Financial Management: Analysis of Hillside Company's Finances

VerifiedAdded on 2022/08/17

|11

|2440

|13

Report

AI Summary

This report presents a financial analysis of Hillside Company, a publicly traded firm considering expansion through investment in a new plant. It delves into working capital management, capital budgeting, and capital structure. The analysis includes calculations for cash conversion cycles, break-even points, and the application of Net Present Value (NPV) and Internal Rate of Return (IRR) to evaluate project profitability. It also explores financing options, comparing the costs of equity and debt, and provides recommendations for the board of management regarding the proposed project, suggesting acceptance of the investment plan with equity financing to optimize financial risk and increase firm value. The report emphasizes the importance of financial planning and its impact on the firm's future.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Working Capital Requirements...................................................................................................2

Cash and Break-Even Point.........................................................................................................3

Capital Budgeting........................................................................................................................4

Financing.....................................................................................................................................6

Recommendations............................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Working Capital Requirements...................................................................................................2

Cash and Break-Even Point.........................................................................................................3

Capital Budgeting........................................................................................................................4

Financing.....................................................................................................................................6

Recommendations............................................................................................................................8

References........................................................................................................................................9

2FINANCIAL MANAGEMENT

Introduction

The financial analysis has been done for Hillside Company that operates as a public

traded company which is well considering expanding its business operations with the help of

investment in a new plant. There were various techniques and concepts that were introduced in

particular which were related to Working Capital Management, Capital Budgeting and Capital

Structure of a Firm. The business and operational analysis has been specifically considered for

the firm for the purpose of well forecasting the future projections and operational analysis of the

firm for the future period of time period (Levin and Hallgren 2017). In particular, it is important

to note that Net Present Value and Internal Rate of Return were used to evaluate the overall

profitability of the project. While the various financing sources that a firm can in turn use for the

purpose of well financing the project were discussed. Finally the recommendation was given to

the Board of Management considering the project that has been proposed by the firm.

Discussion and Analysis

Working Capital Requirements

The working capital requirement that the firm would be requiring in turn would be

dependent on the amount that is available for the firm for the purpose of investment in the

operations of the firm and that is probably in the form of working capital. The management of

the firm in specific has proposed to increase the payment period of the firm by increasing the

average collection period from 15 days to around 30 days (Su et al., 2018). The same would be

resulting in the decrease in the collection period thereby increasing the cash conversion cycle of

the firm. In order to well analyze the changes that would be observed in the cash conversion

Introduction

The financial analysis has been done for Hillside Company that operates as a public

traded company which is well considering expanding its business operations with the help of

investment in a new plant. There were various techniques and concepts that were introduced in

particular which were related to Working Capital Management, Capital Budgeting and Capital

Structure of a Firm. The business and operational analysis has been specifically considered for

the firm for the purpose of well forecasting the future projections and operational analysis of the

firm for the future period of time period (Levin and Hallgren 2017). In particular, it is important

to note that Net Present Value and Internal Rate of Return were used to evaluate the overall

profitability of the project. While the various financing sources that a firm can in turn use for the

purpose of well financing the project were discussed. Finally the recommendation was given to

the Board of Management considering the project that has been proposed by the firm.

Discussion and Analysis

Working Capital Requirements

The working capital requirement that the firm would be requiring in turn would be

dependent on the amount that is available for the firm for the purpose of investment in the

operations of the firm and that is probably in the form of working capital. The management of

the firm in specific has proposed to increase the payment period of the firm by increasing the

average collection period from 15 days to around 30 days (Su et al., 2018). The same would be

resulting in the decrease in the collection period thereby increasing the cash conversion cycle of

the firm. In order to well analyze the changes that would be observed in the cash conversion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

cycle of the firm has been analyzed before the initiation of the project which has been well

calculated with the help of the following formula:

Cash Conversion Cycle: Days in Inventory + Days Sales Outstanding – Days Payable

Outstanding

The cash conversion cycle for the firm initially was around 18 days which has been well

calculated as follows:

Old Cash Conversion Cycle: 15+15-12: 18 Days

New Cash Conversion Cycle: 30+15-12: 33 Days.

