HI6025 - Analyzing the Impact of IFRS on Asset/Liability Reporting

VerifiedAdded on 2024/06/03

|13

|2583

|266

Report

AI Summary

This report examines the changes in asset and liability reporting following the adoption of International Financial Reporting Standards (IFRS), focusing on the Australian context. It contrasts financial reports before and after IFRS adoption, using Woolworths as a case study to illustrate the impact on long-term capital items, depreciation, revenue recognition, employee benefits, and borrowing costs. The report highlights how IFRS implementation has led to increased liabilities, decreased surplus profits, and a more accurate depreciation accounting. Ultimately, the adoption of IFRS has enhanced the comparability of financial reporting among Australian enterprises and improved investor confidence, leading to more informed financial decision-making.

HI6025 Accounting Theory and Current

Issues

1

Issues

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary:

The following report related with accounting is concerned with identifying various changes that

have occurred in reporting assets and liabilities together with the effects identified in different

kinds of revenues and expenses reported by the company in its financial statements. The effect of

various accounting policies that have affected the financial statements after adopting

International financial reporting Framework ill be analysed and the observations will then be

conceptualized with one of the Australian Company. The various type of accounting issues

which have been major issue of concern after adoption of IFRs will be discussed in this report.

The preparation of this type of report will help the users in getting advance knowledge about the

accounting work to be performed in modern scenario. Also the changes in accounting framework

will be critically evaluated in this report in order to perform the operations effectively and

efficiently.

2

The following report related with accounting is concerned with identifying various changes that

have occurred in reporting assets and liabilities together with the effects identified in different

kinds of revenues and expenses reported by the company in its financial statements. The effect of

various accounting policies that have affected the financial statements after adopting

International financial reporting Framework ill be analysed and the observations will then be

conceptualized with one of the Australian Company. The various type of accounting issues

which have been major issue of concern after adoption of IFRs will be discussed in this report.

The preparation of this type of report will help the users in getting advance knowledge about the

accounting work to be performed in modern scenario. Also the changes in accounting framework

will be critically evaluated in this report in order to perform the operations effectively and

efficiently.

2

Contents

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................4

Content:............................................................................................................................................5

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

3

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................4

Content:............................................................................................................................................5

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

The main purpose of the report prepared in accordance with the accounting framework is to

explain the impact of various types of accounting issues in Australian context. For fulfilling this

purpose the annual reports of the company related with the prior period before adoption of IFRS

will be differentiated with the reports prepared after adoption of IFRS. The changes in different

accounting policies along with the results obtained will be described in this report. A power point

presentation will be prepared in this report in order to demonstrate the understanding of users

regarding the different issues faced in accounting after adoption of IFRS. The information about

all these concepts and procedures will help the company and the management in dealing with

financial problems accurately.

4

The main purpose of the report prepared in accordance with the accounting framework is to

explain the impact of various types of accounting issues in Australian context. For fulfilling this

purpose the annual reports of the company related with the prior period before adoption of IFRS

will be differentiated with the reports prepared after adoption of IFRS. The changes in different

accounting policies along with the results obtained will be described in this report. A power point

presentation will be prepared in this report in order to demonstrate the understanding of users

regarding the different issues faced in accounting after adoption of IFRS. The information about

all these concepts and procedures will help the company and the management in dealing with

financial problems accurately.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Content:

It can be established that during the face of 1990’s and before the adoption of International

Financial Reporting Standards in accounting framework there were no set of guidelines available

for conducting the work of accounting in international business. The lack of tools for

differentiating between various companies all across the world as resulting in inefficiencies to

improve the business operations of company. There were only selected rules and framework

associated with conducting the accounting work in a company. In consideration of this fact there

was required a proper set of framework of accountings standards to be followed by the

enterprises in order to bring comparability between various enterprises form different countries.

The comparability recognized in operational performance will help the company in presenting

the more accurate and useful information for the shareholders and other investors concerned.

However there did already exist some of the standards which needs to be optimized of the

purpose of reporting fairly in the financial statement of company (Morris, 2017)..

