HI5020 Corporate Accounting: Analyzing CBA and NAB Financials

VerifiedAdded on 2023/06/04

|24

|3965

|457

Report

AI Summary

This report provides a comparative analysis of the financial statements of Commonwealth Bank of Australia (CBA) and National Australia Bank (NAB), focusing on consistency in annual reports and compliance with accounting standards. It examines key elements such as owner’s equity, cash flow statements, deferred tax accounting, and other comprehensive income, detailing their impact on the companies' financial positions. The analysis covers ordinary share capital, reserves, retained earnings, operating activities, investing activities, and financing activities. Ultimately, the report concludes that both banks adhere to similar accounting rules and regulations, ensuring relevant information is provided to stakeholders. Desklib offers a platform for students to explore similar documents and solved assignments for further study.

RUNNING HEAD: CORPORATE ACCOUNTING

Corporate accounting

Corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 2

Executive Summary

The report is prepared on Commonwealth Bank of Australia and National Bank of Australia with

a purpose to determine the consistency in the contents of its annual reports. The report

summarizes the presentation, disclosure, compliance with accounting standards and other factors

in order to ensure that proper accounting rules have been followed by the banks. It discusses the

items of Owner’s equity, cash flow statement, accounting for deferred tax and other

comprehensive income statement. The items are explained in detail and the impact of the same

on company’s financial position is analyzed. The report concludes that the financial reports of

both the banks are prepared by keeping in mind the same rules and regulations in order to

provide relevant information to the stakeholders.

Executive Summary

The report is prepared on Commonwealth Bank of Australia and National Bank of Australia with

a purpose to determine the consistency in the contents of its annual reports. The report

summarizes the presentation, disclosure, compliance with accounting standards and other factors

in order to ensure that proper accounting rules have been followed by the banks. It discusses the

items of Owner’s equity, cash flow statement, accounting for deferred tax and other

comprehensive income statement. The items are explained in detail and the impact of the same

on company’s financial position is analyzed. The report concludes that the financial reports of

both the banks are prepared by keeping in mind the same rules and regulations in order to

provide relevant information to the stakeholders.

Corporate accounting 3

Contents

Introduction.................................................................................................................................................4

Description of the companies......................................................................................................................4

Owners’ Equity...........................................................................................................................................5

Part 1.......................................................................................................................................................5

Part 2.......................................................................................................................................................7

Cash Flow Statement...................................................................................................................................7

Part 3.......................................................................................................................................................7

Part 4.....................................................................................................................................................10

Part 5.....................................................................................................................................................15

Other Comprehensive Income Statement..................................................................................................16

Part 6.....................................................................................................................................................17

Part 7.....................................................................................................................................................18

Part 8.....................................................................................................................................................18

Part 9.....................................................................................................................................................18

Accounting for corporate income tax........................................................................................................19

Part 10...................................................................................................................................................20

Part 11...................................................................................................................................................21

Part 12...................................................................................................................................................21

Part 13...................................................................................................................................................21

Part 14...................................................................................................................................................21

Part 15...................................................................................................................................................21

Part 16...................................................................................................................................................21

Conclusion.................................................................................................................................................22

References.................................................................................................................................................23

Contents

Introduction.................................................................................................................................................4

Description of the companies......................................................................................................................4

Owners’ Equity...........................................................................................................................................5

Part 1.......................................................................................................................................................5

Part 2.......................................................................................................................................................7

Cash Flow Statement...................................................................................................................................7

Part 3.......................................................................................................................................................7

Part 4.....................................................................................................................................................10

Part 5.....................................................................................................................................................15

Other Comprehensive Income Statement..................................................................................................16

Part 6.....................................................................................................................................................17

Part 7.....................................................................................................................................................18

Part 8.....................................................................................................................................................18

Part 9.....................................................................................................................................................18

Accounting for corporate income tax........................................................................................................19

Part 10...................................................................................................................................................20

Part 11...................................................................................................................................................21

Part 12...................................................................................................................................................21

Part 13...................................................................................................................................................21

Part 14...................................................................................................................................................21

Part 15...................................................................................................................................................21

Part 16...................................................................................................................................................21

Conclusion.................................................................................................................................................22

References.................................................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 4

Introduction

The report provide insights about the importance of complying with the accounting standards

and principles for the purpose of recording, recognizing and presenting the financial information

in the annual reports. It is very important for the companies to properly follow all the rules and

regulations so that reliable and relevant information can be communicated to the investors and

shareholders (Brigham and Ehrhardt, 2013).