So, it could be well analyzed that if the firm change their receivable period from 15 days to 30

days then then the cash conversion cycle of the firm would be increasing which well says that the

firm can face liquidity issues in terms of lower working capital that in turn can influence the

daily operations of the firm and the ability of the firm i0n well paying off the current obligations

of the firm. The same could also financially affect the firm in the form of higher cost of

borrowing as the firm have to do the same for the purpose of paying off its current liabilities of

the firm.

Cash and Break-Even Point

The cash and break-even point for the firm has been well calculated with the help of the

given formula:

Breakeven Point: Fixed Cost/(Sale Price -Cost of Raw Material)

The breakeven point for the firm has been well calculated from the given set of data that was

provided whereby the management of the firm are well undertaking for expanding their current

cycle of the firm has been analyzed before the initiation of the project which has been well

calculated with the help of the following formula:

Cash Conversion Cycle: Days in Inventory + Days Sales Outstanding – Days Payable

Outstanding

The cash conversion cycle for the firm initially was around 18 days which has been well

calculated as follows:

Old Cash Conversion Cycle: 15+15-12: 18 Days

New Cash Conversion Cycle: 30+15-12: 33 Days.

So, it could be well analyzed that if the firm change their receivable period from 15 days to 30

days then then the cash conversion cycle of the firm would be increasing which well says that the

firm can face liquidity issues in terms of lower working capital that in turn can influence the

daily operations of the firm and the ability of the firm i0n well paying off the current obligations

of the firm. The same could also financially affect the firm in the form of higher cost of

borrowing as the firm have to do the same for the purpose of paying off its current liabilities of

the firm.

Cash and Break-Even Point

The cash and break-even point for the firm has been well calculated with the help of the

given formula:

Breakeven Point: Fixed Cost/(Sale Price -Cost of Raw Material)

The breakeven point for the firm has been well calculated from the given set of data that was

provided whereby the management of the firm are well undertaking for expanding their current

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

operations by investing into new plants which in turn would be increasing the cash flows of the

firm (Siziba and Hall 2019). The marketing team of the firm would be undertaking an aggressive

marketing campaign in which they believe that the same would be allowing them to increase the

sales revenue of the firm around 5,000 products on an annual basis. The same would be done if

the firm is well willing to spend around $40,000 as an marketing expenses, however it is

important to note the amount of units that needs to be well sold for well covering the fixed cost

of the firm which is well shown below. It is estimated that around 571.43 units needs to be well

sold for well covering the fixed cost of the firm and the same can be easily done as the increase

in the units sold will be around 5,000 units, so the management of the firm must go ahead with

the launching of marketing campaign.

Capital Budgeting

In order to well evaluate the project, the net present value approach has been specifically

applied for the purpose of valuation of the project considered. All the considerable amount of

cash flows that would be flowing to the firm has been specifically considered for analysis

purpose (Al-Mutairi, Naser and Saeid 2018). The discounting rate that has been specifically

considered for analysis purpose is the Cost of Capital which well undertakes both the cost of

equity that has been evaluated with the help of models like Capital Asset Pricing Model and the

key set of formula that is applied is as follows:

Required Return: Risk Free Rate (Rf) + Beta*(Return on Market- Risk Free Rate).

The cost of equity for the firm was calculated to be 11.00% and the same well shows that the

equity shareholders are requiring around 11% on any capital that they would be investing based

on the risk and return that is associated for investment purpose.

operations by investing into new plants which in turn would be increasing the cash flows of the

firm (Siziba and Hall 2019). The marketing team of the firm would be undertaking an aggressive

marketing campaign in which they believe that the same would be allowing them to increase the

sales revenue of the firm around 5,000 products on an annual basis. The same would be done if

the firm is well willing to spend around $40,000 as an marketing expenses, however it is

important to note the amount of units that needs to be well sold for well covering the fixed cost

of the firm which is well shown below. It is estimated that around 571.43 units needs to be well

sold for well covering the fixed cost of the firm and the same can be easily done as the increase

in the units sold will be around 5,000 units, so the management of the firm must go ahead with

the launching of marketing campaign.

