HI5020 Corporate Accounting: Analysis of Financial Statements

VerifiedAdded on 2023/04/22

|25

|4640

|111

Report

AI Summary

This report provides a comprehensive analysis of the financial statements of three ASX-listed companies: Altura Mining, Rio Tinto, and BHP Billiton. It examines key aspects of their corporate accounting practices, focusing on the reporting of assets, liabilities, equity, other comprehensive income (OCI), and cash flows. The analysis includes a comparative assessment of debt and equity positions, cash flow activities, and items reported under OCI. Furthermore, the report delves into the accounting for corporate income tax, calculating cash tax rates and discussing deferred tax assets and liabilities. The study aims to provide insights into the financial health and reporting strategies of these companies, highlighting significant changes and trends in their financial performance.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary

Aims of the report is to analyse the finance statement of 3 ASX listed entities and the way

they reported various items like assets, liabilities, other comprehensive income and cash flow

statement. For this report 3 companies that will be taken into consideration are Altura

Mining, Rio Tinto and BHP Billiton. The report will represent the amount of changes for

assets, liabilities and cash flows. It will further focus on corporate income tax and will

compute the cash tax rate of the companies.

CORPORATE ACCOUNTING

Executive summary

Aims of the report is to analyse the finance statement of 3 ASX listed entities and the way

they reported various items like assets, liabilities, other comprehensive income and cash flow

statement. For this report 3 companies that will be taken into consideration are Altura

Mining, Rio Tinto and BHP Billiton. The report will represent the amount of changes for

assets, liabilities and cash flows. It will further focus on corporate income tax and will

compute the cash tax rate of the companies.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Equity and liabilities..................................................................................................................3

(i) Equity items....................................................................................................................3

(ii) Liability items................................................................................................................6

(iii) Comparative analysis of debt and equity position.........................................................9

Cash flow statement.................................................................................................................10

(iv) Listed cash flow items...............................................................................................10

(v) Comparative analysis.................................................................................................11

(vi) Comparative analysis selected for explaining insights..............................................14

Other comprehensive income statement..................................................................................14

(vii) Reported items under other comprehensive income (OCI).......................................14

(viii) Why items of OCI are not reported in the profit and loss statement.........................16

(ix) Comparative analysis of items reported under OCI..................................................16

(x) Including comprehensive income for evaluating the manager’s performance..........16

Accounting for corporate income tax.......................................................................................17

(xi) Tax expenses recorded in financial statement of 2017..............................................17

(xii) Effective rate of tax...................................................................................................17

(xiii) Deferred tax assets or deferred tax liabilities............................................................17

(xiv) Increase or decrease in deferred tax assets or liabilities reported by the entities......18

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Equity and liabilities..................................................................................................................3

(i) Equity items....................................................................................................................3

(ii) Liability items................................................................................................................6

(iii) Comparative analysis of debt and equity position.........................................................9

Cash flow statement.................................................................................................................10

(iv) Listed cash flow items...............................................................................................10

(v) Comparative analysis.................................................................................................11

(vi) Comparative analysis selected for explaining insights..............................................14

Other comprehensive income statement..................................................................................14

(vii) Reported items under other comprehensive income (OCI).......................................14

(viii) Why items of OCI are not reported in the profit and loss statement.........................16

(ix) Comparative analysis of items reported under OCI..................................................16

(x) Including comprehensive income for evaluating the manager’s performance..........16

Accounting for corporate income tax.......................................................................................17

(xi) Tax expenses recorded in financial statement of 2017..............................................17

(xii) Effective rate of tax...................................................................................................17

(xiii) Deferred tax assets or deferred tax liabilities............................................................17

(xiv) Increase or decrease in deferred tax assets or liabilities reported by the entities......18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

(xv) Cash tax.....................................................................................................................18

(xvi) Rate of cash tax.........................................................................................................19

(xvii) Difference of cash tax rate from the book tax rate....................................................19

Conclusion................................................................................................................................19

Reference..................................................................................................................................21

CORPORATE ACCOUNTING

(xv) Cash tax.....................................................................................................................18

(xvi) Rate of cash tax.........................................................................................................19

(xvii) Difference of cash tax rate from the book tax rate....................................................19

Conclusion................................................................................................................................19

Reference..................................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Introduction

Altura Mining is an ASX listed company based in Perth, Australia and carries on the

business of lithium. It is engaged in exploration and development of coal mining and

minerals. The company is fulfilling the increasing demand of raw material required for

manufacturing lithium ion batteries. It is focussed on developing and constructing its 100%

owned lithium project Pilgangoora located in Pilbara, Western Australia (Alturamining.com,

2018).

Incorporated on 30th March 1962, Rio Tinto became the leading mining and metal

company in Australia. It’s major business is finding, mining and processing of mineral

resources. It has various segments like Iron Ore, Aluminium, minerals and energy, Diamonds

and copper. The company assists in meeting the society’s requirement through different

researches and innovations and help the world to grow (Riotinto.com, 2018).

Established during 2001 through merging of Broken Hill, Billiton and Proprietary,

BHP Billiton became the biggest mining and global resources organization. It is 7th biggest

producer in world for aluminium and considered as the largest producer of manganese,

copper, nickel, aluminium, iron ore, titanium, uranium and silver (BHP, 2018).

Equity and liabilities

(i) Equity items

Altura Mining – equity items listed in the balance sheet of the company are as follows –

Contributed equity – contributed equity that is also known as paid in capital is the

component of total equity recognised in the balance sheet of the company. Another

way of reporting the contributed equity is to record it under the head shareholder’s

CORPORATE ACCOUNTING

Introduction

Altura Mining is an ASX listed company based in Perth, Australia and carries on the

business of lithium. It is engaged in exploration and development of coal mining and

minerals. The company is fulfilling the increasing demand of raw material required for

manufacturing lithium ion batteries. It is focussed on developing and constructing its 100%

owned lithium project Pilgangoora located in Pilbara, Western Australia (Alturamining.com,

2018).

