HI5020 Corporate Accounting: Financial Analysis of CSR Limited

VerifiedAdded on 2023/06/12

|13

|2914

|163

Report

AI Summary

This report provides a detailed financial analysis of CSR Limited, focusing on their cash flow statements, income tax expenses, and overall financial health based on their annual reports from 2015 to 2017. The analysis includes a breakdown of cash flows from operating, investing, and financing activities, highlighting key changes and trends over the years. It also examines the items reported under the Other Comprehensive Income Statement, explaining why these items are not included in the Profit and Loss Statement. Furthermore, the report verifies the company's income tax expense, deferred tax assets and liabilities, and reconciles the income tax expense shown in the income statement with the income tax paid in the cash flow statement. The analysis concludes that CSR Limited has followed the requirements of the Australian Tax Office (ATO) while estimating different taxes that has been included in the financial statement of the company. Desklib provides access to similar solved assignments and past papers for students.

Running head:CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE ACCOUNTING

Table of Contents

Changes in each item of cash flows statement for the firm over the past year along with the

reasons for the change................................................................................................................3

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................5

Items of Other Comprehensive Income Statement....................................................................6

Reasons for the items have not been reported in Income Statement/Profit and Loss Statement

....................................................................................................................................................7

Clear description of your firm’s income tax expense................................................................8

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income.....................................................................................................................8

Deferred tax that is reported in the balance sheet along with the reasons for the record...........9

Current tax assets or income tax payable recorded by the company.........................................9

Verification of the income tax expense shown in the income statement same as the income

tax paid shown in the cash flow statement...............................................................................10

Unique characteristics in the financial statements, new insights, and other information........10

Appendix..................................................................................................................................12

Table of Contents

Changes in each item of cash flows statement for the firm over the past year along with the

reasons for the change................................................................................................................3

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................5

Items of Other Comprehensive Income Statement....................................................................6

Reasons for the items have not been reported in Income Statement/Profit and Loss Statement

....................................................................................................................................................7

Clear description of your firm’s income tax expense................................................................8

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income.....................................................................................................................8

Deferred tax that is reported in the balance sheet along with the reasons for the record...........9

Current tax assets or income tax payable recorded by the company.........................................9

Verification of the income tax expense shown in the income statement same as the income

tax paid shown in the cash flow statement...............................................................................10

Unique characteristics in the financial statements, new insights, and other information........10

Appendix..................................................................................................................................12

3CORPORATE ACCOUNTING

Changes in each item of cash flows statement for the firm over the past year along with

the reasons for the change

By evaluating the cash flow statements of the business organisations, it becomes

easier to gain an understanding of their inflows as well as outflows(Siew 2015). For this

paper, CSR Limited is chosen and each item of its cash flow statement is analysed critically

as follows:

Cash flows from operations:

The cash flow statement mainly consist of three sections that involves cash flow from

investing activities, operating activities, financing activities and net cash as well as cash

equivalents. The items that are included in the operating activities involves depreciation,

adjustments to net income, liabilities changes, inventory changes, changes in accounts

receivable and changes in other operating activities (Sierra‐García, Zorio‐Grima and García‐

Benau 2015). It has been seen that the total cash flow of operating activities has increased in

the year 2017 to $264800 from the year 2016 and 2015.

Cash flows from investing activities:

The items that are included in the investment activities are capital expenses,

investments and other cash flow from investment activities. It is evident that the total cash

used for the investment activities decreased in the year 2016 to -$80800 from $ -45400 in the

year 2015 and then decreased to $ -60700 in the year 2017.

Cash flows from financing activities:

In this cash flow statement of CSR limited, financing activities mainly consists of the

paid dividends, net borrowings, purchase as well as sale of stocks and other cash flows from

Changes in each item of cash flows statement for the firm over the past year along with

the reasons for the change

By evaluating the cash flow statements of the business organisations, it becomes

easier to gain an understanding of their inflows as well as outflows(Siew 2015). For this

paper, CSR Limited is chosen and each item of its cash flow statement is analysed critically

as follows:

Cash flows from operations:

The cash flow statement mainly consist of three sections that involves cash flow from

investing activities, operating activities, financing activities and net cash as well as cash

equivalents. The items that are included in the operating activities involves depreciation,

adjustments to net income, liabilities changes, inventory changes, changes in accounts

receivable and changes in other operating activities (Sierra‐García, Zorio‐Grima and García‐

Benau 2015). It has been seen that the total cash flow of operating activities has increased in

the year 2017 to $264800 from the year 2016 and 2015.

Cash flows from investing activities:

The items that are included in the investment activities are capital expenses,

investments and other cash flow from investment activities. It is evident that the total cash

used for the investment activities decreased in the year 2016 to -$80800 from $ -45400 in the

year 2015 and then decreased to $ -60700 in the year 2017.

