Comprehensive Financial Accounting Report for HNC Business Unit 10

VerifiedAdded on 2023/06/10

|33

|7917

|68

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles and practices, focusing on Unit 10 of the HNC Business curriculum. It begins by defining financial accounting and explaining relevant regulations, accounting rules, and principles. The report then delves into the application of the double-entry bookkeeping system, demonstrating how to record sales and purchases in a general ledger and develop a trial balance. It also covers the preparation of final accounts for different business types, including sole traders, partnerships, and limited companies, considering adjustments for accruals, depreciation, and prepayments. Furthermore, the report explores bank reconciliation statements, detailing the process and importance of ensuring the validity of bank records, and concludes with a discussion on reconciling control accounts and clearing suspense accounts. The report includes practical applications and examples to illustrate key concepts and provides a thorough understanding of financial accounting practices.

HNC BUSINESS

(UNIT 10 FINANCIAL

ACCOUNTING)

(UNIT 10 FINANCIAL

ACCOUNTING)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assignment cover sheet

Name: Inderdeep Bal

Address: 51 Cedar Close

Armley

Leeds

Post code / Zip: LS12 1SL

Telephone No: 07581363395

Email Address: kulwinderkaur@talktalk.net

Date: 15/6/18

Course Name: Business, accounting and finance

2

Name: Inderdeep Bal

Address: 51 Cedar Close

Armley

Leeds

Post code / Zip: LS12 1SL

Telephone No: 07581363395

Email Address: kulwinderkaur@talktalk.net

Date: 15/6/18

Course Name: Business, accounting and finance

2

Tutor Name: Jeremy Oughton

Assignment

Name:

Unit 10– Financial accounting

3

Assignment

Name:

Unit 10– Financial accounting

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TABLE OF CONTENT

4

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

S

INTROUCTION........................................................................................................................1

LO1 Record transactions in business using double entry book keeping and also extract trial

balance........................................................................................................................................2

Define financial accounting....................................................................................................2

Explain regulations related to the financial accounting.........................................................2

Explain accounting rules and principles.................................................................................3

Describe conventions and concept of consistency and material disclosure...........................4

P1 Apply debit and credit system of the double entry book- keeping system and also record

sales and purchases transactions in a general ledger account.................................................4

P2 Develop trial balance by using the balance off rules to match the figures........................6

M1 Evaluate sales and purchase transactions to compile a trial balance by using the system

of double entry book keeping.................................................................................................7

D1 Record transactions in a correct way by producing an accurate trial balance by

completing the balance off ledger accounts in accordance with the accounting principles...8

LO2 Prepare final accounts for Sole traders, partnerships or limited companies by using

accounting principles, conventions and standards...................................................................11

P3 Prepare final accounts from trial balance figures adjusting for accrual, depreciation and

prepayments..........................................................................................................................11

P4 Generate final accounts examples for different business types such as sole traders,

partnerships or limited companies........................................................................................15

M2 Analyze various financial statements by using example such as profit and loss

accounts, balance sheet and cash flow statement.................................................................16

D2 Use appropriate calculations for preparing the final accounts.......................................19

LO3 Perform Bank reconciliation statements to ensure validity of the bank records.............20

P5 Use the bank reconciliation process to prepare a number of bank reconciliations.........20

M3 Apply the reconciliation process by reflecting the use of deposit in transit, outstanding

checks and not sufficient funds check..................................................................................21

D3 Prepare bank reconciliations by applying tools and techniques to check general

accounts and balance sheets.................................................................................................21

LO4 Reconcile control accounts and shift the recorded transactions from the suspense

account into the correct account...............................................................................................22

P6 Describe the processes to reconcile control accounts and clearing of the suspense

accounts by using several examples.....................................................................................22

M4 Show different types of accounts and explain how and why these are reconciled........23

INTROUCTION........................................................................................................................1

LO1 Record transactions in business using double entry book keeping and also extract trial

balance........................................................................................................................................2

Define financial accounting....................................................................................................2

Explain regulations related to the financial accounting.........................................................2

Explain accounting rules and principles.................................................................................3

Describe conventions and concept of consistency and material disclosure...........................4