Late in the year 2004, there was a necessity to adopt the IFRS in the accounting framework and

Australia became the first and foremost country to adopt and implement the International

Financial Reporting standards in preparing the accounting records for local and other

government authorities. However the full applicability along with the compliances was executed

in 2005 – 2006. After the adoption of IFRS in Australia there were general public debate arsing

in Australia regarding the behavioural implications associate with this type of framework. Te

adoption of IFRS in international accounting and the work related with accounting in Australia

will largely impact the accounting work quality and financial performance of company

(Sudaryanti, et. al., 2015). The implication of necessary standards to be adopted and followed by

the enterprise will help in improving the quality of reporting associate with financial statements.

In context if the various accounting bodies as presented by the accounting standards board the

adoption of IFRs has resulted in bringing transparency among the different type of reporting

globally. It was observed that the profit making companies of Australia together with the

government entities were uncertain about the impact that the adoption of IFRS will have on

financial reporting. The general phenomenon was associated with positive impact of IFRS that

5

It can be established that during the face of 1990’s and before the adoption of International

Financial Reporting Standards in accounting framework there were no set of guidelines available

for conducting the work of accounting in international business. The lack of tools for

differentiating between various companies all across the world as resulting in inefficiencies to

improve the business operations of company. There were only selected rules and framework

associated with conducting the accounting work in a company. In consideration of this fact there

was required a proper set of framework of accountings standards to be followed by the

enterprises in order to bring comparability between various enterprises form different countries.

The comparability recognized in operational performance will help the company in presenting

the more accurate and useful information for the shareholders and other investors concerned.

However there did already exist some of the standards which needs to be optimized of the

purpose of reporting fairly in the financial statement of company (Morris, 2017)..

Late in the year 2004, there was a necessity to adopt the IFRS in the accounting framework and

Australia became the first and foremost country to adopt and implement the International

Financial Reporting standards in preparing the accounting records for local and other

government authorities. However the full applicability along with the compliances was executed

in 2005 – 2006. After the adoption of IFRS in Australia there were general public debate arsing

in Australia regarding the behavioural implications associate with this type of framework. Te

adoption of IFRS in international accounting and the work related with accounting in Australia

will largely impact the accounting work quality and financial performance of company

(Sudaryanti, et. al., 2015). The implication of necessary standards to be adopted and followed by

the enterprise will help in improving the quality of reporting associate with financial statements.

In context if the various accounting bodies as presented by the accounting standards board the

adoption of IFRs has resulted in bringing transparency among the different type of reporting

globally. It was observed that the profit making companies of Australia together with the

government entities were uncertain about the impact that the adoption of IFRS will have on

financial reporting. The general phenomenon was associated with positive impact of IFRS that

5

will result in more accurate comparability of accounting records of different entities

internationally and globally.

It was established that there were certain types of debate arsing form the adoption of IFRS in

international accounting and by the Australian entities and the same were associate with

recognizing the effect with which it is operating in the corporate entities. However it was

concluded that the framework of accounting resulted in increase in the liabilities reported by the

company, minimizing the equity proportion of company as reported in the balance sheet of

company and the companies were recognizing the significant decrease in the surplus maintained

by the company after its adoption. The recent researches related to the recognition of the impact

of IFRs on corporate reporting shows that the positive relationship exists between the net profit

obtained by the company together with the market value of the share price of company and the

impact of IFRS (Morris, 2017).. However there exists some of the cases where negative impact

associated with this kind of adoption are demonstrated. In order to evaluate and analyse the

impact created by implementation of IFRS in Australian accounting there has been chosen some

of the surplus along with the losses, assets, equity and other financial items of the enterprise and

the changes in these items before and after adoption of IFRS will be analysed for the purpose of

obtaining the evidences. The various indicators that will support the conclusion will be

accumulated and recorded for the purpose of analysing the impact of the accounting framework.

The adoption of the concerned accounting framework have significantly affected the treatment of

various issues elated with the accounting work to be performed for property, plant and

equipments and other items of asset recognition. The accounting policies related with

depreciation recognition and measurement policy have been improvised for the company and the

identification and recognition of intangible assets and other liabilities of company have changed

after its adoption. The various types of comparison between the accounting standards and the

compliance framework will help the company in improving the accounting work performed

(Sudaryanti, et. al., 2015).

For the purpose of recognizing the differences among the treatment of accounting work before

and after adoption of IFRS a company has been chosen and the financial rep[orts prepared by the

company before the adoption of IFRS will be compared with the treatment of financial items

after adoption of IFRS. This will help in recognizing the effects associated with accounting

6

internationally and globally.

