HI5020 Corporate Accounting: Financial Analysis of GWA Group Limited

VerifiedAdded on 2023/06/11

|13

|3082

|63

Report

AI Summary

This report provides a comprehensive analysis of GWA Group Limited's financial statements, focusing on the cash flow statement, income tax expenses, and deferred tax assets. The analysis includes a breakdown of cash flow from operating, investing, and financing activities over three years (2015-2017), highlighting changes and trends. It also examines the components of other comprehensive income, the differences between accounting income and taxable income, and the treatment of deferred tax assets and liabilities. The report further discusses the differences between income tax paid and income tax expenses, emphasizing the detailed tax treatment disclosures by GWA Group Limited, making it a valuable resource for understanding corporate accounting practices. Desklib offers similar solved assignments for students.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student

Name of the University

Author Note

Corporate accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Table of Contents

Requirement i)............................................................................................................................2

Requirement ii)...........................................................................................................................3

Requirement iii).........................................................................................................................3

Requirement iv)..........................................................................................................................4

Requirement v)...........................................................................................................................5

Requirement vi)..........................................................................................................................5

Requirement vii).........................................................................................................................5

Requirement viii).......................................................................................................................6

Requirement ix)..........................................................................................................................6

Requirement x)...........................................................................................................................7

Requirement xi)..........................................................................................................................8

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

Table of Contents

Requirement i)............................................................................................................................2

Requirement ii)...........................................................................................................................3

Requirement iii).........................................................................................................................3

Requirement iv)..........................................................................................................................4

Requirement v)...........................................................................................................................5

Requirement vi)..........................................................................................................................5

Requirement vii).........................................................................................................................5

Requirement viii).......................................................................................................................6

Requirement ix)..........................................................................................................................6

Requirement x)...........................................................................................................................7

Requirement xi)..........................................................................................................................8

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

CORPORATE ACCOUNTING

Requirement i)

Analysis of elements of cash flow of GWA Group limited:

The cash flow statement of GWA Group is segmented into three parts comprising of

cash flow from operating activities, cash flow from financing activities and cash flow from

investing activities. Several items as reported under the operating activities include receipt

from customers, cash generated from operations, interest received, income tax paid and

interest and facility paid. Net cash from operating activities has increased from $ 54924 in

year 2016 compared to $ 57171 (Gwagroup.com.au, 2018). This increase in cash flow from

operating activities is because of reduction in payment made to suppliers and employees,

facility and interest fees paid and income tax paid. In addition to this, total amount of interest

received has increased in recent year. Cash flow from investing activities include items such

as acquisition of intangible assets, property, equipment and plant, proceeds generated from

sales of such assets, net transaction costs and business disposal. In year, total amount of net

cash generated from investing activities stood at $ 12 as against net cash used from investing

activities of amount $ 4911 (Gwagroup.com.au, 2018). This is so because a significant

amount has been invested for acquiring intangible assets, property, equipment and plant.

Items under the cash flow from financing activities include repayment of borrowings,

proceeds from borrowing, dividend paid, payment for on market share buyback and capital

return to LTI grants holders. There is decrease is net cash used in financing activities from $

53791 in year 2016 as against $ 51590 in year 2017. This decrease in net cash used is

attributable to higher amount of dividend paid and repayment of borrowings. There is

increment in payment from borrowings that has led to decrease in net cash used in financing

activities.

Requirement i)

Analysis of elements of cash flow of GWA Group limited:

The cash flow statement of GWA Group is segmented into three parts comprising of

cash flow from operating activities, cash flow from financing activities and cash flow from

investing activities. Several items as reported under the operating activities include receipt

from customers, cash generated from operations, interest received, income tax paid and

interest and facility paid. Net cash from operating activities has increased from $ 54924 in

year 2016 compared to $ 57171 (Gwagroup.com.au, 2018). This increase in cash flow from

operating activities is because of reduction in payment made to suppliers and employees,

facility and interest fees paid and income tax paid. In addition to this, total amount of interest

received has increased in recent year. Cash flow from investing activities include items such

as acquisition of intangible assets, property, equipment and plant, proceeds generated from

sales of such assets, net transaction costs and business disposal. In year, total amount of net

cash generated from investing activities stood at $ 12 as against net cash used from investing

activities of amount $ 4911 (Gwagroup.com.au, 2018). This is so because a significant

amount has been invested for acquiring intangible assets, property, equipment and plant.

