Financial Management Case Study Report: Hillside Industries Analysis

VerifiedAdded on 2022/08/17

|11

|2799

|237

Case Study

AI Summary

This report presents a comprehensive financial management case study analysis of Hillside Industries, a public listed company considering expansion. The report evaluates working capital decisions, including the impact of increasing the debtor turnover period and the calculation of the cash conversion cycle. It then delves into breakeven analysis, comparing accounting and cash breakeven points, and assessing a proposed new technology investment. The project proposal is evaluated using the Net Present Value (NPV) method, including the calculation of the Weighted Average Cost of Capital (WACC) and a detailed NPV analysis. Finally, the report examines methods of financing, comparing the cost of equity and debt, and discussing the implications of each financing option, offering recommendations based on the analysis.

FINANCIAL MANAGEMENT

CASE STUDY REPORT

2/12/2020

STUDENT’S NAME:

CASE STUDY REPORT

2/12/2020

STUDENT’S NAME:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................2

Working capital decisions.....................................................................................................................2

Forecasted sales and productivity..........................................................................................................3

Evaluation of the project proposal.........................................................................................................4

Methods of financing and the resulting impacts....................................................................................6

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

Introduction...........................................................................................................................................2

Working capital decisions.....................................................................................................................2

Forecasted sales and productivity..........................................................................................................3

Evaluation of the project proposal.........................................................................................................4

Methods of financing and the resulting impacts....................................................................................6

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

Introduction

Few important aspects of the financial management in an organisation are that of the

decisions related to the working capital, investing and the financing. The senior management

of an organisation is required to consider the various factors involved, and making informed

judgements, because the above mentioned decisions are not only irreversible, but also involve

huge amount of investments (Ross et.al, 2014). The aim of the following report is to guide

the management of the company Hillside Industries regarding the various aspects of the

financial management decisions. The first part would involve the evaluation of the working

capital decision, followed by the analysis of the cash and the accounting break even points.

The latter part would involve the evaluation of the project proposal using the NPV method,

and the analysis of the cost of capital and financing structure.

Working capital decisions

Working capital decisions are one significant business decisions and deals with the day to day

working of the entity. The efficient decisions ensure that there are sufficient short term assets

for the fulfilment of the short term obligations (Brigham and Ehrhardt, 2013). In the given

case study, the management is contemplating the increase of the debtor turnover period from

15 to 30 days, as suggested by the marketing department of the entity. The said move is

suggested to increase the demand of the products by the ease of the payment terms to the

debtors. However, there may be serious implications of the said increase which are elaborated

as follows.

Cash conversion cycle is referred to as a metric that aids in the measurement of the time

(generally in number of days) taken by the company to convert its current resources such as

inventory and debtors into cash (Rὂhrich, 2014). Thus, the company’s operational and

managerial efficiency is gauged through the said metric. The formula for the cash conversion

cycle is stated as follows.

CCC = DSO + DIO – DPO

Where,

DSO = Daily sales outstanding or the Average Collection Period

Few important aspects of the financial management in an organisation are that of the

decisions related to the working capital, investing and the financing. The senior management

of an organisation is required to consider the various factors involved, and making informed

judgements, because the above mentioned decisions are not only irreversible, but also involve

huge amount of investments (Ross et.al, 2014). The aim of the following report is to guide

the management of the company Hillside Industries regarding the various aspects of the

financial management decisions. The first part would involve the evaluation of the working

capital decision, followed by the analysis of the cash and the accounting break even points.

The latter part would involve the evaluation of the project proposal using the NPV method,

and the analysis of the cost of capital and financing structure.

Working capital decisions

Working capital decisions are one significant business decisions and deals with the day to day

working of the entity. The efficient decisions ensure that there are sufficient short term assets

for the fulfilment of the short term obligations (Brigham and Ehrhardt, 2013). In the given

case study, the management is contemplating the increase of the debtor turnover period from

15 to 30 days, as suggested by the marketing department of the entity. The said move is

suggested to increase the demand of the products by the ease of the payment terms to the

debtors. However, there may be serious implications of the said increase which are elaborated

as follows.

Cash conversion cycle is referred to as a metric that aids in the measurement of the time

(generally in number of days) taken by the company to convert its current resources such as

inventory and debtors into cash (Rὂhrich, 2014). Thus, the company’s operational and

managerial efficiency is gauged through the said metric. The formula for the cash conversion

cycle is stated as follows.

CCC = DSO + DIO – DPO

Where,

DSO = Daily sales outstanding or the Average Collection Period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIO = Days of inventory outstanding

DPO = Days of payable outstanding or the Average Payment Period

The DSO refers to the number of days taken by the company to release the cash from the

debtors. Thus, the efficiency of the collection of cash from the sales of the company is to be

calculated in this part of the cash conversion cycle. The formula for the calculation of the

Daily Sales Outstanding is listed as follows.

