HI5020 Corporate Accounting Project: CBA and Westpac Bank Analysis

VerifiedAdded on 2023/06/08

|18

|3951

|286

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, comparing the Commonwealth Bank of Australia (CBA) and Westpac Bank. It examines key financial statements, including owner's equity, cash flow statements, and comprehensive income statements, along with corporate taxation treatments. The analysis includes a detailed review of equity items, debt-equity positions, cash flow activities (operating, investing, and financing), comprehensive income statement components, and corporate income tax accounting. Comparative analyses are conducted to assess the performance of each bank, focusing on cash flow management and profitability. The report concludes with an overall evaluation of the banks' financial health and adherence to corporate accounting principles, emphasizing the importance of transparent financial reporting for stakeholders.

Running Head: Corporate Accounting

1

Project Report: Corporate Accounting

1

Project Report: Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

2

Executive summary

The report has been prepared to evaluate the importance of the corporate accounting

in an organization. The report has been prepared to understand the process of corporate

accounting in better way. The Commonwealth bank of Australia and Westpac bank has been

taken into the context to identify the overall position of the business in an organization in

order to present, record and evaluate the final financial statement items and figures of the

business. The cash flow statement, owner’s equity, comprehensive income statement and

corporate taxation treatment of the business has been studied in the report. Through

conducting the study, it has been found that the annual report of an organization must be

transparent enough for the shareholders to make better decisions.

2

Executive summary

The report has been prepared to evaluate the importance of the corporate accounting

in an organization. The report has been prepared to understand the process of corporate

accounting in better way. The Commonwealth bank of Australia and Westpac bank has been

taken into the context to identify the overall position of the business in an organization in

order to present, record and evaluate the final financial statement items and figures of the

business. The cash flow statement, owner’s equity, comprehensive income statement and

corporate taxation treatment of the business has been studied in the report. Through

conducting the study, it has been found that the annual report of an organization must be

transparent enough for the shareholders to make better decisions.

Corporate Accounting

3

Contents

Introduction of report........................................................................................................4

Companies brief................................................................................................................4

Commonwealths bank of Australia..............................................................................4

Westpac bank................................................................................................................4

Owner’s equity..................................................................................................................5

1.Equity item list...........................................................................................................5

2.Debt and equity position............................................................................................5

Cash flow statement..........................................................................................................6

3.Cash flow item list.....................................................................................................6

4.Comparative analysis in cash flows...........................................................................8

5.Comparative analysis among the companies.............................................................9

Comprehensive income statement..................................................................................10

6.Comprehensive income statement items.................................................................10

7.Reasons....................................................................................................................10

8.Comparative analysis...............................................................................................11

9.Manager’s performance...........................................................................................11

Accounting for corporate income tax.............................................................................11

10.Tax expenses of companies...................................................................................11

11.Effective tax rate....................................................................................................12

12.Deferred tax assets or liabilities.............................................................................12

13.Changes in the figures of Deferred tax assets or liabilities...................................13

14.Cash tax amount....................................................................................................13

15.Cash tax rate..........................................................................................................14

3

Contents

Introduction of report........................................................................................................4

Companies brief................................................................................................................4

Commonwealths bank of Australia..............................................................................4

Westpac bank................................................................................................................4

Owner’s equity..................................................................................................................5

1.Equity item list...........................................................................................................5

2.Debt and equity position............................................................................................5

Cash flow statement..........................................................................................................6

3.Cash flow item list.....................................................................................................6

4.Comparative analysis in cash flows...........................................................................8

5.Comparative analysis among the companies.............................................................9

Comprehensive income statement..................................................................................10

6.Comprehensive income statement items.................................................................10

7.Reasons....................................................................................................................10

8.Comparative analysis...............................................................................................11

9.Manager’s performance...........................................................................................11

Accounting for corporate income tax.............................................................................11

10.Tax expenses of companies...................................................................................11

11.Effective tax rate....................................................................................................12

12.Deferred tax assets or liabilities.............................................................................12

13.Changes in the figures of Deferred tax assets or liabilities...................................13

14.Cash tax amount....................................................................................................13

15.Cash tax rate..........................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

4

16.Book and cash tax rate...........................................................................................14

Conclusion......................................................................................................................14

References.......................................................................................................................16

4

16.Book and cash tax rate...........................................................................................14

Conclusion......................................................................................................................14

References.......................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

5

Introduction of report:

Corporate accounting is accounting’s part which focuses on the treatment of the

accounting figures of the company. It evaluates the different item of the final financial

statement of an organization to conclude that whether the company has followed the proper

policies or whether the proper presentation has been done by the business to reach over the

conclusion. The corporate accounting process plays a crucial role in an organization and

stakeholder in order to make it easier for the internal and external stakeholder of the business

to identify the performance of the business and compare it with the other companies in the

same industry for the purpose of the investment etc. (Lumby and Jones, 2007).

The report has been conducted to understand the process of corporate accounting in

better way. The Commonwealth bank of Australia and Westpac bank has been taken into the

context to identify the overall position of the business in an organization in order to present,

record and evaluate the final financial statement items and figures of the business. The cash

flow statement, owner’s equity, comprehensive income statement and corporate taxation

treatment of the business has been studied in the report.