Cash flows from financing activities:

In this cash flow statement of CSR limited, financing activities mainly consists of the

paid dividends, net borrowings, purchase as well as sale of stocks and other cash flows from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CORPORATE ACCOUNTING

the financing activities. There has been rise in total cash used in the financing activities in the

year 2017 to $-257900 from the year 2016 and 2015.

Moreover, the change in cash and cash equivalents amounts to -$ 54000 in the year

2017, $4700 in the year 2016 and $4700 in the year 2015.

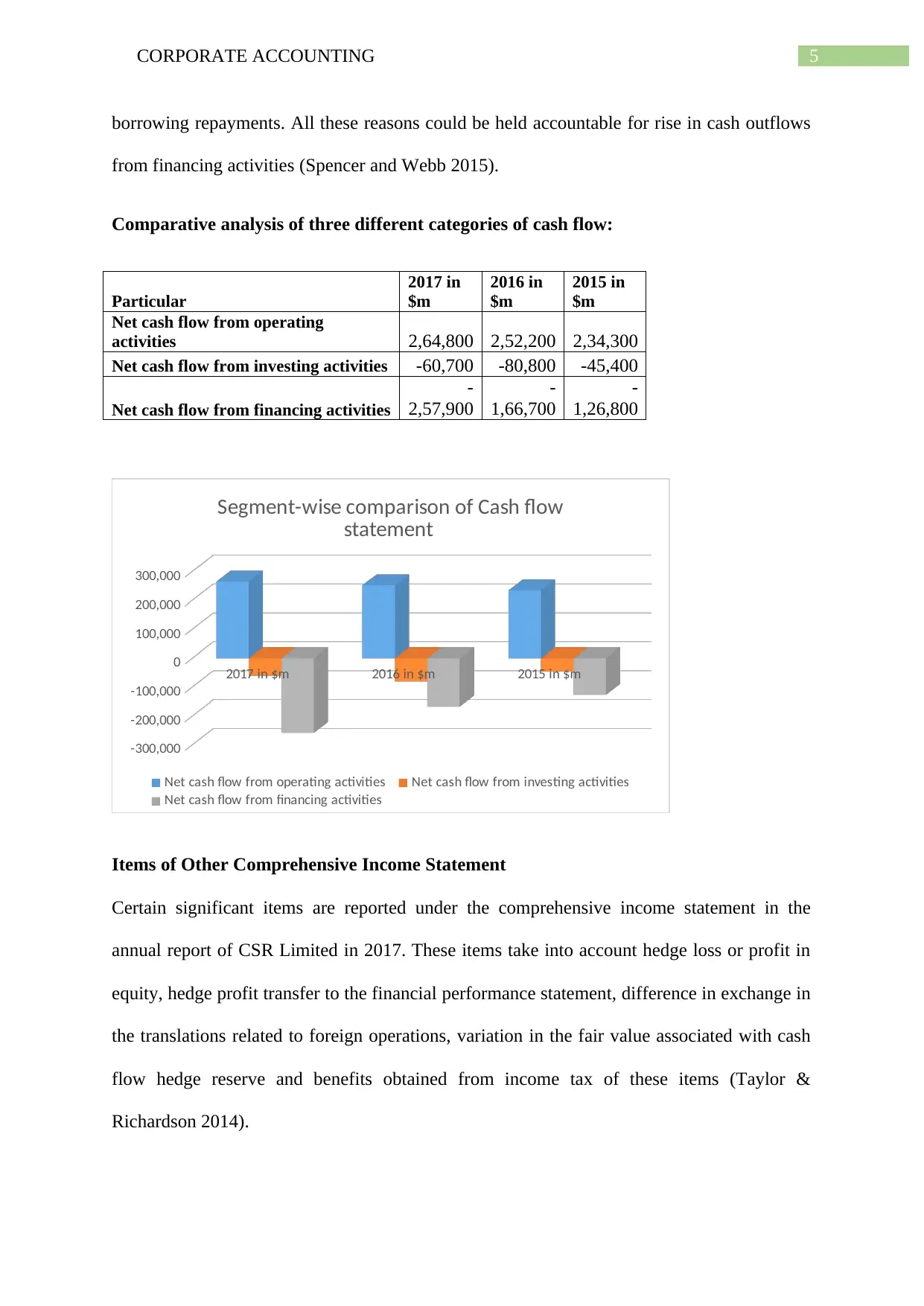

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

In order to carry out the comparative analysis of the cash flow statement of CSR

Limited in 2017, the following figure is represented:

The above figure denotes continual rise in cash flows from operating activities in the

context of CSR Limited from $ 234300 in 2015 to $ 252200 million in 2016 and to $

2648000 million in 2017. The primary cause for rise in this section is the increase in amounts

from the customers. In addition to this, rise in receipt of interest and dividend could be held

accountable for this rise (Paterson 2016).