Incorporated on 30th March 1962, Rio Tinto became the leading mining and metal

company in Australia. It’s major business is finding, mining and processing of mineral

resources. It has various segments like Iron Ore, Aluminium, minerals and energy, Diamonds

and copper. The company assists in meeting the society’s requirement through different

researches and innovations and help the world to grow (Riotinto.com, 2018).

Established during 2001 through merging of Broken Hill, Billiton and Proprietary,

BHP Billiton became the biggest mining and global resources organization. It is 7th biggest

producer in world for aluminium and considered as the largest producer of manganese,

copper, nickel, aluminium, iron ore, titanium, uranium and silver (BHP, 2018).

Equity and liabilities

(i) Equity items

Altura Mining – equity items listed in the balance sheet of the company are as follows –

Contributed equity – contributed equity that is also known as paid in capital is the

component of total equity recognised in the balance sheet of the company. Another

way of reporting the contributed equity is to record it under the head shareholder’s

5

CORPORATE ACCOUNTING

equity as a separate account. It represents the contributed amount of shareholders for

share of ownership in the company (Titman, Keown & Martin, 2017).

Reserves – reserve is considered as an equity component that does not consider the

part of basis share capital. It represents the surplus accumulated through various

sources including revaluation reserve that is upward revaluation of the assets or

issuance of share at premium (Maaloul & Zéghal, 2015).

Accumulated loss – generally the amount of retained earnings that is the accumulated

earnings are used for distributing dividend. If the account balances of accumulated

earning shows negative figure the amount of retained earnings will also represent

negative balance that is reported as accumulated loss.

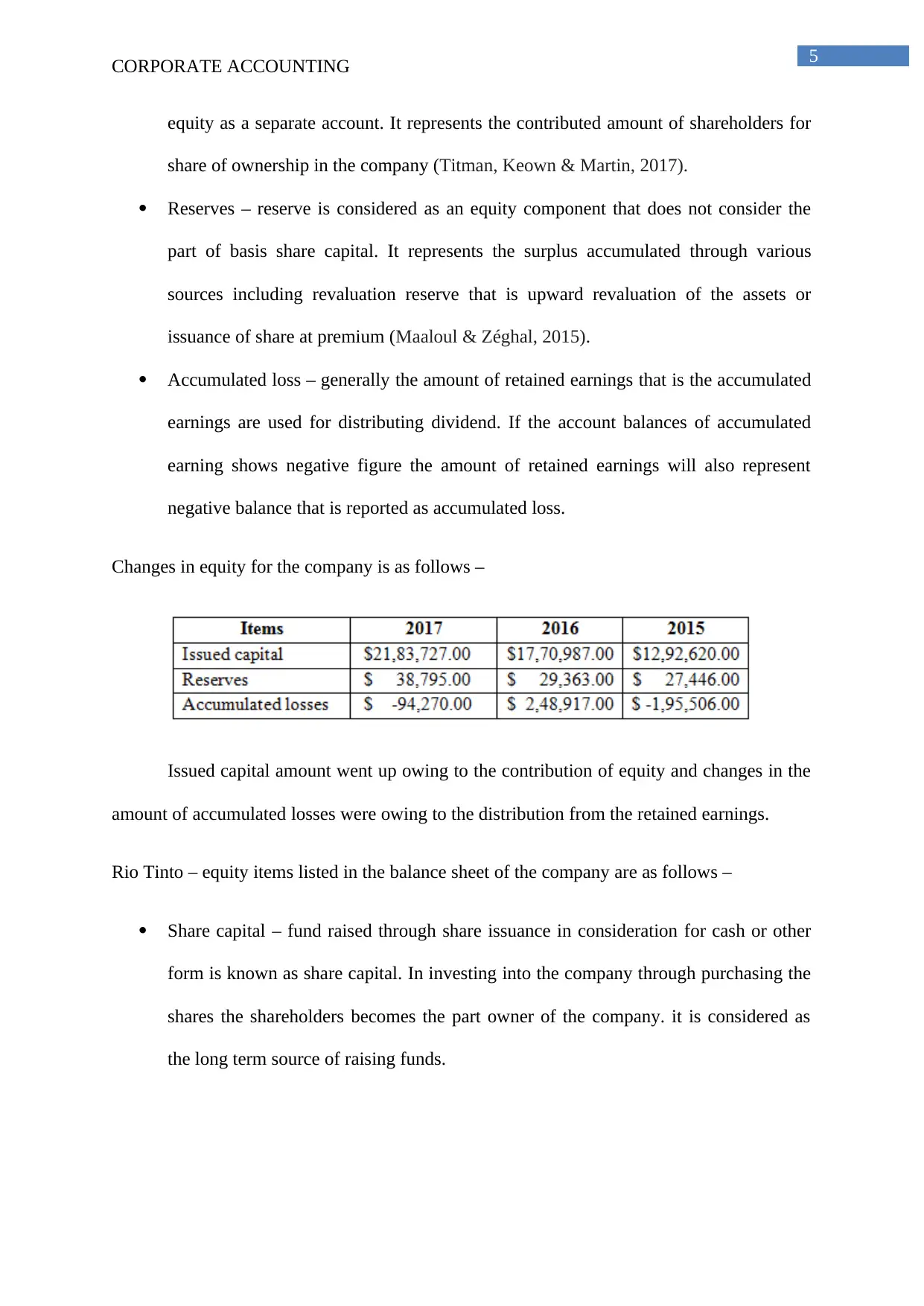

Changes in equity for the company is as follows –

Issued capital amount went up owing to the contribution of equity and changes in the

amount of accumulated losses were owing to the distribution from the retained earnings.