Companies brief:

Commonwealths bank of Australia:

Commonwealth bank of Australia (CBA) is an Australian bank which operating area

is worldwide. Mainly, the operating market of the business is new Zealand, Asia, United

states, united kingdom etc. the bank offers numerous financial services and products such as

consumer banking, corporate banking, investment management, global wealth management,

mortgages, private equity etc. the company is among the largest bank of the Australia and the

services of the bank are also huge in numbers (Home, 2018).

Westpac bank:

Westpac Bank is an Australian bank and financial service provider company. The

company is serving its operation at worldwide level. However, the main operating market of

the business is New Zealand, Australia, Asia, United States pacific region. The bank offers

numerous financial services and products such as consumer banking, corporate banking,

investment management, global wealth management, and mortgages, private equity etc.

5

Introduction of report:

Corporate accounting is accounting’s part which focuses on the treatment of the

accounting figures of the company. It evaluates the different item of the final financial

statement of an organization to conclude that whether the company has followed the proper

policies or whether the proper presentation has been done by the business to reach over the

conclusion. The corporate accounting process plays a crucial role in an organization and

stakeholder in order to make it easier for the internal and external stakeholder of the business

to identify the performance of the business and compare it with the other companies in the

same industry for the purpose of the investment etc. (Lumby and Jones, 2007).

The report has been conducted to understand the process of corporate accounting in

better way. The Commonwealth bank of Australia and Westpac bank has been taken into the

context to identify the overall position of the business in an organization in order to present,

record and evaluate the final financial statement items and figures of the business. The cash

flow statement, owner’s equity, comprehensive income statement and corporate taxation

treatment of the business has been studied in the report.

Companies brief:

Commonwealths bank of Australia:

Commonwealth bank of Australia (CBA) is an Australian bank which operating area

is worldwide. Mainly, the operating market of the business is new Zealand, Asia, United

states, united kingdom etc. the bank offers numerous financial services and products such as

consumer banking, corporate banking, investment management, global wealth management,

mortgages, private equity etc. the company is among the largest bank of the Australia and the

services of the bank are also huge in numbers (Home, 2018).

Westpac bank:

Westpac Bank is an Australian bank and financial service provider company. The

company is serving its operation at worldwide level. However, the main operating market of

the business is New Zealand, Australia, Asia, United States pacific region. The bank offers

numerous financial services and products such as consumer banking, corporate banking,

investment management, global wealth management, and mortgages, private equity etc.

Corporate Accounting

6

(Home, 2018). The bank is among the largest bank of the Australia and the services of the

bank are also huge in numbers.

Owner’s equity:

Owner’s equity is a head of statement of financial performance of an entity which

represents the entire funds which has been raised by the business through issuing the share

and through keeping few amount from the profit of the company for any emergency.

1. Equity item list:

The equity item list of CBA and Westpac bank has been prepared to enhance the

understanding about the equity items and identify the changes into the equity position of the

company from last year. The equity item list is as follows:

Equity Items

Commonwealth bank of

Australia Westpac Bank

AUD in million 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Share capital

Ordinary share capital 35262 34125 3.33% 34889 33469 4.24%

Other equity instrument - 406 -437 -369 18.43%

Reserves 2556 3115 -17.95% 858 790 8.61%

Retained earnings 22312 20430 9.21% 16871 15311 10.19%

Total stockholder's equity 60130 58076 3.54% 52181 49201 6.06%

(Annual report, 2017)

Above table represent that the main equity item of a business is share capital, reserves

and retained earnings. Share capital represents the amount which has been generated by an

entity through issuance of the equity shares and preference shares in the market. In case of

share capital in CBA, 3.33% improvement has been seen and the Westpac bank depicts

4.24% increment in equity share and 18.43% in preference shares of the company.

In addition, reserve stand for the amount which is kept aside by the business for any

sudden issue in the business which has been lowered by CBA by 17.95% and improved by

Westpac by 18.43%. The retained earnings are the amount which is retained for future

investment of the company. The retained earnings of both the company has been improved by

9.21% and 10.19% respectively.

6

(Home, 2018). The bank is among the largest bank of the Australia and the services of the

bank are also huge in numbers.

Owner’s equity:

Owner’s equity is a head of statement of financial performance of an entity which

represents the entire funds which has been raised by the business through issuing the share

and through keeping few amount from the profit of the company for any emergency.

1. Equity item list:

The equity item list of CBA and Westpac bank has been prepared to enhance the

understanding about the equity items and identify the changes into the equity position of the

company from last year. The equity item list is as follows:

Equity Items

Commonwealth bank of

Australia Westpac Bank

AUD in million 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Share capital

Ordinary share capital 35262 34125 3.33% 34889 33469 4.24%

Other equity instrument - 406 -437 -369 18.43%

Reserves 2556 3115 -17.95% 858 790 8.61%

Retained earnings 22312 20430 9.21% 16871 15311 10.19%

Total stockholder's equity 60130 58076 3.54% 52181 49201 6.06%

(Annual report, 2017)

Above table represent that the main equity item of a business is share capital, reserves

and retained earnings. Share capital represents the amount which has been generated by an

entity through issuance of the equity shares and preference shares in the market. In case of

share capital in CBA, 3.33% improvement has been seen and the Westpac bank depicts

4.24% increment in equity share and 18.43% in preference shares of the company.