Capital Budgeting

In order to well evaluate the project, the net present value approach has been specifically

applied for the purpose of valuation of the project considered. All the considerable amount of

cash flows that would be flowing to the firm has been specifically considered for analysis

purpose (Al-Mutairi, Naser and Saeid 2018). The discounting rate that has been specifically

considered for analysis purpose is the Cost of Capital which well undertakes both the cost of

equity that has been evaluated with the help of models like Capital Asset Pricing Model and the

key set of formula that is applied is as follows:

Required Return: Risk Free Rate (Rf) + Beta*(Return on Market- Risk Free Rate).

The cost of equity for the firm was calculated to be 11.00% and the same well shows that the

equity shareholders are requiring around 11% on any capital that they would be investing based

on the risk and return that is associated for investment purpose.

5FINANCIAL MANAGEMENT

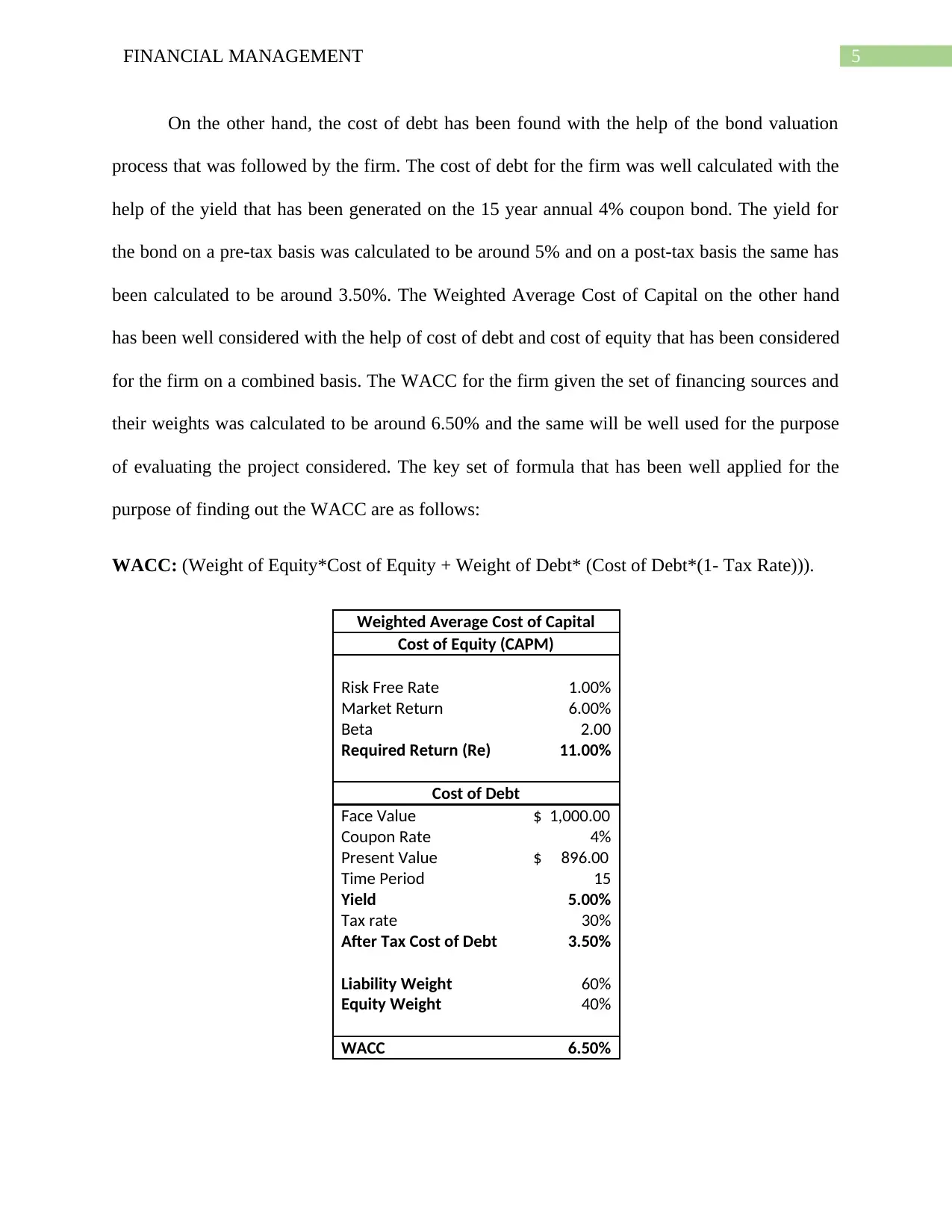

On the other hand, the cost of debt has been found with the help of the bond valuation

