HI5020 Corporate Accounting Tutorial Project - Trimester 1, 2021

VerifiedAdded on 2022/11/24

|10

|2738

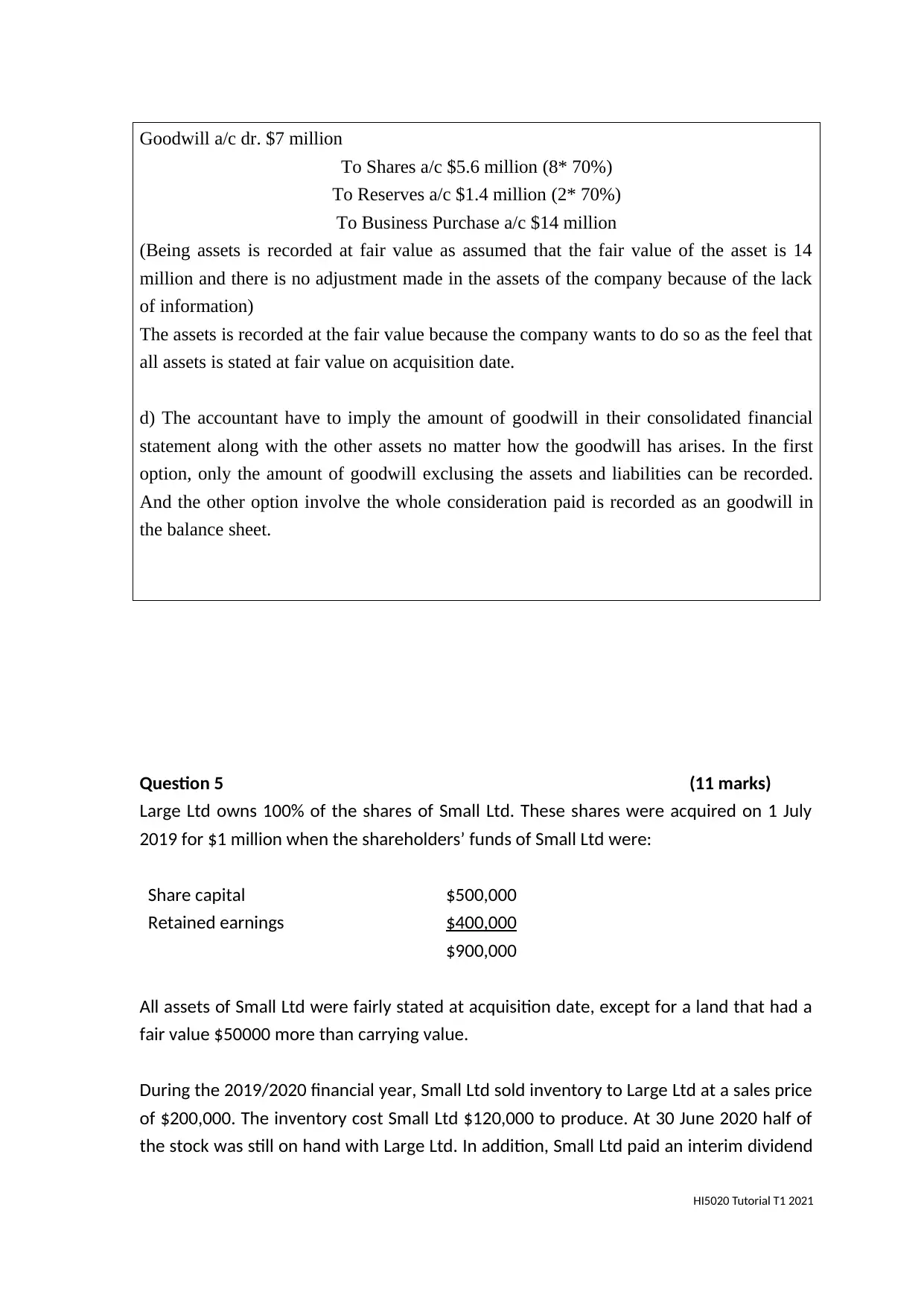

|179

Homework Assignment

AI Summary

This document presents a comprehensive solution to a HI5020 Corporate Accounting tutorial project. The assignment covers key accounting concepts including the differentiation between the definition and recognition criteria of assets, and the implications of asset ownership. It also includes detailed journal entries for share issuance, including oversubscription, allotment, and call money, along with share forfeitures. Furthermore, the solution addresses complex topics such as goodwill calculation and consolidation, with detailed explanations and journal entries for both proportionate and fair value methods. The assignment also includes calculations for cash receipts from customers and cash payments to suppliers, and the preparation of consolidation journal entries for a parent company's investment in a subsidiary, considering intercompany transactions like inventory sales and dividend payments. The solution provides a detailed breakdown of each question, supporting students in understanding and applying corporate accounting principles.

Student Number: (enter on the line below)

Student Name: (enter on the line below)

HI5020

CORPORATE ACCOUNTING

TUTORIAL PROJECT

TRIMESTER 1, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HI5020 Tutorial T1 2021

Student Name: (enter on the line below)

HI5020

CORPORATE ACCOUNTING

TUTORIAL PROJECT

TRIMESTER 1, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HI5020 Tutorial T1 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