In addition, reserve stand for the amount which is kept aside by the business for any

sudden issue in the business which has been lowered by CBA by 17.95% and improved by

Westpac by 18.43%. The retained earnings are the amount which is retained for future

investment of the company. The retained earnings of both the company has been improved by

9.21% and 10.19% respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

7

2. Debt and equity position:

Debt is the borrowings of an organization which has been raised by the business from

the market whereas the equity stands for the amount which has been raised by the business

through selling the ownership in the market. The debt and equity level of CBA and Westpac

are as follows:

Equity Items

Commonwealth bank of

Australia

Westpac

Bank

AUD in million 2017 2017

Long term debt 17953 17666

Equity 60130 52181

Debt / Equity 29.86% 33.86%

(Annual report, 2017)

The debt equity level of the CBA is 29.86% and the Westpac bank is 33.86% which

represents the higher position of Westpac. The Westpac is managing higher debt in context

The debt equity level of the CBA is 29.86% and the Westpac bank is 33.86% which

represents the higher position of Westpac. The Westpac is managing higher debt in context

with the equity than the CBA.

Cash flow statement:

Cash flow statement is a financial statement of an entity which represents the entire

changes in the cash outflow and inflow position of the company in a specific period of time.

3. Cash flow item list:

The cash flow item list of CBA and Westpac bank has been prepared to enhance the

understanding about the cash flow items and identify the changes into the cash flow position

of the company from last year. The equity item list is as follows:

7

2. Debt and equity position:

Debt is the borrowings of an organization which has been raised by the business from

the market whereas the equity stands for the amount which has been raised by the business

through selling the ownership in the market. The debt and equity level of CBA and Westpac

are as follows:

Equity Items

Commonwealth bank of

Australia

Westpac

Bank

AUD in million 2017 2017

Long term debt 17953 17666

Equity 60130 52181

Debt / Equity 29.86% 33.86%

(Annual report, 2017)

The debt equity level of the CBA is 29.86% and the Westpac bank is 33.86% which

represents the higher position of Westpac. The Westpac is managing higher debt in context

The debt equity level of the CBA is 29.86% and the Westpac bank is 33.86% which

represents the higher position of Westpac. The Westpac is managing higher debt in context

with the equity than the CBA.

Cash flow statement:

Cash flow statement is a financial statement of an entity which represents the entire

changes in the cash outflow and inflow position of the company in a specific period of time.

3. Cash flow item list:

The cash flow item list of CBA and Westpac bank has been prepared to enhance the

understanding about the cash flow items and identify the changes into the cash flow position

of the company from last year. The equity item list is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

