HI5020 Corporate Accounting: CIMIC Group Limited Financial Report

VerifiedAdded on 2024/05/31

|14

|2505

|464

Report

AI Summary

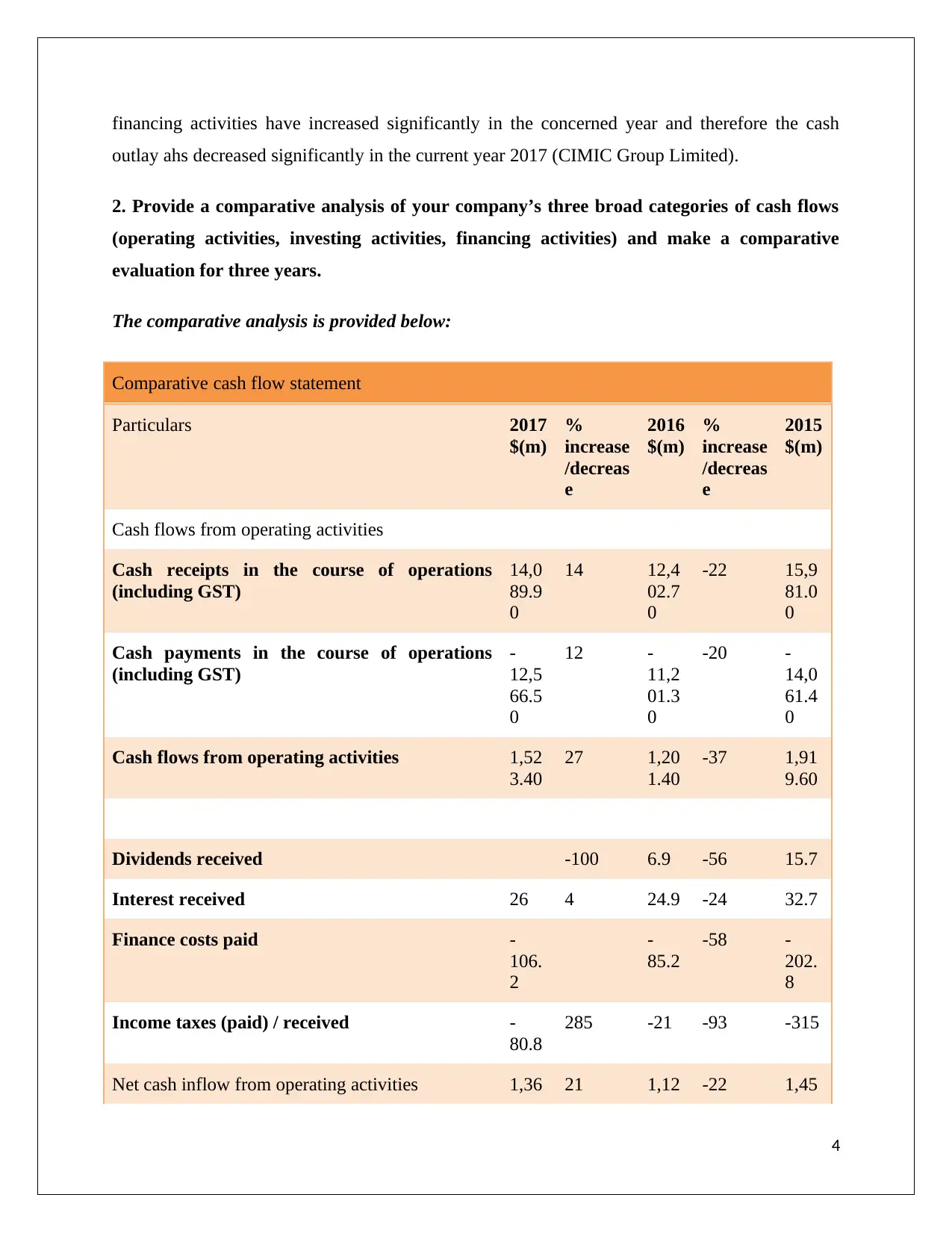

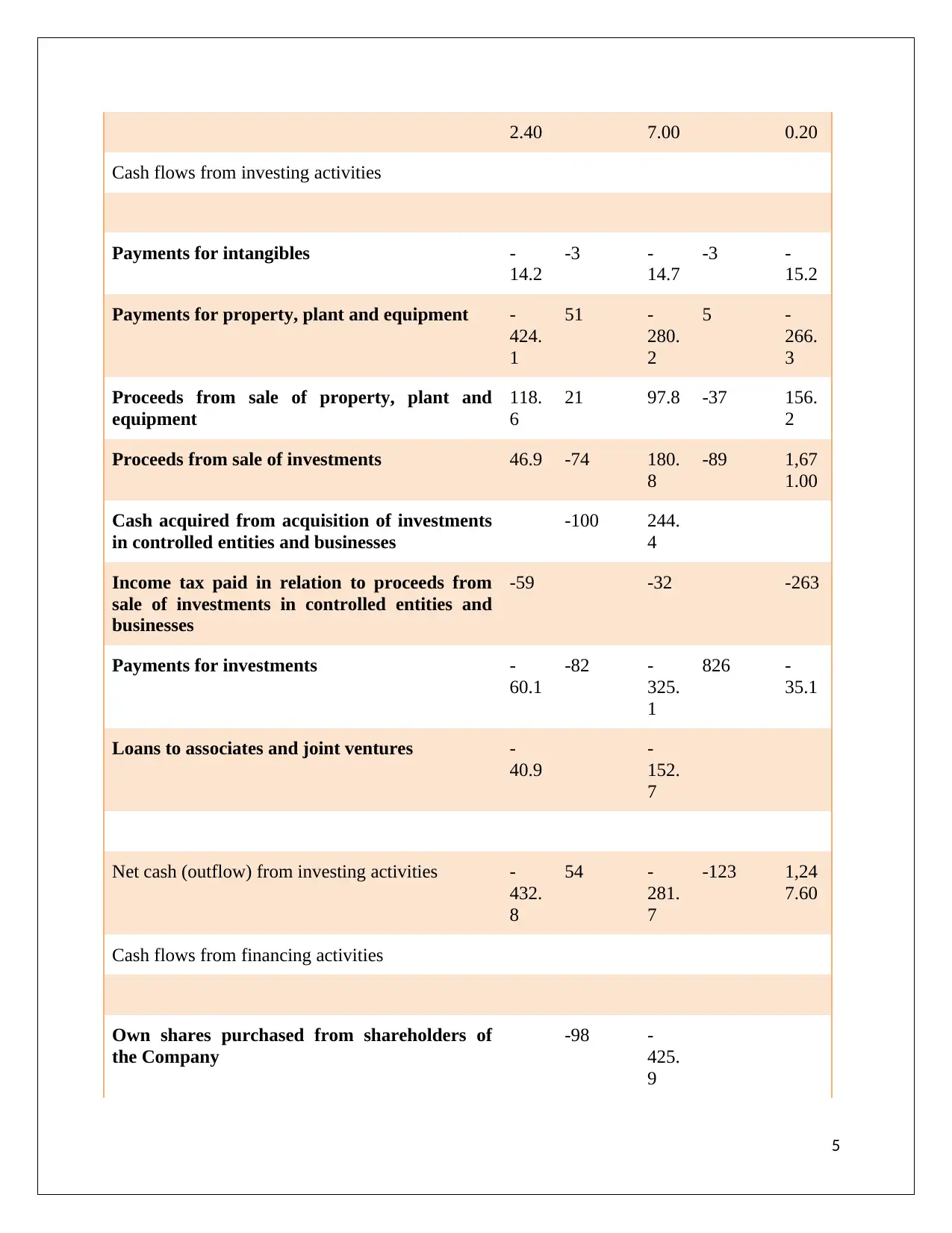

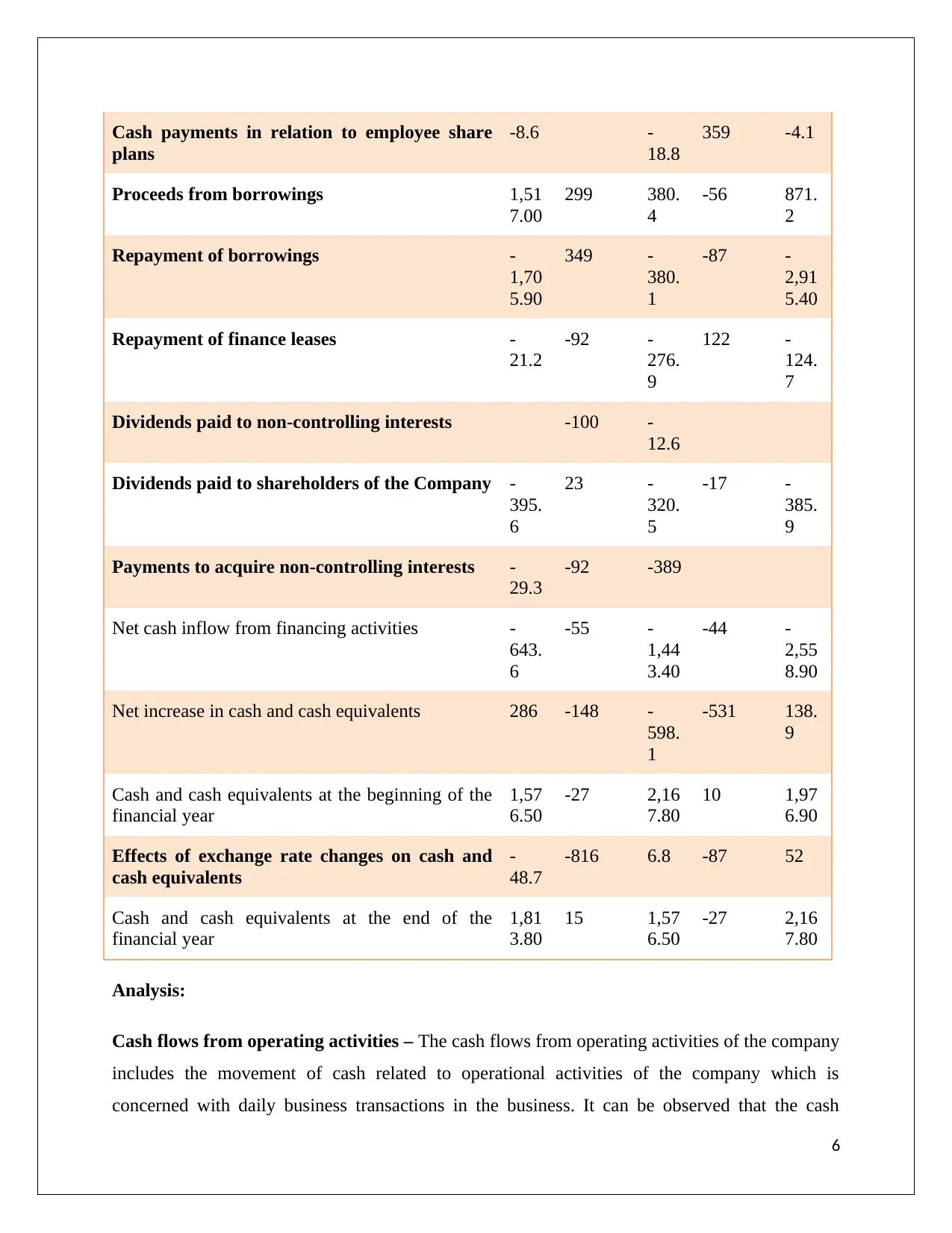

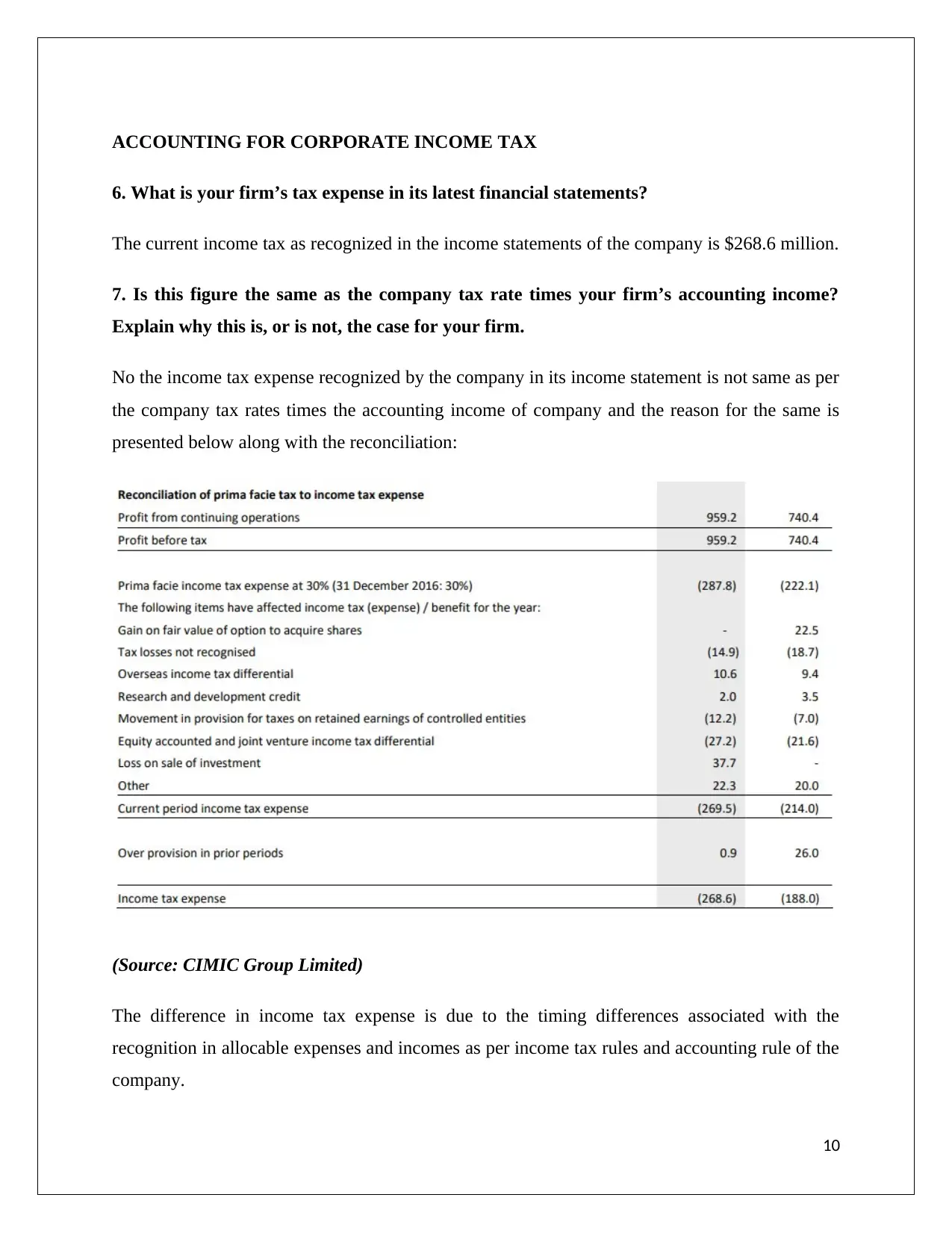

This corporate accounting report provides an analysis of CIMIC Group Limited's financial statements, including a comparative analysis of cash flow statements, an examination of the other comprehensive income statement, and an assessment of the company's income tax expense, deferred tax assets, and liabilities. The report identifies key changes in cash flows from operating, investing, and financing activities over three years, noting an increase in operating cash inflows and a decrease in financing cash outflows. It also explains the items reported in the other comprehensive income statement and why they are not included in the profit and loss statement. Furthermore, the report reconciles the company's income tax expense with its accounting income, comments on deferred tax assets and liabilities, and discusses the differences between income tax expense and income tax paid. The analysis reveals that CIMIC Group follows a corporate income tax rate of 30%, but also points out potential inconsistencies in the creation of deferred tax assets.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.