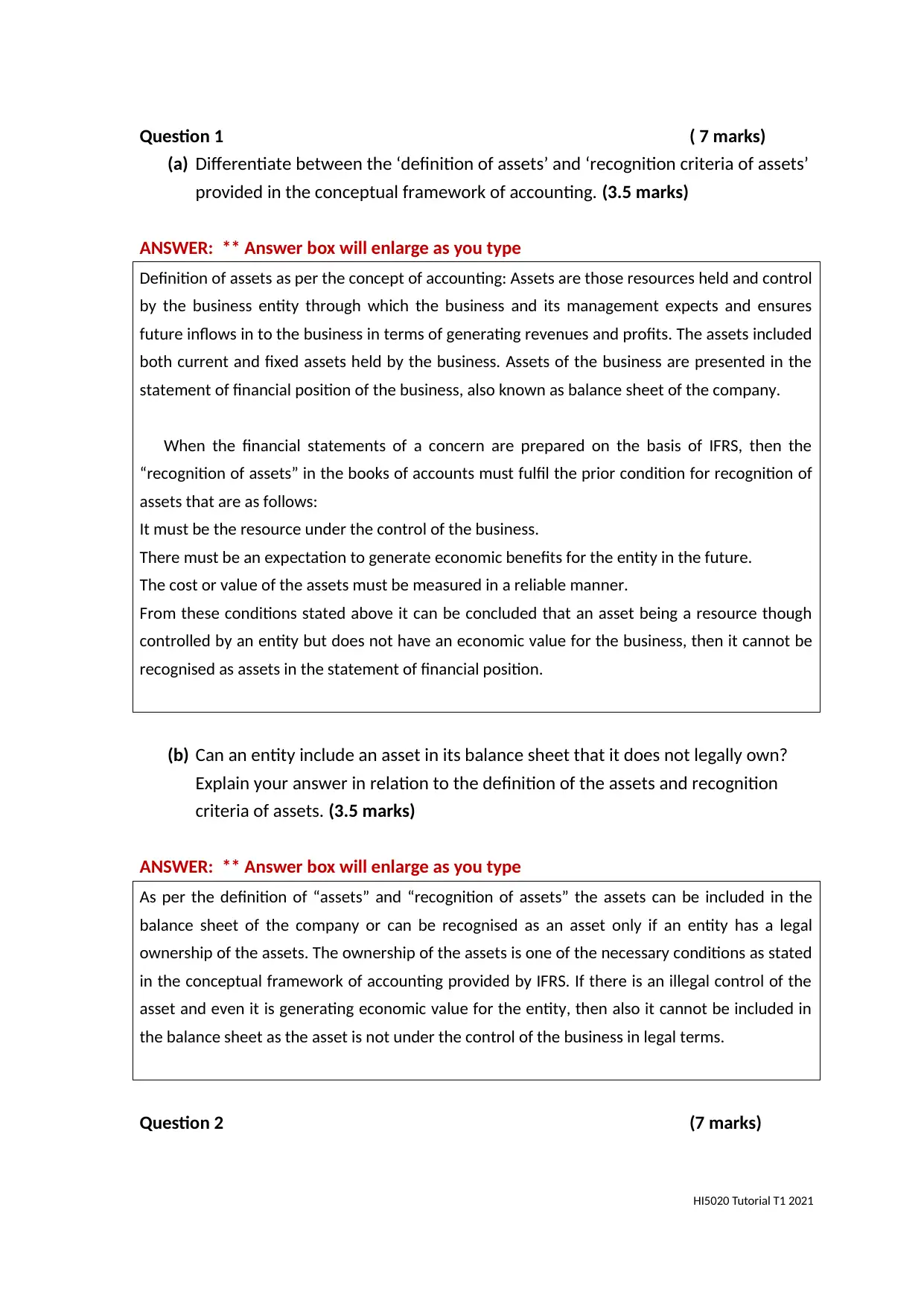

Question 1 ( 7 marks)

(a) Differentiate between the ‘definition of assets’ and ‘recognition criteria of assets’

provided in the conceptual framework of accounting. (3.5 marks)

ANSWER: ** Answer box will enlarge as you type

Definition of assets as per the concept of accounting: Assets are those resources held and control

by the business entity through which the business and its management expects and ensures

future inflows in to the business in terms of generating revenues and profits. The assets included

both current and fixed assets held by the business. Assets of the business are presented in the

statement of financial position of the business, also known as balance sheet of the company.

When the financial statements of a concern are prepared on the basis of IFRS, then the

“recognition of assets” in the books of accounts must fulfil the prior condition for recognition of

assets that are as follows:

It must be the resource under the control of the business.

There must be an expectation to generate economic benefits for the entity in the future.

The cost or value of the assets must be measured in a reliable manner.

From these conditions stated above it can be concluded that an asset being a resource though

controlled by an entity but does not have an economic value for the business, then it cannot be

recognised as assets in the statement of financial position.

(b) Can an entity include an asset in its balance sheet that it does not legally own?

Explain your answer in relation to the definition of the assets and recognition

criteria of assets. (3.5 marks)

ANSWER: ** Answer box will enlarge as you type

As per the definition of “assets” and “recognition of assets” the assets can be included in the

balance sheet of the company or can be recognised as an asset only if an entity has a legal

ownership of the assets. The ownership of the assets is one of the necessary conditions as stated

in the conceptual framework of accounting provided by IFRS. If there is an illegal control of the

asset and even it is generating economic value for the entity, then also it cannot be included in

the balance sheet as the asset is not under the control of the business in legal terms.

Question 2 (7 marks)

HI5020 Tutorial T1 2021

(a) Differentiate between the ‘definition of assets’ and ‘recognition criteria of assets’

provided in the conceptual framework of accounting. (3.5 marks)

ANSWER: ** Answer box will enlarge as you type

Definition of assets as per the concept of accounting: Assets are those resources held and control

by the business entity through which the business and its management expects and ensures

future inflows in to the business in terms of generating revenues and profits. The assets included

both current and fixed assets held by the business. Assets of the business are presented in the

statement of financial position of the business, also known as balance sheet of the company.

When the financial statements of a concern are prepared on the basis of IFRS, then the

“recognition of assets” in the books of accounts must fulfil the prior condition for recognition of

assets that are as follows:

It must be the resource under the control of the business.

There must be an expectation to generate economic benefits for the entity in the future.

The cost or value of the assets must be measured in a reliable manner.

From these conditions stated above it can be concluded that an asset being a resource though

controlled by an entity but does not have an economic value for the business, then it cannot be

recognised as assets in the statement of financial position.

(b) Can an entity include an asset in its balance sheet that it does not legally own?

Explain your answer in relation to the definition of the assets and recognition

criteria of assets. (3.5 marks)

ANSWER: ** Answer box will enlarge as you type

As per the definition of “assets” and “recognition of assets” the assets can be included in the

balance sheet of the company or can be recognised as an asset only if an entity has a legal

ownership of the assets. The ownership of the assets is one of the necessary conditions as stated

in the conceptual framework of accounting provided by IFRS. If there is an illegal control of the

asset and even it is generating economic value for the entity, then also it cannot be included in

the balance sheet as the asset is not under the control of the business in legal terms.