Rio Tinto – equity items listed in the balance sheet of the company are as follows –

Share capital – fund raised through share issuance in consideration for cash or other

form is known as share capital. In investing into the company through purchasing the

shares the shareholders becomes the part owner of the company. it is considered as

the long term source of raising funds.

CORPORATE ACCOUNTING

equity as a separate account. It represents the contributed amount of shareholders for

share of ownership in the company (Titman, Keown & Martin, 2017).

Reserves – reserve is considered as an equity component that does not consider the

part of basis share capital. It represents the surplus accumulated through various

sources including revaluation reserve that is upward revaluation of the assets or

issuance of share at premium (Maaloul & Zéghal, 2015).

Accumulated loss – generally the amount of retained earnings that is the accumulated

earnings are used for distributing dividend. If the account balances of accumulated

earning shows negative figure the amount of retained earnings will also represent

negative balance that is reported as accumulated loss.

Changes in equity for the company is as follows –

Issued capital amount went up owing to the contribution of equity and changes in the

amount of accumulated losses were owing to the distribution from the retained earnings.

Rio Tinto – equity items listed in the balance sheet of the company are as follows –

Share capital – fund raised through share issuance in consideration for cash or other

form is known as share capital. In investing into the company through purchasing the

shares the shareholders becomes the part owner of the company. it is considered as

the long term source of raising funds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

Share premium – share premium is the value of share exceeding its par value. Share

premium amount can be used only for some particular purposes mentioned in the

company’s bylaws (Marshall, 2016).

Other reserves – as described for Altura Mining

Retained earnings – retained earnings is the surplus amount available at the date of

balance sheet and the amount of retained earnings is reduced with the distribution of

dividend to the shareholders (Reid & Myddelton, 2017).

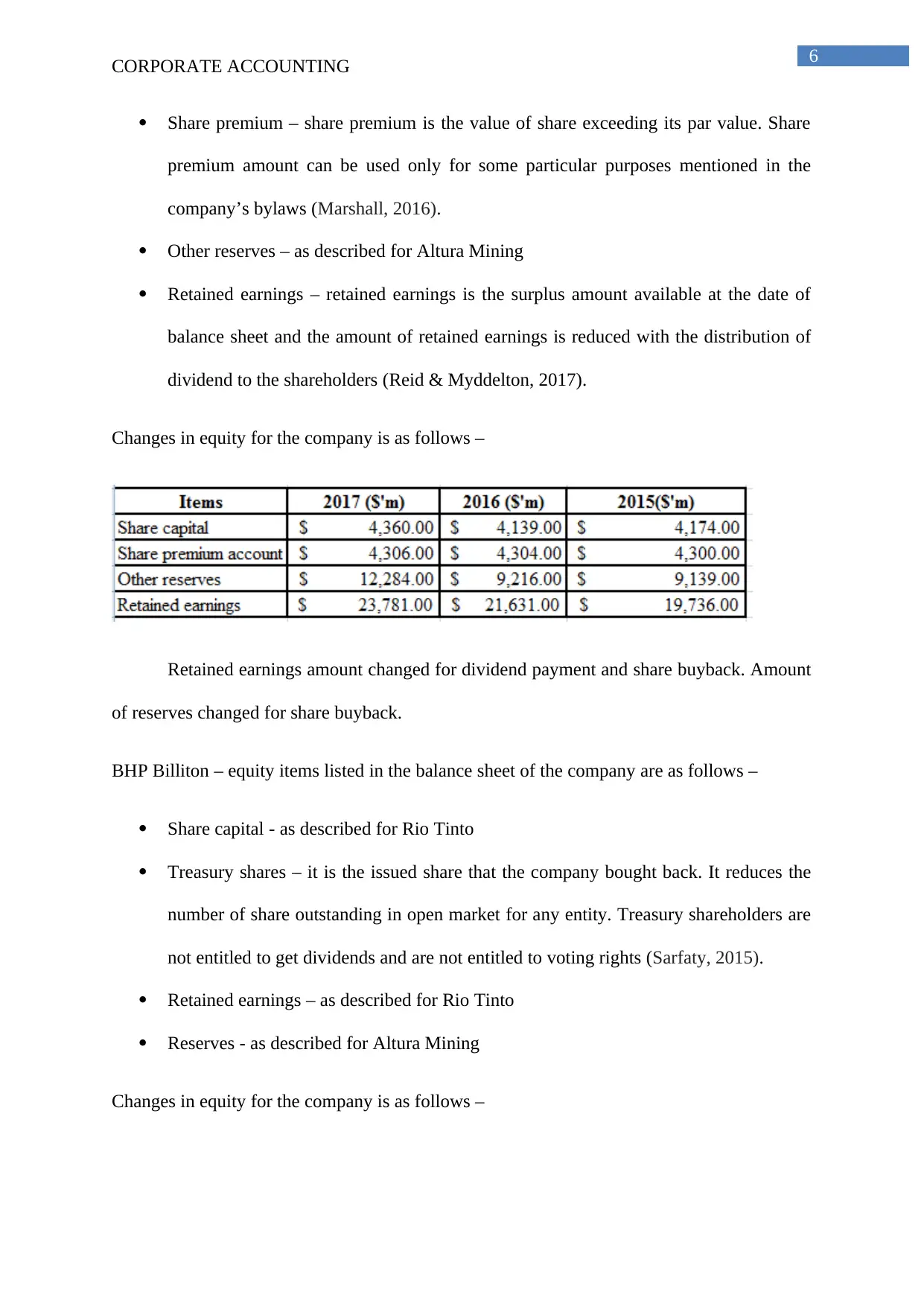

Changes in equity for the company is as follows –

Retained earnings amount changed for dividend payment and share buyback. Amount

of reserves changed for share buyback.

