Taxation Law Assignment Solution: HI6028, Semester 2, Holmes Institute

VerifiedAdded on 2022/10/17

|13

|2797

|90

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing key aspects of Australian taxation. The solution delves into the entitlement of input tax credits for City Sky Co., analyzing GST implications on land purchases and developmental services, including the application of the reverse charge mechanism. Furthermore, it examines capital gains tax (CGT) events, specifically the sale of land, shares in Rio Tinto (pre-CGT asset), a stamp collection, and a grand piano (personal use asset). The analysis includes detailed calculations and references to relevant legislation (ITAA 97, GST Act 1999), providing a thorough understanding of taxation principles applied to real-world scenarios. The assignment covers topics such as acquisition costs, incidental costs, cost of ownership, enhancement costs, and title costs, and the tax treatment of collectables and personal use assets, with the aim of helping students understand and apply the concepts learned in the course.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

The matters that is discussed in this question is related to the entitlement of input tax

credit for the relevant income year of the City Sky Co.

Laws:

GST is regarded as the transaction based tax. The elements of the CGT generally

includes the supplier that provides the subject matter of supply and recipient that receives the

supply and are required to pay the price in return of consideration. Under “sec 9-40 & 13-15,

GST Act 1999” the liability for GST happens when there is any taxable supply or importation

is made by the taxpayer (James 2018). The GST is generally payable on the value that is

added to the taxable supply. According to the “sec 9-10, GST Act 1999” a supply is regarded

the transaction which constitute any form of goods and service. It also includes the provision

of any form of advice or information. While “sec 9-10 of the GST Act 1999” says that GST

is commonly imposed on the taxable supply (Millar 2016). An individual taxpayer might

make a taxable supply if there is any kind of supply for the consideration of price during the

course or progress of the company. The taxable supply must be related with Australia and the

company should be the registered company.

The tax treatment related to land and the proceeds that are originating from the sale of

land is usually reliant on whether it is treated as the capital asset or the subject to business or

any form of commercial transaction (Giesecke and Tran 2018). Vacant land is generally

treated as the capital asset which is subjected to the capital gains tax. However, when the

transactions relating to land is considered as the part of business activity, then any further

sales proceeds will be treated as the ordinary income and will be subject to GST. While a

taxpayer that purchases land for the use in business or for making profit then the sales

Answer to question 1:

Issues:

The matters that is discussed in this question is related to the entitlement of input tax

credit for the relevant income year of the City Sky Co.

Laws:

GST is regarded as the transaction based tax. The elements of the CGT generally

includes the supplier that provides the subject matter of supply and recipient that receives the

supply and are required to pay the price in return of consideration. Under “sec 9-40 & 13-15,

GST Act 1999” the liability for GST happens when there is any taxable supply or importation

is made by the taxpayer (James 2018). The GST is generally payable on the value that is

added to the taxable supply. According to the “sec 9-10, GST Act 1999” a supply is regarded

the transaction which constitute any form of goods and service. It also includes the provision

of any form of advice or information. While “sec 9-10 of the GST Act 1999” says that GST

is commonly imposed on the taxable supply (Millar 2016). An individual taxpayer might

make a taxable supply if there is any kind of supply for the consideration of price during the

course or progress of the company. The taxable supply must be related with Australia and the

company should be the registered company.

The tax treatment related to land and the proceeds that are originating from the sale of

land is usually reliant on whether it is treated as the capital asset or the subject to business or

any form of commercial transaction (Giesecke and Tran 2018). Vacant land is generally

treated as the capital asset which is subjected to the capital gains tax. However, when the

transactions relating to land is considered as the part of business activity, then any further

sales proceeds will be treated as the ordinary income and will be subject to GST. While a

taxpayer that purchases land for the use in business or for making profit then the sales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

revenue made from the land is treated as ordinary income and might be required to be

registered for goods and services.

If a taxpayer purchases a vacant land with the objective of building a dwelling for the

purpose of renting out then they may allowed to claim income tax deduction for the

expenditure such as the interest on loan, council rates and other holding costs (Datt, Nienaber

and Tran-Nam 2017). However, under “division 40” no GST is payable on such supplies and

the supplier cannot claim any input tax credits in such situation.

As stated by the ATO, the taxpayers must understand that there could be some

situation where the purchaser may be required to pay GST. This is known as reverse charge.

Reverse charge is generally required to be paid on certain offshore purchases, despite the fact

that the taxpayer is purchaser and even though the sale will attract GST liability (Main 2017).

Things beside the goods and actual property would attract GST when the Australian business

usually buys them. This includes the purchase is done out of Australia and it is made through

the business which is carried by the seller out of Australia.

The rules of reverse charge is applicable when the purchase satisfies both the

“conditions” as well as “circumstances” which is outlined below.

