HI5020 Corporate Accounting: Comparative Analysis of Myer & Kathmandu

VerifiedAdded on 2023/06/04

|18

|4290

|486

Report

AI Summary

This report provides a comparative financial analysis of Myer Holdings Ltd and Kathmandu Holdings Ltd, two companies listed on the Australian Securities Exchange (ASX). The analysis covers key areas such as owner's equity, cash flow statements, other comprehensive income statements, and corporate income tax. The report finds that Myer Holdings Ltd has a higher equity compared to Kathmandu Holdings Ltd, but also a higher debt-to-equity ratio, indicating a greater reliance on debt financing. The cash flow analysis reveals that Myer Holdings Ltd made larger investments, resulting in a greater net decrease in cash held. The study also examines the components of other comprehensive income for both companies and calculates their effective tax rates, noting a higher rate for Kathmandu Ltd. The analysis is based on the companies' annual reports and relevant accounting standards.

CORPORATE

ACCOUNTING

2018

ACCOUNTING

2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Corporate accounting deals with the procedures related to preparation of balance sheet,

comprehensive statement of profit and loss and cash flow statement. Further, with the

assistance of financial reporting management is able to disclose the financial position of the

company to investors, administrators as well as to government. Present report revolves

around analysis regarding the equity, cash flow statement, another comprehensive statement

and tax expenses of Myer Holding and Kathmandu Holdings Ltd are done. The study reveals

that the equity of Myer Holdings Ltd is higher than the Kathmandu Ltd. Moreover, the net

decrease in cash flow of Kathmandu Ltd is more due to the repayment of loans and

procurement of assets. Since the profit is already included in the other comprehensive income

statement, there will be no impact on the shareholder's profit appropriation in case

comprehensive income items are included in profit and loss account. Subsequently, an

effective tax rate of both the companies is calculated under which the tax rate of Kathmandu

Ltd is more in comparison to Myer Ltd.

Corporate accounting deals with the procedures related to preparation of balance sheet,

comprehensive statement of profit and loss and cash flow statement. Further, with the

assistance of financial reporting management is able to disclose the financial position of the

company to investors, administrators as well as to government. Present report revolves

around analysis regarding the equity, cash flow statement, another comprehensive statement

and tax expenses of Myer Holding and Kathmandu Holdings Ltd are done. The study reveals

that the equity of Myer Holdings Ltd is higher than the Kathmandu Ltd. Moreover, the net

decrease in cash flow of Kathmandu Ltd is more due to the repayment of loans and

procurement of assets. Since the profit is already included in the other comprehensive income

statement, there will be no impact on the shareholder's profit appropriation in case

comprehensive income items are included in profit and loss account. Subsequently, an

effective tax rate of both the companies is calculated under which the tax rate of Kathmandu

Ltd is more in comparison to Myer Ltd.

Table of Contents

Introduction................................................................................................................................5

Overview of Companies............................................................................................................5

Myer Holdings Ltd.................................................................................................................5

Kathmandu Holdings Ltd.......................................................................................................5

OWNERS EQUITY...................................................................................................................6

(I)............................................................................................................................................6

(II)..........................................................................................................................................7

CASH FLOWS STATEMENT..........................................................................................7

(III).........................................................................................................................................7

(IV).........................................................................................................................................9

(V)........................................................................................................................................10

OTHER COMPREHENSIVE INCOME STATEMENT........................................................10

(VI).......................................................................................................................................10

(VII)......................................................................................................................................11

(IX).......................................................................................................................................12

ACCOUNTING FOR CROPORATE INCOME TAX............................................................13

(X)........................................................................................................................................13

(XI).......................................................................................................................................13

(XII)......................................................................................................................................14

(XIII)....................................................................................................................................14

(XIV)....................................................................................................................................15

(XV).....................................................................................................................................15

(XVI)....................................................................................................................................16

Conclusion................................................................................................................................16

References................................................................................................................................17

Introduction................................................................................................................................5

Overview of Companies............................................................................................................5

Myer Holdings Ltd.................................................................................................................5

Kathmandu Holdings Ltd.......................................................................................................5

OWNERS EQUITY...................................................................................................................6

(I)............................................................................................................................................6

(II)..........................................................................................................................................7

CASH FLOWS STATEMENT..........................................................................................7

(III).........................................................................................................................................7

(IV).........................................................................................................................................9

(V)........................................................................................................................................10

OTHER COMPREHENSIVE INCOME STATEMENT........................................................10

(VI).......................................................................................................................................10

(VII)......................................................................................................................................11

(IX).......................................................................................................................................12

ACCOUNTING FOR CROPORATE INCOME TAX............................................................13

(X)........................................................................................................................................13

(XI).......................................................................................................................................13

(XII)......................................................................................................................................14

(XIII)....................................................................................................................................14

(XIV)....................................................................................................................................15

(XV).....................................................................................................................................15

(XVI)....................................................................................................................................16

Conclusion................................................................................................................................16

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List of Tables

Table 1: Equity assessment of Myer Ltd and Kathmandu Ltd...................................................6

Table 2: Statement representing debt-equity of both the companies.........................................7

Table 3: Statement representing variants of cash flow statement of Myer Holdings................8

Table 4: Statement representing variants of cash flow statement of Kathmandu Holdings......8

Table 5: Statement representing comparative analysis of cash flow statement of Myer

Holdings.....................................................................................................................................9

Table 6: Statement representing comparative analysis of cash flow statement of Kathmandu

Holdings.....................................................................................................................................9

Table 7: Comparative Analysis of Cash Flow of Myer Holding and Kathmandu Holding.....10

Table 8 Elements of Other Comprehensive Income of Myer Holding....................................11

Table 9: Elements of Other Comprehensive Income of Kathmandu Holding.........................11

Table 10: Statement presenting income tax expense of Myer Holding and Kathmandu

Holding.....................................................................................................................................13

Table 11: Statement representing deferred tax asset and deferred tax liabilities.....................14

Table 1: Equity assessment of Myer Ltd and Kathmandu Ltd...................................................6

Table 2: Statement representing debt-equity of both the companies.........................................7

Table 3: Statement representing variants of cash flow statement of Myer Holdings................8

Table 4: Statement representing variants of cash flow statement of Kathmandu Holdings......8

Table 5: Statement representing comparative analysis of cash flow statement of Myer

Holdings.....................................................................................................................................9

Table 6: Statement representing comparative analysis of cash flow statement of Kathmandu

Holdings.....................................................................................................................................9

Table 7: Comparative Analysis of Cash Flow of Myer Holding and Kathmandu Holding.....10

Table 8 Elements of Other Comprehensive Income of Myer Holding....................................11

Table 9: Elements of Other Comprehensive Income of Kathmandu Holding.........................11

Table 10: Statement presenting income tax expense of Myer Holding and Kathmandu

Holding.....................................................................................................................................13

Table 11: Statement representing deferred tax asset and deferred tax liabilities.....................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial Reporting comprises disclosure of financial information to the various stakeholders

relating to financial performance and financial position of the company over a specified time.

