HI6026 Audit Report: Embracing Enhanced Auditor Reporting in Australia

VerifiedAdded on 2023/06/04

|11

|3077

|270

Report

AI Summary

This report examines how companies listed on the Australian Stock Exchange (ASX) adhere to auditing standards, emphasizing enhanced transparency in financial reporting. It covers key aspects such as the auditor's independence declaration, opinion, non-audit services, remuneration, the audit committee's role and composition, the auditor's report to shareholders, and a review of key audit matters. The report analyzes Altium Limited's annual report to assess its compliance with auditing guidelines and standards, referencing the Corporations Act 2001 and relevant accounting standards. It highlights the importance of auditor independence, ethical conduct, and unbiased opinions in providing stakeholders with reliable information for decision-making. The analysis includes a discussion of different types of auditor opinions, the implications of non-audit services, and the role of the audit committee in ensuring financial compliance and internal controls.

Audit, Assurance and Compliance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is meant to highlight how companies listed in Australia Stock Exchange

conform to auditing standards. The report elaborates on auditing requirements and

reporting which is aimed at enhancing the transparency in financial reporting. The report

will touch on various issues including auditors opinion, auditors remuneration, the roles

and responsibilities of auditors and the management just to mention a few.

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Background of the Report............................................................................................................3

Scope of the Report.....................................................................................................................3

2

This report is meant to highlight how companies listed in Australia Stock Exchange

conform to auditing standards. The report elaborates on auditing requirements and

reporting which is aimed at enhancing the transparency in financial reporting. The report

will touch on various issues including auditors opinion, auditors remuneration, the roles

and responsibilities of auditors and the management just to mention a few.

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Background of the Report............................................................................................................3

Scope of the Report.....................................................................................................................3

2

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration................................................................................4

2) Independent auditor’s opinion..........................................................................................5

3) Non-Audit services performed by the Auditor.................................................................5

4) Auditors’ Remuneration....................................................................................................6

5) Role, functions and composition of the Audit Committee................................................7

6) Independent Auditors report to the shareholders..............................................................7

7) Review all Key Audit Matters..........................................................................................8

Conclusion.......................................................................................................................................9

References........................................................................................................................................9

3

1) Auditor’s Independence Declaration................................................................................4

2) Independent auditor’s opinion..........................................................................................5

3) Non-Audit services performed by the Auditor.................................................................5

4) Auditors’ Remuneration....................................................................................................6

5) Role, functions and composition of the Audit Committee................................................7

6) Independent Auditors report to the shareholders..............................................................7

7) Review all Key Audit Matters..........................................................................................8

Conclusion.......................................................................................................................................9

References........................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Background of the Report

The main purpose of audit reporting is to enhance transparency. The audit report targeted the

annual report of Altium limited so as to ascertain the conformance of that annual report to the set

standards. The audit report will be of use to all the stakeholders, both internal and external, with

regards to making prudent decisions going forward

Scope of the Report

This report is mainly aimed at analyzing various aspects as pertaining to audit reporting. The

report will mainly touch on seven key issues namely; Auditor’s Independence Declaration;

Independent Auditor’s Report; The report will also highlight the Non-audit services which are

performed by the auditor; Auditor’s Remuneration as per the financial statement; Audit

Committee, its makeup, roles and functions; Independent Auditor’s Report to the shareholders

and lastly the analysis of Key Audit issues. The report will focus on Altium Limited which is an

American based software company

Discussion

As earlier indicated, Altium Limited is an American based company, listed in the Australia stock

exchange (ASX). The company is a renowned software producer mainly specialized in PC-based

electronic design software (Altium Limited, 2018). By virtue of the organization being listed in

the ASX, it has to adhere to strict guidelines and conformance to quality standard auditing

reporting system it is through the evaluation of the financial annual report that one can be able to

ascertain whether the guidelines and standards of auditing have been followed.

1) Auditor’s Independence Declaration

The primary law that stipulates and governs the compliance of audit processes and reporting is

the Corporations Act, 2001(CCH Australia Limited, 2011). The conduct, rules and procedures of

how an auditor carries out his mandate is described in that act. The act also stipulates the

responsibilities of the management in facilitating the auditor when performing his tasks. The law

actually prohibits the interference of the management in the auditing process.