The report analyse the financial statements of CBA and National Bank of Australia and discusses

the each line item of the statements prepared. It includes the evaluation of comprehensive

income statement, cash flow statement, balance sheet and reporting of tax expense. The

evaluation is done are compared to each other.

Description of the companies

Commonwealth Bank

CBA is an Australian banking group that is engaged in providing integrated financial services to

the countries like Australia, New Zealand and others. Its core activities include distribution of

financial services. It operates through retail banking services, Bankwest, New Zealand other

divisions. The services offered by the company include business loans, international payments,

insurance services and credit cards. It is listed on ASX and considered as the largest financial

institution in the country (Bloomberg. 2018).

National Bank of Australia

Introduction

The report provide insights about the importance of complying with the accounting standards

and principles for the purpose of recording, recognizing and presenting the financial information

in the annual reports. It is very important for the companies to properly follow all the rules and

regulations so that reliable and relevant information can be communicated to the investors and

shareholders (Brigham and Ehrhardt, 2013).

The report analyse the financial statements of CBA and National Bank of Australia and discusses

the each line item of the statements prepared. It includes the evaluation of comprehensive

income statement, cash flow statement, balance sheet and reporting of tax expense. The

evaluation is done are compared to each other.

Description of the companies

Commonwealth Bank

CBA is an Australian banking group that is engaged in providing integrated financial services to

the countries like Australia, New Zealand and others. Its core activities include distribution of

financial services. It operates through retail banking services, Bankwest, New Zealand other

divisions. The services offered by the company include business loans, international payments,

insurance services and credit cards. It is listed on ASX and considered as the largest financial

institution in the country (Bloomberg. 2018).

National Bank of Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 5

It is also a financial institution having its operations in Australia, United States and United

Kingdom. It operates through segments like Consumer Banking and Wealth, Corporate and

Institutional banking, Business and private banking and NZ Banking segments. It offers services

like term deposits, savings account, statutory trust and farm management accounts. NBA also

look for provide commercial and personal loans to its clients across the country (Bloomberg.

2018).