Each part of the financial report, i.e. statement of profit and loss, statement of affairs of the

company, statement of changes in equity and cash flow statement reveal significant

information relating to the organization. The manner in which operations are being continued

in the company can be revealed from same. The present report provides an assessment of

equity, other comprehensive income, taxation and cash flow of Mayer Holding and

Kathmandu Holding. Further, all these specified parts of the financial report of both the

companies have been compared in order to provide an appropriate opinion.

OVERVIEW OF COMPANIES

Myer Holdings Ltd

Myer Holdings Limited (Myer) is a department store company situated in Australia. Its

department store network comprises a trail of about 60 retail locations in Australia. The Myer

retail deals with 11 different types of products such as Women’s wear, Menswear, Youth

shop, Intimate wears, Cosmetics, perfumes, homewares, electrical appliances, toys, handbags,

accessories along with general products. In addition to this, it also owns women wear fashion

brand sass & bide, which is an Australian designer brand. The brand of the company

comprises TOPSHOP TOPMAN, Seed, French Connection, Mimco, Veronika Mainr, Jack &

Jones as well as Industrie. Moreover, its ancillary companies are Myer Pty Ltd, NB Elizabeth

Pty, NB Russell Pty Ltd, Warehouse Solutions Pty Ltd, Myer Group Finance Ltd, Myer

Group Pty Ltd and Myer Travel Pty Ltd. Apart from this, the company also undertakes

activities outside the department store with its ancillaries sass & bide, FSS Retail Pty Ltd.

Kathmandu Holdings Ltd

Kathmandu Holdings Ltd is a public company established in New Zealand dealing with

design, marketing and retail sale of clothing as well as clothing and equipment for travel and

outdoor use. Approximately1900 employees are employed in the company. It operates in

New Zealand, Australia and UK. Further, it is administrated by its head office in

Christchurch which is located in New Zealand. Currently, the company is functioning 163

Financial Reporting comprises disclosure of financial information to the various stakeholders

relating to financial performance and financial position of the company over a specified time.

Each part of the financial report, i.e. statement of profit and loss, statement of affairs of the

company, statement of changes in equity and cash flow statement reveal significant

information relating to the organization. The manner in which operations are being continued

in the company can be revealed from same. The present report provides an assessment of

equity, other comprehensive income, taxation and cash flow of Mayer Holding and

Kathmandu Holding. Further, all these specified parts of the financial report of both the

companies have been compared in order to provide an appropriate opinion.

OVERVIEW OF COMPANIES

Myer Holdings Ltd

Myer Holdings Limited (Myer) is a department store company situated in Australia. Its

department store network comprises a trail of about 60 retail locations in Australia. The Myer

retail deals with 11 different types of products such as Women’s wear, Menswear, Youth

shop, Intimate wears, Cosmetics, perfumes, homewares, electrical appliances, toys, handbags,

accessories along with general products. In addition to this, it also owns women wear fashion

brand sass & bide, which is an Australian designer brand. The brand of the company

comprises TOPSHOP TOPMAN, Seed, French Connection, Mimco, Veronika Mainr, Jack &

Jones as well as Industrie. Moreover, its ancillary companies are Myer Pty Ltd, NB Elizabeth

Pty, NB Russell Pty Ltd, Warehouse Solutions Pty Ltd, Myer Group Finance Ltd, Myer

Group Pty Ltd and Myer Travel Pty Ltd. Apart from this, the company also undertakes

activities outside the department store with its ancillaries sass & bide, FSS Retail Pty Ltd.

Kathmandu Holdings Ltd

Kathmandu Holdings Ltd is a public company established in New Zealand dealing with

design, marketing and retail sale of clothing as well as clothing and equipment for travel and

outdoor use. Approximately1900 employees are employed in the company. It operates in

New Zealand, Australia and UK. Further, it is administrated by its head office in

Christchurch which is located in New Zealand. Currently, the company is functioning 163