8

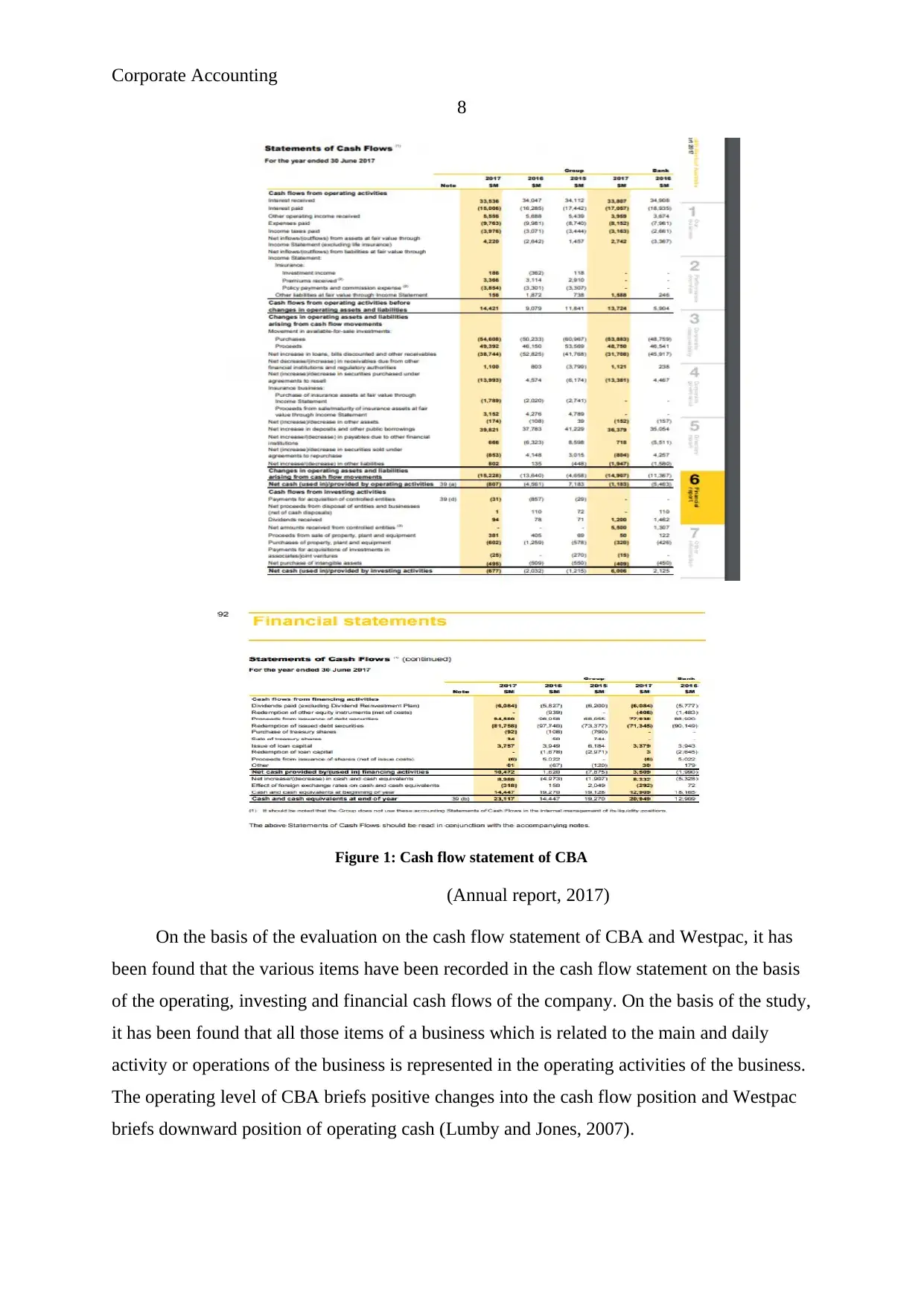

Figure 1: Cash flow statement of CBA

(Annual report, 2017)

On the basis of the evaluation on the cash flow statement of CBA and Westpac, it has

been found that the various items have been recorded in the cash flow statement on the basis

of the operating, investing and financial cash flows of the company. On the basis of the study,

it has been found that all those items of a business which is related to the main and daily

activity or operations of the business is represented in the operating activities of the business.

The operating level of CBA briefs positive changes into the cash flow position and Westpac

briefs downward position of operating cash (Lumby and Jones, 2007).

8

Figure 1: Cash flow statement of CBA

(Annual report, 2017)

On the basis of the evaluation on the cash flow statement of CBA and Westpac, it has

been found that the various items have been recorded in the cash flow statement on the basis

of the operating, investing and financial cash flows of the company. On the basis of the study,

it has been found that all those items of a business which is related to the main and daily

activity or operations of the business is represented in the operating activities of the business.

The operating level of CBA briefs positive changes into the cash flow position and Westpac

briefs downward position of operating cash (Lumby and Jones, 2007).

Corporate Accounting

9

Further, all those items of a business which is related to the investment activity or

operations of the business is represented in the investing activities of the business. The

investing level of CBA and Westpac briefs positive changes. Lastly, all those items of a

business which is related to the financial activity or operations of the business are represented

in the financing activities of the business. The financial level of CBA briefs positive changes

and in Westpac, it offers the negative changes.

