HI6028 Taxation Law T2 2018: Analysis of Capital Gains and FBT

VerifiedAdded on 2023/06/08

|13

|3637

|210

Report

AI Summary

This assignment provides a detailed analysis of Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT) implications under Australian Taxation Law, referencing key legislation such as ITAA 1997 and FBTAA 1986. It examines scenarios involving the sale of vacant land, stolen antique bed, painting, shares, and a violin to determine CGT liabilities. The report also addresses FBT repercussions related to car benefits and parking expenses, applying relevant sections of FBTAA 1986 and case law to evaluate taxable fringe benefits. This document is available on Desklib, a platform offering various study tools and solved assignments for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer to question 1:

The rulings under the “section 102-20 of the ITAA 1997” has defined that taxpayer is

liable to account only for those changes which are a result of CT event. It needs to be also

taken into consideration the ruling under “section 104-10 (1) of the ITAA 1997”. This

directly related to any event of CGT for which the A1 will be held for disposal of the asset.

The rulings as per the “Sara Lee Household v FC of T (2000)” needs to be understood with

the facts which are crucial for the validity of the contract. Moreover, the CGT should not be

considered as separate entity an income which is to be charged as per a taxpayer entering into

contract (Law.ato.gov.au 2018).

The rulings under “section 102-5, ITAA 1997” has further shown that the various

types of the consideration taken up by the taxpayer needs to be defined as per the accounting

of the net capital gains as per the earnings which are chargeable. The taxpayers will be

further able to provide the various types of the provisions for the quarantined items associated

to the capital loss set off as per the capital gains. In addition to this, the CG will be also

applicable for the assets pertaining to activities more than or less than the date of 20th

September 1985. The event of CGT as per C1 has taken place at the time when there is any

loss or destruction of CGT asset (Woellner et al. 2016).

Activity associated to selling a portion of vacant land:

It needs to be understood that an individual responsible for acquiring of the vacant

land for private purpose or investment is subjected to the CGT at the time of selling the land

by the taxpayer. In such a situation the taxpayer in the present situation is seen to be

responsible for moving forward with the contract of sale of vacant block of land. As per the

given extract of towards information the property was acquired in the bidding price $ 100000

Answer to question 1:

The rulings under the “section 102-20 of the ITAA 1997” has defined that taxpayer is

liable to account only for those changes which are a result of CT event. It needs to be also

taken into consideration the ruling under “section 104-10 (1) of the ITAA 1997”. This

directly related to any event of CGT for which the A1 will be held for disposal of the asset.

The rulings as per the “Sara Lee Household v FC of T (2000)” needs to be understood with

the facts which are crucial for the validity of the contract. Moreover, the CGT should not be

considered as separate entity an income which is to be charged as per a taxpayer entering into

contract (Law.ato.gov.au 2018).

The rulings under “section 102-5, ITAA 1997” has further shown that the various

types of the consideration taken up by the taxpayer needs to be defined as per the accounting

of the net capital gains as per the earnings which are chargeable. The taxpayers will be

further able to provide the various types of the provisions for the quarantined items associated

to the capital loss set off as per the capital gains. In addition to this, the CG will be also

applicable for the assets pertaining to activities more than or less than the date of 20th

September 1985. The event of CGT as per C1 has taken place at the time when there is any

loss or destruction of CGT asset (Woellner et al. 2016).

Activity associated to selling a portion of vacant land:

It needs to be understood that an individual responsible for acquiring of the vacant

land for private purpose or investment is subjected to the CGT at the time of selling the land

by the taxpayer. In such a situation the taxpayer in the present situation is seen to be

responsible for moving forward with the contract of sale of vacant block of land. As per the

given extract of towards information the property was acquired in the bidding price $ 100000

2TAXATION LAW

with an $ 20,000 pertaining to local council for the land tax and water during the period of

ownership (Braithwaite 2017).

As per the explanation of the ATO, the unoccupied property in possession of the tax

payer needs to subjected for the CGT similar to other properties. In addition to this, the ATO

will also require to record the cost and date of the acquisition land. This depicted to be

inclusive of the interest on loan and council rates (Tan, Braithwaite and Reinhart 2016).