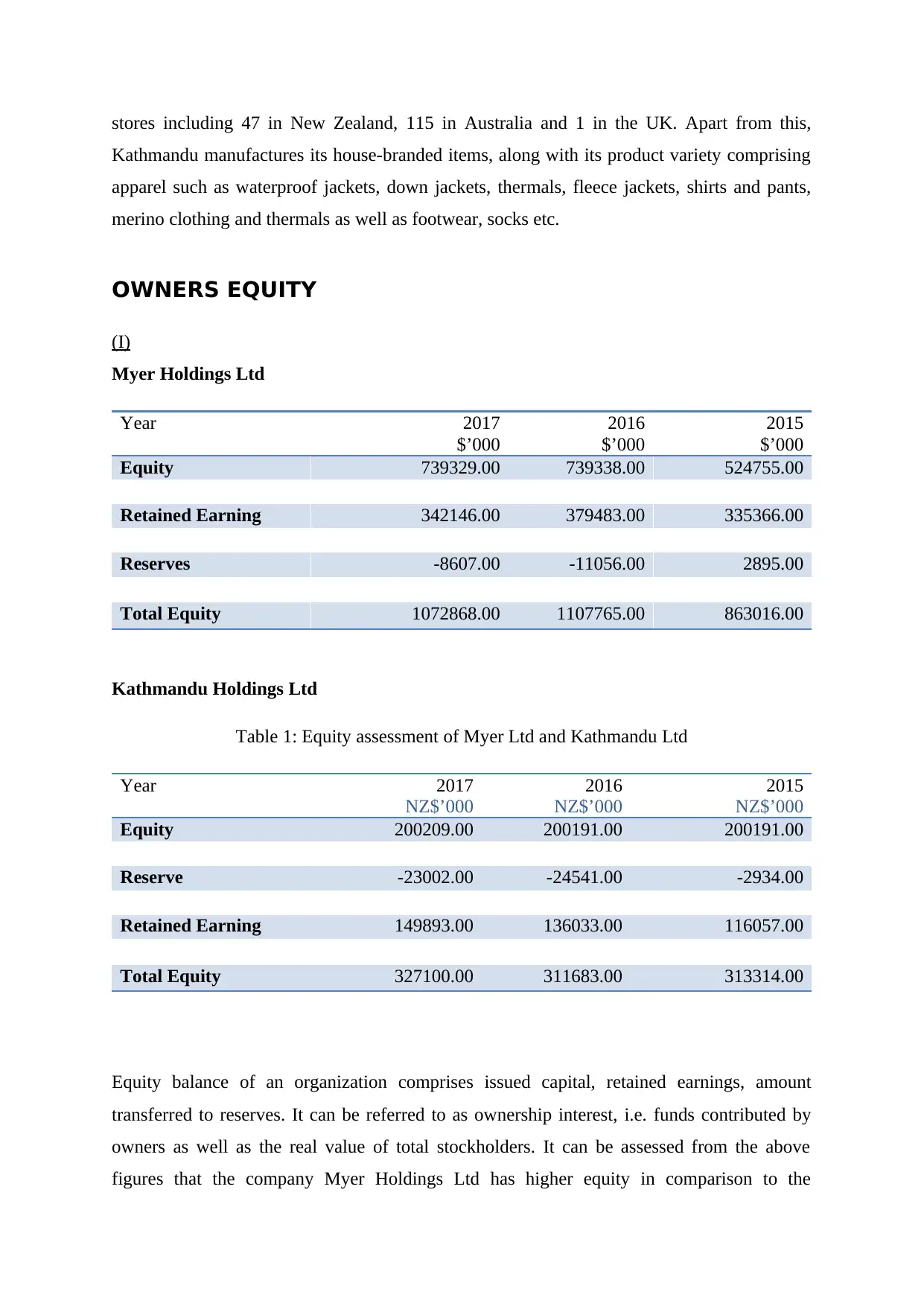

stores including 47 in New Zealand, 115 in Australia and 1 in the UK. Apart from this,

Kathmandu manufactures its house-branded items, along with its product variety comprising

apparel such as waterproof jackets, down jackets, thermals, fleece jackets, shirts and pants,

merino clothing and thermals as well as footwear, socks etc.

OWNERS EQUITY

(I)

Myer Holdings Ltd

Year 2017

$’000

2016

$’000

2015

$’000

Equity 739329.00 739338.00 524755.00

Retained Earning 342146.00 379483.00 335366.00

Reserves -8607.00 -11056.00 2895.00

Total Equity 1072868.00 1107765.00 863016.00

Kathmandu Holdings Ltd

Table 1: Equity assessment of Myer Ltd and Kathmandu Ltd

Year 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Equity 200209.00 200191.00 200191.00

Reserve -23002.00 -24541.00 -2934.00

Retained Earning 149893.00 136033.00 116057.00

Total Equity 327100.00 311683.00 313314.00

Equity balance of an organization comprises issued capital, retained earnings, amount

transferred to reserves. It can be referred to as ownership interest, i.e. funds contributed by

owners as well as the real value of total stockholders. It can be assessed from the above

figures that the company Myer Holdings Ltd has higher equity in comparison to the

Kathmandu manufactures its house-branded items, along with its product variety comprising

apparel such as waterproof jackets, down jackets, thermals, fleece jackets, shirts and pants,

merino clothing and thermals as well as footwear, socks etc.

OWNERS EQUITY

(I)

Myer Holdings Ltd

Year 2017

$’000

2016

$’000

2015

$’000

Equity 739329.00 739338.00 524755.00

Retained Earning 342146.00 379483.00 335366.00

Reserves -8607.00 -11056.00 2895.00

Total Equity 1072868.00 1107765.00 863016.00

Kathmandu Holdings Ltd

Table 1: Equity assessment of Myer Ltd and Kathmandu Ltd

Year 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Equity 200209.00 200191.00 200191.00

Reserve -23002.00 -24541.00 -2934.00

Retained Earning 149893.00 136033.00 116057.00

Total Equity 327100.00 311683.00 313314.00

Equity balance of an organization comprises issued capital, retained earnings, amount

transferred to reserves. It can be referred to as ownership interest, i.e. funds contributed by

owners as well as the real value of total stockholders. It can be assessed from the above

figures that the company Myer Holdings Ltd has higher equity in comparison to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

