Accounting Theory and Current Issues Tutorial Questions - HI6025

VerifiedAdded on 2022/12/27

|9

|1666

|75

Homework Assignment

AI Summary

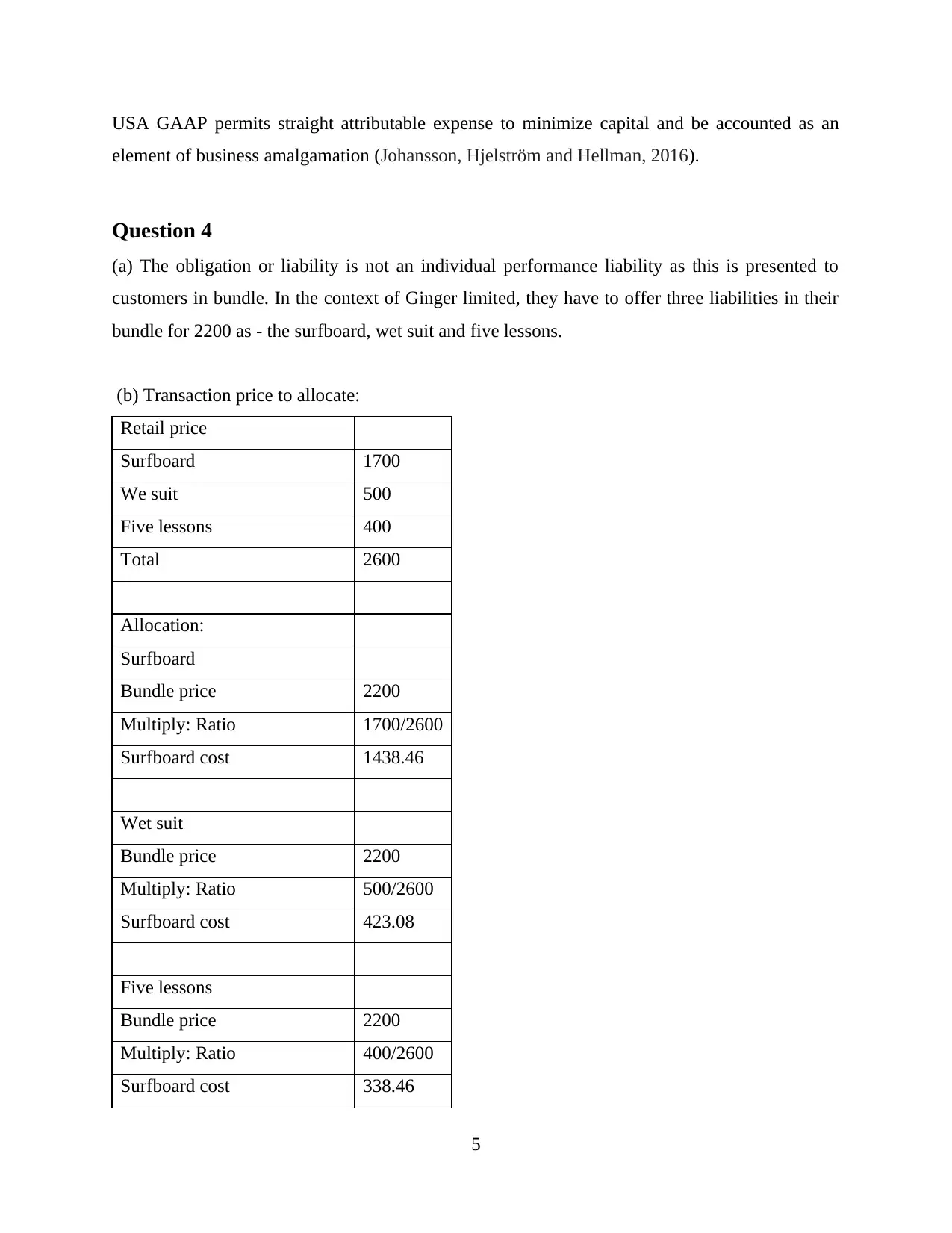

This document presents a comprehensive solution to a set of tutorial questions from the HI6025 Accounting Theory and Current Issues unit. The solution addresses key concepts in accounting theory, including the primary users of financial reports and the application of accounting standards. It analyzes topics like asset revaluation, goodwill, and the implications of IFRS 3. Furthermore, the solution delves into the specifics of IAS 16 regarding property, plant, and equipment (PP&E), covering recognition, initial measurement, and different accounting models. The assignment also explores corporate social responsibility (CSR) and its connection to accountability and accounting practices, providing a well-rounded understanding of the topics covered in the unit. References to relevant academic sources are also provided.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.