HI5020 Corporate Accounting: Financial Analysis of IPH Limited

VerifiedAdded on 2024/05/31

|12

|2730

|405

Report

AI Summary

This report provides a comprehensive analysis of IPH Limited's financial statements, focusing on cash flow statements, other comprehensive income, and accounting for corporate income tax. It examines changes in cash flow items over the past year, provides a comparative analysis of operating, investing, and financing activities over three years, and explains the items reported in the other comprehensive income statement. The report also delves into the company's tax expense, deferred tax assets and liabilities, and the differences between income tax expense and income tax paid. It also provides a detailed explanation of deferred tax assets and liabilities reported on the balance sheet and the reasons for their recording, highlighting interesting and confusing aspects of the company's tax treatment. The analysis aims to provide insights into how companies account for income tax, offering a detailed understanding of IPH Limited's financial practices.

Hi5020 Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:........................................................................................................................4

CASH FLOWS STATEMENT:..............................................................................................5

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and writes your understanding of each item. Discuss any changes in each item

of CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for

the change........................................................................................................................5

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years...................................................................................................6

OTHER COMPREHENSIVE INCOME STATEMENT:..........................................................7

(iii) What items have been reported in the other comprehensive income statement?................7

(iv) Explain your understanding of each item reported in the other comprehensive income

statement:.........................................................................................................................7

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.. 7

ACCOUNTING FOR CORPORATE INCOME TAX:.............................................................8

(vi) What is your firm’s tax expense in its latest financial statements?...................................8

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.............................................................8

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded..............................................8

Introduction:........................................................................................................................4

CASH FLOWS STATEMENT:..............................................................................................5

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and writes your understanding of each item. Discuss any changes in each item

of CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for

the change........................................................................................................................5

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative

evaluation for three years...................................................................................................6

OTHER COMPREHENSIVE INCOME STATEMENT:..........................................................7

(iii) What items have been reported in the other comprehensive income statement?................7

(iv) Explain your understanding of each item reported in the other comprehensive income

statement:.........................................................................................................................7

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.. 7

ACCOUNTING FOR CORPORATE INCOME TAX:.............................................................8

(vi) What is your firm’s tax expense in its latest financial statements?...................................8

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.............................................................8

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded..............................................8

(ix) Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?...............................................9

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..........................................10

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?..................................................................................................10

Conclusion:........................................................................................................................11

References:........................................................................................................................12

the income tax payable not the same as income tax expense?...............................................9

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..........................................10

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?..................................................................................................10

Conclusion:........................................................................................................................11

References:........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

In this report, proper analysis will be done through comparative and corporative analysis in the

management of IPH Limited. This reading will explain about management and corporate income

tax and its method of accounting in the business. It will also explain the significance of corporate

income tax management and way to manage income tax such as deferred and current tax in order

to measure accuracy and efficacy of corporate income and income tax expense. It will describe

the way how to manage comprehensive income statement and differences and reason to manage

those items which are not recognised in original profit and loss statement of the IPH limited.

In this report, proper analysis will be done through comparative and corporative analysis in the

management of IPH Limited. This reading will explain about management and corporate income

tax and its method of accounting in the business. It will also explain the significance of corporate

income tax management and way to manage income tax such as deferred and current tax in order

to measure accuracy and efficacy of corporate income and income tax expense. It will describe

the way how to manage comprehensive income statement and differences and reason to manage

those items which are not recognised in original profit and loss statement of the IPH limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASH FLOWS STATEMENT:

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and writes your understanding of each item. Discuss any changes in each item of

CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for the

change.

Cash flow statements are made by any company to figure out three major activities related to

business activity these activities are an investment, operation and financial activities. IPH

Limited is the industrial company which needs to adopt cash flow statement to understand

changes and behaviour and to observe cash requirements in the form of investment, operation

and financial acts. In the financial statement of IPH Limited cash from generation has been

classified into three major parts first is operation activities, second would be investing activities

and third is financial activities:

1. Operational activities: operational activities contains those expense and receipts related to

operational activities of the business such as receipts from customers, payment to suppliers and

associates, interest received and income tax paid which has been increased in last three years.

Total cash flow from operating activity was 49,922 in FY17 (IPH limited 2017)

2. Financial activities: Cash flow from financing activities contains major activities such as

proceed from shares and debentures and payment of dividend and repayment of borrowings. All

items were nil or equal to zero in 2017 except dividend paid to shareholders which were 40,407

negative in 2017. Total net cash used from financing activities was (40407) with was reduced as

used cash flow from 2016.