In relation to cash flows from investing activities, increase in cash outflows could be

observed in 2016 as opposed to 2015 from $45400 in 2015 to $80800 in 2016. This is

because additional investments are made in order to purchase cash and cash equivalents.

However, in 2017, decrease in cash outflows could be identified, which have been to $80800

in 2016 to -$607000 in 2017. This is because investment amounts have been reduced for

purchasing plant and equipment (Xu, Davidson and Cheong 2017).

For cash flows from financing activities, rising trend is observed in terms of outflows

from 2015 to 2017 from -$126800 in 2015 to -$166700 in 2016 and to -$257900 in 2017.

This is because additional dividend payments are made over the years coupled with the

the financing activities. There has been rise in total cash used in the financing activities in the

year 2017 to $-257900 from the year 2016 and 2015.

Moreover, the change in cash and cash equivalents amounts to -$ 54000 in the year

2017, $4700 in the year 2016 and $4700 in the year 2015.

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

In order to carry out the comparative analysis of the cash flow statement of CSR

Limited in 2017, the following figure is represented:

The above figure denotes continual rise in cash flows from operating activities in the

context of CSR Limited from $ 234300 in 2015 to $ 252200 million in 2016 and to $

2648000 million in 2017. The primary cause for rise in this section is the increase in amounts

from the customers. In addition to this, rise in receipt of interest and dividend could be held

accountable for this rise (Paterson 2016).

In relation to cash flows from investing activities, increase in cash outflows could be

observed in 2016 as opposed to 2015 from $45400 in 2015 to $80800 in 2016. This is

because additional investments are made in order to purchase cash and cash equivalents.

However, in 2017, decrease in cash outflows could be identified, which have been to $80800

in 2016 to -$607000 in 2017. This is because investment amounts have been reduced for

purchasing plant and equipment (Xu, Davidson and Cheong 2017).

For cash flows from financing activities, rising trend is observed in terms of outflows

from 2015 to 2017 from -$126800 in 2015 to -$166700 in 2016 and to -$257900 in 2017.

This is because additional dividend payments are made over the years coupled with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE ACCOUNTING

borrowing repayments. All these reasons could be held accountable for rise in cash outflows

from financing activities (Spencer and Webb 2015).

Comparative analysis of three different categories of cash flow:

Particular

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 2,64,800 2,52,200 2,34,300

Net cash flow from investing activities -60,700 -80,800 -45,400

Net cash flow from financing activities

-

2,57,900

-

1,66,700

-

1,26,800

2017 in $m 2016 in $m 2015 in $m

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

Segment-wise comparison of Cash flow

statement

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Items of Other Comprehensive Income Statement

Certain significant items are reported under the comprehensive income statement in the

annual report of CSR Limited in 2017. These items take into account hedge loss or profit in

equity, hedge profit transfer to the financial performance statement, difference in exchange in

the translations related to foreign operations, variation in the fair value associated with cash

flow hedge reserve and benefits obtained from income tax of these items (Taylor &

Richardson 2014).

borrowing repayments. All these reasons could be held accountable for rise in cash outflows

from financing activities (Spencer and Webb 2015).

Comparative analysis of three different categories of cash flow:

Particular

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 2,64,800 2,52,200 2,34,300

Net cash flow from investing activities -60,700 -80,800 -45,400

Net cash flow from financing activities

-

2,57,900

-

1,66,700

-

1,26,800

2017 in $m 2016 in $m 2015 in $m

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

Segment-wise comparison of Cash flow

statement

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Items of Other Comprehensive Income Statement

Certain significant items are reported under the comprehensive income statement in the

annual report of CSR Limited in 2017. These items take into account hedge loss or profit in

equity, hedge profit transfer to the financial performance statement, difference in exchange in

the translations related to foreign operations, variation in the fair value associated with cash

flow hedge reserve and benefits obtained from income tax of these items (Taylor &

Richardson 2014).

6CORPORATE ACCOUNTING

Reasons for the items have not been reported in Income Statement/Profit and Loss

Statement

In order to gain an in-depth understanding of the above-stated items reported in the

other comprehensive income statement of CSR Limited in 2017, the items that have been

found are foreign currency translation reservewhich is used for specific item is to convert the

outcomes of the cross-border subsidiaries of the parent organisation to the reporting currency

where financial reporting is conducted (Tschopp and Nastanski 2014). This is a significant

aspect in the consolidation procedure where the ascertainment of the cross-border currency of

the foreign subsidiary is made in the currency for conducting financial reporting process

(Jagannathan2017). The Cash flow hedge reserve helps in the exposure formed could be

minimised or removed because of the significant variations in asset and liability positions of

the corporate entities. Certain risk variations are the primary reasons behind the occurrence of

this item such as interest related to debt risk, risk related to interest rate and others (Wong and

Joshi 2015).