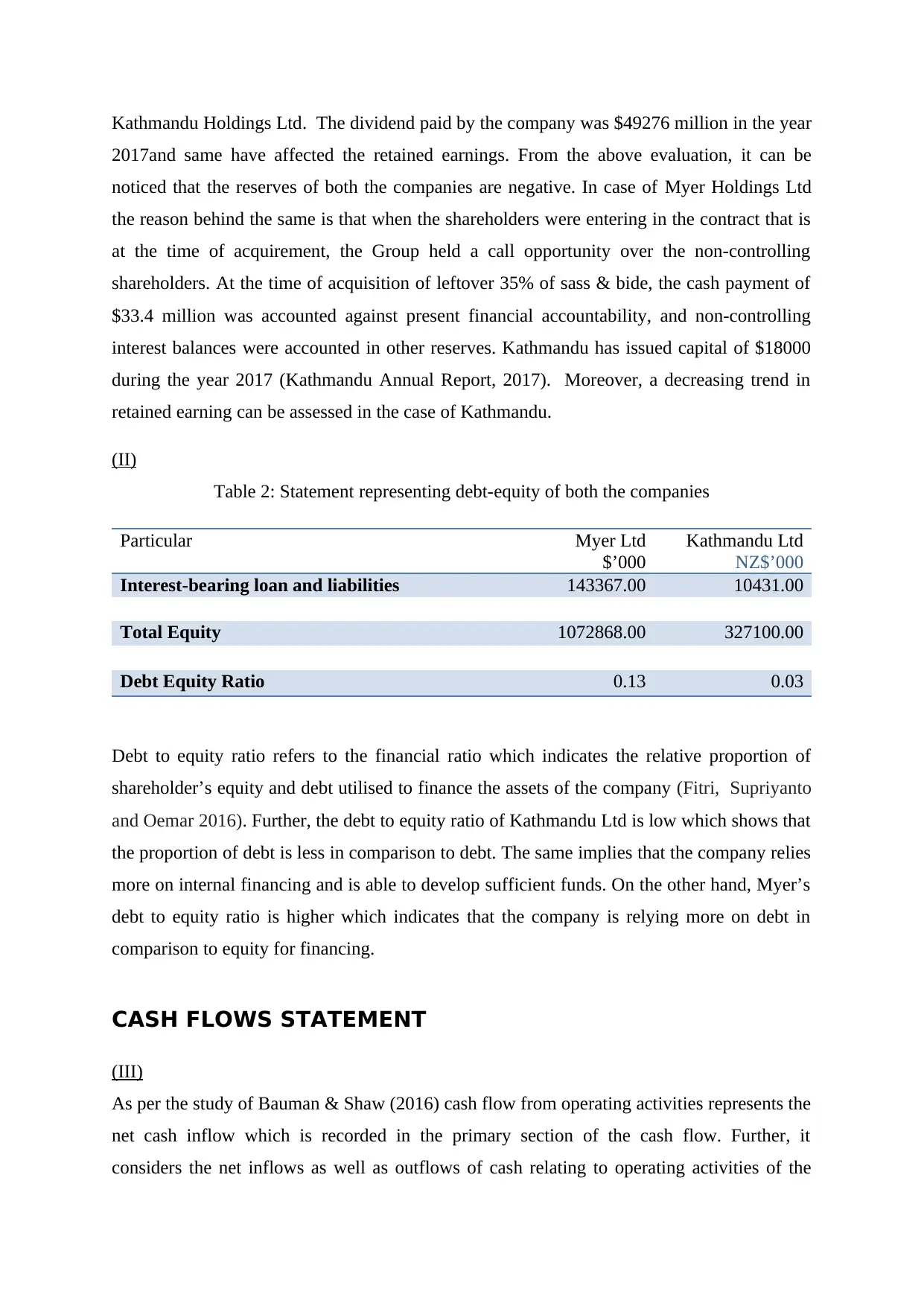

Kathmandu Holdings Ltd. The dividend paid by the company was $49276 million in the year

2017and same have affected the retained earnings. From the above evaluation, it can be

noticed that the reserves of both the companies are negative. In case of Myer Holdings Ltd

the reason behind the same is that when the shareholders were entering in the contract that is

at the time of acquirement, the Group held a call opportunity over the non-controlling

shareholders. At the time of acquisition of leftover 35% of sass & bide, the cash payment of

$33.4 million was accounted against present financial accountability, and non-controlling

interest balances were accounted in other reserves. Kathmandu has issued capital of $18000

during the year 2017 (Kathmandu Annual Report, 2017). Moreover, a decreasing trend in

retained earning can be assessed in the case of Kathmandu.

(II)

Table 2: Statement representing debt-equity of both the companies

Particular Myer Ltd

$’000

Kathmandu Ltd

NZ$’000

Interest-bearing loan and liabilities 143367.00 10431.00

Total Equity 1072868.00 327100.00

Debt Equity Ratio 0.13 0.03

Debt to equity ratio refers to the financial ratio which indicates the relative proportion of

shareholder’s equity and debt utilised to finance the assets of the company (Fitri, Supriyanto

and Oemar 2016). Further, the debt to equity ratio of Kathmandu Ltd is low which shows that

the proportion of debt is less in comparison to debt. The same implies that the company relies

more on internal financing and is able to develop sufficient funds. On the other hand, Myer’s

debt to equity ratio is higher which indicates that the company is relying more on debt in

comparison to equity for financing.

CASH FLOWS STATEMENT

(III)

As per the study of Bauman & Shaw (2016) cash flow from operating activities represents the

net cash inflow which is recorded in the primary section of the cash flow. Further, it

considers the net inflows as well as outflows of cash relating to operating activities of the

2017and same have affected the retained earnings. From the above evaluation, it can be

noticed that the reserves of both the companies are negative. In case of Myer Holdings Ltd

the reason behind the same is that when the shareholders were entering in the contract that is

at the time of acquirement, the Group held a call opportunity over the non-controlling

shareholders. At the time of acquisition of leftover 35% of sass & bide, the cash payment of

$33.4 million was accounted against present financial accountability, and non-controlling

interest balances were accounted in other reserves. Kathmandu has issued capital of $18000

during the year 2017 (Kathmandu Annual Report, 2017). Moreover, a decreasing trend in

retained earning can be assessed in the case of Kathmandu.

(II)

Table 2: Statement representing debt-equity of both the companies

Particular Myer Ltd

$’000

Kathmandu Ltd

NZ$’000

Interest-bearing loan and liabilities 143367.00 10431.00

Total Equity 1072868.00 327100.00

Debt Equity Ratio 0.13 0.03

Debt to equity ratio refers to the financial ratio which indicates the relative proportion of

shareholder’s equity and debt utilised to finance the assets of the company (Fitri, Supriyanto

and Oemar 2016). Further, the debt to equity ratio of Kathmandu Ltd is low which shows that

the proportion of debt is less in comparison to debt. The same implies that the company relies

more on internal financing and is able to develop sufficient funds. On the other hand, Myer’s

debt to equity ratio is higher which indicates that the company is relying more on debt in

comparison to equity for financing.

CASH FLOWS STATEMENT

(III)

As per the study of Bauman & Shaw (2016) cash flow from operating activities represents the

net cash inflow which is recorded in the primary section of the cash flow. Further, it

considers the net inflows as well as outflows of cash relating to operating activities of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company (Cable, Healy, and Sun, 2018). According to Collins, Hribar and Tian (2014),

investing activities of cash flow refers to an item of a cash flow statement which reports the

aggregate change in the cash position of the company resulting from the gains and losses of

the investment. Financing activities of cash flow refer to that category of cash flow statement

which accounts external activities that enable a company to raise capital (Lee 2014).

Moreover, with accordance to Gitman, Juchau and Flanagan (2015), it also involves payment

of dividend to investors, changing in loans or issuing more inventories.

Table 3: Statement representing variants of cash flow statement of Myer Holdings

(Amount in $000)

Year 2017 2016 2015

Operating Cash Inflow 149278.00 149490.00 96915.00

Investing Cash Outflow -109456.00 -58251.00 -62350.00

Financing Cash Outflow -54438.00 -99355.00 -54806.00

Net Decrease in Cash Held -14,616 -8116 -20241

Table 4: Statement representing variants of cash flow statement of Kathmandu Holdings

Particulars 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Operating Cash Inflow 67273.00 69080.00 29627.00

Investing Cash Outflow -13275.00 -23191.00 -19980.00

Financing Cash Outflow -57382.00 -40730.00 -14898.00

Net Decrease in Cash Held -3384 5159 -5251

investing activities of cash flow refers to an item of a cash flow statement which reports the

aggregate change in the cash position of the company resulting from the gains and losses of

the investment. Financing activities of cash flow refer to that category of cash flow statement

which accounts external activities that enable a company to raise capital (Lee 2014).