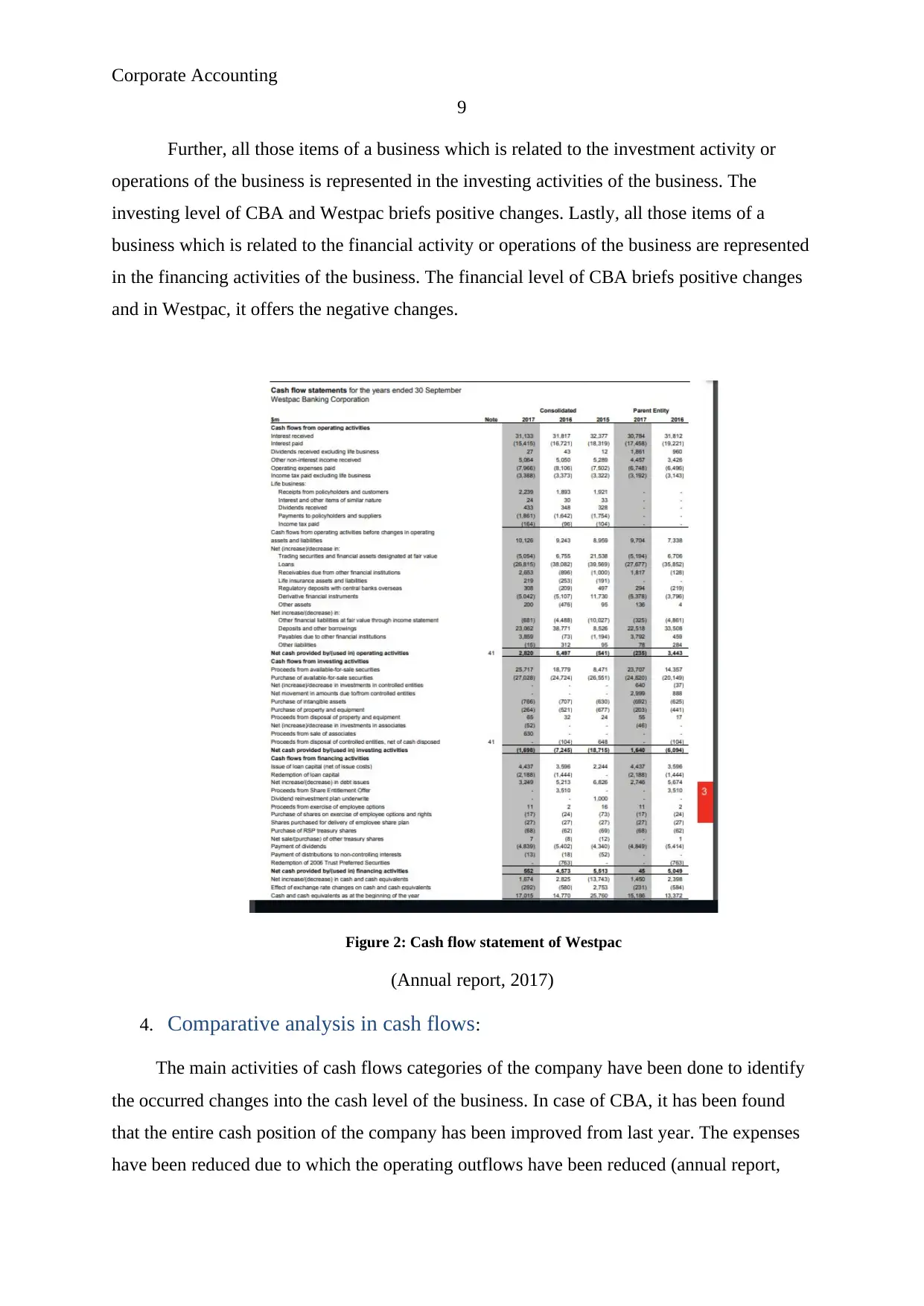

Figure 2: Cash flow statement of Westpac

(Annual report, 2017)

4. Comparative analysis in cash flows:

The main activities of cash flows categories of the company have been done to identify

the occurred changes into the cash level of the business. In case of CBA, it has been found

that the entire cash position of the company has been improved from last year. The expenses

have been reduced due to which the operating outflows have been reduced (annual report,

9

Further, all those items of a business which is related to the investment activity or

operations of the business is represented in the investing activities of the business. The

investing level of CBA and Westpac briefs positive changes. Lastly, all those items of a

business which is related to the financial activity or operations of the business are represented

in the financing activities of the business. The financial level of CBA briefs positive changes

and in Westpac, it offers the negative changes.

Figure 2: Cash flow statement of Westpac

(Annual report, 2017)

4. Comparative analysis in cash flows:

The main activities of cash flows categories of the company have been done to identify

the occurred changes into the cash level of the business. In case of CBA, it has been found

that the entire cash position of the company has been improved from last year. The expenses

have been reduced due to which the operating outflows have been reduced (annual report,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

