HI6026 - Audit, Assurance, Stakeholder Analysis of ANZ Banking Group

VerifiedAdded on 2023/04/23

|17

|4350

|220

Report

AI Summary

This report analyzes key stakeholder relationships and the auditing system within the Australian and New Zealand Banking Group (ANZ). It examines the importance of whistleblowing, referencing the Enron scandal as a case of corrupt practices. The report emphasizes the necessity of a robust auditing system and assurance mechanisms to enhance investor confidence. It details stakeholder management techniques employed by ANZ, focusing on trust, relationship building, and mutual respect. The analysis includes a stakeholder map and power matrix to illustrate the influence and interests of various stakeholders. Furthermore, the report discusses the role of whistleblowers in exposing unethical conduct, referencing the Whistle Blowing Act (1998) and the Enron scandal, where Sheron Watkins revealed financial malpractices. The Enron case highlights the dangers of prioritizing brand image over transparency and ethical financial reporting, ultimately leading to the company's collapse.

0

Running head: AUDIT AND ASSURANCE

AUDIT AND ASSURANCE

Name of the Student

Name of the University

Author’s Note

Running head: AUDIT AND ASSURANCE

AUDIT AND ASSURANCE

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT & ASSURANCE

Executive Summary

The purpose of the report is to analyze the key stakeholder analysis as well as the auditing

system in relation to the Australian and New Zealand bank. The report has also analyzed the

importance of whistle blowing in relation to the case of Enron which was diagnosed with a

corrupt practice. The report has analyzed in details the need for good auditing system as well as

making assurance which can make the organization better for the investors. The following

paragraphs of the report aims at providing a detailed analysis on the various factors related to

auditing and the ethics which are involved in the whistle blowing case.

Executive Summary

The purpose of the report is to analyze the key stakeholder analysis as well as the auditing

system in relation to the Australian and New Zealand bank. The report has also analyzed the

importance of whistle blowing in relation to the case of Enron which was diagnosed with a

corrupt practice. The report has analyzed in details the need for good auditing system as well as

making assurance which can make the organization better for the investors. The following

paragraphs of the report aims at providing a detailed analysis on the various factors related to

auditing and the ethics which are involved in the whistle blowing case.

2AUDIT & ASSURANCE

Table of Contents

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................3

Key Stakeholder Analysis................................................................................................................3

Independence & Whistleblowing....................................................................................................7

Enron Scandal..................................................................................................................................8

Audit Quality.................................................................................................................................10

Conclusion.....................................................................................................................................12

References..................................................................................................................................14

Table of Contents

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................3

Key Stakeholder Analysis................................................................................................................3

Independence & Whistleblowing....................................................................................................7

Enron Scandal..................................................................................................................................8

Audit Quality.................................................................................................................................10

Conclusion.....................................................................................................................................12

References..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT & ASSURANCE

Introduction

The effective working of an organization requires strong corporate objectives. These

objectives need to be pursued in a diligent manner to make sure that the business process is

conducted in an efficient manner (Ashcraft et al. 2017). The whole task of processing a business

requires simultaneous control of various internal processes along with the monitoring of all the

accounting systems. The prevention of the fraudulent financial transaction is also a part of the

measurement of the business performance for which the system of auditing is needed (Chambers

and Odar 2015). Auditing is defined as the act of maintenance of financial records by an

organization with the engagement of operational aspects for the authentic maintenance of the

financial stability related to the organization (Averhals, VanCaneghem and Willekens 2018). The

need for auditing is to ensure that there are no discrepancies in the financial records and to track

and solve if any. This is done to ensure that the organization has better credibility in terms of

business and financial aspects (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The following

assessment is an analysis of the different aspects of the auditing system and the amount of

assurance that has been fed by the circumstances hampering the performance of the organization

in the future.

Key Stakeholder Analysis

Australia and New Zealand banking group is amongst the five largest and well-

established companies in the province of Australia. It has a potential place on the global basis

which ranks amongst the top 50 banks in the world (ANZ.com 2018). There are major

stakeholders in the bank who get affected by the problems as well as profit of the bank. The

major stakeholders who are involved in the ASX Company are the government, customers of the

bank, suppliers, employees of the bank and the other people involved in the public organizations

Introduction

The effective working of an organization requires strong corporate objectives. These

objectives need to be pursued in a diligent manner to make sure that the business process is

conducted in an efficient manner (Ashcraft et al. 2017). The whole task of processing a business

requires simultaneous control of various internal processes along with the monitoring of all the

accounting systems. The prevention of the fraudulent financial transaction is also a part of the

measurement of the business performance for which the system of auditing is needed (Chambers

and Odar 2015). Auditing is defined as the act of maintenance of financial records by an

organization with the engagement of operational aspects for the authentic maintenance of the

financial stability related to the organization (Averhals, VanCaneghem and Willekens 2018). The

need for auditing is to ensure that there are no discrepancies in the financial records and to track

and solve if any. This is done to ensure that the organization has better credibility in terms of

business and financial aspects (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The following

assessment is an analysis of the different aspects of the auditing system and the amount of

assurance that has been fed by the circumstances hampering the performance of the organization

in the future.