Moreover, with accordance to Gitman, Juchau and Flanagan (2015), it also involves payment

of dividend to investors, changing in loans or issuing more inventories.

Table 3: Statement representing variants of cash flow statement of Myer Holdings

(Amount in $000)

Year 2017 2016 2015

Operating Cash Inflow 149278.00 149490.00 96915.00

Investing Cash Outflow -109456.00 -58251.00 -62350.00

Financing Cash Outflow -54438.00 -99355.00 -54806.00

Net Decrease in Cash Held -14,616 -8116 -20241

Table 4: Statement representing variants of cash flow statement of Kathmandu Holdings

Particulars 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Operating Cash Inflow 67273.00 69080.00 29627.00

Investing Cash Outflow -13275.00 -23191.00 -19980.00

Financing Cash Outflow -57382.00 -40730.00 -14898.00

Net Decrease in Cash Held -3384 5159 -5251

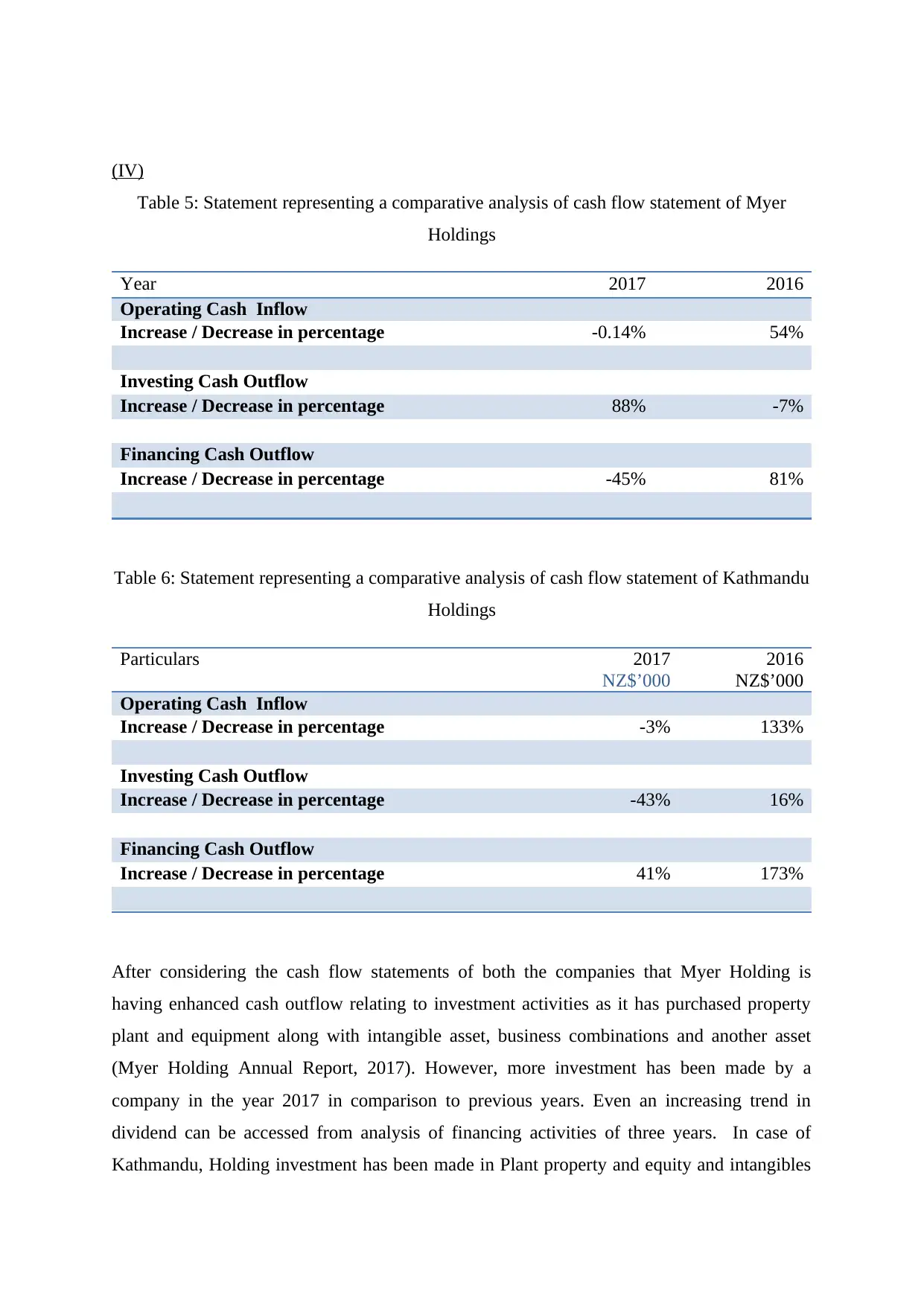

(IV)

Table 5: Statement representing a comparative analysis of cash flow statement of Myer

Holdings

Year 2017 2016

Operating Cash Inflow

Increase / Decrease in percentage -0.14% 54%

Investing Cash Outflow

Increase / Decrease in percentage 88% -7%

Financing Cash Outflow

Increase / Decrease in percentage -45% 81%

Table 6: Statement representing a comparative analysis of cash flow statement of Kathmandu

Holdings

Particulars 2017

NZ$’000

2016

NZ$’000

Operating Cash Inflow

Increase / Decrease in percentage -3% 133%

Investing Cash Outflow

Increase / Decrease in percentage -43% 16%

Financing Cash Outflow

Increase / Decrease in percentage 41% 173%

After considering the cash flow statements of both the companies that Myer Holding is

having enhanced cash outflow relating to investment activities as it has purchased property

plant and equipment along with intangible asset, business combinations and another asset

(Myer Holding Annual Report, 2017). However, more investment has been made by a

company in the year 2017 in comparison to previous years. Even an increasing trend in

dividend can be accessed from analysis of financing activities of three years. In case of

Kathmandu, Holding investment has been made in Plant property and equity and intangibles

Table 5: Statement representing a comparative analysis of cash flow statement of Myer

Holdings

Year 2017 2016

Operating Cash Inflow

Increase / Decrease in percentage -0.14% 54%

Investing Cash Outflow

Increase / Decrease in percentage 88% -7%

Financing Cash Outflow

Increase / Decrease in percentage -45% 81%

Table 6: Statement representing a comparative analysis of cash flow statement of Kathmandu

Holdings

Particulars 2017

NZ$’000

2016

NZ$’000

Operating Cash Inflow

Increase / Decrease in percentage -3% 133%

Investing Cash Outflow

Increase / Decrease in percentage -43% 16%

Financing Cash Outflow

Increase / Decrease in percentage 41% 173%

After considering the cash flow statements of both the companies that Myer Holding is

having enhanced cash outflow relating to investment activities as it has purchased property

plant and equipment along with intangible asset, business combinations and another asset

(Myer Holding Annual Report, 2017). However, more investment has been made by a

company in the year 2017 in comparison to previous years. Even an increasing trend in

dividend can be accessed from analysis of financing activities of three years. In case of

Kathmandu, Holding investment has been made in Plant property and equity and intangibles

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

only. After analyzing three years, it can be concluded that major of the investment has been

made in the year 2016 (Kathmandu Holdings Ltd Annual Report 2017).