BHP Billiton – equity items listed in the balance sheet of the company are as follows –

Share capital - as described for Rio Tinto

Treasury shares – it is the issued share that the company bought back. It reduces the

number of share outstanding in open market for any entity. Treasury shareholders are

not entitled to get dividends and are not entitled to voting rights (Sarfaty, 2015).

Retained earnings – as described for Rio Tinto

Reserves - as described for Altura Mining

Changes in equity for the company is as follows –

CORPORATE ACCOUNTING

Share premium – share premium is the value of share exceeding its par value. Share

premium amount can be used only for some particular purposes mentioned in the

company’s bylaws (Marshall, 2016).

Other reserves – as described for Altura Mining

Retained earnings – retained earnings is the surplus amount available at the date of

balance sheet and the amount of retained earnings is reduced with the distribution of

dividend to the shareholders (Reid & Myddelton, 2017).

Changes in equity for the company is as follows –

Retained earnings amount changed for dividend payment and share buyback. Amount

of reserves changed for share buyback.

BHP Billiton – equity items listed in the balance sheet of the company are as follows –

Share capital - as described for Rio Tinto

Treasury shares – it is the issued share that the company bought back. It reduces the

number of share outstanding in open market for any entity. Treasury shareholders are

not entitled to get dividends and are not entitled to voting rights (Sarfaty, 2015).

Retained earnings – as described for Rio Tinto

Reserves - as described for Altura Mining

Changes in equity for the company is as follows –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