10

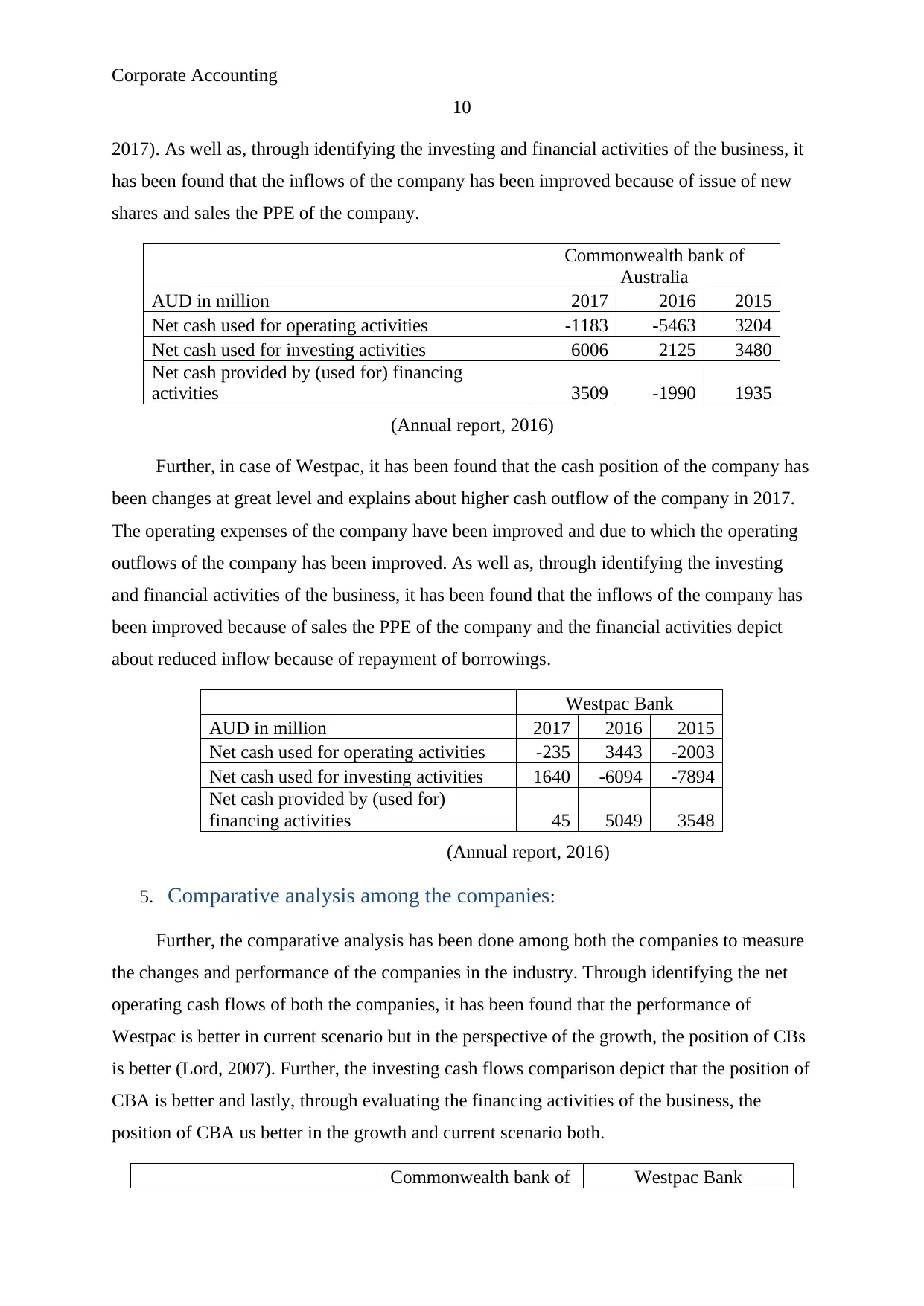

2017). As well as, through identifying the investing and financial activities of the business, it

has been found that the inflows of the company has been improved because of issue of new

shares and sales the PPE of the company.

Commonwealth bank of

Australia

AUD in million 2017 2016 2015

Net cash used for operating activities -1183 -5463 3204

Net cash used for investing activities 6006 2125 3480

Net cash provided by (used for) financing

activities 3509 -1990 1935

(Annual report, 2016)

Further, in case of Westpac, it has been found that the cash position of the company has

been changes at great level and explains about higher cash outflow of the company in 2017.

The operating expenses of the company have been improved and due to which the operating

outflows of the company has been improved. As well as, through identifying the investing

and financial activities of the business, it has been found that the inflows of the company has

been improved because of sales the PPE of the company and the financial activities depict

about reduced inflow because of repayment of borrowings.

Westpac Bank

AUD in million 2017 2016 2015

Net cash used for operating activities -235 3443 -2003

Net cash used for investing activities 1640 -6094 -7894

Net cash provided by (used for)

financing activities 45 5049 3548

(Annual report, 2016)

5. Comparative analysis among the companies:

Further, the comparative analysis has been done among both the companies to measure

the changes and performance of the companies in the industry. Through identifying the net

operating cash flows of both the companies, it has been found that the performance of

Westpac is better in current scenario but in the perspective of the growth, the position of CBs

is better (Lord, 2007). Further, the investing cash flows comparison depict that the position of

CBA is better and lastly, through evaluating the financing activities of the business, the

position of CBA us better in the growth and current scenario both.

