Comprehensive Tax Analysis: HI6028 Taxation Theory, Practice & Law

VerifiedAdded on 2023/06/04

|14

|3019

|353

Report

AI Summary

This report provides a comprehensive analysis of taxation theory, practice, and law, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). It examines the tax implications of various transactions, including asset sales and employee benefits. The report identifies whether receipts are revenue or capital, discusses CGT exemptions for pre-CGT assets and personal use items, and details the calculation of capital gains, including the application of discounts. It also addresses the timing of CGT application and analyzes fringe benefits such as car and loan benefits, outlining the relevant legislative clauses and calculation methods for FBT liability. The analysis is based on relevant sections of the Income Tax Assessment Act (ITAA) and Fringe Benefit Tax Assessment Act.

Taxation Theory, Practice & Law

Student Name

[Pick the date]

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

After considering the details about the various transactions that the given client has enacted over

the past year, the key objective is to provide advice in relation to the potential tax liability that

could arise considering the information that has been provided for the tax year under assessment

i.e. 2017/2018.

Law

Receipts Type

The sale of any product tends to lead to production of cash which can assume namely two types

i.e. revenue or capital. This distinction has significance from tax perspective as the former would

be added to the assessable income while the latter would be virtually tax free. As a result, the

cash proceeds need to be appropriately identified into the correct category (Hodgson,Mortimer

and Butler, 2016). This process would require giving due consideration to a plethora of factors

especially the motive of the taxpayer along with the associated circumstantial evidence linked

with the transaction. The key point is whether the underlying transaction can be termed business

or not which would go a long way to segregate the two receipts. For instance, an individual

running an antique shop would have to consider the proceeds of sale of antique items as revenue

owing to the antique items being termed as trading stock. However, for a collector, the same of

any antique would not bring in revenue receipts but rather capital proceeds which would be tax

free with the exception of capital gains tax on any potential gains that might be derived during

the sale (Gilders, et. al., 2015).

No levying of CGT

If certain conditions are complied with, then no CGT would be levied on the potential capital

gains that result from asset sale. In this regards, a particular asset category need to be highlighted

which is outlined in s. 149-10 and named as pre-CGT asset (Deutsch, et.al., 2015). In line with

the name, the acquisition of these assets was bought in the years when no tax was levied on any

CGT event related losses or gains realised. Since the assets were bought under the regime where

CGT was not applicable, hence the same treatment needs to be extended to these assets under the

1

Issue

After considering the details about the various transactions that the given client has enacted over

the past year, the key objective is to provide advice in relation to the potential tax liability that

could arise considering the information that has been provided for the tax year under assessment

i.e. 2017/2018.

Law

Receipts Type

The sale of any product tends to lead to production of cash which can assume namely two types

i.e. revenue or capital. This distinction has significance from tax perspective as the former would

be added to the assessable income while the latter would be virtually tax free. As a result, the

cash proceeds need to be appropriately identified into the correct category (Hodgson,Mortimer

and Butler, 2016). This process would require giving due consideration to a plethora of factors

especially the motive of the taxpayer along with the associated circumstantial evidence linked

with the transaction. The key point is whether the underlying transaction can be termed business

or not which would go a long way to segregate the two receipts. For instance, an individual

running an antique shop would have to consider the proceeds of sale of antique items as revenue

owing to the antique items being termed as trading stock. However, for a collector, the same of

any antique would not bring in revenue receipts but rather capital proceeds which would be tax

free with the exception of capital gains tax on any potential gains that might be derived during

the sale (Gilders, et. al., 2015).

No levying of CGT

If certain conditions are complied with, then no CGT would be levied on the potential capital

gains that result from asset sale. In this regards, a particular asset category need to be highlighted

which is outlined in s. 149-10 and named as pre-CGT asset (Deutsch, et.al., 2015). In line with

the name, the acquisition of these assets was bought in the years when no tax was levied on any

CGT event related losses or gains realised. Since the assets were bought under the regime where

CGT was not applicable, hence the same treatment needs to be extended to these assets under the

1

current regime owing to which s. 149-10 was inserted in the current tax laws so as to make

exception for these assets. In terms of date, the relevant period of pre-CGT asset possession

terminated on September 19, 1985 and any asset which has been bought after this date would be

considered potentially eligible for CGT (Gilders, et. al., 2015).

Additionally, certain specific exceptions tend to exist for some special asset classes as have been

outlined below.

Collectibles – Exempt from CGT if the underlying cost price of the object fails to exceed a

minimum price of $ 500

Personal use assets - Exempt from CGT if the underlying cost price of the object fails to exceed a

minimum price of $ 10,000

Capital Gains Determination

The liability related to CGT can only be computed once the net capital gains for the client have

been derived considering the cumulative effect of the various transactions in the manner

indicated follows (Barkoczy, 2017).

The initial step is the happening of a CGT event which brings into consideration the necessity to

compute the losses or gains incurred on the underlying asset. In this endeavour, a key role is

played by determining the appropriate CGT event as attached with the underlying event is the

basic formula for gains or loss computation (Deutsch, et.al., 2015). While a number of possible

options for CGT occur, the one that is useful is A1 since it relates to asset disposal which is the

key concern in this case. Also, the relevant formula applicable for computation of relevant gains

or losses is provided by the appropriate CGT event (Hodgson, Mortimer and Butler, 2016).

