HI6026 Audit, Assurance and Compliance Report

VerifiedAdded on 2020/03/13

|8

|2059

|214

Report

AI Summary

This report analyzes the audit, assurance, and compliance aspects of DIPL's financial statements, focusing on analytical procedures, inherent risks, and fraud risk factors. It includes detailed evaluations of financial ratios and the implications of DIPL's loan and new IT system on its financial integrity. The report emphasizes the auditor's role in monitoring these risks and ensuring accurate financial reporting.

Running Head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Subject Code- HI6026

Trimester No.- 2

Student’s name-

Word Count - 1500

Professor –

University -

Audit, Assurance and Compliance

Subject Code- HI6026

Trimester No.- 2

Student’s name-

Word Count - 1500

Professor –

University -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE P a g e

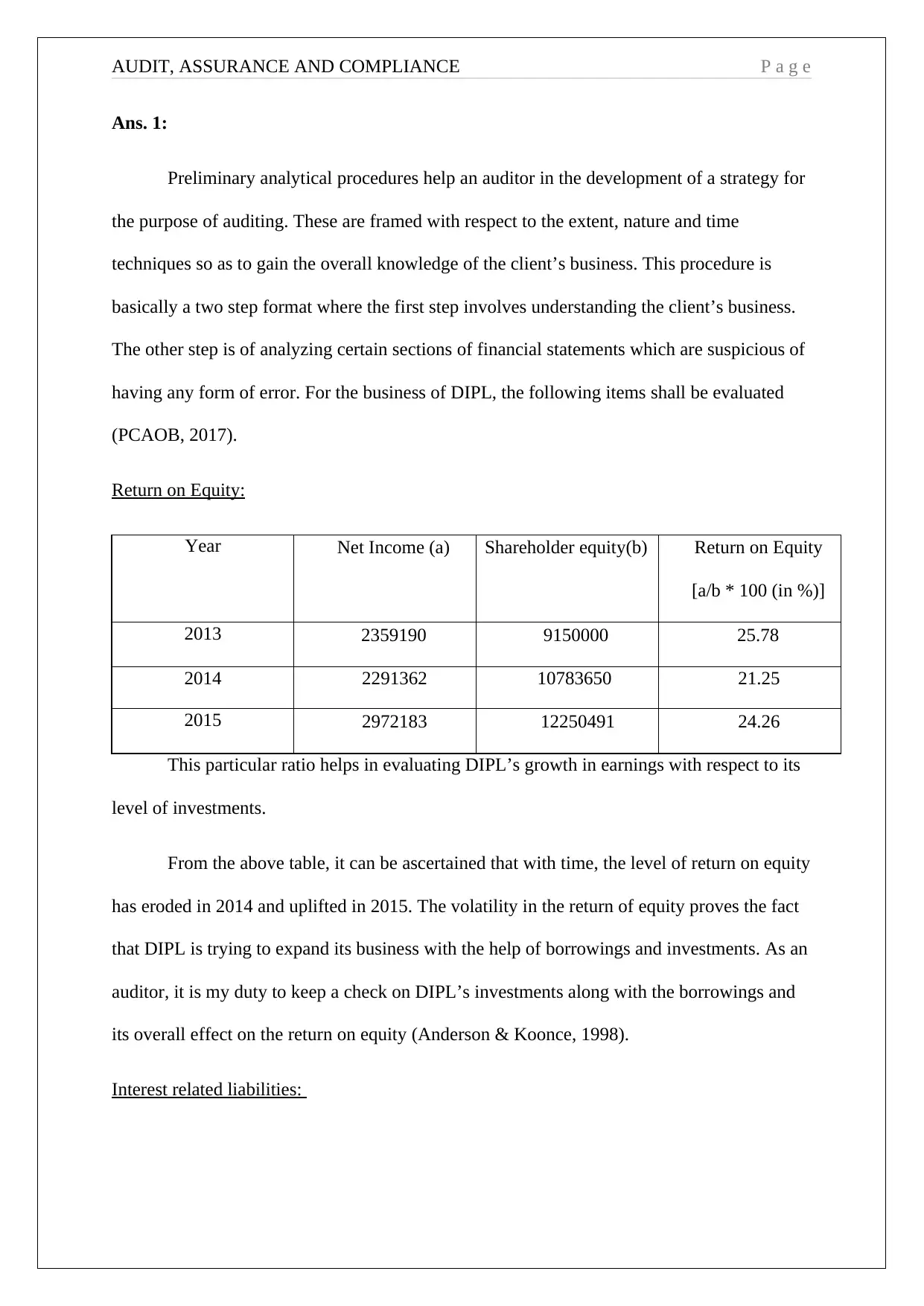

Ans. 1:

Preliminary analytical procedures help an auditor in the development of a strategy for

the purpose of auditing. These are framed with respect to the extent, nature and time

techniques so as to gain the overall knowledge of the client’s business. This procedure is

basically a two step format where the first step involves understanding the client’s business.

The other step is of analyzing certain sections of financial statements which are suspicious of

having any form of error. For the business of DIPL, the following items shall be evaluated

(PCAOB, 2017).

Return on Equity:

Year Net Income (a) Shareholder equity(b) Return on Equity

[a/b * 100 (in %)]

2013 2359190 9150000 25.78

2014 2291362 10783650 21.25

2015 2972183 12250491 24.26

This particular ratio helps in evaluating DIPL’s growth in earnings with respect to its

level of investments.