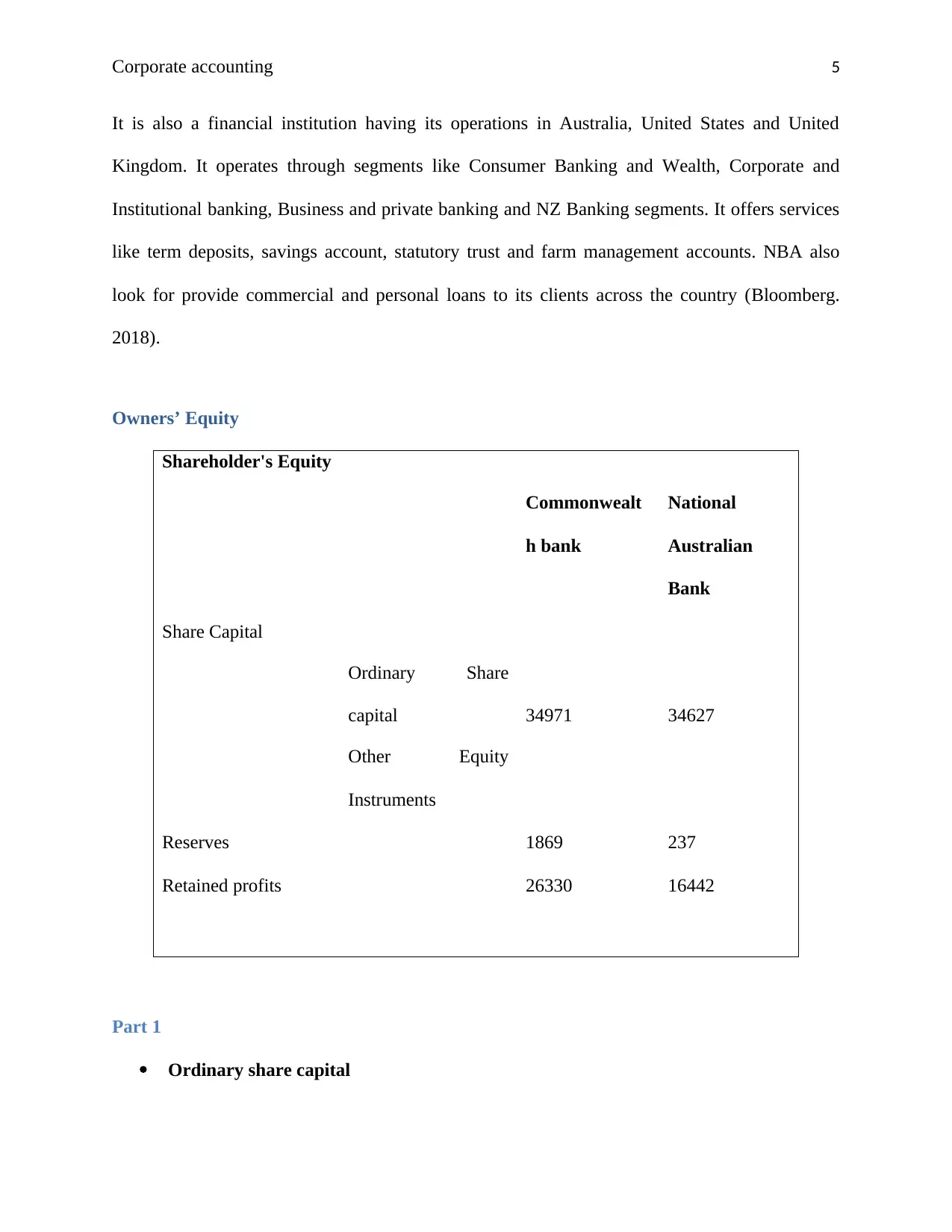

Owners’ Equity

Shareholder's Equity

Commonwealt

h bank

National

Australian

Bank

Share Capital

Ordinary Share

capital 34971 34627

Other Equity

Instruments

Reserves 1869 237

Retained profits 26330 16442

Part 1

Ordinary share capital

It is also a financial institution having its operations in Australia, United States and United

Kingdom. It operates through segments like Consumer Banking and Wealth, Corporate and

Institutional banking, Business and private banking and NZ Banking segments. It offers services

like term deposits, savings account, statutory trust and farm management accounts. NBA also

look for provide commercial and personal loans to its clients across the country (Bloomberg.

2018).

Owners’ Equity

Shareholder's Equity

Commonwealt

h bank

National

Australian

Bank

Share Capital

Ordinary Share

capital 34971 34627

Other Equity

Instruments

Reserves 1869 237

Retained profits 26330 16442

Part 1

Ordinary share capital

Corporate accounting 6

Ordinary share capital is the capital which is given by the proprietors of the business in return of

shares. They are positioned after the inclination shares. The conventional offer capital of the

Commonwealth Bank of Australia is A$34971 and that of the National Australian Bank is

A$34627 which is lower when contrasted with the previous bank. The investor capital of both

the banks have been quickened when contrasted with the earlier year from the yearly reports,

potentially on the grounds that the organizations may have sold the offers which raised the

income and diminished the costs. The offer capital of Commonwealth bank expanded from

A$33845 to A$34971 and that of the National Bank of Australia is A$34285 to A$34627, which

is as yet a moderate raise.

Other equity Investments

They are the record which fills in as a legitimate proof of the proprietorship right in a firm like

an offer declaration. They are issued to the investors of the organization and are utilized to

support the business.

Reserves

They represent the amount kept aside by the firm with the purpose of meeting its liabilities that

may arise in future. CBA has reserved worth $1869 and NBA reported the same amounted to

$237. The reserves have been diminished in the event of Commonwealth Bank of Australia

because of the debt repayments.

