Comprehensive Management Accounting Report for Hichrom Ltd: Strategies

VerifiedAdded on 2021/01/02

|16

|5344

|342

Report

AI Summary

This report examines management accounting practices within Hichrom Ltd., a company specializing in chromatography products. It covers various management accounting systems, including cost accounting, price optimization, inventory management, and job costing, and evaluates their benefits. The report details different reporting methods like account receivable aging reports and performance reports. It analyzes costing techniques such as marginal and absorption costing, and discusses budgetary control and planning tools. The final sections address how management accounting systems respond to financial problems, with the aim of guiding Hichrom Ltd. towards sustainable success. The report integrates these elements to provide a comprehensive overview of management accounting's role in business strategy and financial management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems........................1

P2: Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1: Management accounting system and its reporting are integrated within organisational

process.........................................................................................................................................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate techniques............................................................5

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4: Budgetary control and advantages and disadvantages of planning tools used in budgetary

control ........................................................................................................................................8

M3: Uses and applications of planning tools for preparing and forecasting budgets ..............10

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems........................1

P2: Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1: Management accounting system and its reporting are integrated within organisational

process.........................................................................................................................................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate techniques............................................................5

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4: Budgetary control and advantages and disadvantages of planning tools used in budgetary

control ........................................................................................................................................8

M3: Uses and applications of planning tools for preparing and forecasting budgets ..............10

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting has evolved to assist the management in performing its

functions of providing accounting information to management and assisting in performing

management function like planning, organising, controlling and decision making. This is

principle used in preparing financial statements consists of profit & loss a/c, Balance sheet,

statement of owner's equity and funds flow statements etc. for identifying company's financial

position and evaluate it's assets, liabilities and owners equity at a given accounting period

(Ahmad and Mohamed Zabri, 2015.).

Hichrom Ltd. is a growing company which is world's leading in high and ultra high

performance chromatography columns and accessories manufacturing and distributing chain. In

this report organisation works on various management accounting systems, reporting methods

and evaluate their benefits on organisation performance. Management uses different costing

techniques for evaluating their financial statement. Hichrom Ltd. applies various planning tools

which are used for controlling budgets and helps in forecasting. Accounting manager adopt

various accounting systems to resolve company's financial issues so that manager can lead

Hichrom Ltd. to achieve success.

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting aggregation of two words 'management' and 'accounting' where

the term management means art of planning, organising, directing, controlling and decision

making and accounting refers to recording, classifying and summarizing of monetary

transactions. Therefore it is a systematic approach used as planning effectively, directing it's

operations and solving problems. Hichrom Ltd. products are used in forensics, frontiers of

science and medicines as analysis of new drugs content, pharmaceuticals batch testing and

identify contaminants in blood, water etc. Pharmaceuticals, food, plastic and oil industries and

agrochemical are the customers of Hichrom Ltd. Therefore it is important to prepare financial

statements in order to expand its business in global market. It can be complete by using various

management accounting systems in way to make effective plans and decision to achieve

company's goal (Budding, Grossi and Tagesson, 2014.).

Different management accounting systems are:

1

Management accounting has evolved to assist the management in performing its

functions of providing accounting information to management and assisting in performing

management function like planning, organising, controlling and decision making. This is

principle used in preparing financial statements consists of profit & loss a/c, Balance sheet,

statement of owner's equity and funds flow statements etc. for identifying company's financial

position and evaluate it's assets, liabilities and owners equity at a given accounting period

(Ahmad and Mohamed Zabri, 2015.).

Hichrom Ltd. is a growing company which is world's leading in high and ultra high

performance chromatography columns and accessories manufacturing and distributing chain. In

this report organisation works on various management accounting systems, reporting methods

and evaluate their benefits on organisation performance. Management uses different costing

techniques for evaluating their financial statement. Hichrom Ltd. applies various planning tools

which are used for controlling budgets and helps in forecasting. Accounting manager adopt

various accounting systems to resolve company's financial issues so that manager can lead

Hichrom Ltd. to achieve success.

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting aggregation of two words 'management' and 'accounting' where

the term management means art of planning, organising, directing, controlling and decision

making and accounting refers to recording, classifying and summarizing of monetary

transactions. Therefore it is a systematic approach used as planning effectively, directing it's

operations and solving problems. Hichrom Ltd. products are used in forensics, frontiers of

science and medicines as analysis of new drugs content, pharmaceuticals batch testing and

identify contaminants in blood, water etc. Pharmaceuticals, food, plastic and oil industries and

agrochemical are the customers of Hichrom Ltd. Therefore it is important to prepare financial

statements in order to expand its business in global market. It can be complete by using various

management accounting systems in way to make effective plans and decision to achieve

company's goal (Budding, Grossi and Tagesson, 2014.).

Different management accounting systems are:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting systems: This is the accounting system used by company to estimate

the production cost for execution of different organisational activities like production and

distribution activities. Hichrom Ltd. is supplying to many countries through various distribution

network thus it important for management to optimum utilization of it's resources in manner to

reducing the chances of wastage. It can be possible through using cost accounting system which

set a cost guidelines for company after analysing future uncertainties and their effectiveness.

This system is analysis on the basis of actual, standard and normal costing. Actual costing is used

in determination of actual commodity cost based on product cost like actual material, labour and

variable overheads. Standard costing is based on pre-estimated materials, labour and

manufacturing overhead costs. Normal costing is derived on the basis of actual direct costs and

standard overhead rate (Cheng, 2012.).

Price optimisation systems: It is another effective accounting system that helps

management in makes best pricing policies for identifying the representation of targeted market

and knowing their willingness to pay for the services and product offered by Hichrom Ltd. This

will effect in maximizing the customer's faithfulness and satisfaction level of targeted market.

Therefore increase in prices of product and services offered may leads to maximize the chances

of shifting faithful customers toward competitors which is not good for Hichrom Ltd. This

system is used as a tool which helps in improvement or recommends change in price that benefits

company to achieve desired target.

