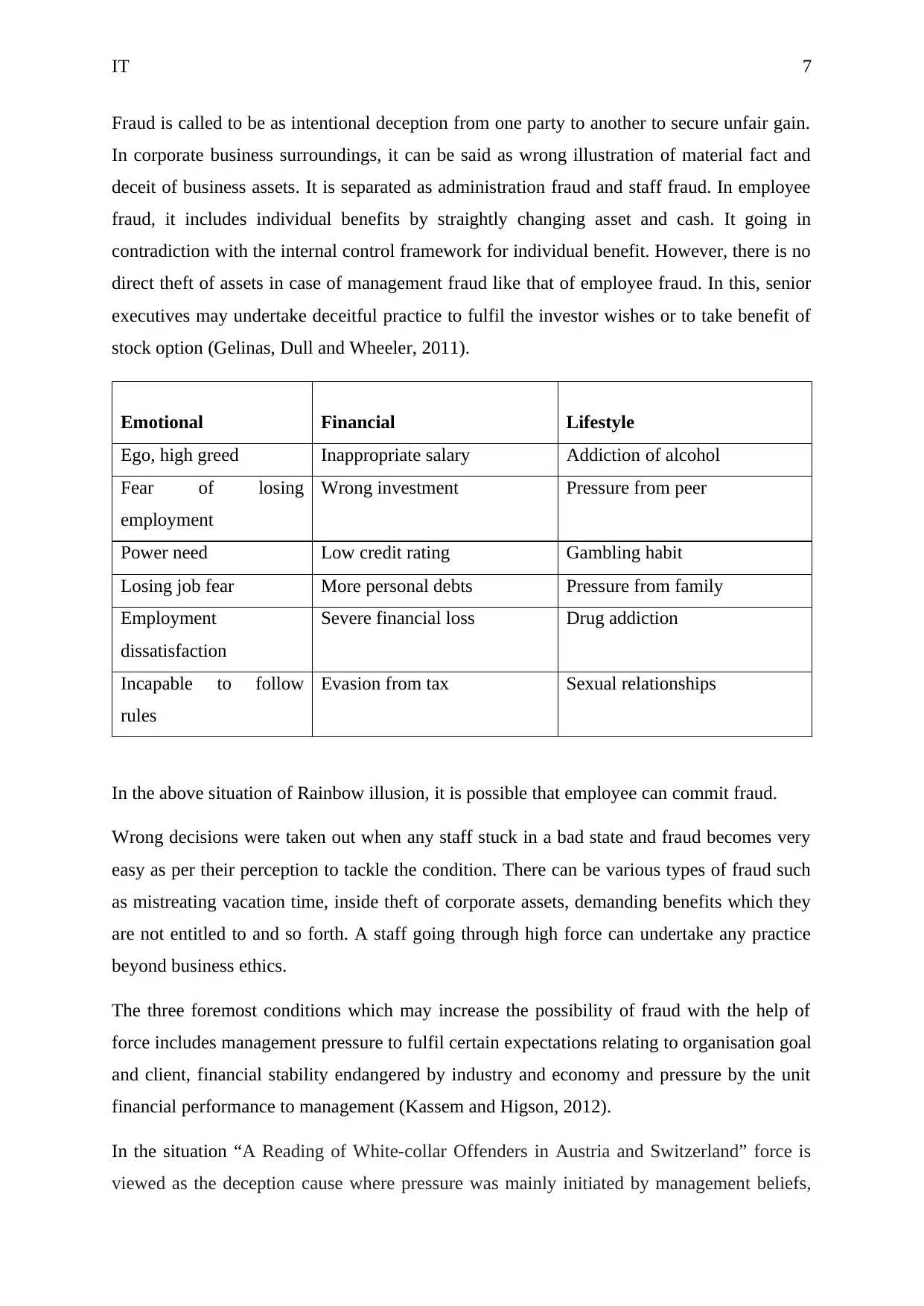

Fraud is called to be as intentional deception from one party to another to secure unfair gain.

