HI6028 Taxation Theory, Practice & Law: Australian Taxation Report

VerifiedAdded on 2023/03/30

|13

|2353

|447

Report

AI Summary

This report provides a detailed analysis of taxation theory and practices in Australia, focusing on individual income evaluation. It addresses three key questions related to taxation theories and their application under Australian law. The report examines capital gains tax (CGT) situations, including Helen's account transactions, and assesses Barbara's income from personal work, clarifying what constitutes personal exertion income. Additionally, it evaluates Patrick's income, considering scenarios involving loans to his son and the tax implications of interest received. The analysis incorporates relevant sections of the International Transactional Analysis Association and rulings from the Australian Taxation Office (ATO) to provide a comprehensive understanding of the taxation principles involved.

TAXATION PRACTISES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................2

Answer-1...............................................................................................................................................2

Answer-2...............................................................................................................................................5

Answer-3...............................................................................................................................................7

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Introduction...........................................................................................................................................2

Answer-1...............................................................................................................................................2

Answer-2...............................................................................................................................................5

Answer-3...............................................................................................................................................7

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Introduction

The report considers a discussion on taxation theory and practises for evaluating the

individual income. The report will include three questions that is most relevant to taxation

theories for the application of laws in Australia. The discussion will carry on capital gain tax

situations of the Helen account transaction on capital gain (Paris, 2017). Moreover, the

discussion will consider Barbara`s income from his personal work. Apart from this, the report

will consider assessment of income of Patrick (Paris, 2017).

Answer-1

By considering the taxation policy and theory of Australia, calculation of capital gain is

defined as when selling and disposing off the immovable and movable property is more than

purchasing price of the assets (Cobiac, Tam, Veerman, and Blakely, 2017). The difference

between the sales price and the cost price of the movable and immovable property. Tax is

related to concerned department when there is a chance to occurrence of capital gain and it is

exempt from the list when capital gain does not occur (Cobiac, Tam, Veerman, and Blakely,

2017). CGT is charged on the basis of income tax of an individual. This signifies that there

will be increase in the burden of taxpayer. However, if the (assesse) bears the whole capital

loss then there will be no provision against setting off in lieu of income (except capital gain)

but this income will be carried forward to the next year as it will be used to set off the losses

(Cobiac, Tam, Veerman, and Blakely, 2017).

Most importantly, assets that are purchased after 20th September 1985 are further entitled to

the taxation of capital gain regime. Until that time, there was no rate specified as the

Australian taxation system (Chardon, Freudenberg, and Bramble, 2016). When the assesse

holds the assets for a time of 12 months or higher. In this case, the capital gain is limited to

the 23.5 percent because of 50 percent of the CGT discount. This discounting benefit is not

The report considers a discussion on taxation theory and practises for evaluating the

individual income. The report will include three questions that is most relevant to taxation

theories for the application of laws in Australia. The discussion will carry on capital gain tax

situations of the Helen account transaction on capital gain (Paris, 2017). Moreover, the

discussion will consider Barbara`s income from his personal work. Apart from this, the report

will consider assessment of income of Patrick (Paris, 2017).

Answer-1

By considering the taxation policy and theory of Australia, calculation of capital gain is

defined as when selling and disposing off the immovable and movable property is more than

purchasing price of the assets (Cobiac, Tam, Veerman, and Blakely, 2017). The difference

between the sales price and the cost price of the movable and immovable property. Tax is

related to concerned department when there is a chance to occurrence of capital gain and it is

exempt from the list when capital gain does not occur (Cobiac, Tam, Veerman, and Blakely,

2017). CGT is charged on the basis of income tax of an individual. This signifies that there

will be increase in the burden of taxpayer. However, if the (assesse) bears the whole capital

loss then there will be no provision against setting off in lieu of income (except capital gain)

but this income will be carried forward to the next year as it will be used to set off the losses

(Cobiac, Tam, Veerman, and Blakely, 2017).