Job costing systems: It refers to such accounting system where manufacturing cost is

assigning to single product or group of products which helps management in preparing an

impressive budget. Hichrom Ltd. manager considering all activities performed in producing

product and it's cost allocation basis which bring profits in coming future. Process coasting i.e.

identifying product at individual level of manufacturing, standard costing i.e. an estimated cost

compare with actual used in performing company's operation, contract costing are the various job

costing systems . Hichrom Ltd. is using contract costing system for tracking their resources used

in production and marketing processes (Cleary, 2015).

Inventory management system: This system company approaches in direct

management of inventory to maintain sufficient inventory level and meet customer's needs and

requirements. Hichrom Ltd. is using this framework to manage their inventory on daily basis by

tracking inventory level, creating material bills, production output and their sales. Company also

2

the production cost for execution of different organisational activities like production and

distribution activities. Hichrom Ltd. is supplying to many countries through various distribution

network thus it important for management to optimum utilization of it's resources in manner to

reducing the chances of wastage. It can be possible through using cost accounting system which

set a cost guidelines for company after analysing future uncertainties and their effectiveness.

This system is analysis on the basis of actual, standard and normal costing. Actual costing is used

in determination of actual commodity cost based on product cost like actual material, labour and

variable overheads. Standard costing is based on pre-estimated materials, labour and

manufacturing overhead costs. Normal costing is derived on the basis of actual direct costs and

standard overhead rate (Cheng, 2012.).

Price optimisation systems: It is another effective accounting system that helps

management in makes best pricing policies for identifying the representation of targeted market

and knowing their willingness to pay for the services and product offered by Hichrom Ltd. This

will effect in maximizing the customer's faithfulness and satisfaction level of targeted market.

Therefore increase in prices of product and services offered may leads to maximize the chances

of shifting faithful customers toward competitors which is not good for Hichrom Ltd. This

system is used as a tool which helps in improvement or recommends change in price that benefits

company to achieve desired target.

Job costing systems: It refers to such accounting system where manufacturing cost is

assigning to single product or group of products which helps management in preparing an

impressive budget. Hichrom Ltd. manager considering all activities performed in producing

product and it's cost allocation basis which bring profits in coming future. Process coasting i.e.

identifying product at individual level of manufacturing, standard costing i.e. an estimated cost

compare with actual used in performing company's operation, contract costing are the various job

costing systems . Hichrom Ltd. is using contract costing system for tracking their resources used

in production and marketing processes (Cleary, 2015).

Inventory management system: This system company approaches in direct

management of inventory to maintain sufficient inventory level and meet customer's needs and

requirements. Hichrom Ltd. is using this framework to manage their inventory on daily basis by

tracking inventory level, creating material bills, production output and their sales. Company also

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

adopt this system to fight against the situation of increases in product demand in future through

getting accessibility of material in store. Company uses this system as to avoid excessive

inventory impact on revenue loss. FIFO i.e. valuation of inventory on the basis of goods first

purchased are sold first, LIFO i.e. goods purchases last are sold first for inventory valuation and

average inventory management system are the examples of this system.

P2: Different methods used for management accounting reporting

Management accounting reporting displays a complete picture which helps in analysing

the performance of company. Hichrom Ltd. is an expanding manufacturing and distributing

company and it's management always tried and true to expand their business with the help of

maintaining accounting reports on regular basis i.e. daily, monthly, quarterly, yearly. Such

reports includes income statements, Balance sheet etc. Management accounting reporting is used

to maintain several different types of reports like performance reports, inventory and

manufacturing report, account receivable aging report, job cost reports etc. which gives useful

information and company create effective plans and policies on the basis of that information

(Derchi, Burkert and Oyon, 2013).

Different management accounting reporting are:

Account receivable aging reports: This report is important for any organisation that

offers credit to customers and maintain strong financial position of the company because it

provides a summary of credit balances in form as lists of non-paying customers invoices sorted

by customer name with details of all bills, invoice number or date. Hichrom Ltd. is maintaining

this aging report as a recovery tool that carries a detail information related to average collection

period and to determine invoices which are overdue for payments. If it's collection period is less

than standard that means they should decreases their sales practices so that they don't aspect any

future credit risk. This report is also used as a technique for estimating bad debts that are used to

revise the percentage for bad debts a/c. This aging report is also known as a agenda of accounts

receivable.

Performance report: This report consist of current performance of company within

various departments. Accounting managers of individual departments should maintain all records

related to their functioning in this report so that they achieve pre-decided objectives. In the same

way Hichrom Ltd. is also maintaining their organisational performance report in individual

levels. They are also assigning roles and responsibilities to each level managers so that

3

getting accessibility of material in store. Company uses this system as to avoid excessive

inventory impact on revenue loss. FIFO i.e. valuation of inventory on the basis of goods first

purchased are sold first, LIFO i.e. goods purchases last are sold first for inventory valuation and

average inventory management system are the examples of this system.

P2: Different methods used for management accounting reporting

Management accounting reporting displays a complete picture which helps in analysing

the performance of company. Hichrom Ltd. is an expanding manufacturing and distributing

company and it's management always tried and true to expand their business with the help of

maintaining accounting reports on regular basis i.e. daily, monthly, quarterly, yearly. Such

reports includes income statements, Balance sheet etc. Management accounting reporting is used

to maintain several different types of reports like performance reports, inventory and

manufacturing report, account receivable aging report, job cost reports etc. which gives useful

information and company create effective plans and policies on the basis of that information

(Derchi, Burkert and Oyon, 2013).

Different management accounting reporting are:

Account receivable aging reports: This report is important for any organisation that

offers credit to customers and maintain strong financial position of the company because it

provides a summary of credit balances in form as lists of non-paying customers invoices sorted

by customer name with details of all bills, invoice number or date. Hichrom Ltd. is maintaining

this aging report as a recovery tool that carries a detail information related to average collection

period and to determine invoices which are overdue for payments. If it's collection period is less

than standard that means they should decreases their sales practices so that they don't aspect any

future credit risk. This report is also used as a technique for estimating bad debts that are used to

revise the percentage for bad debts a/c. This aging report is also known as a agenda of accounts

receivable.