3. Investing activities: net cash flow from investing activities includes payment related to

purchasing properties, plants and developed software as per investment conditions. Payment for

purchase of subsidiaries, new properties, plants and internally developed equipment’s are

included as investment items to disclose and analyse comparatively through investment

activities, cash flow generation from investing activity around 42,377 in 2017 (NCERT, 2014).

(i) From your firm’s financial statement, list each item reported in the CASH FLOWS

STATEMENT and writes your understanding of each item. Discuss any changes in each item of

CASH FLOWS STATEMENT for your firm over the past year articulating the reasons for the

change.

Cash flow statements are made by any company to figure out three major activities related to

business activity these activities are an investment, operation and financial activities. IPH

Limited is the industrial company which needs to adopt cash flow statement to understand

changes and behaviour and to observe cash requirements in the form of investment, operation

and financial acts. In the financial statement of IPH Limited cash from generation has been

classified into three major parts first is operation activities, second would be investing activities

and third is financial activities:

1. Operational activities: operational activities contains those expense and receipts related to

operational activities of the business such as receipts from customers, payment to suppliers and

associates, interest received and income tax paid which has been increased in last three years.

Total cash flow from operating activity was 49,922 in FY17 (IPH limited 2017)

2. Financial activities: Cash flow from financing activities contains major activities such as

proceed from shares and debentures and payment of dividend and repayment of borrowings. All

items were nil or equal to zero in 2017 except dividend paid to shareholders which were 40,407

negative in 2017. Total net cash used from financing activities was (40407) with was reduced as

used cash flow from 2016.

3. Investing activities: net cash flow from investing activities includes payment related to

purchasing properties, plants and developed software as per investment conditions. Payment for

purchase of subsidiaries, new properties, plants and internally developed equipment’s are

included as investment items to disclose and analyse comparatively through investment

activities, cash flow generation from investing activity around 42,377 in 2017 (NCERT, 2014).

(ii) Provide a comparative analysis of your company’s three broad categories of cash flows

(operating activities, investing activities, financing activities) and make a comparative evaluation

for three years.

Comparative evaluation of three years of IPH limited:

1. Operating activity: cash flow behaviour and changes through operational activities contains

following items such as receipts from customers, payment to suppliers and employees and

interest received etc. such items creates fluctuations in cash flow generation from operating

activities. In 2017 company has received less interest than last two years of 2015 and 2016.

Payment to suppliers has been increased in 2017 than 2016 and 2015 which was 206,480 in 2017

and 151,164 in 2016. Total net cash flow from net cash flow operating activity contains 49,933

and 42,055 in 2017 and 2016.

2. Investing activity: in the financial year of 2017 company has paid total dividend around

40,207 which was equal to net cash used for investment activity. The company has made total

proceed from shares and debentures around 108,454 (IPH limited 2016).

3. Financial activity: total cash and cash equivalent around 32,872 and 53,307 which was

negative in 2017 and 2016 through financing activities. Cash at the beginning was 58,761 in

2017 which was reduced in the comparison of 2016 and 2015

(operating activities, investing activities, financing activities) and make a comparative evaluation

for three years.

Comparative evaluation of three years of IPH limited:

1. Operating activity: cash flow behaviour and changes through operational activities contains

following items such as receipts from customers, payment to suppliers and employees and

interest received etc. such items creates fluctuations in cash flow generation from operating

activities. In 2017 company has received less interest than last two years of 2015 and 2016.

Payment to suppliers has been increased in 2017 than 2016 and 2015 which was 206,480 in 2017

and 151,164 in 2016. Total net cash flow from net cash flow operating activity contains 49,933

and 42,055 in 2017 and 2016.

2. Investing activity: in the financial year of 2017 company has paid total dividend around

40,207 which was equal to net cash used for investment activity. The company has made total

proceed from shares and debentures around 108,454 (IPH limited 2016).

3. Financial activity: total cash and cash equivalent around 32,872 and 53,307 which was

negative in 2017 and 2016 through financing activities. Cash at the beginning was 58,761 in

2017 which was reduced in the comparison of 2016 and 2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

OTHER COMPREHENSIVE INCOME STATEMENT:

(iii) What items have been reported in the other comprehensive income statement?