From the above table, it can be ascertained that with time, the level of return on equity

has eroded in 2014 and uplifted in 2015. The volatility in the return of equity proves the fact

that DIPL is trying to expand its business with the help of borrowings and investments. As an

auditor, it is my duty to keep a check on DIPL’s investments along with the borrowings and

its overall effect on the return on equity (Anderson & Koonce, 1998).

Interest related liabilities:

Ans. 1:

Preliminary analytical procedures help an auditor in the development of a strategy for

the purpose of auditing. These are framed with respect to the extent, nature and time

techniques so as to gain the overall knowledge of the client’s business. This procedure is

basically a two step format where the first step involves understanding the client’s business.

The other step is of analyzing certain sections of financial statements which are suspicious of

having any form of error. For the business of DIPL, the following items shall be evaluated

(PCAOB, 2017).

Return on Equity:

Year Net Income (a) Shareholder equity(b) Return on Equity

[a/b * 100 (in %)]

2013 2359190 9150000 25.78

2014 2291362 10783650 21.25

2015 2972183 12250491 24.26

This particular ratio helps in evaluating DIPL’s growth in earnings with respect to its

level of investments.

From the above table, it can be ascertained that with time, the level of return on equity

has eroded in 2014 and uplifted in 2015. The volatility in the return of equity proves the fact

that DIPL is trying to expand its business with the help of borrowings and investments. As an

auditor, it is my duty to keep a check on DIPL’s investments along with the borrowings and

its overall effect on the return on equity (Anderson & Koonce, 1998).

Interest related liabilities:

AUDIT, ASSURANCE AND COMPLIANCE P a g e

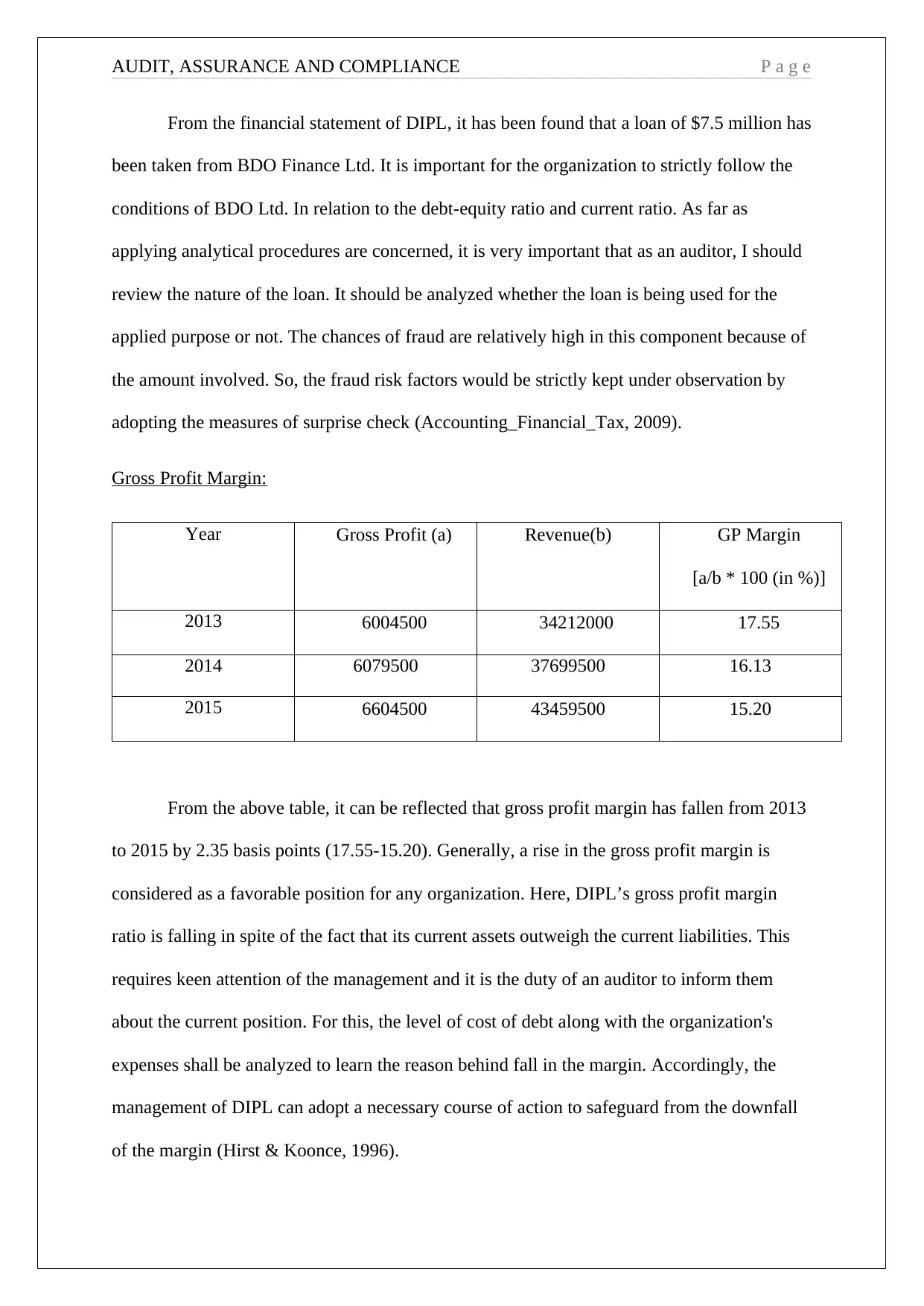

From the financial statement of DIPL, it has been found that a loan of $7.5 million has

been taken from BDO Finance Ltd. It is important for the organization to strictly follow the

conditions of BDO Ltd. In relation to the debt-equity ratio and current ratio. As far as

applying analytical procedures are concerned, it is very important that as an auditor, I should

review the nature of the loan. It should be analyzed whether the loan is being used for the

applied purpose or not. The chances of fraud are relatively high in this component because of

the amount involved. So, the fraud risk factors would be strictly kept under observation by

adopting the measures of surprise check (Accounting_Financial_Tax, 2009).

