Audit Report Analysis of Adelaide Brighton Limited: HI6026

VerifiedAdded on 2023/06/04

|15

|3101

|161

Report

AI Summary

This report presents an analysis of an audit assignment focusing on the enhanced auditor reporting requirements implemented in Australia. The assignment examines the annual report of Adelaide Brighton Limited to evaluate the incorporation of key audit matters and the communication of material financial information. The report covers various aspects of the audit, including independence requirements, non-audit services, auditor remuneration, key audit matters and audit procedures performed, audit committee, audit opinion, and the responsibilities of directors and management versus the auditor. The analysis also assesses the effectiveness of the material information reported and addresses potential missing or under-reported information. The report concludes with an overall assessment of the effectiveness of the material information and provides insights into the adoption of enhanced auditor reporting in Australia. The assignment highlights the importance of clear communication and the impact of key audit matters on the audit process. The report also includes an analysis of the audit procedures used to address the key audit matters, ensuring the reliability of the financial statements. The report further provides an understanding of the role and responsibilities of the audit committee in overseeing the audit process. The assignment concludes with an evaluation of the audit opinion and its implications for the stakeholders.

Audit Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 7th Sep 2018.

Executive Summary

1 | P a g e

By student name

Professor

University

Date: 7th Sep 2018.

Executive Summary

1 | P a g e

2

The assignment draws attention towards the fact that there is an urgent need to improve the

quality of the audit report prepared by the Auditor’s of the ASX listed companies for which the

incorporation of the key audit matters along with the better way of communicating the material

financial information is highly recommended. This new form of reporting has been defined as

enhanced auditor’s reporting requirement. In order to evaluate whether the enhanced auditor’s

report meet its very purpose for which it was proposed, the Annual return of one of the ASX

listed companies naming Adelaide Brighton Limited’s for the period 1st july,2016 ending on 31st

December,2017 has been chosen to study and analyze . With a view to facilitating the process of

this evaluation, a set of questionnaire has also been formulated so that to address the issues rose

by it. This process of study and analysis of the Annual return of the Company through the set of

questionnaire can conclude that recommendation of enhanced auditor’s reporting has finally

succeeded to evidence its worth from the financial perspective across the world.

2 | P a g e

The assignment draws attention towards the fact that there is an urgent need to improve the

quality of the audit report prepared by the Auditor’s of the ASX listed companies for which the

incorporation of the key audit matters along with the better way of communicating the material

financial information is highly recommended. This new form of reporting has been defined as

enhanced auditor’s reporting requirement. In order to evaluate whether the enhanced auditor’s

report meet its very purpose for which it was proposed, the Annual return of one of the ASX

listed companies naming Adelaide Brighton Limited’s for the period 1st july,2016 ending on 31st

December,2017 has been chosen to study and analyze . With a view to facilitating the process of

this evaluation, a set of questionnaire has also been formulated so that to address the issues rose

by it. This process of study and analysis of the Annual return of the Company through the set of

questionnaire can conclude that recommendation of enhanced auditor’s reporting has finally

succeeded to evidence its worth from the financial perspective across the world.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Table of Contents

Executive Summary.........................................................................................................................2

Contents……………………………………………………………………………………………………………………………………………..… 3

Introduction.....................................................................................................................................4

Independence requirements...........................................................................................................4

Non-audit services provided............................................................................................................4

Analysis of the Auditor’s remuneration..........................................................................................5

Key audit matters, and audit procedures performed..................................................................5-8

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Directors and management responsibilities versus Auditor's responsibilities to……………………. 9

Material subsequent events……………………………………………………………………………………………….. 10

Assessment of the effectiveness of the material information………………………………………………… 10

Material information which could be missing, under-reported and/or not fully explained or

disclosed………………………………………………………………………………………………………………………………….10

Follow-up questions to the Auditor at the company’s Annual General Meeting.........................11

Conclusion......................................................................................................................................11

References.....................................................................................................................................11

3 | P a g e

Table of Contents

Executive Summary.........................................................................................................................2