P1 Apply debit and credit system of the double entry book- keeping system and also record

sales and purchases transactions in a general ledger account.................................................4

P2 Develop trial balance by using the balance off rules to match the figures........................6

M1 Evaluate sales and purchase transactions to compile a trial balance by using the system

of double entry book keeping.................................................................................................7

D1 Record transactions in a correct way by producing an accurate trial balance by

completing the balance off ledger accounts in accordance with the accounting principles...8

LO2 Prepare final accounts for Sole traders, partnerships or limited companies by using

accounting principles, conventions and standards...................................................................11

P3 Prepare final accounts from trial balance figures adjusting for accrual, depreciation and

prepayments..........................................................................................................................11

P4 Generate final accounts examples for different business types such as sole traders,

partnerships or limited companies........................................................................................15

M2 Analyze various financial statements by using example such as profit and loss

accounts, balance sheet and cash flow statement.................................................................16

D2 Use appropriate calculations for preparing the final accounts.......................................19

LO3 Perform Bank reconciliation statements to ensure validity of the bank records.............20

P5 Use the bank reconciliation process to prepare a number of bank reconciliations.........20

M3 Apply the reconciliation process by reflecting the use of deposit in transit, outstanding

checks and not sufficient funds check..................................................................................21

D3 Prepare bank reconciliations by applying tools and techniques to check general

accounts and balance sheets.................................................................................................21

LO4 Reconcile control accounts and shift the recorded transactions from the suspense

account into the correct account...............................................................................................22

P6 Describe the processes to reconcile control accounts and clearing of the suspense

accounts by using several examples.....................................................................................22

M4 Show different types of accounts and explain how and why these are reconciled........23

D4 Generate accurate accounts that will reconcile by using various methods.....................24

CONCLUSION........................................................................................................................24

REFERENCES.........................................................................................................................25

CONCLUSION........................................................................................................................24

REFERENCES.........................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTROUCTION

Accounting has become the most integral business function which helps in managing

all the risks identified by an entity owner. The requirement of the accounting will get

increases with several changes takes places in the external entity such as changing the

taxation requirements, determining the financial position and the actual worth of an entity.

The motive of an entity behind using the accounting system is to record all the transactions

takes places in a business by using single entry or double entry system of bookkeeping which

selects by various business users according to their purpose. A focus of the current

assignment lies in reflecting the financial accounting concepts by explaining the accounting

principles, conventions and all the standards used in an entity for different business purposes.

The worth of an entity will be ascertained by the business owner by recording all the

transactions related to various categories such as purchases, sales, and expenses. This

assignment will highlight various learning objectives which help an individual in completing

this report as per the desired objectives to get the relevant data. The first learning objective of

this assignment reflects the recording of all the business transactions by using the double-

entry book-keeping system under which every transaction has double effects which are

shown while preparing the final accounts which consists of two financial statements out of

the standard three financial statements such as profit and loss account and balance sheet. A

particular transaction is recorded by showing the business transaction’s recording as debit and

credit which have different meanings as per the different business accounts in which they are

recorded. Trial balances are recorded to get rid of all the mistakes found in the journals and

all the ledger accounts by matching the balance of the overall trial balance. The

appropriateness and the validity of the entire balance are checked by using accounting

principles to determine the actual worth of the business concern as their motive is to attract

all its stakeholders by keeping a transparent relationship with all its clients who, in turn, helps

in enhancing the overall production of the company. Second learning objective of the current

report is related with the preparation of the final accounts for different users of the business

such as sole traders, partnerships or limited companies by following the double entry system

of bookkeeping which will uses the double effect of all the transactions recorded in the

journals and general ledgers as all these further posted in two of the final accounts. The final

accounts consist of two of the accounts which are two of the statements used in determining

the financial position of an enterprise. This will emphasize on several final accounts

adjustments for all the accruals, depreciation and prepayments transactions booked in the

1

Accounting has become the most integral business function which helps in managing

all the risks identified by an entity owner. The requirement of the accounting will get

increases with several changes takes places in the external entity such as changing the

taxation requirements, determining the financial position and the actual worth of an entity.

