HI6028 Taxation Assignment

VerifiedAdded on 2019/10/30

|14

|2884

|103

Homework Assignment

AI Summary

This document presents solved solutions for a HI6028 Taxation Theory, Practice & Law assignment. It addresses several tax-related scenarios, including capital gains tax calculations, fringe benefits tax on employee loans, tax implications of rental property co-ownership, tax avoidance schemes, and the tax treatment of timber disposal. Each question follows a structured approach: identifying the issue, outlining relevant regulations and legal provisions, applying these provisions to the specific case, and drawing a conclusion. The solutions cite relevant Australian tax legislation, rulings (like TR 93/32 and TR 95/6), and academic sources. The assignment demonstrates a comprehensive understanding of Australian taxation principles and their practical application in various situations.

HI6028 Taxation Theory, Practice &

Law

T2 2017 Individual Assignment

Law

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Application of legal provisions..............................................................................................4

Conclusion..............................................................................................................................5

References..............................................................................................................................5

Question 2..................................................................................................................................7

Issue........................................................................................................................................7

Regulations.............................................................................................................................7

Application of legal provisions..............................................................................................7

Conclusion..............................................................................................................................8

References..............................................................................................................................8

Question 3..................................................................................................................................9

Issue........................................................................................................................................9

Regulations.............................................................................................................................9

Application of legal provisions............................................................................................10

Conclusion............................................................................................................................10

References............................................................................................................................10

Question 4................................................................................................................................12

Description of issues............................................................................................................12

Legal provisions...................................................................................................................12

Application of described provisions.....................................................................................12

Conclusion............................................................................................................................12

References............................................................................................................................13

Question 1..................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Application of legal provisions..............................................................................................4

Conclusion..............................................................................................................................5

References..............................................................................................................................5

Question 2..................................................................................................................................7

Issue........................................................................................................................................7

Regulations.............................................................................................................................7

Application of legal provisions..............................................................................................7

Conclusion..............................................................................................................................8

References..............................................................................................................................8

Question 3..................................................................................................................................9

Issue........................................................................................................................................9

Regulations.............................................................................................................................9

Application of legal provisions............................................................................................10

Conclusion............................................................................................................................10

References............................................................................................................................10

Question 4................................................................................................................................12

Description of issues............................................................................................................12

Legal provisions...................................................................................................................12

Application of described provisions.....................................................................................12

Conclusion............................................................................................................................12

References............................................................................................................................13

Question 5................................................................................................................................14

Issue......................................................................................................................................14

Regulations...........................................................................................................................14

Application of legal provisions............................................................................................15

Conclusion............................................................................................................................15

Reference..............................................................................................................................15

Issue......................................................................................................................................14

Regulations...........................................................................................................................14

Application of legal provisions............................................................................................15

Conclusion............................................................................................................................15