In the present aspect the taxpayer’s expenses are seen with the expenses pertaining to

the local council along with tax on land and water. The taxpayers need to be also cautious

during the claiming of the deductions pertaining to the IT purpose as the there was no

instance of revenue generated from the land. Instead of this, the taxpayer will be able to

consider the local expenses for water and sewage in the cost base of property as this will help

in the computation of the net CGT at the time land was sold (Middleton 2015).

Antique Bed:

The definition of as per the “section 108-10(2) of the ITAA 1997”. “Section 108-

10(1), ITAA 1997” have detailed about quarantining about the items which apples to the

items under CL. As stated in the “section 108-10(2), ITAA 1997” the collectibles refer to

postage stamp, rarer portfolios and manuscript. There are also few items which are needed to

be included for the personal usage of the taxpayers. There are also certain rules which are

applicable for the collectables (Ali et al. 2017).

Moreover, as collectibles are worth less than $ 500, the CL and CG are taken into

account with the cost and time consideration. This amendment suggests that the taxpayer’s

antique bed was stolen from his place of abode. Despite of this, insurance companies have

stated that the antique bed was not any specific item but the insurance policy itself. This

with an $ 20,000 pertaining to local council for the land tax and water during the period of

ownership (Braithwaite 2017).

As per the explanation of the ATO, the unoccupied property in possession of the tax

payer needs to subjected for the CGT similar to other properties. In addition to this, the ATO

will also require to record the cost and date of the acquisition land. This depicted to be

inclusive of the interest on loan and council rates (Tan, Braithwaite and Reinhart 2016).

In the present aspect the taxpayer’s expenses are seen with the expenses pertaining to

the local council along with tax on land and water. The taxpayers need to be also cautious

during the claiming of the deductions pertaining to the IT purpose as the there was no

instance of revenue generated from the land. Instead of this, the taxpayer will be able to

consider the local expenses for water and sewage in the cost base of property as this will help

in the computation of the net CGT at the time land was sold (Middleton 2015).

Antique Bed:

The definition of as per the “section 108-10(2) of the ITAA 1997”. “Section 108-

10(1), ITAA 1997” have detailed about quarantining about the items which apples to the

items under CL. As stated in the “section 108-10(2), ITAA 1997” the collectibles refer to

postage stamp, rarer portfolios and manuscript. There are also few items which are needed to

be included for the personal usage of the taxpayers. There are also certain rules which are

applicable for the collectables (Ali et al. 2017).

Moreover, as collectibles are worth less than $ 500, the CL and CG are taken into

account with the cost and time consideration. This amendment suggests that the taxpayer’s

antique bed was stolen from his place of abode. Despite of this, insurance companies have

stated that the antique bed was not any specific item but the insurance policy itself. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

accentuates the insurance paid by the taxpayer as per the contents of the household policy

with a payment of $ 11,000 (Middleton 2015).

The legal aspects under “section 104-20(1), ITAA 1997”, have shown that CGT event

as per C1 which is considered in case asset is destroyed. In this time period in case of any

event which is linked with CGT, the compensation is received with the losses as per the

determination of the CG or CL. The antique bed was also seen to be stolen. In addition to

this, there had been no specification of the insurance policy and confirmation of the

compensation which is raised to the CGT event C1 as per the asset lost from the taxpayer

(Richardson 2016).

Painting:

The definition as per the asset to be used for the personal use has shown various

rulings from the “section 108-20(2), ITAA 1997”. “Section 108-20(1)” has particularized on

the issues disregarded by the taxpayer on any event of capital loss which was made from the

asset pertaining to personal use. As stated under “section 108-20(2), ITAA 1997”, the assets

for the personal use needs to be considered for the collected amount which is to be kept as per

the private use of taxpayer or the enjoyments pertaining to land or building. The rulings of

“section 118-10(3), ITAA 1997” have also defined about the capital gains which needs to be

made for the personal use of the assets and regarded for the cast based lower than $ 10,000.

The decision of acquirement of painting needs to be done with an amount of $ 2000 on 2nd

May 1985. The taxpayers are needed to neglect gains of capital as per the selling of the

painting as this needs to be considered under the relevant applications (Cao et al. 2015).