process that was followed by the firm. The cost of debt for the firm was well calculated with the

help of the yield that has been generated on the 15 year annual 4% coupon bond. The yield for

the bond on a pre-tax basis was calculated to be around 5% and on a post-tax basis the same has

been calculated to be around 3.50%. The Weighted Average Cost of Capital on the other hand

has been well considered with the help of cost of debt and cost of equity that has been considered

for the firm on a combined basis. The WACC for the firm given the set of financing sources and

their weights was calculated to be around 6.50% and the same will be well used for the purpose

of evaluating the project considered. The key set of formula that has been well applied for the

purpose of finding out the WACC are as follows:

WACC: (Weight of Equity*Cost of Equity + Weight of Debt* (Cost of Debt*(1- Tax Rate))).

Weighted Average Cost of Capital

Cost of Equity (CAPM)

Risk Free Rate 1.00%

Market Return 6.00%

Beta 2.00

Required Return (Re) 11.00%

Cost of Debt

Face Value $ 1,000.00

Coupon Rate 4%

Present Value $ 896.00

Time Period 15

Yield 5.00%

Tax rate 30%

After Tax Cost of Debt 3.50%

Liability Weight 60%

Equity Weight 40%

WACC 6.50%

On the other hand, the cost of debt has been found with the help of the bond valuation

process that was followed by the firm. The cost of debt for the firm was well calculated with the

help of the yield that has been generated on the 15 year annual 4% coupon bond. The yield for

the bond on a pre-tax basis was calculated to be around 5% and on a post-tax basis the same has

been calculated to be around 3.50%. The Weighted Average Cost of Capital on the other hand

has been well considered with the help of cost of debt and cost of equity that has been considered

for the firm on a combined basis. The WACC for the firm given the set of financing sources and

their weights was calculated to be around 6.50% and the same will be well used for the purpose

of evaluating the project considered. The key set of formula that has been well applied for the

purpose of finding out the WACC are as follows:

WACC: (Weight of Equity*Cost of Equity + Weight of Debt* (Cost of Debt*(1- Tax Rate))).

Weighted Average Cost of Capital

Cost of Equity (CAPM)