The issue of ethical considerations which governs the auditor has also been captured in the act,

where it stipulates that an auditor or the auditing committee for that matter is supposed to

produce an unbiased, professional and independent report. At times, there is a high likely hood

4

Background of the Report

The main purpose of audit reporting is to enhance transparency. The audit report targeted the

annual report of Altium limited so as to ascertain the conformance of that annual report to the set

standards. The audit report will be of use to all the stakeholders, both internal and external, with

regards to making prudent decisions going forward

Scope of the Report

This report is mainly aimed at analyzing various aspects as pertaining to audit reporting. The

report will mainly touch on seven key issues namely; Auditor’s Independence Declaration;

Independent Auditor’s Report; The report will also highlight the Non-audit services which are

performed by the auditor; Auditor’s Remuneration as per the financial statement; Audit

Committee, its makeup, roles and functions; Independent Auditor’s Report to the shareholders

and lastly the analysis of Key Audit issues. The report will focus on Altium Limited which is an

American based software company

Discussion

As earlier indicated, Altium Limited is an American based company, listed in the Australia stock

exchange (ASX). The company is a renowned software producer mainly specialized in PC-based

electronic design software (Altium Limited, 2018). By virtue of the organization being listed in

the ASX, it has to adhere to strict guidelines and conformance to quality standard auditing

reporting system it is through the evaluation of the financial annual report that one can be able to

ascertain whether the guidelines and standards of auditing have been followed.

1) Auditor’s Independence Declaration

The primary law that stipulates and governs the compliance of audit processes and reporting is

the Corporations Act, 2001(CCH Australia Limited, 2011). The conduct, rules and procedures of

how an auditor carries out his mandate is described in that act. The act also stipulates the

responsibilities of the management in facilitating the auditor when performing his tasks. The law

actually prohibits the interference of the management in the auditing process.

The issue of ethical considerations which governs the auditor has also been captured in the act,

where it stipulates that an auditor or the auditing committee for that matter is supposed to

produce an unbiased, professional and independent report. At times, there is a high likely hood

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that external interference might bar the auditor from achieving that which he is mandated to and

that’s which they ought to be vigilant and incorruptible in order to give a credible and reliable

audit report (CAANZ (Chartered Accountants Australia & New Zealand), 2016). From the

provisions of Corporations Act, 2001 mainly APES 110, indicate the ethical considerations

which are supposed to govern how an auditor performs his tasks that section of the Corporations

act stipulate that an auditor is required to declare that he/she acted in an ethical manner while

performing their roles and duties. This declaration by the auditor is supposed to be captured in

the declaration of independence which is a standalone section in the annual report of an

organization (Chartered Accountants (Australia-Newzealand), 2018).

It is paramount for the auditor to be independent preferably not working within the organization

in order to avoid such internal interference. One of the regulations which govern the

independence of an auditor is Section 307C of the Corporations Act, 2001, which in a nut shell

indicates that an auditor needs to state the declaration of independence and capture the same as

part of the organization’s annual report. This particular section of the law clearly states that an

auditor is supposed to display the highest level of independence from the organization (Wolters

Kluwer, 2018).

From the annual report of Altium LTD, it can be noted that the auditor has clearly declared their

independence from both internal and external influence and that they have carried out their

mandate with in an ethical manner. All this was captured in the auditor’s statement of declaration

of independence as stipulated in the Corporations Act of 2001 and also the code of ethics

(Altium Limited, 2017).

2) Independent auditor’s opinion

As indicated by (Porter et al., 2014), an audit processes is aimed at providing an honest unbiased

opinion with regards to the financial statement of an organization which are prepared initially by

the management. The reason for the auditor’s report is to provide the relevant stakeholders with

a reliable document which they can use to make key decisions, financial or otherwise with

regards to the organization (Basu, 2010). From the auditor’s report, the most essential

information to be obtained is the auditor’s opinion. An auditor’s opinion can be described as a

written statement which indicates the qualified, unbiased and independent analysis made by the

auditor with regards to the accuracy and completeness of an organizations financial statement.

5

that’s which they ought to be vigilant and incorruptible in order to give a credible and reliable

audit report (CAANZ (Chartered Accountants Australia & New Zealand), 2016). From the

provisions of Corporations Act, 2001 mainly APES 110, indicate the ethical considerations

which are supposed to govern how an auditor performs his tasks that section of the Corporations

act stipulate that an auditor is required to declare that he/she acted in an ethical manner while

performing their roles and duties. This declaration by the auditor is supposed to be captured in

the declaration of independence which is a standalone section in the annual report of an

organization (Chartered Accountants (Australia-Newzealand), 2018).