Contents……………………………………………………………………………………………………………………………………………..… 3

Introduction.....................................................................................................................................4

Independence requirements...........................................................................................................4

Non-audit services provided............................................................................................................4

Analysis of the Auditor’s remuneration..........................................................................................5

Key audit matters, and audit procedures performed..................................................................5-8

Audit Committee..............................................................................................................................9

Audit Opinion...................................................................................................................................9

Directors and management responsibilities versus Auditor's responsibilities to……………………. 9

Material subsequent events……………………………………………………………………………………………….. 10

Assessment of the effectiveness of the material information………………………………………………… 10

Material information which could be missing, under-reported and/or not fully explained or

disclosed………………………………………………………………………………………………………………………………….10

Follow-up questions to the Auditor at the company’s Annual General Meeting.........................11

Conclusion......................................................................................................................................11

References.....................................................................................................................................11

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

The idea behind emphasizing the need of an enhanced Auditor’s reporting came to IAASB in the

year 2016, though many other countries across the globe had adopted the same long back before

its recommendation by the IAASB. Like the UK have had similar requirements in place since

2013, but after its recommendation by the IAASB it attracted the attention of various other

countries which committed to adopt the same in future and this process of adoption is still going

on(Alexander, 2016). Our research work is primarily focused on the evaluation of the fact

whether the annual report of the company being chosen meet the purpose of enhanced auditor’s

report by incorporating the key audit matters or not.

Independence requirements

An Auditor is said to be independent when his or her expressed opinion is free from any

influence from any party directly or indirectly having vested financial interest in the affairs of the

entity for which the audit opinion is given. The principle of integrity along with the objectivity to

make the correct professional judgment is needed to express an independent view by the auditor.

In our case the statutory Auditor of Adelaide Brighton limited is PWC clearly

acknowledged that to the best of their knowledge and belief that there has not been any breach of

the Section 307C of the Corporation Act, 2001 in relation to Auditor independence requirement

found and non contravention of professional code of conduct has been observed to ensure the

Auditor independence requirement(Arnott, et al., 2017).

4 | P a g e

Introduction

The idea behind emphasizing the need of an enhanced Auditor’s reporting came to IAASB in the

year 2016, though many other countries across the globe had adopted the same long back before

its recommendation by the IAASB. Like the UK have had similar requirements in place since

2013, but after its recommendation by the IAASB it attracted the attention of various other

countries which committed to adopt the same in future and this process of adoption is still going

on(Alexander, 2016). Our research work is primarily focused on the evaluation of the fact

whether the annual report of the company being chosen meet the purpose of enhanced auditor’s

report by incorporating the key audit matters or not.

Independence requirements

An Auditor is said to be independent when his or her expressed opinion is free from any

influence from any party directly or indirectly having vested financial interest in the affairs of the

entity for which the audit opinion is given. The principle of integrity along with the objectivity to

make the correct professional judgment is needed to express an independent view by the auditor.

In our case the statutory Auditor of Adelaide Brighton limited is PWC clearly

acknowledged that to the best of their knowledge and belief that there has not been any breach of

the Section 307C of the Corporation Act, 2001 in relation to Auditor independence requirement

found and non contravention of professional code of conduct has been observed to ensure the

Auditor independence requirement(Arnott, et al., 2017).