Performance report: This report consist of current performance of company within

various departments. Accounting managers of individual departments should maintain all records

related to their functioning in this report so that they achieve pre-decided objectives. In the same

way Hichrom Ltd. is also maintaining their organisational performance report in individual

levels. They are also assigning roles and responsibilities to each level managers so that

3

company's overall performance maximizes and their performance also attract investors for

further investments. This report compares company's actual production with standard and takes

essential actions against adverse variations (Huber and Scheytt, 2013).

Inventory management reports: This report requires to maintain sufficient inventory

level with accurate valuation of inventory. EOQ (economic order quantity) and ABC analysis are

the examples of inventory management reporting. EOQ refers to the order quantity that reduces

the cost of ordering and holding and ABC analysis explained which inventory requires more

attention and which is not. Hichrom Ltd. is in manufacturing of UHPLC & HPLC columns and

accessories with less fault temperament and it finds inventory management reports very valuable

for inventory valuation.

Job cost reporting: This managerial accounting reports shows expenses for a particular

project related to present status of job which helps in evaluating job's profitability. It helps

management in analysing whether the invested amount spend on the product will be recovered

or not in coming future. When there are various jobs in department it is hard to manage so

creating job cost reports helps in identifying problems related to job cost. Hichrom Ltd. aim is

prepare this report for identifying the cost included in different job orders. This will create a

favourable impact on the company's profitability (Ji, 2017).

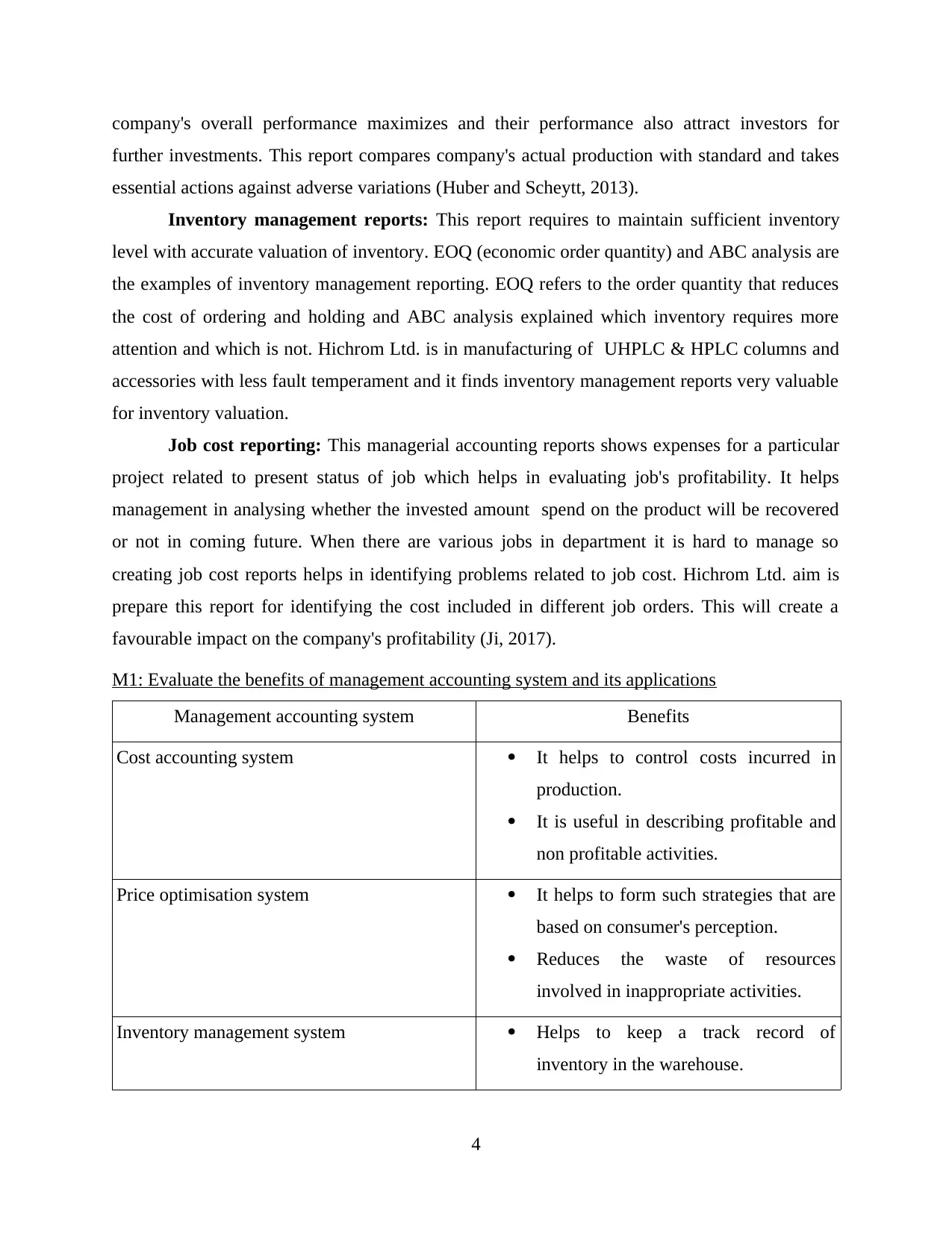

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It helps to control costs incurred in

production.

It is useful in describing profitable and

non profitable activities.

Price optimisation system It helps to form such strategies that are

based on consumer's perception.

Reduces the waste of resources

involved in inappropriate activities.

Inventory management system Helps to keep a track record of

inventory in the warehouse.

4

further investments. This report compares company's actual production with standard and takes

essential actions against adverse variations (Huber and Scheytt, 2013).

Inventory management reports: This report requires to maintain sufficient inventory

level with accurate valuation of inventory. EOQ (economic order quantity) and ABC analysis are

the examples of inventory management reporting. EOQ refers to the order quantity that reduces

the cost of ordering and holding and ABC analysis explained which inventory requires more

attention and which is not. Hichrom Ltd. is in manufacturing of UHPLC & HPLC columns and

accessories with less fault temperament and it finds inventory management reports very valuable

for inventory valuation.

Job cost reporting: This managerial accounting reports shows expenses for a particular

project related to present status of job which helps in evaluating job's profitability. It helps

management in analysing whether the invested amount spend on the product will be recovered

or not in coming future. When there are various jobs in department it is hard to manage so

creating job cost reports helps in identifying problems related to job cost. Hichrom Ltd. aim is

prepare this report for identifying the cost included in different job orders. This will create a

favourable impact on the company's profitability (Ji, 2017).