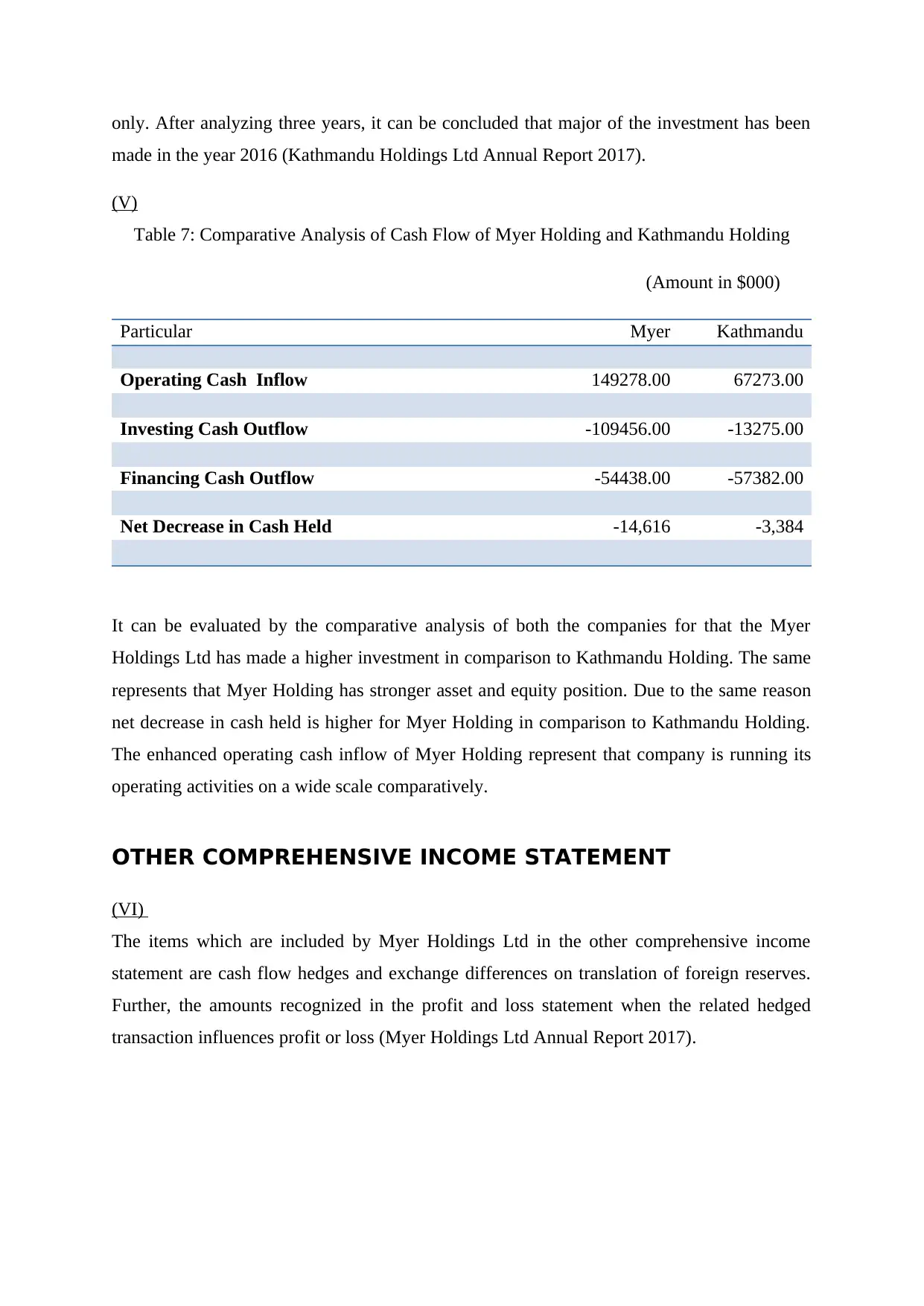

(V)

Table 7: Comparative Analysis of Cash Flow of Myer Holding and Kathmandu Holding

(Amount in $000)

Particular Myer Kathmandu

Operating Cash Inflow 149278.00 67273.00

Investing Cash Outflow -109456.00 -13275.00

Financing Cash Outflow -54438.00 -57382.00

Net Decrease in Cash Held -14,616 -3,384

It can be evaluated by the comparative analysis of both the companies for that the Myer

Holdings Ltd has made a higher investment in comparison to Kathmandu Holding. The same

represents that Myer Holding has stronger asset and equity position. Due to the same reason

net decrease in cash held is higher for Myer Holding in comparison to Kathmandu Holding.

The enhanced operating cash inflow of Myer Holding represent that company is running its

operating activities on a wide scale comparatively.

OTHER COMPREHENSIVE INCOME STATEMENT

(VI)

The items which are included by Myer Holdings Ltd in the other comprehensive income

statement are cash flow hedges and exchange differences on translation of foreign reserves.

Further, the amounts recognized in the profit and loss statement when the related hedged

transaction influences profit or loss (Myer Holdings Ltd Annual Report 2017).

made in the year 2016 (Kathmandu Holdings Ltd Annual Report 2017).

(V)

Table 7: Comparative Analysis of Cash Flow of Myer Holding and Kathmandu Holding

(Amount in $000)

Particular Myer Kathmandu

Operating Cash Inflow 149278.00 67273.00

Investing Cash Outflow -109456.00 -13275.00

Financing Cash Outflow -54438.00 -57382.00

Net Decrease in Cash Held -14,616 -3,384

It can be evaluated by the comparative analysis of both the companies for that the Myer

Holdings Ltd has made a higher investment in comparison to Kathmandu Holding. The same

represents that Myer Holding has stronger asset and equity position. Due to the same reason

net decrease in cash held is higher for Myer Holding in comparison to Kathmandu Holding.