Conditions relating to purchase:

The rules of reverse charge is applicable when;

a. The taxpayer purchase things that is completely or partially for business carried out in

Australia

b. The taxpayer is registered under GST.

revenue made from the land is treated as ordinary income and might be required to be

registered for goods and services.

If a taxpayer purchases a vacant land with the objective of building a dwelling for the

purpose of renting out then they may allowed to claim income tax deduction for the

expenditure such as the interest on loan, council rates and other holding costs (Datt, Nienaber

and Tran-Nam 2017). However, under “division 40” no GST is payable on such supplies and

the supplier cannot claim any input tax credits in such situation.

As stated by the ATO, the taxpayers must understand that there could be some

situation where the purchaser may be required to pay GST. This is known as reverse charge.

Reverse charge is generally required to be paid on certain offshore purchases, despite the fact

that the taxpayer is purchaser and even though the sale will attract GST liability (Main 2017).

Things beside the goods and actual property would attract GST when the Australian business

usually buys them. This includes the purchase is done out of Australia and it is made through

the business which is carried by the seller out of Australia.

The rules of reverse charge is applicable when the purchase satisfies both the

“conditions” as well as “circumstances” which is outlined below.

Conditions relating to purchase:

The rules of reverse charge is applicable when;

a. The taxpayer purchase things that is completely or partially for business carried out in

Australia

b. The taxpayer is registered under GST.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Circumstances relating to purchase:

A taxpayer will be considered liable for GST under the rules of reverse charge if any one

of the conditions below is satisfied;

a. Things purchased by taxpayer for business that is done or carried out of Australia

b. The sale is associated to Australia since the things purchased has the right or option of

acquiring additional thing.

Application:

The case study provides the concerned company City Sky Co is registered for GST.

The company will be considered eligible for availing the input tax credit whenever it is

applicable. As understood, City Sky Co has bought a vacant piece of land and has the

intention of constructing 15 apartments for sell. In the current case, land is treated as the

immovable property. Land cannot viewed as taxable supply instead it constitute a CGT asset

(Brandon 2019). Perhaps the vacant land bought by City Sky Co neither constitute good nor

does it constitute a service. Within sec 9-5, GST Act 1999, the vacant does not amounts to a

taxable supply, there no GST is payable in this regard.

Evidences suggest that City Sky Co is looking forward to build a residential

apartment for the purpose of sale. The land falls under the provision of black credit. This

implies that, goods and service is acquired by the taxpayer is for the purpose constructing an

immovable property irrespective of whether in his own account or for progressing the

business. Such transactions does attracts input tax credit (Zu and Krever 2017.). Therefore,

no input tax credit entitlements originates for City Sky Co Ltd.

The company additionally reports that it has occurred developmental service that cost

$33,000 from local lawyer. The services taken from the legal advocate would be falling

within the purview of “reverse charge mechanism”. The reverse charge mechanism requires

Circumstances relating to purchase:

A taxpayer will be considered liable for GST under the rules of reverse charge if any one

of the conditions below is satisfied;

a. Things purchased by taxpayer for business that is done or carried out of Australia

b. The sale is associated to Australia since the things purchased has the right or option of

acquiring additional thing.

Application:

The case study provides the concerned company City Sky Co is registered for GST.

The company will be considered eligible for availing the input tax credit whenever it is

applicable. As understood, City Sky Co has bought a vacant piece of land and has the

intention of constructing 15 apartments for sell. In the current case, land is treated as the

immovable property. Land cannot viewed as taxable supply instead it constitute a CGT asset

(Brandon 2019). Perhaps the vacant land bought by City Sky Co neither constitute good nor

does it constitute a service. Within sec 9-5, GST Act 1999, the vacant does not amounts to a

taxable supply, there no GST is payable in this regard.

Evidences suggest that City Sky Co is looking forward to build a residential

apartment for the purpose of sale. The land falls under the provision of black credit. This

implies that, goods and service is acquired by the taxpayer is for the purpose constructing an

immovable property irrespective of whether in his own account or for progressing the

business. Such transactions does attracts input tax credit (Zu and Krever 2017.). Therefore,

no input tax credit entitlements originates for City Sky Co Ltd.

The company additionally reports that it has occurred developmental service that cost

$33,000 from local lawyer. The services taken from the legal advocate would be falling

within the purview of “reverse charge mechanism”. The reverse charge mechanism requires

5TAXATION LAW

the service receiver to pay the GST. As the service of advocate acquired from Maurice

Blackburn is in carrying on the enterprise activity and also has connection with Australia,

therefore, City Sky Co can claim the input tax credit for the GST paid on services availed.

The service of advocate satisfies the reverse charge condition because the purchase is

solely for business it is carrying in Australia and also meets the circumstances where the sale

is related to Australia because the legal services represents the right to acquire the vacant

land. So City Sky Co is entitled to input tax credit relating to taxes paid on services from

Maurice Blackburn.