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It helps to control costs incurred in

production.

It is useful in describing profitable and

non profitable activities.

Price optimisation system It helps to form such strategies that are

based on consumer's perception.

Reduces the waste of resources

involved in inappropriate activities.

Inventory management system Helps to keep a track record of

inventory in the warehouse.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase productivity, profitability and

efficiency of work.

Job costing system Help to evaluate the performance of

each employee.

Provide detailed report of each job and

separately divide profits of each job.

D1: Management accounting system and its reporting are integrated within organisational

process

Management accounting system and its reporting are used to plan, control and regulate

activities within Hichrom Ltd. Different type of management accounting reports are used to

evaluate performance of employees and to analyse each job according to the strategy. These are

helpful for the organisation to deal with risks and uncertainty in future. This system is currently

used by organisation control cost so that it can retain old new customers and target new

customers. It is also implemented to keep a record of inventory to increase productivity of

organisation (Leitner, 2013).

TASK 2

P3: Calculation of cost using an appropriate techniques

Cost - It refers to amount of money individual paid in order to achieve something. It can

be classified into monetary valuation of material, labour efforts, time consumed, risk incurred,

opportunities give up in production and distribution of stock or services. Management uses

costing methods in determination of cost of production, cost of goods sold and net operating

income with the helps two costing method.

Hichrom Ltd. is a manufacturer and distributor of chromatography accessories thus for

determining optimum profits company uses both marginal and absorption costing method for

evaluation of net profit. This helps management in decision making regarding minimization of

cost in order to achieve profits (M Ancini, Vaassen and D Ameri, 2013). Types of costs are

described below:

Marginal costing: It is a special technique of presenting cost information that may assist

in profit planning, cost control and managerial decision making. Due to involvement of costs like

material and labour with budgeted fixed cost it is also known as variable cost. This cost is arises

5

efficiency of work.

Job costing system Help to evaluate the performance of

each employee.

Provide detailed report of each job and

separately divide profits of each job.

D1: Management accounting system and its reporting are integrated within organisational

process

Management accounting system and its reporting are used to plan, control and regulate

activities within Hichrom Ltd. Different type of management accounting reports are used to

evaluate performance of employees and to analyse each job according to the strategy. These are

helpful for the organisation to deal with risks and uncertainty in future. This system is currently

used by organisation control cost so that it can retain old new customers and target new

customers. It is also implemented to keep a record of inventory to increase productivity of

organisation (Leitner, 2013).

TASK 2

P3: Calculation of cost using an appropriate techniques

Cost - It refers to amount of money individual paid in order to achieve something. It can

be classified into monetary valuation of material, labour efforts, time consumed, risk incurred,

opportunities give up in production and distribution of stock or services. Management uses

costing methods in determination of cost of production, cost of goods sold and net operating

income with the helps two costing method.

Hichrom Ltd. is a manufacturer and distributor of chromatography accessories thus for

determining optimum profits company uses both marginal and absorption costing method for

evaluation of net profit. This helps management in decision making regarding minimization of

cost in order to achieve profits (M Ancini, Vaassen and D Ameri, 2013). Types of costs are

described below:

Marginal costing: It is a special technique of presenting cost information that may assist

in profit planning, cost control and managerial decision making. Due to involvement of costs like

material and labour with budgeted fixed cost it is also known as variable cost. This cost is arises

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to produce additional unit of output rather than budgeted output. Many companies adopting this

costing technique for increasing in net operating profit as compare to profit arises from

absorption costing method (Nicolaou, 2011).

Absorption costing: It is a method considering all types of costs like fixed and variable

cost that affects net profit. Direct cost like wages, raw material in process and overhead costs. In

this method net profitability of company is affected with change in fixed cost that means in fixed

cost increases profit decreases. That's why most companies doesn't preferred this method for

calculation of company's net income.