Clear description of the firm’s income tax expense

The basic purpose of CSR Limited in forming the other comprehensive income

statement delivers the users with the essential information in relation to the above-mentioned

aspects. Thus, this statement provides an overview of transparent and holistic approach of

such items. Such causes are not engaged directly in order to derive income (Wahlen, Baginski

& Bradshaw 2014).

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income

CSR Limited is obliged to conduct its tax accounting in accordance with the norms of

the Australian taxation law (Joubert, Garvie and Parle 2017). In the years 2016 and 2017, the

Reasons for the items have not been reported in Income Statement/Profit and Loss

Statement

In order to gain an in-depth understanding of the above-stated items reported in the

other comprehensive income statement of CSR Limited in 2017, the items that have been

found are foreign currency translation reservewhich is used for specific item is to convert the

outcomes of the cross-border subsidiaries of the parent organisation to the reporting currency

where financial reporting is conducted (Tschopp and Nastanski 2014). This is a significant

aspect in the consolidation procedure where the ascertainment of the cross-border currency of

the foreign subsidiary is made in the currency for conducting financial reporting process

(Jagannathan2017). The Cash flow hedge reserve helps in the exposure formed could be

minimised or removed because of the significant variations in asset and liability positions of

the corporate entities. Certain risk variations are the primary reasons behind the occurrence of

this item such as interest related to debt risk, risk related to interest rate and others (Wong and

Joshi 2015).

Clear description of the firm’s income tax expense

The basic purpose of CSR Limited in forming the other comprehensive income

statement delivers the users with the essential information in relation to the above-mentioned

aspects. Thus, this statement provides an overview of transparent and holistic approach of

such items. Such causes are not engaged directly in order to derive income (Wahlen, Baginski

& Bradshaw 2014).

Verification of the figure of tax being same as the company tax rate times the firm’s

accounting income

CSR Limited is obliged to conduct its tax accounting in accordance with the norms of

the Australian taxation law (Joubert, Garvie and Parle 2017). In the years 2016 and 2017, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CORPORATE ACCOUNTING

tax rate that could be applied to the organisation is 30%. Based on the statement of financial

performance in 2017, the income tax expense reported has been $61.70 million in 2017 and

$64.40 million in 2016.

Deferred tax that is reported in the balance sheet along with the reasons for the record

The Deferred tax is accounted by the method of balance sheet asset resulting from

temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements (Warren and Jones 2018). Recognition of deferred tax

liabilities are done to the extent that the availability of taxable profit in future is probable

against the temporary differences that are deductible. Deferred tax assets have been observed

to be $201.20 million in 2017, which were $239.30 million in 2016.

Current tax assets or income tax payable recorded by the company

As per the latest annual report of CSR Limited in 2017, it could be found that

adequate disclosures have been made regarding deferred tax assets and deferred tax

liabilities. Deferred tax assets have been observed to be $201.20 million in 2017, which were

$239.30 million in 2016. In 2016, deferred tax liabilities were reported to be $20.90 million,

while no such liabilities are realised in the year 2017. The Income tax expenses is the amount

that is calculated based on the standard accounting rules and on the amount of tax that is

owed by company to tax authorities (Ijiri 2018). Income tax payable is the amount that the

company owes in terms of tax based on tax code rules. Until the company makes the payment

of tax, the amount of income tax payable appears on the balance sheet section as liability.

tax rate that could be applied to the organisation is 30%. Based on the statement of financial

performance in 2017, the income tax expense reported has been $61.70 million in 2017 and

$64.40 million in 2016.

Deferred tax that is reported in the balance sheet along with the reasons for the record

The Deferred tax is accounted by the method of balance sheet asset resulting from

temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements (Warren and Jones 2018). Recognition of deferred tax

liabilities are done to the extent that the availability of taxable profit in future is probable

against the temporary differences that are deductible. Deferred tax assets have been observed

to be $201.20 million in 2017, which were $239.30 million in 2016.

Current tax assets or income tax payable recorded by the company

As per the latest annual report of CSR Limited in 2017, it could be found that

adequate disclosures have been made regarding deferred tax assets and deferred tax

liabilities. Deferred tax assets have been observed to be $201.20 million in 2017, which were

$239.30 million in 2016. In 2016, deferred tax liabilities were reported to be $20.90 million,

while no such liabilities are realised in the year 2017. The Income tax expenses is the amount

that is calculated based on the standard accounting rules and on the amount of tax that is

owed by company to tax authorities (Ijiri 2018). Income tax payable is the amount that the

company owes in terms of tax based on tax code rules. Until the company makes the payment

of tax, the amount of income tax payable appears on the balance sheet section as liability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE ACCOUNTING

Verification of the income tax expense shown in the income statement same as the

income tax paid shown in the cash flow statement

According to the latest annual report of CSR Limited, the income tax expense of the

organisation has been $61.70 million in 2017, which was $64.40 million in 2016. On the

contrary, the disclosed income tax expense in the cash flow statement has been $52.70

million in 2017 as opposed to $14.60 million in 2016. This clearly signifies the difference

between the two reported amounts. In this case, it is worth mentioning that the income tax

expense recorded in the income statement is the amount incurred in the current taxation year

of the organisation and the payment is required to be made in the upcoming year.