Here,

Average Accounts Receivable = ½ * (Beginning Accounts Receivable + Ending Accounts

Receivable)

It is desired by the managers of an organisation to reduce the value of DSO, because of the

importance of the cash in the running of the business and the concept of the time value of

money, which means money collected sooner by a business, is of more value than the money

collected later (Scott, 2012). This is because of the ability to earn interest on the funds.

Thus, the increment of the number of days in the payment period from 15 days to 30 days,

would lead to the increment in the daily sales outstanding. The result of the same would be

increment in the overall cash conversion cycle. This can lead to the issues of liquidity crunch

in the organisation, where the entity is not having enough cash for the payment of debts.

Forecasted sales and productivity

Breakeven analysis is one of the most significant tools to evaluate the vitality of a business

decision as it highlights the impact of the same on the productivity in terms of the units to be

produced and the revenues to be charged therein, to cover the fixed and the variable costs.

Thus, the relationship between the fixed costs, variable costs and the revenues is analysed.

The breakeven point has two variations in the form of the accounting break-even point and

the cash breakeven point, which are described as follows.

DPO = Days of payable outstanding or the Average Payment Period

The DSO refers to the number of days taken by the company to release the cash from the

debtors. Thus, the efficiency of the collection of cash from the sales of the company is to be

calculated in this part of the cash conversion cycle. The formula for the calculation of the

Daily Sales Outstanding is listed as follows.

Here,

Average Accounts Receivable = ½ * (Beginning Accounts Receivable + Ending Accounts

Receivable)

It is desired by the managers of an organisation to reduce the value of DSO, because of the

importance of the cash in the running of the business and the concept of the time value of

money, which means money collected sooner by a business, is of more value than the money

collected later (Scott, 2012). This is because of the ability to earn interest on the funds.

Thus, the increment of the number of days in the payment period from 15 days to 30 days,

would lead to the increment in the daily sales outstanding. The result of the same would be

increment in the overall cash conversion cycle. This can lead to the issues of liquidity crunch

in the organisation, where the entity is not having enough cash for the payment of debts.

Forecasted sales and productivity

Breakeven analysis is one of the most significant tools to evaluate the vitality of a business

decision as it highlights the impact of the same on the productivity in terms of the units to be

produced and the revenues to be charged therein, to cover the fixed and the variable costs.

Thus, the relationship between the fixed costs, variable costs and the revenues is analysed.

The breakeven point has two variations in the form of the accounting break-even point and

the cash breakeven point, which are described as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