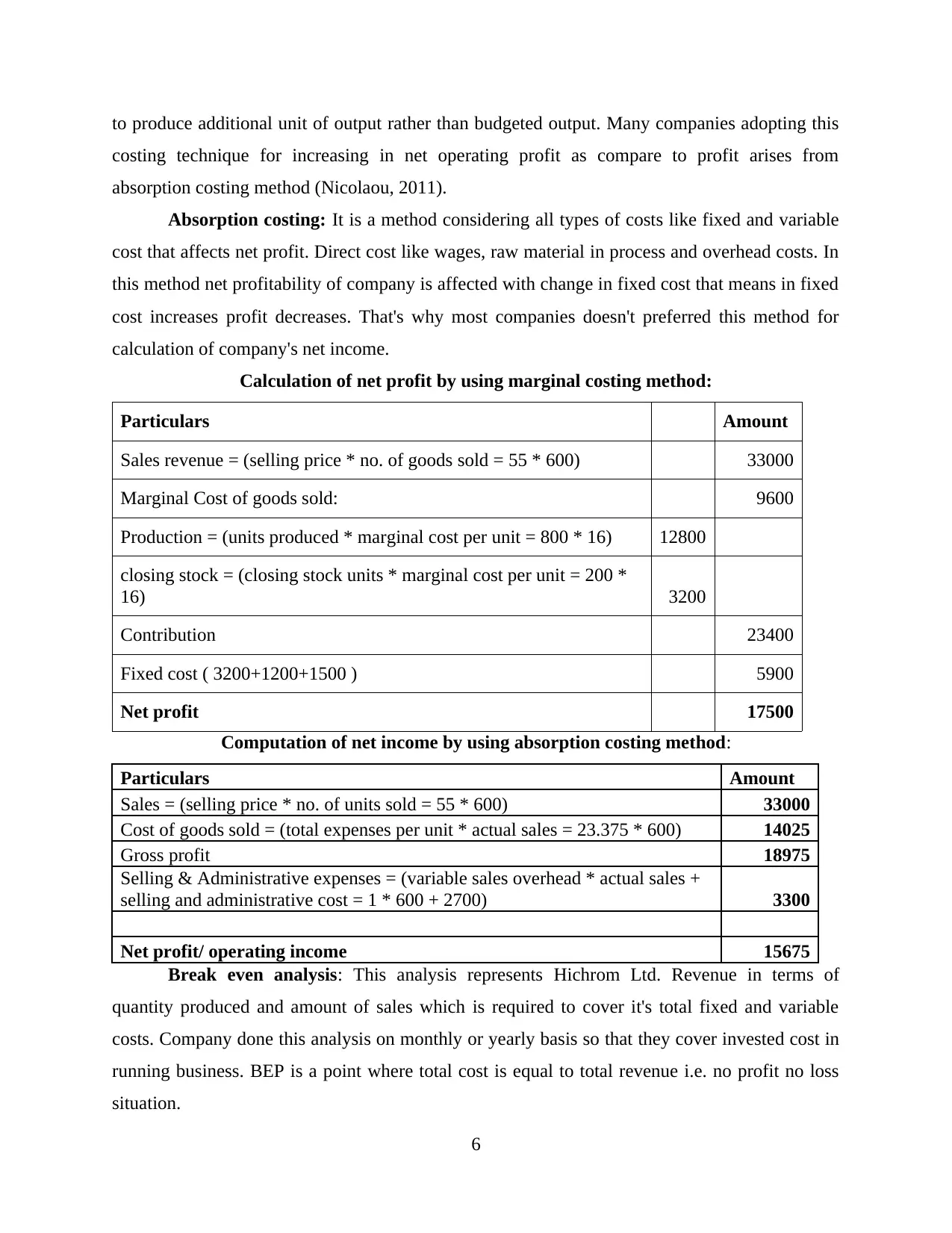

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: This analysis represents Hichrom Ltd. Revenue in terms of

quantity produced and amount of sales which is required to cover it's total fixed and variable

costs. Company done this analysis on monthly or yearly basis so that they cover invested cost in

running business. BEP is a point where total cost is equal to total revenue i.e. no profit no loss

situation.

6

costing technique for increasing in net operating profit as compare to profit arises from

absorption costing method (Nicolaou, 2011).

Absorption costing: It is a method considering all types of costs like fixed and variable

cost that affects net profit. Direct cost like wages, raw material in process and overhead costs. In

this method net profitability of company is affected with change in fixed cost that means in fixed

cost increases profit decreases. That's why most companies doesn't preferred this method for

calculation of company's net income.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: This analysis represents Hichrom Ltd. Revenue in terms of

quantity produced and amount of sales which is required to cover it's total fixed and variable

costs. Company done this analysis on monthly or yearly basis so that they cover invested cost in

running business. BEP is a point where total cost is equal to total revenue i.e. no profit no loss

situation.

6

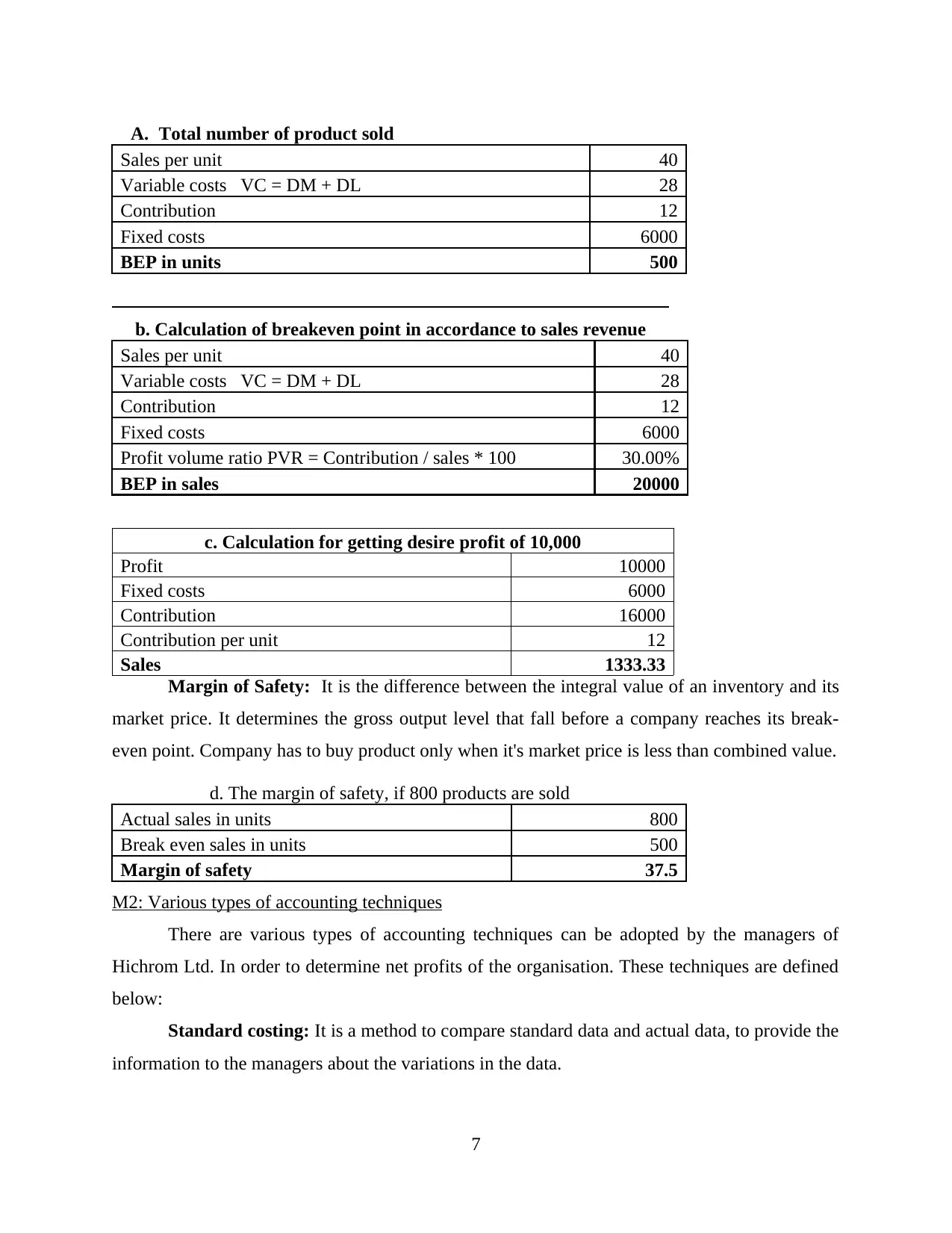

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is the difference between the integral value of an inventory and its

market price. It determines the gross output level that fall before a company reaches its break-

even point. Company has to buy product only when it's market price is less than combined value.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques

There are various types of accounting techniques can be adopted by the managers of

Hichrom Ltd. In order to determine net profits of the organisation. These techniques are defined

below:

Standard costing: It is a method to compare standard data and actual data, to provide the

information to the managers about the variations in the data.