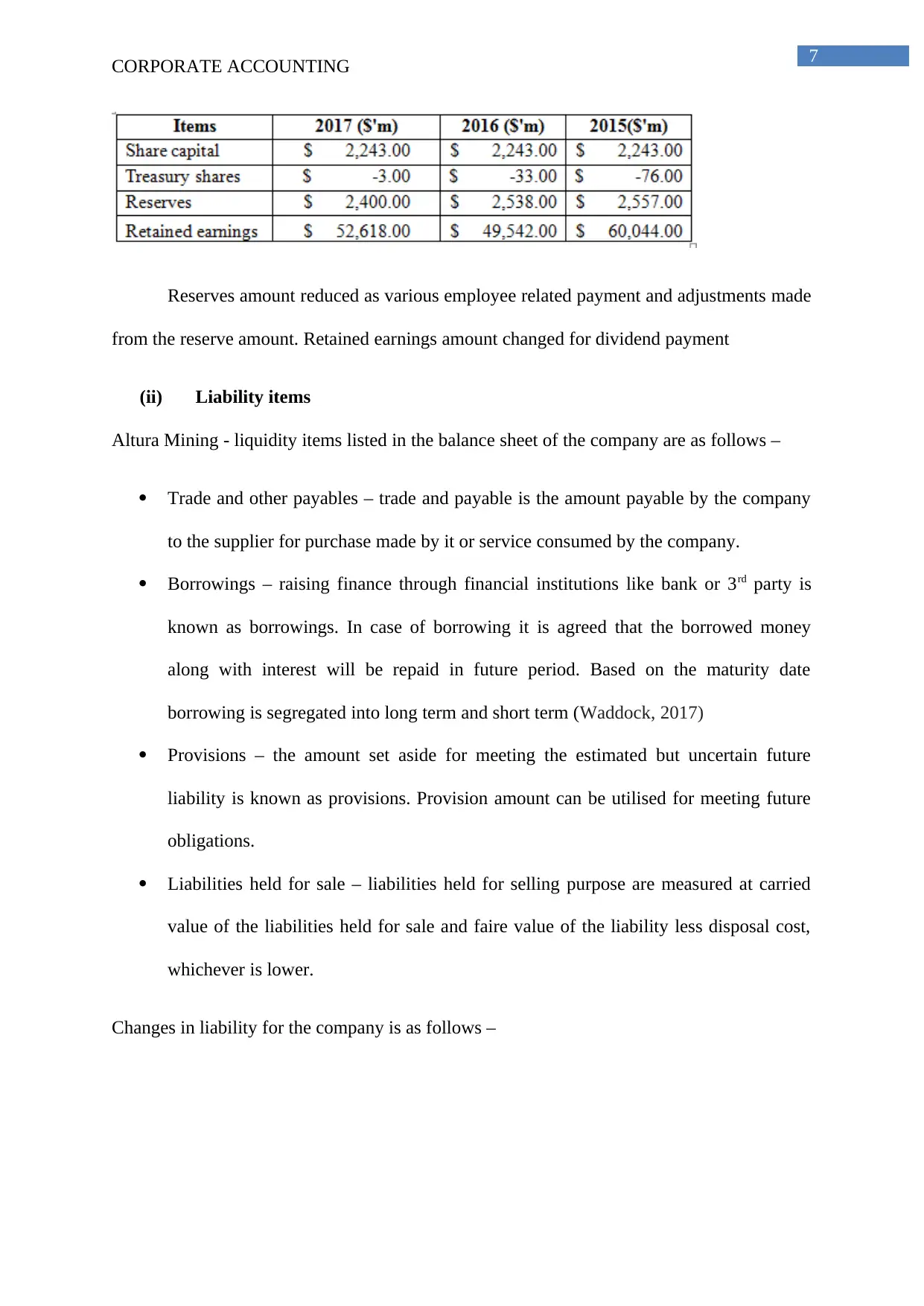

Reserves amount reduced as various employee related payment and adjustments made

from the reserve amount. Retained earnings amount changed for dividend payment

(ii) Liability items

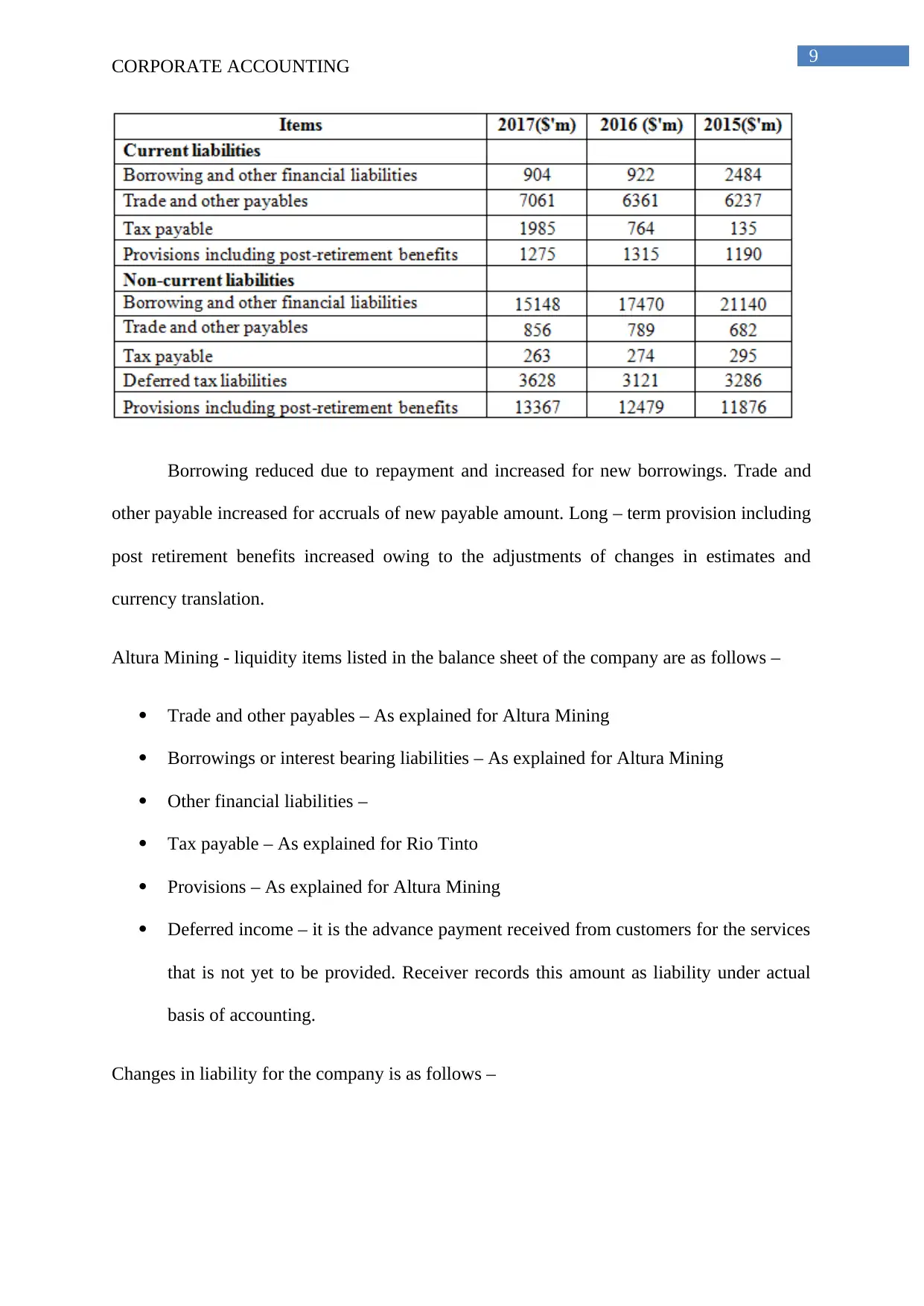

Altura Mining - liquidity items listed in the balance sheet of the company are as follows –

Trade and other payables – trade and payable is the amount payable by the company

to the supplier for purchase made by it or service consumed by the company.

Borrowings – raising finance through financial institutions like bank or 3rd party is

known as borrowings. In case of borrowing it is agreed that the borrowed money

along with interest will be repaid in future period. Based on the maturity date

borrowing is segregated into long term and short term (Waddock, 2017)

Provisions – the amount set aside for meeting the estimated but uncertain future

liability is known as provisions. Provision amount can be utilised for meeting future

obligations.

Liabilities held for sale – liabilities held for selling purpose are measured at carried

value of the liabilities held for sale and faire value of the liability less disposal cost,

whichever is lower.

Changes in liability for the company is as follows –

CORPORATE ACCOUNTING

Reserves amount reduced as various employee related payment and adjustments made

from the reserve amount. Retained earnings amount changed for dividend payment

(ii) Liability items

Altura Mining - liquidity items listed in the balance sheet of the company are as follows –

Trade and other payables – trade and payable is the amount payable by the company

to the supplier for purchase made by it or service consumed by the company.

Borrowings – raising finance through financial institutions like bank or 3rd party is

known as borrowings. In case of borrowing it is agreed that the borrowed money

along with interest will be repaid in future period. Based on the maturity date

borrowing is segregated into long term and short term (Waddock, 2017)

Provisions – the amount set aside for meeting the estimated but uncertain future

liability is known as provisions. Provision amount can be utilised for meeting future

obligations.

Liabilities held for sale – liabilities held for selling purpose are measured at carried

value of the liabilities held for sale and faire value of the liability less disposal cost,

whichever is lower.