Conclusion:

On a conclusive note, no input tax credit entitlement arises for the purchase of vacant

land for City Sky Co however, the company is entitled to input tax credit relating to taxes

paid on services from Maurice Blackburn.

Answer to question 2:

Sale of block of land:

Under “sec 104-10, ITAA 97” a CGT event A1 is usually concerned with the sale of

asset upon the change of ownership (Schellekens 2016). The cost of asset generally has five

elements under “sec 110-25, ITAA 97”. These are as follows;

1. Acquisition Cost: The acquisition cost is held as the first element of CGT asset under

“s.110-25(2), ITAA 1997” (Huizinga, Voget and Wagner 2018). This includes

a. The total amount of money that is paid for acquiring the asset

b. The market value prevalent of the asset or they are required to provide in regard to

purchasing it.

the service receiver to pay the GST. As the service of advocate acquired from Maurice

Blackburn is in carrying on the enterprise activity and also has connection with Australia,

therefore, City Sky Co can claim the input tax credit for the GST paid on services availed.

The service of advocate satisfies the reverse charge condition because the purchase is

solely for business it is carrying in Australia and also meets the circumstances where the sale

is related to Australia because the legal services represents the right to acquire the vacant

land. So City Sky Co is entitled to input tax credit relating to taxes paid on services from

Maurice Blackburn.

Conclusion:

On a conclusive note, no input tax credit entitlement arises for the purchase of vacant

land for City Sky Co however, the company is entitled to input tax credit relating to taxes

paid on services from Maurice Blackburn.

Answer to question 2:

Sale of block of land:

Under “sec 104-10, ITAA 97” a CGT event A1 is usually concerned with the sale of

asset upon the change of ownership (Schellekens 2016). The cost of asset generally has five

elements under “sec 110-25, ITAA 97”. These are as follows;

1. Acquisition Cost: The acquisition cost is held as the first element of CGT asset under

“s.110-25(2), ITAA 1997” (Huizinga, Voget and Wagner 2018). This includes

a. The total amount of money that is paid for acquiring the asset

b. The market value prevalent of the asset or they are required to provide in regard to

purchasing it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

2. Incidental Cost: Within “s.110-35 ITAA 97”, these cost include the cost paid to

surveyor, legal fees, stamp duty, borrowing expenses etc.

3. Cost of ownership: This is usually applied for assets purchased following 20th August

1991. Under “sec 110-25 (4), ITAA 1997” the ownership cost include;

a. interest money for borrowed funds to purchase asset

b. Land taxes and rates

c. Cost of maintaining, insurance and repair of asset

4. Enhancement Cost: This is regarded as the fourth element which includes the capital

expenses occurred in increasing or preserving the value of asset under “sec 110-25

(5), ITAA 97” (Freebairn 2016).

5. Title Cost: This is regarded as the fifth element of cost base under “sec 110-25 (6),

ITAA 1997” which includes cost occurred for establishing, preserving or defending

the title to the asset.