Items under the cash flow from financing activities include repayment of borrowings,

proceeds from borrowing, dividend paid, payment for on market share buyback and capital

return to LTI grants holders. There is decrease is net cash used in financing activities from $

53791 in year 2016 as against $ 51590 in year 2017. This decrease in net cash used is

attributable to higher amount of dividend paid and repayment of borrowings. There is

increment in payment from borrowings that has led to decrease in net cash used in financing

activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Requirement ii)

Comparative analysis of cash flow items for three years:

Particular 2015 2016 2017

Net cash flows from operating activities

$

43,505.00 54,924 57,171

Net cash flows used in investing

activities

$

1,16,596.00 12

-

4,911

Net cash flows used in financing

activities -155524

-

53,791

-

51,590

It can be seen from above table that there is increase in net cash flow from operating

activities from $ 43505 in year 2015 to $ 54924 and $ 57171 in year 2016 and 2017. Now,

looking at the figures, the amount of net cash flow from investing activities in year 2016 and

2015 compared to net cash used from investing activities. There has been decrease in net cash

flow from financing activities from $ 155524 in year 2015 compared to $ 53791 in year 2016

and $ 51590 in year 2017 respectively (Gwagroup.com.au, 2018).

Requirement ii)

Comparative analysis of cash flow items for three years:

Particular 2015 2016 2017

Net cash flows from operating activities

$

43,505.00 54,924 57,171

Net cash flows used in investing

activities

$

1,16,596.00 12

-

4,911

Net cash flows used in financing

activities -155524

-

53,791

-

51,590

It can be seen from above table that there is increase in net cash flow from operating

activities from $ 43505 in year 2015 to $ 54924 and $ 57171 in year 2016 and 2017. Now,

looking at the figures, the amount of net cash flow from investing activities in year 2016 and

2015 compared to net cash used from investing activities. There has been decrease in net cash

flow from financing activities from $ 155524 in year 2015 compared to $ 53791 in year 2016

and $ 51590 in year 2017 respectively (Gwagroup.com.au, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