Retained earnings

It reflects the amount retained by the company in the business after paying all of its liabilities

and other payments. It is the profit left with the company for paying dividends to its

Ordinary share capital is the capital which is given by the proprietors of the business in return of

shares. They are positioned after the inclination shares. The conventional offer capital of the

Commonwealth Bank of Australia is A$34971 and that of the National Australian Bank is

A$34627 which is lower when contrasted with the previous bank. The investor capital of both

the banks have been quickened when contrasted with the earlier year from the yearly reports,

potentially on the grounds that the organizations may have sold the offers which raised the

income and diminished the costs. The offer capital of Commonwealth bank expanded from

A$33845 to A$34971 and that of the National Bank of Australia is A$34285 to A$34627, which

is as yet a moderate raise.

Other equity Investments

They are the record which fills in as a legitimate proof of the proprietorship right in a firm like

an offer declaration. They are issued to the investors of the organization and are utilized to

support the business.

Reserves

They represent the amount kept aside by the firm with the purpose of meeting its liabilities that

may arise in future. CBA has reserved worth $1869 and NBA reported the same amounted to

$237. The reserves have been diminished in the event of Commonwealth Bank of Australia

because of the debt repayments.

Retained earnings

It reflects the amount retained by the company in the business after paying all of its liabilities

and other payments. It is the profit left with the company for paying dividends to its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 7

shareholders. It tends to be utilized by the organization to pay the obligations and in addition the

future profits. The upsurge in retained income implies the organizations are steady and

beneficial. The RE of NBA has shown an upsurge from $16736 to $16442 while on the other

side; CBA’s earnings reflected an increase from A$23435 to A$26330(Commonwealth Bank,

2018).

Part 2

Comparative analysis

The relative examination of the investor’s value of both the organizations exhibits the money

related position of the organization. The above components decide how much the proprietors has

put resources into the business and how they are performing in contrast with the previous years

and the contenders as well. The share capital of Commonwealth bank expanded from A$33845

to A$34971 and that of the National Bank of Australia is A$34285 to A$34627, which is as yet a

moderate raise.

Cash Flow Statement

Part 3

Operating activities

Operating activities are the operations of the business which are straightforwardly identified with

the supply of the merchandise and the administrations to the market. These exercises are

considered as the centre exercises of the organization and precedents of such exercises are

conveying, showcasing and offering of an item or an administration.

Funds from operations

shareholders. It tends to be utilized by the organization to pay the obligations and in addition the

future profits. The upsurge in retained income implies the organizations are steady and

beneficial. The RE of NBA has shown an upsurge from $16736 to $16442 while on the other

side; CBA’s earnings reflected an increase from A$23435 to A$26330(Commonwealth Bank,

2018).

Part 2

Comparative analysis

The relative examination of the investor’s value of both the organizations exhibits the money

related position of the organization. The above components decide how much the proprietors has

put resources into the business and how they are performing in contrast with the previous years

and the contenders as well. The share capital of Commonwealth bank expanded from A$33845

to A$34971 and that of the National Bank of Australia is A$34285 to A$34627, which is as yet a

moderate raise.

Cash Flow Statement

Part 3

Operating activities

Operating activities are the operations of the business which are straightforwardly identified with

the supply of the merchandise and the administrations to the market. These exercises are

considered as the centre exercises of the organization and precedents of such exercises are

conveying, showcasing and offering of an item or an administration.

Funds from operations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 8

They are the amount which is utilized by the land speculation trusts to define the cash flow from

their operations.The Funds from operations are ascertained by including back the depreciation

value and subtracting any profit on sale (Collins Hribar and Tian, 2014).

Changes in the Working Capital

Net Working Capital is characterized as the distinction between the current assets and current

liabilities. In this manner an adjustment in the measure of the working capital will be reflected.

Net Operating Cash Flow

Net Operating income alludes to the money sum created by the organization through the income

it acquires, barring costs which are in connection to the long term investment on capital things.