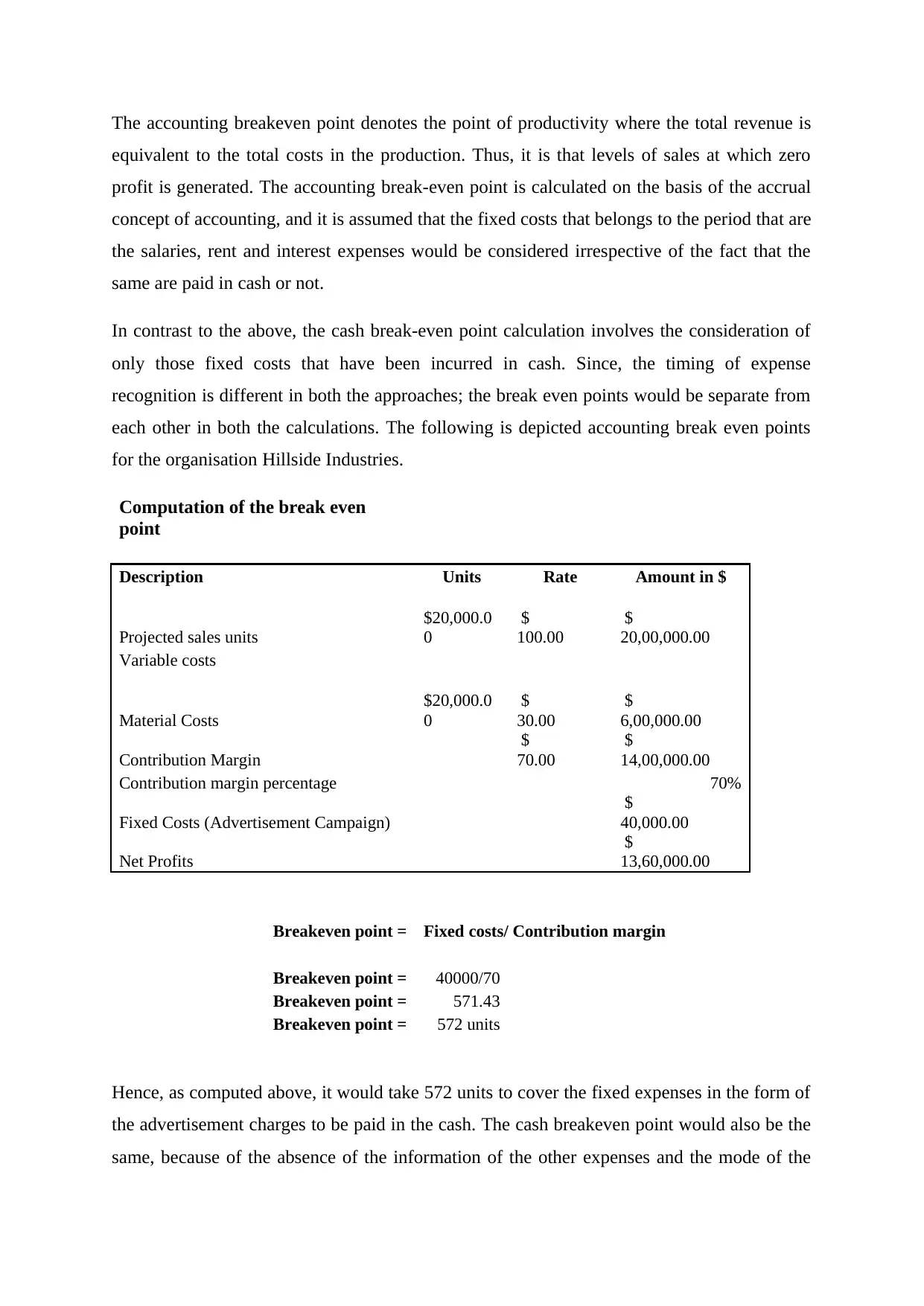

The accounting breakeven point denotes the point of productivity where the total revenue is

equivalent to the total costs in the production. Thus, it is that levels of sales at which zero

profit is generated. The accounting break-even point is calculated on the basis of the accrual

concept of accounting, and it is assumed that the fixed costs that belongs to the period that are

the salaries, rent and interest expenses would be considered irrespective of the fact that the

same are paid in cash or not.

In contrast to the above, the cash break-even point calculation involves the consideration of

only those fixed costs that have been incurred in cash. Since, the timing of expense

recognition is different in both the approaches; the break even points would be separate from

each other in both the calculations. The following is depicted accounting break even points

for the organisation Hillside Industries.

Computation of the break even

point

Description Units Rate Amount in $

Projected sales units

$20,000.0

0

$

100.00

$

20,00,000.00

Variable costs

Material Costs

$20,000.0

0

$

30.00

$

6,00,000.00

Contribution Margin

$

70.00

$

14,00,000.00

Contribution margin percentage 70%

Fixed Costs (Advertisement Campaign)

$

40,000.00

Net Profits

$

13,60,000.00

Breakeven point = Fixed costs/ Contribution margin

Breakeven point = 40000/70

Breakeven point = 571.43

Breakeven point = 572 units

Hence, as computed above, it would take 572 units to cover the fixed expenses in the form of

the advertisement charges to be paid in the cash. The cash breakeven point would also be the

same, because of the absence of the information of the other expenses and the mode of the

equivalent to the total costs in the production. Thus, it is that levels of sales at which zero

profit is generated. The accounting break-even point is calculated on the basis of the accrual

concept of accounting, and it is assumed that the fixed costs that belongs to the period that are

the salaries, rent and interest expenses would be considered irrespective of the fact that the

same are paid in cash or not.

In contrast to the above, the cash break-even point calculation involves the consideration of

only those fixed costs that have been incurred in cash. Since, the timing of expense

recognition is different in both the approaches; the break even points would be separate from

each other in both the calculations. The following is depicted accounting break even points

for the organisation Hillside Industries.

Computation of the break even

point

Description Units Rate Amount in $

Projected sales units

$20,000.0

0

$

100.00

$

20,00,000.00

Variable costs

Material Costs

$20,000.0

0

$

30.00

$

6,00,000.00

Contribution Margin

$

70.00

$

14,00,000.00

Contribution margin percentage 70%

Fixed Costs (Advertisement Campaign)

$

40,000.00

Net Profits

$

13,60,000.00

Breakeven point = Fixed costs/ Contribution margin

Breakeven point = 40000/70

Breakeven point = 571.43

Breakeven point = 572 units

Hence, as computed above, it would take 572 units to cover the fixed expenses in the form of

the advertisement charges to be paid in the cash. The cash breakeven point would also be the

same, because of the absence of the information of the other expenses and the mode of the

payments. Accordingly, it has been suggested to accept the proposal of the new technology

which would raise the demand of its products in the market, and thus ensure that the

production facilities are not lying idle.