Most importantly, assets that are purchased after 20th September 1985 are further entitled to

the taxation of capital gain regime. Until that time, there was no rate specified as the

Australian taxation system (Chardon, Freudenberg, and Bramble, 2016). When the assesse

holds the assets for a time of 12 months or higher. In this case, the capital gain is limited to

the 23.5 percent because of 50 percent of the CGT discount. This discounting benefit is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

given to the companies (Forrest, and Hirayama, 2015). Even though, each asset, which is

purchased before 21 September 1999 can avail the benefit of indexation method. The assesse

can be used any of the two methods that give low tax value. This discount method and the

indexation method can not avail benefit when the asset holds less than 12 months.

Indexation method- This method evaluates the value of acquired expenditure and assets. As

per the method, the calculation is based on dividing the CPI where the asset is integrated in

the quarter. It is calculated to enrich the account encountered on the cost-based inflation for

the asset.

In first case of Helen`s transaction, indexation method has been used because these

transactions are purchased and processed before 21st September, 1999.

1. When the asset has been acquired before 1999 then indexation method will be

applicable while calculating CGT.

Particular Selling price Purchase price Capital gain /loss

Amount ($) 12000 12042 (42)

Working note-

a. Purchase cost= 112.6/61.2

= 1.838*(5500) = 10120.

b. It has been observed that historical sculpture has been sold off for $6000 on 1st

January 2019 that was purchased on December 1993 for $5500. When tax amount on

purchased before 21 September 1999 can avail the benefit of indexation method. The assesse

can be used any of the two methods that give low tax value. This discount method and the

indexation method can not avail benefit when the asset holds less than 12 months.

Indexation method- This method evaluates the value of acquired expenditure and assets. As

per the method, the calculation is based on dividing the CPI where the asset is integrated in

the quarter. It is calculated to enrich the account encountered on the cost-based inflation for

the asset.

In first case of Helen`s transaction, indexation method has been used because these

transactions are purchased and processed before 21st September, 1999.

1. When the asset has been acquired before 1999 then indexation method will be

applicable while calculating CGT.

Particular Selling price Purchase price Capital gain /loss

Amount ($) 12000 12042 (42)

Working note-

a. Purchase cost= 112.6/61.2

= 1.838*(5500) = 10120.

b. It has been observed that historical sculpture has been sold off for $6000 on 1st

January 2019 that was purchased on December 1993 for $5500. When tax amount on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital gain is calculated through indexation method, there is an estimated loss of

4120.