It is paramount for the auditor to be independent preferably not working within the organization

in order to avoid such internal interference. One of the regulations which govern the

independence of an auditor is Section 307C of the Corporations Act, 2001, which in a nut shell

indicates that an auditor needs to state the declaration of independence and capture the same as

part of the organization’s annual report. This particular section of the law clearly states that an

auditor is supposed to display the highest level of independence from the organization (Wolters

Kluwer, 2018).

From the annual report of Altium LTD, it can be noted that the auditor has clearly declared their

independence from both internal and external influence and that they have carried out their

mandate with in an ethical manner. All this was captured in the auditor’s statement of declaration

of independence as stipulated in the Corporations Act of 2001 and also the code of ethics

(Altium Limited, 2017).

2) Independent auditor’s opinion

As indicated by (Porter et al., 2014), an audit processes is aimed at providing an honest unbiased

opinion with regards to the financial statement of an organization which are prepared initially by

the management. The reason for the auditor’s report is to provide the relevant stakeholders with

a reliable document which they can use to make key decisions, financial or otherwise with

regards to the organization (Basu, 2010). From the auditor’s report, the most essential

information to be obtained is the auditor’s opinion. An auditor’s opinion can be described as a

written statement which indicates the qualified, unbiased and independent analysis made by the

auditor with regards to the accuracy and completeness of an organizations financial statement.

5

There are mainly four types of opinions that can be expressed by the auditor namely; unqualified

opinion, qualified opinion, disclaimer and lastly adverse opinion.

As indicated in the annual report of Altium LTD, the auditor gave an unqualified opinion

indicating that the organization conformed to the required accounting standards and practices and

that they have prepared their financial statements in a clear and transparent manner.

3) Non-Audit services performed by the Auditor

Non-audit services can be referred to as those services which are carried out by the auditor

outside of the prescribed audit services. Without proper judgment and a high ethical standing,

such services can elicit personal interest of the auditor to the business and in turn affect the

independence of the auditor (Frankel, 2018). In some countries, auditors are barred from taking

up such services in those companies which they are auditing. Some scholars argue that this is

indeed best practice in order to prevent cases of breech of independence. For example in the

United States of America, Sarbanes and Oxley act prohibit auditors from undertaking such non-

auditing services for the companies they are auditing (Mitchell, 2018). Currently there are no

such restrictions in Australia that prohibit auditors from undertaking the non-audit services in

companies they are auditing. The auditors are however required to declare their independence in

writing and in the instance of a possible conflict of interest, then the auditor must absolve

themselves from undertaking the task.

From the annual report, it can be seen that the auditors in Altium LTD carried out non-auditing

services such as tax consulting in the year 2016 however similar services were not done in 2017

It is assumed that since the auditors declared their independence statement in the report, they

carried out those services with regards to ethical considerations and high levels of objectivity and

independence (Altium Limited, 2017).

4) Auditors’ Remuneration

Just like any other expense, the auditor’s remuneration needs to be captured in the organizations

expenses. An auditor’s remuneration can be termed as the fee payable to the auditor for carrying

out his tasks for the organization. The remuneration is for both the audit and non-audit services

provided by the auditor (Caanz , 2015).

6

opinion, qualified opinion, disclaimer and lastly adverse opinion.

As indicated in the annual report of Altium LTD, the auditor gave an unqualified opinion

indicating that the organization conformed to the required accounting standards and practices and

that they have prepared their financial statements in a clear and transparent manner.

3) Non-Audit services performed by the Auditor

Non-audit services can be referred to as those services which are carried out by the auditor

outside of the prescribed audit services. Without proper judgment and a high ethical standing,

such services can elicit personal interest of the auditor to the business and in turn affect the

independence of the auditor (Frankel, 2018). In some countries, auditors are barred from taking

up such services in those companies which they are auditing. Some scholars argue that this is

indeed best practice in order to prevent cases of breech of independence. For example in the

United States of America, Sarbanes and Oxley act prohibit auditors from undertaking such non-

auditing services for the companies they are auditing (Mitchell, 2018). Currently there are no

such restrictions in Australia that prohibit auditors from undertaking the non-audit services in

companies they are auditing. The auditors are however required to declare their independence in

writing and in the instance of a possible conflict of interest, then the auditor must absolve

themselves from undertaking the task.