Key Stakeholder Analysis

Australia and New Zealand banking group is amongst the five largest and well-

established companies in the province of Australia. It has a potential place on the global basis

which ranks amongst the top 50 banks in the world (ANZ.com 2018). There are major

stakeholders in the bank who get affected by the problems as well as profit of the bank. The

major stakeholders who are involved in the ASX Company are the government, customers of the

bank, suppliers, employees of the bank and the other people involved in the public organizations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT & ASSURANCE

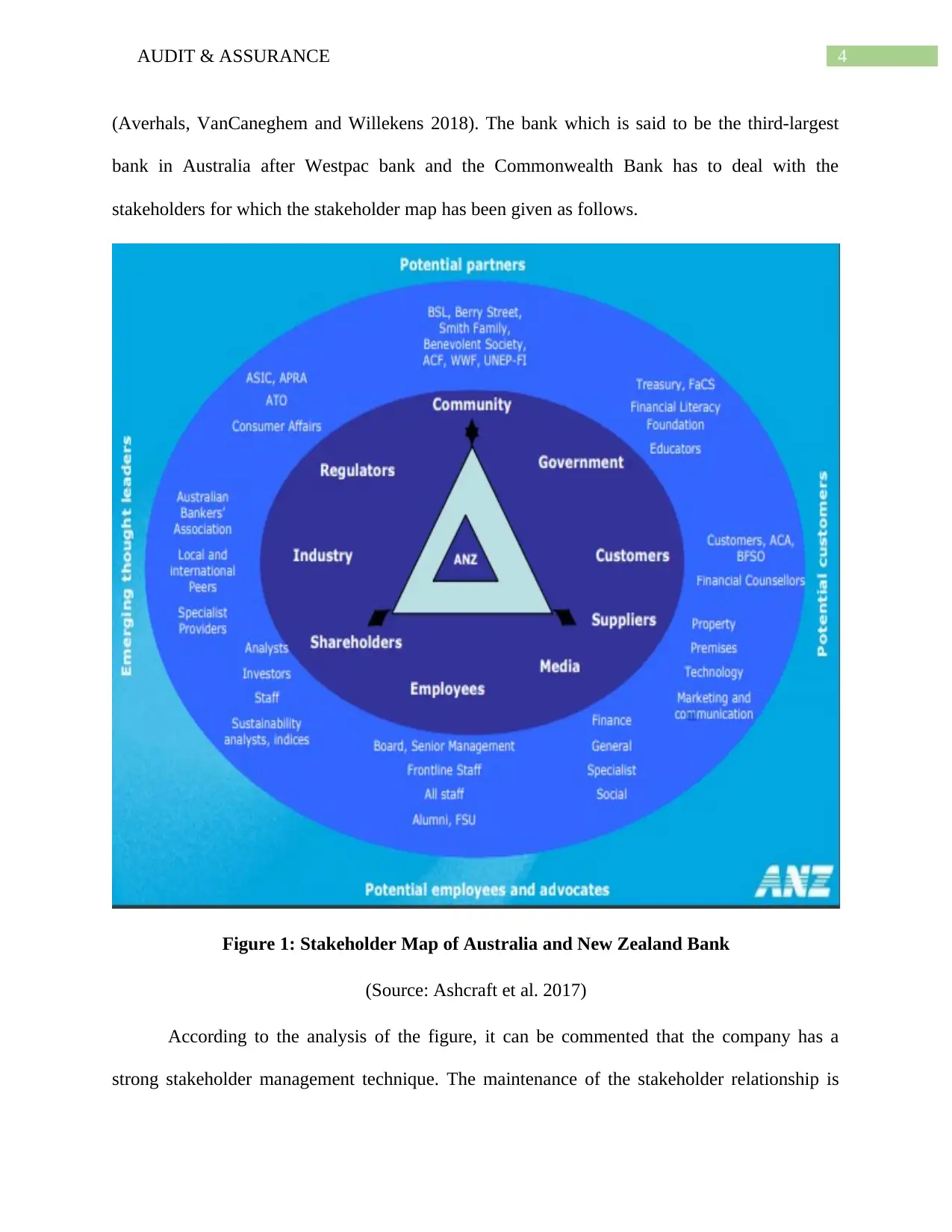

(Averhals, VanCaneghem and Willekens 2018). The bank which is said to be the third-largest

bank in Australia after Westpac bank and the Commonwealth Bank has to deal with the

stakeholders for which the stakeholder map has been given as follows.