Shares:

ATO have suggested that the shares considered by the company are considered with

the CGT similar to the other assets. The CGT is depicted to be appropriate for the investors

accentuates the insurance paid by the taxpayer as per the contents of the household policy

with a payment of $ 11,000 (Middleton 2015).

The legal aspects under “section 104-20(1), ITAA 1997”, have shown that CGT event

as per C1 which is considered in case asset is destroyed. In this time period in case of any

event which is linked with CGT, the compensation is received with the losses as per the

determination of the CG or CL. The antique bed was also seen to be stolen. In addition to

this, there had been no specification of the insurance policy and confirmation of the

compensation which is raised to the CGT event C1 as per the asset lost from the taxpayer

(Richardson 2016).

Painting:

The definition as per the asset to be used for the personal use has shown various

rulings from the “section 108-20(2), ITAA 1997”. “Section 108-20(1)” has particularized on

the issues disregarded by the taxpayer on any event of capital loss which was made from the

asset pertaining to personal use. As stated under “section 108-20(2), ITAA 1997”, the assets

for the personal use needs to be considered for the collected amount which is to be kept as per

the private use of taxpayer or the enjoyments pertaining to land or building. The rulings of

“section 118-10(3), ITAA 1997” have also defined about the capital gains which needs to be

made for the personal use of the assets and regarded for the cast based lower than $ 10,000.

The decision of acquirement of painting needs to be done with an amount of $ 2000 on 2nd

May 1985. The taxpayers are needed to neglect gains of capital as per the selling of the

painting as this needs to be considered under the relevant applications (Cao et al. 2015).

Shares:

ATO have suggested that the shares considered by the company are considered with

the CGT similar to the other assets. The CGT is depicted to be appropriate for the investors

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

who are making capital gains as per the shares during the occurrence of the CGT event. The

profits obtained by the taxpayers are seen with the selling of the shares which are needed to

be treated as an ordinary income. The similar treatment for the CG are seen to be reported as

per the share disposition pertaining to the Common Ltd, PHB Ltd. Despite of this, the losses

needs to be considered with the claiming of the capital loss offset as per the capital gains

which are considered from the selling of the shares (Saad 2014).

Violin:

The statement as per the “Subdivision 108-C” has suggested about the assets which

are to be used for the personal use. The treatment of the personal use of assets are generally

seen in terms of the household items such as boats, furniture and electrical goods. It is further

explained in “Section 108-20(2), ITAA 1997” that the options and rights to obtain the assets

for the taxpayers are seen for their personal enjoyment. The rulings as per “Section 118-

10(3)” has stated that the capital gains are not inclusive of the assets which are priced less

than $ 10,000 (Davison, Monotti and Wiseman 2015).

The evidence associated to the same can be seen with the information related to the

purchasing of the violin worth $ 5,500 and selling it in $ 12,000. In general, the violin needed

to kept for the personal use of the taxpayer. The cost basis of the assets needs to be also

considered with the assets less than $ 10,000. Henceforth, “section 118-10 (3), ITAA 1997”

has suggested about the capital gains which are to be disregarded (Cao et al. 2015).

