Corporate Accounting Analysis: HI5020 Report on Healthcare Firms

VerifiedAdded on 2023/06/04

|32

|4575

|494

Report

AI Summary

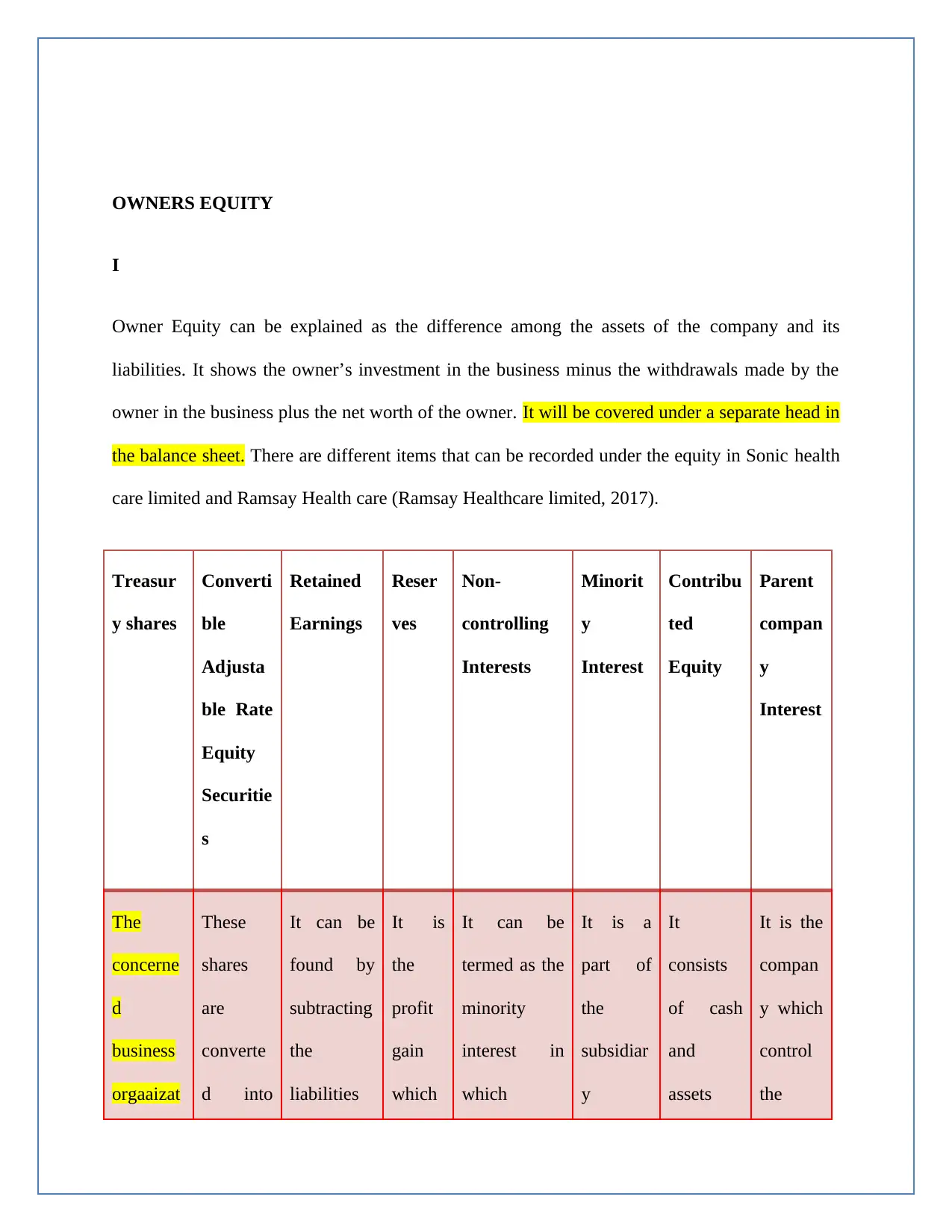

This report presents a comprehensive analysis of corporate accounting practices, focusing on two publicly listed healthcare companies, RHC Ramsay Health Care and SHL Sonic Healthcare Limited. The report delves into key financial aspects, including owner's equity, examining the components and trends over a three-year period (2015-2017). It scrutinizes cash flow statements, differentiating between operating, investing, and financing activities to assess the companies' financial performance. The analysis further extends to other comprehensive income statements and accounting for corporate income tax. A comparative analysis is conducted on debt and equity ratios to evaluate the financial structure of both companies. The report utilizes financial statements to understand revenue, expenses, and tax rates, providing a thorough examination of the companies' financial health and operational strategies. It also includes an introduction to the companies, highlighting their business operations and market positions, and concludes with a summary of the key findings.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.