7

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is the difference between the integral value of an inventory and its

market price. It determines the gross output level that fall before a company reaches its break-

even point. Company has to buy product only when it's market price is less than combined value.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques

There are various types of accounting techniques can be adopted by the managers of

Hichrom Ltd. In order to determine net profits of the organisation. These techniques are defined

below:

Standard costing: It is a method to compare standard data and actual data, to provide the

information to the managers about the variations in the data.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing: It is the additional cost of such units which are newly added to the

production. It involves direct material, direct labour, direct expenses and variable overheads.

Historical costing: It is the actual cost of the asset of good at the time of transaction. It

helps to differentiate the actual cost and the replacement cost.

D2: Data interpretation

As per the preceding computation, it has been cleared that marginal costing method will

be more profitable to Hichrom Ltd. in comparison of absorption costing method. It is because of

increment in earnings while using marginal costing method. While computing net profits for

Hichrom Ltd., the marginal costing method calculates £17500 as gain whereas absorption costing

method calculates £15675 as gain, and the difference of £9600 in gain occurs due to change in

variable cost. In Break even, the total number of units sold are 500 and break even sales is

20000. To earn minimum profit of £10000, Hichrom Ltd. have to sale 1333.33 units. Margin of

safety is 37.5 when 800 production units are sold.

TASK 3

P4: Budgetary control and advantages and disadvantages of planning tools used in budgetary

control

Budgetary control - It is the procedure to control costs which considers the formulation

of budgets. It helps to find out different budgeted figures for Hichrom Ltd. for the future period

and then compare forecasted figures with actual figures, and also helps to control over the

organisation. Budgetary control is also used to set goals for managers of Hichrom Ltd. that are

based on the budget, and also frame reward policy when goals are achieved. It is a preparation

method which is used by organisation to pre plan all expenses that are going to happen in future

to reduce waste of monetary factors in and outside of the organisation.

The process of budgetary control includes various steps like, preparation of organisation

charts, setting budget centre, prepare budget manual, form budget committee, set budget period

to achieve goals. It is used by Hichrom Ltd. to forecast future consequences that can probably

happen. There are various planning tools to use in budgetary control those are forecasting tools,

contingency tools and scenario tools. These are explained below:

Forecasting tools: It is used by Hichrom Ltd. to manage future of the business. It is the

tool that is helpful in making predictions of future condition of business, based on past and

8

production. It involves direct material, direct labour, direct expenses and variable overheads.

Historical costing: It is the actual cost of the asset of good at the time of transaction. It

helps to differentiate the actual cost and the replacement cost.

D2: Data interpretation

As per the preceding computation, it has been cleared that marginal costing method will

be more profitable to Hichrom Ltd. in comparison of absorption costing method. It is because of

increment in earnings while using marginal costing method. While computing net profits for

Hichrom Ltd., the marginal costing method calculates £17500 as gain whereas absorption costing

method calculates £15675 as gain, and the difference of £9600 in gain occurs due to change in

variable cost. In Break even, the total number of units sold are 500 and break even sales is

20000. To earn minimum profit of £10000, Hichrom Ltd. have to sale 1333.33 units. Margin of

safety is 37.5 when 800 production units are sold.

TASK 3

P4: Budgetary control and advantages and disadvantages of planning tools used in budgetary

control

Budgetary control - It is the procedure to control costs which considers the formulation

of budgets. It helps to find out different budgeted figures for Hichrom Ltd. for the future period

and then compare forecasted figures with actual figures, and also helps to control over the

organisation. Budgetary control is also used to set goals for managers of Hichrom Ltd. that are

based on the budget, and also frame reward policy when goals are achieved. It is a preparation

method which is used by organisation to pre plan all expenses that are going to happen in future

to reduce waste of monetary factors in and outside of the organisation.

The process of budgetary control includes various steps like, preparation of organisation

charts, setting budget centre, prepare budget manual, form budget committee, set budget period

to achieve goals. It is used by Hichrom Ltd. to forecast future consequences that can probably

happen. There are various planning tools to use in budgetary control those are forecasting tools,

contingency tools and scenario tools. These are explained below:

Forecasting tools: It is used by Hichrom Ltd. to manage future of the business. It is the

tool that is helpful in making predictions of future condition of business, based on past and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

current data of organisation. It helps organisation to determine what resources might be

mandatory to meet the risk or uncertainty that can happen in future. It is also used to determine

customer demand in the future for its products (Nørreklit, 2014).

Advantages Disadvantages

It provides valuable information for the

business that is helpful for managers in

decision making.

The main source of data derives from

the experience of qualified managers

and employees.

It is tot possible to forecast accurately

and no one can perfectly sure about the

future.

Making a decision on the wrongly

forecasted report can harm the

company.