Risk Free Rate 1.00%

Market Return 6.00%

Beta 2.00

Required Return (Re) 11.00%

Cost of Debt

Face Value $ 1,000.00

Coupon Rate 4%

Present Value $ 896.00

Time Period 15

Yield 5.00%

Tax rate 30%

After Tax Cost of Debt 3.50%

Liability Weight 60%

Equity Weight 40%

WACC 6.50%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

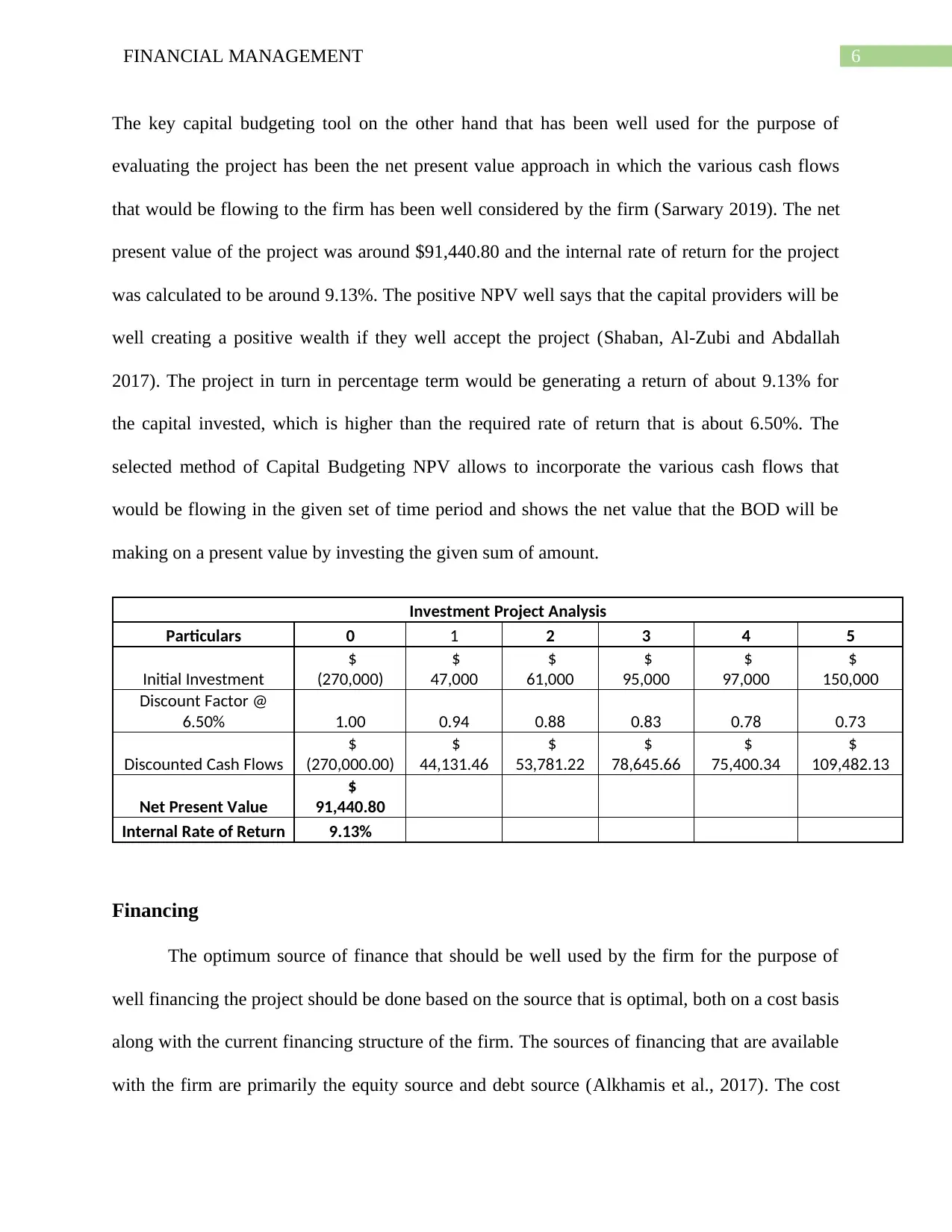

The key capital budgeting tool on the other hand that has been well used for the purpose of

evaluating the project has been the net present value approach in which the various cash flows

that would be flowing to the firm has been well considered by the firm (Sarwary 2019). The net

present value of the project was around $91,440.80 and the internal rate of return for the project

was calculated to be around 9.13%. The positive NPV well says that the capital providers will be

well creating a positive wealth if they well accept the project (Shaban, Al-Zubi and Abdallah

2017). The project in turn in percentage term would be generating a return of about 9.13% for

the capital invested, which is higher than the required rate of return that is about 6.50%. The

selected method of Capital Budgeting NPV allows to incorporate the various cash flows that

would be flowing in the given set of time period and shows the net value that the BOD will be

making on a present value by investing the given sum of amount.

Investment Project Analysis

Particulars 0 1 2 3 4 5

Initial Investment

$

(270,000)

$

47,000

$

61,000

$

95,000

$

97,000

$

150,000

Discount Factor @

6.50% 1.00 0.94 0.88 0.83 0.78 0.73

Discounted Cash Flows

$

(270,000.00)

$

44,131.46

$

53,781.22

$

78,645.66

$

75,400.34

$

109,482.13

Net Present Value

$

91,440.80

Internal Rate of Return 9.13%

Financing

The optimum source of finance that should be well used by the firm for the purpose of

well financing the project should be done based on the source that is optimal, both on a cost basis

along with the current financing structure of the firm. The sources of financing that are available

with the firm are primarily the equity source and debt source (Alkhamis et al., 2017). The cost

The key capital budgeting tool on the other hand that has been well used for the purpose of

evaluating the project has been the net present value approach in which the various cash flows

that would be flowing to the firm has been well considered by the firm (Sarwary 2019). The net

present value of the project was around $91,440.80 and the internal rate of return for the project

was calculated to be around 9.13%. The positive NPV well says that the capital providers will be

well creating a positive wealth if they well accept the project (Shaban, Al-Zubi and Abdallah

2017). The project in turn in percentage term would be generating a return of about 9.13% for

the capital invested, which is higher than the required rate of return that is about 6.50%. The

selected method of Capital Budgeting NPV allows to incorporate the various cash flows that

would be flowing in the given set of time period and shows the net value that the BOD will be

making on a present value by investing the given sum of amount.