Investing Activities

They are those exercises which will give the future advantage to the organization. The income

from the contributing exercises is a thing which reports the adjustment in the total position of the

organization whether through interest in the advantages and offer of the benefits.

Capital Expenditures

The sum an organization spends with a specific end goal to achieve the settled resources, land,

structures and the gear. It is comprehended that the use on the capital things will give the

advantage to the organization over the long haul (Campbell, 2015).

Net Assets from Acquisitions

They are the amount which is utilized by the land speculation trusts to define the cash flow from

their operations.The Funds from operations are ascertained by including back the depreciation

value and subtracting any profit on sale (Collins Hribar and Tian, 2014).

Changes in the Working Capital

Net Working Capital is characterized as the distinction between the current assets and current

liabilities. In this manner an adjustment in the measure of the working capital will be reflected.

Net Operating Cash Flow

Net Operating income alludes to the money sum created by the organization through the income

it acquires, barring costs which are in connection to the long term investment on capital things.

Investing Activities

They are those exercises which will give the future advantage to the organization. The income

from the contributing exercises is a thing which reports the adjustment in the total position of the

organization whether through interest in the advantages and offer of the benefits.

Capital Expenditures

The sum an organization spends with a specific end goal to achieve the settled resources, land,

structures and the gear. It is comprehended that the use on the capital things will give the

advantage to the organization over the long haul (Campbell, 2015).

Net Assets from Acquisitions

Corporate accounting 9

The net resources from acquisitions are fundamentally the sum which is landed subsequent to

including all the above resources and consumptions.

Sales of Fixed Assets and Businesses

It is an ordinary procedure which is attempted either to pick up leverage when the cost is correct

or can empowers the income and benefits or when the piece of the advantage or a whole resource

winds up pointless.

Buy/Sale of Investments

All the transactions related to investments are made from the brokers and purchase of the same is

done with an intention to secure the company. The correct market cost or the positive market

cost when arrives the organization sells the investment.

Financing Activities

This category of activities includes business transactions with creditors and investors. They

generally contribute to the expansion of business operation or enhancing its existing activities. It

is the third category which is reflected in cash flow statement after reporting operating and

investing activities.

Transactions like cash dividends paid, issue of shares and debt, change in long term debt,

payment of financial obligations all appear under the financing activities of the company.

Net Change in Cash

The net change in the money mirrors the expansion or diminishing in the money and the money

counterparts from the beginning stage to the end purpose of a year. The net change is computed

The net resources from acquisitions are fundamentally the sum which is landed subsequent to

including all the above resources and consumptions.

Sales of Fixed Assets and Businesses

It is an ordinary procedure which is attempted either to pick up leverage when the cost is correct

or can empowers the income and benefits or when the piece of the advantage or a whole resource

winds up pointless.

Buy/Sale of Investments

All the transactions related to investments are made from the brokers and purchase of the same is

done with an intention to secure the company. The correct market cost or the positive market

cost when arrives the organization sells the investment.

Financing Activities

This category of activities includes business transactions with creditors and investors. They

generally contribute to the expansion of business operation or enhancing its existing activities. It

is the third category which is reflected in cash flow statement after reporting operating and

investing activities.

Transactions like cash dividends paid, issue of shares and debt, change in long term debt,

payment of financial obligations all appear under the financing activities of the company.

Net Change in Cash

The net change in the money mirrors the expansion or diminishing in the money and the money

counterparts from the beginning stage to the end purpose of a year. The net change is computed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 10

because of money from working, contributing and the financing exercises (Graham and Lin,

2018).