In the other comprehensive income statement of IPH Limited Company contains those items

which are related to subsequently realise into two parts expense and revenue from the operating

activities of IPH limited. Comprehensive income is the addition of net income which has not

been realised including those items which unrealisable holding gains and revenues such as items

available for sale security and foreign currency such items are not included in the original profit

and loss accounts of the company and adjusted in the comprehensive income to figure

comprehensive picture of the IPH Limited.

(iv) Explain your understanding of each item reported in the other comprehensive income

statement:

Items which are involved in comprehensive income statement but excluded from original profit

and loss accounts are taken as those items which are subsequently reclassified to the profit and

loss, foreign currency transactions and other comprehensive income items of the year including

net tax. The total net comprehensive income for the year was 39,848 and 30,632 in 2016 of the

financial year of the company. In the financial year of 2017, the total net comprehensive income

for the year is attributable to two parts first would be the non-controlling interest which was nil

in 2017 and owners’ equity of IPH Limited equal to 39,348 (Illustrative IFRS consolidated

financial statements, 2015).

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.

These all items are recorded in the income statement to measure relevancy and efficacy of such

items in the market. These items are reported in the comprehensive income statement to

recognise specific varieties of income statement especially to measure shareholder equity and

actual situation of the net worth of the company (Tweedie, 2011).

(iii) What items have been reported in the other comprehensive income statement?

In the other comprehensive income statement of IPH Limited Company contains those items

which are related to subsequently realise into two parts expense and revenue from the operating

activities of IPH limited. Comprehensive income is the addition of net income which has not

been realised including those items which unrealisable holding gains and revenues such as items

available for sale security and foreign currency such items are not included in the original profit

and loss accounts of the company and adjusted in the comprehensive income to figure

comprehensive picture of the IPH Limited.

(iv) Explain your understanding of each item reported in the other comprehensive income

statement:

Items which are involved in comprehensive income statement but excluded from original profit

and loss accounts are taken as those items which are subsequently reclassified to the profit and

loss, foreign currency transactions and other comprehensive income items of the year including

net tax. The total net comprehensive income for the year was 39,848 and 30,632 in 2016 of the

financial year of the company. In the financial year of 2017, the total net comprehensive income

for the year is attributable to two parts first would be the non-controlling interest which was nil

in 2017 and owners’ equity of IPH Limited equal to 39,348 (Illustrative IFRS consolidated

financial statements, 2015).

(v) Why these items have not been reported in Income Statement/Profit and Loss Statement.

These all items are recorded in the income statement to measure relevancy and efficacy of such

items in the market. These items are reported in the comprehensive income statement to

recognise specific varieties of income statement especially to measure shareholder equity and

actual situation of the net worth of the company (Tweedie, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR CORPORATE INCOME TAX:

(vi) What is your firm’s tax expense in its latest financial statements?

In the current income tax expense in the latest financial statement of the company would be

14,308 and profit after income tax expense would be 42,893.

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

As per company’s provision an act of income tax assessment act 1997, this figure as similar to

company’s corporate tax times financial firms accounting income. The major benefit of such tax

payable on the current period tax payable and recoverable in respect of national income tax rate

for proper justification of each current tax and deferred tax rates and their assets and liabilities to

define attributable differences between assets and liabilities. Income tax expense is segregated

into two parts first would be current tax 16,565 and other would be deferred tax 2984 as a loss in

the financial year of 2017 (Rafay and Ajmal, 2014).

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

Deferred tax is included in the income tax expense which comprises as the increment in deferred

tax assets around 2062 and decrease in deferred tax liabilities around 985 mentioned in the latest

income tax expense statement.

(vi) What is your firm’s tax expense in its latest financial statements?

In the current income tax expense in the latest financial statement of the company would be

14,308 and profit after income tax expense would be 42,893.

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

As per company’s provision an act of income tax assessment act 1997, this figure as similar to

company’s corporate tax times financial firms accounting income. The major benefit of such tax

payable on the current period tax payable and recoverable in respect of national income tax rate

for proper justification of each current tax and deferred tax rates and their assets and liabilities to

define attributable differences between assets and liabilities. Income tax expense is segregated

into two parts first would be current tax 16,565 and other would be deferred tax 2984 as a loss in

the financial year of 2017 (Rafay and Ajmal, 2014).

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

Deferred tax is included in the income tax expense which comprises as the increment in deferred

tax assets around 2062 and decrease in deferred tax liabilities around 985 mentioned in the latest

income tax expense statement.