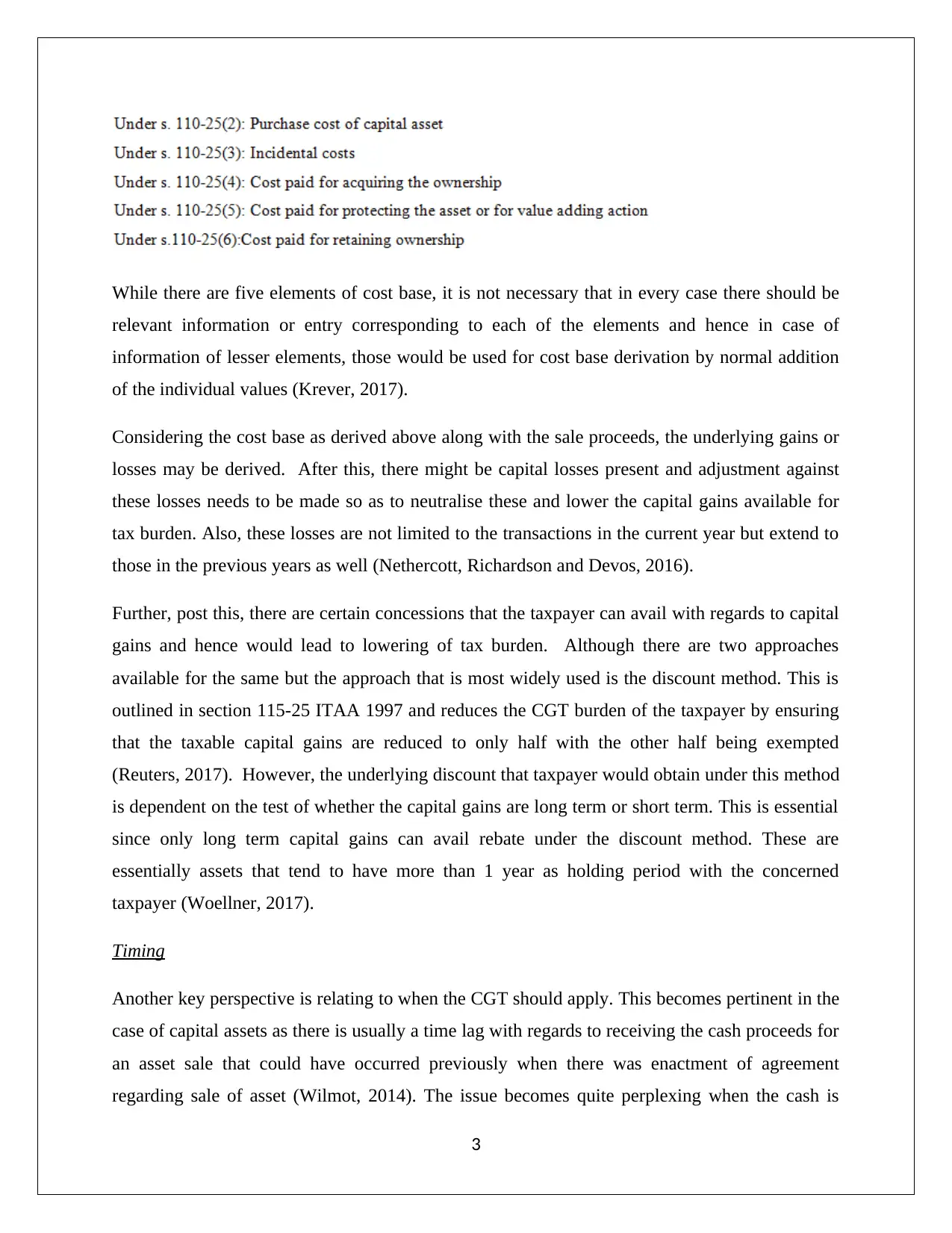

For determination of capital gains as per the approach outlined in A1 event, a critical inputs

required is the cost base whose prominent components are outlined as follows (Barkoczy, 2017).

2

exception for these assets. In terms of date, the relevant period of pre-CGT asset possession

terminated on September 19, 1985 and any asset which has been bought after this date would be

considered potentially eligible for CGT (Gilders, et. al., 2015).

Additionally, certain specific exceptions tend to exist for some special asset classes as have been

outlined below.

Collectibles – Exempt from CGT if the underlying cost price of the object fails to exceed a

minimum price of $ 500

Personal use assets - Exempt from CGT if the underlying cost price of the object fails to exceed a

minimum price of $ 10,000

Capital Gains Determination

The liability related to CGT can only be computed once the net capital gains for the client have

been derived considering the cumulative effect of the various transactions in the manner

indicated follows (Barkoczy, 2017).

The initial step is the happening of a CGT event which brings into consideration the necessity to

compute the losses or gains incurred on the underlying asset. In this endeavour, a key role is

played by determining the appropriate CGT event as attached with the underlying event is the

basic formula for gains or loss computation (Deutsch, et.al., 2015). While a number of possible

options for CGT occur, the one that is useful is A1 since it relates to asset disposal which is the

key concern in this case. Also, the relevant formula applicable for computation of relevant gains

or losses is provided by the appropriate CGT event (Hodgson, Mortimer and Butler, 2016).

For determination of capital gains as per the approach outlined in A1 event, a critical inputs

required is the cost base whose prominent components are outlined as follows (Barkoczy, 2017).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

While there are five elements of cost base, it is not necessary that in every case there should be

relevant information or entry corresponding to each of the elements and hence in case of

information of lesser elements, those would be used for cost base derivation by normal addition

of the individual values (Krever, 2017).

Considering the cost base as derived above along with the sale proceeds, the underlying gains or

losses may be derived. After this, there might be capital losses present and adjustment against

these losses needs to be made so as to neutralise these and lower the capital gains available for

tax burden. Also, these losses are not limited to the transactions in the current year but extend to

those in the previous years as well (Nethercott, Richardson and Devos, 2016).