Gross Profit Margin:

Year Gross Profit (a) Revenue(b) GP Margin

[a/b * 100 (in %)]

2013 6004500 34212000 17.55

2014 6079500 37699500 16.13

2015 6604500 43459500 15.20

From the above table, it can be reflected that gross profit margin has fallen from 2013

to 2015 by 2.35 basis points (17.55-15.20). Generally, a rise in the gross profit margin is

considered as a favorable position for any organization. Here, DIPL’s gross profit margin

ratio is falling in spite of the fact that its current assets outweigh the current liabilities. This

requires keen attention of the management and it is the duty of an auditor to inform them

about the current position. For this, the level of cost of debt along with the organization's

expenses shall be analyzed to learn the reason behind fall in the margin. Accordingly, the

management of DIPL can adopt a necessary course of action to safeguard from the downfall

of the margin (Hirst & Koonce, 1996).

From the financial statement of DIPL, it has been found that a loan of $7.5 million has

been taken from BDO Finance Ltd. It is important for the organization to strictly follow the

conditions of BDO Ltd. In relation to the debt-equity ratio and current ratio. As far as

applying analytical procedures are concerned, it is very important that as an auditor, I should

review the nature of the loan. It should be analyzed whether the loan is being used for the

applied purpose or not. The chances of fraud are relatively high in this component because of

the amount involved. So, the fraud risk factors would be strictly kept under observation by

adopting the measures of surprise check (Accounting_Financial_Tax, 2009).

Gross Profit Margin:

Year Gross Profit (a) Revenue(b) GP Margin

[a/b * 100 (in %)]

2013 6004500 34212000 17.55

2014 6079500 37699500 16.13

2015 6604500 43459500 15.20

From the above table, it can be reflected that gross profit margin has fallen from 2013

to 2015 by 2.35 basis points (17.55-15.20). Generally, a rise in the gross profit margin is

considered as a favorable position for any organization. Here, DIPL’s gross profit margin

ratio is falling in spite of the fact that its current assets outweigh the current liabilities. This

requires keen attention of the management and it is the duty of an auditor to inform them

about the current position. For this, the level of cost of debt along with the organization's

expenses shall be analyzed to learn the reason behind fall in the margin. Accordingly, the

management of DIPL can adopt a necessary course of action to safeguard from the downfall

of the margin (Hirst & Koonce, 1996).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE P a g e