Changes in liability for the company is as follows –

8

CORPORATE ACCOUNTING

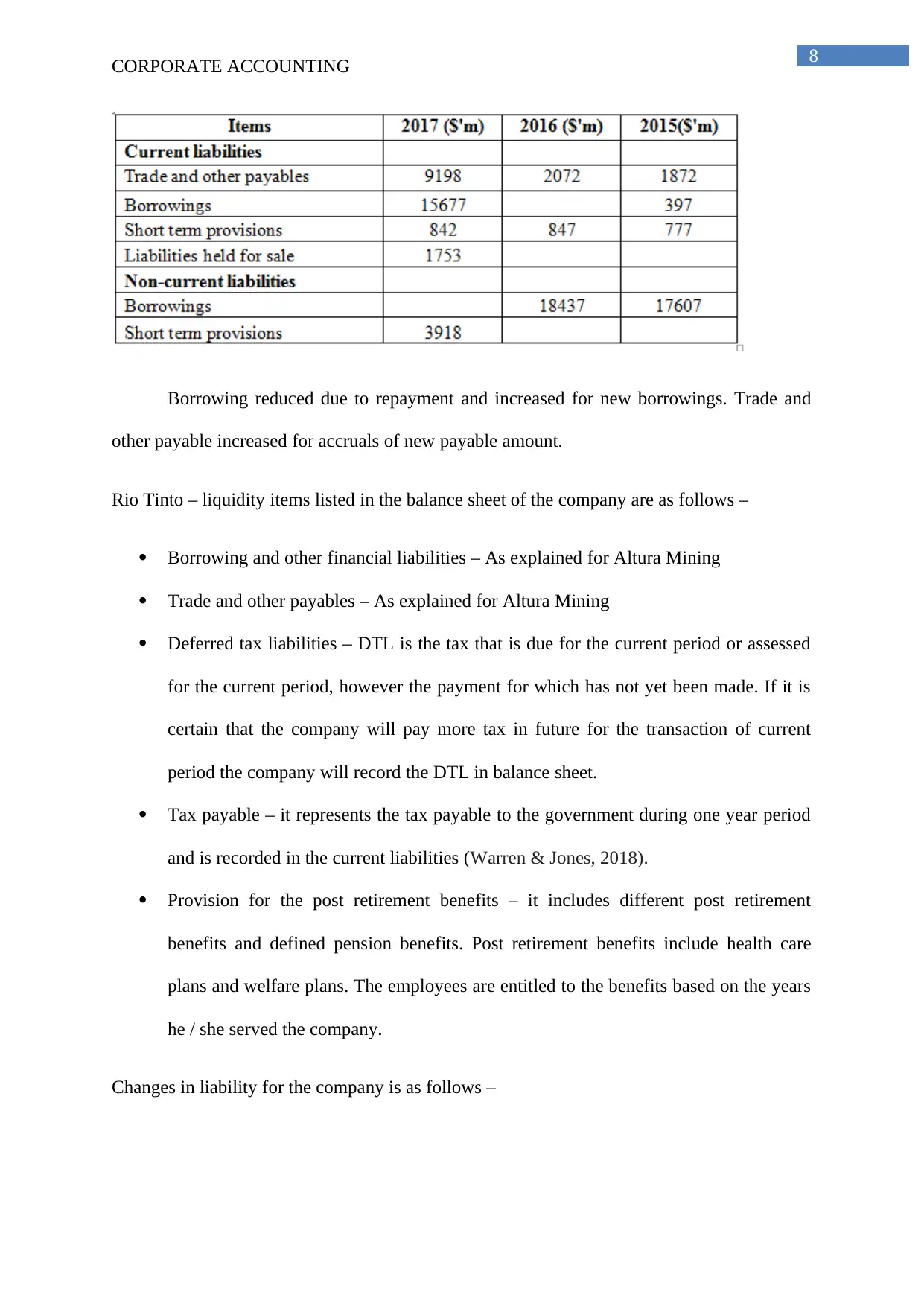

Borrowing reduced due to repayment and increased for new borrowings. Trade and

other payable increased for accruals of new payable amount.

Rio Tinto – liquidity items listed in the balance sheet of the company are as follows –

Borrowing and other financial liabilities – As explained for Altura Mining

Trade and other payables – As explained for Altura Mining

Deferred tax liabilities – DTL is the tax that is due for the current period or assessed

for the current period, however the payment for which has not yet been made. If it is

certain that the company will pay more tax in future for the transaction of current

period the company will record the DTL in balance sheet.

Tax payable – it represents the tax payable to the government during one year period

and is recorded in the current liabilities (Warren & Jones, 2018).

Provision for the post retirement benefits – it includes different post retirement

benefits and defined pension benefits. Post retirement benefits include health care

plans and welfare plans. The employees are entitled to the benefits based on the years

he / she served the company.

Changes in liability for the company is as follows –

CORPORATE ACCOUNTING

Borrowing reduced due to repayment and increased for new borrowings. Trade and

other payable increased for accruals of new payable amount.

Rio Tinto – liquidity items listed in the balance sheet of the company are as follows –

Borrowing and other financial liabilities – As explained for Altura Mining

Trade and other payables – As explained for Altura Mining

Deferred tax liabilities – DTL is the tax that is due for the current period or assessed

for the current period, however the payment for which has not yet been made. If it is

certain that the company will pay more tax in future for the transaction of current

period the company will record the DTL in balance sheet.

Tax payable – it represents the tax payable to the government during one year period

and is recorded in the current liabilities (Warren & Jones, 2018).

Provision for the post retirement benefits – it includes different post retirement

benefits and defined pension benefits. Post retirement benefits include health care

plans and welfare plans. The employees are entitled to the benefits based on the years

he / she served the company.

Changes in liability for the company is as follows –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Borrowing reduced due to repayment and increased for new borrowings. Trade and

other payable increased for accruals of new payable amount. Long – term provision including

post retirement benefits increased owing to the adjustments of changes in estimates and

currency translation.

Altura Mining - liquidity items listed in the balance sheet of the company are as follows –

Trade and other payables – As explained for Altura Mining

Borrowings or interest bearing liabilities – As explained for Altura Mining

Other financial liabilities –

Tax payable – As explained for Rio Tinto

Provisions – As explained for Altura Mining

Deferred income – it is the advance payment received from customers for the services

that is not yet to be provided. Receiver records this amount as liability under actual

basis of accounting.