Reference..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

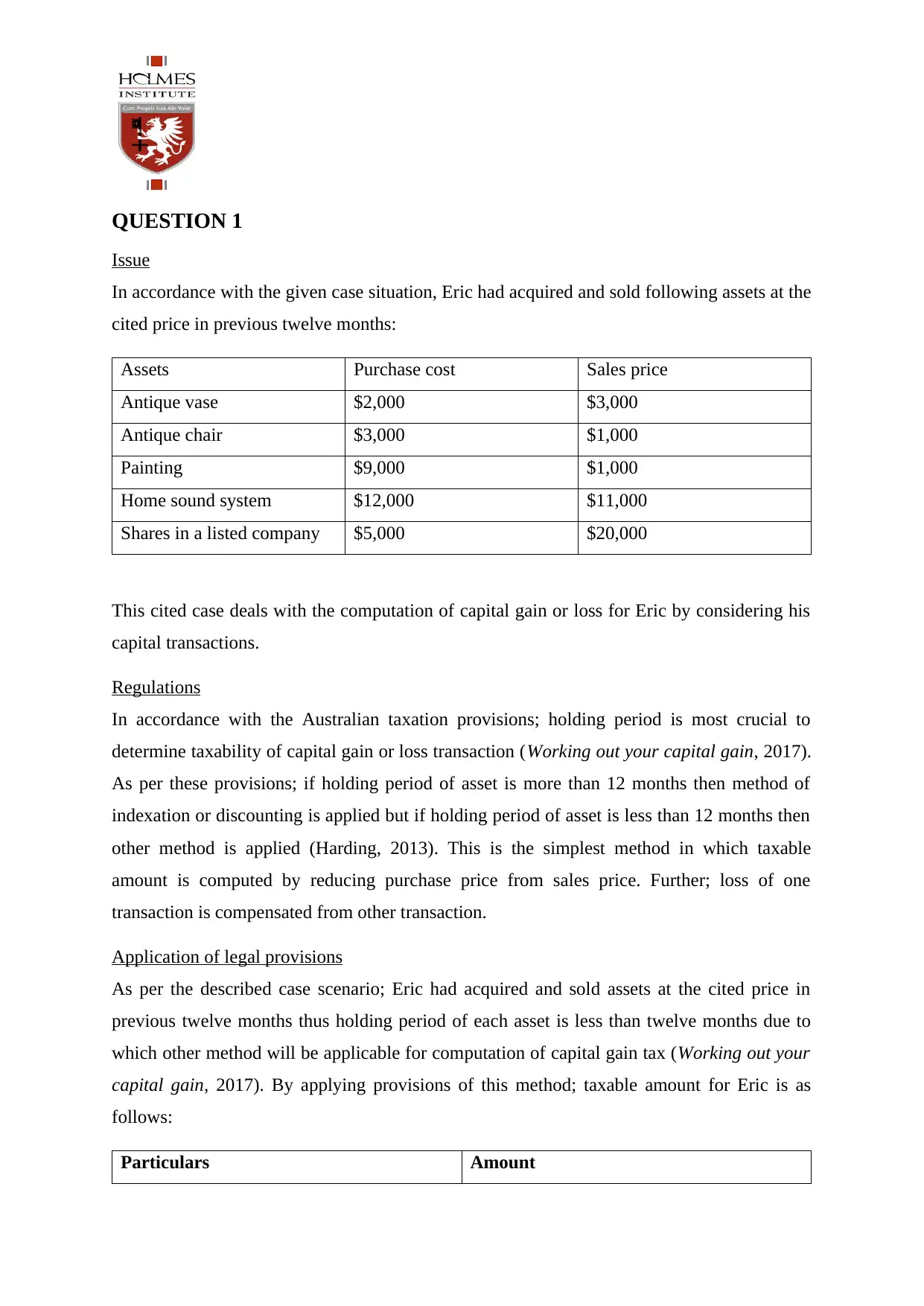

QUESTION 1

Issue

In accordance with the given case situation, Eric had acquired and sold following assets at the

cited price in previous twelve months:

Assets Purchase cost Sales price

Antique vase $2,000 $3,000

Antique chair $3,000 $1,000

Painting $9,000 $1,000

Home sound system $12,000 $11,000

Shares in a listed company $5,000 $20,000

This cited case deals with the computation of capital gain or loss for Eric by considering his

capital transactions.

Regulations

In accordance with the Australian taxation provisions; holding period is most crucial to

determine taxability of capital gain or loss transaction (Working out your capital gain, 2017).

As per these provisions; if holding period of asset is more than 12 months then method of

indexation or discounting is applied but if holding period of asset is less than 12 months then

other method is applied (Harding, 2013). This is the simplest method in which taxable

amount is computed by reducing purchase price from sales price. Further; loss of one

transaction is compensated from other transaction.

Application of legal provisions

As per the described case scenario; Eric had acquired and sold assets at the cited price in

previous twelve months thus holding period of each asset is less than twelve months due to

which other method will be applicable for computation of capital gain tax (Working out your

capital gain, 2017). By applying provisions of this method; taxable amount for Eric is as

follows:

Particulars Amount

Issue

In accordance with the given case situation, Eric had acquired and sold following assets at the

cited price in previous twelve months:

Assets Purchase cost Sales price

Antique vase $2,000 $3,000

Antique chair $3,000 $1,000

Painting $9,000 $1,000

Home sound system $12,000 $11,000

Shares in a listed company $5,000 $20,000

This cited case deals with the computation of capital gain or loss for Eric by considering his

capital transactions.