From the annual report, it can be seen that the auditors in Altium LTD carried out non-auditing

services such as tax consulting in the year 2016 however similar services were not done in 2017

It is assumed that since the auditors declared their independence statement in the report, they

carried out those services with regards to ethical considerations and high levels of objectivity and

independence (Altium Limited, 2017).

4) Auditors’ Remuneration

Just like any other expense, the auditor’s remuneration needs to be captured in the organizations

expenses. An auditor’s remuneration can be termed as the fee payable to the auditor for carrying

out his tasks for the organization. The remuneration is for both the audit and non-audit services

provided by the auditor (Caanz , 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

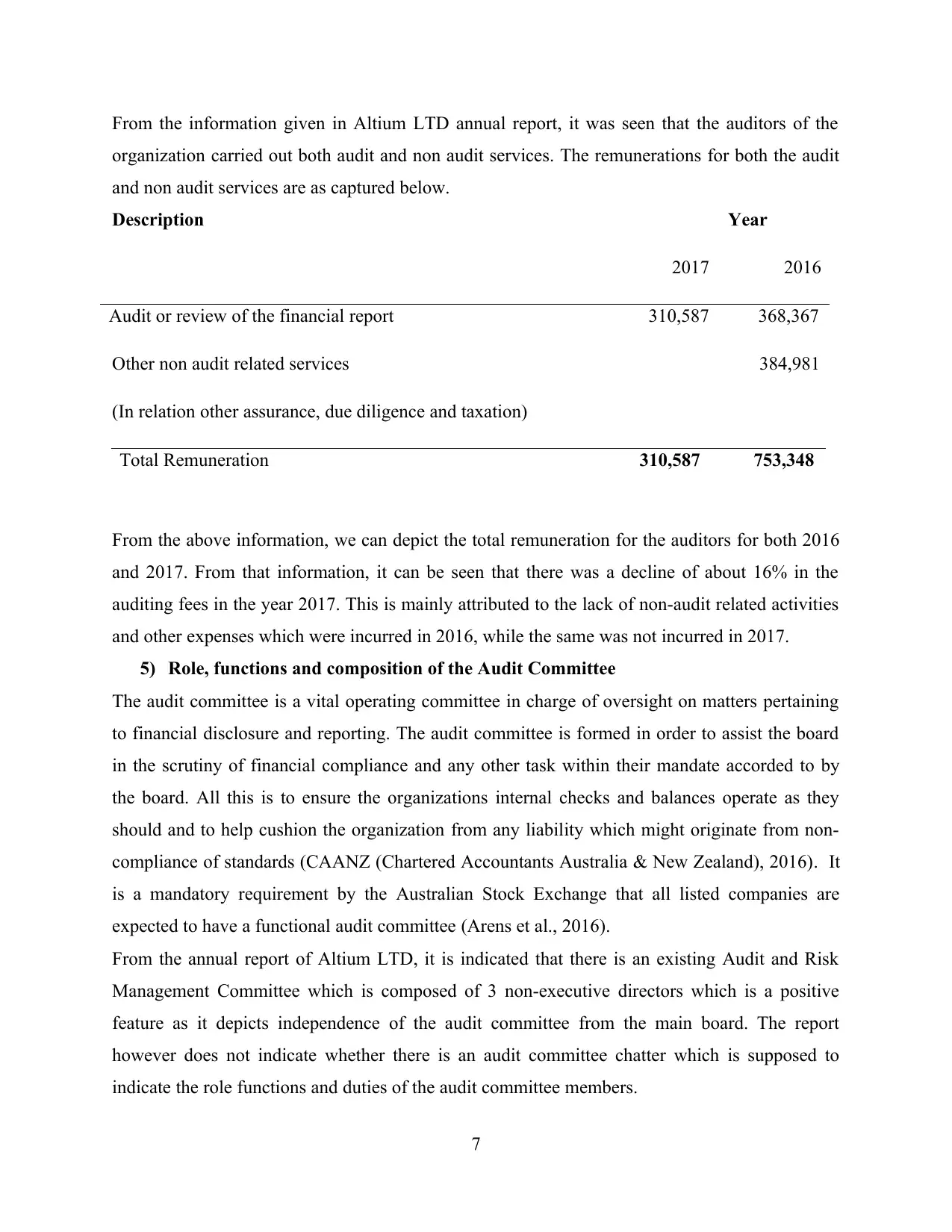

From the information given in Altium LTD annual report, it was seen that the auditors of the

organization carried out both audit and non audit services. The remunerations for both the audit

and non audit services are as captured below.