2015 2016 2017

$-200,000.00

$-150,000.00

$-100,000.00

$-50,000.00

$-

$50,000.00

$100,000.00

$150,000.00

43,505 54,924 57,171

116,596

12

-4,911

-155,524

-53,791 -51,590

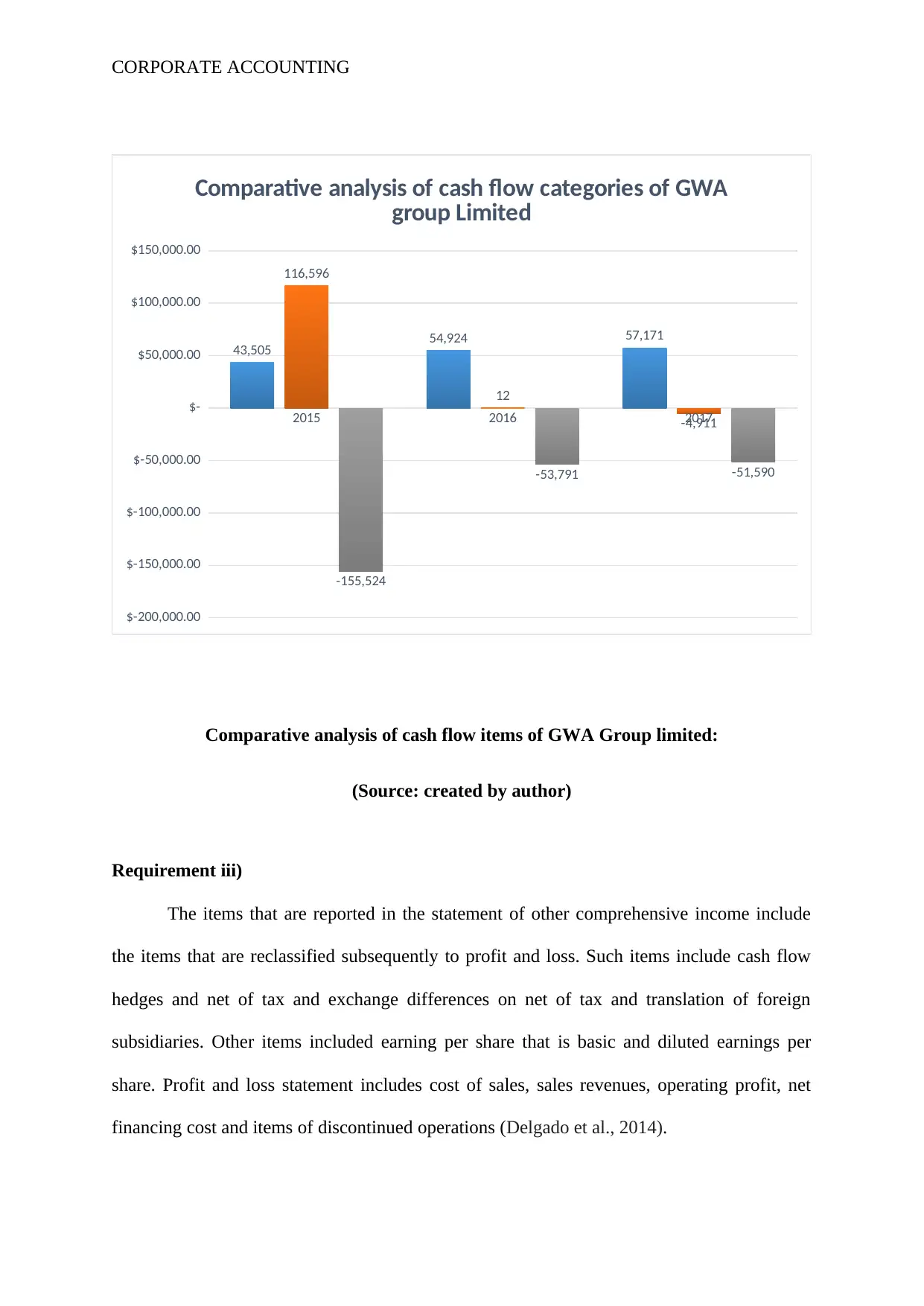

Comparative analysis of cash flow categories of GWA

group Limited

Comparative analysis of cash flow items of GWA Group limited:

(Source: created by author)

Requirement iii)

The items that are reported in the statement of other comprehensive income include

the items that are reclassified subsequently to profit and loss. Such items include cash flow

hedges and net of tax and exchange differences on net of tax and translation of foreign

subsidiaries. Other items included earning per share that is basic and diluted earnings per

share. Profit and loss statement includes cost of sales, sales revenues, operating profit, net

financing cost and items of discontinued operations (Delgado et al., 2014).

2015 2016 2017

$-200,000.00

$-150,000.00

$-100,000.00

$-50,000.00

$-

$50,000.00

$100,000.00

$150,000.00

43,505 54,924 57,171

116,596

12

-4,911

-155,524

-53,791 -51,590

Comparative analysis of cash flow categories of GWA

group Limited

Comparative analysis of cash flow items of GWA Group limited:

(Source: created by author)

Requirement iii)

The items that are reported in the statement of other comprehensive income include

the items that are reclassified subsequently to profit and loss. Such items include cash flow

hedges and net of tax and exchange differences on net of tax and translation of foreign

subsidiaries. Other items included earning per share that is basic and diluted earnings per

share. Profit and loss statement includes cost of sales, sales revenues, operating profit, net

financing cost and items of discontinued operations (Delgado et al., 2014).

CORPORATE ACCOUNTING

Requirement iv)

Difference sin exchange rate is the difference that results from translation of given

number of one unit of currency to another currency at different exchange rate. Organizations

having foreign operations such as associate, subsidiary, brand and joint venture are exposed

to fluctuations from foreign exchange rate (Hopper & Bui, 2016).

A cash flow hedging is hedging against the exposure of any variation in cash flow of

specific liabilities or assets attributable from particular level of risks. It is a strategy that is

used by organization for hedging to eliminate the risks that arises from change in cash flow.

Earnings per share of organization that is the proportion of the profits that is

attributable to the shareholders of company. It is obtained by deducting net income from

preferred stock to the total numbers of outstanding shares (Hopper & Bui, 2016).