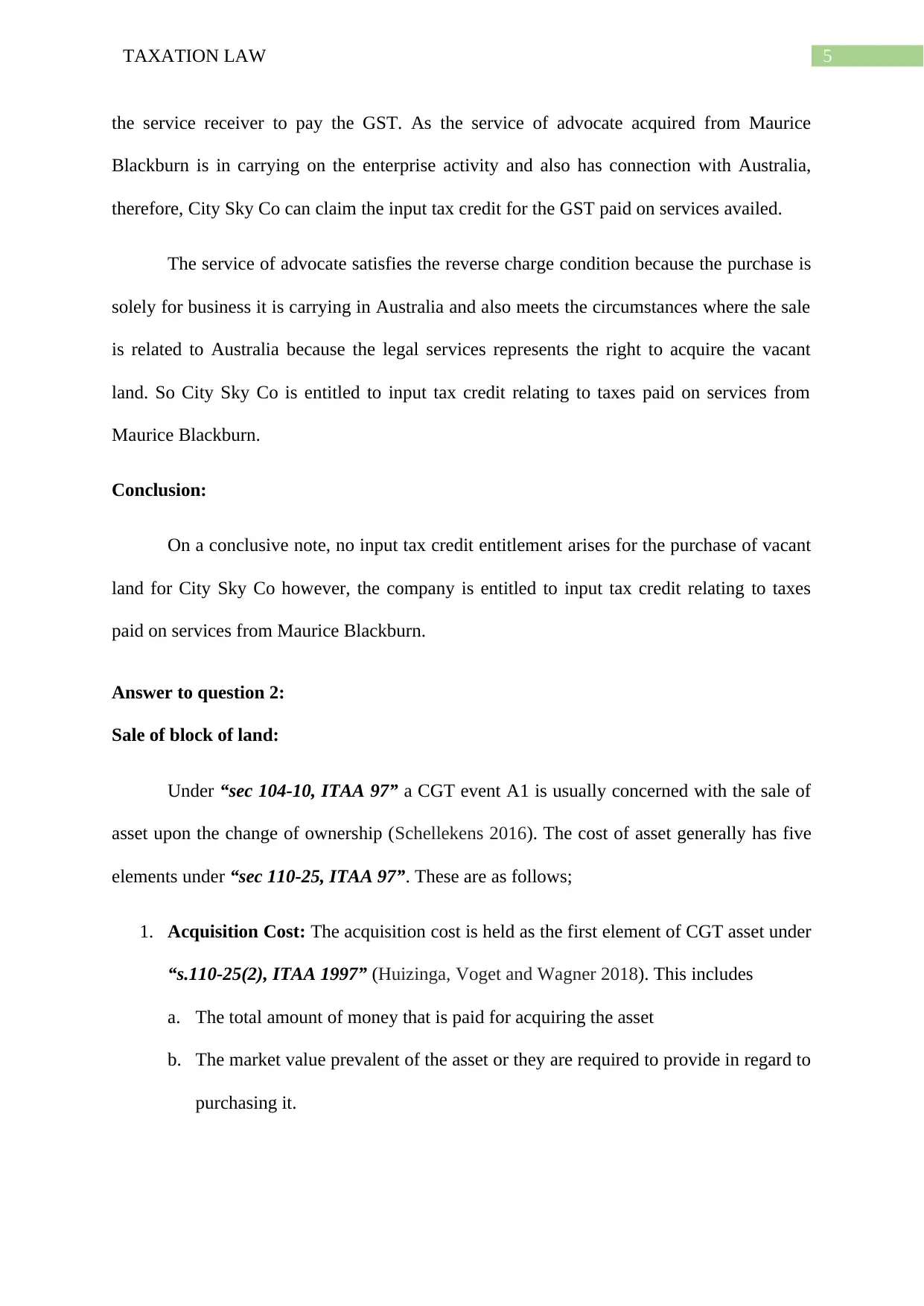

Details furnished by Emma suggest that a block of land was sold during the year and

realised a sum of $1,000,000 from that sale. However prior to sale, Emma paid a purchase

price of $250,000 to acquire the property. The purchase price paid to acquire the asset forms

the part of first element cost base for Emma in determining her capital gains under “sec 110-

25 (2), ITAA 97” (Evans, Minas and Lim 2015). Emma while purchasing the land also paid

incidental cost associated to it. This includes the stamp duty and legal fees of $5,000 and

$10,000 respectively. Under “sec 110-35 ITAA 1997”, these cost will be included in the cost

base of block of land to ascertain the overall cost base of asset.

An interest on loan totalling $32,000 was paid by Emma. All through the ownership

period expenses relating to council rates, water rates and insurance totalling $22,000 was paid

by Emma. These expenses are categorized as cost of ownership of land. Referring “sec 110-

25 (4)”, this will be included under the third element cost base to determine the overall value

2. Incidental Cost: Within “s.110-35 ITAA 97”, these cost include the cost paid to

surveyor, legal fees, stamp duty, borrowing expenses etc.

3. Cost of ownership: This is usually applied for assets purchased following 20th August

1991. Under “sec 110-25 (4), ITAA 1997” the ownership cost include;

a. interest money for borrowed funds to purchase asset

b. Land taxes and rates

c. Cost of maintaining, insurance and repair of asset

4. Enhancement Cost: This is regarded as the fourth element which includes the capital

expenses occurred in increasing or preserving the value of asset under “sec 110-25

(5), ITAA 97” (Freebairn 2016).

5. Title Cost: This is regarded as the fifth element of cost base under “sec 110-25 (6),

ITAA 1997” which includes cost occurred for establishing, preserving or defending

the title to the asset.

Details furnished by Emma suggest that a block of land was sold during the year and

realised a sum of $1,000,000 from that sale. However prior to sale, Emma paid a purchase

price of $250,000 to acquire the property. The purchase price paid to acquire the asset forms

the part of first element cost base for Emma in determining her capital gains under “sec 110-

25 (2), ITAA 97” (Evans, Minas and Lim 2015). Emma while purchasing the land also paid

incidental cost associated to it. This includes the stamp duty and legal fees of $5,000 and

$10,000 respectively. Under “sec 110-35 ITAA 1997”, these cost will be included in the cost

base of block of land to ascertain the overall cost base of asset.