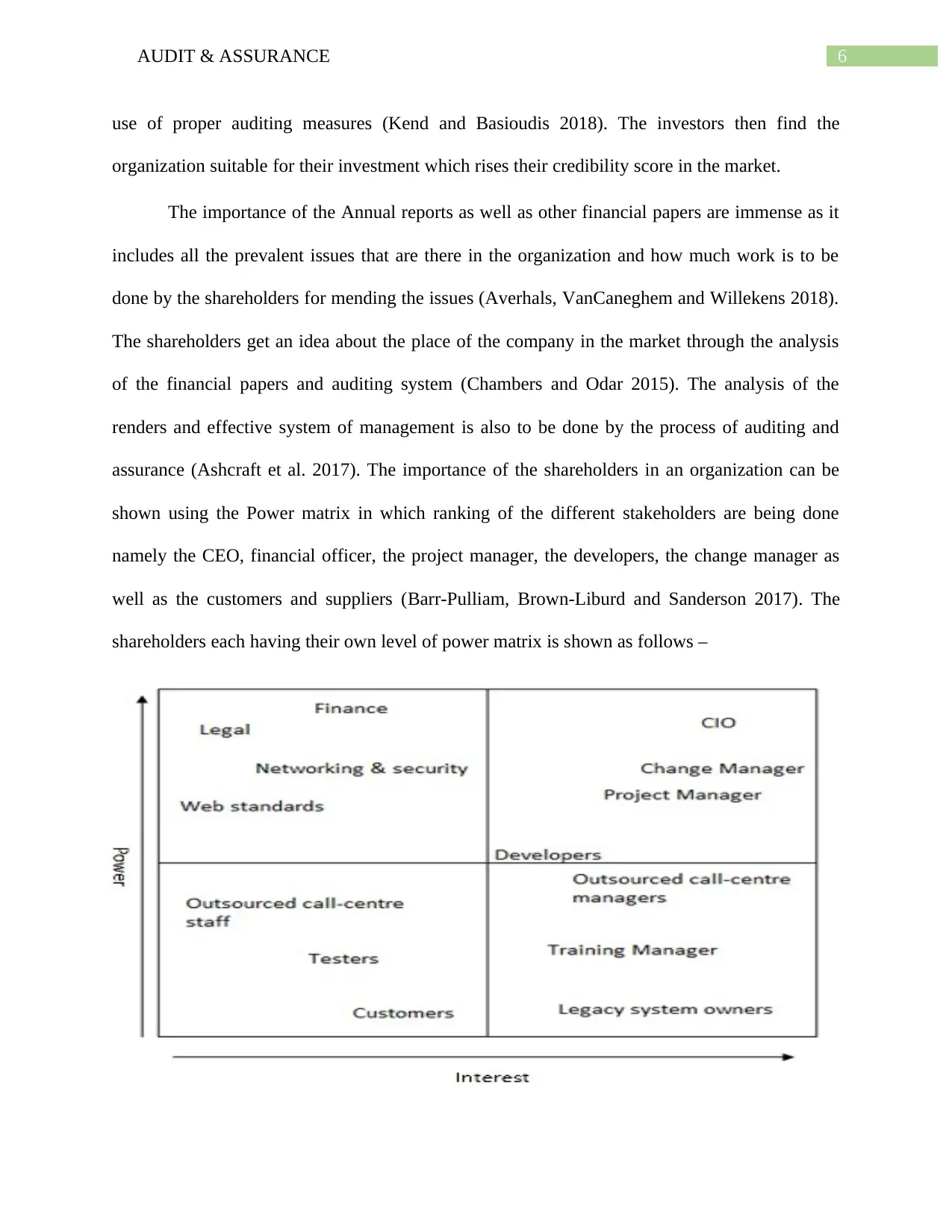

Figure 1: Stakeholder Map of Australia and New Zealand Bank

(Source: Ashcraft et al. 2017)

According to the analysis of the figure, it can be commented that the company has a

strong stakeholder management technique. The maintenance of the stakeholder relationship is

(Averhals, VanCaneghem and Willekens 2018). The bank which is said to be the third-largest

bank in Australia after Westpac bank and the Commonwealth Bank has to deal with the

stakeholders for which the stakeholder map has been given as follows.

Figure 1: Stakeholder Map of Australia and New Zealand Bank

(Source: Ashcraft et al. 2017)

According to the analysis of the figure, it can be commented that the company has a

strong stakeholder management technique. The maintenance of the stakeholder relationship is

5AUDIT & ASSURANCE

done through the abstract ideas of trust, relationship building as well as mutual respect in the

longer phase of time (Chambers and Odar 2015). The company strives in the building up of a

Sustainability Framework which ensures the company to have prioritized the elements of

commercial and retail banking element (Ashcraft et al. 2017). The main aim is to provide better

banking service to all the stakeholders so that their needs and rights are not hampered. The

stakeholders should demand the authentic financial documents for building up their trust on the

organization (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The organization on the other

hand should also supply them with the required materials as well as credible financial resources

for building up their confidence in the policies of the bank (Averhals, VanCaneghem and

Willekens 2018). The reliability of the stakeholders is of utmost importance which can only be

done by the application of suitable financial papers which are legal and authentic.