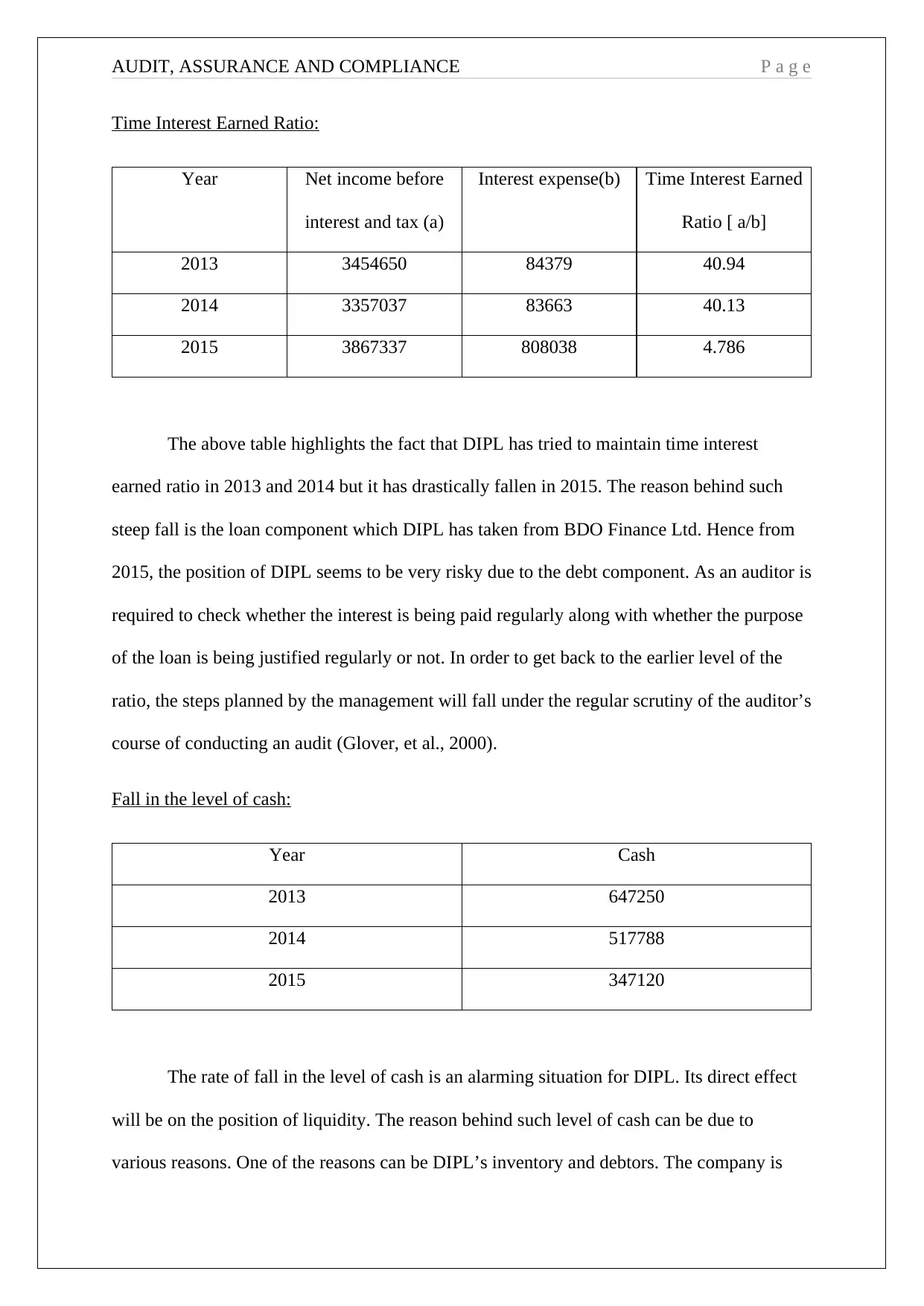

Time Interest Earned Ratio:

Year Net income before

interest and tax (a)

Interest expense(b) Time Interest Earned

Ratio [ a/b]

2013 3454650 84379 40.94

2014 3357037 83663 40.13

2015 3867337 808038 4.786

The above table highlights the fact that DIPL has tried to maintain time interest

earned ratio in 2013 and 2014 but it has drastically fallen in 2015. The reason behind such

steep fall is the loan component which DIPL has taken from BDO Finance Ltd. Hence from

2015, the position of DIPL seems to be very risky due to the debt component. As an auditor is

required to check whether the interest is being paid regularly along with whether the purpose

of the loan is being justified regularly or not. In order to get back to the earlier level of the

ratio, the steps planned by the management will fall under the regular scrutiny of the auditor’s

course of conducting an audit (Glover, et al., 2000).

Fall in the level of cash:

Year Cash

2013 647250

2014 517788

2015 347120

The rate of fall in the level of cash is an alarming situation for DIPL. Its direct effect

will be on the position of liquidity. The reason behind such level of cash can be due to

various reasons. One of the reasons can be DIPL’s inventory and debtors. The company is

Time Interest Earned Ratio:

Year Net income before

interest and tax (a)

Interest expense(b) Time Interest Earned

Ratio [ a/b]

2013 3454650 84379 40.94

2014 3357037 83663 40.13

2015 3867337 808038 4.786

The above table highlights the fact that DIPL has tried to maintain time interest

earned ratio in 2013 and 2014 but it has drastically fallen in 2015. The reason behind such

steep fall is the loan component which DIPL has taken from BDO Finance Ltd. Hence from

2015, the position of DIPL seems to be very risky due to the debt component. As an auditor is

required to check whether the interest is being paid regularly along with whether the purpose

of the loan is being justified regularly or not. In order to get back to the earlier level of the

ratio, the steps planned by the management will fall under the regular scrutiny of the auditor’s

course of conducting an audit (Glover, et al., 2000).