Description Year

2017 2016

Audit or review of the financial report 310,587 368,367

Other non audit related services 384,981

(In relation other assurance, due diligence and taxation)

Total Remuneration 310,587 753,348

From the above information, we can depict the total remuneration for the auditors for both 2016

and 2017. From that information, it can be seen that there was a decline of about 16% in the

auditing fees in the year 2017. This is mainly attributed to the lack of non-audit related activities

and other expenses which were incurred in 2016, while the same was not incurred in 2017.

5) Role, functions and composition of the Audit Committee

The audit committee is a vital operating committee in charge of oversight on matters pertaining

to financial disclosure and reporting. The audit committee is formed in order to assist the board

in the scrutiny of financial compliance and any other task within their mandate accorded to by

the board. All this is to ensure the organizations internal checks and balances operate as they

should and to help cushion the organization from any liability which might originate from non-

compliance of standards (CAANZ (Chartered Accountants Australia & New Zealand), 2016). It

is a mandatory requirement by the Australian Stock Exchange that all listed companies are

expected to have a functional audit committee (Arens et al., 2016).

From the annual report of Altium LTD, it is indicated that there is an existing Audit and Risk

Management Committee which is composed of 3 non-executive directors which is a positive

feature as it depicts independence of the audit committee from the main board. The report

however does not indicate whether there is an audit committee chatter which is supposed to

indicate the role functions and duties of the audit committee members.

7

organization carried out both audit and non audit services. The remunerations for both the audit

and non audit services are as captured below.

Description Year

2017 2016

Audit or review of the financial report 310,587 368,367

Other non audit related services 384,981

(In relation other assurance, due diligence and taxation)

Total Remuneration 310,587 753,348

From the above information, we can depict the total remuneration for the auditors for both 2016

and 2017. From that information, it can be seen that there was a decline of about 16% in the

auditing fees in the year 2017. This is mainly attributed to the lack of non-audit related activities

and other expenses which were incurred in 2016, while the same was not incurred in 2017.

5) Role, functions and composition of the Audit Committee

The audit committee is a vital operating committee in charge of oversight on matters pertaining

to financial disclosure and reporting. The audit committee is formed in order to assist the board

in the scrutiny of financial compliance and any other task within their mandate accorded to by

the board. All this is to ensure the organizations internal checks and balances operate as they

should and to help cushion the organization from any liability which might originate from non-

compliance of standards (CAANZ (Chartered Accountants Australia & New Zealand), 2016). It

is a mandatory requirement by the Australian Stock Exchange that all listed companies are

expected to have a functional audit committee (Arens et al., 2016).

From the annual report of Altium LTD, it is indicated that there is an existing Audit and Risk

Management Committee which is composed of 3 non-executive directors which is a positive

feature as it depicts independence of the audit committee from the main board. The report

however does not indicate whether there is an audit committee chatter which is supposed to

indicate the role functions and duties of the audit committee members.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6) Independent Auditors report to the shareholders

As stipulated by the Australian Accounting Standards, it is the responsibility of the auditor to

submit their report and express their professional view on the financial statements provided by

the organization. It is from the auditor’s report and opinion for that matter that various users of

the report are going to base their decisions on (Gay & Simnett, 2015).

On the other hand, it is the responsibility of the management through their accounting policies, to

prepare their financial statements. This is by no means the task of auditors as occasionally

mistaken (Knechel & Salterio, 2016). The management is supposed to ensure that they formulate

their reports in conformance to the set standards and avoidance of misstatements (Media, 2015).

Subsequent events are any identified activities which may occur after the completion of a

financial reporting period of an organization. Reporting of any subsequent events to the

stakeholders should also be done. This is done so as to ascertain their overall impact on the

financial statement for that particular period. One example can be obtained from the annual

report of Altium LTD where the organization undertook an acquisition of Upverter Inc in August

2017. The implications of that takeover were huge and the company was supposed to give an

issuance of ordinary shares. .

7) Review all Key Audit Matters

For the purposes of promoting transparency in audit reporting, compliance of new regulations are

required to be undertaken by the auditors. These requirements are known as the Enhanced Audit

Reporting Requirements. These requirements mandate the auditors contracted by the company to

report any other significant matter on a separate report.