This engages the stakeholders with the firms which gives profit to the firm in the longer

run. The trustworthiness of the stakeholders is needed as it helps them to engage more with the

bank. The engagement is done on the basis of structural approach of the firm as well as the need

to have financial information which is relevant to the case (Barr-Pulliam, Brown-Liburd and

Sanderson 2017). Moreover, the old and existing stakeholders need to know about the new

shareholders who are entering the organization as well as involving with the working (Chambers

and Odar 2015), This is done to clarify the ownership and the management of the regulatory

protocols in a work organization for a better environment and clarity within the shareholders

(Ashcraft et al. 2017). Moreover, it has also been investigated that with good auditing system

which is credible to the organization, the issues that could have affected the long term working

of the organization can be mended. The issues which are assessed in relation to the strategies of

the organization as well as coordination of different perspectives can be also eliminated by the

done through the abstract ideas of trust, relationship building as well as mutual respect in the

longer phase of time (Chambers and Odar 2015). The company strives in the building up of a

Sustainability Framework which ensures the company to have prioritized the elements of

commercial and retail banking element (Ashcraft et al. 2017). The main aim is to provide better

banking service to all the stakeholders so that their needs and rights are not hampered. The

stakeholders should demand the authentic financial documents for building up their trust on the

organization (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The organization on the other

hand should also supply them with the required materials as well as credible financial resources

for building up their confidence in the policies of the bank (Averhals, VanCaneghem and

Willekens 2018). The reliability of the stakeholders is of utmost importance which can only be

done by the application of suitable financial papers which are legal and authentic.

This engages the stakeholders with the firms which gives profit to the firm in the longer

run. The trustworthiness of the stakeholders is needed as it helps them to engage more with the

bank. The engagement is done on the basis of structural approach of the firm as well as the need

to have financial information which is relevant to the case (Barr-Pulliam, Brown-Liburd and

Sanderson 2017). Moreover, the old and existing stakeholders need to know about the new

shareholders who are entering the organization as well as involving with the working (Chambers

and Odar 2015), This is done to clarify the ownership and the management of the regulatory

protocols in a work organization for a better environment and clarity within the shareholders

(Ashcraft et al. 2017). Moreover, it has also been investigated that with good auditing system

which is credible to the organization, the issues that could have affected the long term working

of the organization can be mended. The issues which are assessed in relation to the strategies of

the organization as well as coordination of different perspectives can be also eliminated by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT & ASSURANCE

use of proper auditing measures (Kend and Basioudis 2018). The investors then find the

organization suitable for their investment which rises their credibility score in the market.

The importance of the Annual reports as well as other financial papers are immense as it

includes all the prevalent issues that are there in the organization and how much work is to be

done by the shareholders for mending the issues (Averhals, VanCaneghem and Willekens 2018).

The shareholders get an idea about the place of the company in the market through the analysis

of the financial papers and auditing system (Chambers and Odar 2015). The analysis of the

renders and effective system of management is also to be done by the process of auditing and

assurance (Ashcraft et al. 2017). The importance of the shareholders in an organization can be