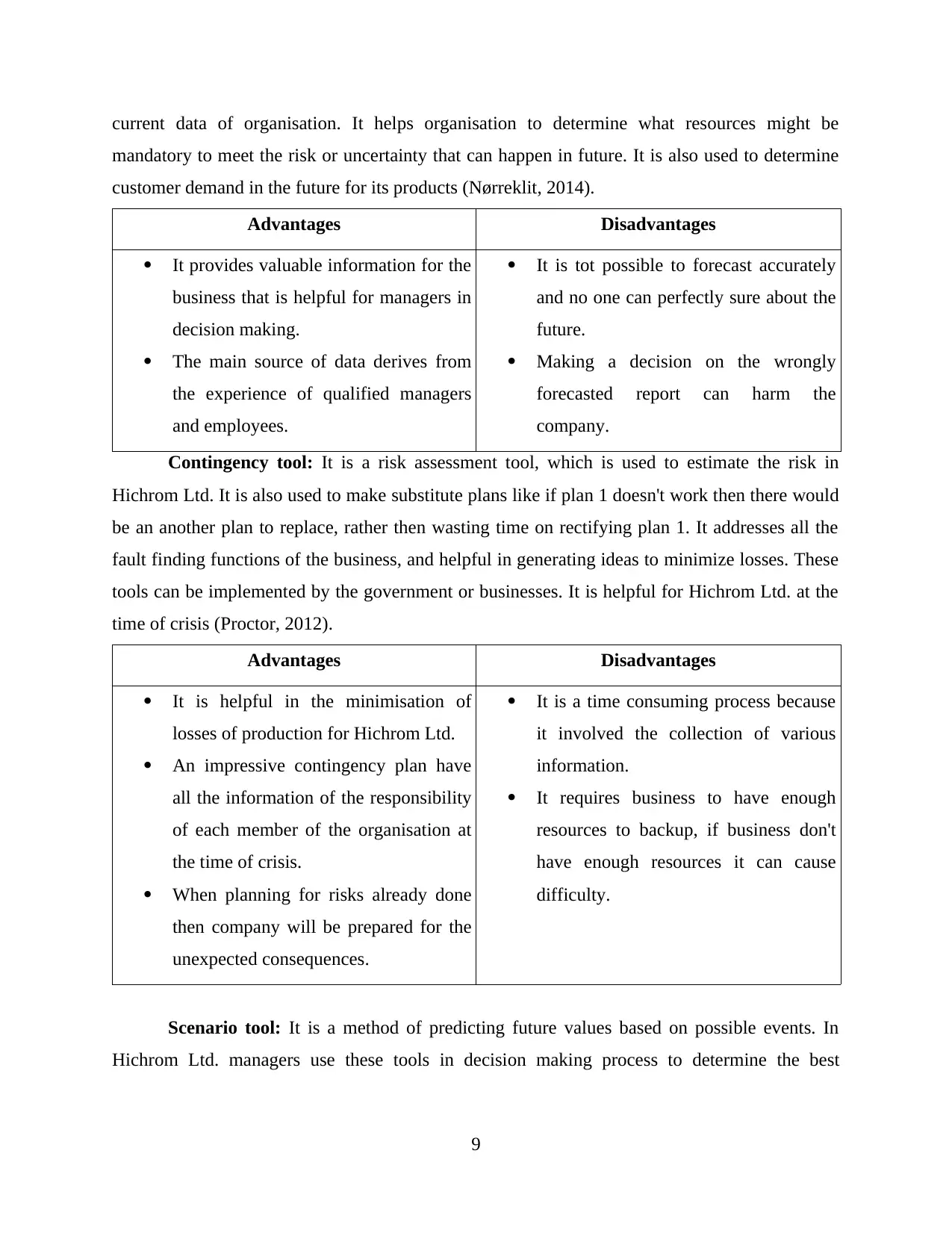

Contingency tool: It is a risk assessment tool, which is used to estimate the risk in

Hichrom Ltd. It is also used to make substitute plans like if plan 1 doesn't work then there would

be an another plan to replace, rather then wasting time on rectifying plan 1. It addresses all the

fault finding functions of the business, and helpful in generating ideas to minimize losses. These

tools can be implemented by the government or businesses. It is helpful for Hichrom Ltd. at the

time of crisis (Proctor, 2012).

Advantages Disadvantages

It is helpful in the minimisation of

losses of production for Hichrom Ltd.

An impressive contingency plan have

all the information of the responsibility

of each member of the organisation at

the time of crisis.

When planning for risks already done

then company will be prepared for the

unexpected consequences.

It is a time consuming process because

it involved the collection of various

information.

It requires business to have enough

resources to backup, if business don't

have enough resources it can cause

difficulty.

Scenario tool: It is a method of predicting future values based on possible events. In

Hichrom Ltd. managers use these tools in decision making process to determine the best

9

mandatory to meet the risk or uncertainty that can happen in future. It is also used to determine

customer demand in the future for its products (Nørreklit, 2014).

Advantages Disadvantages

It provides valuable information for the

business that is helpful for managers in

decision making.

The main source of data derives from

the experience of qualified managers

and employees.

It is tot possible to forecast accurately

and no one can perfectly sure about the

future.

Making a decision on the wrongly

forecasted report can harm the

company.

Contingency tool: It is a risk assessment tool, which is used to estimate the risk in

Hichrom Ltd. It is also used to make substitute plans like if plan 1 doesn't work then there would

be an another plan to replace, rather then wasting time on rectifying plan 1. It addresses all the

fault finding functions of the business, and helpful in generating ideas to minimize losses. These

tools can be implemented by the government or businesses. It is helpful for Hichrom Ltd. at the

time of crisis (Proctor, 2012).

Advantages Disadvantages

It is helpful in the minimisation of

losses of production for Hichrom Ltd.

An impressive contingency plan have

all the information of the responsibility

of each member of the organisation at

the time of crisis.

When planning for risks already done

then company will be prepared for the

unexpected consequences.

It is a time consuming process because

it involved the collection of various

information.

It requires business to have enough

resources to backup, if business don't

have enough resources it can cause

difficulty.