The motive of an entity behind using the accounting system is to record all the transactions

takes places in a business by using single entry or double entry system of bookkeeping which

selects by various business users according to their purpose. A focus of the current

assignment lies in reflecting the financial accounting concepts by explaining the accounting

principles, conventions and all the standards used in an entity for different business purposes.

The worth of an entity will be ascertained by the business owner by recording all the

transactions related to various categories such as purchases, sales, and expenses. This

assignment will highlight various learning objectives which help an individual in completing

this report as per the desired objectives to get the relevant data. The first learning objective of

this assignment reflects the recording of all the business transactions by using the double-

entry book-keeping system under which every transaction has double effects which are

shown while preparing the final accounts which consists of two financial statements out of

the standard three financial statements such as profit and loss account and balance sheet. A

particular transaction is recorded by showing the business transaction’s recording as debit and

credit which have different meanings as per the different business accounts in which they are

recorded. Trial balances are recorded to get rid of all the mistakes found in the journals and

all the ledger accounts by matching the balance of the overall trial balance. The

appropriateness and the validity of the entire balance are checked by using accounting

principles to determine the actual worth of the business concern as their motive is to attract

all its stakeholders by keeping a transparent relationship with all its clients who, in turn, helps

in enhancing the overall production of the company. Second learning objective of the current

report is related with the preparation of the final accounts for different users of the business

such as sole traders, partnerships or limited companies by following the double entry system

of bookkeeping which will uses the double effect of all the transactions recorded in the

journals and general ledgers as all these further posted in two of the final accounts. The final

accounts consist of two of the accounts which are two of the statements used in determining

the financial position of an enterprise. This will emphasize on several final accounts

adjustments for all the accruals, depreciation and prepayments transactions booked in the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business which are carried forward from the general accounts to the final accounts as per

their nature of accounts. The third objective is all about the preparation of bank reconciliation

statement and its importance for an entity in comparing its business vouchers with the bank

statements to know the gaps occurred in these statements. All the differences are rectified by

using various approaches and method. Lastly, this report will focus on the reconciliation of

all the bank statements by focusing on the suspense accounts which consists of all the

adjustments used in the business transactions. In this phase, control measures are used by an

entity.

LO1 RECORD TRANSACTIONS IN BUSINESS USING DOUBLE

ENTRY BOOK KEEPING AND ALSO EXTRACT TRIAL BALANCE

Define financial accounting

Financial accounting is a term used to describe the procedure for preparing a various

set of financial statements that help in determining the entire financial performance of the

company. This will consist of preparing the income statement, positional statement, and cash

flow statements and changes in equity. This accounting procedure will focus on meeting all

the needs of the users that get benefit from the prepared statements includes inventors who

rely on the financial status of an entity before investing in it, creditors, suppliers and lastly the

major user of an entity is its customers. Financial accounting is used by an entity in

predicting future performance of the business concern as compared to the management

accounting whose motive is just to create all kinds of budgets to ensure proper business

management (Financial accounting, 2018). Different financial statements are based on using

several formulas to know the actual worth of an entity such as expenses deducted from the

generated revenues will help in determining the net income earned by the firm, liabilities

incurred in an entity + equity shareholders held by an entity will collaborated to form total

assets of the concern and cash inflow is estimated by adding up cash balances of different

sectors such as cash from operating activities, cash from financing and cash from investing

sector.

Explain regulations related to the financial accounting

Generally accepted accounting practices are a world-recognized practice that

facilitates all the users in the domestic as well as in the global region in meeting all their

accounting requirements. This regulation is a standardized framework that helps all the firms

to keep their accounting records in a systematic order. This framework consists of various

2

their nature of accounts. The third objective is all about the preparation of bank reconciliation

statement and its importance for an entity in comparing its business vouchers with the bank

statements to know the gaps occurred in these statements. All the differences are rectified by

using various approaches and method. Lastly, this report will focus on the reconciliation of

all the bank statements by focusing on the suspense accounts which consists of all the

adjustments used in the business transactions. In this phase, control measures are used by an

entity.