Regulations

In accordance with the Australian taxation provisions; holding period is most crucial to

determine taxability of capital gain or loss transaction (Working out your capital gain, 2017).

As per these provisions; if holding period of asset is more than 12 months then method of

indexation or discounting is applied but if holding period of asset is less than 12 months then

other method is applied (Harding, 2013). This is the simplest method in which taxable

amount is computed by reducing purchase price from sales price. Further; loss of one

transaction is compensated from other transaction.

Application of legal provisions

As per the described case scenario; Eric had acquired and sold assets at the cited price in

previous twelve months thus holding period of each asset is less than twelve months due to

which other method will be applicable for computation of capital gain tax (Working out your

capital gain, 2017). By applying provisions of this method; taxable amount for Eric is as

follows:

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital gain

Shares in a listed company $15000

Antique vase $1,000

Total capital gain $16,000

Capital loss

Antique chair $2,000

Painting $8,000

Home sound system $1,000

Total capital Loss $11,000

Net capital gain (Total capital gain- Total

capital loss)

$5,000

Working note

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Antique vase $2,000 $3,000 $1,000 (gain)

Antique chair $3,000 $1,000 $2,000 (loss)

Painting $9,000 $1,000 $8,000 (loss)

Home sound system $12,000 $11,000 $1,000 (loss)

Shares in a listed

company

$5,000 $20,000 $15,000 (gain)

Conclusion

In accordance with the above computation, taxable amount for capital gain for Eric is

$15,000 as amount of loss from capital transactions is compensated from the gain earned by

him.

References

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Shares in a listed company $15000

Antique vase $1,000

Total capital gain $16,000

Capital loss

Antique chair $2,000

Painting $8,000

Home sound system $1,000

Total capital Loss $11,000

Net capital gain (Total capital gain- Total

capital loss)

$5,000

Working note

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Antique vase $2,000 $3,000 $1,000 (gain)

Antique chair $3,000 $1,000 $2,000 (loss)

Painting $9,000 $1,000 $8,000 (loss)

Home sound system $12,000 $11,000 $1,000 (loss)

Shares in a listed

company

$5,000 $20,000 $15,000 (gain)

Conclusion

In accordance with the above computation, taxable amount for capital gain for Eric is

$15,000 as amount of loss from capital transactions is compensated from the gain earned by

him.

References

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Working out your capital gain. 2017. [Online]. Available through <

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 16th September 2017].

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 16th September 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

Issue

In accordance with the given case situation Brian is an executive in bank and as part of

remuneration package he gets a loan with tenure of three years of $1m at a special interest

rate of 1% pa and the same is payable in monthly instalments. 40% of the income is used by

him for purpose of producing income. By considering this transaction, this part deals with

taxation on benefit provided to Brian as per Australian taxation provisions of Fringe tax

benefits.

Regulations

The fringe benefit tax has determined several fringe benefits types and contains particular

rules of valuation for each and every type of benefit. In the event of loan, FB takes place

where there is less or no interest charged against loan (Woellner and et.al. 2016). Fringe

benefit taxable value is determined by the difference of interest rate with the statutory interest

rate (Reportable fringe benefits – facts for employees, 2016). For the fringe benefit tax, tax

rate for year ended are as follows:

Loan Fringe Benefits

Benchmark Interest Rates1

FBT Year Ended 31 March Rate %

2017 5.65

2016 5.65

Application of legal provisions

By applicability of cited provisions; taxable amount for Brian is as follows:

Step 1: The amount of interest payable by Brain

$1,000,000*1% = $10,000

1 These rates apply to loans other than pre-July 1986 fixed interest loans and pre-3 April 1986 variable interest

housing loans.

Issue

In accordance with the given case situation Brian is an executive in bank and as part of

remuneration package he gets a loan with tenure of three years of $1m at a special interest

rate of 1% pa and the same is payable in monthly instalments. 40% of the income is used by

him for purpose of producing income. By considering this transaction, this part deals with

taxation on benefit provided to Brian as per Australian taxation provisions of Fringe tax

benefits.