Question 2 (7 marks)

HI5020 Tutorial T1 2021

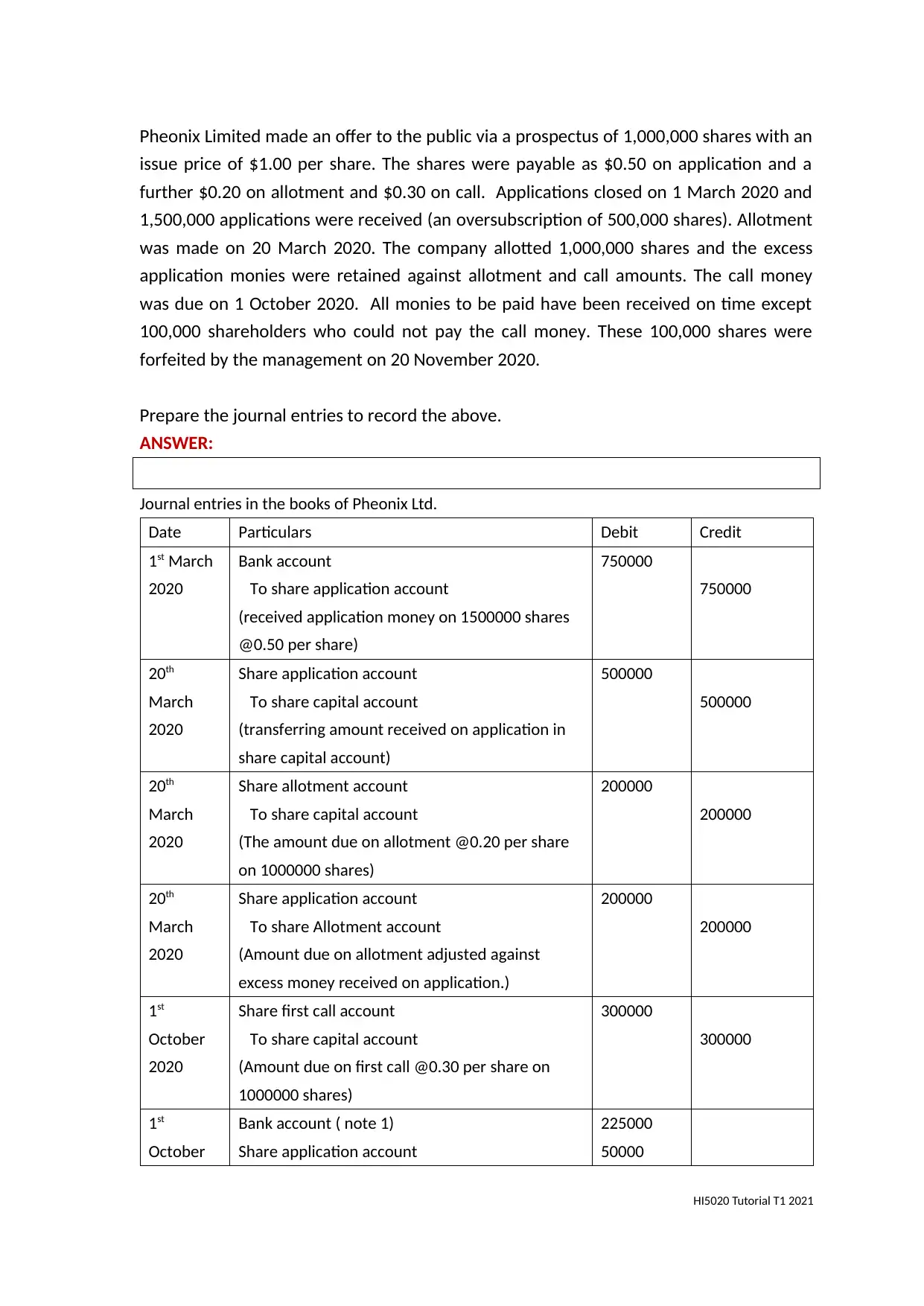

Pheonix Limited made an offer to the public via a prospectus of 1,000,000 shares with an

issue price of $1.00 per share. The shares were payable as $0.50 on application and a

further $0.20 on allotment and $0.30 on call. Applications closed on 1 March 2020 and

1,500,000 applications were received (an oversubscription of 500,000 shares). Allotment

was made on 20 March 2020. The company allotted 1,000,000 shares and the excess

application monies were retained against allotment and call amounts. The call money

was due on 1 October 2020. All monies to be paid have been received on time except

100,000 shareholders who could not pay the call money. These 100,000 shares were

forfeited by the management on 20 November 2020.

Prepare the journal entries to record the above.

ANSWER:

Journal entries in the books of Pheonix Ltd.

Date Particulars Debit Credit

1st March

2020

Bank account

To share application account

(received application money on 1500000 shares

@0.50 per share)

750000

750000

20th

March

2020

Share application account

To share capital account

(transferring amount received on application in

share capital account)

500000

500000

20th

March

2020

Share allotment account

To share capital account

(The amount due on allotment @0.20 per share

on 1000000 shares)

200000

200000

20th

March

2020

Share application account

To share Allotment account

(Amount due on allotment adjusted against

excess money received on application.)

200000

200000

1st

October

2020

Share first call account

To share capital account

(Amount due on first call @0.30 per share on

1000000 shares)

300000

300000

1st

October

Bank account ( note 1)

Share application account

225000

50000

HI5020 Tutorial T1 2021

issue price of $1.00 per share. The shares were payable as $0.50 on application and a

further $0.20 on allotment and $0.30 on call. Applications closed on 1 March 2020 and

1,500,000 applications were received (an oversubscription of 500,000 shares). Allotment

was made on 20 March 2020. The company allotted 1,000,000 shares and the excess

application monies were retained against allotment and call amounts. The call money

was due on 1 October 2020. All monies to be paid have been received on time except

100,000 shareholders who could not pay the call money. These 100,000 shares were

forfeited by the management on 20 November 2020.

Prepare the journal entries to record the above.

ANSWER:

Journal entries in the books of Pheonix Ltd.

Date Particulars Debit Credit

1st March

2020

Bank account

To share application account

(received application money on 1500000 shares

@0.50 per share)

750000

750000

20th

March

2020

Share application account

To share capital account

(transferring amount received on application in

share capital account)

500000

500000

20th

March

2020

Share allotment account

To share capital account

(The amount due on allotment @0.20 per share

on 1000000 shares)

200000

200000

20th

March

2020

Share application account

To share Allotment account

(Amount due on allotment adjusted against

excess money received on application.)