LO1 RECORD TRANSACTIONS IN BUSINESS USING DOUBLE

ENTRY BOOK KEEPING AND ALSO EXTRACT TRIAL BALANCE

Define financial accounting

Financial accounting is a term used to describe the procedure for preparing a various

set of financial statements that help in determining the entire financial performance of the

company. This will consist of preparing the income statement, positional statement, and cash

flow statements and changes in equity. This accounting procedure will focus on meeting all

the needs of the users that get benefit from the prepared statements includes inventors who

rely on the financial status of an entity before investing in it, creditors, suppliers and lastly the

major user of an entity is its customers. Financial accounting is used by an entity in

predicting future performance of the business concern as compared to the management

accounting whose motive is just to create all kinds of budgets to ensure proper business

management (Financial accounting, 2018). Different financial statements are based on using

several formulas to know the actual worth of an entity such as expenses deducted from the

generated revenues will help in determining the net income earned by the firm, liabilities

incurred in an entity + equity shareholders held by an entity will collaborated to form total

assets of the concern and cash inflow is estimated by adding up cash balances of different

sectors such as cash from operating activities, cash from financing and cash from investing

sector.

Explain regulations related to the financial accounting

Generally accepted accounting practices are a world-recognized practice that

facilitates all the users in the domestic as well as in the global region in meeting all their

accounting requirements. This regulation is a standardized framework that helps all the firms

to keep their accounting records in a systematic order. This framework consists of various

2

steps which consist of professional regulation, UK Company’s law requirements, EU

directives and lastly stock exchange regulations (UK financial accounting regulations, 2013).

UK GAAP will emphasize meeting various needs of different business users which consist of

several users such as charity, pensioners, insurance and banking companies in dealing with

the accounting needs of an entity. Statement of recommended practice issues by all the stated

business sectors by using all the accounting conventions which helps in determining the

financial performance of an entity. The preparation of the financial statements will get easy

by using all these statements as per the stated guidelines mentioned in the UK regulations.

Explain accounting rules and principles

There are three rules of accounting which are also considered as the golden rules of

accounting on which the whole system of accounting based upon. First among the three

accounting rule is ‘Debit the receiver and the credit the giver’ is one of the accounting rules

applied in the case of personal account as when a real person receives the cash then this will

shown as debit and when they pay any amount will show as a credit in the accounts

(Accounting rules, 2018). Another rule is ‘ Debit what comes in and credit what goes out is

for the real accounts such as land and building and plant and machinery account under which

debit signifies the incoming of the amount and cash outflow will show as a credit balance. By

default, all these accounts have a debit balance. Third and last rule of accounting is ‘Debit all

these expenses and losses and credit income and gains will apply in the case of nominal

account.

Accounting principle

Accrual- Under this concept, the transactions will get booked in the books of

accounts when the transactions get due and cleared when the receipt of the

transactions will get completed. Under this all the credit and cash transaction are

recorded as the double entry book system is also based on this principle (Accounting

principles, 2017).

Consistency- This principle says that once an accounting method or principle uses by

an entity will continue until the wound up of the company for a long-term purpose.

Going concern- Every entity wants to run its business for an indefinite period of time

so as can be done according to this principle, in which the existence of an entity is

assumed to be run for the indefinite period as all the transactions are adjusted

accordingly.

3

directives and lastly stock exchange regulations (UK financial accounting regulations, 2013).

UK GAAP will emphasize meeting various needs of different business users which consist of

several users such as charity, pensioners, insurance and banking companies in dealing with

the accounting needs of an entity. Statement of recommended practice issues by all the stated

business sectors by using all the accounting conventions which helps in determining the

financial performance of an entity. The preparation of the financial statements will get easy

by using all these statements as per the stated guidelines mentioned in the UK regulations.

Explain accounting rules and principles

There are three rules of accounting which are also considered as the golden rules of

accounting on which the whole system of accounting based upon. First among the three

accounting rule is ‘Debit the receiver and the credit the giver’ is one of the accounting rules

applied in the case of personal account as when a real person receives the cash then this will

shown as debit and when they pay any amount will show as a credit in the accounts

(Accounting rules, 2018). Another rule is ‘ Debit what comes in and credit what goes out is

for the real accounts such as land and building and plant and machinery account under which

debit signifies the incoming of the amount and cash outflow will show as a credit balance. By

default, all these accounts have a debit balance. Third and last rule of accounting is ‘Debit all

these expenses and losses and credit income and gains will apply in the case of nominal

account.