Investment Project Analysis

Particulars 0 1 2 3 4 5

Initial Investment

$

(270,000)

$

47,000

$

61,000

$

95,000

$

97,000

$

150,000

Discount Factor @

6.50% 1.00 0.94 0.88 0.83 0.78 0.73

Discounted Cash Flows

$

(270,000.00)

$

44,131.46

$

53,781.22

$

78,645.66

$

75,400.34

$

109,482.13

Net Present Value

$

91,440.80

Internal Rate of Return 9.13%

Financing

The optimum source of finance that should be well used by the firm for the purpose of

well financing the project should be done based on the source that is optimal, both on a cost basis

along with the current financing structure of the firm. The sources of financing that are available

with the firm are primarily the equity source and debt source (Alkhamis et al., 2017). The cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

associated with the equity sources was found out to be around 11.00% and on the other hand the

cost of debt for the firm on a post-tax basis has been around 3.50% for the firm given the set of

examples and assumptions that has been placed down for the firm. However, it is important to

note that it was observed from the financials of the Hillside Firm that the liabilities of the firm

currently comprise about 60% of the balance sheet stating that the equity fund for the firm stands

at 40%. The proportion of equity finance on a considerable basis for the firm has been very low

and that can be because of the high cost that is associated with the firm. On the other hand, the

cost of debt for the firm has been comparatively lower for the firm and along with that the firm is

also getting a tax shield for the interest payments that it would be doing which on a further note

would be reducing the effective cost of debt. Debt financing increases the financial risk of the

firm and in the case of Hillside Firm the debt funds is greater than, which could have well

reduced the total cost of borrowings but in turn would have increased the financial risk of the

firm. It was also observed that with the proposed investment project, the liquidity stricture or the

amount of working capital available would be reducing and further addition of debt in the total

financing structure would be degrading the financial situation of the firm. On the other hand, the

equity finance are on a comparative basis a safer source of finance whereby the firm would not

be liable to pay any fixed amount of return or could potentially increase the financial risk of the

business. Even, if the expected future free cash flows for the investment project does not

materializes well for the firm, even then the firm would not be facing any problem with the

same.

associated with the equity sources was found out to be around 11.00% and on the other hand the

cost of debt for the firm on a post-tax basis has been around 3.50% for the firm given the set of

examples and assumptions that has been placed down for the firm. However, it is important to

note that it was observed from the financials of the Hillside Firm that the liabilities of the firm

currently comprise about 60% of the balance sheet stating that the equity fund for the firm stands

at 40%. The proportion of equity finance on a considerable basis for the firm has been very low

and that can be because of the high cost that is associated with the firm. On the other hand, the

cost of debt for the firm has been comparatively lower for the firm and along with that the firm is

also getting a tax shield for the interest payments that it would be doing which on a further note

would be reducing the effective cost of debt. Debt financing increases the financial risk of the

firm and in the case of Hillside Firm the debt funds is greater than, which could have well

reduced the total cost of borrowings but in turn would have increased the financial risk of the

firm. It was also observed that with the proposed investment project, the liquidity stricture or the

amount of working capital available would be reducing and further addition of debt in the total

financing structure would be degrading the financial situation of the firm. On the other hand, the

equity finance are on a comparative basis a safer source of finance whereby the firm would not

be liable to pay any fixed amount of return or could potentially increase the financial risk of the

business. Even, if the expected future free cash flows for the investment project does not

materializes well for the firm, even then the firm would not be facing any problem with the

same.