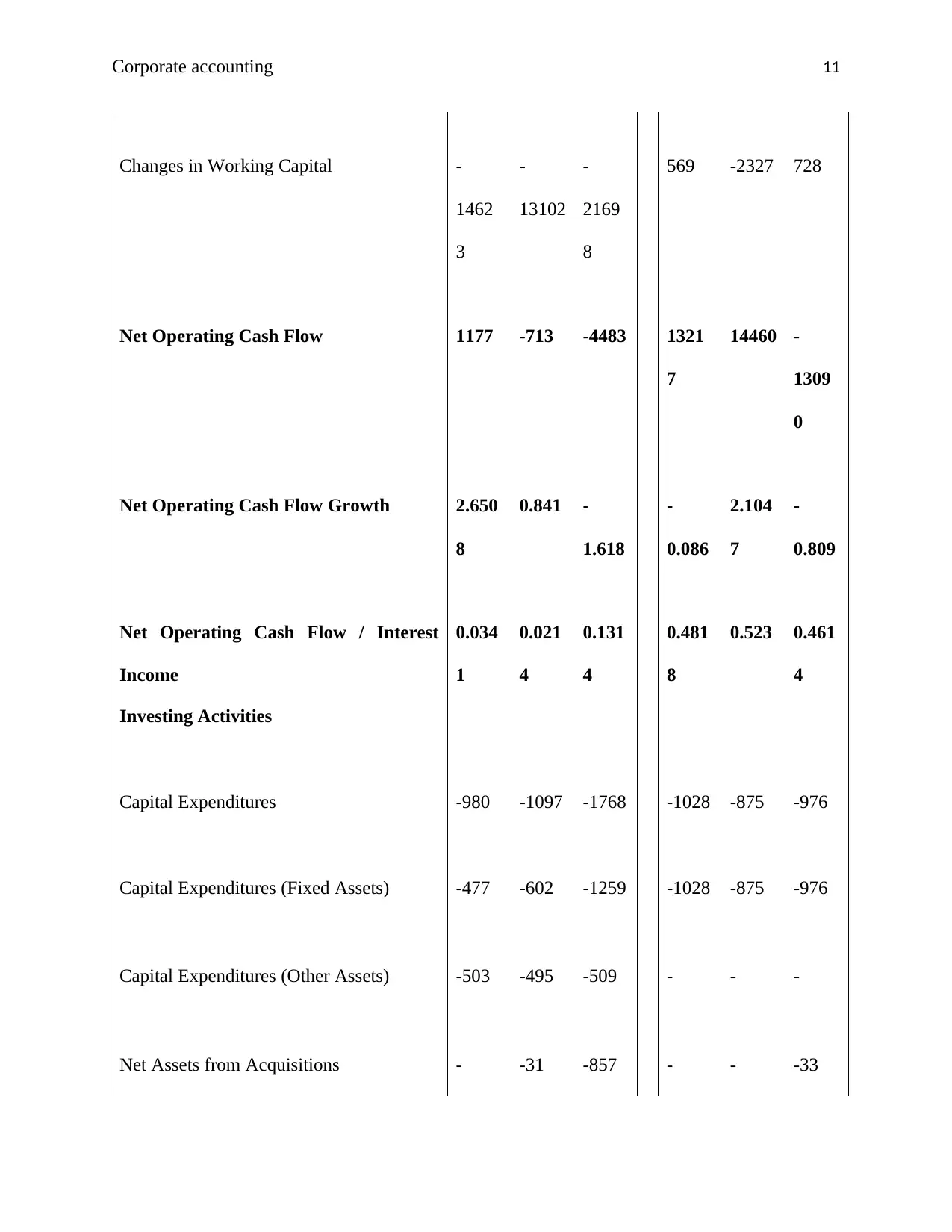

Free Cash Flow

The free income is estimated by how much measure of the money the organization can produce

in the wake of satisfying for every one of the costs and can be utilized for the extension, profits,

decrease of the obligations and for other purposes.

From the income beneath it very well may be broke down and seen that if there should arise an

occurrence of the Commonwealth bank the net money from working exercises has been

enhanced and come to 2.651 from 0.841 when contrasted with the earlier year fundamentally on

account of the expansion in the assets from tasks and that of the National Australian Bank have

been lessened to 569 from (2327), the organization is attempting to improve.

Part 4

Cash flow Statement Commonwealth

Bank

National Australian

Bank

Fiscal year is July-June. All values

AUD Millions.

2018 2017 2016 2018 2017 2016

Funds from Operations 1580

0

12389 1721

5

1264

8

16787 -

1381

8

Funds from Operations Growth 0.275

3

-

0.280

3

0.346

9

-

0.246

6

2.214

9

-

1.425

1

because of money from working, contributing and the financing exercises (Graham and Lin,

2018).