Accounting principle

Accrual- Under this concept, the transactions will get booked in the books of

accounts when the transactions get due and cleared when the receipt of the

transactions will get completed. Under this all the credit and cash transaction are

recorded as the double entry book system is also based on this principle (Accounting

principles, 2017).

Consistency- This principle says that once an accounting method or principle uses by

an entity will continue until the wound up of the company for a long-term purpose.

Going concern- Every entity wants to run its business for an indefinite period of time

so as can be done according to this principle, in which the existence of an entity is

assumed to be run for the indefinite period as all the transactions are adjusted

accordingly.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Describe conventions and concept of consistency and material disclosure

The convention is a term used to denote all the customs and traditions used by an

individual in treating all the business transactions properly as per the stated rules and the

regulations. An entity owner will use several accounting conventions to guide all the

accountants who are handling business transactions by posting the same into several accounts

to determine the financial position of an entity owner. This phase will include the accounting

conventions related to the consistency and the material concept to treat various transactions

takes places in an entity are given as below:

Consistency Convention- Consistency convention says that the accounting method uses by

an entity for depreciation or for managing all the inventories will remain the same without

changing all the used method unless and until the pronouncements of the statutory body

otherwise note is to be attached at the end of the financial statement for changing the method

frequently in a particular financial year.

Materiality Convention- This convention states the treatment of all the business transactions

by checking its materiality to be considered in the books of account (Accounting conventions,

2016). The consideration of all the transactions in the books of account which will have a

significant impact o the financial performance are covered in the accounts and rest are not

considered as out of scope as they regarded as the non-material items which do not require

disclosure in the final accounts in determining the financial status of an entity.

P1 Apply debit and credit system of the double entry book- keeping system and also record

sales and purchases transactions in a general ledger account

Double entry system of bookkeeping is a modernized system of recording all the

business transactions which have a dual effect which reflects the preparation of all the final

accounts. Under this method, all the discrepancies will be checked by an entity owner and an

accountant by reconciling all the accounts as every transaction are recorded twice in two of

the financial statements such as profit and loss accounts and balance sheet. Every transaction

is categorized into debit or credit entries which have different meaning while treating the

same in journals, ledgers, trial balance as per the default balances of all the accounts covered

in the books of accounts (Double entry accounting, 2017). Debit entries are recorded on the

left side and credit entries of all the transactions. In the system of double-entry

bookkeeping, debit means receipt and credit means the payment made by an individual or

company who balance will get reduces by showing credit balances. Debit shows the increases

4

The convention is a term used to denote all the customs and traditions used by an

individual in treating all the business transactions properly as per the stated rules and the

regulations. An entity owner will use several accounting conventions to guide all the

accountants who are handling business transactions by posting the same into several accounts

to determine the financial position of an entity owner. This phase will include the accounting

conventions related to the consistency and the material concept to treat various transactions

takes places in an entity are given as below:

Consistency Convention- Consistency convention says that the accounting method uses by

an entity for depreciation or for managing all the inventories will remain the same without

changing all the used method unless and until the pronouncements of the statutory body

otherwise note is to be attached at the end of the financial statement for changing the method

frequently in a particular financial year.

Materiality Convention- This convention states the treatment of all the business transactions

by checking its materiality to be considered in the books of account (Accounting conventions,

2016). The consideration of all the transactions in the books of account which will have a

significant impact o the financial performance are covered in the accounts and rest are not

considered as out of scope as they regarded as the non-material items which do not require

disclosure in the final accounts in determining the financial status of an entity.