Regulations

The fringe benefit tax has determined several fringe benefits types and contains particular

rules of valuation for each and every type of benefit. In the event of loan, FB takes place

where there is less or no interest charged against loan (Woellner and et.al. 2016). Fringe

benefit taxable value is determined by the difference of interest rate with the statutory interest

rate (Reportable fringe benefits – facts for employees, 2016). For the fringe benefit tax, tax

rate for year ended are as follows:

Loan Fringe Benefits

Benchmark Interest Rates1

FBT Year Ended 31 March Rate %

2017 5.65

2016 5.65

Application of legal provisions

By applicability of cited provisions; taxable amount for Brian is as follows:

Step 1: The amount of interest payable by Brain

$1,000,000*1% = $10,000

1 These rates apply to loans other than pre-July 1986 fixed interest loans and pre-3 April 1986 variable interest

housing loans.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step 2: The amount of interest as per statutory interest rate

$1,000,000*5.65%= $56,500

Step 3: The taxable value of loan fringe benefit

=$56,500 -$10,000

=$46,500

Step 4: Taking proportion of loan used for purpose of producing income

=$46,500*40%

=$18,600

Conclusion

Taxable amount for fringe benefit will be $18,600 irrespective of fact that interest is paid

monthly or yearly basis. Further, if Brian is released from the obligation of payment of

interest then entire value of interest i.e. $56,500 will be taxable.

References

Reportable fringe benefits – facts for employees, 2016. [Online]. Available through <

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/In-detail/Employees/Reportable-

fringe-benefits---facts-for-employees/>. [Accessed on 16th September 2017].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

$1,000,000*5.65%= $56,500

Step 3: The taxable value of loan fringe benefit

=$56,500 -$10,000

=$46,500

Step 4: Taking proportion of loan used for purpose of producing income

=$46,500*40%

=$18,600

Conclusion

Taxable amount for fringe benefit will be $18,600 irrespective of fact that interest is paid

monthly or yearly basis. Further, if Brian is released from the obligation of payment of

interest then entire value of interest i.e. $56,500 will be taxable.

References

Reportable fringe benefits – facts for employees, 2016. [Online]. Available through <

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/In-detail/Employees/Reportable-

fringe-benefits---facts-for-employees/>. [Accessed on 16th September 2017].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

QUESTION 3

Issue

According to given case scenario; Jack and his wife Jill purchased rental property by making

use of borrowed money in form joint tenants. For this aspect; they had formed written

agreement that they will share profit in 10:90 for Jack and Jill respectively but entire 100%

loss will be allocate to Jack. In last year loss of $10000 has been occurred so this case deals

with tax treatment of loss by considering provisions cited under TR 93/32 “Income Tax:

rental property – division of net income or loss between co-owners”. This part will also

include description of tax implication of capital gain or loss if property is sold by joint

tenants.

Regulations

Rule

According to the provisions listed in TR 93/32 “Income Tax: rental property – division of net

loss or income between partner” the grounds on which net loss or income from rental

property is divided between owners is acceptable for the purpose of income tax.

Ruling

- Joint ownership of a rental place can be considered as partnership for the purpose of

income tax, however, it cannot be considered as a partnership under general law

unless it is to carry on a business.

- If joint ownership is just for the purpose of income tax i.e. the loss or income accruing

from rental place is obtained from jointly owned place and not from apportionment of

partnership loss or profit (Tax Ruling TR 93/32, 2017).

- Moreover, joint owners of the rental place are not considered as partners in general,

hence an oral or written agreement does not have any impact on sharing of loss or

income pertaining to property.

The relationship among these co-owners is considered to be co-ownership, and if they

consent to partnership as per subsection 6(1), this would be regarded as irrelevant, because

their unreal partnership will undertake such implications that they need to address one

Issue

According to given case scenario; Jack and his wife Jill purchased rental property by making

use of borrowed money in form joint tenants. For this aspect; they had formed written

agreement that they will share profit in 10:90 for Jack and Jill respectively but entire 100%

loss will be allocate to Jack. In last year loss of $10000 has been occurred so this case deals

with tax treatment of loss by considering provisions cited under TR 93/32 “Income Tax:

rental property – division of net income or loss between co-owners”. This part will also

include description of tax implication of capital gain or loss if property is sold by joint

tenants.

Regulations

Rule

According to the provisions listed in TR 93/32 “Income Tax: rental property – division of net

loss or income between partner” the grounds on which net loss or income from rental

property is divided between owners is acceptable for the purpose of income tax.