Fall in the level of cash:

Year Cash

2013 647250

2014 517788

2015 347120

The rate of fall in the level of cash is an alarming situation for DIPL. Its direct effect

will be on the position of liquidity. The reason behind such level of cash can be due to

various reasons. One of the reasons can be DIPL’s inventory and debtors. The company is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE P a g e

blocking its cash in these two components. Another reason is that DIPL is supposedly billing

its clients at a lower rate. For this, surprise check of cash will be adopted as and when

required (PCAOB, 2017).

Thus these were some analytical procedures wihcih will be applied on DIPL’s

financial statements. The above parameters are quite crucial which requires the above stated

planning for conducting audit.

Ans. 2:

Inherent risk is those risk which lies beyond the control of an auditor’s audit

procedures and methods of control (My_Accounting_Course, 2017). The two inherent risk

factors are DIPL’s acquisition of Nuclear Publishing Ltd. with an aim to earn higher profit

margin and the shift from the manual system to the new computerized system installation.

The reason behind the acquisition of the organization was uplifting the level of DIPL’s profit

margin of medical textbooks. The latest news related to the textbooks that it will turn obsolete

will result in fall in the return and increase in the level of DIPL. The company will face fall in

its revenue and profit margin simultaneously. Since the acquisition is the most relevant part

of DIPL’s undertaking, it may face threat to going concern in the near future.

With the new IT system, chances of errors are quite high because of the pressure

involved amongst the employees. The new system has its own limitations like the software

may crash or there might be any coding error. Due to the prevalence of the system errors, the

financial statements will be materially misstated in an unintentional or intentional manner.

Due to the pressure and coding error, some of the transactions might not enter into the

system. Undue advantage can be taken of this situation. Employees may skip entering some

revenue transactions and they can use it for their personal benefit. This will ultimately lead to

fraud and it will be very difficult to trace who has actually committed the fraud. It is

blocking its cash in these two components. Another reason is that DIPL is supposedly billing

its clients at a lower rate. For this, surprise check of cash will be adopted as and when

required (PCAOB, 2017).

Thus these were some analytical procedures wihcih will be applied on DIPL’s

financial statements. The above parameters are quite crucial which requires the above stated

planning for conducting audit.

Ans. 2:

Inherent risk is those risk which lies beyond the control of an auditor’s audit

procedures and methods of control (My_Accounting_Course, 2017). The two inherent risk

factors are DIPL’s acquisition of Nuclear Publishing Ltd. with an aim to earn higher profit

margin and the shift from the manual system to the new computerized system installation.

The reason behind the acquisition of the organization was uplifting the level of DIPL’s profit

margin of medical textbooks. The latest news related to the textbooks that it will turn obsolete

will result in fall in the return and increase in the level of DIPL. The company will face fall in

its revenue and profit margin simultaneously. Since the acquisition is the most relevant part

of DIPL’s undertaking, it may face threat to going concern in the near future.

With the new IT system, chances of errors are quite high because of the pressure

involved amongst the employees. The new system has its own limitations like the software

may crash or there might be any coding error. Due to the prevalence of the system errors, the

financial statements will be materially misstated in an unintentional or intentional manner.

Due to the pressure and coding error, some of the transactions might not enter into the

system. Undue advantage can be taken of this situation. Employees may skip entering some

revenue transactions and they can use it for their personal benefit. This will ultimately lead to

fraud and it will be very difficult to trace who has actually committed the fraud. It is

AUDIT, ASSURANCE AND COMPLIANCE P a g e

classified as the intervention of human nature in conducting fraud in an organization (Hirst &

Koonce, 1996).