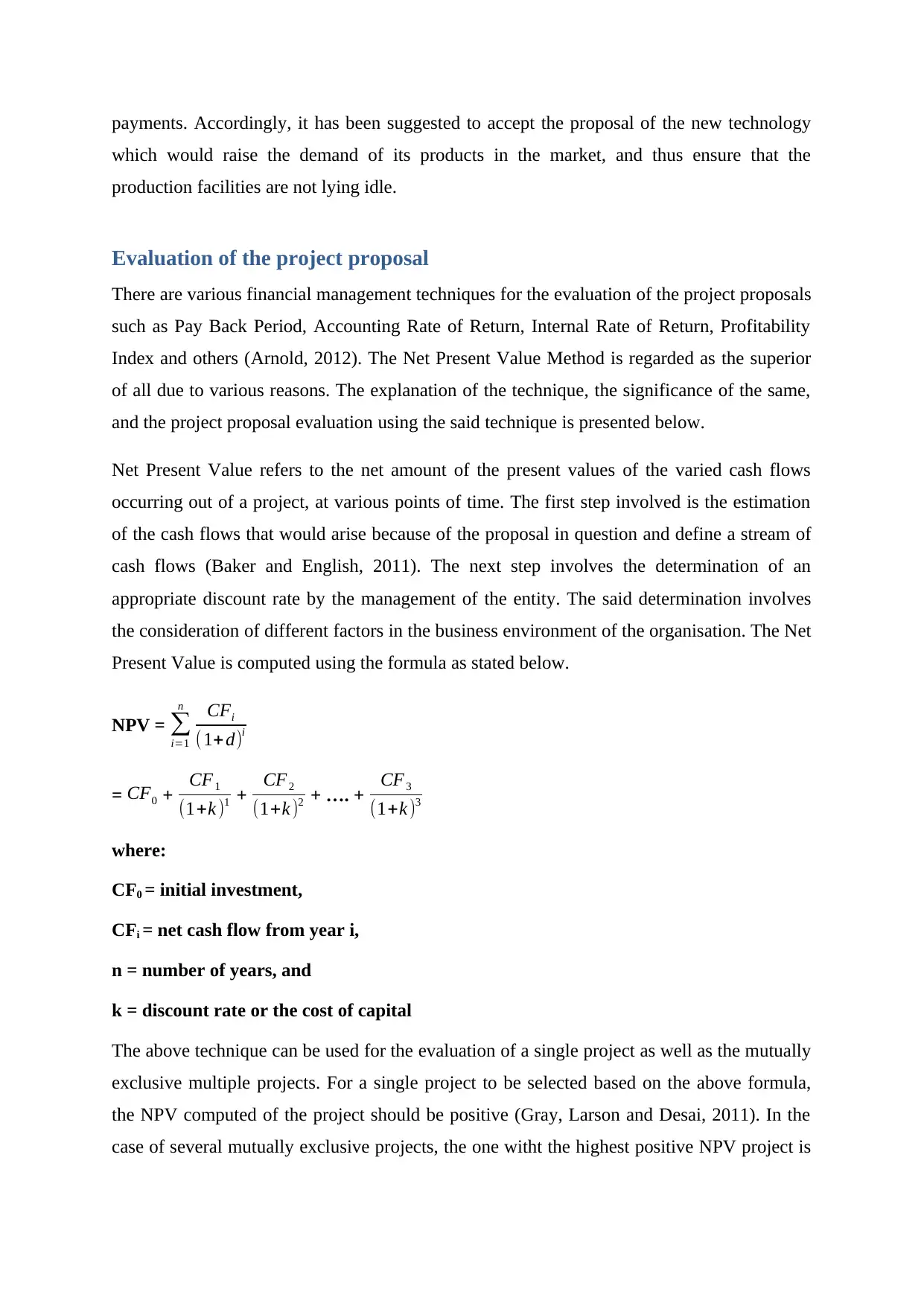

Evaluation of the project proposal

There are various financial management techniques for the evaluation of the project proposals

such as Pay Back Period, Accounting Rate of Return, Internal Rate of Return, Profitability

Index and others (Arnold, 2012). The Net Present Value Method is regarded as the superior

of all due to various reasons. The explanation of the technique, the significance of the same,

and the project proposal evaluation using the said technique is presented below.

Net Present Value refers to the net amount of the present values of the varied cash flows

occurring out of a project, at various points of time. The first step involved is the estimation

of the cash flows that would arise because of the proposal in question and define a stream of

cash flows (Baker and English, 2011). The next step involves the determination of an

appropriate discount rate by the management of the entity. The said determination involves

the consideration of different factors in the business environment of the organisation. The Net

Present Value is computed using the formula as stated below.

NPV = ∑

i=1

n CFi

(1+d)i

= CF0 + CF1

(1+k )1 + CF2

(1+k )2 + …. + CF3

(1+k )3

where:

CF0 = initial investment,

CFi = net cash flow from year i,

n = number of years, and

k = discount rate or the cost of capital

The above technique can be used for the evaluation of a single project as well as the mutually

exclusive multiple projects. For a single project to be selected based on the above formula,

the NPV computed of the project should be positive (Gray, Larson and Desai, 2011). In the

case of several mutually exclusive projects, the one witht the highest positive NPV project is

which would raise the demand of its products in the market, and thus ensure that the

production facilities are not lying idle.

Evaluation of the project proposal

There are various financial management techniques for the evaluation of the project proposals

such as Pay Back Period, Accounting Rate of Return, Internal Rate of Return, Profitability

Index and others (Arnold, 2012). The Net Present Value Method is regarded as the superior

of all due to various reasons. The explanation of the technique, the significance of the same,

and the project proposal evaluation using the said technique is presented below.