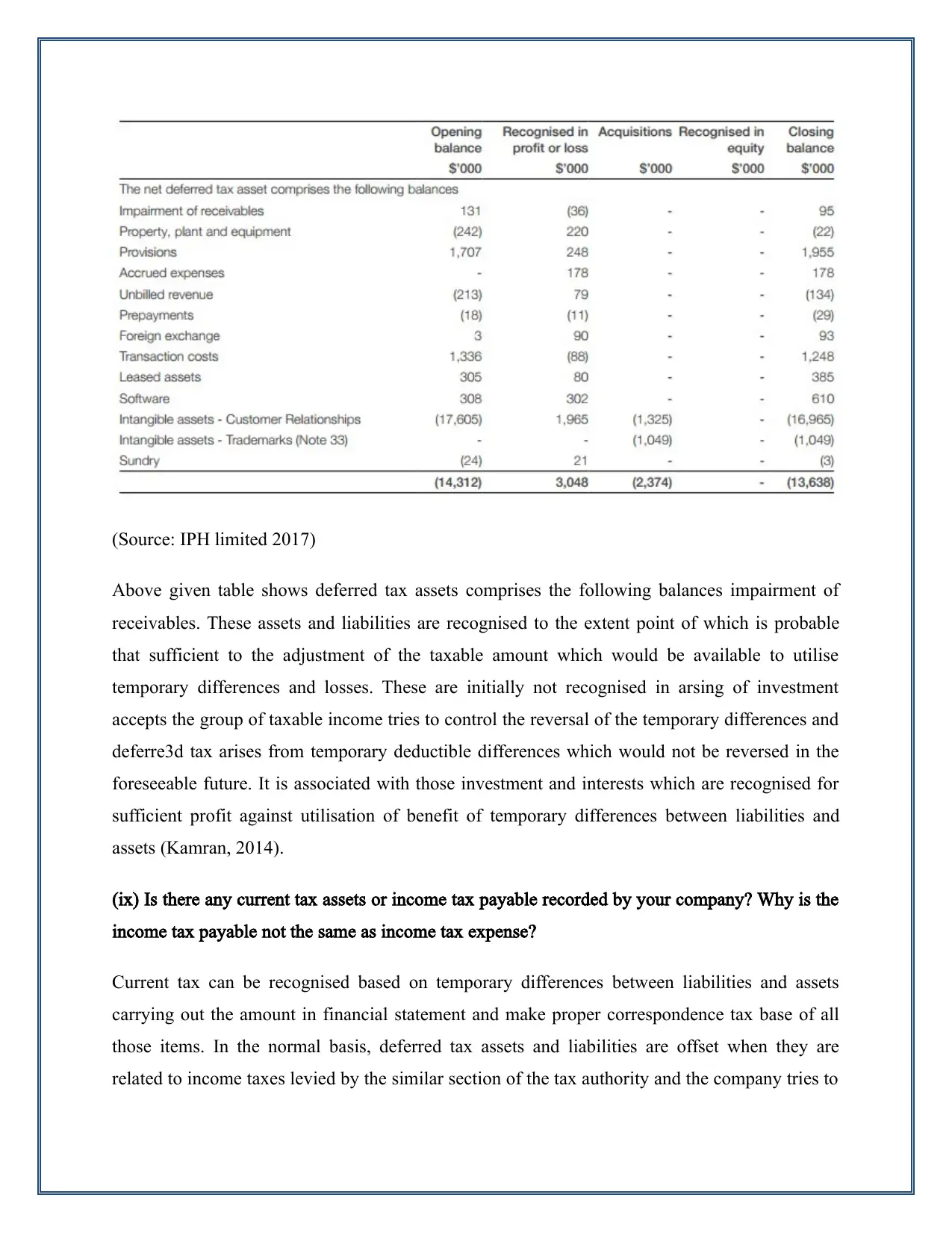

(Source: IPH limited 2017)

Above given table shows deferred tax assets comprises the following balances impairment of

receivables. These assets and liabilities are recognised to the extent point of which is probable

that sufficient to the adjustment of the taxable amount which would be available to utilise

temporary differences and losses. These are initially not recognised in arsing of investment

accepts the group of taxable income tries to control the reversal of the temporary differences and

deferre3d tax arises from temporary deductible differences which would not be reversed in the

foreseeable future. It is associated with those investment and interests which are recognised for

sufficient profit against utilisation of benefit of temporary differences between liabilities and

assets (Kamran, 2014).