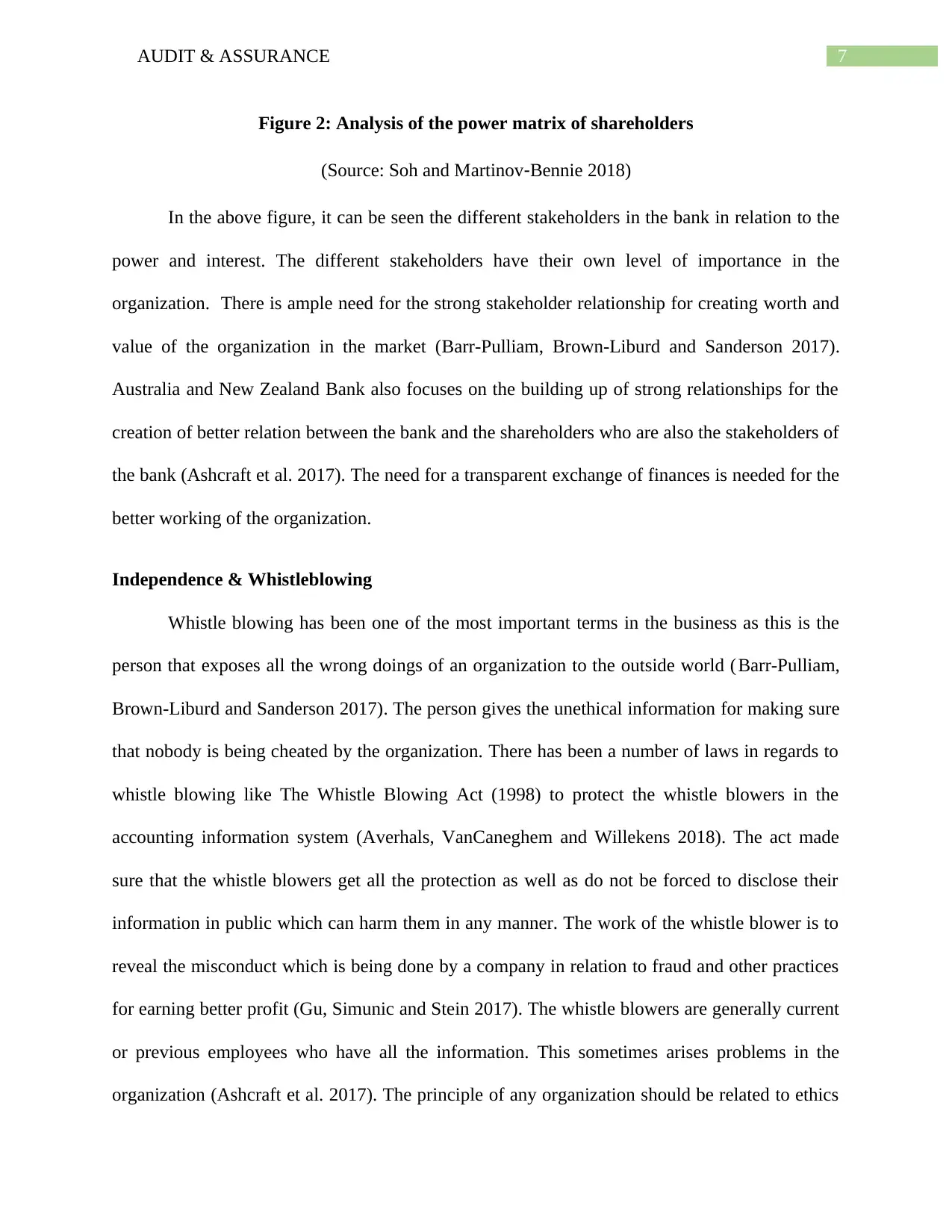

shown using the Power matrix in which ranking of the different stakeholders are being done

namely the CEO, financial officer, the project manager, the developers, the change manager as

well as the customers and suppliers (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The

shareholders each having their own level of power matrix is shown as follows –

use of proper auditing measures (Kend and Basioudis 2018). The investors then find the

organization suitable for their investment which rises their credibility score in the market.

The importance of the Annual reports as well as other financial papers are immense as it

includes all the prevalent issues that are there in the organization and how much work is to be

done by the shareholders for mending the issues (Averhals, VanCaneghem and Willekens 2018).

The shareholders get an idea about the place of the company in the market through the analysis

of the financial papers and auditing system (Chambers and Odar 2015). The analysis of the

renders and effective system of management is also to be done by the process of auditing and

assurance (Ashcraft et al. 2017). The importance of the shareholders in an organization can be

shown using the Power matrix in which ranking of the different stakeholders are being done

namely the CEO, financial officer, the project manager, the developers, the change manager as

well as the customers and suppliers (Barr-Pulliam, Brown-Liburd and Sanderson 2017). The

shareholders each having their own level of power matrix is shown as follows –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT & ASSURANCE

Figure 2: Analysis of the power matrix of shareholders

(Source: Soh and Martinov‐Bennie 2018)

In the above figure, it can be seen the different stakeholders in the bank in relation to the

power and interest. The different stakeholders have their own level of importance in the

organization. There is ample need for the strong stakeholder relationship for creating worth and

value of the organization in the market (Barr-Pulliam, Brown-Liburd and Sanderson 2017).

Australia and New Zealand Bank also focuses on the building up of strong relationships for the

creation of better relation between the bank and the shareholders who are also the stakeholders of

the bank (Ashcraft et al. 2017). The need for a transparent exchange of finances is needed for the

better working of the organization.