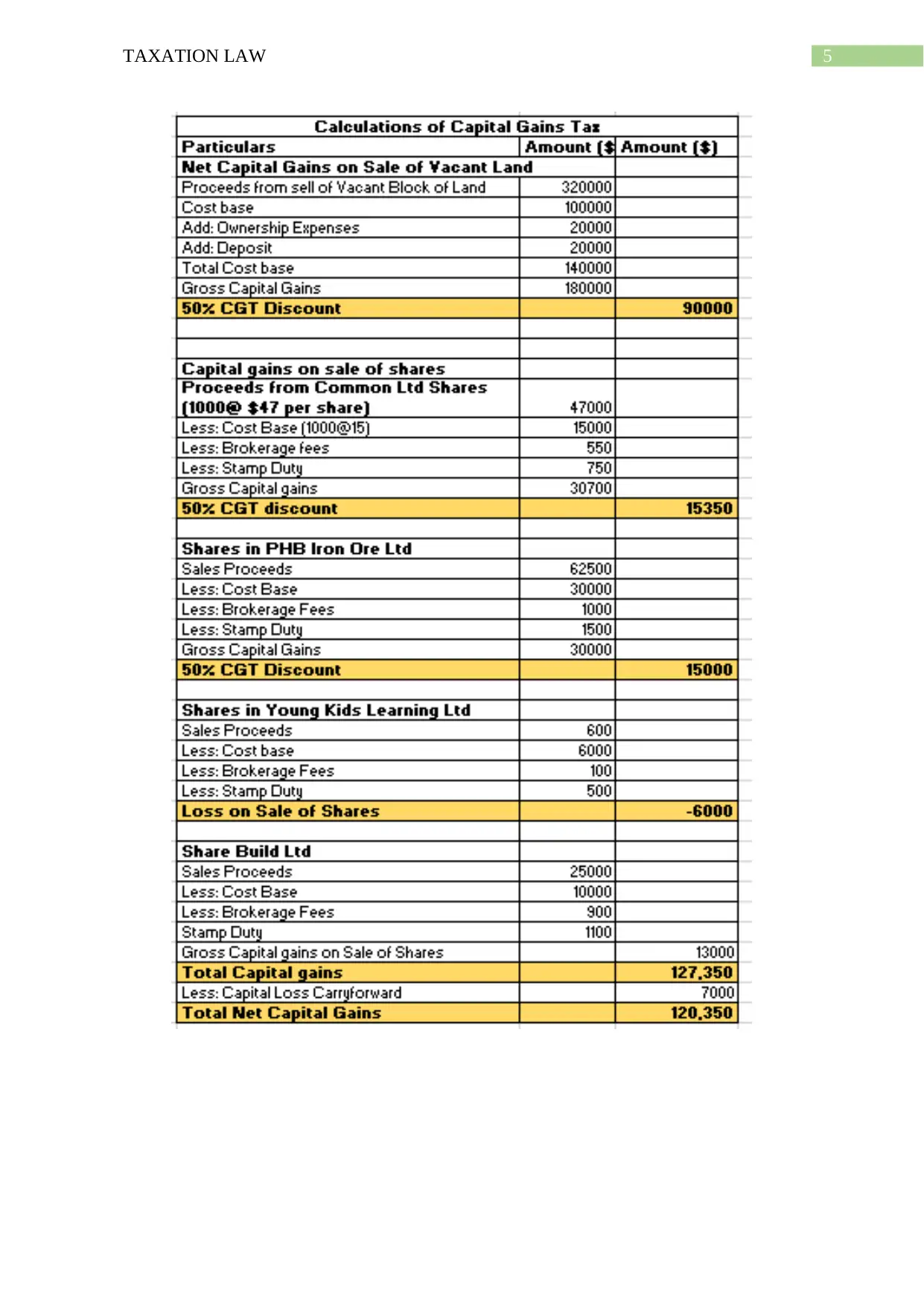

The total amount of the capital gains is shown as follows:

who are making capital gains as per the shares during the occurrence of the CGT event. The

profits obtained by the taxpayers are seen with the selling of the shares which are needed to

be treated as an ordinary income. The similar treatment for the CG are seen to be reported as

per the share disposition pertaining to the Common Ltd, PHB Ltd. Despite of this, the losses

needs to be considered with the claiming of the capital loss offset as per the capital gains

which are considered from the selling of the shares (Saad 2014).

Violin:

The statement as per the “Subdivision 108-C” has suggested about the assets which

are to be used for the personal use. The treatment of the personal use of assets are generally

seen in terms of the household items such as boats, furniture and electrical goods. It is further

explained in “Section 108-20(2), ITAA 1997” that the options and rights to obtain the assets

for the taxpayers are seen for their personal enjoyment. The rulings as per “Section 118-

10(3)” has stated that the capital gains are not inclusive of the assets which are priced less

than $ 10,000 (Davison, Monotti and Wiseman 2015).

The evidence associated to the same can be seen with the information related to the

purchasing of the violin worth $ 5,500 and selling it in $ 12,000. In general, the violin needed

to kept for the personal use of the taxpayer. The cost basis of the assets needs to be also

considered with the assets less than $ 10,000. Henceforth, “section 118-10 (3), ITAA 1997”

has suggested about the capital gains which are to be disregarded (Cao et al. 2015).