(ix) Is there any current tax assets or income tax payable recorded by your company? Why is the

income tax payable not the same as income tax expense?

Current tax can be recognised based on temporary differences between liabilities and assets

carrying out the amount in financial statement and make proper correspondence tax base of all

those items. In the normal basis, deferred tax assets and liabilities are offset when they are

related to income taxes levied by the similar section of the tax authority and the company tries to

Above given table shows deferred tax assets comprises the following balances impairment of

receivables. These assets and liabilities are recognised to the extent point of which is probable

that sufficient to the adjustment of the taxable amount which would be available to utilise

temporary differences and losses. These are initially not recognised in arsing of investment

accepts the group of taxable income tries to control the reversal of the temporary differences and

deferre3d tax arises from temporary deductible differences which would not be reversed in the

foreseeable future. It is associated with those investment and interests which are recognised for

sufficient profit against utilisation of benefit of temporary differences between liabilities and

assets (Kamran, 2014).

(ix) Is there any current tax assets or income tax payable recorded by your company? Why is the

income tax payable not the same as income tax expense?

Current tax can be recognised based on temporary differences between liabilities and assets

carrying out the amount in financial statement and make proper correspondence tax base of all

those items. In the normal basis, deferred tax assets and liabilities are offset when they are

related to income taxes levied by the similar section of the tax authority and the company tries to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

settle current tax asset on such net basis. Total current tax assets are given as income tax expense

around 16,845 in the financial statement of the IPH limited company (Taxadda, 2017).

(x) Is the income tax expense shown in the income statement same as the income tax paid shown

in the cash flow statement? If not why is the difference?

No, such expense shown in the financial statement is not same as given in the cash flow

statement. In the income tax statement, it has been mentioned around 14,308 in the income

statement which is totally different from the amount mentioned in the cash flow statement. It is

around 17.671 in negative. Such differences are raised to temporary differences between income

tax assets and liabilities whether it would be current tax asset or liabilities. Such adjustment is

made with the national income tax rates to all financial jurisdiction arranged by differences

occurred between asset and liabilities through carrying the amount of financial statement

(Merritt, 2015).

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you gained

about how companies account for income tax as a result of examining your firm’s tax expense in

its accounts?

Through above analysis, it has been observed that this report has been very difficult and quite

interesting to understand and recognise the way to treat the taxation and financial allocation of

resources in the IHP limited. The company has made a flexible and effective adjustment related

to cash flow changes ad fluctuation in the balance sheet. After this point, the overall analysis was

made, related to the proper arrangement of operational and financial activities to measure cash

flow activity. Another point which was hardly identified was differences to record income tax

expense recorded in the income statement and in cash flow statement as income tax payable. The

accuracy of cash flow changes has been made perfectly by observing the nature cash inflows and

outflows through the management. The company has made the proper realisation of deferred tax

rates and current tax rates by analysing temporary differences between assets and liabilities

according to the profit and loss account of the company (Rafay and Ajmal, 2014).

around 16,845 in the financial statement of the IPH limited company (Taxadda, 2017).

(x) Is the income tax expense shown in the income statement same as the income tax paid shown

in the cash flow statement? If not why is the difference?

No, such expense shown in the financial statement is not same as given in the cash flow

statement. In the income tax statement, it has been mentioned around 14,308 in the income

statement which is totally different from the amount mentioned in the cash flow statement. It is

around 17.671 in negative. Such differences are raised to temporary differences between income

tax assets and liabilities whether it would be current tax asset or liabilities. Such adjustment is

made with the national income tax rates to all financial jurisdiction arranged by differences

occurred between asset and liabilities through carrying the amount of financial statement

(Merritt, 2015).

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you gained

about how companies account for income tax as a result of examining your firm’s tax expense in

its accounts?