8FINANCIAL MANAGEMENT

Recommendations

The recommended plan for investment and increasing the capacity of the plant should be

well accepted by the management of the firm as the same would be positively increasing the

wealth and value of the firm for the defined period of five years. The increase in the sales

revenue and profitability basis would also be helping the firm in covering the amount of

marketing expenses which it would be incurring on a yearly basis. The cash and breakeven point

was also found out to be minimal given the additional set of increase that it would be seeing in

the increase in the products sold. Finally it was also recommended that the management of the

firm should well go ahead with equity fiancé for the purpose of funding the project so that the

financial risk for the firm stays at an optimal set of rate.

Recommendations

The recommended plan for investment and increasing the capacity of the plant should be

well accepted by the management of the firm as the same would be positively increasing the

wealth and value of the firm for the defined period of five years. The increase in the sales

revenue and profitability basis would also be helping the firm in covering the amount of

marketing expenses which it would be incurring on a yearly basis. The cash and breakeven point

was also found out to be minimal given the additional set of increase that it would be seeing in

the increase in the products sold. Finally it was also recommended that the management of the

firm should well go ahead with equity fiancé for the purpose of funding the project so that the

financial risk for the firm stays at an optimal set of rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

References

Alkhamis, N., Noreen, U., Ghonaim, L., Alghonaim, S., Ibrahim, S. and Alturki, R.A.A., 2017.

Capital Budgeting and Capital Structure Decisions in Saudi Arabia. Advanced Science

Letters, 23(1), pp.330-332.

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1),

p.1468232.

Hall, J.H. and Sibanda, T., 2016. Capital Budgeting Practices: An Empirical Study of Listed

Small en Medium Enterprises. Corporate Ownership & Control, p.200.

Levin, V. and Hallgren, A., 2017. The choice of capital budgeting techniques: a human capital

approach.

Sarwary, Z., 2019. Capital Budgeting Techniques in SMEs: A Literature Review. Journal of

Accounting and Finance, 19(3).

Shaban, O.S., Al-Zubi, Z. and Abdallah, A.A., 2017. The Extent of Using Capital Budgeting

Techniques in Evaluating Manager¡¯ s Investments Projects Decisions (A Case Study on

Jordanian Industrial Companies). International Journal of Economics and Finance, 9(12),

pp.175-179.

Siziba, S. and Hall, J.H., 2019. The evolution of the application of capital budgeting techniques

in enterprises. Global Finance Journal, p.100504.

References

Alkhamis, N., Noreen, U., Ghonaim, L., Alghonaim, S., Ibrahim, S. and Alturki, R.A.A., 2017.

Capital Budgeting and Capital Structure Decisions in Saudi Arabia. Advanced Science

Letters, 23(1), pp.330-332.

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1),

p.1468232.

Hall, J.H. and Sibanda, T., 2016. Capital Budgeting Practices: An Empirical Study of Listed

Small en Medium Enterprises. Corporate Ownership & Control, p.200.

Levin, V. and Hallgren, A., 2017. The choice of capital budgeting techniques: a human capital

approach.

Sarwary, Z., 2019. Capital Budgeting Techniques in SMEs: A Literature Review. Journal of

Accounting and Finance, 19(3).

Shaban, O.S., Al-Zubi, Z. and Abdallah, A.A., 2017. The Extent of Using Capital Budgeting

Techniques in Evaluating Manager¡¯ s Investments Projects Decisions (A Case Study on

Jordanian Industrial Companies). International Journal of Economics and Finance, 9(12),

pp.175-179.

Siziba, S. and Hall, J.H., 2019. The evolution of the application of capital budgeting techniques

in enterprises. Global Finance Journal, p.100504.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

Su, S.H., Lee, H.L., Chou, J.J., Yeh, J.Y. and Thi, M.H.V., 2018. Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal of

Organizational Innovation (Online), 10(4), pp.111-120.

Winfree, J.A., Rosentraub, M.S., Mills, B.M. and Zondlak, M.P., 2018. Capital Budgeting and

Team Investments. In Sports Finance and Management (pp. 343-374). Taylor & Francis.

Su, S.H., Lee, H.L., Chou, J.J., Yeh, J.Y. and Thi, M.H.V., 2018. Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal of

Organizational Innovation (Online), 10(4), pp.111-120.

Winfree, J.A., Rosentraub, M.S., Mills, B.M. and Zondlak, M.P., 2018. Capital Budgeting and

Team Investments. In Sports Finance and Management (pp. 343-374). Taylor & Francis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.