Changes in liability for the company is as follows –

CORPORATE ACCOUNTING

Borrowing reduced due to repayment and increased for new borrowings. Trade and

other payable increased for accruals of new payable amount. Long – term provision including

post retirement benefits increased owing to the adjustments of changes in estimates and

currency translation.

Altura Mining - liquidity items listed in the balance sheet of the company are as follows –

Trade and other payables – As explained for Altura Mining

Borrowings or interest bearing liabilities – As explained for Altura Mining

Other financial liabilities –

Tax payable – As explained for Rio Tinto

Provisions – As explained for Altura Mining

Deferred income – it is the advance payment received from customers for the services

that is not yet to be provided. Receiver records this amount as liability under actual

basis of accounting.

Changes in liability for the company is as follows –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

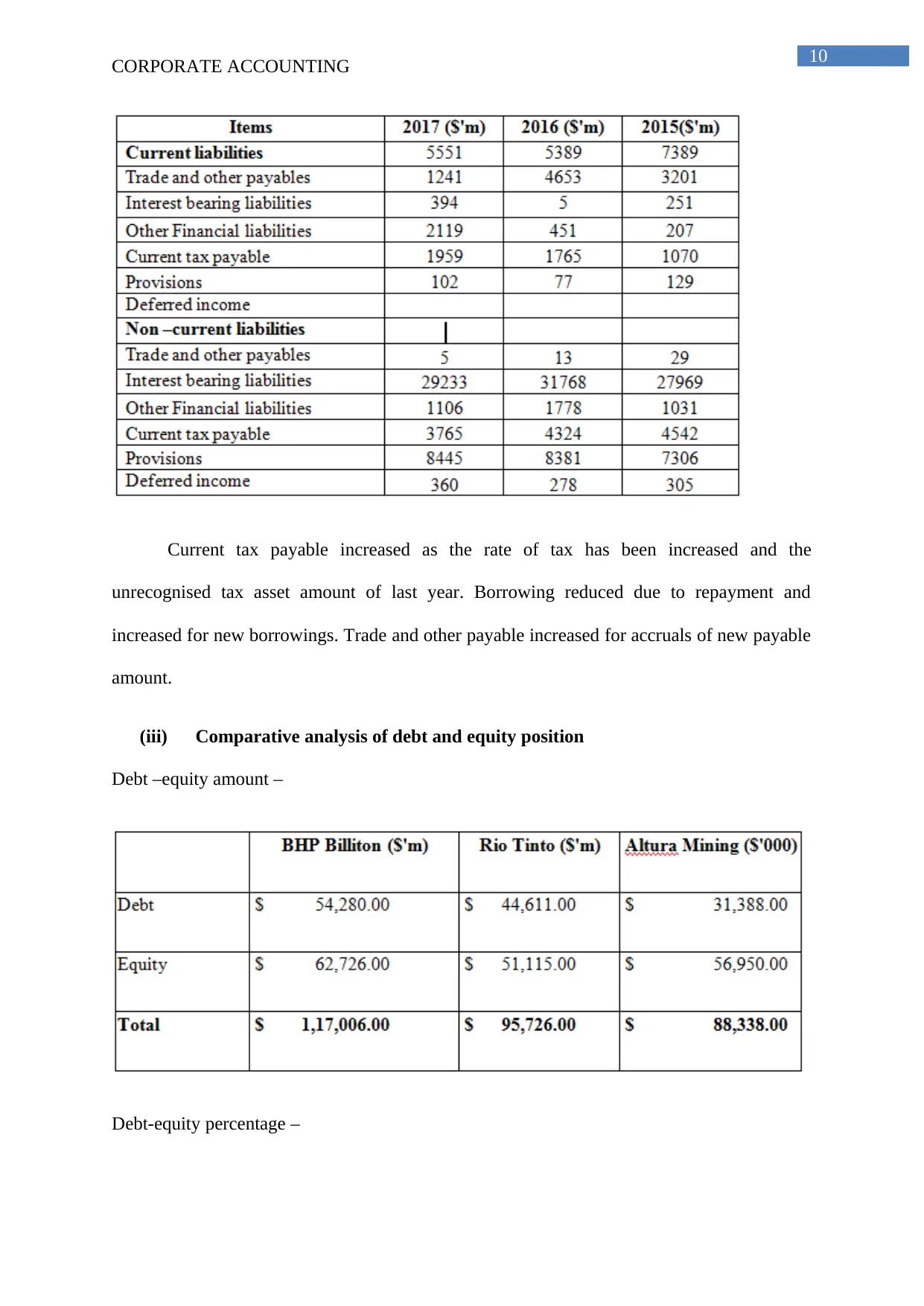

Current tax payable increased as the rate of tax has been increased and the

unrecognised tax asset amount of last year. Borrowing reduced due to repayment and

increased for new borrowings. Trade and other payable increased for accruals of new payable

amount.

(iii) Comparative analysis of debt and equity position

Debt –equity amount –

Debt-equity percentage –

CORPORATE ACCOUNTING

Current tax payable increased as the rate of tax has been increased and the

unrecognised tax asset amount of last year. Borrowing reduced due to repayment and

increased for new borrowings. Trade and other payable increased for accruals of new payable

amount.