The above two inherent risk can misstate the financial statements in their own

manner. The report will be misleading and the decisions made on its basis will turn out to be

a failure for the organization. These two are quite a risky component and it has the potential

to create a volatile situation in the financial statements. Due to system change, some errors

have been found in terms of the incorrect accounting period. It is an inherent nature of the

system which is also very difficult for an auditor to trace it and take the necessary course of

action.

Ans. 3:

As per the background information of DIPL, its two fraud risk factors are loan taken

from BDO Finance Ltd. and another is the adoption of new IT system in their course of

operations. DIPL us under the pressure to pay off such a heavy amount of loan. Secondly, it

is under pressure to maintain or follow the conditions as stated by BDO Finance Ltd. The

funds are supposed to serve the purpose of growth but under immense pressure, the scope of

manipulating the financial statements stands high. This will eventually lead to a situation of

internal and external fraud of DIPL (Payne & Ramsay, 2005).

Due to the ineffective installation of the new IT system, it has developed a scope to

gain undue advantage out of it. False transactions can be made in the name of the company or

transactions of the heavy amount can be deleted which will falsify the financial statements.

As far as the limitation on the auditor while conducting an audit is concerned, the above risk

factors have their own role play in it. The loan of $ 7.5 million requires careful attention

towards it. As an auditor, it is required to thoroughly check for the reason behind such loan

and its application into the business. In the case of any suspicious activity found during the

classified as the intervention of human nature in conducting fraud in an organization (Hirst &

Koonce, 1996).

The above two inherent risk can misstate the financial statements in their own

manner. The report will be misleading and the decisions made on its basis will turn out to be

a failure for the organization. These two are quite a risky component and it has the potential

to create a volatile situation in the financial statements. Due to system change, some errors

have been found in terms of the incorrect accounting period. It is an inherent nature of the

system which is also very difficult for an auditor to trace it and take the necessary course of

action.

Ans. 3:

As per the background information of DIPL, its two fraud risk factors are loan taken

from BDO Finance Ltd. and another is the adoption of new IT system in their course of

operations. DIPL us under the pressure to pay off such a heavy amount of loan. Secondly, it

is under pressure to maintain or follow the conditions as stated by BDO Finance Ltd. The

funds are supposed to serve the purpose of growth but under immense pressure, the scope of

manipulating the financial statements stands high. This will eventually lead to a situation of

internal and external fraud of DIPL (Payne & Ramsay, 2005).

Due to the ineffective installation of the new IT system, it has developed a scope to

gain undue advantage out of it. False transactions can be made in the name of the company or

transactions of the heavy amount can be deleted which will falsify the financial statements.

As far as the limitation on the auditor while conducting an audit is concerned, the above risk

factors have their own role play in it. The loan of $ 7.5 million requires careful attention

towards it. As an auditor, it is required to thoroughly check for the reason behind such loan

and its application into the business. In the case of any suspicious activity found during the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE P a g e

scrutiny, the same can be informed and discussed with the management. If the fraud cannot

be easily traced, the auditor's report will stand invalid and against the conceptual framework

of auditing (Knapp & Knapp, 2001).

In order to check for the effectiveness and efficiency of the newly adopted IT system,

various IT tools are available for the purpose of conducting an audit. One of the methods is of

Computer Assisted Audit Technique which helps in locating loopholes of such kind of

systems. It will also help in effectively maintaining audit trail during the course of the audit.

Thus, the debt component and the newly adopted IT system are two major fraud risk factors

of DIPL which has the potential to materialize the fraud at any moment of time (Anderson &

Koonce, 1998).

scrutiny, the same can be informed and discussed with the management. If the fraud cannot

be easily traced, the auditor's report will stand invalid and against the conceptual framework

of auditing (Knapp & Knapp, 2001).