It was established that there were certain types of debate arsing form the adoption of IFRS in

international accounting and by the Australian entities and the same were associate with

recognizing the effect with which it is operating in the corporate entities. However it was

concluded that the framework of accounting resulted in increase in the liabilities reported by the

company, minimizing the equity proportion of company as reported in the balance sheet of

company and the companies were recognizing the significant decrease in the surplus maintained

by the company after its adoption. The recent researches related to the recognition of the impact

of IFRs on corporate reporting shows that the positive relationship exists between the net profit

obtained by the company together with the market value of the share price of company and the

impact of IFRS (Morris, 2017).. However there exists some of the cases where negative impact

associated with this kind of adoption are demonstrated. In order to evaluate and analyse the

impact created by implementation of IFRS in Australian accounting there has been chosen some

of the surplus along with the losses, assets, equity and other financial items of the enterprise and

the changes in these items before and after adoption of IFRS will be analysed for the purpose of

obtaining the evidences. The various indicators that will support the conclusion will be

accumulated and recorded for the purpose of analysing the impact of the accounting framework.

The adoption of the concerned accounting framework have significantly affected the treatment of

various issues elated with the accounting work to be performed for property, plant and

equipments and other items of asset recognition. The accounting policies related with

depreciation recognition and measurement policy have been improvised for the company and the

identification and recognition of intangible assets and other liabilities of company have changed

after its adoption. The various types of comparison between the accounting standards and the

compliance framework will help the company in improving the accounting work performed

(Sudaryanti, et. al., 2015).

For the purpose of recognizing the differences among the treatment of accounting work before

and after adoption of IFRS a company has been chosen and the financial rep[orts prepared by the

company before the adoption of IFRS will be compared with the treatment of financial items

after adoption of IFRS. This will help in recognizing the effects associated with accounting