Ruling

- Joint ownership of a rental place can be considered as partnership for the purpose of

income tax, however, it cannot be considered as a partnership under general law

unless it is to carry on a business.

- If joint ownership is just for the purpose of income tax i.e. the loss or income accruing

from rental place is obtained from jointly owned place and not from apportionment of

partnership loss or profit (Tax Ruling TR 93/32, 2017).

- Moreover, joint owners of the rental place are not considered as partners in general,

hence an oral or written agreement does not have any impact on sharing of loss or

income pertaining to property.

The relationship among these co-owners is considered to be co-ownership, and if they

consent to partnership as per subsection 6(1), this would be regarded as irrelevant, because

their unreal partnership will undertake such implications that they need to address one

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

another as a real partner for certain specific purpose. The partners can just deduct the interest

of the partner in event of loss of partnership. Individual interest is such interest that is

completely allowed to the partner, be compared with their mutual interest in the rental place

as a whole (Kirchler, Niemirowski and Wearing, 2006).

Application of legal provisions

Jack and Jill bought the rental place as co-tenants. Both of them consented to bear loss

and share income from the property as follows:

Jack Jill

Ratio for distribution of profit 10% 90%

Ratio for distribution of loss 100% nil

Renting or having a single premise is not regarded as conducting a business. Both

Jack and Jill are hence not co-partners under the general law, nonetheless, their association

would be seen as partnership for income tax purposes. Income and loss accrued from the

property should be distributed in equal ratio because they have 50:50 in the business. Their

agreement to share profit and loss in different ratios is their agreement which has no impact

for the intention of income tax.

Conclusion

By taking into account the above-mentioned provisions, it could be cited that 50% of

loss will be assigned to Mr. Jack for income tax purposes. Moreover, if in times ahead they

choose to sell their property then also aforementioned provisions would be applicable as per

which Jack could claim 50% of capital loss or gain.

References

Tax Ruling TR 93/32. Income tax: rental property – division of net income or loss between

co-owners. 2017. [Online]. Available through <http://law.ato.gov.au/atolaw/view.htm?

docid=TXR/TR9332/NAT/ATO/00001#P24>. [Accessed on 16th September 2017].

Kirchler, E., Niemirowski, A. and Wearing, A., 2006. Shared subjective views, intent to

cooperate and tax compliance: Similarities between Australian taxpayers and tax officers.

Journal of economic psychology, 27(4), pp.502-517.

of the partner in event of loss of partnership. Individual interest is such interest that is

completely allowed to the partner, be compared with their mutual interest in the rental place

as a whole (Kirchler, Niemirowski and Wearing, 2006).

Application of legal provisions

Jack and Jill bought the rental place as co-tenants. Both of them consented to bear loss

and share income from the property as follows:

Jack Jill

Ratio for distribution of profit 10% 90%

Ratio for distribution of loss 100% nil

Renting or having a single premise is not regarded as conducting a business. Both

Jack and Jill are hence not co-partners under the general law, nonetheless, their association

would be seen as partnership for income tax purposes. Income and loss accrued from the

property should be distributed in equal ratio because they have 50:50 in the business. Their

agreement to share profit and loss in different ratios is their agreement which has no impact

for the intention of income tax.

Conclusion

By taking into account the above-mentioned provisions, it could be cited that 50% of

loss will be assigned to Mr. Jack for income tax purposes. Moreover, if in times ahead they

choose to sell their property then also aforementioned provisions would be applicable as per

which Jack could claim 50% of capital loss or gain.

References

Tax Ruling TR 93/32. Income tax: rental property – division of net income or loss between

co-owners. 2017. [Online]. Available through <http://law.ato.gov.au/atolaw/view.htm?

docid=TXR/TR9332/NAT/ATO/00001#P24>. [Accessed on 16th September 2017].

Kirchler, E., Niemirowski, A. and Wearing, A., 2006. Shared subjective views, intent to

cooperate and tax compliance: Similarities between Australian taxpayers and tax officers.