Further, post this, there are certain concessions that the taxpayer can avail with regards to capital

gains and hence would lead to lowering of tax burden. Although there are two approaches

available for the same but the approach that is most widely used is the discount method. This is

outlined in section 115-25 ITAA 1997 and reduces the CGT burden of the taxpayer by ensuring

that the taxable capital gains are reduced to only half with the other half being exempted

(Reuters, 2017). However, the underlying discount that taxpayer would obtain under this method

is dependent on the test of whether the capital gains are long term or short term. This is essential

since only long term capital gains can avail rebate under the discount method. These are

essentially assets that tend to have more than 1 year as holding period with the concerned

taxpayer (Woellner, 2017).

Timing

Another key perspective is relating to when the CGT should apply. This becomes pertinent in the

case of capital assets as there is usually a time lag with regards to receiving the cash proceeds for

an asset sale that could have occurred previously when there was enactment of agreement

regarding sale of asset (Wilmot, 2014). The issue becomes quite perplexing when the cash is

3

relevant information or entry corresponding to each of the elements and hence in case of

information of lesser elements, those would be used for cost base derivation by normal addition

of the individual values (Krever, 2017).

Considering the cost base as derived above along with the sale proceeds, the underlying gains or

losses may be derived. After this, there might be capital losses present and adjustment against

these losses needs to be made so as to neutralise these and lower the capital gains available for

tax burden. Also, these losses are not limited to the transactions in the current year but extend to

those in the previous years as well (Nethercott, Richardson and Devos, 2016).

Further, post this, there are certain concessions that the taxpayer can avail with regards to capital

gains and hence would lead to lowering of tax burden. Although there are two approaches

available for the same but the approach that is most widely used is the discount method. This is

outlined in section 115-25 ITAA 1997 and reduces the CGT burden of the taxpayer by ensuring

that the taxable capital gains are reduced to only half with the other half being exempted

(Reuters, 2017). However, the underlying discount that taxpayer would obtain under this method

is dependent on the test of whether the capital gains are long term or short term. This is essential

since only long term capital gains can avail rebate under the discount method. These are

essentially assets that tend to have more than 1 year as holding period with the concerned

taxpayer (Woellner, 2017).

Timing

Another key perspective is relating to when the CGT should apply. This becomes pertinent in the

case of capital assets as there is usually a time lag with regards to receiving the cash proceeds for

an asset sale that could have occurred previously when there was enactment of agreement

regarding sale of asset (Wilmot, 2014). The issue becomes quite perplexing when the cash is

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

received in a different tax year while contract has been signed in a different year. In such cases,

it is advisable that the tax implications need to be represented in the year when asset sales occur

as confirmed through TR 94/29 which hails the same treatment (Sadiq, et.al., 2015).

Application

Receipts Type

The transactions entered into by the given client are not in the capacity of a business but in the

capacity of an investor. This implies that the client does not consider the liquidated objects as

goods to be sold but these are rather assets which potentially can be disposed. Under the current

circumstances, it would be appropriate to conclude that the disposal of various assets by the

client tend to amount to capital transactions. The end result of this is that the concerned cash that

the client derives from the assets would be tax free but any capital gains realised in the

liquidation process would only be taxed.

No levying of CGT

The first step in a bid to determine the tax consequences for the client is to identify the presence

of any CGT exempt assets owing to their category being pre-CGT asset. As explained earlier, the

criterion to decide the same is to review the purchase date by the current taxpayer (client),

Having reviewed the date of purchase for the various assets, it is apparent that painting is one

asset disposed which had a date of purchase pre-dating into the pre-CGT era making the given

asset free from any liabilities on account of CGT. The capital proceeds on sale are otherwise also

tax exempt.

Keeping in mind the specific exemptions, collectible limit has been maintained in the form of an

antique bed which the taxpayer had spent $ 3,500 in purchasing and hence ensuring that the cost

is higher than the limit set of $ 500. The violin sold is an item of personal use which can be

inferred from the personal use of the violin by the client for entertaining herself and this usage is

not sporadic in nature. Further, the purchase cost of violin is $ 5,500 and fails to meet the

qualification limit of $ 10,000 and hence violin is free from any possible CGT liabilities.

Capital Gains Determination

4

it is advisable that the tax implications need to be represented in the year when asset sales occur

as confirmed through TR 94/29 which hails the same treatment (Sadiq, et.al., 2015).

Application

Receipts Type

The transactions entered into by the given client are not in the capacity of a business but in the

capacity of an investor. This implies that the client does not consider the liquidated objects as

goods to be sold but these are rather assets which potentially can be disposed. Under the current

circumstances, it would be appropriate to conclude that the disposal of various assets by the

client tend to amount to capital transactions. The end result of this is that the concerned cash that

the client derives from the assets would be tax free but any capital gains realised in the

liquidation process would only be taxed.

No levying of CGT

The first step in a bid to determine the tax consequences for the client is to identify the presence

of any CGT exempt assets owing to their category being pre-CGT asset. As explained earlier, the

criterion to decide the same is to review the purchase date by the current taxpayer (client),

Having reviewed the date of purchase for the various assets, it is apparent that painting is one

asset disposed which had a date of purchase pre-dating into the pre-CGT era making the given

asset free from any liabilities on account of CGT. The capital proceeds on sale are otherwise also

tax exempt.

Keeping in mind the specific exemptions, collectible limit has been maintained in the form of an

antique bed which the taxpayer had spent $ 3,500 in purchasing and hence ensuring that the cost

is higher than the limit set of $ 500. The violin sold is an item of personal use which can be

inferred from the personal use of the violin by the client for entertaining herself and this usage is

not sporadic in nature. Further, the purchase cost of violin is $ 5,500 and fails to meet the

qualification limit of $ 10,000 and hence violin is free from any possible CGT liabilities.