Net Present Value refers to the net amount of the present values of the varied cash flows

occurring out of a project, at various points of time. The first step involved is the estimation

of the cash flows that would arise because of the proposal in question and define a stream of

cash flows (Baker and English, 2011). The next step involves the determination of an

appropriate discount rate by the management of the entity. The said determination involves

the consideration of different factors in the business environment of the organisation. The Net

Present Value is computed using the formula as stated below.

NPV = ∑

i=1

n CFi

(1+d)i

= CF0 + CF1

(1+k )1 + CF2

(1+k )2 + …. + CF3

(1+k )3

where:

CF0 = initial investment,

CFi = net cash flow from year i,

n = number of years, and

k = discount rate or the cost of capital

The above technique can be used for the evaluation of a single project as well as the mutually

exclusive multiple projects. For a single project to be selected based on the above formula,

the NPV computed of the project should be positive (Gray, Larson and Desai, 2011). In the

case of several mutually exclusive projects, the one witht the highest positive NPV project is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

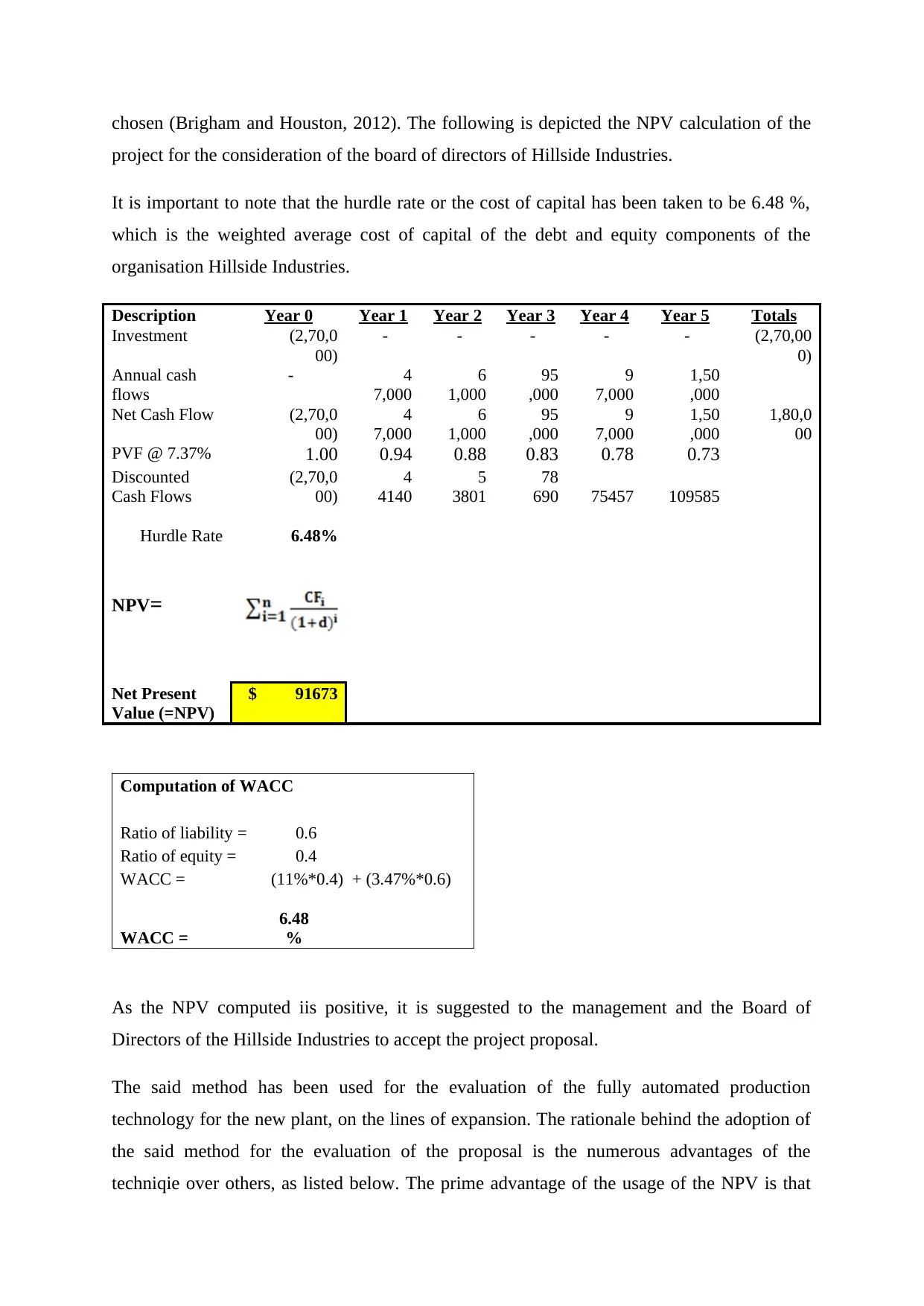

chosen (Brigham and Houston, 2012). The following is depicted the NPV calculation of the

project for the consideration of the board of directors of Hillside Industries.