Through above analysis, it has been observed that this report has been very difficult and quite

interesting to understand and recognise the way to treat the taxation and financial allocation of

resources in the IHP limited. The company has made a flexible and effective adjustment related

to cash flow changes ad fluctuation in the balance sheet. After this point, the overall analysis was

made, related to the proper arrangement of operational and financial activities to measure cash

flow activity. Another point which was hardly identified was differences to record income tax

expense recorded in the income statement and in cash flow statement as income tax payable. The

accuracy of cash flow changes has been made perfectly by observing the nature cash inflows and

outflows through the management. The company has made the proper realisation of deferred tax

rates and current tax rates by analysing temporary differences between assets and liabilities

according to the profit and loss account of the company (Rafay and Ajmal, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion:

This report has been made to describe management and corporate accounting within the

company. Overall analysis has been revolved around management and accounting formation of

IPH Limited which indicated how the company has managed its accounting income tax expense

and the relevant way to manage income tax expense, it has defined the reason of temporary

differences between assets and liabilities of deferred tax and current tax. This report has been

classified into three parts. The first part was related to the management of cash flow statement, in

which all classified operating and investing activities have been with the three years of

comparison between financial cash flow statements of IPH limited. This ready also has been

including the discussion of corporate income tax and comprehensive income statement for the

proper corporate management of the company.

This report has been made to describe management and corporate accounting within the

company. Overall analysis has been revolved around management and accounting formation of

IPH Limited which indicated how the company has managed its accounting income tax expense

and the relevant way to manage income tax expense, it has defined the reason of temporary

differences between assets and liabilities of deferred tax and current tax. This report has been

classified into three parts. The first part was related to the management of cash flow statement, in

which all classified operating and investing activities have been with the three years of

comparison between financial cash flow statements of IPH limited. This ready also has been

including the discussion of corporate income tax and comprehensive income statement for the

proper corporate management of the company.

References:

1. .Illustrative IFRS consolidated financial statements, 2015. Introduction.

PricewaterhouseCoopers

LL.

2. Kamran, A., (2014). Explain the reason for the creation of deferred tax asset and liability?

[Online] Bayt.com. Available at: https://www.bayt.com/en/specialties/q/80018/explain-the-

reason-of-creation-of-deferred-tax-asset-and-liability/ [Accessed on: 15 May 2018].

3. Merritt, C., (2015). Tax Payable vs. Deferred Income Tax Liability. [Online] Chron.com.

Available at: http://smallbusiness.chron.com/tax-payable-vs-deferred-income-tax-liability-

48704.html [Accessed on: 15 May 2018].

4. NCERT, (2014). Cash Flow Statement.

NCERT Publication.

5. Rafay, A. and Ajmal, M., (2014). Earnings Management Through Deferred Taxes Recognized

Under IAS 12: Evidence From Pakistan.

The Lahore Journal of Business. pp. 1–19.

6. Taxadda, (2017). What is deferred tax asset and deferred tax liability (DTA & DTL). [Online]Taxadda.com. Available at: http://taxadda.com/deferred-tax-asset-deferred-tax-liability-dta-dtl/

[Accessed on: 15 May 2018].

7. Tweedie, D., (2011). Measuring Assets and Liabilities Investment Professionals’ Views.PricewaterhouseCoopers LL.

8. IPH limited 2017. Annual Report, 2017.

IPH Limited.

9. IPH limited 2016. Annual Report, 2016.

IPH Limited.

1. .Illustrative IFRS consolidated financial statements, 2015. Introduction.

PricewaterhouseCoopers

LL.

2. Kamran, A., (2014). Explain the reason for the creation of deferred tax asset and liability?

[Online] Bayt.com. Available at: https://www.bayt.com/en/specialties/q/80018/explain-the-

reason-of-creation-of-deferred-tax-asset-and-liability/ [Accessed on: 15 May 2018].

3. Merritt, C., (2015). Tax Payable vs. Deferred Income Tax Liability. [Online] Chron.com.

Available at: http://smallbusiness.chron.com/tax-payable-vs-deferred-income-tax-liability-

48704.html [Accessed on: 15 May 2018].

4. NCERT, (2014). Cash Flow Statement.

NCERT Publication.

5. Rafay, A. and Ajmal, M., (2014). Earnings Management Through Deferred Taxes Recognized

Under IAS 12: Evidence From Pakistan.

The Lahore Journal of Business. pp. 1–19.

6. Taxadda, (2017). What is deferred tax asset and deferred tax liability (DTA & DTL). [Online]Taxadda.com. Available at: http://taxadda.com/deferred-tax-asset-deferred-tax-liability-dta-dtl/

[Accessed on: 15 May 2018].

7. Tweedie, D., (2011). Measuring Assets and Liabilities Investment Professionals’ Views.PricewaterhouseCoopers LL.

8. IPH limited 2017. Annual Report, 2017.

IPH Limited.

9. IPH limited 2016. Annual Report, 2016.

IPH Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.