200000

200000

1st

October

2020

Share first call account

To share capital account

(Amount due on first call @0.30 per share on

1000000 shares)

300000

300000

1st

October

Bank account ( note 1)

Share application account

225000

50000

HI5020 Tutorial T1 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

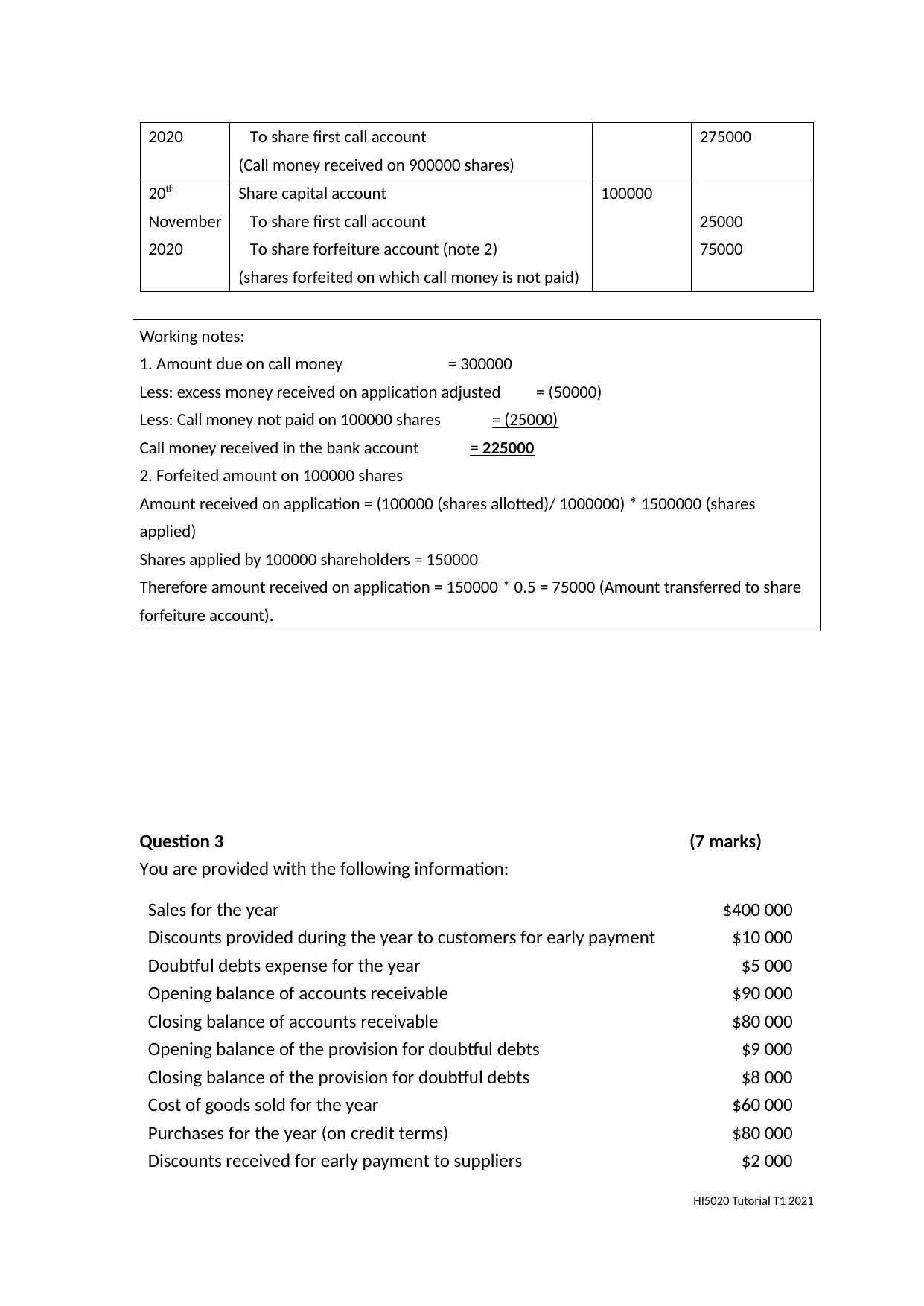

2020 To share first call account

(Call money received on 900000 shares)

275000

20th

November

2020

Share capital account

To share first call account

To share forfeiture account (note 2)

(shares forfeited on which call money is not paid)

100000

25000

75000

Working notes:

1. Amount due on call money = 300000

Less: excess money received on application adjusted = (50000)

Less: Call money not paid on 100000 shares = (25000)

Call money received in the bank account = 225000

2. Forfeited amount on 100000 shares

Amount received on application = (100000 (shares allotted)/ 1000000) * 1500000 (shares

applied)

Shares applied by 100000 shareholders = 150000

Therefore amount received on application = 150000 * 0.5 = 75000 (Amount transferred to share

forfeiture account).

Question 3 (7 marks)

You are provided with the following information:

Sales for the year $400 000

Discounts provided during the year to customers for early payment $10 000

Doubtful debts expense for the year $5 000

Opening balance of accounts receivable $90 000

Closing balance of accounts receivable $80 000

Opening balance of the provision for doubtful debts $9 000

Closing balance of the provision for doubtful debts $8 000

Cost of goods sold for the year $60 000

Purchases for the year (on credit terms) $80 000

Discounts received for early payment to suppliers $2 000

HI5020 Tutorial T1 2021

(Call money received on 900000 shares)

275000

20th

November

2020

Share capital account

To share first call account

To share forfeiture account (note 2)

(shares forfeited on which call money is not paid)

100000

25000

75000

Working notes:

1. Amount due on call money = 300000

Less: excess money received on application adjusted = (50000)

Less: Call money not paid on 100000 shares = (25000)

Call money received in the bank account = 225000

2. Forfeited amount on 100000 shares

Amount received on application = (100000 (shares allotted)/ 1000000) * 1500000 (shares

applied)

Shares applied by 100000 shareholders = 150000

Therefore amount received on application = 150000 * 0.5 = 75000 (Amount transferred to share

forfeiture account).

Question 3 (7 marks)

You are provided with the following information:

Sales for the year $400 000

Discounts provided during the year to customers for early payment $10 000

Doubtful debts expense for the year $5 000

Opening balance of accounts receivable $90 000

Closing balance of accounts receivable $80 000

Opening balance of the provision for doubtful debts $9 000

Closing balance of the provision for doubtful debts $8 000

Cost of goods sold for the year $60 000

Purchases for the year (on credit terms) $80 000

Discounts received for early payment to suppliers $2 000

HI5020 Tutorial T1 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

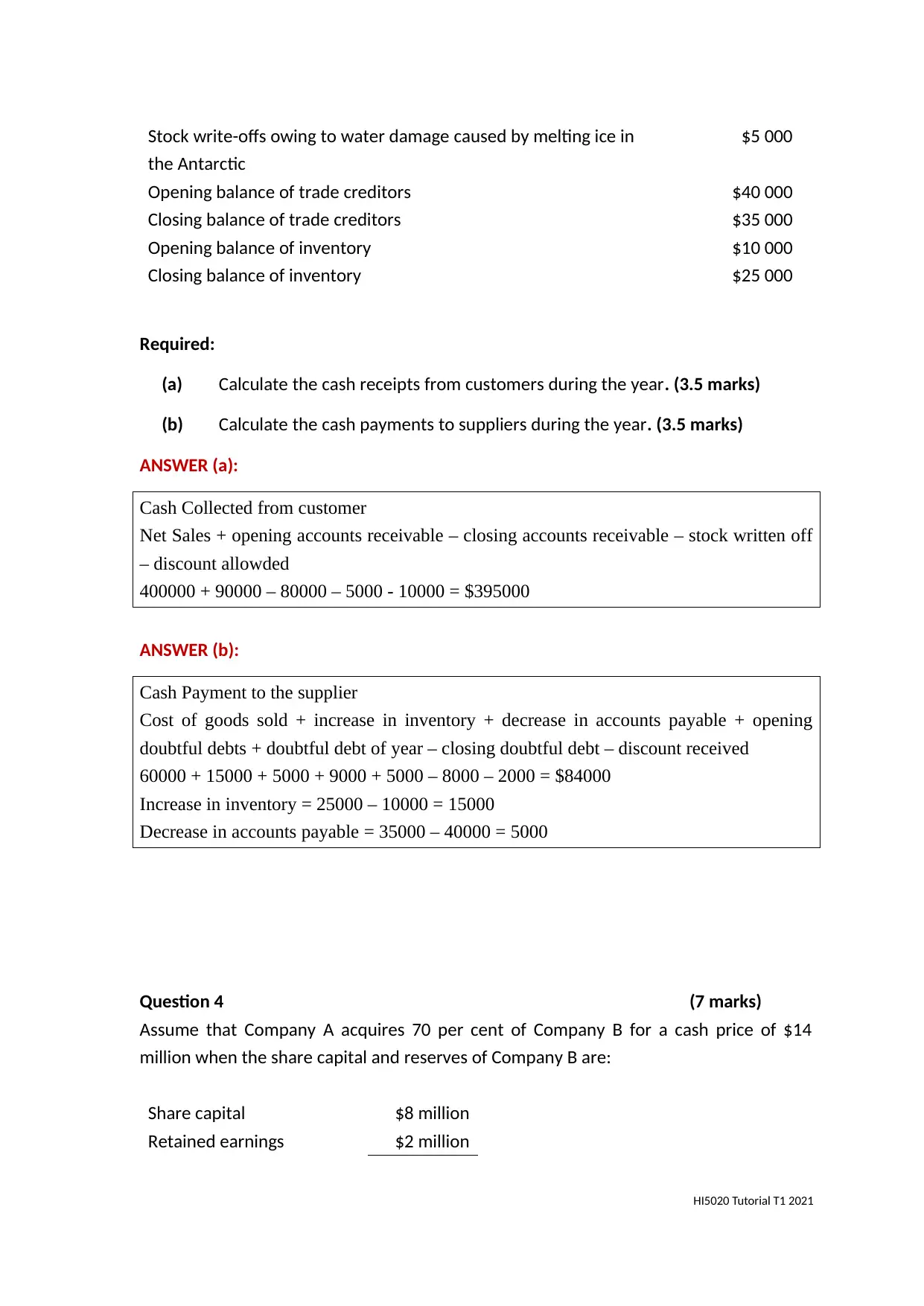

Stock write-offs owing to water damage caused by melting ice in

the Antarctic

$5 000

Opening balance of trade creditors $40 000

Closing balance of trade creditors $35 000

Opening balance of inventory $10 000

Closing balance of inventory $25 000

Required:

(a) Calculate the cash receipts from customers during the year. (3.5 marks)

(b) Calculate the cash payments to suppliers during the year. (3.5 marks)

ANSWER (a):

Cash Collected from customer

Net Sales + opening accounts receivable – closing accounts receivable – stock written off

– discount allowded

400000 + 90000 – 80000 – 5000 - 10000 = $395000

ANSWER (b):

Cash Payment to the supplier

Cost of goods sold + increase in inventory + decrease in accounts payable + opening

doubtful debts + doubtful debt of year – closing doubtful debt – discount received

60000 + 15000 + 5000 + 9000 + 5000 – 8000 – 2000 = $84000

Increase in inventory = 25000 – 10000 = 15000

Decrease in accounts payable = 35000 – 40000 = 5000

Question 4 (7 marks)

Assume that Company A acquires 70 per cent of Company B for a cash price of $14

million when the share capital and reserves of Company B are:

Share capital $8 million

Retained earnings $2 million

HI5020 Tutorial T1 2021

the Antarctic

$5 000

Opening balance of trade creditors $40 000

Closing balance of trade creditors $35 000

Opening balance of inventory $10 000

Closing balance of inventory $25 000

Required:

(a) Calculate the cash receipts from customers during the year. (3.5 marks)

(b) Calculate the cash payments to suppliers during the year. (3.5 marks)

ANSWER (a):

Cash Collected from customer

Net Sales + opening accounts receivable – closing accounts receivable – stock written off

– discount allowded

400000 + 90000 – 80000 – 5000 - 10000 = $395000

ANSWER (b):

Cash Payment to the supplier

Cost of goods sold + increase in inventory + decrease in accounts payable + opening

doubtful debts + doubtful debt of year – closing doubtful debt – discount received

60000 + 15000 + 5000 + 9000 + 5000 – 8000 – 2000 = $84000

Increase in inventory = 25000 – 10000 = 15000

Decrease in accounts payable = 35000 – 40000 = 5000

Question 4 (7 marks)

Assume that Company A acquires 70 per cent of Company B for a cash price of $14

million when the share capital and reserves of Company B are:

Share capital $8 million

Retained earnings $2 million

HI5020 Tutorial T1 2021

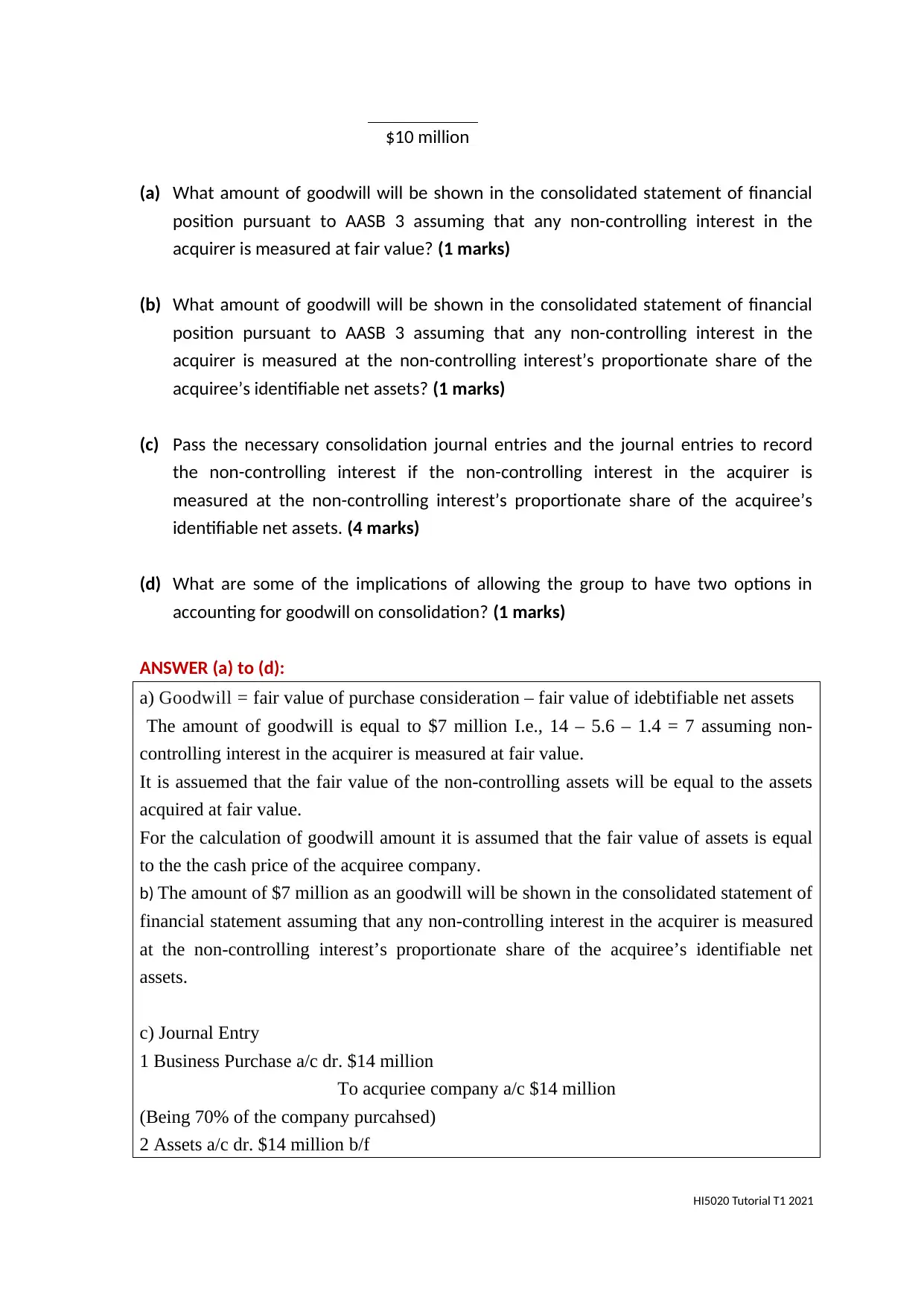

$10 million

(a) What amount of goodwill will be shown in the consolidated statement of financial

position pursuant to AASB 3 assuming that any non-controlling interest in the

acquirer is measured at fair value? (1 marks)

(b) What amount of goodwill will be shown in the consolidated statement of financial

position pursuant to AASB 3 assuming that any non-controlling interest in the

acquirer is measured at the non-controlling interest’s proportionate share of the

acquiree’s identifiable net assets? (1 marks)

(c) Pass the necessary consolidation journal entries and the journal entries to record

the non-controlling interest if the non-controlling interest in the acquirer is

measured at the non-controlling interest’s proportionate share of the acquiree’s

identifiable net assets. (4 marks)

(d) What are some of the implications of allowing the group to have two options in

accounting for goodwill on consolidation? (1 marks)

ANSWER (a) to (d):

a) Goodwill = fair value of purchase consideration – fair value of idebtifiable net assets

The amount of goodwill is equal to $7 million I.e., 14 – 5.6 – 1.4 = 7 assuming non-

controlling interest in the acquirer is measured at fair value.

It is assuemed that the fair value of the non-controlling assets will be equal to the assets

acquired at fair value.

For the calculation of goodwill amount it is assumed that the fair value of assets is equal

to the the cash price of the acquiree company.

b) The amount of $7 million as an goodwill will be shown in the consolidated statement of

financial statement assuming that any non-controlling interest in the acquirer is measured

at the non-controlling interest’s proportionate share of the acquiree’s identifiable net

assets.

c) Journal Entry

1 Business Purchase a/c dr. $14 million

To acquriee company a/c $14 million

(Being 70% of the company purcahsed)

2 Assets a/c dr. $14 million b/f

HI5020 Tutorial T1 2021

(a) What amount of goodwill will be shown in the consolidated statement of financial

position pursuant to AASB 3 assuming that any non-controlling interest in the

acquirer is measured at fair value? (1 marks)

(b) What amount of goodwill will be shown in the consolidated statement of financial

position pursuant to AASB 3 assuming that any non-controlling interest in the

acquirer is measured at the non-controlling interest’s proportionate share of the

acquiree’s identifiable net assets? (1 marks)

(c) Pass the necessary consolidation journal entries and the journal entries to record

the non-controlling interest if the non-controlling interest in the acquirer is

measured at the non-controlling interest’s proportionate share of the acquiree’s

identifiable net assets. (4 marks)

(d) What are some of the implications of allowing the group to have two options in

accounting for goodwill on consolidation? (1 marks)

ANSWER (a) to (d):

a) Goodwill = fair value of purchase consideration – fair value of idebtifiable net assets

The amount of goodwill is equal to $7 million I.e., 14 – 5.6 – 1.4 = 7 assuming non-

controlling interest in the acquirer is measured at fair value.

It is assuemed that the fair value of the non-controlling assets will be equal to the assets

acquired at fair value.