Requirement v)

The reason why the items of other comprehensive income are not recorded in the

profit and loss statement because it contains some of the items that does not impact the

dividend payment of shareholders of company and therefore, there should be a separate

presentation in the statement of profit and loss. Items such as cash flow hedges and exchange

rate differences on foreign subsidiaries translation and net of taxes do not have a direct

impact in the wealth of shareholders. They are kept aside by companies in the form of

reserves so that they can be used for specific purposes. For instance, the gain or loss that

arises from the revaluation of assets is treated separately. Moreover, any loss or gain resulting

from impairment of assets is also included in the other comprehensive income (Harakeh et

al., 2016). Such item does not impact the dividend payment to shareholders directly. On other

hand, the items reported in the profit and loss statement have a direct impact on the dividend

amount that is distributed to shareholders. However, organization can keep the amount of

Requirement iv)

Difference sin exchange rate is the difference that results from translation of given

number of one unit of currency to another currency at different exchange rate. Organizations

having foreign operations such as associate, subsidiary, brand and joint venture are exposed

to fluctuations from foreign exchange rate (Hopper & Bui, 2016).

A cash flow hedging is hedging against the exposure of any variation in cash flow of

specific liabilities or assets attributable from particular level of risks. It is a strategy that is

used by organization for hedging to eliminate the risks that arises from change in cash flow.

Earnings per share of organization that is the proportion of the profits that is

attributable to the shareholders of company. It is obtained by deducting net income from

preferred stock to the total numbers of outstanding shares (Hopper & Bui, 2016).

Requirement v)

The reason why the items of other comprehensive income are not recorded in the

profit and loss statement because it contains some of the items that does not impact the

dividend payment of shareholders of company and therefore, there should be a separate

presentation in the statement of profit and loss. Items such as cash flow hedges and exchange

rate differences on foreign subsidiaries translation and net of taxes do not have a direct

impact in the wealth of shareholders. They are kept aside by companies in the form of

reserves so that they can be used for specific purposes. For instance, the gain or loss that

arises from the revaluation of assets is treated separately. Moreover, any loss or gain resulting

from impairment of assets is also included in the other comprehensive income (Harakeh et

al., 2016). Such item does not impact the dividend payment to shareholders directly. On other

hand, the items reported in the profit and loss statement have a direct impact on the dividend

amount that is distributed to shareholders. However, organization can keep the amount of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

profit aside in the form of retained earnings for repayment in the business and such amount is

not attributable to dividend payment to shareholders.

Requirement vi)

The income tax expense recorded by GWA Group limited in financial year 2017 and

2016 stood at $ 21585 and $ 19837. It is indicated by the figures that there is reduction in

total amount of income tax expense incurred by organization. Income tax expense on other

hand in year 2015 stood at $ 3544 (Gwagroup.com.au, 2018). Therefore, there is consistent

increase in total amount of income tax expenses incurred.

Requirement vii)

The accounting income generated by GWA Group limited is recorded at $ 75256 and

$ 71757 for financial year 2017 and 2016. Applicable income tax rate for the corporation is

30%. Therefore, the accounting income times the tax rate of company is recorded at (30% of

$ 75256) = 22576.8 and (30% of 71757) = 21527.1 for both the financial year 2017 and 2016

respectively. The amount of income tax expense recorded by GWA Group limited in

financial year 2017 and 2016 stood at $ 21585 and $ 19837 (Gwagroup.com.au, 2018). It can

be seen from the figures that there is considerable difference between the amount of

accounting income taxation rate and the income tax expense incurred by company. The

reason for difference between the income tax expense and the accounting income is that the

computation of both the figures has been done ob different method. The income tax expense

incurred by organization is based on the taxation rule compared to accounting income

computation that is based on accounting rule (Cao et al., 2015). Therefore, the difference in

method of computation of accounting income and taxable income is the contributing factor

for creating difference between the values of income tax expense and accounting income.

profit aside in the form of retained earnings for repayment in the business and such amount is

not attributable to dividend payment to shareholders.

Requirement vi)

The income tax expense recorded by GWA Group limited in financial year 2017 and

2016 stood at $ 21585 and $ 19837. It is indicated by the figures that there is reduction in

total amount of income tax expense incurred by organization. Income tax expense on other

hand in year 2015 stood at $ 3544 (Gwagroup.com.au, 2018). Therefore, there is consistent

increase in total amount of income tax expenses incurred.