Capital Gains Determination

4

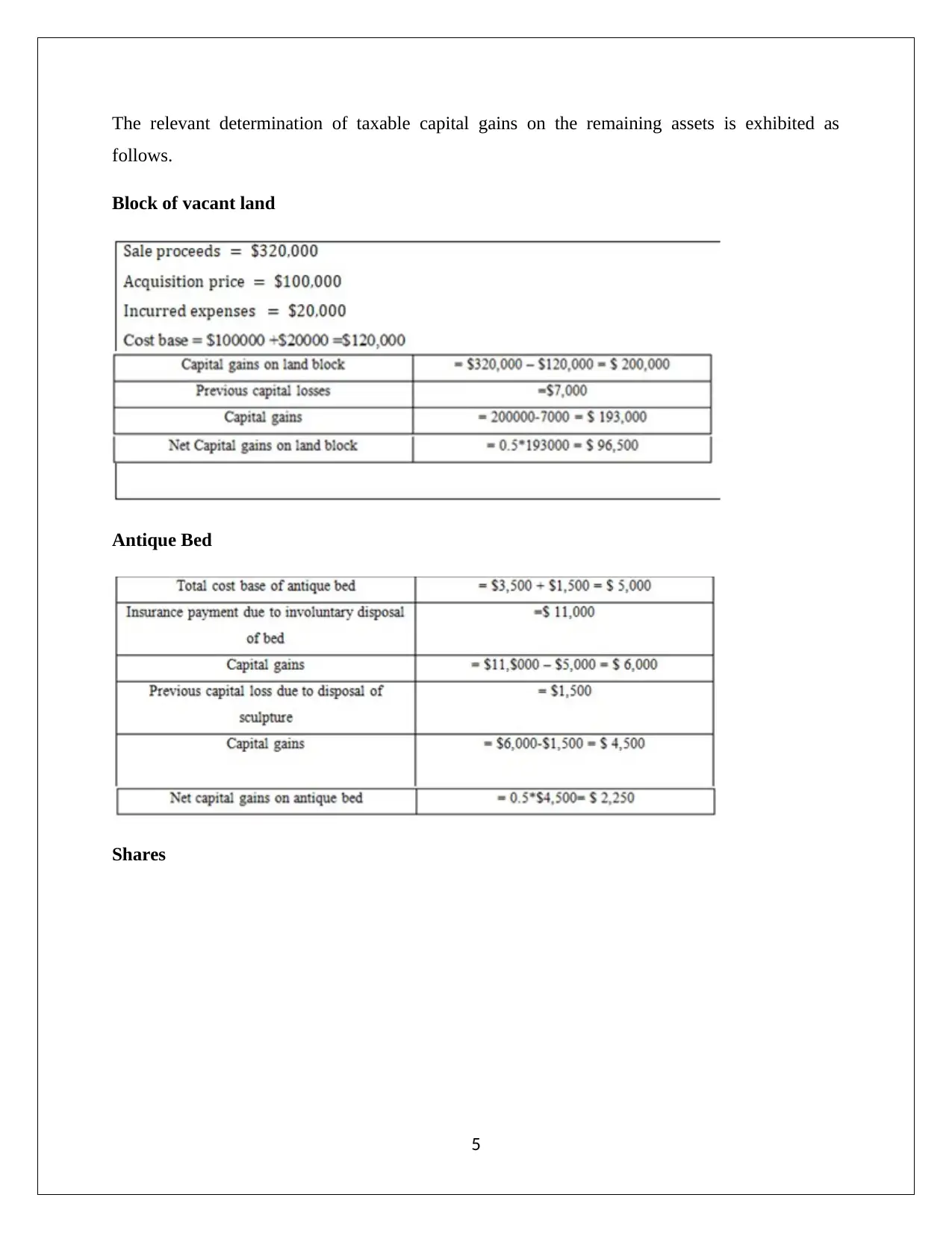

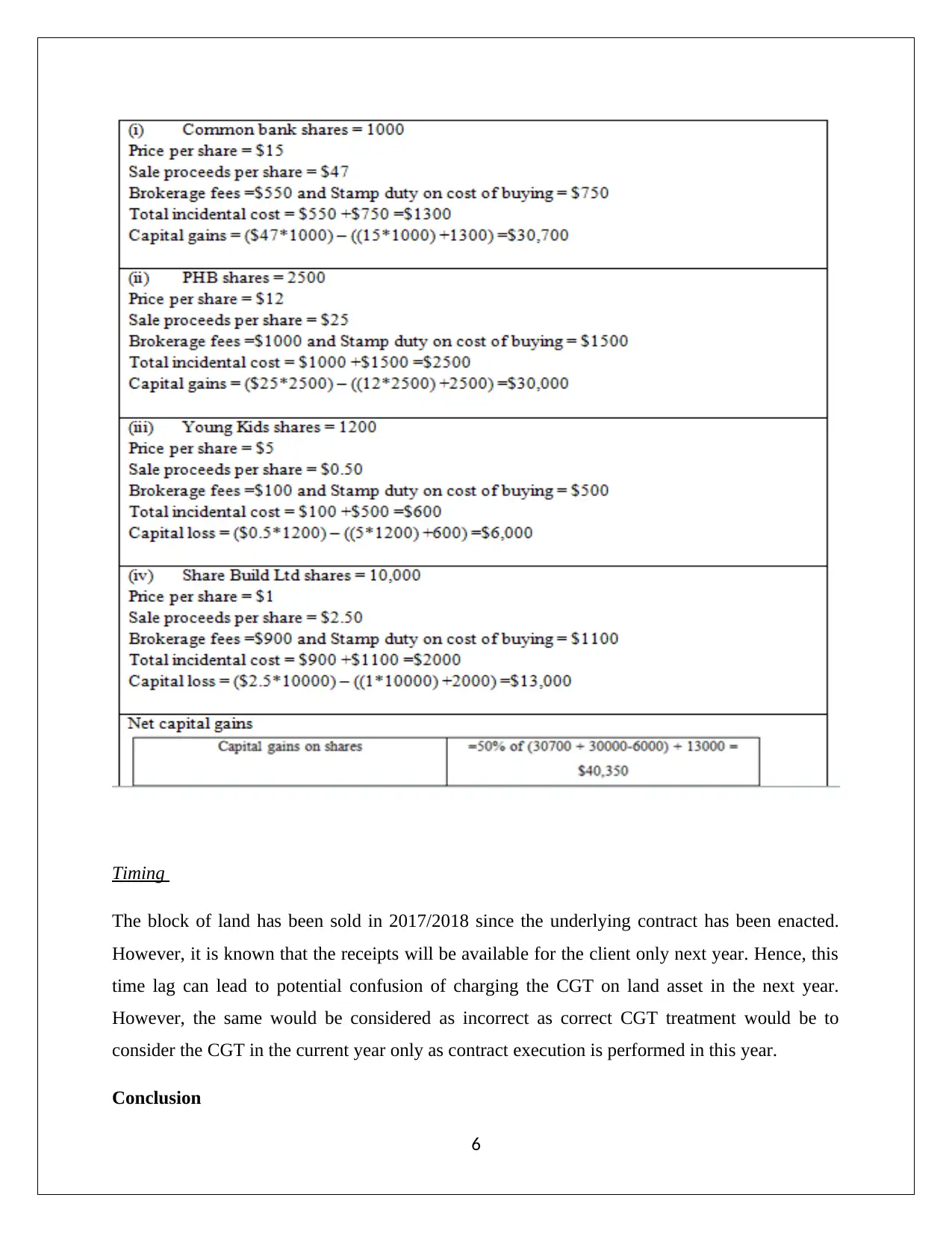

The relevant determination of taxable capital gains on the remaining assets is exhibited as

follows.

Block of vacant land

Antique Bed

Shares

5

follows.

Block of vacant land

Antique Bed

Shares

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Timing

The block of land has been sold in 2017/2018 since the underlying contract has been enacted.

However, it is known that the receipts will be available for the client only next year. Hence, this

time lag can lead to potential confusion of charging the CGT on land asset in the next year.

However, the same would be considered as incorrect as correct CGT treatment would be to

consider the CGT in the current year only as contract execution is performed in this year.

Conclusion

6

The block of land has been sold in 2017/2018 since the underlying contract has been enacted.

However, it is known that the receipts will be available for the client only next year. Hence, this

time lag can lead to potential confusion of charging the CGT on land asset in the next year.

However, the same would be considered as incorrect as correct CGT treatment would be to

consider the CGT in the current year only as contract execution is performed in this year.

Conclusion

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The client would need to pay CGT on the capital gains that result from sale land, shares and

stealing of antique bed. The remaining assets would not impose any CGT induced tax liability on

the client. Further, the capital proceeds from asset sale would be exempt from any tax.

Question 2

Issue

There is difference in the nature of fringe benefits and other employment benefits. The most

crucial difference is apparent in the fact that the tax burden of fringe benefits falls on the

employer in sharp contrast with the other employment benefits that contribute to the assessable

income of the employee. In this backdrop, the key aim of the analysis is to analyse the facts in

light of the appropriate legislation and opine on the tax burden for the concerned parties.

Law

The fringe benefits of consequence (considering the facts of the situation at hand) are discussed

as follows.

Car Fringe Benefit

Legislative Clause – “Section 7, Fringe Benefit Tax Assessment Act”

Requirement – While it is common that vehicle is provided to the employee for performing job

duties, the key aspect is permission to use the vehicle for own use of employee. Benefits to the

employee would arise only when vehicle used by employee for private use as there is no

obligation on the employer to provide any conveyance for the same and hence this amounts to a

benefit provided to employee (Sadiq, et.al., 2015).

Three steps process:

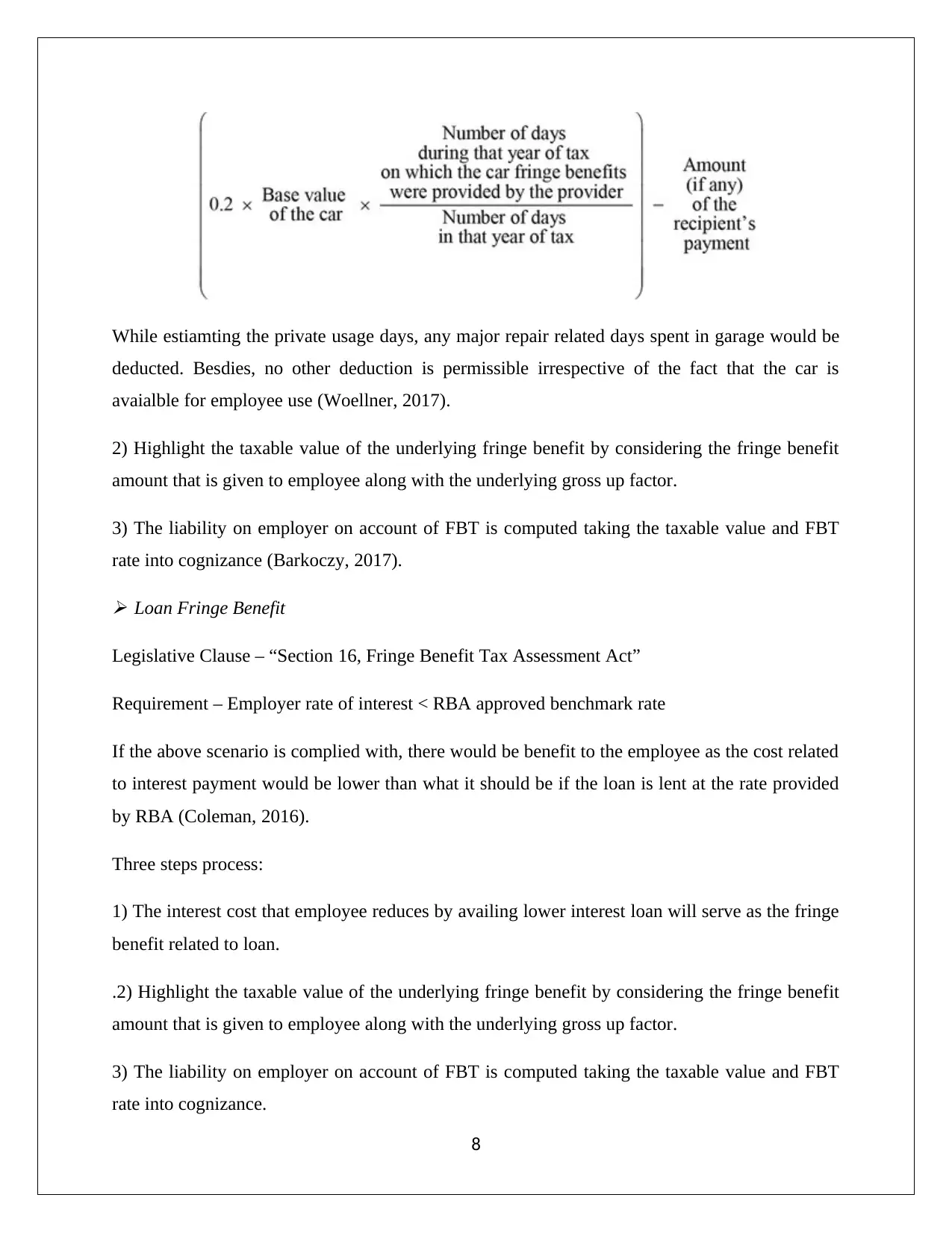

.1) Section 9 (i.e. statutory formula) can be utilised for estimating the extent of fringe benefits in

relation to car that the employee avails during the year under consideration (Wilmot, 2014).

7

stealing of antique bed. The remaining assets would not impose any CGT induced tax liability on

the client. Further, the capital proceeds from asset sale would be exempt from any tax.

Question 2

Issue

There is difference in the nature of fringe benefits and other employment benefits. The most

crucial difference is apparent in the fact that the tax burden of fringe benefits falls on the

employer in sharp contrast with the other employment benefits that contribute to the assessable

income of the employee. In this backdrop, the key aim of the analysis is to analyse the facts in

light of the appropriate legislation and opine on the tax burden for the concerned parties.

Law

The fringe benefits of consequence (considering the facts of the situation at hand) are discussed

as follows.

Car Fringe Benefit

Legislative Clause – “Section 7, Fringe Benefit Tax Assessment Act”

Requirement – While it is common that vehicle is provided to the employee for performing job

duties, the key aspect is permission to use the vehicle for own use of employee. Benefits to the

employee would arise only when vehicle used by employee for private use as there is no

obligation on the employer to provide any conveyance for the same and hence this amounts to a

benefit provided to employee (Sadiq, et.al., 2015).

Three steps process:

.1) Section 9 (i.e. statutory formula) can be utilised for estimating the extent of fringe benefits in

relation to car that the employee avails during the year under consideration (Wilmot, 2014).

7

While estiamting the private usage days, any major repair related days spent in garage would be

deducted. Besdies, no other deduction is permissible irrespective of the fact that the car is

avaialble for employee use (Woellner, 2017).

2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance (Barkoczy, 2017).

Loan Fringe Benefit

Legislative Clause – “Section 16, Fringe Benefit Tax Assessment Act”

Requirement – Employer rate of interest < RBA approved benchmark rate

If the above scenario is complied with, there would be benefit to the employee as the cost related

to interest payment would be lower than what it should be if the loan is lent at the rate provided

by RBA (Coleman, 2016).

Three steps process:

1) The interest cost that employee reduces by availing lower interest loan will serve as the fringe

benefit related to loan.

.2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance.

8

deducted. Besdies, no other deduction is permissible irrespective of the fact that the car is

avaialble for employee use (Woellner, 2017).

2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance (Barkoczy, 2017).

Loan Fringe Benefit

Legislative Clause – “Section 16, Fringe Benefit Tax Assessment Act”

Requirement – Employer rate of interest < RBA approved benchmark rate

If the above scenario is complied with, there would be benefit to the employee as the cost related

to interest payment would be lower than what it should be if the loan is lent at the rate provided

by RBA (Coleman, 2016).

Three steps process:

1) The interest cost that employee reduces by availing lower interest loan will serve as the fringe

benefit related to loan.

.2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The employer can avail some deductions if the employer utilises the loan amount for obtaining

taxable proceeds as per deductible rule (s. 18) (Coleman, 2016).

Internal expense fringe benefit

Legislative Clause – “Section 20, Fringe Benefit Tax Assessment Act”

Requirement –Some part of the personal expense of the given employee needs to be met with the

payment made by employer (Krever, 2017).

Three steps process:

1) The payment made by employer in the context of serving personal expense of employee

would be linked to fringe benefit amount.