4 | P a g e

5

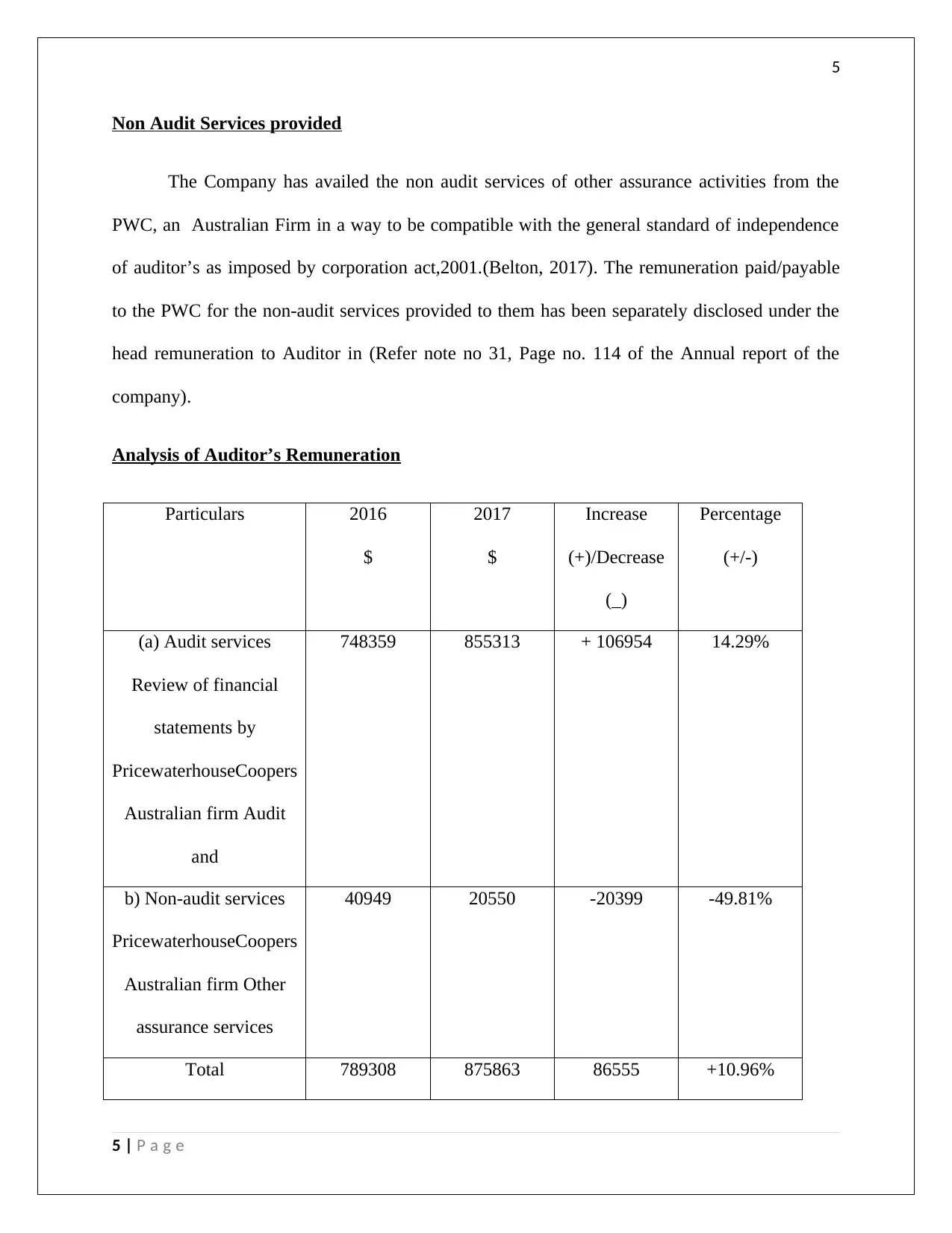

Non Audit Services provided

The Company has availed the non audit services of other assurance activities from the

PWC, an Australian Firm in a way to be compatible with the general standard of independence

of auditor’s as imposed by corporation act,2001.(Belton, 2017). The remuneration paid/payable

to the PWC for the non-audit services provided to them has been separately disclosed under the

head remuneration to Auditor in (Refer note no 31, Page no. 114 of the Annual report of the

company).