The enhanced operating cash inflow of Myer Holding represent that company is running its

operating activities on a wide scale comparatively.

OTHER COMPREHENSIVE INCOME STATEMENT

(VI)

The items which are included by Myer Holdings Ltd in the other comprehensive income

statement are cash flow hedges and exchange differences on translation of foreign reserves.

Further, the amounts recognized in the profit and loss statement when the related hedged

transaction influences profit or loss (Myer Holdings Ltd Annual Report 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

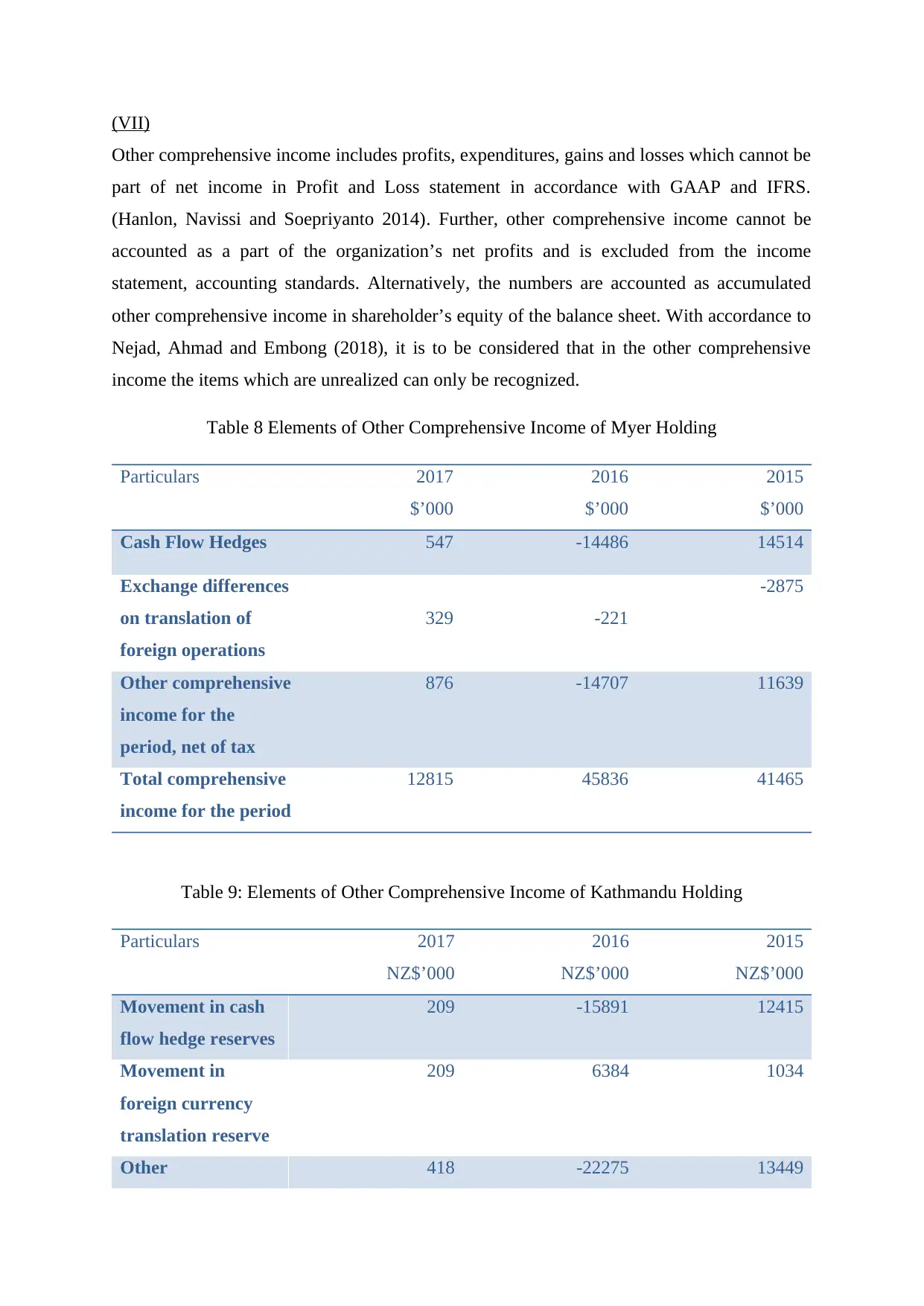

(VII)

Other comprehensive income includes profits, expenditures, gains and losses which cannot be

part of net income in Profit and Loss statement in accordance with GAAP and IFRS.

(Hanlon, Navissi and Soepriyanto 2014). Further, other comprehensive income cannot be

accounted as a part of the organization’s net profits and is excluded from the income

statement, accounting standards. Alternatively, the numbers are accounted as accumulated

other comprehensive income in shareholder’s equity of the balance sheet. With accordance to

Nejad, Ahmad and Embong (2018), it is to be considered that in the other comprehensive

income the items which are unrealized can only be recognized.

Table 8 Elements of Other Comprehensive Income of Myer Holding

Particulars 2017

$’000

2016

$’000

2015

$’000

Cash Flow Hedges 547 -14486 14514

Exchange differences

on translation of

foreign operations

329 -221

-2875

Other comprehensive

income for the

period, net of tax

876 -14707 11639

Total comprehensive

income for the period

12815 45836 41465

Table 9: Elements of Other Comprehensive Income of Kathmandu Holding

Particulars 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Movement in cash

flow hedge reserves

209 -15891 12415

Movement in

foreign currency

translation reserve

209 6384 1034

Other 418 -22275 13449

Other comprehensive income includes profits, expenditures, gains and losses which cannot be

part of net income in Profit and Loss statement in accordance with GAAP and IFRS.

(Hanlon, Navissi and Soepriyanto 2014). Further, other comprehensive income cannot be

accounted as a part of the organization’s net profits and is excluded from the income

statement, accounting standards. Alternatively, the numbers are accounted as accumulated

other comprehensive income in shareholder’s equity of the balance sheet. With accordance to

Nejad, Ahmad and Embong (2018), it is to be considered that in the other comprehensive

income the items which are unrealized can only be recognized.