Independence & Whistleblowing

Whistle blowing has been one of the most important terms in the business as this is the

person that exposes all the wrong doings of an organization to the outside world (Barr-Pulliam,

Brown-Liburd and Sanderson 2017). The person gives the unethical information for making sure

that nobody is being cheated by the organization. There has been a number of laws in regards to

whistle blowing like The Whistle Blowing Act (1998) to protect the whistle blowers in the

accounting information system (Averhals, VanCaneghem and Willekens 2018). The act made

sure that the whistle blowers get all the protection as well as do not be forced to disclose their

information in public which can harm them in any manner. The work of the whistle blower is to

reveal the misconduct which is being done by a company in relation to fraud and other practices

for earning better profit (Gu, Simunic and Stein 2017). The whistle blowers are generally current

or previous employees who have all the information. This sometimes arises problems in the

organization (Ashcraft et al. 2017). The principle of any organization should be related to ethics

Figure 2: Analysis of the power matrix of shareholders

(Source: Soh and Martinov‐Bennie 2018)

In the above figure, it can be seen the different stakeholders in the bank in relation to the

power and interest. The different stakeholders have their own level of importance in the

organization. There is ample need for the strong stakeholder relationship for creating worth and

value of the organization in the market (Barr-Pulliam, Brown-Liburd and Sanderson 2017).

Australia and New Zealand Bank also focuses on the building up of strong relationships for the

creation of better relation between the bank and the shareholders who are also the stakeholders of

the bank (Ashcraft et al. 2017). The need for a transparent exchange of finances is needed for the

better working of the organization.

Independence & Whistleblowing

Whistle blowing has been one of the most important terms in the business as this is the

person that exposes all the wrong doings of an organization to the outside world (Barr-Pulliam,

Brown-Liburd and Sanderson 2017). The person gives the unethical information for making sure

that nobody is being cheated by the organization. There has been a number of laws in regards to

whistle blowing like The Whistle Blowing Act (1998) to protect the whistle blowers in the

accounting information system (Averhals, VanCaneghem and Willekens 2018). The act made

sure that the whistle blowers get all the protection as well as do not be forced to disclose their

information in public which can harm them in any manner. The work of the whistle blower is to

reveal the misconduct which is being done by a company in relation to fraud and other practices

for earning better profit (Gu, Simunic and Stein 2017). The whistle blowers are generally current

or previous employees who have all the information. This sometimes arises problems in the

organization (Ashcraft et al. 2017). The principle of any organization should be related to ethics

8AUDIT & ASSURANCE

and proper wok environment. However, this has been hampered by the people many times. The

whistle blowers tries to restore the information with transparency (Martínez-Ferrero andGarcía-

Sánchez 2018). There are types of whistle blowing activity among which two are important –

reporting the misconduct of the organization as well as reporting people outside the organization

for the preachment of laws. The act of whistleblower is mentioned in the APES 110 of the code

of business ethics. They take into consideration the various analysis of the documentation of the

organization as well as employees and government 9 Barr-Pulliam, Brown-Liburd and Sanderson

2017). They have their own risk in which they involve to drive the actual information by raising

voice against the politics and legal aspects of business. They mend the needs of the shareholders

for which protection is must for the whistle blowers under the Federal protection.

Enron Scandal

One of the major scandals which can be mentioned in details in this regard in the Enron

Scandal and its increasing profit margin due to unethical means. Enron is an electric company

which recorded sky-high growth from the time of 1995-2000 (Pratt and Peters 2017). The

shareholders became more interested in the organization for the rapid growth of the firm and

their expectancy to earn more profit. However, during the time of 2000 to 2002 it was seen that

the stock prices of Enron went down (Averhals, VanCaneghem and Willekens 2018). However,

it was a terrible loss to the stakeholders as all the investors re-invested in the company and the

stock prices went down marking their loss. However, the company showed in their financial

papers that the amount of profit was very high to attract more investors in the company. After

analyzing the case, it was found that the company was trying to just maintain the brand image

and there was no prominent practice of fraudulency (Soh and Martinov‐Bennie 2018). The brand

image which lasted for 20 years had to be maintained for which the company showed the

and proper wok environment. However, this has been hampered by the people many times. The

whistle blowers tries to restore the information with transparency (Martínez-Ferrero andGarcía-

Sánchez 2018). There are types of whistle blowing activity among which two are important –

reporting the misconduct of the organization as well as reporting people outside the organization

for the preachment of laws. The act of whistleblower is mentioned in the APES 110 of the code

of business ethics. They take into consideration the various analysis of the documentation of the

organization as well as employees and government 9 Barr-Pulliam, Brown-Liburd and Sanderson

2017). They have their own risk in which they involve to drive the actual information by raising

voice against the politics and legal aspects of business. They mend the needs of the shareholders

for which protection is must for the whistle blowers under the Federal protection.

Enron Scandal

One of the major scandals which can be mentioned in details in this regard in the Enron

Scandal and its increasing profit margin due to unethical means. Enron is an electric company

which recorded sky-high growth from the time of 1995-2000 (Pratt and Peters 2017). The

shareholders became more interested in the organization for the rapid growth of the firm and

their expectancy to earn more profit. However, during the time of 2000 to 2002 it was seen that

the stock prices of Enron went down (Averhals, VanCaneghem and Willekens 2018). However,

it was a terrible loss to the stakeholders as all the investors re-invested in the company and the

stock prices went down marking their loss. However, the company showed in their financial

papers that the amount of profit was very high to attract more investors in the company. After

analyzing the case, it was found that the company was trying to just maintain the brand image

and there was no prominent practice of fraudulency (Soh and Martinov‐Bennie 2018). The brand

image which lasted for 20 years had to be maintained for which the company showed the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT & ASSURANCE

revenue figures and not the profit margins for maintaining the investor interest in the company.