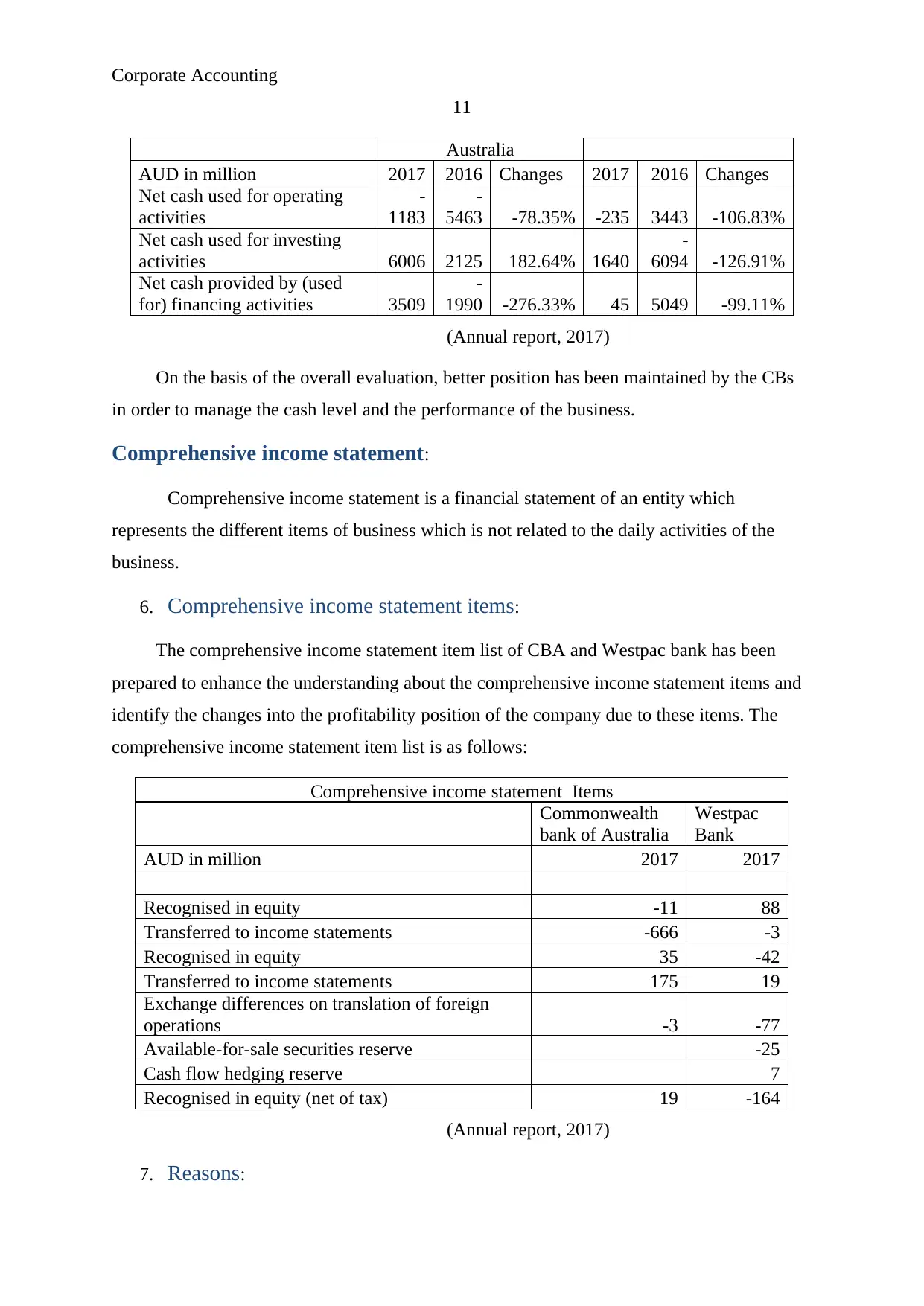

Commonwealth bank of Westpac Bank

10

2017). As well as, through identifying the investing and financial activities of the business, it

has been found that the inflows of the company has been improved because of issue of new

shares and sales the PPE of the company.

Commonwealth bank of

Australia

AUD in million 2017 2016 2015

Net cash used for operating activities -1183 -5463 3204

Net cash used for investing activities 6006 2125 3480

Net cash provided by (used for) financing

activities 3509 -1990 1935

(Annual report, 2016)

Further, in case of Westpac, it has been found that the cash position of the company has

been changes at great level and explains about higher cash outflow of the company in 2017.

The operating expenses of the company have been improved and due to which the operating

outflows of the company has been improved. As well as, through identifying the investing

and financial activities of the business, it has been found that the inflows of the company has

been improved because of sales the PPE of the company and the financial activities depict

about reduced inflow because of repayment of borrowings.

Westpac Bank

AUD in million 2017 2016 2015

Net cash used for operating activities -235 3443 -2003

Net cash used for investing activities 1640 -6094 -7894

Net cash provided by (used for)

financing activities 45 5049 3548

(Annual report, 2016)

5. Comparative analysis among the companies:

Further, the comparative analysis has been done among both the companies to measure

the changes and performance of the companies in the industry. Through identifying the net

operating cash flows of both the companies, it has been found that the performance of

Westpac is better in current scenario but in the perspective of the growth, the position of CBs

is better (Lord, 2007). Further, the investing cash flows comparison depict that the position of

CBA is better and lastly, through evaluating the financing activities of the business, the

position of CBA us better in the growth and current scenario both.

Commonwealth bank of Westpac Bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

11

Australia

AUD in million 2017 2016 Changes 2017 2016 Changes

Net cash used for operating

activities

-

1183

-

5463 -78.35% -235 3443 -106.83%

Net cash used for investing

activities 6006 2125 182.64% 1640

-

6094 -126.91%

Net cash provided by (used

for) financing activities 3509

-

1990 -276.33% 45 5049 -99.11%

(Annual report, 2017)

On the basis of the overall evaluation, better position has been maintained by the CBs

in order to manage the cash level and the performance of the business.

Comprehensive income statement:

Comprehensive income statement is a financial statement of an entity which

represents the different items of business which is not related to the daily activities of the

business.