P1 Apply debit and credit system of the double entry book- keeping system and also record

sales and purchases transactions in a general ledger account

Double entry system of bookkeeping is a modernized system of recording all the

business transactions which have a dual effect which reflects the preparation of all the final

accounts. Under this method, all the discrepancies will be checked by an entity owner and an

accountant by reconciling all the accounts as every transaction are recorded twice in two of

the financial statements such as profit and loss accounts and balance sheet. Every transaction

is categorized into debit or credit entries which have different meaning while treating the

same in journals, ledgers, trial balance as per the default balances of all the accounts covered

in the books of accounts (Double entry accounting, 2017). Debit entries are recorded on the

left side and credit entries of all the transactions. In the system of double-entry

bookkeeping, debit means receipt and credit means the payment made by an individual or

company who balance will get reduces by showing credit balances. Debit shows the increases

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the asset, cash or reducing the overall liability incurred in an entity while on another hand,

credit refers to an increment of the liability and decreasing all the liabilities.

Examples of accounts having debit balance

Cash and bank balance

Plant and machinery

Trade receivables

Inventory in hand

Current asset

Cost of revenue

Wages

Trade payments

Examples of accounts having credit balance

Sales

Trade payable

Gain on sale of machinery

Retained earnings

Equity capital

Sales and the purchases are two common events takes places in a normal daily routine

of an entity in order to determine the entire financial performance of an entity in a given

period of time. Every entity operates its business to conduct saes activities which, in turn,

generates revenues to meet up the total costs of purchases incurred by an entity owner to

purchases the inventories and raw materials for producing the final output. Sales and

purchases leader under the double entry system of accounting will consists of both cash

and the credit sales incurred by the firm in a particular time span. Cash sales and cash

purchases are covered in the cash account ledger and rests credit sales as the credit

purchases are only covered in the sales and the purchases leader created by the firm by

preparing general leader accounts.