This made a ripple in the government as it came to the realization that the firm was cheating the

shareholders by revealing wrong data and just to maintain their position in the market (Louwers

et al. 2015). This led to the support of the unethical business practices for which Enron collapsed

along with Arthur Anderson. Enron had a perception that their financial data being hypothetical

did not arise any issues in the minds of the people and the perceptive data could have been taken

into consideration (Simnett, Carson and Vanstraelen 2016). They therefore tried to maintain their

financial perspectives and give accounting figures as per the needs of the company.

The work of the whistle blowers in this case was of immense importance. The whistle

blower in this case is Sheron Watkins who was a student of Enron. He revealed to the world the

financial malpractices of the firm in relation to the financial numbers and not revealing the actual

information which is there in the company (Simnett, Carson and Vanstraelen 2016). He made it

into focus that the company did not bother to give the correct information to the people but made

sure to gain enough profit by keeping the figures as per the requirement of the firm (Averhals,

VanCaneghem and Willekens 2018). They cheated on the people as this did not benefit the

stakeholders in any manner but only made profit for the company in the longer phase of time.

The investors will invest in the company based on the figures and would not get the

desired amount of profit in the longer span (Simetinger 2018). The aqua advanced technology

and production services will be deployed by the workers with more efficiency and have higher

productivity in the near future. The financial figures which will be represented in the data will

only benefit the organization not the people involved (Schmidt, Wood and Grabski 2016). The

stakeholders will invest based on the non-restricted in the financial statements and will expect

profit which will not be in practical. The company in their reports accessed the targets that were

revenue figures and not the profit margins for maintaining the investor interest in the company.

This made a ripple in the government as it came to the realization that the firm was cheating the

shareholders by revealing wrong data and just to maintain their position in the market (Louwers

et al. 2015). This led to the support of the unethical business practices for which Enron collapsed

along with Arthur Anderson. Enron had a perception that their financial data being hypothetical

did not arise any issues in the minds of the people and the perceptive data could have been taken

into consideration (Simnett, Carson and Vanstraelen 2016). They therefore tried to maintain their

financial perspectives and give accounting figures as per the needs of the company.

The work of the whistle blowers in this case was of immense importance. The whistle

blower in this case is Sheron Watkins who was a student of Enron. He revealed to the world the

financial malpractices of the firm in relation to the financial numbers and not revealing the actual

information which is there in the company (Simnett, Carson and Vanstraelen 2016). He made it

into focus that the company did not bother to give the correct information to the people but made

sure to gain enough profit by keeping the figures as per the requirement of the firm (Averhals,

VanCaneghem and Willekens 2018). They cheated on the people as this did not benefit the

stakeholders in any manner but only made profit for the company in the longer phase of time.

The investors will invest in the company based on the figures and would not get the

desired amount of profit in the longer span (Simetinger 2018). The aqua advanced technology

and production services will be deployed by the workers with more efficiency and have higher

productivity in the near future. The financial figures which will be represented in the data will

only benefit the organization not the people involved (Schmidt, Wood and Grabski 2016). The

stakeholders will invest based on the non-restricted in the financial statements and will expect

profit which will not be in practical. The company in their reports accessed the targets that were

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT & ASSURANCE

not achievable and even manipulated the figures in order to keep the interest of the investors

alive. This type of practice is not worthy of the act and therefore needs serious attention to it

(Simetinger 2018). The whistle blower opened the fact in front of the whole world which led to

the collapse of the organization (Barr-Pulliam, Brown-Liburd and Sanderson 2017). They gave

feasible information about the unethical acts of the company which led to the elimination of the

unethical acts of the organization which hindered the trust present.

In order to complete the act, the whistle blower should first find out more about the

problems and then find valuable information in relation to it. They should have ample

information to expose the organization (Eaton et al. 2017). Then they should find out a journalist

who can help them in their work and also reveal the truth to the world. They are taking the risk

for doing something good which should be recognized by the federal claims and should be kept

anonymous by the government to keep them safe and sound (Averhals, VanCaneghem and

Willekens 2018). There are laws like Paying payment rights act 1996 which gives the whistle

blowers the right to receive protection for the act if they expose something bad. They should be

protected so that they do not feel any danger in the work and can carry out their work for the

betterment of the people in a great fashion (Schmidt, Wood and Grabski 2016). They should be

protected and appreciated so that many people can come up for being a dedicated whistle blower

in the future for the greater people.