Unique characteristics in the financial statements, new insights, and other information

On the basis of the analysis of all the disclosed financial information, no surprising or

confusing elements could be observed in the tax-related treatment of CSR Limited. This is

because the organisation has supplied the necessary justifications and clarifications of the

taxation treatment as footnotes in the financial report (Brooks 2015). It can be seen from the

above discussion that this enterprise has followed all the basic requirements of the Australian

Tax Office (ATO) while estimating different taxes that has been included in the financial

statement of the company. CSR Limited needs to incur lower depreciation amount because of

the variations in the norms of preparing the income statement.

Verification of the income tax expense shown in the income statement same as the

income tax paid shown in the cash flow statement

According to the latest annual report of CSR Limited, the income tax expense of the

organisation has been $61.70 million in 2017, which was $64.40 million in 2016. On the

contrary, the disclosed income tax expense in the cash flow statement has been $52.70

million in 2017 as opposed to $14.60 million in 2016. This clearly signifies the difference

between the two reported amounts. In this case, it is worth mentioning that the income tax

expense recorded in the income statement is the amount incurred in the current taxation year

of the organisation and the payment is required to be made in the upcoming year.

Unique characteristics in the financial statements, new insights, and other information

On the basis of the analysis of all the disclosed financial information, no surprising or

confusing elements could be observed in the tax-related treatment of CSR Limited. This is

because the organisation has supplied the necessary justifications and clarifications of the

taxation treatment as footnotes in the financial report (Brooks 2015). It can be seen from the

above discussion that this enterprise has followed all the basic requirements of the Australian

Tax Office (ATO) while estimating different taxes that has been included in the financial

statement of the company. CSR Limited needs to incur lower depreciation amount because of

the variations in the norms of preparing the income statement.

9CORPORATE ACCOUNTING

References

Brooks, R., 2015. Financial management: core concepts. Pearson.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Paterson, R., 2016. Off balance sheet finance. Springer.

Sierra‐García, L., Zorio‐Grima, A. and García‐Benau, M.A., 2015. Stakeholder engagement,

corporate social responsibility and integrated reporting: an exploratory study. Corporate

Social Responsibility and Environmental Management, 22(5), pp.286-304.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Spencer, A.W. and Webb, T.Z., 2015. Leases: A review of contemporary academic literature

relating to lessees. Accounting Horizons, 29(4), pp.997-1023.

Taylor, G., & Richardson, G. 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Wahlen, J., Baginski, S., & Bradshaw, M. 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

References

Brooks, R., 2015. Financial management: core concepts. Pearson.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Paterson, R., 2016. Off balance sheet finance. Springer.

Sierra‐García, L., Zorio‐Grima, A. and García‐Benau, M.A., 2015. Stakeholder engagement,

corporate social responsibility and integrated reporting: an exploratory study. Corporate

Social Responsibility and Environmental Management, 22(5), pp.286-304.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Spencer, A.W. and Webb, T.Z., 2015. Leases: A review of contemporary academic literature

relating to lessees. Accounting Horizons, 29(4), pp.997-1023.

Taylor, G., & Richardson, G. 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Wahlen, J., Baginski, S., & Bradshaw, M. 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CORPORATE ACCOUNTING

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), p.27.

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating

to capitalised leases. Pacific Accounting Review, 29(1), pp.34-54.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting Business & Finance

Journal, 9(3), p.27.

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating

to capitalised leases. Pacific Accounting Review, 29(1), pp.34-54.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CORPORATE ACCOUNTING