2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance (Nethercott, Richardson and Devos, 2016).

Application

(a) The liability on account of FBT for Rapid Heat has been derived as exhibited below.

Car fringe benefit

Considering the facts, it can be said that the new Toyota car provided is Jasmine is not restrictive

in use for professional purpose and hence can be used for her personal use. Further, for the

purpose of applying statutory formula based fringe benefits related to car, no deduction in days

when repairs are minor is available. Also, in relation to time spent by car at airport parking, it is

pivotal that there was car available for Jasmine but it was her inability to use it.

9

taxable proceeds as per deductible rule (s. 18) (Coleman, 2016).

Internal expense fringe benefit

Legislative Clause – “Section 20, Fringe Benefit Tax Assessment Act”

Requirement –Some part of the personal expense of the given employee needs to be met with the

payment made by employer (Krever, 2017).

Three steps process:

1) The payment made by employer in the context of serving personal expense of employee

would be linked to fringe benefit amount.

2) Highlight the taxable value of the underlying fringe benefit by considering the fringe benefit

amount that is given to employee along with the underlying gross up factor.

3) The liability on employer on account of FBT is computed taking the taxable value and FBT

rate into cognizance (Nethercott, Richardson and Devos, 2016).

Application

(a) The liability on account of FBT for Rapid Heat has been derived as exhibited below.

Car fringe benefit

Considering the facts, it can be said that the new Toyota car provided is Jasmine is not restrictive

in use for professional purpose and hence can be used for her personal use. Further, for the

purpose of applying statutory formula based fringe benefits related to car, no deduction in days

when repairs are minor is available. Also, in relation to time spent by car at airport parking, it is

pivotal that there was car available for Jasmine but it was her inability to use it.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

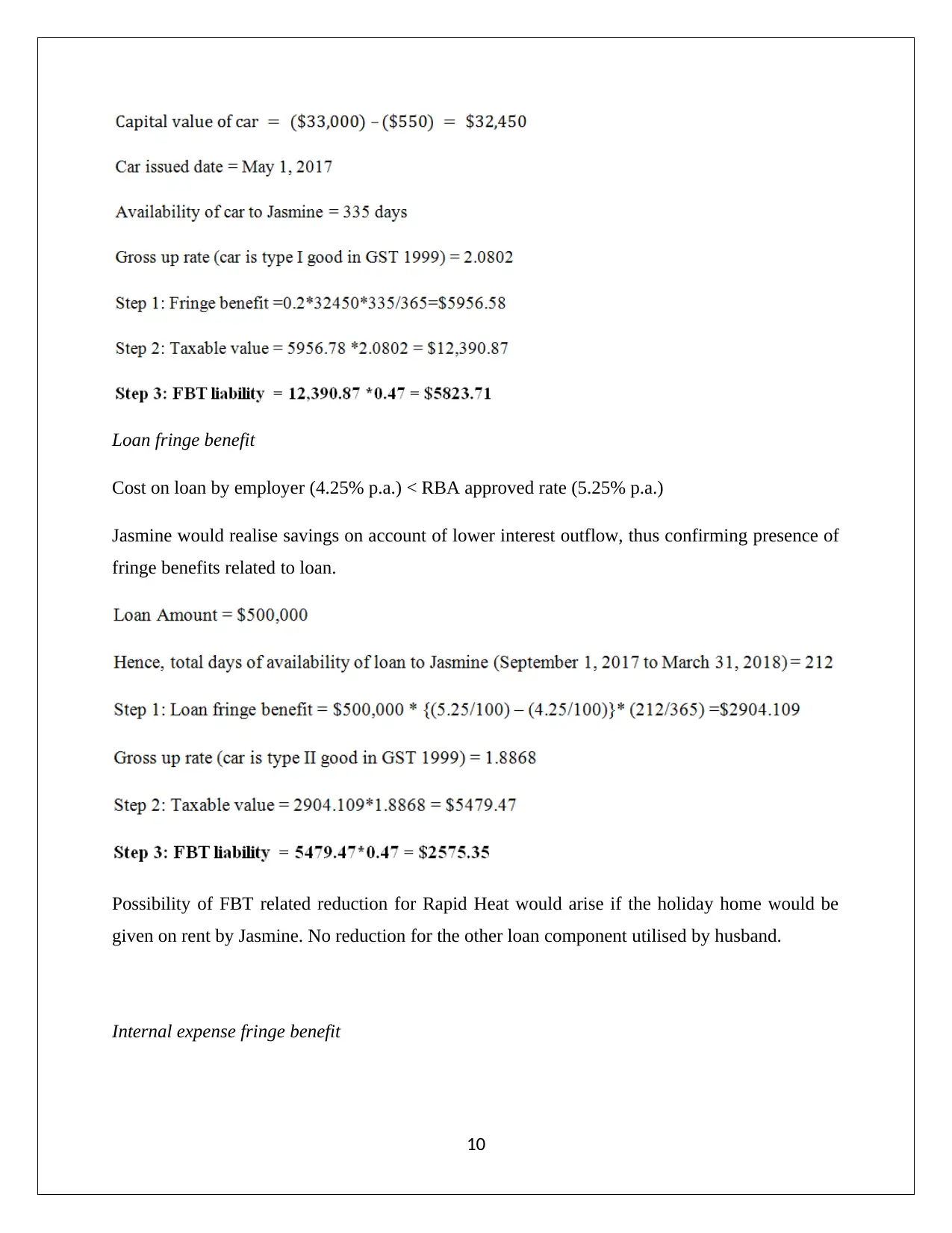

Loan fringe benefit

Cost on loan by employer (4.25% p.a.) < RBA approved rate (5.25% p.a.)