An interest on loan totalling $32,000 was paid by Emma. All through the ownership

period expenses relating to council rates, water rates and insurance totalling $22,000 was paid

by Emma. These expenses are categorized as cost of ownership of land. Referring “sec 110-

25 (4)”, this will be included under the third element cost base to determine the overall value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

of land. During the year legal fees was occurred of $5,000 for settling the dispute with

neighbour. Under the fifth element of cost base the legal expense of $5,000 will be included

to determine the overall cost of asset. This is because under “sec 110-25 (6), ITAA 1997” the

legal expenses is capital expense that was occurred by Emma in defending her right over the

land. Finally, an expense of $27,500 was incurred to remove the hazardous pine trees on the

block of land before finally putting the property on sale. Referring “sec 110-25 (5), ITAA

1997” the expenses should be included under the fourth element of cost base of asset by

Emma to determine the overall cost base of land.

of land. During the year legal fees was occurred of $5,000 for settling the dispute with

neighbour. Under the fifth element of cost base the legal expense of $5,000 will be included

to determine the overall cost of asset. This is because under “sec 110-25 (6), ITAA 1997” the

legal expenses is capital expense that was occurred by Emma in defending her right over the

land. Finally, an expense of $27,500 was incurred to remove the hazardous pine trees on the

block of land before finally putting the property on sale. Referring “sec 110-25 (5), ITAA

1997” the expenses should be included under the fourth element of cost base of asset by

Emma to determine the overall cost base of land.

8TAXATION LAW

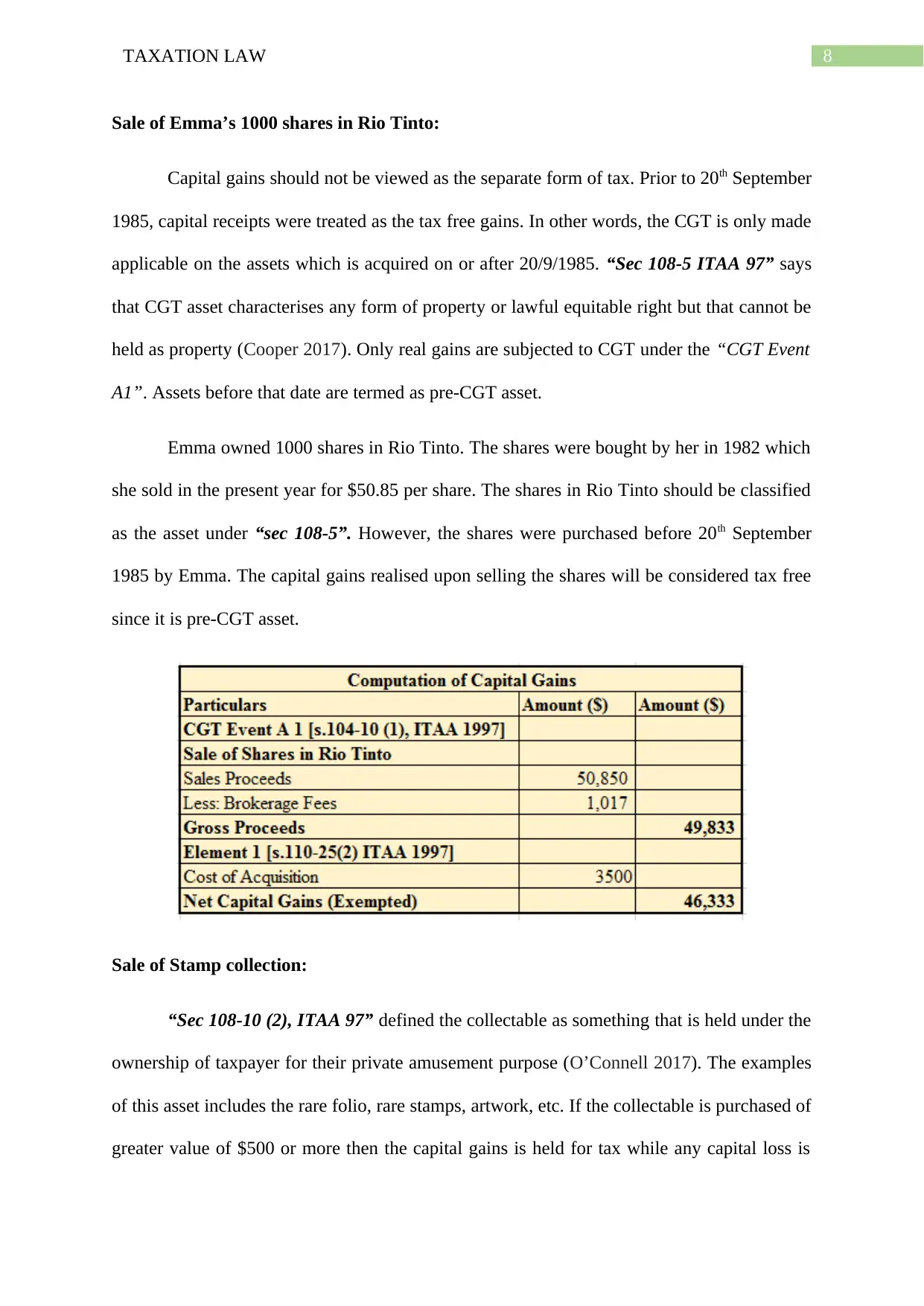

Sale of Emma’s 1000 shares in Rio Tinto:

Capital gains should not be viewed as the separate form of tax. Prior to 20th September

1985, capital receipts were treated as the tax free gains. In other words, the CGT is only made

applicable on the assets which is acquired on or after 20/9/1985. “Sec 108-5 ITAA 97” says

that CGT asset characterises any form of property or lawful equitable right but that cannot be

held as property (Cooper 2017). Only real gains are subjected to CGT under the “CGT Event

A1”. Assets before that date are termed as pre-CGT asset.

Emma owned 1000 shares in Rio Tinto. The shares were bought by her in 1982 which

she sold in the present year for $50.85 per share. The shares in Rio Tinto should be classified

as the asset under “sec 108-5”. However, the shares were purchased before 20th September

1985 by Emma. The capital gains realised upon selling the shares will be considered tax free

since it is pre-CGT asset.

Sale of Stamp collection:

“Sec 108-10 (2), ITAA 97” defined the collectable as something that is held under the

ownership of taxpayer for their private amusement purpose (O’Connell 2017). The examples

of this asset includes the rare folio, rare stamps, artwork, etc. If the collectable is purchased of

greater value of $500 or more then the capital gains is held for tax while any capital loss is

Sale of Emma’s 1000 shares in Rio Tinto:

Capital gains should not be viewed as the separate form of tax. Prior to 20th September

1985, capital receipts were treated as the tax free gains. In other words, the CGT is only made

applicable on the assets which is acquired on or after 20/9/1985. “Sec 108-5 ITAA 97” says

that CGT asset characterises any form of property or lawful equitable right but that cannot be

held as property (Cooper 2017). Only real gains are subjected to CGT under the “CGT Event

A1”. Assets before that date are termed as pre-CGT asset.

Emma owned 1000 shares in Rio Tinto. The shares were bought by her in 1982 which

she sold in the present year for $50.85 per share. The shares in Rio Tinto should be classified

as the asset under “sec 108-5”. However, the shares were purchased before 20th September

1985 by Emma. The capital gains realised upon selling the shares will be considered tax free

since it is pre-CGT asset.

Sale of Stamp collection:

“Sec 108-10 (2), ITAA 97” defined the collectable as something that is held under the

ownership of taxpayer for their private amusement purpose (O’Connell 2017). The examples

of this asset includes the rare folio, rare stamps, artwork, etc. If the collectable is purchased of

greater value of $500 or more then the capital gains is held for tax while any capital loss is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

