Analysis of Financial Statements: Westpac, ANZ, and Commonwealth Bank

VerifiedAdded on 2023/04/25

|26

|4347

|246

Report

AI Summary

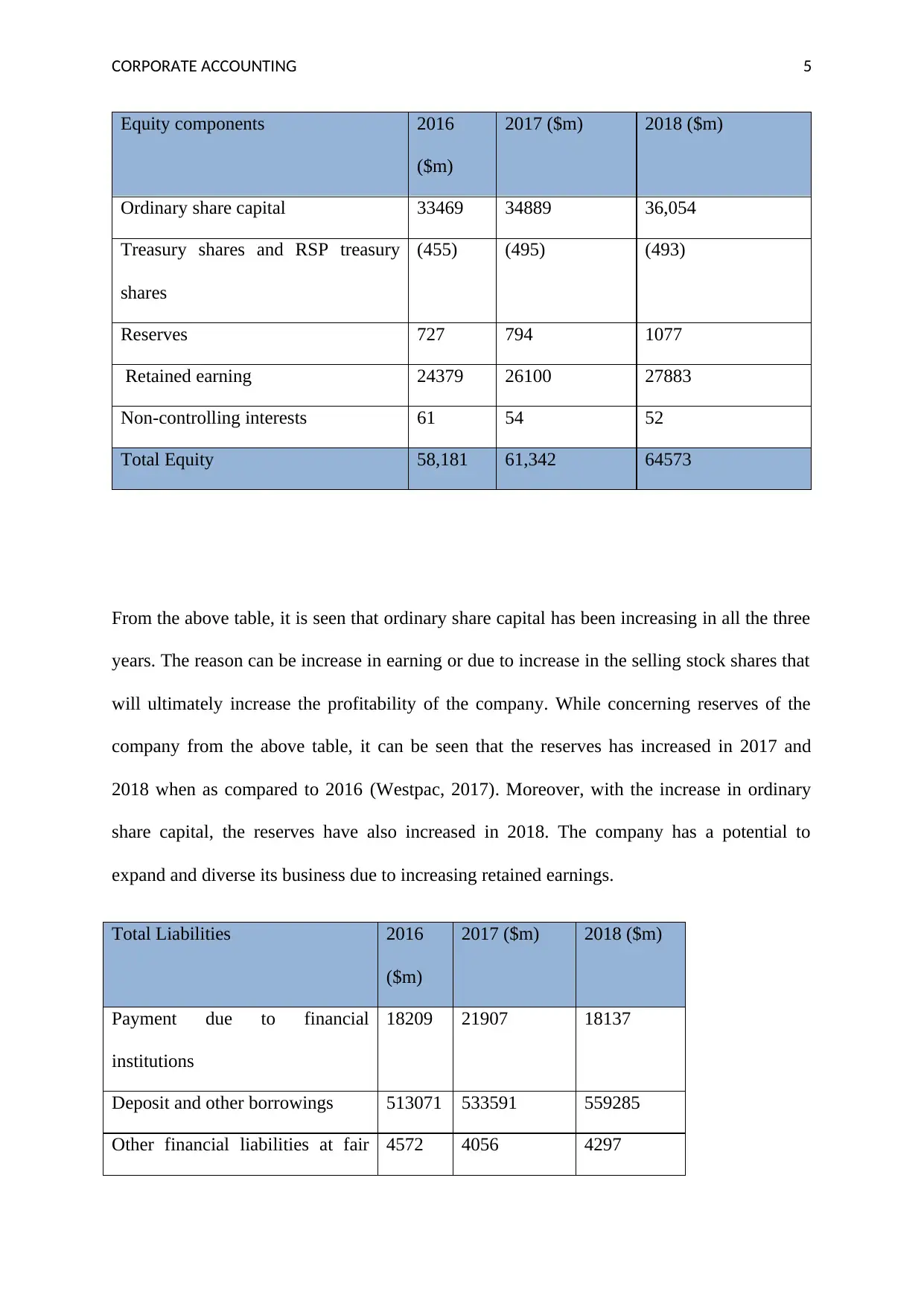

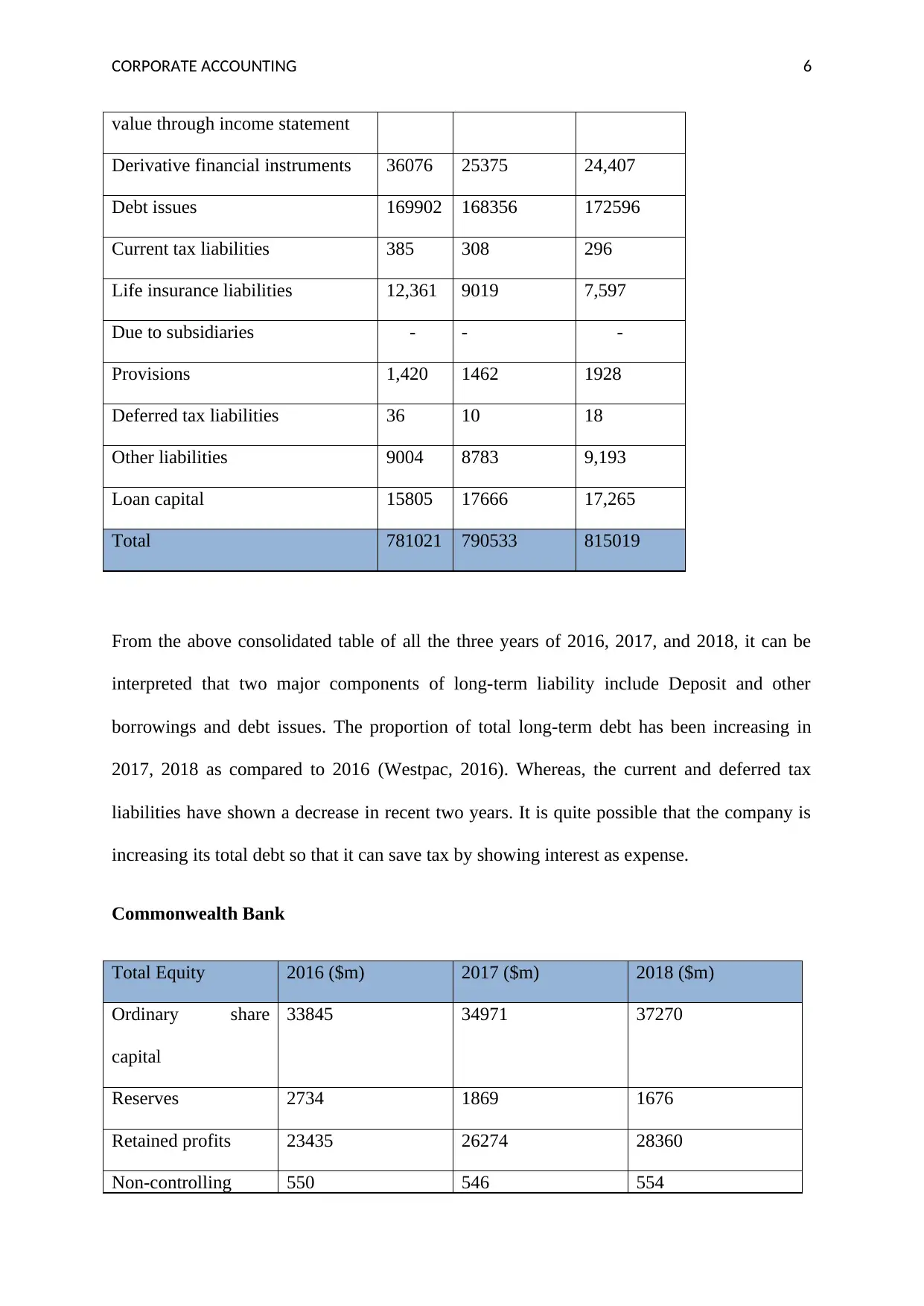