The total amount of the capital gains is shown as follows:

5TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Answer to A:

Issues:

The present problems for the evaluation of the FBT repercussions should be

considered as per the rulings stated with “FBTAA 1986”. The problems with determination is

depicted as per the private reason constituting of the fringe benefit as per the “section 7,

FBTAA 1986”. The “section 39 A, FBTAA 1986” is applicable for the taxpayers who can be

held liable for the different types of the expenses pertaining to car parking. The issue needs to

be discussed by considering the fringe benefit as per “subdivision A of FBTAA, 1986”.

Rule:

The rulings as per the fringe benefit is seen where a payment associated to the

employee will form a part of the wages and salary. The legislation as per the fringe benefit

tax comprises of the benefits which is provided to the employees as per the employment. This

is implied as per the benefit which is given to an individual employee.

The law as per “section 7, FBTAA 1986” states that the fringe benefit during the day

is considered as per the employment of the employee. The benefit of the fringe benefit is

mainly constituted of the perks as per the employment of the employees. In the given case car

is regarded as the main form of the fringe benefit which is facilitated by the employer to the

employee. The advantages related to the car fringe benefits needs to be also regarded with the

availability of the fringe benefits which are in relation to the benefits to their employment

(Burton and Karlinsky 2016).

The “sub-section 136 (1), FBTAA 1986” shows that the car held by the employee are

die to the fact of employment therefore usage of the car will be held as per FBT. The usage of

the vehicle by the employee is not to be seen with the direction of gaining assessable income

Answer to question 2:

Answer to A:

Issues:

The present problems for the evaluation of the FBT repercussions should be

considered as per the rulings stated with “FBTAA 1986”. The problems with determination is

depicted as per the private reason constituting of the fringe benefit as per the “section 7,

FBTAA 1986”. The “section 39 A, FBTAA 1986” is applicable for the taxpayers who can be

held liable for the different types of the expenses pertaining to car parking. The issue needs to

be discussed by considering the fringe benefit as per “subdivision A of FBTAA, 1986”.

Rule:

The rulings as per the fringe benefit is seen where a payment associated to the

employee will form a part of the wages and salary. The legislation as per the fringe benefit

tax comprises of the benefits which is provided to the employees as per the employment. This

is implied as per the benefit which is given to an individual employee.

The law as per “section 7, FBTAA 1986” states that the fringe benefit during the day

is considered as per the employment of the employee. The benefit of the fringe benefit is

mainly constituted of the perks as per the employment of the employees. In the given case car

is regarded as the main form of the fringe benefit which is facilitated by the employer to the

employee. The advantages related to the car fringe benefits needs to be also regarded with the

availability of the fringe benefits which are in relation to the benefits to their employment

(Burton and Karlinsky 2016).

The “sub-section 136 (1), FBTAA 1986” shows that the car held by the employee are

die to the fact of employment therefore usage of the car will be held as per FBT. The usage of

the vehicle by the employee is not to be seen with the direction of gaining assessable income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

which will be considered as private. Furthermore, the commissioner of the tax as per the

“Federal Commissioner of Taxation v Lunney (1958)” demonstrates that the position of the

tax payer is confirmed with the place of travel of the employee to the place of business. This

is to be treated as private in nature (Braithwaite, Reinhart and Job 2018).

The “Subdivision B 22A of the FBTAA 1986” is also seen to be related to the various

categories of the expenses as per the FBT. The expense pertaining to the fringe benefit needs

to be taken into account with the reimbursing at the movement of occurrence. The general

rule of thumb for including the expenses is depicted with the subsequent reimbursing of the

expenses for the employees as per the origination of the fringe benefits. The taxable value of

the fringe benefit expense is to be duly reimbursed to the employees (Daniel, Keen, Świstak

and Thuronyi, 2016).