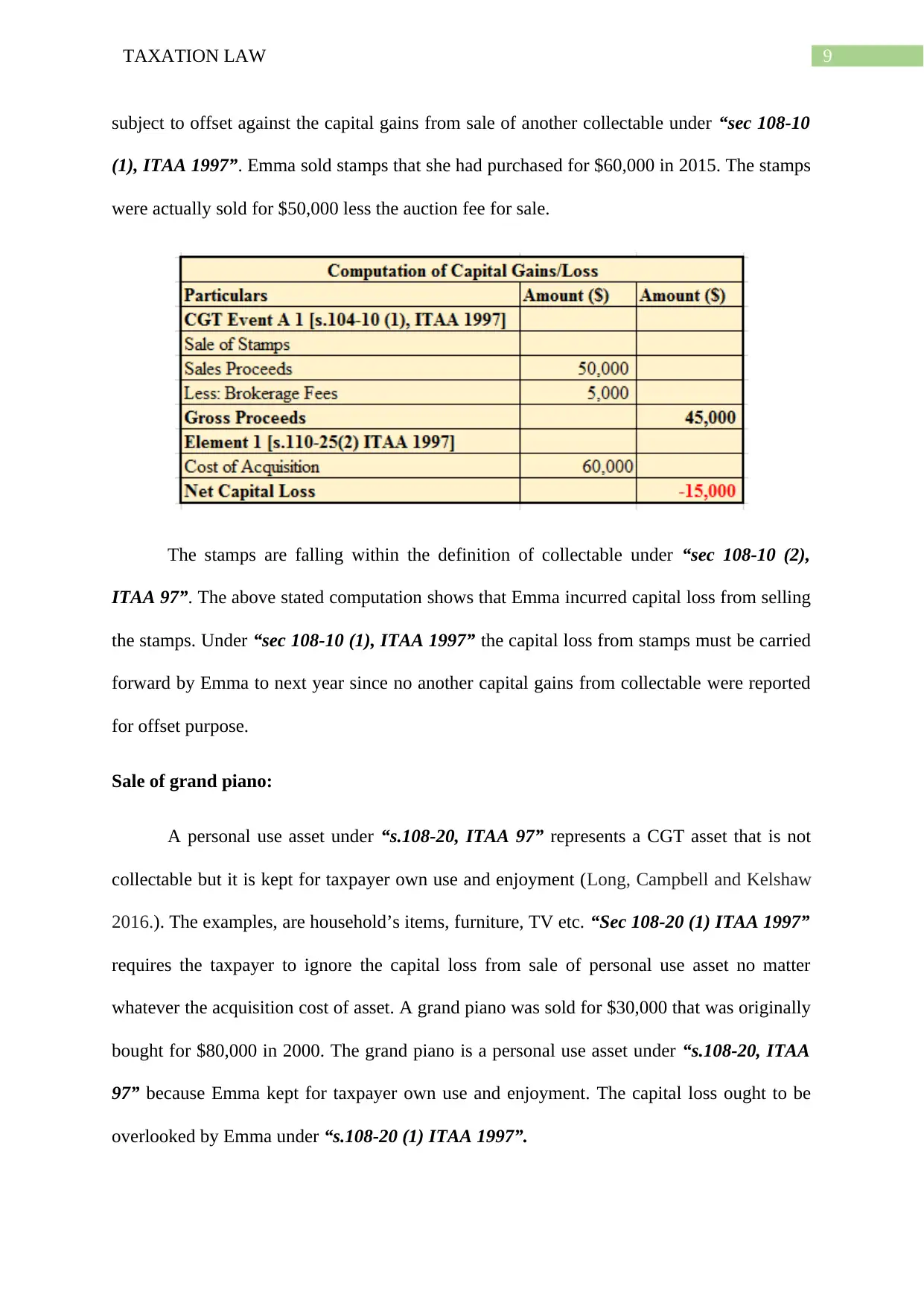

subject to offset against the capital gains from sale of another collectable under “sec 108-10

(1), ITAA 1997”. Emma sold stamps that she had purchased for $60,000 in 2015. The stamps

were actually sold for $50,000 less the auction fee for sale.

The stamps are falling within the definition of collectable under “sec 108-10 (2),

ITAA 97”. The above stated computation shows that Emma incurred capital loss from selling

the stamps. Under “sec 108-10 (1), ITAA 1997” the capital loss from stamps must be carried

forward by Emma to next year since no another capital gains from collectable were reported

for offset purpose.