Requirement vii)

The accounting income generated by GWA Group limited is recorded at $ 75256 and

$ 71757 for financial year 2017 and 2016. Applicable income tax rate for the corporation is

30%. Therefore, the accounting income times the tax rate of company is recorded at (30% of

$ 75256) = 22576.8 and (30% of 71757) = 21527.1 for both the financial year 2017 and 2016

respectively. The amount of income tax expense recorded by GWA Group limited in

financial year 2017 and 2016 stood at $ 21585 and $ 19837 (Gwagroup.com.au, 2018). It can

be seen from the figures that there is considerable difference between the amount of

accounting income taxation rate and the income tax expense incurred by company. The

reason for difference between the income tax expense and the accounting income is that the

computation of both the figures has been done ob different method. The income tax expense

incurred by organization is based on the taxation rule compared to accounting income

computation that is based on accounting rule (Cao et al., 2015). Therefore, the difference in

method of computation of accounting income and taxable income is the contributing factor

for creating difference between the values of income tax expense and accounting income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Requirement viii)

From the annual report, it can be seen that the company has not recorded any amount

of deferred tax liabilities in the current reporting year. On other hand, the amount of deferred

tax assets that is recorded in the balance sheet under section noncurrent assets stood at $

16023 in year 2017 compared to $ 18189 in year 2016 respectively. Total amount of deferred

tax assets recorded by GWA Group in year 2015 stood at $ 22103. It is suggested by the

figures that there is considerable decline in the amount of net deferred assets recorded in the

statement of financial position of company. On other hand, a deferred tax expense of amount

$ 1222 is recorded in year 2017 compared to $ 5120 in year 2016 respectively

(Gwagroup.com.au, 2018).

Organization offsets the amount of deferred tax assets and liabilities reported if there

is right that is legally enforced for offsetting current tax liabilities sand current tax assets.

Such offsetting is attributable to the tax that is levied by the income taxation authority. In

addition to this, it helps in settling of current tax liabilities and assets on net basis that will be

realized simultaneously (Petty et al. 2015).

The reason why the deferred tax assets are recognized is attributable to deductible

temporary differences relating to tax credits and unused tax losses. Recognition of deferred

tax assets are done to the extent that there will be availability of future taxable profits so that

they can be utilized. At each reporting date, the management of organization conducts

reviewing of deferred tax assets and the amount of such assets are reduced to the extent that it

is no longer possible to realize the benefits related to taxation. Recording of deferred tax

assets in the statement of financial position is because of the consequence of deferred tax that

are based on temporary difference between the expenses and revenue recorded resulting from

Requirement viii)

From the annual report, it can be seen that the company has not recorded any amount

of deferred tax liabilities in the current reporting year. On other hand, the amount of deferred

tax assets that is recorded in the balance sheet under section noncurrent assets stood at $

16023 in year 2017 compared to $ 18189 in year 2016 respectively. Total amount of deferred

tax assets recorded by GWA Group in year 2015 stood at $ 22103. It is suggested by the

figures that there is considerable decline in the amount of net deferred assets recorded in the

statement of financial position of company. On other hand, a deferred tax expense of amount

$ 1222 is recorded in year 2017 compared to $ 5120 in year 2016 respectively

(Gwagroup.com.au, 2018).

Organization offsets the amount of deferred tax assets and liabilities reported if there

is right that is legally enforced for offsetting current tax liabilities sand current tax assets.

Such offsetting is attributable to the tax that is levied by the income taxation authority. In

addition to this, it helps in settling of current tax liabilities and assets on net basis that will be

realized simultaneously (Petty et al. 2015).

The reason why the deferred tax assets are recognized is attributable to deductible

temporary differences relating to tax credits and unused tax losses. Recognition of deferred

tax assets are done to the extent that there will be availability of future taxable profits so that

they can be utilized. At each reporting date, the management of organization conducts

reviewing of deferred tax assets and the amount of such assets are reduced to the extent that it

is no longer possible to realize the benefits related to taxation. Recording of deferred tax

assets in the statement of financial position is because of the consequence of deferred tax that

are based on temporary difference between the expenses and revenue recorded resulting from

CORPORATE ACCOUNTING

accounting return and taxation return. Deferred taxes can be recorded for deferrals for either

tax payable and tax expenses that leads to the generation of tax liabilities and tax assets on

balance sheet (Grubert & Altshuler, 2016).