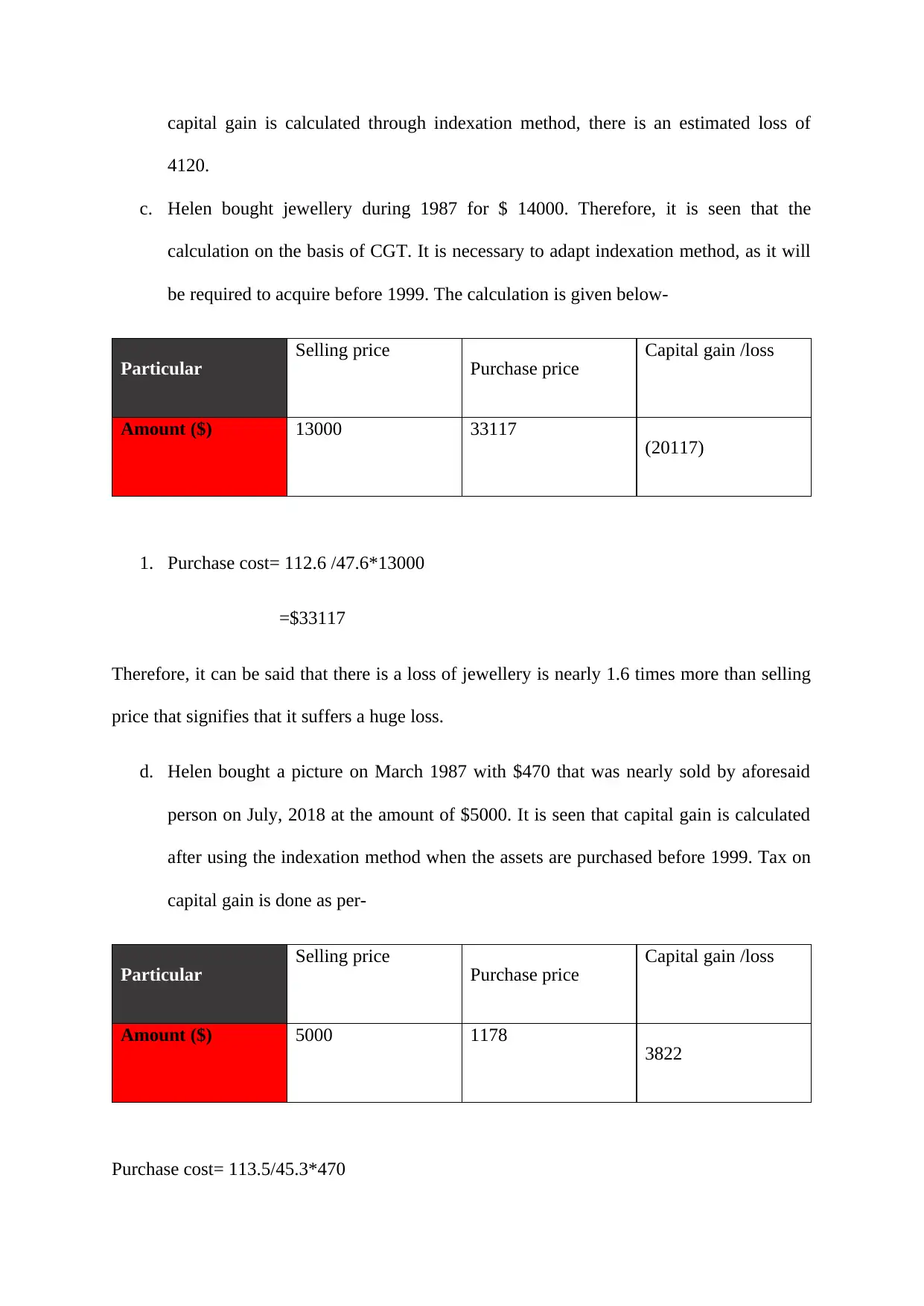

c. Helen bought jewellery during 1987 for $ 14000. Therefore, it is seen that the

calculation on the basis of CGT. It is necessary to adapt indexation method, as it will

be required to acquire before 1999. The calculation is given below-

Particular Selling price Purchase price Capital gain /loss

Amount ($) 13000 33117 (20117)

1. Purchase cost= 112.6 /47.6*13000

=$33117

Therefore, it can be said that there is a loss of jewellery is nearly 1.6 times more than selling

price that signifies that it suffers a huge loss.

d. Helen bought a picture on March 1987 with $470 that was nearly sold by aforesaid

person on July, 2018 at the amount of $5000. It is seen that capital gain is calculated

after using the indexation method when the assets are purchased before 1999. Tax on

capital gain is done as per-

Particular Selling price Purchase price Capital gain /loss

Amount ($) 5000 1178 3822

Purchase cost= 113.5/45.3*470

4120.

c. Helen bought jewellery during 1987 for $ 14000. Therefore, it is seen that the

calculation on the basis of CGT. It is necessary to adapt indexation method, as it will

be required to acquire before 1999. The calculation is given below-

Particular Selling price Purchase price Capital gain /loss

Amount ($) 13000 33117 (20117)

1. Purchase cost= 112.6 /47.6*13000

=$33117

Therefore, it can be said that there is a loss of jewellery is nearly 1.6 times more than selling

price that signifies that it suffers a huge loss.