As stated in the “Sub-Division B 39C of the FBTAA 1986” elucidates taxable charge

of the car parking fringe benefits. The fringe benefits pertaining to the car parking needs to be

considered as per the FBT year in connection with the commercial parking stations. These are

considered to be located in 1 km radius and those held for charging lower fees. The benefits

considered with the car parking are enumerated as follows:

a. Parking is made in the employer’s premise

b. Parking is made within a radius of 1 km

c. Parking facility availed more than four hours in a certain day

d. The car is facilitated to the employer as per the employment duration

e. The car is used by the employee for travelling across workplace and place of adobe for at

least once in a day.

which will be considered as private. Furthermore, the commissioner of the tax as per the

“Federal Commissioner of Taxation v Lunney (1958)” demonstrates that the position of the

tax payer is confirmed with the place of travel of the employee to the place of business. This

is to be treated as private in nature (Braithwaite, Reinhart and Job 2018).

The “Subdivision B 22A of the FBTAA 1986” is also seen to be related to the various

categories of the expenses as per the FBT. The expense pertaining to the fringe benefit needs

to be taken into account with the reimbursing at the movement of occurrence. The general

rule of thumb for including the expenses is depicted with the subsequent reimbursing of the

expenses for the employees as per the origination of the fringe benefits. The taxable value of

the fringe benefit expense is to be duly reimbursed to the employees (Daniel, Keen, Świstak

and Thuronyi, 2016).

As stated in the “Sub-Division B 39C of the FBTAA 1986” elucidates taxable charge

of the car parking fringe benefits. The fringe benefits pertaining to the car parking needs to be

considered as per the FBT year in connection with the commercial parking stations. These are

considered to be located in 1 km radius and those held for charging lower fees. The benefits

considered with the car parking are enumerated as follows:

a. Parking is made in the employer’s premise

b. Parking is made within a radius of 1 km

c. Parking facility availed more than four hours in a certain day

d. The car is facilitated to the employer as per the employment duration

e. The car is used by the employee for travelling across workplace and place of adobe for at

least once in a day.

8TAXATION LAW

As per the statement of “Division 4 of the FBTAA 1986”, the FB in relation to the

debt is made to the employee when the employer agrees with such a debt instrument. The

main purpose of such an act needs to be considered as per the “subsection 136 (1), FBTAA

1986”. This is further seen under the obligation of paying or repaying of the sum to any other

individual. The FB loan is also encompassed when the charges of the lower amount of

interest is included during a particular FBT year. The lesser is the interest rate, the lesser will

be the statutory interest rate (Sawyer 2016).

Application:

It is noted that Jasmine is employed with Rapid Heat Pty Ltd. (RHP) At the course of

his employment, Jasmine was given vehicle access as she considered lot of travelling for the

purpose of employment. Jasmine was also seen to use the car not only for work but also

private related use. Mentioning to the “sub-section 136 (1), FBTAA 1986” it can be seen that

the FB associated to the car was provided under the employment agreement. The excerpt

taken from “FC of T v Lunney (1958)”, shows that the vehicle usage by Jasmine was beyond

the purpose of work and hence should be seen with the benefit as per “FBTAA, 1986”

(Frecknall-Hughes and Kirchler 2015).

At the later stage Jasmine incurred a cost of $ 550 related to the minor repairs. These

expenses were although allied to the reimbursement of the expenses by RHP Ltd to Jasmine.

The compensation for the car maintenance job further constituted of the payment pertaining

to the FB as per “subdivision B 22A of the FBTAA 1986”. The expenses reimbursed to

Jasmine is seen as per the acknowledgement of the receipt (Picard et al. 2016).

In the final section it needs to be noted that Jasmine parked the car at the property of

commercial airport. She did not use it for a total of ten days as the car was parked. Moreover,

she did not use the car. In this case, there cannot be scope for car parking fringe benefit

As per the statement of “Division 4 of the FBTAA 1986”, the FB in relation to the

debt is made to the employee when the employer agrees with such a debt instrument. The

main purpose of such an act needs to be considered as per the “subsection 136 (1), FBTAA

1986”. This is further seen under the obligation of paying or repaying of the sum to any other

individual. The FB loan is also encompassed when the charges of the lower amount of

interest is included during a particular FBT year. The lesser is the interest rate, the lesser will

be the statutory interest rate (Sawyer 2016).