In order to check for the effectiveness and efficiency of the newly adopted IT system,

various IT tools are available for the purpose of conducting an audit. One of the methods is of

Computer Assisted Audit Technique which helps in locating loopholes of such kind of

systems. It will also help in effectively maintaining audit trail during the course of the audit.

Thus, the debt component and the newly adopted IT system are two major fraud risk factors

of DIPL which has the potential to materialize the fraud at any moment of time (Anderson &

Koonce, 1998).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE P a g e

References

Accounting_Financial_Tax, 2009. Analytical Procedures in Auditing. [Online]

Available at: http://accounting-financial-tax.com/2009/10/analytical-procedures-in-auditing/

[Accessed 15 August 2017].

Anderson, U. & Koonce, L., 1998. Evaluating the sufficiency of causes in audit analytical

procedures. Auditing- A Journal of Practise and Theory, 17(1), pp. 1-12.

Glover, S., Jiambalvo, J. & Kennedy, J., 2000. Analytical procedures and audit-planning

decisions. Auditing: A Journal of Practice & Theory, 19(2), pp. 27-45.

Hirst, D. & Koonce, L., 1996. , 1996. Audit analytical procedures: A field investigation..

Contemporary Accounting Research, 13(2), pp. 457-486.

Johnstone, K., Gramling, A. & Rittenberg, L. E., 2012. Auditing: A Risk-Based Approach To

Conducting a Quality Audit. 9 ed. New York: Cengage Learning.

Knapp, C. A. & Knapp, M. C., 2001. Knapp,The effects of experience and explicit fraud risk

assessment in detecting fraud with analytical procedures. Accounting, Organizations and

Society, 26(1), pp. 25-37.

My_Accounting_Course, 2017. What is Inherent Risk?. [Online]

Available at: http://www.myaccountingcourse.com/accounting-dictionary/inherent-risk

[Accessed 15 August 2017].

Payne, E. A. & Ramsay, R. J., 2005. Fraud risk assessments and auditors’ professional

skepticism. Managerial Auditing Journal, 20(3), pp. 321-330.

PCAOB, 2017. Analytical Procedures. [Online]

Available at: https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx

[Accessed 15 August 2017].

References

Accounting_Financial_Tax, 2009. Analytical Procedures in Auditing. [Online]

Available at: http://accounting-financial-tax.com/2009/10/analytical-procedures-in-auditing/

[Accessed 15 August 2017].

Anderson, U. & Koonce, L., 1998. Evaluating the sufficiency of causes in audit analytical

procedures. Auditing- A Journal of Practise and Theory, 17(1), pp. 1-12.

Glover, S., Jiambalvo, J. & Kennedy, J., 2000. Analytical procedures and audit-planning

decisions. Auditing: A Journal of Practice & Theory, 19(2), pp. 27-45.

Hirst, D. & Koonce, L., 1996. , 1996. Audit analytical procedures: A field investigation..

Contemporary Accounting Research, 13(2), pp. 457-486.

Johnstone, K., Gramling, A. & Rittenberg, L. E., 2012. Auditing: A Risk-Based Approach To

Conducting a Quality Audit. 9 ed. New York: Cengage Learning.

Knapp, C. A. & Knapp, M. C., 2001. Knapp,The effects of experience and explicit fraud risk

assessment in detecting fraud with analytical procedures. Accounting, Organizations and

Society, 26(1), pp. 25-37.

My_Accounting_Course, 2017. What is Inherent Risk?. [Online]

Available at: http://www.myaccountingcourse.com/accounting-dictionary/inherent-risk

[Accessed 15 August 2017].

Payne, E. A. & Ramsay, R. J., 2005. Fraud risk assessments and auditors’ professional

skepticism. Managerial Auditing Journal, 20(3), pp. 321-330.

PCAOB, 2017. Analytical Procedures. [Online]

Available at: https://pcaobus.org/Standards/Archived/Pages/AU329A.aspx

[Accessed 15 August 2017].

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.