d. Helen bought a picture on March 1987 with $470 that was nearly sold by aforesaid

person on July, 2018 at the amount of $5000. It is seen that capital gain is calculated

after using the indexation method when the assets are purchased before 1999. Tax on

capital gain is done as per-

Particular Selling price Purchase price Capital gain /loss

Amount ($) 5000 1178 3822

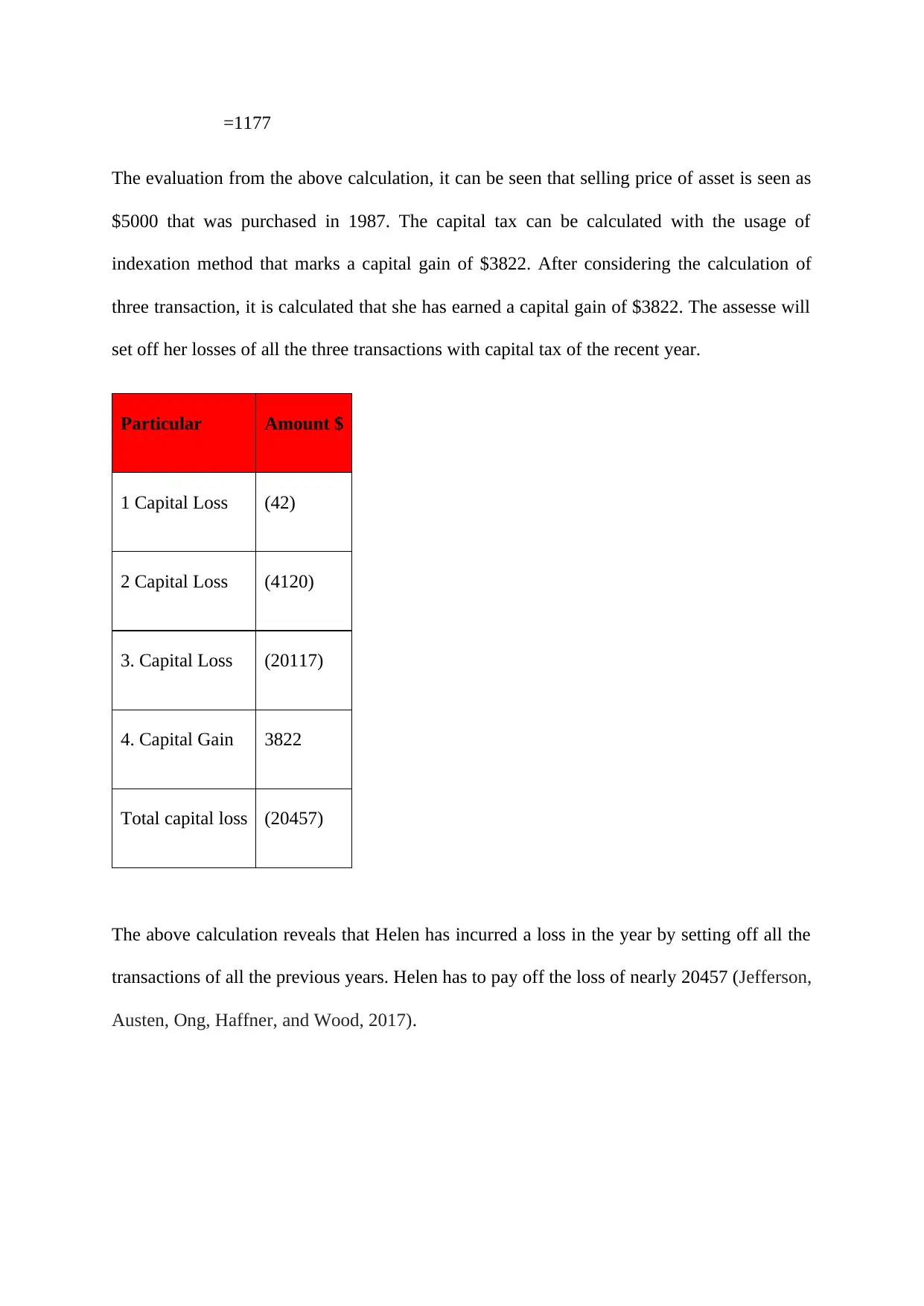

Purchase cost= 113.5/45.3*470

=1177

The evaluation from the above calculation, it can be seen that selling price of asset is seen as