Audit Quality

The role of the auditor and the quality is audit in this fraud case is also noteworthy. The

auditors made sure to incorporate more information which made the expectations of the investors

high and not include relevant information about the true figures of the company (Eaton et al.

2017). They did not undergo true exchange of financial information which could have benefited

not achievable and even manipulated the figures in order to keep the interest of the investors

alive. This type of practice is not worthy of the act and therefore needs serious attention to it

(Simetinger 2018). The whistle blower opened the fact in front of the whole world which led to

the collapse of the organization (Barr-Pulliam, Brown-Liburd and Sanderson 2017). They gave

feasible information about the unethical acts of the company which led to the elimination of the

unethical acts of the organization which hindered the trust present.

In order to complete the act, the whistle blower should first find out more about the

problems and then find valuable information in relation to it. They should have ample

information to expose the organization (Eaton et al. 2017). Then they should find out a journalist

who can help them in their work and also reveal the truth to the world. They are taking the risk

for doing something good which should be recognized by the federal claims and should be kept

anonymous by the government to keep them safe and sound (Averhals, VanCaneghem and

Willekens 2018). There are laws like Paying payment rights act 1996 which gives the whistle

blowers the right to receive protection for the act if they expose something bad. They should be

protected so that they do not feel any danger in the work and can carry out their work for the

betterment of the people in a great fashion (Schmidt, Wood and Grabski 2016). They should be

protected and appreciated so that many people can come up for being a dedicated whistle blower

in the future for the greater people.

Audit Quality

The role of the auditor and the quality is audit in this fraud case is also noteworthy. The

auditors made sure to incorporate more information which made the expectations of the investors

high and not include relevant information about the true figures of the company (Eaton et al.

2017). They did not undergo true exchange of financial information which could have benefited

11AUDIT & ASSURANCE

the people. People like were Ken Lay and Jeff Skilling who was the CEO of the company were

involved in the case with the fraudulent auditing system (Ashcraft et al. 2017). The senior people

of the firm including Arthur Anderson got benefited by the whole process while the common

investors suffered as the prices of the shares dropped to a major level (Gist et al. 2015). The

sudden suffering made certain people go bankrupt which is obviously not something which can

be encouraged in a workplace. The only aim of the organization was to create a goodwill in the

mind of the investors without caring for the people. The hypothetical situation was created just to

trick the investors into something that is not actual but just to seal the original practices and get

away with the fraud ones (Knechel 2016). There were certain people who knew about the frauds

and therefore got away with it. However, there were people who never knew and got bankrupt

for the selfishness of the company.

It is always to be remembered that the external auditors should not be influenced under

any circumstances for making sure that correct accounting has been done. Their privacy should

be maintained as well as they should not be given authority to any kind of benefits rather than

their deserved (Gist et al. 2015). The Independence Policy statement made sure that the external

and internal auditing system aligned with the services that are being audited in a fashion (Eaton

et al. 2017). The committees are responsible for the section of the auditing parties and also to

ensure that they work in a legal manner (Griffiths 2016). In relation to the Independence Policy,

it should be mentioned that there are assurance and approvals from the members before applying

the same in the auditing system. Approval from the Audit and Risk committee is also required in

the proceedings.

According to the business practice code of ethics, it can be said that APES Code 110

measures the personal accounts for the audit management program (Griffiths 2016). The half-

the people. People like were Ken Lay and Jeff Skilling who was the CEO of the company were

involved in the case with the fraudulent auditing system (Ashcraft et al. 2017). The senior people

of the firm including Arthur Anderson got benefited by the whole process while the common

investors suffered as the prices of the shares dropped to a major level (Gist et al. 2015). The

sudden suffering made certain people go bankrupt which is obviously not something which can

be encouraged in a workplace. The only aim of the organization was to create a goodwill in the

mind of the investors without caring for the people. The hypothetical situation was created just to

trick the investors into something that is not actual but just to seal the original practices and get

away with the fraud ones (Knechel 2016). There were certain people who knew about the frauds

and therefore got away with it. However, there were people who never knew and got bankrupt

for the selfishness of the company.

It is always to be remembered that the external auditors should not be influenced under

any circumstances for making sure that correct accounting has been done. Their privacy should

be maintained as well as they should not be given authority to any kind of benefits rather than

their deserved (Gist et al. 2015). The Independence Policy statement made sure that the external

and internal auditing system aligned with the services that are being audited in a fashion (Eaton

et al. 2017). The committees are responsible for the section of the auditing parties and also to

ensure that they work in a legal manner (Griffiths 2016). In relation to the Independence Policy,

it should be mentioned that there are assurance and approvals from the members before applying

the same in the auditing system. Approval from the Audit and Risk committee is also required in

the proceedings.

According to the business practice code of ethics, it can be said that APES Code 110

measures the personal accounts for the audit management program (Griffiths 2016). The half-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.