Application:

It is noted that Jasmine is employed with Rapid Heat Pty Ltd. (RHP) At the course of

his employment, Jasmine was given vehicle access as she considered lot of travelling for the

purpose of employment. Jasmine was also seen to use the car not only for work but also

private related use. Mentioning to the “sub-section 136 (1), FBTAA 1986” it can be seen that

the FB associated to the car was provided under the employment agreement. The excerpt

taken from “FC of T v Lunney (1958)”, shows that the vehicle usage by Jasmine was beyond

the purpose of work and hence should be seen with the benefit as per “FBTAA, 1986”

(Frecknall-Hughes and Kirchler 2015).

At the later stage Jasmine incurred a cost of $ 550 related to the minor repairs. These

expenses were although allied to the reimbursement of the expenses by RHP Ltd to Jasmine.

The compensation for the car maintenance job further constituted of the payment pertaining

to the FB as per “subdivision B 22A of the FBTAA 1986”. The expenses reimbursed to

Jasmine is seen as per the acknowledgement of the receipt (Picard et al. 2016).

In the final section it needs to be noted that Jasmine parked the car at the property of

commercial airport. She did not use it for a total of ten days as the car was parked. Moreover,

she did not use the car. In this case, there cannot be scope for car parking fringe benefit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

originating from Jasmine pertaining to the car parked at the Rapid Heat premises. This was

seen with the parking of the car within one-kilometre radius of the commercial parking place.

Therefore, it cannot be considered under the FBT (Eccleston and Krever 2017).

It is seen that RHP Ltd disbursed a loan to Jasmine worth $ 500000 as per the

statutory interest rate of $ 4.25%. The total sum of $ 500000 will be made as a loan to

Jasmine which should be considered as per the benefit of employer to employee. This is

directly seen under “Division 4 of the FBTAA 1986”.

Conclusion:

The benefits are per Jasmine is constituted with the benefits under the “section 7 of

the FBTAA 1986”. The usage of vehicle is subjected to the benefits under the “sub-section

136 (1), FBTAA 1986”. Some of the other benefits of the reimbursement of the repair as per

“sub-section 136 (1), FBTAA 1986”. Some of the other reimbursement of the repair of the

expenses are made with the loan constituted to the benefits as per “FBTAA 1986”.

Answer to B:

As stated in the “section 8-1 of the ITAA 1997”, the taxpayers are allowed to claims

for the deductions which are allowed for the expenses which are considered with the

outgoings generated with the assessable income. This is directly claimable for deductions.

The substitute needs to be well-thought-out with the remaining part of the debt

amounting to $50,000 for shares rather than lending the same amount in a situation where

jasmine will be able to claim for an allowable deduction as per “section 8-1, ITAA 1997”.

Despite of this, the remaining part of the loan are seen as per the interest on loan which may

otherwise be considered as per the “section 8-1, ITAA 1997” (Bevacqua 2015).

originating from Jasmine pertaining to the car parked at the Rapid Heat premises. This was

seen with the parking of the car within one-kilometre radius of the commercial parking place.

Therefore, it cannot be considered under the FBT (Eccleston and Krever 2017).

It is seen that RHP Ltd disbursed a loan to Jasmine worth $ 500000 as per the

statutory interest rate of $ 4.25%. The total sum of $ 500000 will be made as a loan to

Jasmine which should be considered as per the benefit of employer to employee. This is

directly seen under “Division 4 of the FBTAA 1986”.

Conclusion:

The benefits are per Jasmine is constituted with the benefits under the “section 7 of

the FBTAA 1986”. The usage of vehicle is subjected to the benefits under the “sub-section

136 (1), FBTAA 1986”. Some of the other benefits of the reimbursement of the repair as per

“sub-section 136 (1), FBTAA 1986”. Some of the other reimbursement of the repair of the

expenses are made with the loan constituted to the benefits as per “FBTAA 1986”.

Answer to B:

As stated in the “section 8-1 of the ITAA 1997”, the taxpayers are allowed to claims

for the deductions which are allowed for the expenses which are considered with the

outgoings generated with the assessable income. This is directly claimable for deductions.