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

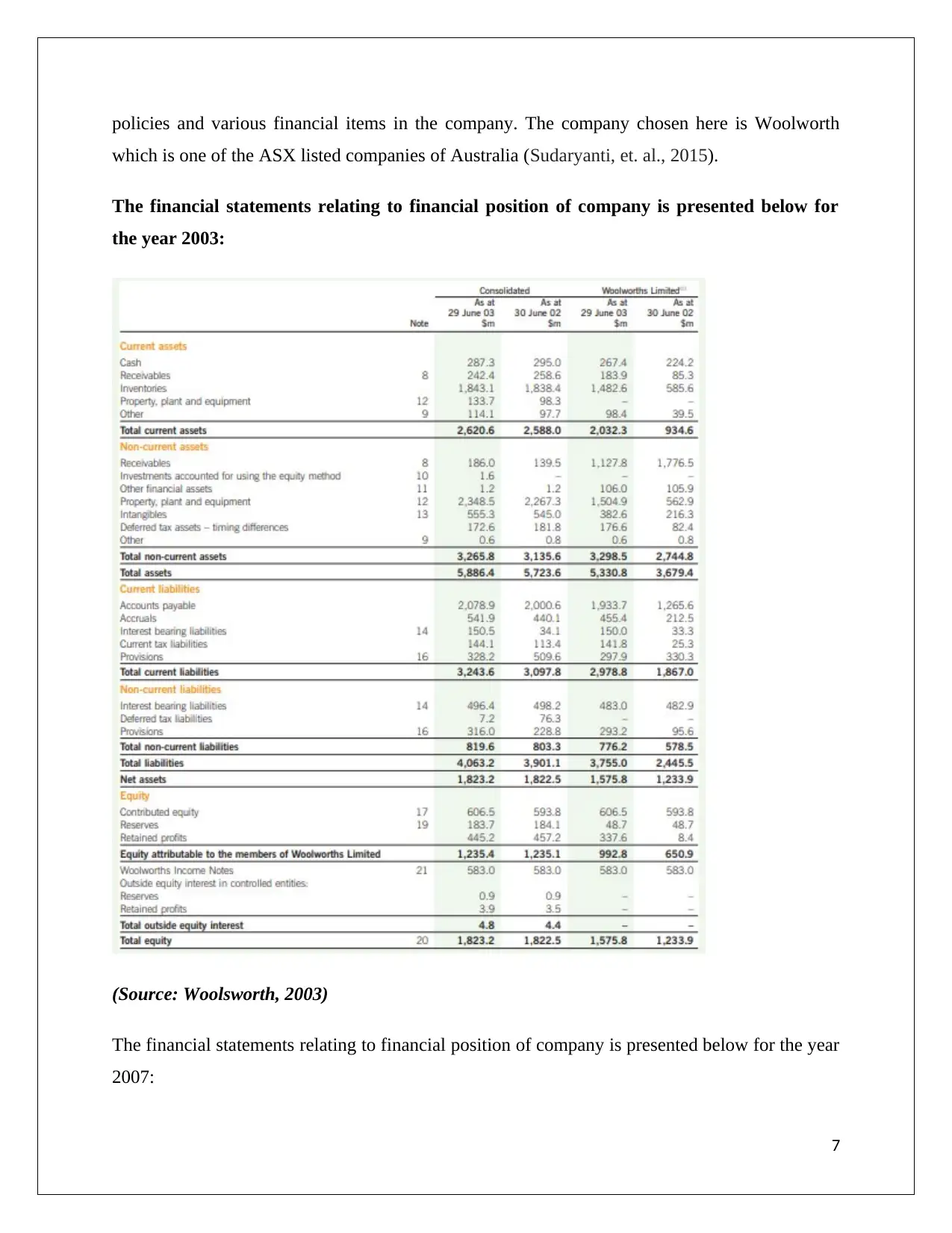

policies and various financial items in the company. The company chosen here is Woolworth

which is one of the ASX listed companies of Australia (Sudaryanti, et. al., 2015).

The financial statements relating to financial position of company is presented below for

the year 2003:

(Source: Woolsworth, 2003)