In corporate business surroundings, it can be said as wrong illustration of material fact and

deceit of business assets. It is separated as administration fraud and staff fraud. In employee

fraud, it includes individual benefits by straightly changing asset and cash. It going in

contradiction with the internal control framework for individual benefit. However, there is no

direct theft of assets in case of management fraud like that of employee fraud. In this, senior

executives may undertake deceitful practice to fulfil the investor wishes or to take benefit of

stock option (Gelinas, Dull and Wheeler, 2011).

Emotional Financial Lifestyle

Ego, high greed Inappropriate salary Addiction of alcohol

Fear of losing

employment

Wrong investment Pressure from peer

Power need Low credit rating Gambling habit

Losing job fear More personal debts Pressure from family

Employment

dissatisfaction

Severe financial loss Drug addiction

Incapable to follow

rules

Evasion from tax Sexual relationships

In the above situation of Rainbow illusion, it is possible that employee can commit fraud.

Wrong decisions were taken out when any staff stuck in a bad state and fraud becomes very

easy as per their perception to tackle the condition. There can be various types of fraud such

as mistreating vacation time, inside theft of corporate assets, demanding benefits which they

are not entitled to and so forth. A staff going through high force can undertake any practice

beyond business ethics.

The three foremost conditions which may increase the possibility of fraud with the help of

force includes management pressure to fulfil certain expectations relating to organisation goal

and client, financial stability endangered by industry and economy and pressure by the unit

financial performance to management (Kassem and Higson, 2012).

In the situation “A Reading of White-collar Offenders in Austria and Switzerland” force is

viewed as the deception cause where pressure was mainly initiated by management beliefs,

Fraud is called to be as intentional deception from one party to another to secure unfair gain.

In corporate business surroundings, it can be said as wrong illustration of material fact and

deceit of business assets. It is separated as administration fraud and staff fraud. In employee

fraud, it includes individual benefits by straightly changing asset and cash. It going in

contradiction with the internal control framework for individual benefit. However, there is no

direct theft of assets in case of management fraud like that of employee fraud. In this, senior

executives may undertake deceitful practice to fulfil the investor wishes or to take benefit of

stock option (Gelinas, Dull and Wheeler, 2011).

Emotional Financial Lifestyle

Ego, high greed Inappropriate salary Addiction of alcohol

Fear of losing

employment

Wrong investment Pressure from peer

Power need Low credit rating Gambling habit

Losing job fear More personal debts Pressure from family

Employment

dissatisfaction

Severe financial loss Drug addiction

Incapable to follow

rules

Evasion from tax Sexual relationships

In the above situation of Rainbow illusion, it is possible that employee can commit fraud.

Wrong decisions were taken out when any staff stuck in a bad state and fraud becomes very

easy as per their perception to tackle the condition. There can be various types of fraud such

as mistreating vacation time, inside theft of corporate assets, demanding benefits which they

are not entitled to and so forth. A staff going through high force can undertake any practice

beyond business ethics.

The three foremost conditions which may increase the possibility of fraud with the help of

force includes management pressure to fulfil certain expectations relating to organisation goal

and client, financial stability endangered by industry and economy and pressure by the unit

financial performance to management (Kassem and Higson, 2012).

In the situation “A Reading of White-collar Offenders in Austria and Switzerland” force is

viewed as the deception cause where pressure was mainly initiated by management beliefs,

IT 8

stock market and other involved parties with also including harassment, maltreatment in

workplace, etc (Fuss and Hecker, 2008).

Any person who has greater level of individual ethics with low forces and narrow prospect to

compel fraud acts fairly rather than one who has low level of individual ethics with high

situational forces and perceives higher opportunities to undertake fraud. One can also not

commit fraud if there is no opportunity and no problem how challenging the situational force

is. The opportunity can also be restricted with execution of control procedures and this

ultimately precludes the conditional pressure in an organisation like Rainbow Illusion that

upsurge the possibility of fraud (Hall, 2012).

Reasons for companies to install a distributed computer

system rather than centralised one

When components of a software system are shared among multiple computers to enhance

performance and efficiency, it is termed as distributed computer system (Ricci, Rokach and

Shapira, 2011). It helps in identifying the IT functions into lesser information processing

units that are shared to end users and positioned under their control. On the other hand, all

data processing is undertaken by one or more larger computers kept at a central location in

centralised computer system and it serves at all areas of the enterprise (Hall, 2012).