Free Cash Flow

The free income is estimated by how much measure of the money the organization can produce

in the wake of satisfying for every one of the costs and can be utilized for the extension, profits,

decrease of the obligations and for other purposes.

From the income beneath it very well may be broke down and seen that if there should arise an

occurrence of the Commonwealth bank the net money from working exercises has been

enhanced and come to 2.651 from 0.841 when contrasted with the earlier year fundamentally on

account of the expansion in the assets from tasks and that of the National Australian Bank have

been lessened to 569 from (2327), the organization is attempting to improve.

Part 4

Cash flow Statement Commonwealth

Bank

National Australian

Bank

Fiscal year is July-June. All values

AUD Millions.

2018 2017 2016 2018 2017 2016

Funds from Operations 1580

0

12389 1721

5

1264

8

16787 -

1381

8

Funds from Operations Growth 0.275

3

-

0.280

3

0.346

9

-

0.246

6

2.214

9

-

1.425

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 11

Changes in Working Capital -

1462

3

-

13102

-

2169

8

569 -2327 728

Net Operating Cash Flow 1177 -713 -4483 1321

7

14460 -

1309

0

Net Operating Cash Flow Growth 2.650

8

0.841 -

1.618

-

0.086

2.104

7

-

0.809

Net Operating Cash Flow / Interest

Income

0.034

1

0.021

4

0.131

4

0.481

8

0.523 0.461

4

Investing Activities

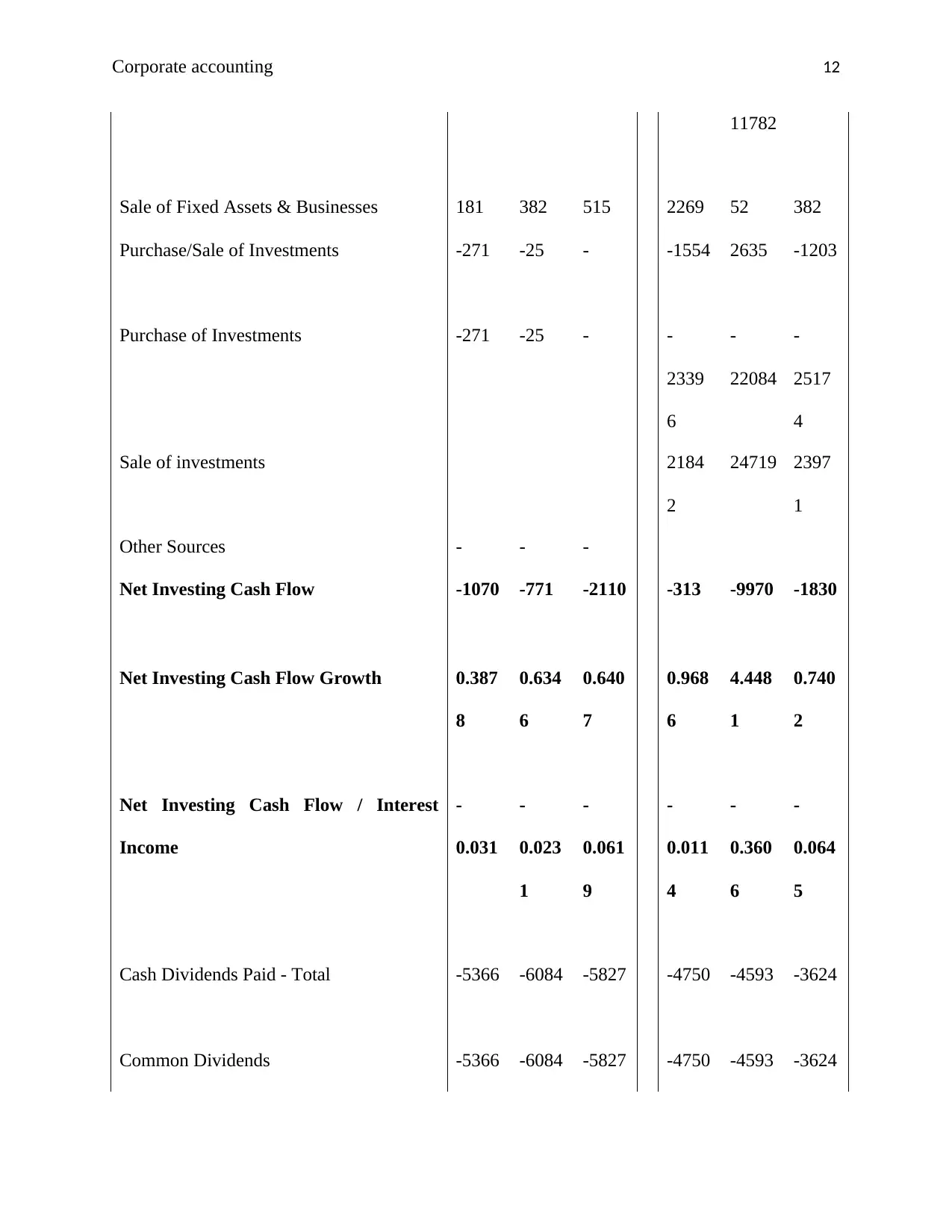

Capital Expenditures -980 -1097 -1768 -1028 -875 -976

Capital Expenditures (Fixed Assets) -477 -602 -1259 -1028 -875 -976

Capital Expenditures (Other Assets) -503 -495 -509 - - -

Net Assets from Acquisitions - -31 -857 - - -33

Changes in Working Capital -

1462

3

-

13102

-

2169

8

569 -2327 728

Net Operating Cash Flow 1177 -713 -4483 1321