$5000 that was purchased in 1987. The capital tax can be calculated with the usage of

indexation method that marks a capital gain of $3822. After considering the calculation of

three transaction, it is calculated that she has earned a capital gain of $3822. The assesse will

set off her losses of all the three transactions with capital tax of the recent year.

Particular Amount $

1 Capital Loss (42)

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20457)

The above calculation reveals that Helen has incurred a loss in the year by setting off all the

transactions of all the previous years. Helen has to pay off the loss of nearly 20457 (Jefferson,

Austen, Ong, Haffner, and Wood, 2017).

The evaluation from the above calculation, it can be seen that selling price of asset is seen as

$5000 that was purchased in 1987. The capital tax can be calculated with the usage of

indexation method that marks a capital gain of $3822. After considering the calculation of

three transaction, it is calculated that she has earned a capital gain of $3822. The assesse will

set off her losses of all the three transactions with capital tax of the recent year.

Particular Amount $

1 Capital Loss (42)

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20457)

The above calculation reveals that Helen has incurred a loss in the year by setting off all the

transactions of all the previous years. Helen has to pay off the loss of nearly 20457 (Jefferson,

Austen, Ong, Haffner, and Wood, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer-2

As per the section 393(10) of International Transactional Analysis Association, 1997, which

defines personal work and income as resulted by person in Australia that includes items are

further listed below-

a. Income generated from salary

b. Commission and Fees

c. Bonuses and Pensions

d. Allowances derived from superannuation and retiring

e. Income from profession and business

f. Allowances derived by assesse within the capacity of employee

g. Gratuities (not lump sum)

h. Income from selling the property

Other similar income perceived with the purview of income from the personal exertion as the

payment is as per the assesse time and the services (Beyer, 2018).

From the clarification in regards to the personal talent and work, the payment received by the

Barbara is $13400 from the Eco Books that owe to personal income. In this case study,

assesse has decided to sell copyright of the husband`s story. Rather than this, she has earned

an income where it is assessable that is not further included in the capital income as the

payment in regards to the time and relatable service. Barbara can be treated as per the income

that she has earned through the sale of the entitlement, right on the writing of the books, and

interest, which was published by Eco Books Ltd (Nelson, Hewson, Sundstrom, and

Hawthorne, 2019).

Barbara earned an income of $4350 in order to sell story manuscript to the Eco Books Ltd

that is a part of personal work exertion income because of similar explanation cleared and

As per the section 393(10) of International Transactional Analysis Association, 1997, which

defines personal work and income as resulted by person in Australia that includes items are

further listed below-

a. Income generated from salary

b. Commission and Fees

c. Bonuses and Pensions

d. Allowances derived from superannuation and retiring

e. Income from profession and business

f. Allowances derived by assesse within the capacity of employee

g. Gratuities (not lump sum)

h. Income from selling the property

Other similar income perceived with the purview of income from the personal exertion as the

payment is as per the assesse time and the services (Beyer, 2018).

From the clarification in regards to the personal talent and work, the payment received by the

Barbara is $13400 from the Eco Books that owe to personal income. In this case study,

assesse has decided to sell copyright of the husband`s story. Rather than this, she has earned

an income where it is assessable that is not further included in the capital income as the

payment in regards to the time and relatable service. Barbara can be treated as per the income

that she has earned through the sale of the entitlement, right on the writing of the books, and

interest, which was published by Eco Books Ltd (Nelson, Hewson, Sundstrom, and

Hawthorne, 2019).