Analysis of Auditor’s Remuneration

Particulars 2016

$

2017

$

Increase

(+)/Decrease

(_)

Percentage

(+/-)

(a) Audit services

Review of financial

statements by

PricewaterhouseCoopers

Australian firm Audit

and

748359 855313 + 106954 14.29%

b) Non-audit services

PricewaterhouseCoopers

Australian firm Other

assurance services

40949 20550 -20399 -49.81%

Total 789308 875863 86555 +10.96%

5 | P a g e

Non Audit Services provided

The Company has availed the non audit services of other assurance activities from the

PWC, an Australian Firm in a way to be compatible with the general standard of independence

of auditor’s as imposed by corporation act,2001.(Belton, 2017). The remuneration paid/payable

to the PWC for the non-audit services provided to them has been separately disclosed under the

head remuneration to Auditor in (Refer note no 31, Page no. 114 of the Annual report of the

company).

Analysis of Auditor’s Remuneration

Particulars 2016

$

2017

$

Increase

(+)/Decrease

(_)

Percentage

(+/-)

(a) Audit services

Review of financial

statements by

PricewaterhouseCoopers

Australian firm Audit

and

748359 855313 + 106954 14.29%

b) Non-audit services

PricewaterhouseCoopers

Australian firm Other

assurance services

40949 20550 -20399 -49.81%

Total 789308 875863 86555 +10.96%

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

The above table clearly reflects that though there has been an increase of 14.29% in the

remuneration for the Audit services provided, but at the same time there has been a sharp decline

of 49.81% in the amount of remuneration received by PWC for the non audit services they have

provided and the group resulting into an overall increase of only 10.96% in the amount of

remuneration paid/payable to the Audit Firm(Choy, 2018). Again the reduction in the amount of

remuneration received against the non-audit services by the Audit firm is the reflection of the

fact that auditor’s independence has not been impaired.

Key Audit matters and audit procedure performed

International Standards on Auditing (ISA 701) prescribes the incorporation of key audit

matters (KAM) in an independent auditor’s report. KAM are the matters based on the auditor’s

professional judgment to be informed to those charged with the governance of the entity, which

are summarized hereunder.

i) Account receivable:

Key audit matter

During the year the group identified the discrepancies in form of being underpaid for the

products supplied by it which accounts for impaired amount of accounts receivable of $17.1

million being subsequently included in the category of bad debts in the aforesaid period

through the process of an external expert engagement reflecting the higher risk of material

misstatement(Das, 2017).

6 | P a g e

The above table clearly reflects that though there has been an increase of 14.29% in the

remuneration for the Audit services provided, but at the same time there has been a sharp decline

of 49.81% in the amount of remuneration received by PWC for the non audit services they have

provided and the group resulting into an overall increase of only 10.96% in the amount of

remuneration paid/payable to the Audit Firm(Choy, 2018). Again the reduction in the amount of

remuneration received against the non-audit services by the Audit firm is the reflection of the

fact that auditor’s independence has not been impaired.

Key Audit matters and audit procedure performed

International Standards on Auditing (ISA 701) prescribes the incorporation of key audit

matters (KAM) in an independent auditor’s report. KAM are the matters based on the auditor’s

professional judgment to be informed to those charged with the governance of the entity, which

are summarized hereunder.

i) Account receivable:

Key audit matter

During the year the group identified the discrepancies in form of being underpaid for the

products supplied by it which accounts for impaired amount of accounts receivable of $17.1

million being subsequently included in the category of bad debts in the aforesaid period

through the process of an external expert engagement reflecting the higher risk of material

misstatement(Das, 2017).

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Audit procedure adopted

The procedure adopted to deal with the matter included to get satisfied with the fact that

expert’s opinion can be used for the purpose of audit by evaluating his Competency, objectives

and the results of the work done by the expert involving the test of control. The procedure further

performed to directly obtain the confirmation of outstanding balances from certain selected

customers and those from whom no communication in response to the request for confirmation

received, the proof of product delivery along with the subsequent cash received against such

delivery involving the procedure of testing of balances(Farmer, 2018).

ii) Recoverability of the Goodwill and property, Plant and equipment

Key audit matter

The group formulated a model to assess the certainty of the realisation of the goodwill and plant

and equipment so that the correct carrying amount of these assets being represented by the

financial statement(Goldmann, 2016). Considering the significance of the recorded values of

goodwill and plant and equipment together with the judgments and assumptions used to prepare

a discounted cash flow model by the group make it a key audit matter.