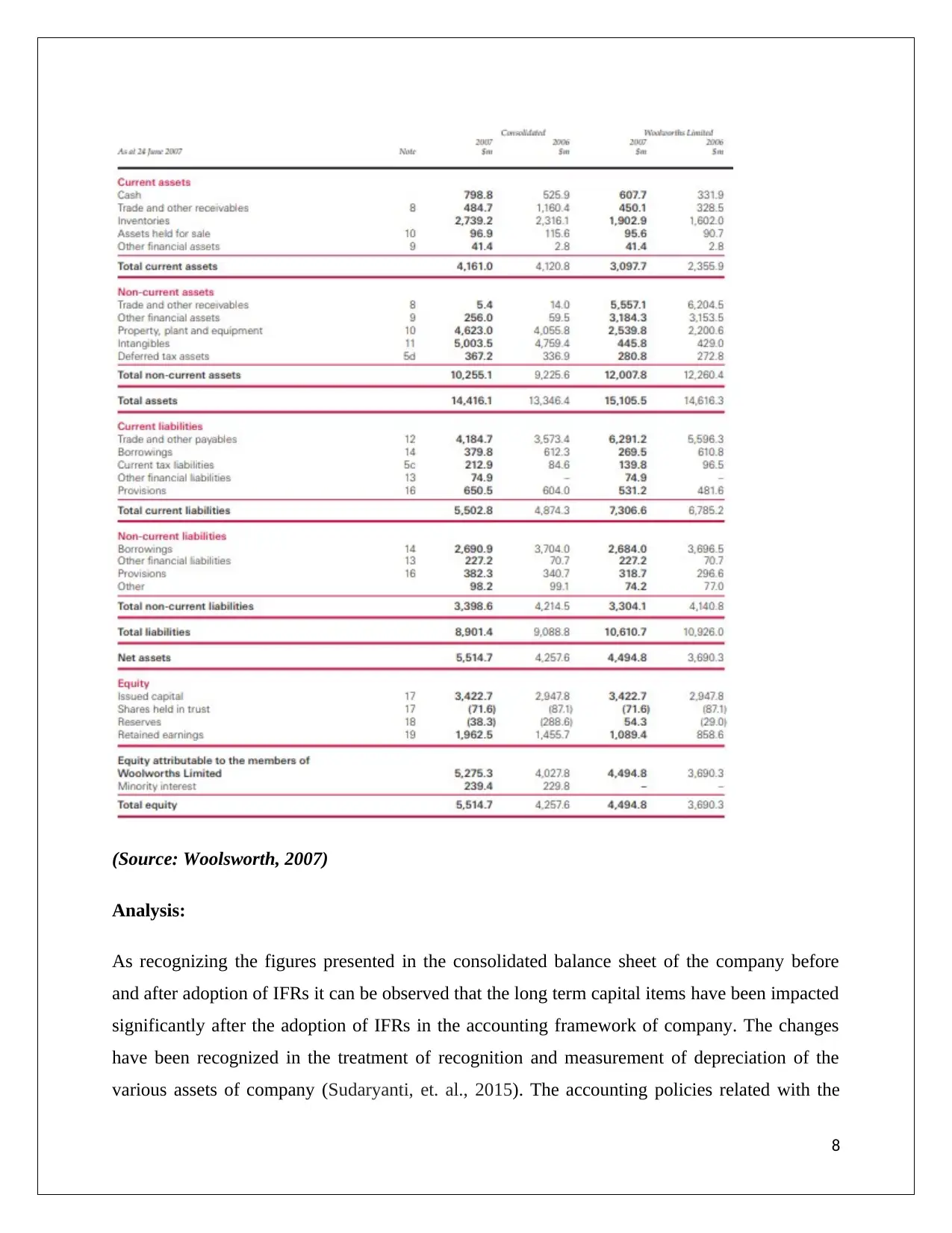

The financial statements relating to financial position of company is presented below for the year

2007:

7

which is one of the ASX listed companies of Australia (Sudaryanti, et. al., 2015).

The financial statements relating to financial position of company is presented below for

the year 2003:

(Source: Woolsworth, 2003)

The financial statements relating to financial position of company is presented below for the year

2007:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Woolsworth, 2007)

Analysis:

As recognizing the figures presented in the consolidated balance sheet of the company before

and after adoption of IFRs it can be observed that the long term capital items have been impacted

significantly after the adoption of IFRs in the accounting framework of company. The changes

have been recognized in the treatment of recognition and measurement of depreciation of the

various assets of company (Sudaryanti, et. al., 2015). The accounting policies related with the

8

Analysis:

As recognizing the figures presented in the consolidated balance sheet of the company before

and after adoption of IFRs it can be observed that the long term capital items have been impacted

significantly after the adoption of IFRs in the accounting framework of company. The changes

have been recognized in the treatment of recognition and measurement of depreciation of the

various assets of company (Sudaryanti, et. al., 2015). The accounting policies related with the

8

recognition and identification of various types of revenues, employee benefits, borrowing costs

and net gain or loss associated with the property, plant and equipment have changed during the

adoption of accounting policies as per IFRS (Kraft & Landsman, 2017). The recognition of

various standards associated with depreciation in the company has resulted in decrease in the

written down value of assets recognized by the company during the year. The treatments of

segmental profits and controlling interest associated with the segmental profits have changed

during this period. The accountings standards include the Australian equivalents to IFRS. Also

the compliances associated with AIFRS ensures that the various financial statement along with

the notes to accounts have been prepared in accordance with the International Financial reporting

Standards. AASB 2007-1 Amendments to Australian Accounting Standards arising from AASB

explanation 11 amends AASB 2 Share-based expenditure to insert the halfway provisions of

IFRS 2, previously contained in AASB 1 First-time Adoption of Australian Equivalents to

International Financial Reporting Standards. AASB 2007-1 is applicable for annual reporting

periods beginning on or after 1 March 2007.

It can be observed tat the earnings management has remained stable for a long period of time

after the transition towards IFRS in respect of the accounting framework. However despite the

potential associated with high volatility tie b recognized in IFRS the earnings have remained

more persistent. It can be recognized that the adoption of IFRS and the concept of goodwill

impairment have resulted in more informed and accurate decision making regarding the

investment to be made in company and the users have became more reliant on financial records.

It has also been observed that after the adoption of IFRS there was a slight increase in the ability

of the accounting numbers and numerical to explain the variations associated with prices of

shares (Bryce, et. al., 2015).