At times there are key issues which might have a major impact on the financial statements of a

company and as such it is important to highlight such matters to the stakeholders. In the annual

report f Altium LTD, two such key matters were noted; Recoverability of deferred tax assets

Carrying value of goodwill and other definite lived intangible assets(Altium Limited,

2017)

These two issues were addressed as follows:

8

As stipulated by the Australian Accounting Standards, it is the responsibility of the auditor to

submit their report and express their professional view on the financial statements provided by

the organization. It is from the auditor’s report and opinion for that matter that various users of

the report are going to base their decisions on (Gay & Simnett, 2015).

On the other hand, it is the responsibility of the management through their accounting policies, to

prepare their financial statements. This is by no means the task of auditors as occasionally

mistaken (Knechel & Salterio, 2016). The management is supposed to ensure that they formulate

their reports in conformance to the set standards and avoidance of misstatements (Media, 2015).

Subsequent events are any identified activities which may occur after the completion of a

financial reporting period of an organization. Reporting of any subsequent events to the

stakeholders should also be done. This is done so as to ascertain their overall impact on the

financial statement for that particular period. One example can be obtained from the annual

report of Altium LTD where the organization undertook an acquisition of Upverter Inc in August

2017. The implications of that takeover were huge and the company was supposed to give an

issuance of ordinary shares. .

7) Review all Key Audit Matters

For the purposes of promoting transparency in audit reporting, compliance of new regulations are

required to be undertaken by the auditors. These requirements are known as the Enhanced Audit

Reporting Requirements. These requirements mandate the auditors contracted by the company to

report any other significant matter on a separate report.

At times there are key issues which might have a major impact on the financial statements of a

company and as such it is important to highlight such matters to the stakeholders. In the annual

report f Altium LTD, two such key matters were noted; Recoverability of deferred tax assets

Carrying value of goodwill and other definite lived intangible assets(Altium Limited,

2017)

These two issues were addressed as follows:

8

The first issue was recoverability of deferred tax assets- This actually pertains to the

identification of deferred tax assets n accordance to the Australian Accounting Standards. As

described in the standards, the level to which tax assets deferred can be known is by ascertaining

the future probability of the company, and by so doing calculating the taxable future profits. Of

key importance therefore is to ensure that the company remains on a profitable trajectory so that

the benefits of the tax deferred can be seen. The purpose of deferred tax assets is to lessen the tax

liability by providing tax benefits on future income, since those tax liabilities can be deducted

from future profits.

The amount of money involved in the deferred tax assets is what makes this to be a key audit

matter. It will be up to the prudence of the auditor to ascertain whether the profits to be generated

will be sufficient enough in future in order to avail the tax benefit later. It was therefore noted

that the auditors of Altium had to carry out test in order to ascertain the profits of the company

on the years to come before making their recommendation.

The second matter was Carrying value of goodwill and other definite lived intangible assets

whereby it is necessary for the assets of the organization to be taken through an annual

impairment assessment as stipulated by the Australian Accounting Standards. This is inclusive of

intangible assets like goodwill. At the end of the financial year, these assets are checked for the

impairment. Certain financial models like estimation of cash flows and discount rates were put in

place by the management in order to perform the impairment test. This prompted the auditors to

view this as a substantial audit matter.

Conclusion

This report aims at establishing whether the organization and the contracted auditor played their

role in ensuring that the accounting standards set were adhered to. The report was also aimed at

establishing the role played by audit reporting in ensuring there is transparency and

accountability within the organization. Various key issues were noted from the annual and

auditor’s report. despite the unqualified opinion by the auditor, which is a positive for Altium

LTD, it s important for the organization to consider displaying their audit committee chatter or

the key details pertaining to that committee to further strengthen the notion of auditors

independence to the stakeholders.

References

9

identification of deferred tax assets n accordance to the Australian Accounting Standards. As

described in the standards, the level to which tax assets deferred can be known is by ascertaining

the future probability of the company, and by so doing calculating the taxable future profits. Of

key importance therefore is to ensure that the company remains on a profitable trajectory so that

the benefits of the tax deferred can be seen. The purpose of deferred tax assets is to lessen the tax

liability by providing tax benefits on future income, since those tax liabilities can be deducted

from future profits.

The amount of money involved in the deferred tax assets is what makes this to be a key audit

matter. It will be up to the prudence of the auditor to ascertain whether the profits to be generated

will be sufficient enough in future in order to avail the tax benefit later. It was therefore noted

that the auditors of Altium had to carry out test in order to ascertain the profits of the company

on the years to come before making their recommendation.