Audit procedure adopted

The issue is dealt with by performing the analytical procedure to evaluate the process of

developing the model of discounted cash flows by comparing the the Board approved budget

with the 2018 forecast figures in the models and for the the discounted rates and growth rate

assumptions performed the sensitivity analysis of along with the substantive tests of detail by

7 | P a g e

Audit procedure adopted

The procedure adopted to deal with the matter included to get satisfied with the fact that

expert’s opinion can be used for the purpose of audit by evaluating his Competency, objectives

and the results of the work done by the expert involving the test of control. The procedure further

performed to directly obtain the confirmation of outstanding balances from certain selected

customers and those from whom no communication in response to the request for confirmation

received, the proof of product delivery along with the subsequent cash received against such

delivery involving the procedure of testing of balances(Farmer, 2018).

ii) Recoverability of the Goodwill and property, Plant and equipment

Key audit matter

The group formulated a model to assess the certainty of the realisation of the goodwill and plant

and equipment so that the correct carrying amount of these assets being represented by the

financial statement(Goldmann, 2016). Considering the significance of the recorded values of

goodwill and plant and equipment together with the judgments and assumptions used to prepare

a discounted cash flow model by the group make it a key audit matter.

Audit procedure adopted

The issue is dealt with by performing the analytical procedure to evaluate the process of

developing the model of discounted cash flows by comparing the the Board approved budget

with the 2018 forecast figures in the models and for the the discounted rates and growth rate

assumptions performed the sensitivity analysis of along with the substantive tests of detail by

7 | P a g e

8

checking that previous year’s budgets were materially consistent with the actual performance to

ensure the reliability of the forecasts made by the group(Grenier, 2017).

iii) Estimation of restoration provision

Key audit matter

The key to the estimation of the rehabilitation provision demands significant judgment to assess

the correct future costs along with the rehabilitation requirements. The rehabilitation provisions

were made for two types of sites, first category being those which were actively remediated and

second being those were not actively remediated(Jefferson, 2017) .The provisions for the first

was represented by costs for completion of the current stage rehabilitation and estimated cost

for future stages of rehabilitation, while second figure of provision involved the process of

cost estimation annualy by operational staff. Future estimation costs require the use of cost

inflation and discounted rates.

Audit procedure adopted

For dealing the above matter the detailed analytical procedure was adopted by checking that

based on our knowledge of group’s operation provision which is in respect to the sites which are

in need of rehabilation,reviewing agreements of new lease contracts, reviewing minutes of

meeting, and engaging in discussion with management . Again the substantive tests of detail

were performed where material change to normal costs was noticed from the previous period.

iv) Accounting for business combinations

Key audit matter

8 | P a g e

checking that previous year’s budgets were materially consistent with the actual performance to

ensure the reliability of the forecasts made by the group(Grenier, 2017).

iii) Estimation of restoration provision

Key audit matter

The key to the estimation of the rehabilitation provision demands significant judgment to assess

the correct future costs along with the rehabilitation requirements. The rehabilitation provisions

were made for two types of sites, first category being those which were actively remediated and

second being those were not actively remediated(Jefferson, 2017) .The provisions for the first

was represented by costs for completion of the current stage rehabilitation and estimated cost

for future stages of rehabilitation, while second figure of provision involved the process of

cost estimation annualy by operational staff. Future estimation costs require the use of cost

inflation and discounted rates.

Audit procedure adopted

For dealing the above matter the detailed analytical procedure was adopted by checking that

based on our knowledge of group’s operation provision which is in respect to the sites which are

in need of rehabilation,reviewing agreements of new lease contracts, reviewing minutes of

meeting, and engaging in discussion with management . Again the substantive tests of detail

were performed where material change to normal costs was noticed from the previous period.

iv) Accounting for business combinations

Key audit matter

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

The fair value of assets and liabilities acquired by the group to be ascertained as per the

Australian Accounting Standards that demanded the significant judgment for which independent

valuation experts were engaged by the firm(Jefferson, 2017).