It is important to note that the hurdle rate or the cost of capital has been taken to be 6.48 %,

which is the weighted average cost of capital of the debt and equity components of the

organisation Hillside Industries.

Description Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Totals

Investment (2,70,0

00)

- - - - - (2,70,00

0)

Annual cash

flows

- 4

7,000

6

1,000

95

,000

9

7,000

1,50

,000

Net Cash Flow (2,70,0

00)

4

7,000

6

1,000

95

,000

9

7,000

1,50

,000

1,80,0

00

PVF @ 7.37% 1.00 0.94 0.88 0.83 0.78 0.73

Discounted

Cash Flows

(2,70,0

00)

4

4140

5

3801

78

690 75457 109585

Hurdle Rate 6.48%

NPV=

Net Present

Value (=NPV)

$ 91673

Computation of WACC

Ratio of liability = 0.6

Ratio of equity = 0.4

WACC = (11%*0.4) + (3.47%*0.6)

WACC =

6.48

%

As the NPV computed iis positive, it is suggested to the management and the Board of

Directors of the Hillside Industries to accept the project proposal.

The said method has been used for the evaluation of the fully automated production

technology for the new plant, on the lines of expansion. The rationale behind the adoption of

the said method for the evaluation of the proposal is the numerous advantages of the

techniqie over others, as listed below. The prime advantage of the usage of the NPV is that

project for the consideration of the board of directors of Hillside Industries.

It is important to note that the hurdle rate or the cost of capital has been taken to be 6.48 %,

which is the weighted average cost of capital of the debt and equity components of the

organisation Hillside Industries.

Description Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Totals

Investment (2,70,0

00)

- - - - - (2,70,00

0)

Annual cash

flows

- 4

7,000

6

1,000

95

,000

9

7,000

1,50

,000

Net Cash Flow (2,70,0

00)

4

7,000

6

1,000

95

,000

9

7,000

1,50

,000

1,80,0

00

PVF @ 7.37% 1.00 0.94 0.88 0.83 0.78 0.73

Discounted

Cash Flows

(2,70,0

00)

4

4140

5

3801

78

690 75457 109585

Hurdle Rate 6.48%

NPV=

Net Present

Value (=NPV)

$ 91673

Computation of WACC

Ratio of liability = 0.6

Ratio of equity = 0.4

WACC = (11%*0.4) + (3.47%*0.6)

WACC =

6.48

%

As the NPV computed iis positive, it is suggested to the management and the Board of

Directors of the Hillside Industries to accept the project proposal.

The said method has been used for the evaluation of the fully automated production

technology for the new plant, on the lines of expansion. The rationale behind the adoption of

the said method for the evaluation of the proposal is the numerous advantages of the

techniqie over others, as listed below. The prime advantage of the usage of the NPV is that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the same is considerate of the time value of money concept, unlike in the Pay Back Period.

The concept of time value of money is significant to be considered in the proposal evaluation

as well, to determine the real cash flows occuring from a project. The yet another major

benefit of the usage of the Net Present Value method is that the results are in absolute terms,

that is either a positive or a negative NPV, unlike in the Internal Rate of Return Method

(IRR), where a project can have more than one IRR. Thus, in the case of the multiple IRRs,

the selection of the project becomes difficult. The said issue is avoided in the NPV method.

The method has further advantage of being the absolute measure of profitability, as all the

cash flows are considered, that the ones even occuring after the life of the project (Goyat and

Nain, 2016). Further to state, that sunk costs are avoided in the said computation, and thus the

results derived from the said technique are realistic. Hence, the above advantages of the NPV

method, makes the method suitable for the evaluation as conducted in the previous parts.

Methods of financing and the resulting impacts

Financing decisions are one of the key decisions of management of an enterprise. These

decisions must be consiously taken after taking into consideration of the various factors

involved. There are primarily two sources of finance that are debt and equity, and each of the

above have their own shares of pros and cons. The following is depicted, the computation of

the cost of equity and the cost of debt, and the analysis of the same in relation to the Hillside

Industries.

Computation of cost of equity

Rf = 1%

Beta = 2

Rm = 6%

Ke = 1% + 2*(6%-1%)

Ke = 11.00%

The concept of time value of money is significant to be considered in the proposal evaluation

as well, to determine the real cash flows occuring from a project. The yet another major

benefit of the usage of the Net Present Value method is that the results are in absolute terms,

that is either a positive or a negative NPV, unlike in the Internal Rate of Return Method

(IRR), where a project can have more than one IRR. Thus, in the case of the multiple IRRs,

the selection of the project becomes difficult. The said issue is avoided in the NPV method.