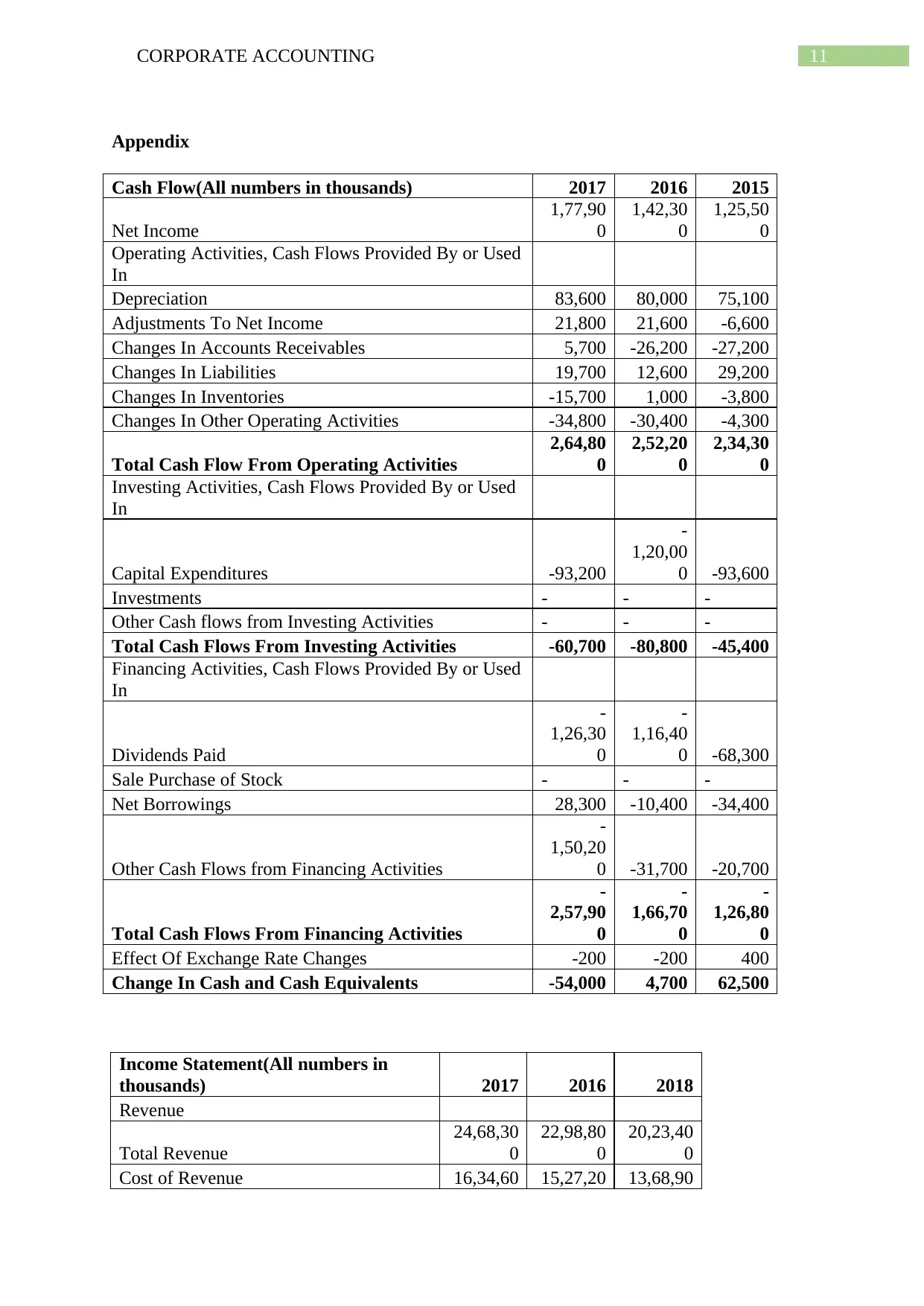

Appendix

Cash Flow(All numbers in thousands) 2017 2016 2015

Net Income

1,77,90

0

1,42,30

0

1,25,50

0

Operating Activities, Cash Flows Provided By or Used

In

Depreciation 83,600 80,000 75,100

Adjustments To Net Income 21,800 21,600 -6,600

Changes In Accounts Receivables 5,700 -26,200 -27,200

Changes In Liabilities 19,700 12,600 29,200

Changes In Inventories -15,700 1,000 -3,800

Changes In Other Operating Activities -34,800 -30,400 -4,300

Total Cash Flow From Operating Activities

2,64,80

0

2,52,20

0

2,34,30

0

Investing Activities, Cash Flows Provided By or Used

In

Capital Expenditures -93,200

-

1,20,00

0 -93,600

Investments - - -

Other Cash flows from Investing Activities - - -

Total Cash Flows From Investing Activities -60,700 -80,800 -45,400

Financing Activities, Cash Flows Provided By or Used

In

Dividends Paid

-

1,26,30

0

-

1,16,40

0 -68,300

Sale Purchase of Stock - - -

Net Borrowings 28,300 -10,400 -34,400

Other Cash Flows from Financing Activities

-

1,50,20

0 -31,700 -20,700

Total Cash Flows From Financing Activities

-

2,57,90

0

-

1,66,70

0

-

1,26,80

0

Effect Of Exchange Rate Changes -200 -200 400

Change In Cash and Cash Equivalents -54,000 4,700 62,500

Income Statement(All numbers in

thousands) 2017 2016 2018

Revenue

Total Revenue

24,68,30

0

22,98,80

0

20,23,40

0

Cost of Revenue 16,34,60 15,27,20 13,68,90

Appendix

Cash Flow(All numbers in thousands) 2017 2016 2015

Net Income

1,77,90

0

1,42,30

0

1,25,50

0

Operating Activities, Cash Flows Provided By or Used

In

Depreciation 83,600 80,000 75,100

Adjustments To Net Income 21,800 21,600 -6,600

Changes In Accounts Receivables 5,700 -26,200 -27,200

Changes In Liabilities 19,700 12,600 29,200

Changes In Inventories -15,700 1,000 -3,800

Changes In Other Operating Activities -34,800 -30,400 -4,300

Total Cash Flow From Operating Activities

2,64,80

0

2,52,20

0

2,34,30

0