Barbara earned an income of $4350 in order to sell story manuscript to the Eco Books Ltd

that is a part of personal work exertion income because of similar explanation cleared and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mentioned in the above part. Although she could not carry any business and profession

(Beyer, 2018).

For interview manuscript, she has collected from writing the economics book for which they

get $3200, as it will be treated according to the personal exertion income. The payment

received by the Barbara is due to the unique and talent skills regarding writing the book of

the economic, which is included for her own work (Nelson, Hewson, Sundstrom, and

Hawthorne, 2019). Therefore, it is personal income for Barbara for her talent (Johnson, and

Breunig, 2016).

When the Barbara write a book on Principles of Economics in her vacant time only after

deciding in order to sell it before selling before selling it to sign the contract with Eco books

ltd where the income for personal services (Nelson, Hewson, Sundstrom, and Hawthorne,

2019). In regards to earn the personal services and efforts, taxpayer earns an income of

personal efforts that are included in the head of income. As per the ATR 1262, where assesse

earned an income and other taxable in the head of income from personal services (Nelson,

Hewson, Sundstrom, and Hawthorne, 2019).

Conclusion

From the above discussion and evaluation, it is seen that assesse earns income from her own

efforts that is inclusive of talents and unique skills that shall use a specialisation in any field

and they would earn income that comes under the heads of income derived from personal

services and other personal exertion. A contract is signed with the other party that can further

provide monetary value to the contractor’s signer. Both the above cases include income from

personal and personal services (Beyer, 2018).

(Beyer, 2018).

For interview manuscript, she has collected from writing the economics book for which they

get $3200, as it will be treated according to the personal exertion income. The payment

received by the Barbara is due to the unique and talent skills regarding writing the book of

the economic, which is included for her own work (Nelson, Hewson, Sundstrom, and

Hawthorne, 2019). Therefore, it is personal income for Barbara for her talent (Johnson, and

Breunig, 2016).

When the Barbara write a book on Principles of Economics in her vacant time only after

deciding in order to sell it before selling before selling it to sign the contract with Eco books

ltd where the income for personal services (Nelson, Hewson, Sundstrom, and Hawthorne,

2019). In regards to earn the personal services and efforts, taxpayer earns an income of

personal efforts that are included in the head of income. As per the ATR 1262, where assesse

earned an income and other taxable in the head of income from personal services (Nelson,

Hewson, Sundstrom, and Hawthorne, 2019).

Conclusion

From the above discussion and evaluation, it is seen that assesse earns income from her own

efforts that is inclusive of talents and unique skills that shall use a specialisation in any field

and they would earn income that comes under the heads of income derived from personal

services and other personal exertion. A contract is signed with the other party that can further

provide monetary value to the contractor’s signer. Both the above cases include income from

personal and personal services (Beyer, 2018).

Answer-3

The examined and taxable income of Patrick in regards to 52000 dollars was given to the son

in order to start a new business where it will attract more tax while receiving excess payment

at the end of five years that is 6000 dollars. The calculation is related to ($58000 - $52000).

The borrowing has not been considered as the gift, as the son will repay it at the end of five

years (Johnson, and Breunig, 2016).

The capital repayment of nearly $52000 that would not part of taxable income of Patrick

where the interest received are subject to taxing by the end of five years. It is actually part of

income while filing the return and it is subject to taxing when received by the end of five

years (Guo, Lv, and Yue, 2019).

When re-examining the above scenario, Patrick gave loan to the son so that he could start a

new venture without creating any formal agreement and does not finally consider the demand

any interest and security for the sum of lending (Beyer, 2018). A person initially consider an

interest income received in the exemption. Capital repayment of the loan will not be assessed

on the part of income level of Patrick and the income will not be considered as the gift

taxable liability.

The son made a repayment of the loan by the end of two years where the interest received by

Patrick was nearly $2400 (Deutscher, and Mazumder, 2019). Most importantly, it would be

the part of the assessable income of the Patrick. As soon as the Patrick got interest income,

that is being received. On the other hand, capital repayment of nearly $ 52000 will not be

assessable on the part of income. This income will be not considered as the gift taxable

liability (Deutscher, and Mazumder, 2019).