There is significant difference between the taxable profit and accounting profit due to

the existence of some items that are allowed or disallowed for purpose of taxation. Such

difference between the taxable income and accounting income is attributable to timing

differences (Bens et al., 2018).

Requirement ix)

Yes, GWA Group limited has recorded deferred tax assets under the heading

noncurrent assets and income tax payable under the heading current liabilities. Total amount

of deferred tax assets recorded by organization in year 2017 and 2016 is recorded at $ 16023

and $ 18189. On other hand, amount of income tax payable recorded by company stood at $

1851 and $ 7346 for financial year 2016 and 2017 respectively.

Requirement x)

The total amount of income tax paid as depicted in the cash flow statement of GWA

group limited stood at $ 19536 in year 2016 compared to $ 14788 in year 2017 indicating that

there has been decline in total amount of income tax paid by organization. The income tax

expense recorded by GWA Group limited in financial year 2017 and 2016 stood at $ 21585

and $ 19837. It is depicted from the figures that there exist difference between the amount of

income tax paid and amount of income tax expenses incurred. Income tax expense amount is

more than the amount of income tax paid as in the usual scenario. This difference in reported

figures is because of method applied for computing both the figures that involves taxation

rule and accounting rule (Acosta et al. 2017).

accounting return and taxation return. Deferred taxes can be recorded for deferrals for either

tax payable and tax expenses that leads to the generation of tax liabilities and tax assets on

balance sheet (Grubert & Altshuler, 2016).

There is significant difference between the taxable profit and accounting profit due to

the existence of some items that are allowed or disallowed for purpose of taxation. Such

difference between the taxable income and accounting income is attributable to timing

differences (Bens et al., 2018).

Requirement ix)

Yes, GWA Group limited has recorded deferred tax assets under the heading

noncurrent assets and income tax payable under the heading current liabilities. Total amount

of deferred tax assets recorded by organization in year 2017 and 2016 is recorded at $ 16023

and $ 18189. On other hand, amount of income tax payable recorded by company stood at $

1851 and $ 7346 for financial year 2016 and 2017 respectively.

Requirement x)

The total amount of income tax paid as depicted in the cash flow statement of GWA

group limited stood at $ 19536 in year 2016 compared to $ 14788 in year 2017 indicating that

there has been decline in total amount of income tax paid by organization. The income tax

expense recorded by GWA Group limited in financial year 2017 and 2016 stood at $ 21585

and $ 19837. It is depicted from the figures that there exist difference between the amount of

income tax paid and amount of income tax expenses incurred. Income tax expense amount is

more than the amount of income tax paid as in the usual scenario. This difference in reported

figures is because of method applied for computing both the figures that involves taxation

rule and accounting rule (Acosta et al. 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Requirement xi)

Analysis of annual report of GWA group limited is illustrative of the fact that the

there is a detailed disclosure of tax treatment by organization which is relevant to the users of

financial statements. There is appropriate segmentation of different items of taxation such as

income tax expense, income tax paid, income tax payable, deferred tax assets and deferred

tax liabilities if reported by organization during a particular reporting period. Notes to

financial statement provide a detailed disclosure of the methods that is used by organization

for computing the taxation elements. Furthermore, there is separate section of deferred tax

liabilities and deferred tax assets that explains in details about the occurrence of such items

and the factors that attributes to it. Sensitivity analysis takes into account the factors related to

taxes. Each and every items relating to treatment of tax is explained in detail for which it will

make users understand the several adjustments. Such explanation is quite an interesting fact

for the financial statement users who are interested in making investment in that particular

organization (Petty et al., 2015).