There is more popular in relation with distribution computer system and it is because due to

the following reason –

Efficiency – In distributed system, the efficiency is being advanced because of gathering of

multiple computes operating parallel to each other and this breaks complex issues into

smaller fragments (Huebscher and McCann, 2008).

Reduction of cost: In distributed system, there is elimination of centralised tasks of data

control and conversion and condense complexity in application which benefits to decrease

development and maintenance costs and ultimately this enhances reduction in cost.

Backup: Backup is effectively available in distributed computer system with arrival of any

disaster such as earthquake, flood and fires. There will not be a big loss if disaster destroys a

single site and it can be regulated by other information processing unit.

stock market and other involved parties with also including harassment, maltreatment in

workplace, etc (Fuss and Hecker, 2008).

Any person who has greater level of individual ethics with low forces and narrow prospect to

compel fraud acts fairly rather than one who has low level of individual ethics with high

situational forces and perceives higher opportunities to undertake fraud. One can also not

commit fraud if there is no opportunity and no problem how challenging the situational force

is. The opportunity can also be restricted with execution of control procedures and this

ultimately precludes the conditional pressure in an organisation like Rainbow Illusion that

upsurge the possibility of fraud (Hall, 2012).

Reasons for companies to install a distributed computer

system rather than centralised one

When components of a software system are shared among multiple computers to enhance

performance and efficiency, it is termed as distributed computer system (Ricci, Rokach and

Shapira, 2011). It helps in identifying the IT functions into lesser information processing

units that are shared to end users and positioned under their control. On the other hand, all

data processing is undertaken by one or more larger computers kept at a central location in

centralised computer system and it serves at all areas of the enterprise (Hall, 2012).

There is more popular in relation with distribution computer system and it is because due to

the following reason –

Efficiency – In distributed system, the efficiency is being advanced because of gathering of

multiple computes operating parallel to each other and this breaks complex issues into

smaller fragments (Huebscher and McCann, 2008).

Reduction of cost: In distributed system, there is elimination of centralised tasks of data

control and conversion and condense complexity in application which benefits to decrease

development and maintenance costs and ultimately this enhances reduction in cost.

Backup: Backup is effectively available in distributed computer system with arrival of any

disaster such as earthquake, flood and fires. There will not be a big loss if disaster destroys a

single site and it can be regulated by other information processing unit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IT 9

However there is much difficulty and complexity in developing distributed computing

systems but with more of its benefits and flexibility, the deployment and use of this system

by the enterprises are growing speedily.

However there is much difficulty and complexity in developing distributed computing

systems but with more of its benefits and flexibility, the deployment and use of this system

by the enterprises are growing speedily.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IT 10

Conclusion

Ultimately, there should be proper implementation of all sides of accounting information to

sustain significant internal control to avoid unethical actions and fraud. In addition, this

report also discusses about situational pressure and importance of distributed computerised

system. It shows that accounting information system plays an important role for the effective

functioning of an enterprise. There is also an interconnection amid transaction processing

cycle and in scenario of Rainbow illusion, strength attributed has highly contributed in sales

transaction control with evading many issues.

Accounting information system offers various benefits to any businesses such as valid

transaction record, properly authorised transactions, fair and true disclosure and so forth.

Though, if any system is altered then it can negatively impact any corporate like Rainbow

Illusion.

Conclusion

Ultimately, there should be proper implementation of all sides of accounting information to

sustain significant internal control to avoid unethical actions and fraud. In addition, this

report also discusses about situational pressure and importance of distributed computerised

system. It shows that accounting information system plays an important role for the effective

functioning of an enterprise. There is also an interconnection amid transaction processing

cycle and in scenario of Rainbow illusion, strength attributed has highly contributed in sales

transaction control with evading many issues.

Accounting information system offers various benefits to any businesses such as valid

transaction record, properly authorised transactions, fair and true disclosure and so forth.

Though, if any system is altered then it can negatively impact any corporate like Rainbow

Illusion.