Journal of economic psychology, 27(4), pp.502-517.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4

Description of issues

As per the facts cited in the case of Duke of Westminster v CIR 19 TC 490, Duke had assured

to pay the additional sum to gardener if they give extra services. The deed had taken place in

written format. Nonetheless, this deed for created with the sole objective to receive a

deduction for the purpose of tax evasion.

Legal provisions

Principle

In the concerned situation of Duke of Westminster v CIR 19 TC 490, the ruling was that

every individual is permissible to manage their affairs, because the tax chargeable according

to the suitable action would be minimum. This ruling is preferred by many people, and they

would prefer seeing the execution of this judgment on a continuous basis, subsequent to the

introduction of any normal anti-avoidance law in Australia (Pinto, 2012).

Application of described provisions

Relevance in present scenario

In the last year, the constitution has established some provisions that requires advisors to

intimate the HMRC about any scheme which can result in tax evasion. Nonetheless, this

would not be viewed all over the board, and it remains to be observed regarding what type of

actions would be taken when getting such notifications. It may be seen in the settlement when

such rulings will serve as an originator to the setting of new provisions instead of more

extensive current rulings (Mete, Dick and Moerman, 2010).

Conclusion

Lord Wilberforce identified that although the ruling of Duke of Westminster prevented the

court from noticing the actual transaction to some alleged basic substance, it would not

“please the court to see the document in blinkers, not accessible from all contexts to which it

really belongs’.

The court should identify the legal nature of the transaction through which it needs to make

attachment of a tax or a tax outcome and in case it results as a mixture or series of

Description of issues

As per the facts cited in the case of Duke of Westminster v CIR 19 TC 490, Duke had assured

to pay the additional sum to gardener if they give extra services. The deed had taken place in

written format. Nonetheless, this deed for created with the sole objective to receive a

deduction for the purpose of tax evasion.

Legal provisions

Principle

In the concerned situation of Duke of Westminster v CIR 19 TC 490, the ruling was that

every individual is permissible to manage their affairs, because the tax chargeable according

to the suitable action would be minimum. This ruling is preferred by many people, and they

would prefer seeing the execution of this judgment on a continuous basis, subsequent to the

introduction of any normal anti-avoidance law in Australia (Pinto, 2012).

Application of described provisions

Relevance in present scenario

In the last year, the constitution has established some provisions that requires advisors to

intimate the HMRC about any scheme which can result in tax evasion. Nonetheless, this

would not be viewed all over the board, and it remains to be observed regarding what type of

actions would be taken when getting such notifications. It may be seen in the settlement when

such rulings will serve as an originator to the setting of new provisions instead of more

extensive current rulings (Mete, Dick and Moerman, 2010).

Conclusion

Lord Wilberforce identified that although the ruling of Duke of Westminster prevented the

court from noticing the actual transaction to some alleged basic substance, it would not

“please the court to see the document in blinkers, not accessible from all contexts to which it

really belongs’.

The court should identify the legal nature of the transaction through which it needs to make

attachment of a tax or a tax outcome and in case it results as a mixture or series of

transactions, intended to work as such, it is that series or combination that is needed to be

regarded by legal authorities in case evaluation.

In these type of situations, the representatives should find facts and make a further decision

by taking into account the matter of law to categories whether the matter is included in the

composite transaction and is advocated by the autonomous transaction.

By taking into account this fact, it is clear that the scheme was just for the purpose of tax

avoidance in absence of any commercial justification, the intention was to follow all its

phases till the end. It will hence be impertinent to evaluate only one phase in the isolation

process.

References

Pinto, D., 2012. Special Tax Payers and Incentive Schemes. In Australian Taxation Law (pp.

1160-1277). CCH Australia Limited.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 21(7),

pp.619-630.

regarded by legal authorities in case evaluation.

In these type of situations, the representatives should find facts and make a further decision

by taking into account the matter of law to categories whether the matter is included in the

composite transaction and is advocated by the autonomous transaction.

By taking into account this fact, it is clear that the scheme was just for the purpose of tax

avoidance in absence of any commercial justification, the intention was to follow all its

phases till the end. It will hence be impertinent to evaluate only one phase in the isolation

process.

References

Pinto, D., 2012. Special Tax Payers and Incentive Schemes. In Australian Taxation Law (pp.

1160-1277). CCH Australia Limited.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 21(7),

pp.619-630.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.