6. Comprehensive income statement items:

The comprehensive income statement item list of CBA and Westpac bank has been

prepared to enhance the understanding about the comprehensive income statement items and

identify the changes into the profitability position of the company due to these items. The

comprehensive income statement item list is as follows:

Comprehensive income statement Items

Commonwealth

bank of Australia

Westpac

Bank

AUD in million 2017 2017

Recognised in equity -11 88

Transferred to income statements -666 -3

Recognised in equity 35 -42

Transferred to income statements 175 19

Exchange differences on translation of foreign

operations -3 -77

Available-for-sale securities reserve -25

Cash flow hedging reserve 7

Recognised in equity (net of tax) 19 -164

(Annual report, 2017)

7. Reasons:

11

Australia

AUD in million 2017 2016 Changes 2017 2016 Changes

Net cash used for operating

activities

-

1183

-

5463 -78.35% -235 3443 -106.83%

Net cash used for investing

activities 6006 2125 182.64% 1640

-

6094 -126.91%

Net cash provided by (used

for) financing activities 3509

-

1990 -276.33% 45 5049 -99.11%

(Annual report, 2017)

On the basis of the overall evaluation, better position has been maintained by the CBs

in order to manage the cash level and the performance of the business.

Comprehensive income statement:

Comprehensive income statement is a financial statement of an entity which

represents the different items of business which is not related to the daily activities of the

business.

6. Comprehensive income statement items:

The comprehensive income statement item list of CBA and Westpac bank has been

prepared to enhance the understanding about the comprehensive income statement items and

identify the changes into the profitability position of the company due to these items. The

comprehensive income statement item list is as follows:

Comprehensive income statement Items

Commonwealth

bank of Australia

Westpac

Bank

AUD in million 2017 2017

Recognised in equity -11 88

Transferred to income statements -666 -3

Recognised in equity 35 -42

Transferred to income statements 175 19

Exchange differences on translation of foreign

operations -3 -77

Available-for-sale securities reserve -25

Cash flow hedging reserve 7

Recognised in equity (net of tax) 19 -164

(Annual report, 2017)

7. Reasons:

Corporate Accounting

12

Comprehensive income statement is prepared separately by the companies in order to

maintain and present the items differently which are not related to business directly. Though,

they play an important role in the financial performance of the business and affect the

profitability position of the business (Jiashu, 2009). These items take place because of the

fluctuations in the economical factors and the fluctuation in the foreign currency. If these

items would be added into the financial performance statement of the business then it could

manipulate the result for the internal analysis of the business.

8. Comparative analysis:

In case of comparative analysis among the profitability level of the business and the

changes in the profitability level of the business after showing the impact of the

comprehensive income statement in the business, it has been found that the various changes

have occurred into the profitability level of both the business (Hillier, Grinblatt and Titman,

2011). In case of Westpac, it has been found that the profit of the company is $ 7843 million

before the impact and after the impact; it has been lowered to $ 7828 million. Further, in case

of CBA, it has been found that it has been found that the profit of the company is $ 8979

million before the impact and after the impact; it has been lowered to $ 8528 million. It

explains that the profit position of both the companies have been lower because of the

comprehensive income statement of the business.

9. Manager’s performance:

A manager and the top level management of a business always been evaluated on the

basis of the financial performance of the business. Such as, if a generate amount has been

generated by the business through its activities, than the performance of the manager would

be marked as good (Higgins, 2012). If the comprehensive income statement items are take

into concern then these items must not been added into the evaluation process because it is

not related to managers and the direct activities of the business.

Accounting for corporate income tax:

Accounting for corporate income tax is a crucial element of an entity which represents

the recording and the presentation of the taxation system of the company (Gapenski, 2008).

10. Tax expenses of companies:

12

Comprehensive income statement is prepared separately by the companies in order to

maintain and present the items differently which are not related to business directly. Though,

they play an important role in the financial performance of the business and affect the

profitability position of the business (Jiashu, 2009). These items take place because of the

fluctuations in the economical factors and the fluctuation in the foreign currency. If these

items would be added into the financial performance statement of the business then it could

manipulate the result for the internal analysis of the business.

8. Comparative analysis:

In case of comparative analysis among the profitability level of the business and the

changes in the profitability level of the business after showing the impact of the

comprehensive income statement in the business, it has been found that the various changes

have occurred into the profitability level of both the business (Hillier, Grinblatt and Titman,

2011). In case of Westpac, it has been found that the profit of the company is $ 7843 million

before the impact and after the impact; it has been lowered to $ 7828 million. Further, in case

of CBA, it has been found that it has been found that the profit of the company is $ 8979

million before the impact and after the impact; it has been lowered to $ 8528 million. It

explains that the profit position of both the companies have been lower because of the

comprehensive income statement of the business.

9. Manager’s performance:

A manager and the top level management of a business always been evaluated on the

basis of the financial performance of the business. Such as, if a generate amount has been

generated by the business through its activities, than the performance of the manager would

be marked as good (Higgins, 2012). If the comprehensive income statement items are take

into concern then these items must not been added into the evaluation process because it is

not related to managers and the direct activities of the business.

Accounting for corporate income tax:

Accounting for corporate income tax is a crucial element of an entity which represents

the recording and the presentation of the taxation system of the company (Gapenski, 2008).

10. Tax expenses of companies:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.