7

14460 -

1309

0

Net Operating Cash Flow Growth 2.650

8

0.841 -

1.618

-

0.086

2.104

7

-

0.809

Net Operating Cash Flow / Interest

Income

0.034

1

0.021

4

0.131

4

0.481

8

0.523 0.461

4

Investing Activities

Capital Expenditures -980 -1097 -1768 -1028 -875 -976

Capital Expenditures (Fixed Assets) -477 -602 -1259 -1028 -875 -976

Capital Expenditures (Other Assets) -503 -495 -509 - - -

Net Assets from Acquisitions - -31 -857 - - -33

Corporate accounting 12

11782

Sale of Fixed Assets & Businesses 181 382 515 2269 52 382

Purchase/Sale of Investments -271 -25 - -1554 2635 -1203

Purchase of Investments -271 -25 - -

2339

6

-

22084

-

2517

4

Sale of investments 2184

2

24719 2397

1

Other Sources - - -

Net Investing Cash Flow -1070 -771 -2110 -313 -9970 -1830

Net Investing Cash Flow Growth 0.387

8

0.634

6

0.640

7

0.968

6

4.448

1

0.740

2

Net Investing Cash Flow / Interest

Income

-

0.031

-

0.023

1

-

0.061

9

-

0.011

4

-

0.360

6

-

0.064

5

Cash Dividends Paid - Total -5366 -6084 -5827 -4750 -4593 -3624

Common Dividends -5366 -6084 -5827 -4750 -4593 -3624

11782

Sale of Fixed Assets & Businesses 181 382 515 2269 52 382

Purchase/Sale of Investments -271 -25 - -1554 2635 -1203

Purchase of Investments -271 -25 - -

2339

6

-

22084

-

2517

4

Sale of investments 2184

2

24719 2397

1

Other Sources - - -

Net Investing Cash Flow -1070 -771 -2110 -313 -9970 -1830

Net Investing Cash Flow Growth 0.387

8

0.634

6

0.640

7

0.968

6

4.448

1

0.740

2

Net Investing Cash Flow / Interest

Income

-

0.031

-

0.023

1

-

0.061

9

-

0.011

4

-

0.360

6

-

0.064

5

Cash Dividends Paid - Total -5366 -6084 -5827 -4750 -4593 -3624

Common Dividends -5366 -6084 -5827 -4750 -4593 -3624

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.