Requirement xi)

Analysis of annual report of GWA group limited is illustrative of the fact that the

there is a detailed disclosure of tax treatment by organization which is relevant to the users of

financial statements. There is appropriate segmentation of different items of taxation such as

income tax expense, income tax paid, income tax payable, deferred tax assets and deferred

tax liabilities if reported by organization during a particular reporting period. Notes to

financial statement provide a detailed disclosure of the methods that is used by organization

for computing the taxation elements. Furthermore, there is separate section of deferred tax

liabilities and deferred tax assets that explains in details about the occurrence of such items

and the factors that attributes to it. Sensitivity analysis takes into account the factors related to

taxes. Each and every items relating to treatment of tax is explained in detail for which it will

make users understand the several adjustments. Such explanation is quite an interesting fact

for the financial statement users who are interested in making investment in that particular

organization (Petty et al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

References list:

Acosta-González, E., Fernández-Rodríguez, F. and Ganga, H., 2017. Predicting Corporate

Financial Failure Using Macroeconomic Variables and Accounting

Data. Computational Economics, pp.1-31.

Balakrishnan, K., Blouin, J., & Guay, W. (2018). Tax Aggressiveness and Corporate

Transparency. The Accounting Review.

Bens, D.A., Monahan, S.J. and Steele, L.B., 2018. The Effect of Aggregation of Accounting

Information via Segment Reporting on Accounting Conservatism. European

Accounting Review, 27(2), pp.237-262.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Delgado, F. J., Fernandez-Rodriguez, E., & Martinez-Arias, A. (2014). Effective tax rates in

corporate taxation: A quantile regression for the EU. Engineering Economics, 25(5),

487-496.

Gitman, L. J., Joehnk, M. D., Smart, S., & Juchau, R. H. (2015). Fundamentals of investing.

Pearson Higher Education AU.

Grubert, H., & Altshuler, R. (2016). Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Guenther, E., Jasch, C., Schmidt, M., Wagner, B., & Ilg, P. (2015). Material flow cost

accounting–looking back and ahead.

References list:

Acosta-González, E., Fernández-Rodríguez, F. and Ganga, H., 2017. Predicting Corporate

Financial Failure Using Macroeconomic Variables and Accounting

Data. Computational Economics, pp.1-31.

Balakrishnan, K., Blouin, J., & Guay, W. (2018). Tax Aggressiveness and Corporate

Transparency. The Accounting Review.

Bens, D.A., Monahan, S.J. and Steele, L.B., 2018. The Effect of Aggregation of Accounting

Information via Segment Reporting on Accounting Conservatism. European

Accounting Review, 27(2), pp.237-262.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Delgado, F. J., Fernandez-Rodriguez, E., & Martinez-Arias, A. (2014). Effective tax rates in

corporate taxation: A quantile regression for the EU. Engineering Economics, 25(5),

487-496.

Gitman, L. J., Joehnk, M. D., Smart, S., & Juchau, R. H. (2015). Fundamentals of investing.

Pearson Higher Education AU.

Grubert, H., & Altshuler, R. (2016). Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Guenther, E., Jasch, C., Schmidt, M., Wagner, B., & Ilg, P. (2015). Material flow cost

accounting–looking back and ahead.

CORPORATE ACCOUNTING

Gwagroup.com.au. (2018). [online] Available at:

http://www.gwagroup.com.au/wp-content/uploads/Annual-Report-2017-1.pdf

[Accessed 25 May 2018].

Harakeh, M., Lee, E., & Walker, M. (2016). Does Changing Accounting Standards Affect

Dividend Policy?.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hopper, T., & Bui, B. (2016). Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag

GmbH.

Li, Z., Wang, L., & Wruck, K. H. (2018). Accounting-Based Compensation and Debt

Contracts.

Petty, J. W., Titman, S., Keown, A. J., Martin, P., Martin, J. D., & Burrow, M.

(2015). Financial management: Principles and applications. Pearson Higher

Education AU.

Gwagroup.com.au. (2018). [online] Available at:

http://www.gwagroup.com.au/wp-content/uploads/Annual-Report-2017-1.pdf

[Accessed 25 May 2018].

Harakeh, M., Lee, E., & Walker, M. (2016). Does Changing Accounting Standards Affect

Dividend Policy?.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hopper, T., & Bui, B. (2016). Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag

GmbH.

Li, Z., Wang, L., & Wruck, K. H. (2018). Accounting-Based Compensation and Debt

Contracts.

Petty, J. W., Titman, S., Keown, A. J., Martin, P., Martin, J. D., & Burrow, M.

(2015). Financial management: Principles and applications. Pearson Higher

Education AU.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.