The second matter was Carrying value of goodwill and other definite lived intangible assets

whereby it is necessary for the assets of the organization to be taken through an annual

impairment assessment as stipulated by the Australian Accounting Standards. This is inclusive of

intangible assets like goodwill. At the end of the financial year, these assets are checked for the

impairment. Certain financial models like estimation of cash flows and discount rates were put in

place by the management in order to perform the impairment test. This prompted the auditors to

view this as a substantial audit matter.

Conclusion

This report aims at establishing whether the organization and the contracted auditor played their

role in ensuring that the accounting standards set were adhered to. The report was also aimed at

establishing the role played by audit reporting in ensuring there is transparency and

accountability within the organization. Various key issues were noted from the annual and

auditor’s report. despite the unqualified opinion by the auditor, which is a positive for Altium

LTD, it s important for the organization to consider displaying their audit committee chatter or

the key details pertaining to that committee to further strengthen the notion of auditors

independence to the stakeholders.

References

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Altium Limited, 2017. Annual Report. Altium Limited.

Altium Limited, 2018. About Us. [Online] Available at: https://www.altium.com/ [Accessed 17

September 2018].

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

ASIC, 2018. Auditor independence and audit quality. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/auditor-

independence-and-audit-quality/ [Accessed 16 September 2018].

Basu, S.K., 2010. Fundamentals of Auditing. Pearson Education.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

Caanz , 2015. Auditing and Assurance Handbook 2015 New Zealand+auditing and Assurance

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

CCH Australia Limited, 2011. Australian Corporations & Securities Legislation 2011:

Corporations Act 2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and Risk. Routledge.

10

Altium Limited, 2018. About Us. [Online] Available at: https://www.altium.com/ [Accessed 17

September 2018].

Arens, A. et al., 2016. Auditing, Assurance Services and Ethics in Australia with ACL Access

Code Card. Pearson Education Australia.

ASIC, 2018. Auditor independence and audit quality. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/auditor-

independence-and-audit-quality/ [Accessed 16 September 2018].

Basu, S.K., 2010. Fundamentals of Auditing. Pearson Education.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

CAANZ (Chartered Accountants Australia & New Zealand), 2016. Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December 2015. John

Wiley & Sons.

Caanz , 2015. Auditing and Assurance Handbook 2015 New Zealand+auditing and Assurance

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

CCH Australia Limited, 2011. Australian Corporations & Securities Legislation 2011:

Corporations Act 2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Chartered Accountants (Australia-Newzealand), 2018. Perspective.

Frankel, R.M., 2018. The Relation Between Auditors' Fees for Non-Audit Services and Earnings

Quality (Classic Reprint). Fb&c Limited.

Gay, G.E. & Simnett, R., 2015. Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Knechel, W.R. & Salterio, S.E., 2016. Auditing: Assurance and Risk. Routledge.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Leung, P., 2009. Modern Auditing & Assurance Services. John Wiley & Sons Australia.

Media, B.L., 2015. CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K., 2018. Independence – Navigating the murky waters between Audit & Non-Audit

services. [Online] Available at: https://rochford-group.com/independence-navigating-murky-

waters-audit-non-audit-services/ [Accessed 11 September 2018].

Porter, B., Simon, J. & Hatherly, D., 2014. Principles of External Auditing. Wiley.

Wolters Kluwer, 2018. Corporations Act 2001, Section 307c Auditor’s Independence

Declaration. [Online] Available at:

https://iknow.cch.com.au/document/atagUio486340sl14508496/corporations-act-2001-section-

307c-auditor-s-independence-declaration [Accessed 9 September 2018].

11

Media, B.L., 2015. CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K., 2018. Independence – Navigating the murky waters between Audit & Non-Audit

services. [Online] Available at: https://rochford-group.com/independence-navigating-murky-

waters-audit-non-audit-services/ [Accessed 11 September 2018].

Porter, B., Simon, J. & Hatherly, D., 2014. Principles of External Auditing. Wiley.

Wolters Kluwer, 2018. Corporations Act 2001, Section 307c Auditor’s Independence

Declaration. [Online] Available at:

https://iknow.cch.com.au/document/atagUio486340sl14508496/corporations-act-2001-section-

307c-auditor-s-independence-declaration [Accessed 9 September 2018].

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.