Scenario tool: It is a method of predicting future values based on possible events. In

Hichrom Ltd. managers use these tools in decision making process to determine the best

9

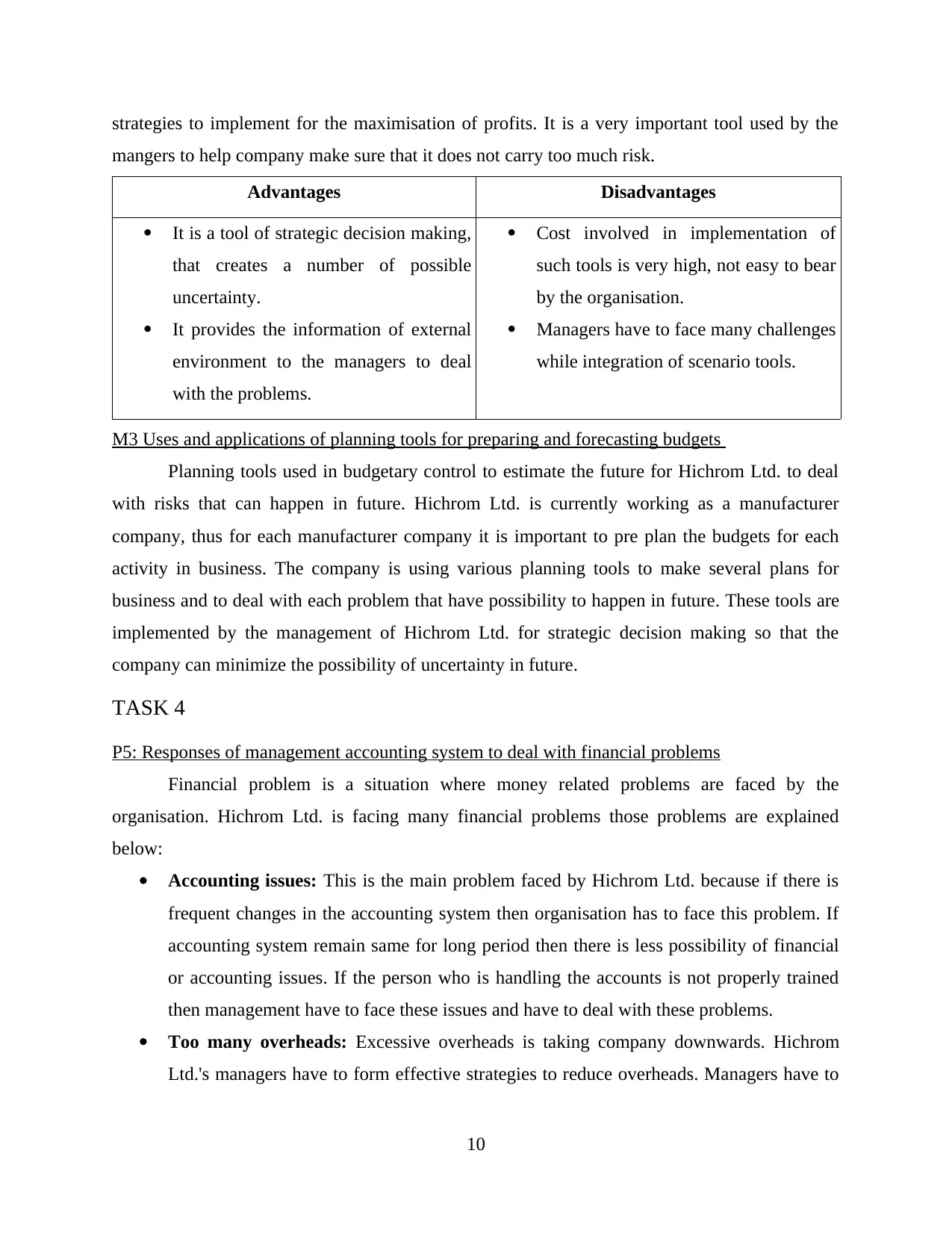

strategies to implement for the maximisation of profits. It is a very important tool used by the

mangers to help company make sure that it does not carry too much risk.

Advantages Disadvantages

It is a tool of strategic decision making,

that creates a number of possible

uncertainty.

It provides the information of external

environment to the managers to deal

with the problems.

Cost involved in implementation of

such tools is very high, not easy to bear

by the organisation.

Managers have to face many challenges

while integration of scenario tools.

M3 Uses and applications of planning tools for preparing and forecasting budgets

Planning tools used in budgetary control to estimate the future for Hichrom Ltd. to deal

with risks that can happen in future. Hichrom Ltd. is currently working as a manufacturer

company, thus for each manufacturer company it is important to pre plan the budgets for each

activity in business. The company is using various planning tools to make several plans for

business and to deal with each problem that have possibility to happen in future. These tools are

implemented by the management of Hichrom Ltd. for strategic decision making so that the

company can minimize the possibility of uncertainty in future.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problem is a situation where money related problems are faced by the

organisation. Hichrom Ltd. is facing many financial problems those problems are explained

below:

Accounting issues: This is the main problem faced by Hichrom Ltd. because if there is

frequent changes in the accounting system then organisation has to face this problem. If

accounting system remain same for long period then there is less possibility of financial

or accounting issues. If the person who is handling the accounts is not properly trained

then management have to face these issues and have to deal with these problems.

Too many overheads: Excessive overheads is taking company downwards. Hichrom

Ltd.'s managers have to form effective strategies to reduce overheads. Managers have to

10

mangers to help company make sure that it does not carry too much risk.

Advantages Disadvantages

It is a tool of strategic decision making,

that creates a number of possible

uncertainty.

It provides the information of external

environment to the managers to deal

with the problems.

Cost involved in implementation of

such tools is very high, not easy to bear

by the organisation.

Managers have to face many challenges

while integration of scenario tools.

M3 Uses and applications of planning tools for preparing and forecasting budgets

Planning tools used in budgetary control to estimate the future for Hichrom Ltd. to deal

with risks that can happen in future. Hichrom Ltd. is currently working as a manufacturer

company, thus for each manufacturer company it is important to pre plan the budgets for each

activity in business. The company is using various planning tools to make several plans for

business and to deal with each problem that have possibility to happen in future. These tools are

implemented by the management of Hichrom Ltd. for strategic decision making so that the

company can minimize the possibility of uncertainty in future.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problem is a situation where money related problems are faced by the

organisation. Hichrom Ltd. is facing many financial problems those problems are explained

below:

Accounting issues: This is the main problem faced by Hichrom Ltd. because if there is

frequent changes in the accounting system then organisation has to face this problem. If

accounting system remain same for long period then there is less possibility of financial

or accounting issues. If the person who is handling the accounts is not properly trained

then management have to face these issues and have to deal with these problems.

Too many overheads: Excessive overheads is taking company downwards. Hichrom

Ltd.'s managers have to form effective strategies to reduce overheads. Managers have to

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.