The son repaid the loan until the ends of two years and the appropriate interest income as

received by Patrick was nearly $2400. It will be included as the assessable income of Patrick.

The examined and taxable income of Patrick in regards to 52000 dollars was given to the son

in order to start a new business where it will attract more tax while receiving excess payment

at the end of five years that is 6000 dollars. The calculation is related to ($58000 - $52000).

The borrowing has not been considered as the gift, as the son will repay it at the end of five

years (Johnson, and Breunig, 2016).

The capital repayment of nearly $52000 that would not part of taxable income of Patrick

where the interest received are subject to taxing by the end of five years. It is actually part of

income while filing the return and it is subject to taxing when received by the end of five

years (Guo, Lv, and Yue, 2019).

When re-examining the above scenario, Patrick gave loan to the son so that he could start a

new venture without creating any formal agreement and does not finally consider the demand

any interest and security for the sum of lending (Beyer, 2018). A person initially consider an

interest income received in the exemption. Capital repayment of the loan will not be assessed

on the part of income level of Patrick and the income will not be considered as the gift

taxable liability.

The son made a repayment of the loan by the end of two years where the interest received by

Patrick was nearly $2400 (Deutscher, and Mazumder, 2019). Most importantly, it would be

the part of the assessable income of the Patrick. As soon as the Patrick got interest income,

that is being received. On the other hand, capital repayment of nearly $ 52000 will not be

assessable on the part of income. This income will be not considered as the gift taxable

liability (Deutscher, and Mazumder, 2019).

The son repaid the loan until the ends of two years and the appropriate interest income as

received by Patrick was nearly $2400. It will be included as the assessable income of Patrick.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The person receiving interest will subject to taxation at the end of two years especially when

it is earned and ought to shown, as it is the part of income level after filing the return for the

next two years (Deutscher, and Mazumder, 2019).

Mode of payment that has been adopted by the David in the case of two years with the help

of cheque that does not finally affect the assessable liability of income. When son will make

payment by the cheque through any mode then it will be considered in paying the tax to the

income tax authority (Carter, and Breunig, 2019). The tax authority monitors the intention of

the parties when doing the examination of the income of the assesse and the mode of payment

gained by assesse that does not matter while previewing of the Australian taxation system

(Carter, and Breunig, 2019).

As per the rules of the gift rather than liability that are framed under the light of (ATO)

Australian Taxation Authority that will affect the pension payment received by the retiring

Patrick that enhance assessable income of Patrick within the assessment year. Patrick has

allowed gift taxation limit of nearly $10000 each year or the $30000 for the next five year

whichever is less. Any payment that has been received and the gift will be part of calculation

assessment income for the Patrick (Carter, and Breunig, 2019).

Conclusion

In the limelight of above discussion on Indexation method and discount method, tax has been

imposed on Helen`s income. Assesse shall follow rules, laws, and regulations that has been

framed by the taxation authority (ATO) within a prescribed manner. In regards to this report,

it is seen that capital transactions will discuss and conclude where Helen incurred capital loss

when considering all the three transactions. After the fourth transaction, it is seen that these

losses have been recovered with the profit of the fourth transaction. She has incurred a capital

loss of $20457. The next part of the report considers the Barbara income due to his personal

it is earned and ought to shown, as it is the part of income level after filing the return for the

next two years (Deutscher, and Mazumder, 2019).

Mode of payment that has been adopted by the David in the case of two years with the help

of cheque that does not finally affect the assessable liability of income. When son will make

payment by the cheque through any mode then it will be considered in paying the tax to the

income tax authority (Carter, and Breunig, 2019). The tax authority monitors the intention of

the parties when doing the examination of the income of the assesse and the mode of payment

gained by assesse that does not matter while previewing of the Australian taxation system

(Carter, and Breunig, 2019).