For the calculation of goodwill amount it is assumed that the fair value of assets is equal

to the the cash price of the acquiree company.

b) The amount of $7 million as an goodwill will be shown in the consolidated statement of

financial statement assuming that any non-controlling interest in the acquirer is measured

at the non-controlling interest’s proportionate share of the acquiree’s identifiable net

assets.

c) Journal Entry

1 Business Purchase a/c dr. $14 million

To acquriee company a/c $14 million

(Being 70% of the company purcahsed)

2 Assets a/c dr. $14 million b/f

HI5020 Tutorial T1 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Goodwill a/c dr. $7 million

To Shares a/c $5.6 million (8* 70%)

To Reserves a/c $1.4 million (2* 70%)

To Business Purchase a/c $14 million

(Being assets is recorded at fair value as assumed that the fair value of the asset is 14

million and there is no adjustment made in the assets of the company because of the lack

of information)

The assets is recorded at the fair value because the company wants to do so as the feel that

all assets is stated at fair value on acquisition date.

d) The accountant have to imply the amount of goodwill in their consolidated financial

statement along with the other assets no matter how the goodwill has arises. In the first

option, only the amount of goodwill exclusing the assets and liabilities can be recorded.

And the other option involve the whole consideration paid is recorded as an goodwill in

the balance sheet.

Question 5 (11 marks)

Large Ltd owns 100% of the shares of Small Ltd. These shares were acquired on 1 July

2019 for $1 million when the shareholders’ funds of Small Ltd were:

Share capital $500,000

Retained earnings $400,000

$900,000

All assets of Small Ltd were fairly stated at acquisition date, except for a land that had a

fair value $50000 more than carrying value.

During the 2019/2020 financial year, Small Ltd sold inventory to Large Ltd at a sales price

of $200,000. The inventory cost Small Ltd $120,000 to produce. At 30 June 2020 half of

the stock was still on hand with Large Ltd. In addition, Small Ltd paid an interim dividend

HI5020 Tutorial T1 2021

To Shares a/c $5.6 million (8* 70%)

To Reserves a/c $1.4 million (2* 70%)

To Business Purchase a/c $14 million

(Being assets is recorded at fair value as assumed that the fair value of the asset is 14

million and there is no adjustment made in the assets of the company because of the lack

of information)

The assets is recorded at the fair value because the company wants to do so as the feel that

all assets is stated at fair value on acquisition date.

d) The accountant have to imply the amount of goodwill in their consolidated financial

statement along with the other assets no matter how the goodwill has arises. In the first

option, only the amount of goodwill exclusing the assets and liabilities can be recorded.

And the other option involve the whole consideration paid is recorded as an goodwill in

the balance sheet.

Question 5 (11 marks)

Large Ltd owns 100% of the shares of Small Ltd. These shares were acquired on 1 July

2019 for $1 million when the shareholders’ funds of Small Ltd were:

Share capital $500,000

Retained earnings $400,000

$900,000

All assets of Small Ltd were fairly stated at acquisition date, except for a land that had a

fair value $50000 more than carrying value.

During the 2019/2020 financial year, Small Ltd sold inventory to Large Ltd at a sales price

of $200,000. The inventory cost Small Ltd $120,000 to produce. At 30 June 2020 half of

the stock was still on hand with Large Ltd. In addition, Small Ltd paid an interim dividend

HI5020 Tutorial T1 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

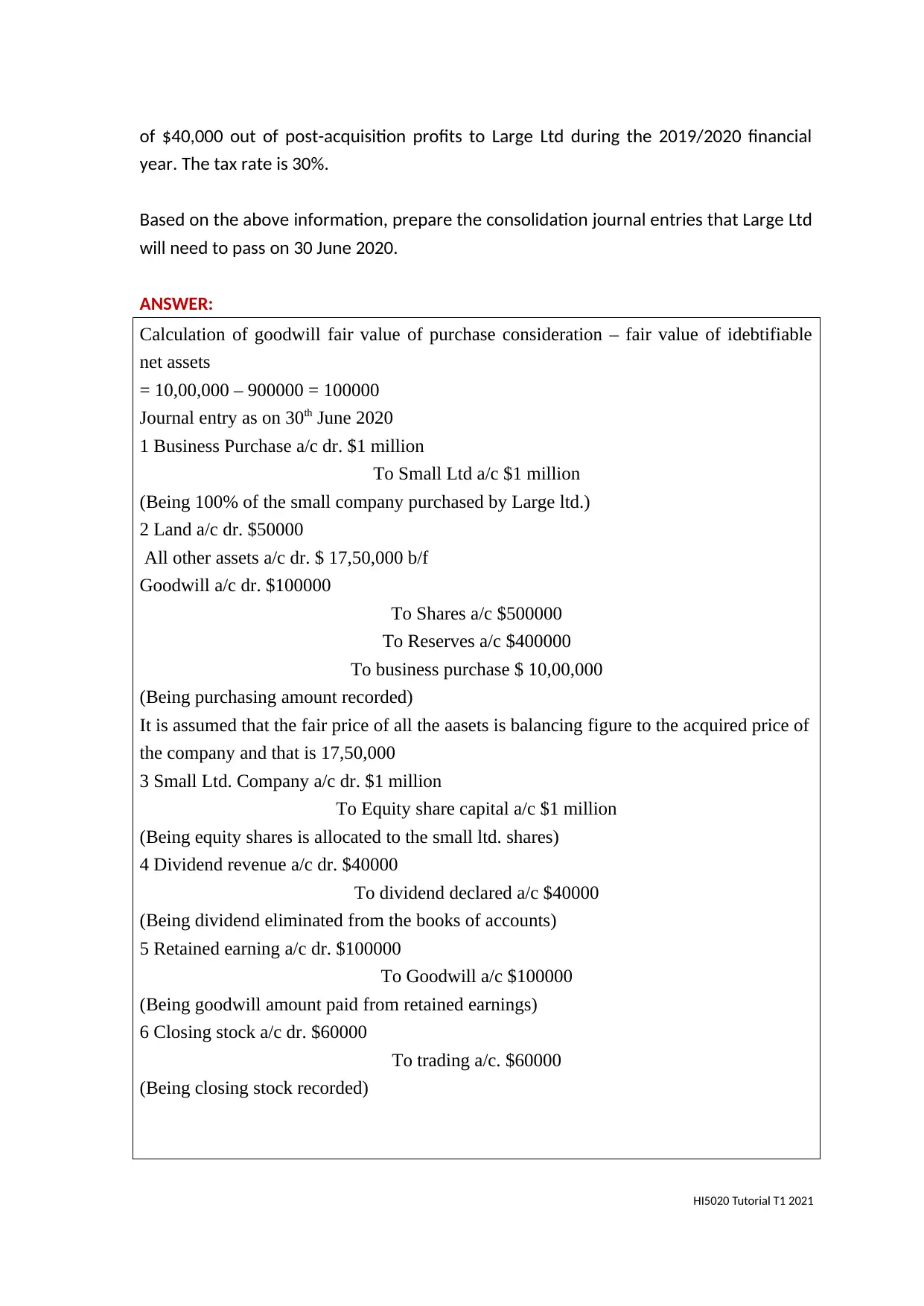

of $40,000 out of post-acquisition profits to Large Ltd during the 2019/2020 financial

year. The tax rate is 30%.