Investing Activities, Cash Flows Provided By or Used

In

Capital Expenditures -93,200

-

1,20,00

0 -93,600

Investments - - -

Other Cash flows from Investing Activities - - -

Total Cash Flows From Investing Activities -60,700 -80,800 -45,400

Financing Activities, Cash Flows Provided By or Used

In

Dividends Paid

-

1,26,30

0

-

1,16,40

0 -68,300

Sale Purchase of Stock - - -

Net Borrowings 28,300 -10,400 -34,400

Other Cash Flows from Financing Activities

-

1,50,20

0 -31,700 -20,700

Total Cash Flows From Financing Activities

-

2,57,90

0

-

1,66,70

0

-

1,26,80

0

Effect Of Exchange Rate Changes -200 -200 400

Change In Cash and Cash Equivalents -54,000 4,700 62,500

Income Statement(All numbers in

thousands) 2017 2016 2018

Revenue

Total Revenue

24,68,30

0

22,98,80

0

20,23,40

0

Cost of Revenue 16,34,60 15,27,20 13,68,90

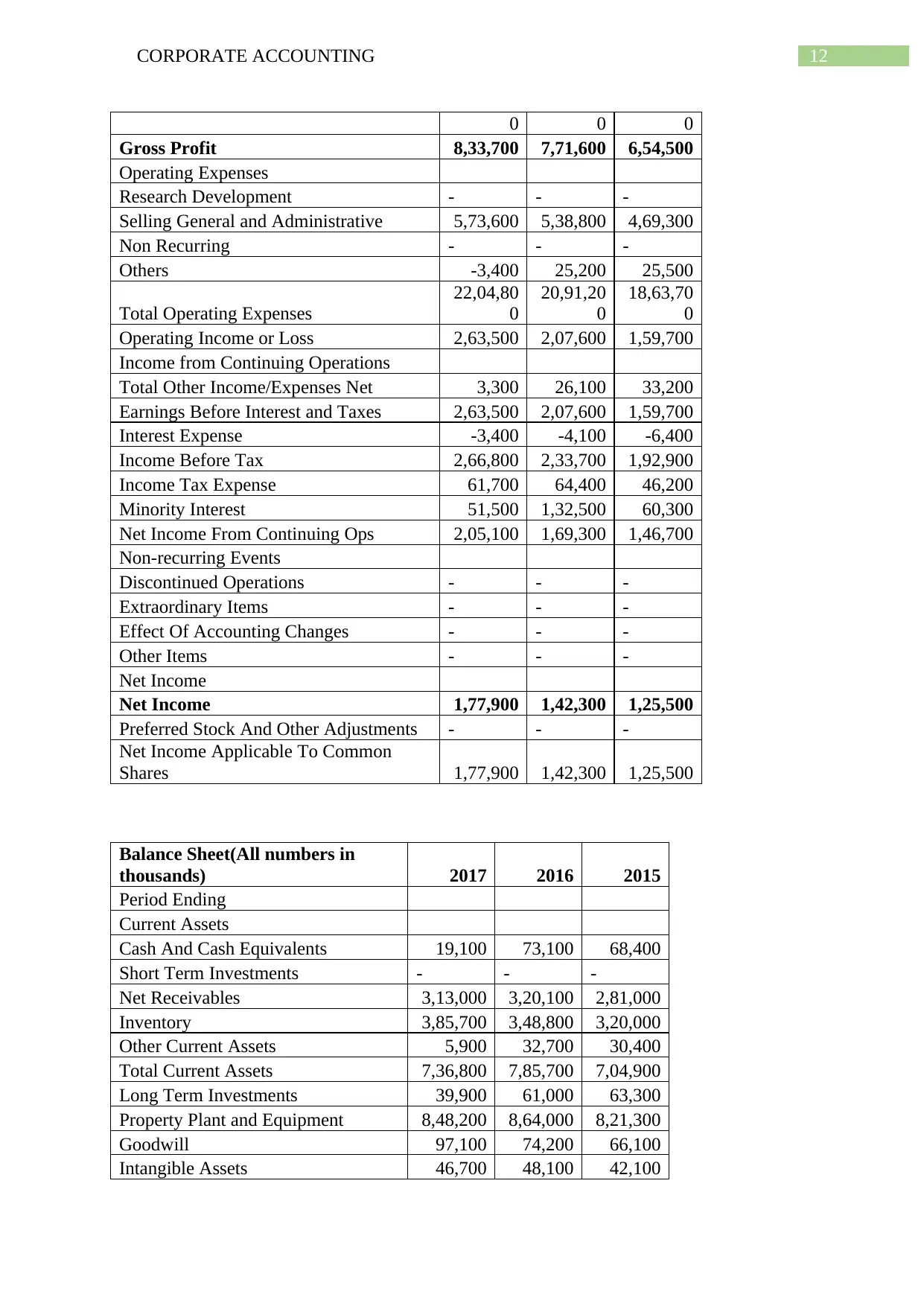

12CORPORATE ACCOUNTING

0 0 0

Gross Profit 8,33,700 7,71,600 6,54,500

Operating Expenses

Research Development - - -

Selling General and Administrative 5,73,600 5,38,800 4,69,300

Non Recurring - - -

Others -3,400 25,200 25,500

Total Operating Expenses

22,04,80

0

20,91,20

0

18,63,70

0

Operating Income or Loss 2,63,500 2,07,600 1,59,700

Income from Continuing Operations

Total Other Income/Expenses Net 3,300 26,100 33,200

Earnings Before Interest and Taxes 2,63,500 2,07,600 1,59,700

Interest Expense -3,400 -4,100 -6,400

Income Before Tax 2,66,800 2,33,700 1,92,900

Income Tax Expense 61,700 64,400 46,200

Minority Interest 51,500 1,32,500 60,300

Net Income From Continuing Ops 2,05,100 1,69,300 1,46,700

Non-recurring Events

Discontinued Operations - - -

Extraordinary Items - - -

Effect Of Accounting Changes - - -

Other Items - - -

Net Income

Net Income 1,77,900 1,42,300 1,25,500

Preferred Stock And Other Adjustments - - -

Net Income Applicable To Common

Shares 1,77,900 1,42,300 1,25,500

Balance Sheet(All numbers in

thousands) 2017 2016 2015

Period Ending