Table 8 Elements of Other Comprehensive Income of Myer Holding

Particulars 2017

$’000

2016

$’000

2015

$’000

Cash Flow Hedges 547 -14486 14514

Exchange differences

on translation of

foreign operations

329 -221

-2875

Other comprehensive

income for the

period, net of tax

876 -14707 11639

Total comprehensive

income for the period

12815 45836 41465

Table 9: Elements of Other Comprehensive Income of Kathmandu Holding

Particulars 2017

NZ$’000

2016

NZ$’000

2015

NZ$’000

Movement in cash

flow hedge reserves

209 -15891 12415

Movement in

foreign currency

translation reserve

209 6384 1034

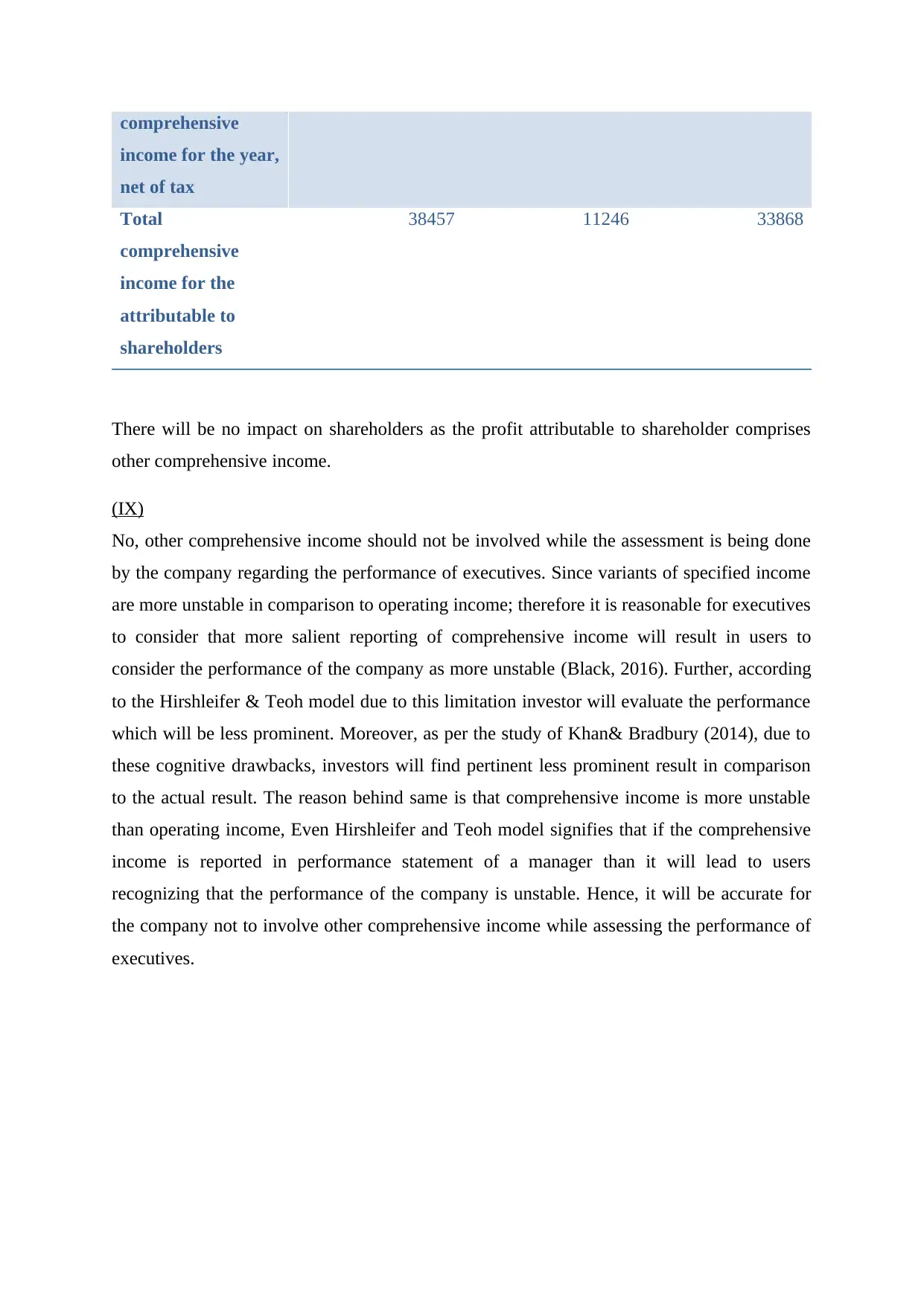

Other 418 -22275 13449

comprehensive

income for the year,

net of tax

Total

comprehensive

income for the

attributable to

shareholders

38457 11246 33868

There will be no impact on shareholders as the profit attributable to shareholder comprises

other comprehensive income.

(IX)

No, other comprehensive income should not be involved while the assessment is being done

by the company regarding the performance of executives. Since variants of specified income

are more unstable in comparison to operating income; therefore it is reasonable for executives

to consider that more salient reporting of comprehensive income will result in users to

consider the performance of the company as more unstable (Black, 2016). Further, according

to the Hirshleifer & Teoh model due to this limitation investor will evaluate the performance

which will be less prominent. Moreover, as per the study of Khan& Bradbury (2014), due to

these cognitive drawbacks, investors will find pertinent less prominent result in comparison

to the actual result. The reason behind same is that comprehensive income is more unstable

than operating income, Even Hirshleifer and Teoh model signifies that if the comprehensive

income is reported in performance statement of a manager than it will lead to users

recognizing that the performance of the company is unstable. Hence, it will be accurate for

the company not to involve other comprehensive income while assessing the performance of

executives.

income for the year,

net of tax

Total

comprehensive

income for the

attributable to

shareholders

38457 11246 33868

There will be no impact on shareholders as the profit attributable to shareholder comprises

other comprehensive income.

(IX)

No, other comprehensive income should not be involved while the assessment is being done

by the company regarding the performance of executives. Since variants of specified income

are more unstable in comparison to operating income; therefore it is reasonable for executives

to consider that more salient reporting of comprehensive income will result in users to

consider the performance of the company as more unstable (Black, 2016). Further, according

to the Hirshleifer & Teoh model due to this limitation investor will evaluate the performance

which will be less prominent. Moreover, as per the study of Khan& Bradbury (2014), due to

these cognitive drawbacks, investors will find pertinent less prominent result in comparison

to the actual result. The reason behind same is that comprehensive income is more unstable

than operating income, Even Hirshleifer and Teoh model signifies that if the comprehensive

income is reported in performance statement of a manager than it will lead to users

recognizing that the performance of the company is unstable. Hence, it will be accurate for

the company not to involve other comprehensive income while assessing the performance of

executives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.