The method has further advantage of being the absolute measure of profitability, as all the

cash flows are considered, that the ones even occuring after the life of the project (Goyat and

Nain, 2016). Further to state, that sunk costs are avoided in the said computation, and thus the

results derived from the said technique are realistic. Hence, the above advantages of the NPV

method, makes the method suitable for the evaluation as conducted in the previous parts.

Methods of financing and the resulting impacts

Financing decisions are one of the key decisions of management of an enterprise. These

decisions must be consiously taken after taking into consideration of the various factors

involved. There are primarily two sources of finance that are debt and equity, and each of the

above have their own shares of pros and cons. The following is depicted, the computation of

the cost of equity and the cost of debt, and the analysis of the same in relation to the Hillside

Industries.

Computation of cost of equity

Rf = 1%

Beta = 2

Rm = 6%

Ke = 1% + 2*(6%-1%)

Ke = 11.00%

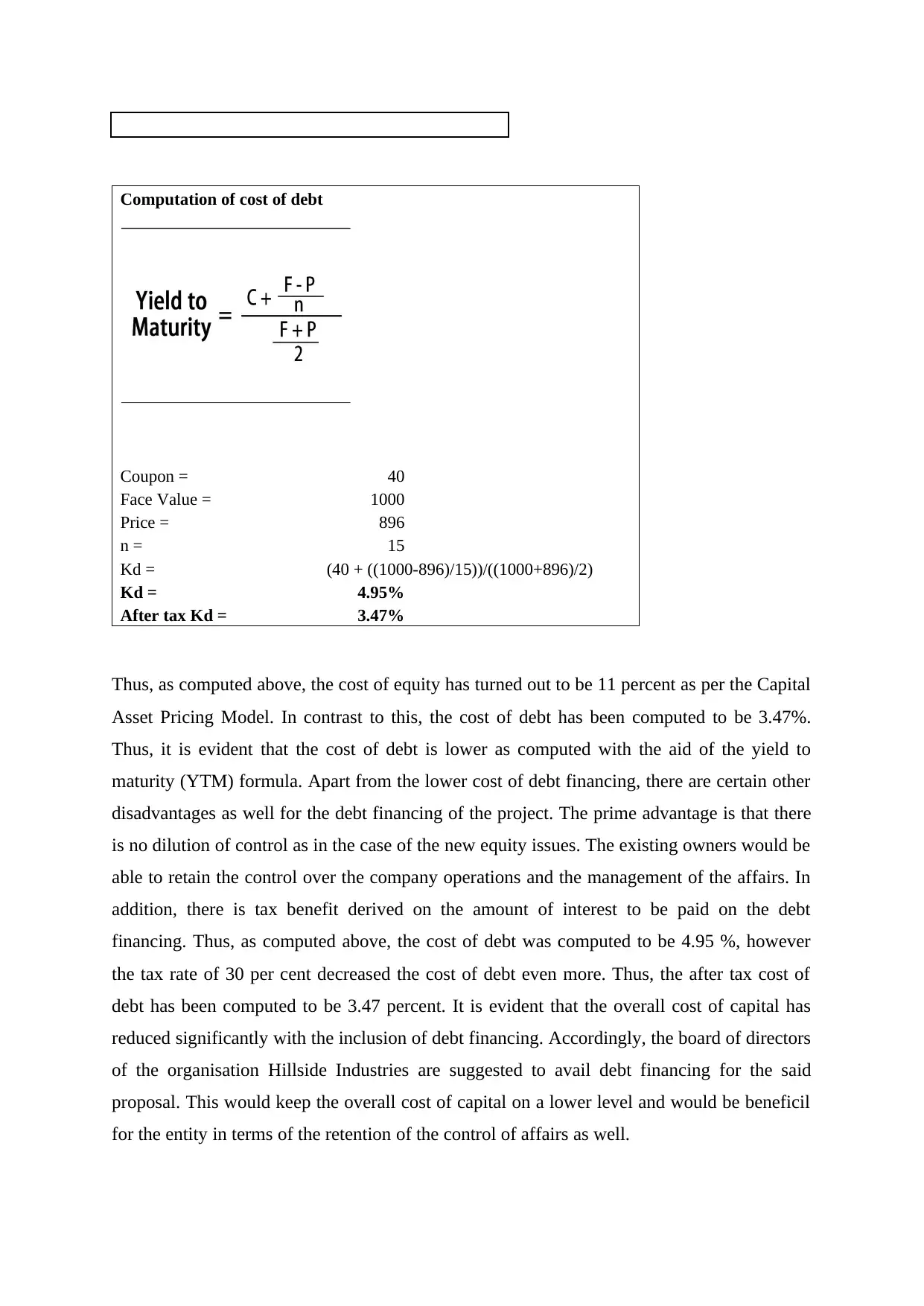

Computation of cost of debt

Coupon = 40

Face Value = 1000

Price = 896

n = 15

Kd = (40 + ((1000-896)/15))/((1000+896)/2)

Kd = 4.95%

After tax Kd = 3.47%

Thus, as computed above, the cost of equity has turned out to be 11 percent as per the Capital

Asset Pricing Model. In contrast to this, the cost of debt has been computed to be 3.47%.