Jasmine would realise savings on account of lower interest outflow, thus confirming presence of

fringe benefits related to loan.

Possibility of FBT related reduction for Rapid Heat would arise if the holiday home would be

given on rent by Jasmine. No reduction for the other loan component utilised by husband.

Internal expense fringe benefit

10

Cost on loan by employer (4.25% p.a.) < RBA approved rate (5.25% p.a.)

Jasmine would realise savings on account of lower interest outflow, thus confirming presence of

fringe benefits related to loan.

Possibility of FBT related reduction for Rapid Heat would arise if the holiday home would be

given on rent by Jasmine. No reduction for the other loan component utilised by husband.

Internal expense fringe benefit

10

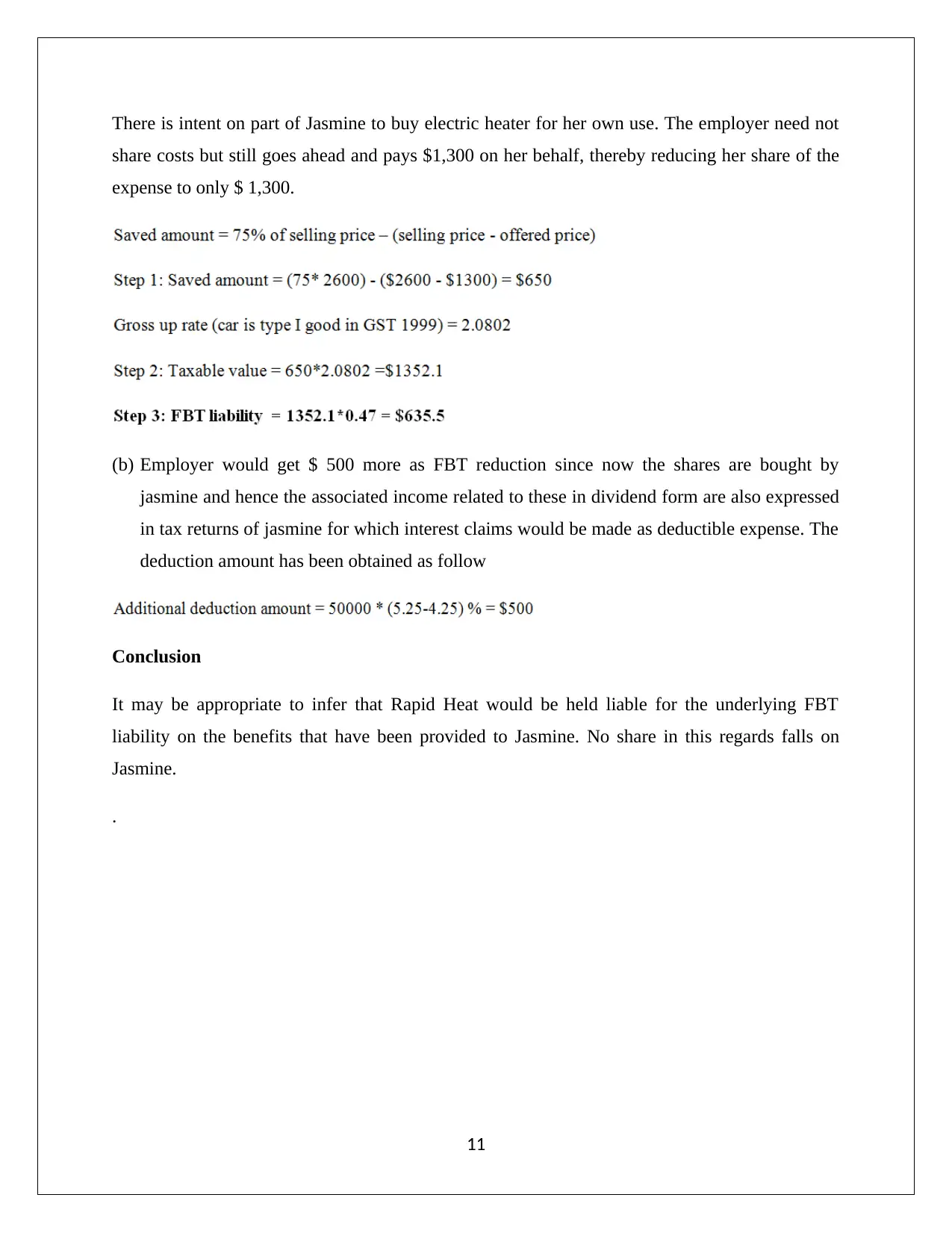

There is intent on part of Jasmine to buy electric heater for her own use. The employer need not

share costs but still goes ahead and pays $1,300 on her behalf, thereby reducing her share of the

expense to only $ 1,300.

(b) Employer would get $ 500 more as FBT reduction since now the shares are bought by

jasmine and hence the associated income related to these in dividend form are also expressed

in tax returns of jasmine for which interest claims would be made as deductible expense. The

deduction amount has been obtained as follow

Conclusion

It may be appropriate to infer that Rapid Heat would be held liable for the underlying FBT

liability on the benefits that have been provided to Jasmine. No share in this regards falls on

Jasmine.

.

11

share costs but still goes ahead and pays $1,300 on her behalf, thereby reducing her share of the

expense to only $ 1,300.

(b) Employer would get $ 500 more as FBT reduction since now the shares are bought by

jasmine and hence the associated income related to these in dividend form are also expressed

in tax returns of jasmine for which interest claims would be made as deductible expense. The

deduction amount has been obtained as follow

Conclusion

It may be appropriate to infer that Rapid Heat would be held liable for the underlying FBT

liability on the benefits that have been provided to Jasmine. No share in this regards falls on

Jasmine.

.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.