Audit procedure adopted

For this the Audit firm applied the substantive tests of detail by where the individual valuation

experts have been recognised group experts and the evaluation for the for each individual expert

valuer’s method, competency and objectivity was done.

v) Measuring the quantity of inventory of raw materials and work in progress

Key audit matter

As the raw material and work in progress were kept in the inventory for quite a long period,

hence ensuring the correct measurement of their quantity became a key audit factor for which

independent surveyor’s were appointed by the group to perform the volumetric surveys in order

to serve the above purpose(Sithole, et al., 2017).

Audit procedure adopted

For this the Audit firm applied the substantive tests of detail by treating the individual valuation

experts as group experts and the evaluation of each individual expert value’s method,

competency and objectivity was done,performing detailed substantive tests through obtaining

and inspecting results ofthe survey results for material stockpiled in various inventory locations

reperforming conversion of the quantities of the group.

Audit Committee

9 | P a g e

The fair value of assets and liabilities acquired by the group to be ascertained as per the

Australian Accounting Standards that demanded the significant judgment for which independent

valuation experts were engaged by the firm(Jefferson, 2017).

Audit procedure adopted

For this the Audit firm applied the substantive tests of detail by where the individual valuation

experts have been recognised group experts and the evaluation for the for each individual expert

valuer’s method, competency and objectivity was done.

v) Measuring the quantity of inventory of raw materials and work in progress

Key audit matter

As the raw material and work in progress were kept in the inventory for quite a long period,

hence ensuring the correct measurement of their quantity became a key audit factor for which

independent surveyor’s were appointed by the group to perform the volumetric surveys in order

to serve the above purpose(Sithole, et al., 2017).

Audit procedure adopted

For this the Audit firm applied the substantive tests of detail by treating the individual valuation

experts as group experts and the evaluation of each individual expert value’s method,

competency and objectivity was done,performing detailed substantive tests through obtaining

and inspecting results ofthe survey results for material stockpiled in various inventory locations

reperforming conversion of the quantities of the group.

Audit Committee

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Yes Adelaide Brighton Limited has had an Audit, Risk and Compliance Committee in

place. Graeme Pettigrew is the Chairman of the Audit, Risk and compliance committee that

consists of four non-executive directors naming Mr. Graeme Pettigrew (Chairman), Mr. Les

Hosking, Ms. Arlene Tansey and Mr. Zlatko Todorcevski. Yes there is an Audit Committee

charter for the Company(Trieu, 2017).

Audit Opinion

The Audit opinion given in the instant case is an unqualified one, which clearly states that

the financial statement for the year ending 31st December, 2018 provides a true and fair view of

the financial position of the group complying with the provisions of the corporation Act, 2001,

Australian Accounting standard and corporation regulations, 2001.

How do the Directors’ and Management’s responsibilities differ from the Auditor’s

responsibilities in relation to the financial report?

Director’s responsibility to the financial report includes preparation of financial statement

as per the Corporations Act 2001 and Australian Accounting Standards and implementation of

an effective system of internal control so as to provide assurance about the true and fair view of

the financial position of the entity by eliminating the probability of fraud, error or material

misstatement in such financial statement together with the determination of ability of the entity

to continue as a going concern with the assistance of a realistic assumption(Werner, 2017).

Auditor’s responsibility is confined to express his opinion with a reasonable assurance on

the financial statement prepared by the management of the organization whether it is free from

fraud, error or material misstatement, but his opinion on such financial statement cannot be

10 | P a g e

Yes Adelaide Brighton Limited has had an Audit, Risk and Compliance Committee in

place. Graeme Pettigrew is the Chairman of the Audit, Risk and compliance committee that

consists of four non-executive directors naming Mr. Graeme Pettigrew (Chairman), Mr. Les

Hosking, Ms. Arlene Tansey and Mr. Zlatko Todorcevski. Yes there is an Audit Committee

charter for the Company(Trieu, 2017).