Thus, it is evident that the cost of debt is lower as computed with the aid of the yield to

maturity (YTM) formula. Apart from the lower cost of debt financing, there are certain other

disadvantages as well for the debt financing of the project. The prime advantage is that there

is no dilution of control as in the case of the new equity issues. The existing owners would be

able to retain the control over the company operations and the management of the affairs. In

addition, there is tax benefit derived on the amount of interest to be paid on the debt

financing. Thus, as computed above, the cost of debt was computed to be 4.95 %, however

the tax rate of 30 per cent decreased the cost of debt even more. Thus, the after tax cost of

debt has been computed to be 3.47 percent. It is evident that the overall cost of capital has

reduced significantly with the inclusion of debt financing. Accordingly, the board of directors

of the organisation Hillside Industries are suggested to avail debt financing for the said

proposal. This would keep the overall cost of capital on a lower level and would be beneficil

for the entity in terms of the retention of the control of affairs as well.

Coupon = 40

Face Value = 1000

Price = 896

n = 15

Kd = (40 + ((1000-896)/15))/((1000+896)/2)

Kd = 4.95%

After tax Kd = 3.47%

Thus, as computed above, the cost of equity has turned out to be 11 percent as per the Capital

Asset Pricing Model. In contrast to this, the cost of debt has been computed to be 3.47%.

Thus, it is evident that the cost of debt is lower as computed with the aid of the yield to

maturity (YTM) formula. Apart from the lower cost of debt financing, there are certain other

disadvantages as well for the debt financing of the project. The prime advantage is that there

is no dilution of control as in the case of the new equity issues. The existing owners would be

able to retain the control over the company operations and the management of the affairs. In

addition, there is tax benefit derived on the amount of interest to be paid on the debt

financing. Thus, as computed above, the cost of debt was computed to be 4.95 %, however

the tax rate of 30 per cent decreased the cost of debt even more. Thus, the after tax cost of

debt has been computed to be 3.47 percent. It is evident that the overall cost of capital has

reduced significantly with the inclusion of debt financing. Accordingly, the board of directors

of the organisation Hillside Industries are suggested to avail debt financing for the said

proposal. This would keep the overall cost of capital on a lower level and would be beneficil

for the entity in terms of the retention of the control of affairs as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

The discussions conducted in the previous parts aid in the conclusion that it would be

beneficial to accept the proposal in question for the organisation Hillside Industries. The

report involved the analysis of the various financial management aspects such as that of

workin capital management, captial financing structure, and the cash and accounting

breakeven points. The future cash flows are further analysed in the light of the Net Present

Value method, and accordingly it has been suggested to accept the proposal. It is further to be

noted that the increase in the average payment period can lead to the cash crunch in the

entity, and thus the same must be taken care of for the management of the day to day

operations and the currernt obligations. Further, it has been recommended to issue bonds or

avail long term loan for the financing of the said project, so as to reduce the overall cost of

capital, and also that it is the cheaper source of financing in comparison to the equity.

The discussions conducted in the previous parts aid in the conclusion that it would be

beneficial to accept the proposal in question for the organisation Hillside Industries. The

report involved the analysis of the various financial management aspects such as that of

workin capital management, captial financing structure, and the cash and accounting

breakeven points. The future cash flows are further analysed in the light of the Net Present

Value method, and accordingly it has been suggested to accept the proposal. It is further to be

noted that the increase in the average payment period can lead to the cash crunch in the

entity, and thus the same must be taken care of for the management of the day to day

operations and the currernt obligations. Further, it has been recommended to issue bonds or

avail long term loan for the financing of the said project, so as to reduce the overall cost of

capital, and also that it is the cheaper source of financing in comparison to the equity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Arnold, G. (2012) Corporate financial management. UK: Pearson Education.

Baker, H. K., and English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F. and Ehrhardt, M. C. (2013) Financial management: Theory & practice.

Boston MA: Cengage Learning.

Brigham, E. F., and Houston, J. F. (2012) Fundamentals of Financial Management. Boston

MA: Cengage Learning.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gray, C. F., Larson, E. W., and Desai, G. V. (2011) Project Management. The Managerial

Process. 4th ed. New Delhi: Tata McGraw Hill Education Pvt. Ltd.

Ross, S. A., Westerfield, R. W., Jaffe, J., and Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

Arnold, G. (2012) Corporate financial management. UK: Pearson Education.

Baker, H. K., and English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F. and Ehrhardt, M. C. (2013) Financial management: Theory & practice.

Boston MA: Cengage Learning.

Brigham, E. F., and Houston, J. F. (2012) Fundamentals of Financial Management. Boston

MA: Cengage Learning.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gray, C. F., Larson, E. W., and Desai, G. V. (2011) Project Management. The Managerial

Process. 4th ed. New Delhi: Tata McGraw Hill Education Pvt. Ltd.

Ross, S. A., Westerfield, R. W., Jaffe, J., and Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.