Based on the above information, prepare the consolidation journal entries that Large Ltd

will need to pass on 30 June 2020.

ANSWER:

Calculation of goodwill fair value of purchase consideration – fair value of idebtifiable

net assets

= 10,00,000 – 900000 = 100000

Journal entry as on 30th June 2020

1 Business Purchase a/c dr. $1 million

To Small Ltd a/c $1 million

(Being 100% of the small company purchased by Large ltd.)

2 Land a/c dr. $50000

All other assets a/c dr. $ 17,50,000 b/f

Goodwill a/c dr. $100000

To Shares a/c $500000

To Reserves a/c $400000

To business purchase $ 10,00,000

(Being purchasing amount recorded)

It is assumed that the fair price of all the aasets is balancing figure to the acquired price of

the company and that is 17,50,000

3 Small Ltd. Company a/c dr. $1 million

To Equity share capital a/c $1 million

(Being equity shares is allocated to the small ltd. shares)

4 Dividend revenue a/c dr. $40000

To dividend declared a/c $40000

(Being dividend eliminated from the books of accounts)

5 Retained earning a/c dr. $100000

To Goodwill a/c $100000

(Being goodwill amount paid from retained earnings)

6 Closing stock a/c dr. $60000

To trading a/c. $60000

(Being closing stock recorded)

HI5020 Tutorial T1 2021

year. The tax rate is 30%.

Based on the above information, prepare the consolidation journal entries that Large Ltd

will need to pass on 30 June 2020.

ANSWER:

Calculation of goodwill fair value of purchase consideration – fair value of idebtifiable

net assets

= 10,00,000 – 900000 = 100000

Journal entry as on 30th June 2020

1 Business Purchase a/c dr. $1 million

To Small Ltd a/c $1 million

(Being 100% of the small company purchased by Large ltd.)

2 Land a/c dr. $50000

All other assets a/c dr. $ 17,50,000 b/f

Goodwill a/c dr. $100000

To Shares a/c $500000

To Reserves a/c $400000

To business purchase $ 10,00,000

(Being purchasing amount recorded)

It is assumed that the fair price of all the aasets is balancing figure to the acquired price of

the company and that is 17,50,000

3 Small Ltd. Company a/c dr. $1 million

To Equity share capital a/c $1 million

(Being equity shares is allocated to the small ltd. shares)

4 Dividend revenue a/c dr. $40000

To dividend declared a/c $40000

(Being dividend eliminated from the books of accounts)

5 Retained earning a/c dr. $100000

To Goodwill a/c $100000

(Being goodwill amount paid from retained earnings)

6 Closing stock a/c dr. $60000

To trading a/c. $60000

(Being closing stock recorded)

HI5020 Tutorial T1 2021

Question 6 (11 marks)

(a) Explain the concepts of Local Currency, Functional Currency and Presentation

Currency with suitable examples. (3 Marks)

(b) Explain the rule for translating the Financial Statements of Foreign Operations

from Local Currency to Functional Currency. (4 Marks)

(c) Explain the rule for translating the Financial Statements of Foreign Operations

from Functional Currency to Presentation Currency. (4 Marks)

ANSWER:

a) The local currency is the currency in circulation in the country where the foreign firm is

operating. The local currency is only the functional currency for the entity which is prevailing in

the primary economic environment of the entity. On the other hand the presentation currency is

as defined by the IAS 21, which states that it is the currency in which the particulars of the

financial statements are presented in monetary terms.

Examples are when a UK based company having its major operations in USA may use US dollars

as its functional currency, whereas the Great Britain pound is actually the local currency of the

company and if the same company resorts to expressing their financial statements in terms of

GBP, then the GBP will be regarded as the presentation currency.

b) The rule of translation states that the entity must first determine its functional currency and

then measure foreign (local) currency transactions by applying the spot exchange rate between

the local and functional currency when the transaction takes place in order to prepare financial

statements.

c) translating financial statements prepared on the basis of functional currency into presentation

currency as follows:

- assets and liabilities are valued at closing exchange rate on the date of balance and any

goodwill arising on date of translation are recognised as assets and liabilities of the foreign

operations.

- income statement items are translated at the exchange rate prevailing on the date of

transaction takes place.

- any kind of exchange differences resulting from the translation must be recognised as other

comprehensive income.

END OF TUTORIAL PROJECT

HI5020 Tutorial T1 2021

(a) Explain the concepts of Local Currency, Functional Currency and Presentation

Currency with suitable examples. (3 Marks)

(b) Explain the rule for translating the Financial Statements of Foreign Operations

from Local Currency to Functional Currency. (4 Marks)

(c) Explain the rule for translating the Financial Statements of Foreign Operations

from Functional Currency to Presentation Currency. (4 Marks)

ANSWER:

a) The local currency is the currency in circulation in the country where the foreign firm is

operating. The local currency is only the functional currency for the entity which is prevailing in

the primary economic environment of the entity. On the other hand the presentation currency is

as defined by the IAS 21, which states that it is the currency in which the particulars of the

financial statements are presented in monetary terms.

Examples are when a UK based company having its major operations in USA may use US dollars

as its functional currency, whereas the Great Britain pound is actually the local currency of the

company and if the same company resorts to expressing their financial statements in terms of

GBP, then the GBP will be regarded as the presentation currency.

b) The rule of translation states that the entity must first determine its functional currency and

then measure foreign (local) currency transactions by applying the spot exchange rate between

the local and functional currency when the transaction takes place in order to prepare financial

statements.

c) translating financial statements prepared on the basis of functional currency into presentation

currency as follows:

- assets and liabilities are valued at closing exchange rate on the date of balance and any

goodwill arising on date of translation are recognised as assets and liabilities of the foreign

operations.

- income statement items are translated at the exchange rate prevailing on the date of

transaction takes place.

- any kind of exchange differences resulting from the translation must be recognised as other

comprehensive income.

END OF TUTORIAL PROJECT

HI5020 Tutorial T1 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Submission instructions:

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897 HI5003

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

HI5020 Tutorial T1 2021

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897 HI5003

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

HI5020 Tutorial T1 2021

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.