The various other items which have been impacted significantly after the adoption of IFRS are as

under:

Employee benefits – The new accounting standard as suggested and employed by the

enterprise in their accounting framework have resulted in changes in recognition and

measurement of defined benefit obligation and other employee benefit expenses

9

and net gain or loss associated with the property, plant and equipment have changed during the

adoption of accounting policies as per IFRS (Kraft & Landsman, 2017). The recognition of

various standards associated with depreciation in the company has resulted in decrease in the

written down value of assets recognized by the company during the year. The treatments of

segmental profits and controlling interest associated with the segmental profits have changed

during this period. The accountings standards include the Australian equivalents to IFRS. Also

the compliances associated with AIFRS ensures that the various financial statement along with

the notes to accounts have been prepared in accordance with the International Financial reporting

Standards. AASB 2007-1 Amendments to Australian Accounting Standards arising from AASB

explanation 11 amends AASB 2 Share-based expenditure to insert the halfway provisions of

IFRS 2, previously contained in AASB 1 First-time Adoption of Australian Equivalents to

International Financial Reporting Standards. AASB 2007-1 is applicable for annual reporting

periods beginning on or after 1 March 2007.

It can be observed tat the earnings management has remained stable for a long period of time

after the transition towards IFRS in respect of the accounting framework. However despite the

potential associated with high volatility tie b recognized in IFRS the earnings have remained

more persistent. It can be recognized that the adoption of IFRS and the concept of goodwill

impairment have resulted in more informed and accurate decision making regarding the

investment to be made in company and the users have became more reliant on financial records.

It has also been observed that after the adoption of IFRS there was a slight increase in the ability

of the accounting numbers and numerical to explain the variations associated with prices of

shares (Bryce, et. al., 2015).

The various other items which have been impacted significantly after the adoption of IFRS are as

under:

Employee benefits – The new accounting standard as suggested and employed by the

enterprise in their accounting framework have resulted in changes in recognition and

measurement of defined benefit obligation and other employee benefit expenses

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

associated with the company. The impact of these policies on the financial statement can

be recognized appropriately by the enterprise.

Depreciation – Te accounting policy related to depreciating the value f different types of

assets in the company have resulted in changes in accumulating the depreciation expense

of the company. The method of applying the deprecation along with the depreciation

rates has changed and the companies are now adopting more relevant and reliable method

of charging depreciation that will result in accurate reporting (Kraft & Landsman, 2017).

Borrowing costs – The treatment of the borrowing cost is related to recognizing and

presenting the interest costs associated with the borrowings obtained by the company

during the year and the repayments associated with it. It can be observed that the changes

in accounting policies relating to recognition of borrowing costs have resulted in increase

in the borrowing costs expenditure and the real accounting interest rate has been applied

by the company to calculate the borrowing costs.

Net gain or loss on property, plant and equipment – The recognition and measurement of

proceeds associated with selling of property, plant and equipment together with the type

of activity performed by the company. The ASSB adoption of accounting standards has

resulted in realising actual profits and losses for the company during the period.

Therefore it can be observed that the major effect associated with this kind of adoption in the

accounting framework has resulted in increase in the liabilities reported by the company and

decreasing the amount of surplus profits recorded by the company together with the equity

component associated and acquiring the more real value of depreciation to be charged for the

company in its annual accounts (Bryce, et. al., 2015).

10

be recognized appropriately by the enterprise.

Depreciation – Te accounting policy related to depreciating the value f different types of

assets in the company have resulted in changes in accumulating the depreciation expense

of the company. The method of applying the deprecation along with the depreciation

rates has changed and the companies are now adopting more relevant and reliable method

of charging depreciation that will result in accurate reporting (Kraft & Landsman, 2017).

Borrowing costs – The treatment of the borrowing cost is related to recognizing and

presenting the interest costs associated with the borrowings obtained by the company

during the year and the repayments associated with it. It can be observed that the changes

in accounting policies relating to recognition of borrowing costs have resulted in increase

in the borrowing costs expenditure and the real accounting interest rate has been applied

by the company to calculate the borrowing costs.

Net gain or loss on property, plant and equipment – The recognition and measurement of

proceeds associated with selling of property, plant and equipment together with the type

of activity performed by the company. The ASSB adoption of accounting standards has

resulted in realising actual profits and losses for the company during the period.

Therefore it can be observed that the major effect associated with this kind of adoption in the

accounting framework has resulted in increase in the liabilities reported by the company and

decreasing the amount of surplus profits recorded by the company together with the equity

component associated and acquiring the more real value of depreciation to be charged for the

company in its annual accounts (Bryce, et. al., 2015).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion:

The report prepared above leads to the conclusion that the adaptability and implementation of

IFRS in the accounting work of companies have impacted significantly the results obtained in

financial reports of company. The implementations of accounting standards which are

recognized internationally have resulted in enhancing the comparability feature of reporting

between different enterprises of the country. The positive effect of recognizing the accounting

standards as per IFRS has resulted in presenting the more accurate information for the

accounting work to be performed. The adoption of IFRS has enhanced the quality of reporting

and has affected the confidence of investors in making financial decision while utilizing the

financial reports of company.