Current Assets

Cash And Cash Equivalents 19,100 73,100 68,400

Short Term Investments - - -

Net Receivables 3,13,000 3,20,100 2,81,000

Inventory 3,85,700 3,48,800 3,20,000

Other Current Assets 5,900 32,700 30,400

Total Current Assets 7,36,800 7,85,700 7,04,900

Long Term Investments 39,900 61,000 63,300

Property Plant and Equipment 8,48,200 8,64,000 8,21,300

Goodwill 97,100 74,200 66,100

Intangible Assets 46,700 48,100 42,100

0 0 0

Gross Profit 8,33,700 7,71,600 6,54,500

Operating Expenses

Research Development - - -

Selling General and Administrative 5,73,600 5,38,800 4,69,300

Non Recurring - - -

Others -3,400 25,200 25,500

Total Operating Expenses

22,04,80

0

20,91,20

0

18,63,70

0

Operating Income or Loss 2,63,500 2,07,600 1,59,700

Income from Continuing Operations

Total Other Income/Expenses Net 3,300 26,100 33,200

Earnings Before Interest and Taxes 2,63,500 2,07,600 1,59,700

Interest Expense -3,400 -4,100 -6,400

Income Before Tax 2,66,800 2,33,700 1,92,900

Income Tax Expense 61,700 64,400 46,200

Minority Interest 51,500 1,32,500 60,300

Net Income From Continuing Ops 2,05,100 1,69,300 1,46,700

Non-recurring Events

Discontinued Operations - - -

Extraordinary Items - - -

Effect Of Accounting Changes - - -

Other Items - - -

Net Income

Net Income 1,77,900 1,42,300 1,25,500

Preferred Stock And Other Adjustments - - -

Net Income Applicable To Common

Shares 1,77,900 1,42,300 1,25,500

Balance Sheet(All numbers in

thousands) 2017 2016 2015

Period Ending

Current Assets

Cash And Cash Equivalents 19,100 73,100 68,400

Short Term Investments - - -

Net Receivables 3,13,000 3,20,100 2,81,000

Inventory 3,85,700 3,48,800 3,20,000

Other Current Assets 5,900 32,700 30,400

Total Current Assets 7,36,800 7,85,700 7,04,900

Long Term Investments 39,900 61,000 63,300

Property Plant and Equipment 8,48,200 8,64,000 8,21,300

Goodwill 97,100 74,200 66,100

Intangible Assets 46,700 48,100 42,100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.