The substitute needs to be well-thought-out with the remaining part of the debt

amounting to $50,000 for shares rather than lending the same amount in a situation where

jasmine will be able to claim for an allowable deduction as per “section 8-1, ITAA 1997”.

Despite of this, the remaining part of the loan are seen as per the interest on loan which may

otherwise be considered as per the “section 8-1, ITAA 1997” (Bevacqua 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Ali, M., Sales, A.B.I.C.L., Barwick, J., Digirolamo, L., Australia, C.R., Officer, D.R., Do,

T.N., Supply, I.W.W., El Boustani, P., Sales, S.H.B.B.H. and Khalid, A., 2017. School of

Business.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

Eccleston, R. and Krever, R. eds., 2017. The Future of Federalism: Intergovernmental

Financial Relations in an Age of Austerity. Edward Elgar Publishing.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

References:

Ali, M., Sales, A.B.I.C.L., Barwick, J., Digirolamo, L., Australia, C.R., Officer, D.R., Do,

T.N., Supply, I.W.W., El Boustani, P., Sales, S.H.B.B.H. and Khalid, A., 2017. School of

Business.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davison, M., Monotti, A. and Wiseman, L., 2015. Australian intellectual property law.

Cambridge University Press.

Eccleston, R. and Krever, R. eds., 2017. The Future of Federalism: Intergovernmental

Financial Relations in an Age of Austerity. Edward Elgar Publishing.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

11TAXATION LAW

Law.ato.gov.au. (2018). ATO ID 2004/120 (Withdrawn) - Does the CGT concession amount

of a discount capital gain form part of a taxpayer's 'net exempt income' in terms of section

36-20 of the Income Tax Assessment Act 1997 (ITAA 1997) against which the taxpayer must

first offset tax losses in accordance with section 36-15 of the ITAA 1997?. [online] Available

at: http://law.ato.gov.au/atolaw/view.htm?docid=%22AID%2FAID2004120%2F00001%22

[Accessed 18 Sep. 2018].

Middleton, T., 2015. Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, pp.555-580.

Picard, R., Belair-Gagnon, V., Ranchordás, S., Aptowitzer, A., Flynn, R., Papandrea, F. and

Townend, J., 2016. The impact of charity and tax law and regulation on not-for-profit news

organizations.

Richardson, G., 2016. The Determinants of Tax Evasion: A Cross-Country Study.

In Financial Crimes: Psychological, Technological, and Ethical Issues (pp. 33-57). Springer,

Cham.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Sawyer, A., 2016. Complexity of tax simplification: A New Zealand perspective. In The

Complexity of Tax Simplification(pp. 110-132). Palgrave Macmillan, London.

Tan, L.M., Braithwaite, V. and Reinhart, M., 2016. Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice. International Small

Business Journal, 34(3), pp.329-344.

Law.ato.gov.au. (2018). ATO ID 2004/120 (Withdrawn) - Does the CGT concession amount

of a discount capital gain form part of a taxpayer's 'net exempt income' in terms of section

36-20 of the Income Tax Assessment Act 1997 (ITAA 1997) against which the taxpayer must

first offset tax losses in accordance with section 36-15 of the ITAA 1997?. [online] Available

at: http://law.ato.gov.au/atolaw/view.htm?docid=%22AID%2FAID2004120%2F00001%22

[Accessed 18 Sep. 2018].

Middleton, T., 2015. Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, pp.555-580.

Picard, R., Belair-Gagnon, V., Ranchordás, S., Aptowitzer, A., Flynn, R., Papandrea, F. and

Townend, J., 2016. The impact of charity and tax law and regulation on not-for-profit news

organizations.

Richardson, G., 2016. The Determinants of Tax Evasion: A Cross-Country Study.

In Financial Crimes: Psychological, Technological, and Ethical Issues (pp. 33-57). Springer,

Cham.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Sawyer, A., 2016. Complexity of tax simplification: A New Zealand perspective. In The

Complexity of Tax Simplification(pp. 110-132). Palgrave Macmillan, London.

Tan, L.M., Braithwaite, V. and Reinhart, M., 2016. Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice. International Small

Business Journal, 34(3), pp.329-344.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.