11

The report prepared above leads to the conclusion that the adaptability and implementation of

IFRS in the accounting work of companies have impacted significantly the results obtained in

financial reports of company. The implementations of accounting standards which are

recognized internationally have resulted in enhancing the comparability feature of reporting

between different enterprises of the country. The positive effect of recognizing the accounting

standards as per IFRS has resulted in presenting the more accurate information for the

accounting work to be performed. The adoption of IFRS has enhanced the quality of reporting

and has affected the confidence of investors in making financial decision while utilizing the

financial reports of company.

11

References:

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, pp.163-181.

Cheung, E. and J. Lau (2016). “Readability of Notes to the Financial Statements and the

Adoption of IFRS.” Australian Accounting Review 26(2): 162-176

Firth, M. and Gounopoulos, D., 2017. IFRS adoption and management earnings forecasts

of Australian IPOs.

Freeman, R.J., Shoulders, C.D., Allison, G.S. and Smith, G.R., 2014. Governmental and

nonprofit accounting. Pearson Education Limited.

Iasplus.com. (2018). AASB research report concludes that IFRS adoption has benefited

the Australian economy. [online] Available at:

https://www.iasplus.com/en/news/2016/10/aasb [Accessed 25 May 2018].

Ji, X. and L. Wei. (2014). “The value relevance and reliability of intangible assets:

Evidence from Australia before and after adopting IFRS.” Asian Review of

Accounting22(3): 182-216.

Jin, K., Y. Shan and S. Taylor (2015). “Matching between revenues and expenses and the

adoption of International Financial Reporting Standards.” Pacific-Basin Finance Journal

35(Part A): 90-107.

Jones, S. ed., 2015. The Routledge companion to financial accounting theory. Routledge.

Khan, S.A., Anderson, M.C., Warsame, H.A. and Wright, M., 2017. IFRS Adoption and

Liquidity: A Comparative Analysis of Canada with Australia and the United Kingdom.

Kraft, P. and Landsman, W.R., 2017. Effect of mandatory IFRS adoption on accounting-

based prediction models for CDS spreads.

Leong, R., 2015. Structuring an undergraduate accounting theory course to enhance the

learning experience of Australian students: Preliminary findings.

Morris, R.D., 2017. Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting

Research, 16(2), pp.155-157.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

12

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, pp.163-181.

Cheung, E. and J. Lau (2016). “Readability of Notes to the Financial Statements and the

Adoption of IFRS.” Australian Accounting Review 26(2): 162-176

Firth, M. and Gounopoulos, D., 2017. IFRS adoption and management earnings forecasts

of Australian IPOs.

Freeman, R.J., Shoulders, C.D., Allison, G.S. and Smith, G.R., 2014. Governmental and

nonprofit accounting. Pearson Education Limited.

Iasplus.com. (2018). AASB research report concludes that IFRS adoption has benefited

the Australian economy. [online] Available at:

https://www.iasplus.com/en/news/2016/10/aasb [Accessed 25 May 2018].

Ji, X. and L. Wei. (2014). “The value relevance and reliability of intangible assets:

Evidence from Australia before and after adopting IFRS.” Asian Review of

Accounting22(3): 182-216.

Jin, K., Y. Shan and S. Taylor (2015). “Matching between revenues and expenses and the

adoption of International Financial Reporting Standards.” Pacific-Basin Finance Journal

35(Part A): 90-107.

Jones, S. ed., 2015. The Routledge companion to financial accounting theory. Routledge.

Khan, S.A., Anderson, M.C., Warsame, H.A. and Wright, M., 2017. IFRS Adoption and

Liquidity: A Comparative Analysis of Canada with Australia and the United Kingdom.

Kraft, P. and Landsman, W.R., 2017. Effect of mandatory IFRS adoption on accounting-

based prediction models for CDS spreads.

Leong, R., 2015. Structuring an undergraduate accounting theory course to enhance the

learning experience of Australian students: Preliminary findings.

Morris, R.D., 2017. Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting

Research, 16(2), pp.155-157.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.