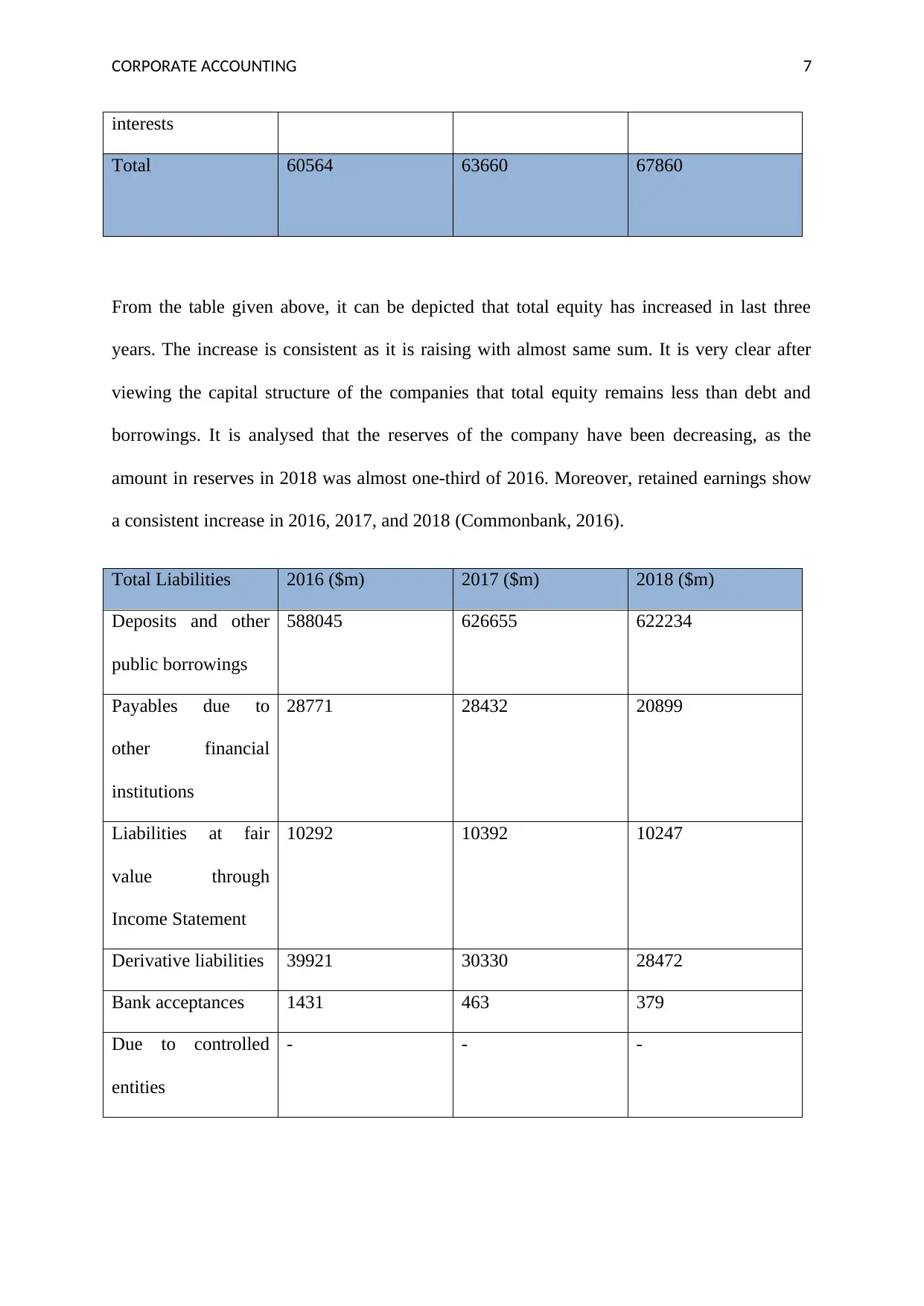

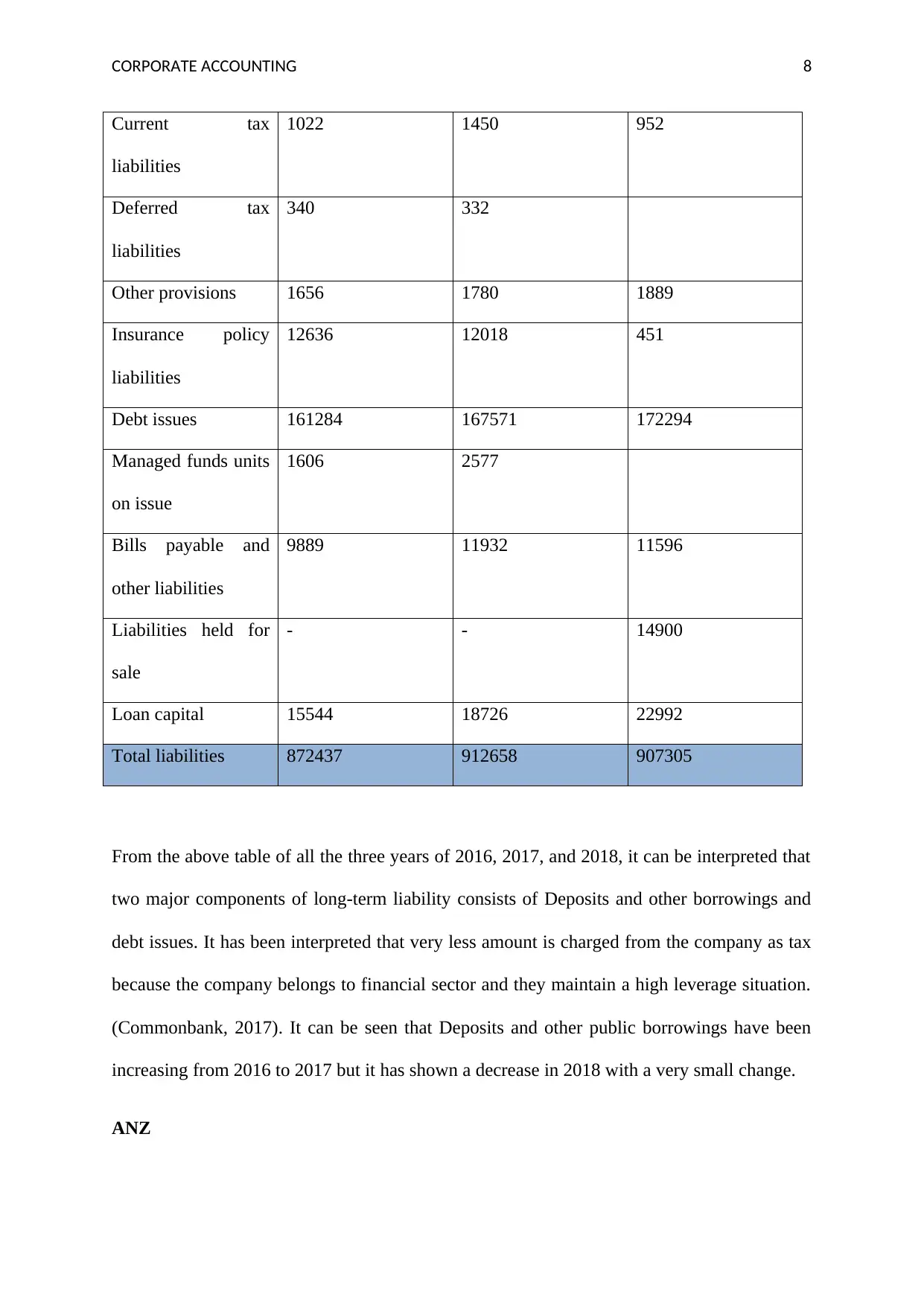

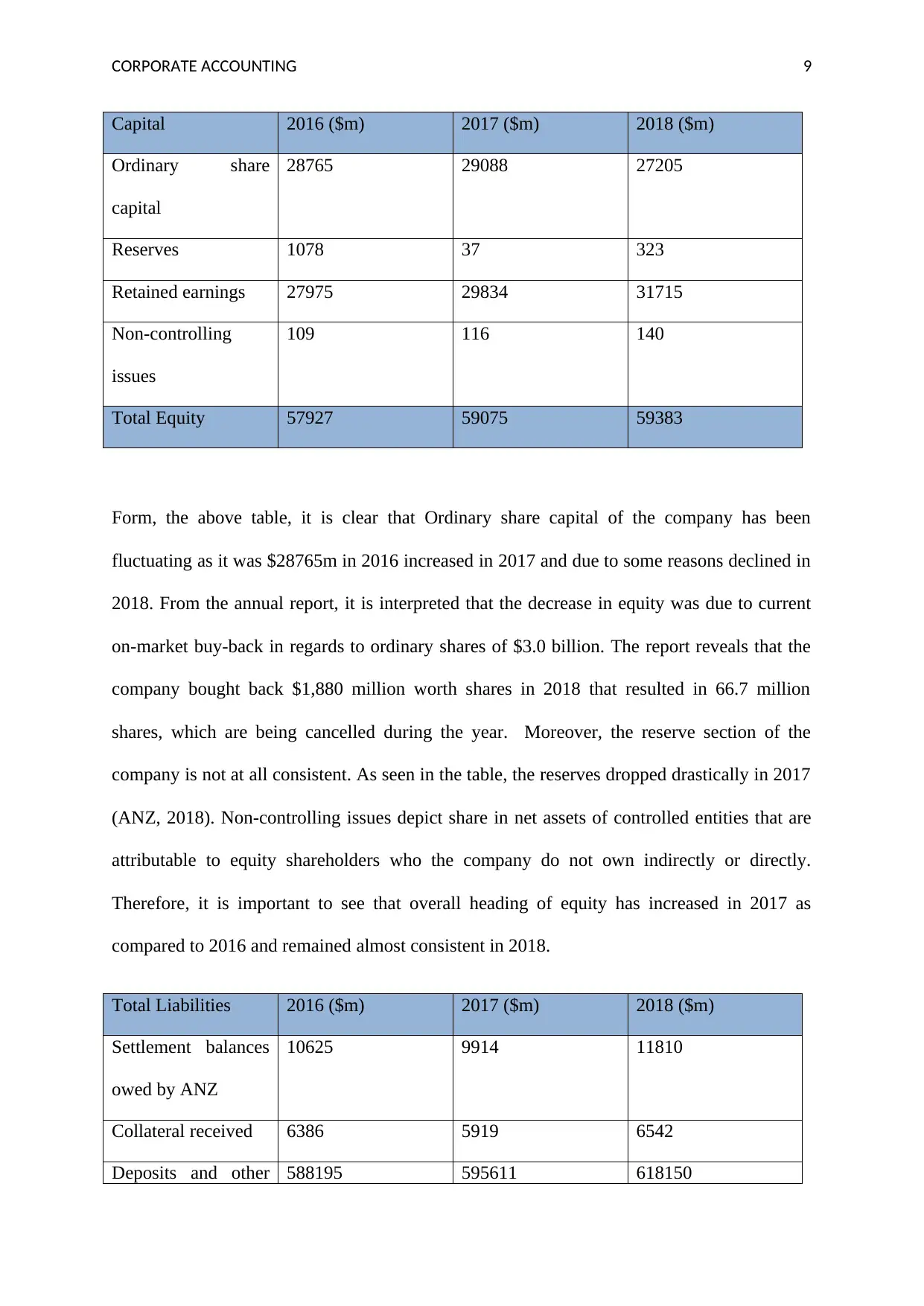

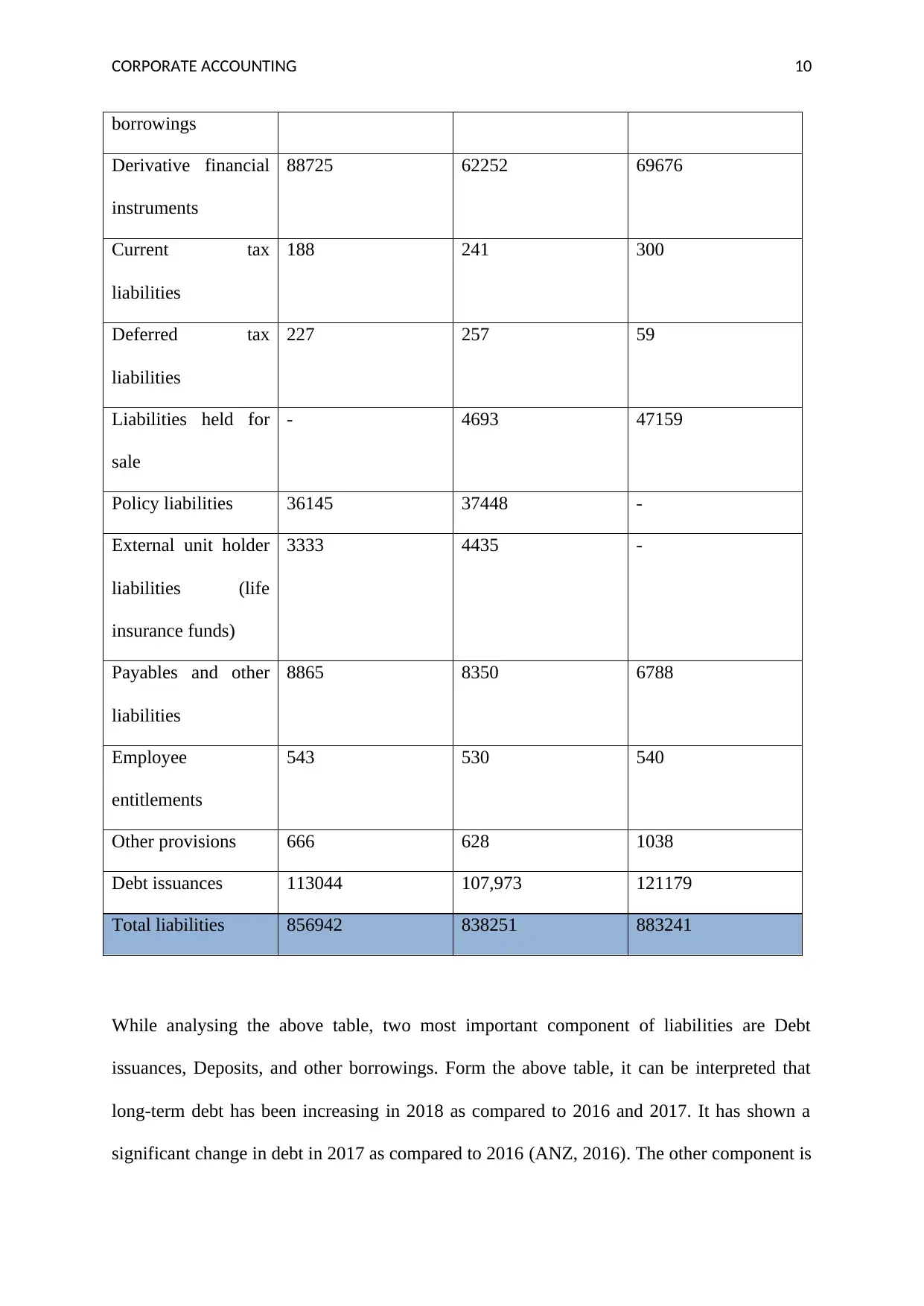

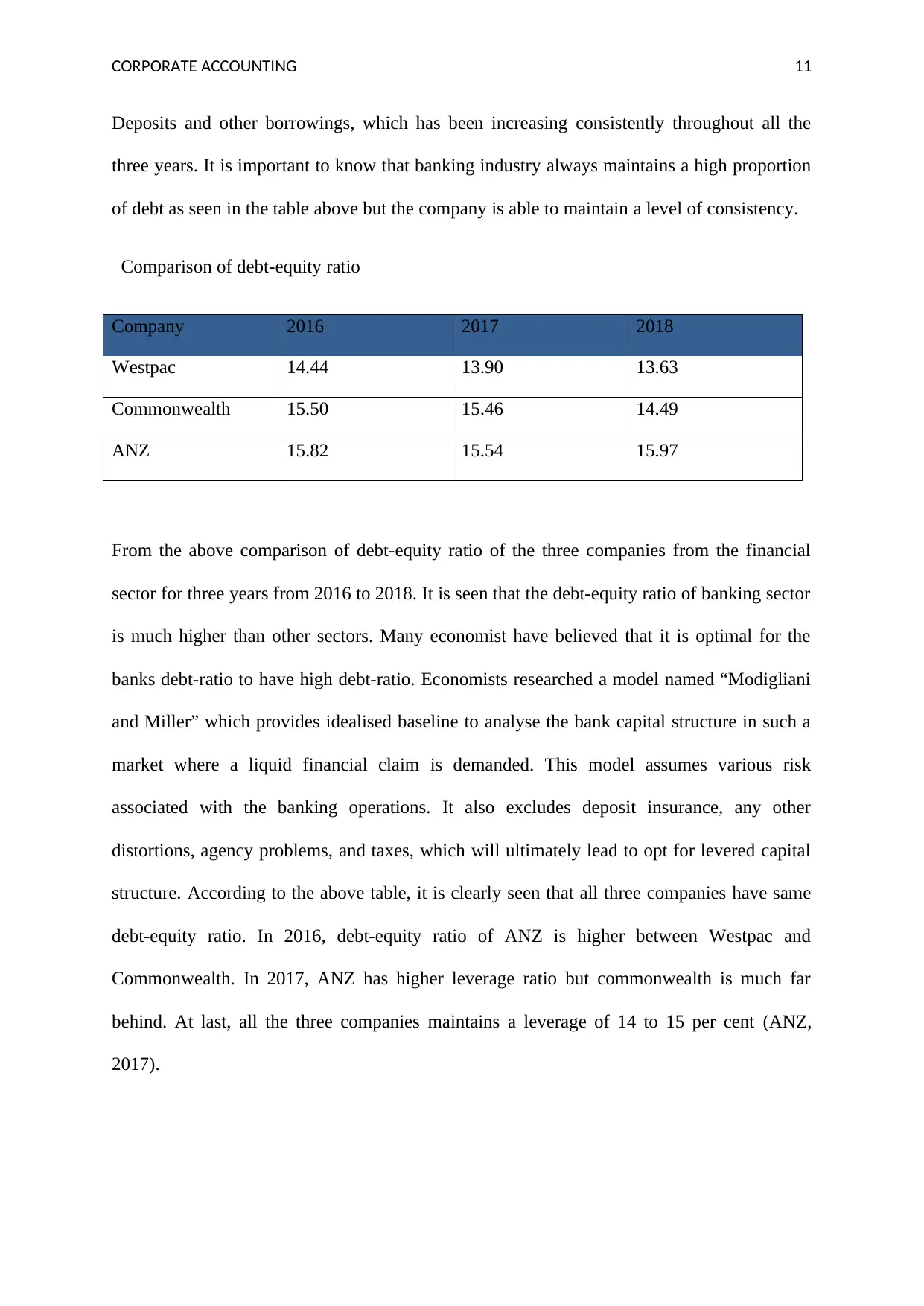

This report provides a comprehensive financial analysis of Westpac, ANZ, and Commonwealth Bank, focusing on their equity, liabilities, and cash flow statements from 2016 to 2018. The analysis includes an examination of the companies' debt-equity ratios, highlighting the high leverage within the financial sector. The report delves into the components of the cash flow statement, revealing insights into the companies' capital positions. Furthermore, it explores the comprehensive income statement, including items not recorded in the income statement, and the impact of deferred tax and liabilities on the companies' consumption and saving patterns. The report also offers a comparative analysis of the financial performance of the three banks, drawing conclusions on their financial stability and profitability. The report structure includes an introduction, analysis of equity and liabilities, cash flow statements, income statements, and corporate income tax accounting, culminating in a conclusion based on the financial data examined. The report adheres to the guidelines of the HI5020 Corporate Accounting course, offering a detailed assessment of the financial health of these prominent Australian banks.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.