IT 11

References

Batt, R. and Colvin, A.J., 2011. An employment systems approach to turnover: Human

resources practices, quits, dismissals, and performance. Academy of management

Journal, 54(4), pp.695-717.

Chang, M.K., Cheung, W., Cheng, C.H. and Yeung, J.H., 2008. Understanding ERP system

adoption from the user's perspective. International Journal of production economics, 113(2),

pp.928-942.

Fuss, R. and Hecker, A., 2008. Profiling white-collar crime: Evidence from German-speaking

countries. Corporate Ownership and Control, 5(4), pp.149-161.

Gelinas, U.J., Dull, R.B. and Wheeler, P., 2011. Accounting information systems. USA:

Cengage learning.

Grabski, S.V., Leech, S.A. and Schmidt, P.J., 2011. A review of ERP research: A future

agenda for accounting information systems. Journal of information systems, 25(1), pp.37-78.

Hall, J.A., 2012. Accounting information systems. USA: Cengage Learning.

Huebscher, M.C. and McCann, J.A., 2008. A survey of autonomic computing—degrees,

models, and applications. ACM Computing Surveys (CSUR), 40(3), p.7.

Karsak, E.E. and Özogul, C.O., 2009. An integrated decision making approach for ERP

system selection. Expert systems with Applications, 36(1), pp.660-667.

Kassem, R. and Higson, A., 2012. The new fraud triangle model. Journal of Emerging

Trends in Economics and Management Sciences, 3(3), pp.191-195.

Putra, A. and Suryaputra, A., 2014. Implementation of Accurate Accounting Information

Systems To Mid-Scale Wholesale Company. IC-ITECHS, 1(1), pp.164-168.

Ricci, F., Rokach, L. and Shapira, B., 2011. Introduction to recommender systems handbook.

In Recommender systems handbook (pp. 1-35). MA: Springer, Boston.

Rimal, B.P., Jukan, A., Katsaros, D. and Goeleven, Y., 2011. Architectural requirements for

cloud computing systems: an enterprise cloud approach. Journal of Grid Computing, 9(1),

pp.3-26.

References

Batt, R. and Colvin, A.J., 2011. An employment systems approach to turnover: Human

resources practices, quits, dismissals, and performance. Academy of management

Journal, 54(4), pp.695-717.

Chang, M.K., Cheung, W., Cheng, C.H. and Yeung, J.H., 2008. Understanding ERP system

adoption from the user's perspective. International Journal of production economics, 113(2),

pp.928-942.

Fuss, R. and Hecker, A., 2008. Profiling white-collar crime: Evidence from German-speaking

countries. Corporate Ownership and Control, 5(4), pp.149-161.

Gelinas, U.J., Dull, R.B. and Wheeler, P., 2011. Accounting information systems. USA:

Cengage learning.

Grabski, S.V., Leech, S.A. and Schmidt, P.J., 2011. A review of ERP research: A future

agenda for accounting information systems. Journal of information systems, 25(1), pp.37-78.

Hall, J.A., 2012. Accounting information systems. USA: Cengage Learning.

Huebscher, M.C. and McCann, J.A., 2008. A survey of autonomic computing—degrees,

models, and applications. ACM Computing Surveys (CSUR), 40(3), p.7.

Karsak, E.E. and Özogul, C.O., 2009. An integrated decision making approach for ERP

system selection. Expert systems with Applications, 36(1), pp.660-667.

Kassem, R. and Higson, A., 2012. The new fraud triangle model. Journal of Emerging

Trends in Economics and Management Sciences, 3(3), pp.191-195.

Putra, A. and Suryaputra, A., 2014. Implementation of Accurate Accounting Information

Systems To Mid-Scale Wholesale Company. IC-ITECHS, 1(1), pp.164-168.

Ricci, F., Rokach, L. and Shapira, B., 2011. Introduction to recommender systems handbook.

In Recommender systems handbook (pp. 1-35). MA: Springer, Boston.

Rimal, B.P., Jukan, A., Katsaros, D. and Goeleven, Y., 2011. Architectural requirements for

cloud computing systems: an enterprise cloud approach. Journal of Grid Computing, 9(1),

pp.3-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.