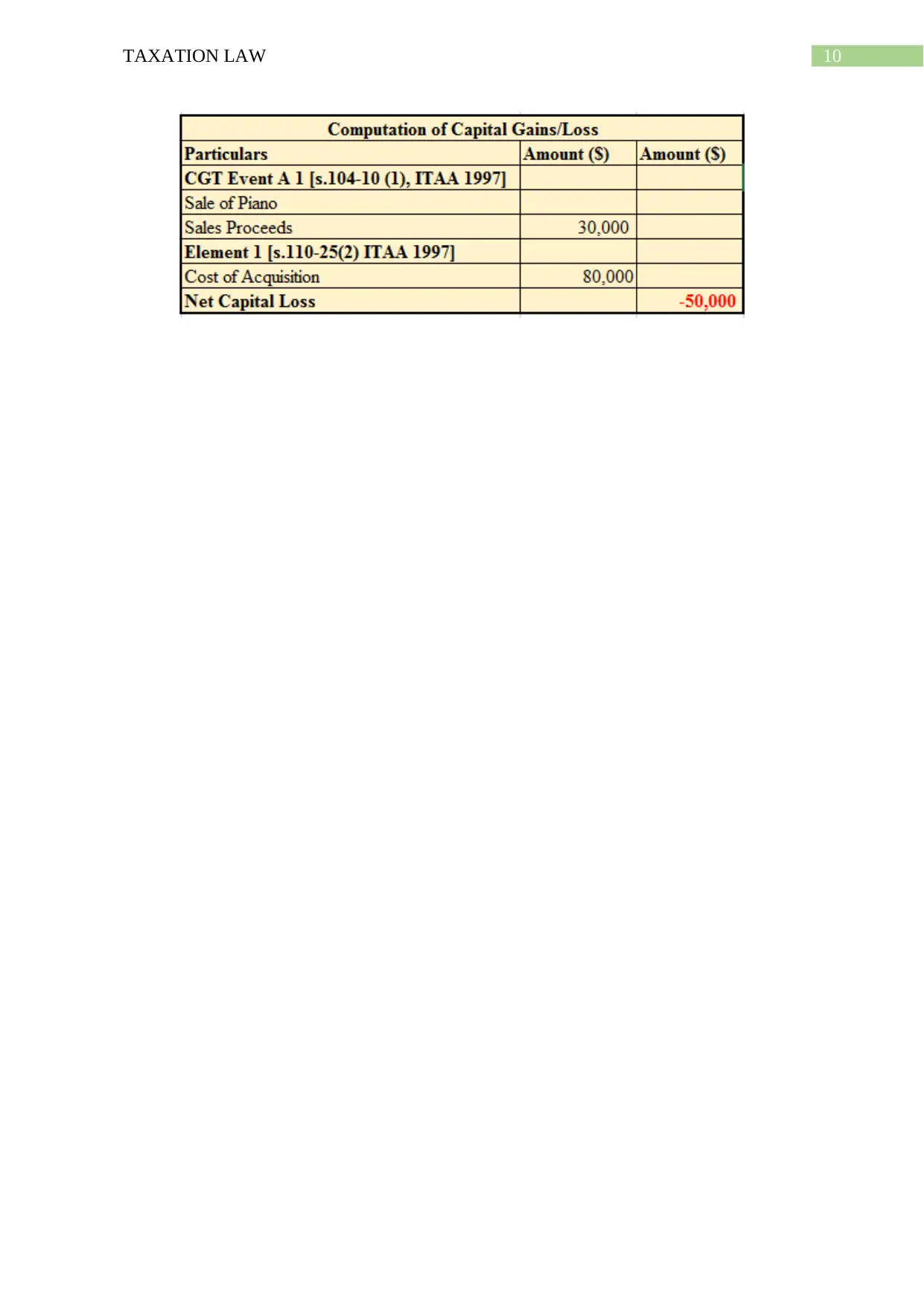

Sale of grand piano:

A personal use asset under “s.108-20, ITAA 97” represents a CGT asset that is not

collectable but it is kept for taxpayer own use and enjoyment (Long, Campbell and Kelshaw

2016.). The examples, are household’s items, furniture, TV etc. “Sec 108-20 (1) ITAA 1997”

requires the taxpayer to ignore the capital loss from sale of personal use asset no matter

whatever the acquisition cost of asset. A grand piano was sold for $30,000 that was originally

bought for $80,000 in 2000. The grand piano is a personal use asset under “s.108-20, ITAA

97” because Emma kept for taxpayer own use and enjoyment. The capital loss ought to be

overlooked by Emma under “s.108-20 (1) ITAA 1997”.

subject to offset against the capital gains from sale of another collectable under “sec 108-10

(1), ITAA 1997”. Emma sold stamps that she had purchased for $60,000 in 2015. The stamps

were actually sold for $50,000 less the auction fee for sale.

The stamps are falling within the definition of collectable under “sec 108-10 (2),

ITAA 97”. The above stated computation shows that Emma incurred capital loss from selling

the stamps. Under “sec 108-10 (1), ITAA 1997” the capital loss from stamps must be carried

forward by Emma to next year since no another capital gains from collectable were reported

for offset purpose.

Sale of grand piano:

A personal use asset under “s.108-20, ITAA 97” represents a CGT asset that is not

collectable but it is kept for taxpayer own use and enjoyment (Long, Campbell and Kelshaw

2016.). The examples, are household’s items, furniture, TV etc. “Sec 108-20 (1) ITAA 1997”

requires the taxpayer to ignore the capital loss from sale of personal use asset no matter

whatever the acquisition cost of asset. A grand piano was sold for $30,000 that was originally

bought for $80,000 in 2000. The grand piano is a personal use asset under “s.108-20, ITAA

97” because Emma kept for taxpayer own use and enjoyment. The capital loss ought to be

overlooked by Emma under “s.108-20 (1) ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

11TAXATION LAW

References:

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia, 53(7), p.357.

Cooper, R., 2017. A brief guide to tax filing. TAXtalk, 2017(65), pp.42-45.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and South

Africa. Austl. Tax F., 32, p.377.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Giesecke, J.A. and Tran, N.H., 2018. The National and Regional Consequences of Australia's

Goods and Services Tax. Economic Record, 94(306), pp.255-275.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Main, J., 2017. Taxation: Tax stings and GST tales of woe. LSJ: Law Society of NSW

Journal, (31), p.84.

References:

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia, 53(7), p.357.

Cooper, R., 2017. A brief guide to tax filing. TAXtalk, 2017(65), pp.42-45.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and South

Africa. Austl. Tax F., 32, p.377.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Giesecke, J.A. and Tran, N.H., 2018. The National and Regional Consequences of Australia's

Goods and Services Tax. Economic Record, 94(306), pp.255-275.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Main, J., 2017. Taxation: Tax stings and GST tales of woe. LSJ: Law Society of NSW

Journal, (31), p.84.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.