As per the rules of the gift rather than liability that are framed under the light of (ATO)

Australian Taxation Authority that will affect the pension payment received by the retiring

Patrick that enhance assessable income of Patrick within the assessment year. Patrick has

allowed gift taxation limit of nearly $10000 each year or the $30000 for the next five year

whichever is less. Any payment that has been received and the gift will be part of calculation

assessment income for the Patrick (Carter, and Breunig, 2019).

Conclusion

In the limelight of above discussion on Indexation method and discount method, tax has been

imposed on Helen`s income. Assesse shall follow rules, laws, and regulations that has been

framed by the taxation authority (ATO) within a prescribed manner. In regards to this report,

it is seen that capital transactions will discuss and conclude where Helen incurred capital loss

when considering all the three transactions. After the fourth transaction, it is seen that these

losses have been recovered with the profit of the fourth transaction. She has incurred a capital

loss of $20457. The next part of the report considers the Barbara income due to his personal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

talent and uniqueness. In the second part, Barbara`s income considers personal exertion. For

the third part, Patrick income is considered as the taxable income according to the rules and

policies as prescribed by ATA (Australian Taxation Authority).

the third part, Patrick income is considered as the taxable income according to the rules and

policies as prescribed by ATA (Australian Taxation Authority).

References

Beyer, V., 2018. Income Tax and Nondiscrimination in the GATT. Journal of International

Economic Law, 21(3), pp.547-566.

Carter, A. and Breunig, R., 2019. Do Earned Income Tax Credits for Older Workers Prolong

Labour Market Participation and Boost Earned Income? Evidence from Australia's Mature

Age Worker Tax Offset. Economic Record.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Cobiac, L.J., Tam, K., Veerman, L. and Blakely, T., 2017. Taxes and subsidies for improving

diet and population health in Australia: a cost-effectiveness modelling study. PLoS

medicine, 14(2), p.e1002232.

Deutscher, N. and Mazumder, B., 2019. Intergenerational mobility in Australia: national and

regional estimates using administrative data.

Forrest, R. and Hirayama, Y., 2015. The financialisation of the social project: Embedded

liberalism, neoliberalism and home ownership. Urban Studies, 52(2), pp.233-244.

Guo, Q., Lv, B. and Yue, X., 2019. Regulating Effect of Tax on Chinese National Income

Distribution. Routledge.

Jefferson, T., Austen, S., Ong, R., Haffner, M.E. and Wood, G.A., 2017. Housing equity

withdrawal: Perceptions of obstacles among older Australian home owners and associated

service providers. Journal of Social Policy, 46(3), pp.623-642.

Beyer, V., 2018. Income Tax and Nondiscrimination in the GATT. Journal of International

Economic Law, 21(3), pp.547-566.

Carter, A. and Breunig, R., 2019. Do Earned Income Tax Credits for Older Workers Prolong

Labour Market Participation and Boost Earned Income? Evidence from Australia's Mature

Age Worker Tax Offset. Economic Record.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Cobiac, L.J., Tam, K., Veerman, L. and Blakely, T., 2017. Taxes and subsidies for improving

diet and population health in Australia: a cost-effectiveness modelling study. PLoS

medicine, 14(2), p.e1002232.

Deutscher, N. and Mazumder, B., 2019. Intergenerational mobility in Australia: national and

regional estimates using administrative data.

Forrest, R. and Hirayama, Y., 2015. The financialisation of the social project: Embedded

liberalism, neoliberalism and home ownership. Urban Studies, 52(2), pp.233-244.

Guo, Q., Lv, B. and Yue, X., 2019. Regulating Effect of Tax on Chinese National Income

Distribution. Routledge.

Jefferson, T., Austen, S., Ong, R., Haffner, M.E. and Wood, G.A., 2017. Housing equity

withdrawal: Perceptions of obstacles among older Australian home owners and associated

service providers. Journal of Social Policy, 46(3), pp.623-642.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.