(iii) Comparative analysis of debt and equity position

Debt –equity amount –

Debt-equity percentage –

11

CORPORATE ACCOUNTING

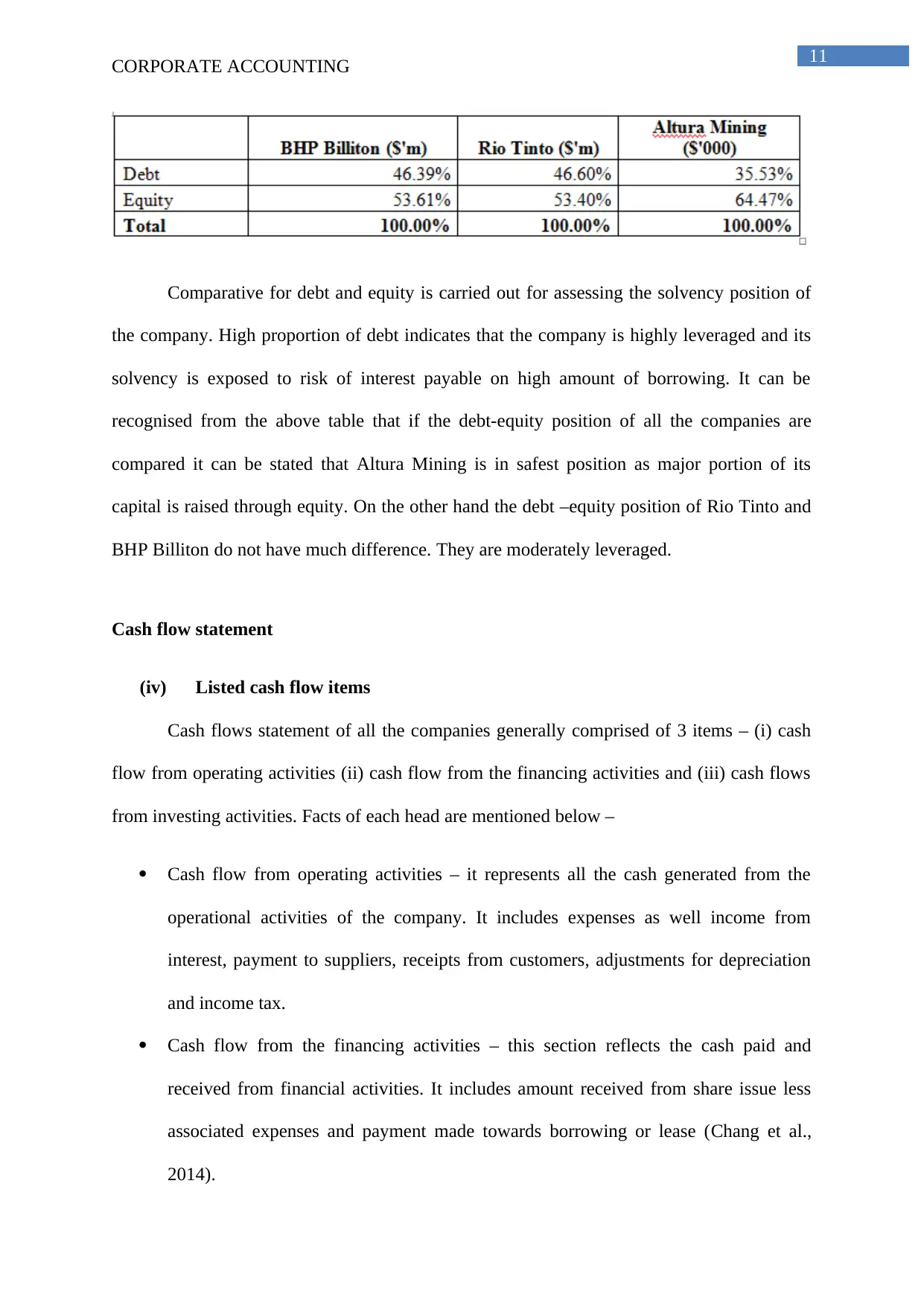

Comparative for debt and equity is carried out for assessing the solvency position of

the company. High proportion of debt indicates that the company is highly leveraged and its

solvency is exposed to risk of interest payable on high amount of borrowing. It can be

recognised from the above table that if the debt-equity position of all the companies are

compared it can be stated that Altura Mining is in safest position as major portion of its

capital is raised through equity. On the other hand the debt –equity position of Rio Tinto and

BHP Billiton do not have much difference. They are moderately leveraged.

Cash flow statement

(iv) Listed cash flow items

Cash flows statement of all the companies generally comprised of 3 items – (i) cash

flow from operating activities (ii) cash flow from the financing activities and (iii) cash flows

from investing activities. Facts of each head are mentioned below –

Cash flow from operating activities – it represents all the cash generated from the

operational activities of the company. It includes expenses as well income from

interest, payment to suppliers, receipts from customers, adjustments for depreciation

and income tax.

Cash flow from the financing activities – this section reflects the cash paid and

received from financial activities. It includes amount received from share issue less

associated expenses and payment made towards borrowing or lease (Chang et al.,

2014).

CORPORATE ACCOUNTING

Comparative for debt and equity is carried out for assessing the solvency position of

the company. High proportion of debt indicates that the company is highly leveraged and its

solvency is exposed to risk of interest payable on high amount of borrowing. It can be

recognised from the above table that if the debt-equity position of all the companies are

compared it can be stated that Altura Mining is in safest position as major portion of its

capital is raised through equity. On the other hand the debt –equity position of Rio Tinto and

BHP Billiton do not have much difference. They are moderately leveraged.

Cash flow statement

(iv) Listed cash flow items

Cash flows statement of all the companies generally comprised of 3 items – (i) cash

flow from operating activities (ii) cash flow from the financing activities and (iii) cash flows

from investing activities. Facts of each head are mentioned below –

Cash flow from operating activities – it represents all the cash generated from the

operational activities of the company. It includes expenses as well income from

interest, payment to suppliers, receipts from customers, adjustments for depreciation

and income tax.

Cash flow from the financing activities – this section reflects the cash paid and

received from financial activities. It includes amount received from share issue less

associated expenses and payment made towards borrowing or lease (Chang et al.,

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.