Audit Opinion

The Audit opinion given in the instant case is an unqualified one, which clearly states that

the financial statement for the year ending 31st December, 2018 provides a true and fair view of

the financial position of the group complying with the provisions of the corporation Act, 2001,

Australian Accounting standard and corporation regulations, 2001.

How do the Directors’ and Management’s responsibilities differ from the Auditor’s

responsibilities in relation to the financial report?

Director’s responsibility to the financial report includes preparation of financial statement

as per the Corporations Act 2001 and Australian Accounting Standards and implementation of

an effective system of internal control so as to provide assurance about the true and fair view of

the financial position of the entity by eliminating the probability of fraud, error or material

misstatement in such financial statement together with the determination of ability of the entity

to continue as a going concern with the assistance of a realistic assumption(Werner, 2017).

Auditor’s responsibility is confined to express his opinion with a reasonable assurance on

the financial statement prepared by the management of the organization whether it is free from

fraud, error or material misstatement, but his opinion on such financial statement cannot be

10 | P a g e

11

guaranteed to the fact that the audit performed as per the Australian Accounting standards will

be able to indicate all of the significant material misstatement found if any.

Events occurring after the balance sheet date

None of the events or matter or circumstance were noticed since 31 December 2017 that

has significantly affected, or may significantly affect the operations of the Group, those (Erik &

Jan, 2017) .

As an interested third party stakeholder, make an assessment of the effectiveness of the

material information reported by the Auditor in your conclusion.

In case of the Annual report of the Adelaide Brighton Limited certain other important

relevant material information like, Sustainability Report , Managing Director and CEO Report,

Chairman’s Report Finance Report, Financial History, and Corporate Governance Statement,

Performance Summary, Information for Shareholders,Map and Review of Operations other than

the Director’s Report and Diversity Report were not made available to the Audit firm PWC and

this was clearly mentioned in the auditor’s report that somewhere provided a wide area of

thought to the prospective stakeholders to make an effective decision making. Hence

effectiveness of this report has somewhere been distorted to a great extent.

Material information which could be missing, under-reported and/or not fully explained

or disclosed in an effective way for the intended users.

The material information which were found absolutely missing in this Annual report were

like, Sustainability Report , Managing Director and CEO Report, Chairman’s Report Finance

Report, Financial History, and Corporate Governance Statement, Performance Summary,

Information for Shareholders,Map and Review of Operations and missing of the above referred

11 | P a g e

guaranteed to the fact that the audit performed as per the Australian Accounting standards will

be able to indicate all of the significant material misstatement found if any.

Events occurring after the balance sheet date

None of the events or matter or circumstance were noticed since 31 December 2017 that

has significantly affected, or may significantly affect the operations of the Group, those (Erik &

Jan, 2017) .

As an interested third party stakeholder, make an assessment of the effectiveness of the

material information reported by the Auditor in your conclusion.

In case of the Annual report of the Adelaide Brighton Limited certain other important

relevant material information like, Sustainability Report , Managing Director and CEO Report,

Chairman’s Report Finance Report, Financial History, and Corporate Governance Statement,

Performance Summary, Information for Shareholders,Map and Review of Operations other than

the Director’s Report and Diversity Report were not made available to the Audit firm PWC and

this was clearly mentioned in the auditor’s report that somewhere provided a wide area of

thought to the prospective stakeholders to make an effective decision making. Hence

effectiveness of this report has somewhere been distorted to a great extent.

Material information which could be missing, under-reported and/or not fully explained

or disclosed in an effective way for the intended users.

The material information which were found absolutely missing in this Annual report were

like, Sustainability Report , Managing Director and CEO Report, Chairman’s Report Finance

Report, Financial History, and Corporate Governance Statement, Performance Summary,

Information for Shareholders,Map and Review of Operations and missing of the above referred

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.