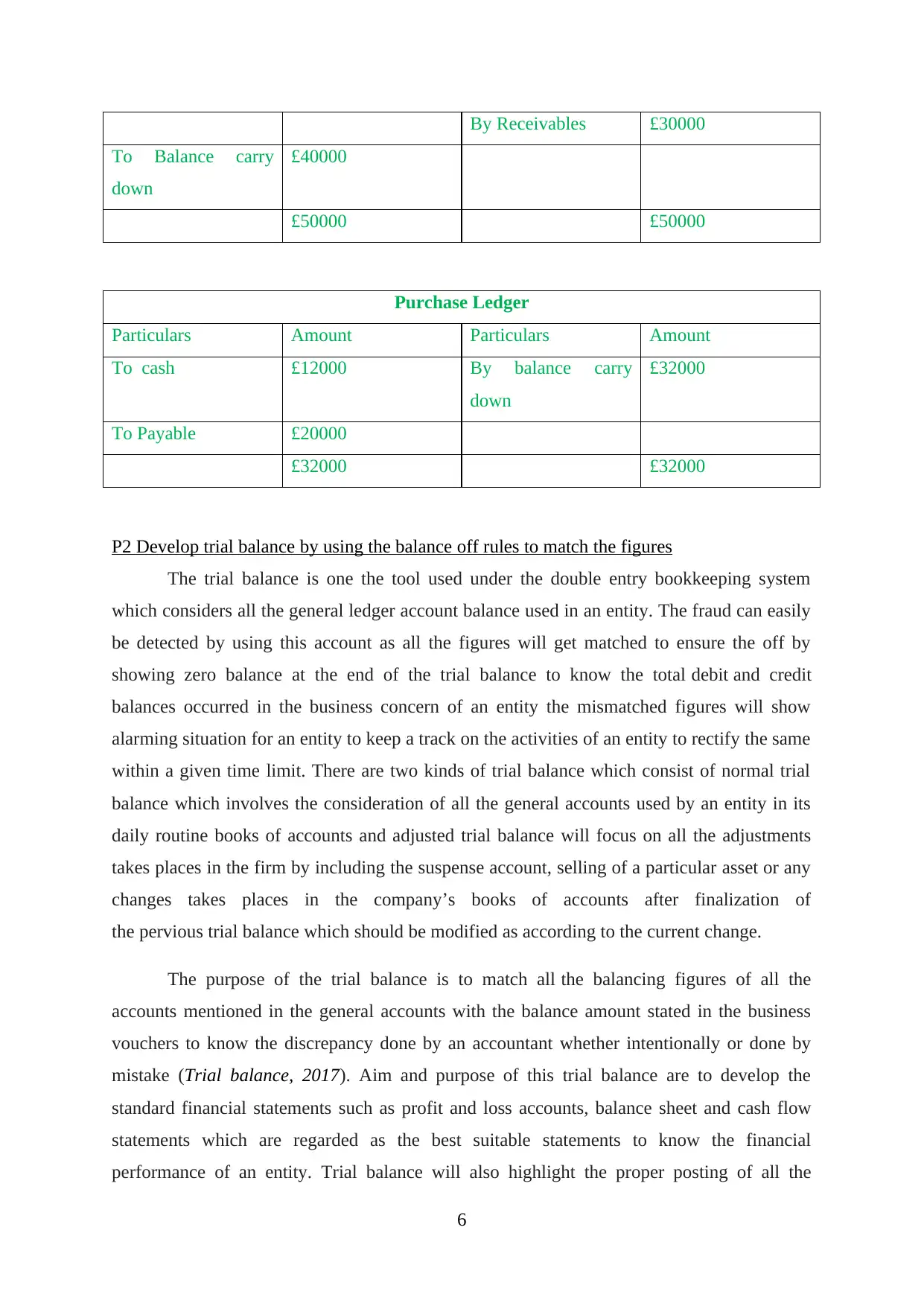

Sales Ledger

Particulars Amount Particulars Amount

To cash £10000 By Receivables £20000

5

credit refers to an increment of the liability and decreasing all the liabilities.

Examples of accounts having debit balance

Cash and bank balance

Plant and machinery

Trade receivables

Inventory in hand

Current asset

Cost of revenue

Wages

Trade payments

Examples of accounts having credit balance

Sales

Trade payable

Gain on sale of machinery

Retained earnings

Equity capital

Sales and the purchases are two common events takes places in a normal daily routine

of an entity in order to determine the entire financial performance of an entity in a given

period of time. Every entity operates its business to conduct saes activities which, in turn,

generates revenues to meet up the total costs of purchases incurred by an entity owner to

purchases the inventories and raw materials for producing the final output. Sales and

purchases leader under the double entry system of accounting will consists of both cash

and the credit sales incurred by the firm in a particular time span. Cash sales and cash

purchases are covered in the cash account ledger and rests credit sales as the credit

purchases are only covered in the sales and the purchases leader created by the firm by

preparing general leader accounts.

Sales Ledger

Particulars Amount Particulars Amount

To cash £10000 By Receivables £20000

5

By Receivables £30000

To Balance carry

down

£40000

£50000 £50000

Purchase Ledger

Particulars Amount Particulars Amount

To cash £12000 By balance carry

down

£32000

To Payable £20000

£32000 £32000

P2 Develop trial balance by using the balance off rules to match the figures

The trial balance is one the tool used under the double entry bookkeeping system

which considers all the general ledger account balance used in an entity. The fraud can easily

be detected by using this account as all the figures will get matched to ensure the off by

showing zero balance at the end of the trial balance to know the total debit and credit

balances occurred in the business concern of an entity the mismatched figures will show

alarming situation for an entity to keep a track on the activities of an entity to rectify the same

within a given time limit. There are two kinds of trial balance which consist of normal trial

balance which involves the consideration of all the general accounts used by an entity in its

daily routine books of accounts and adjusted trial balance will focus on all the adjustments

takes places in the firm by including the suspense account, selling of a particular asset or any

changes takes places in the company’s books of accounts after finalization of

the pervious trial balance which should be modified as according to the current change.

The purpose of the trial balance is to match all the balancing figures of all the

accounts mentioned in the general accounts with the balance amount stated in the business

vouchers to know the discrepancy done by an accountant whether intentionally or done by

mistake (Trial balance, 2017). Aim and purpose of this trial balance are to develop the

standard financial statements such as profit and loss accounts, balance sheet and cash flow

statements which are regarded as the best suitable statements to know the financial

performance of an entity. Trial balance will also highlight the proper posting of all the

6

To Balance carry

down

£40000

£50000 £50000

Purchase Ledger

Particulars Amount Particulars Amount

To cash £12000 By balance carry

down

£32000

To Payable £20000

£32000 £32000

P2 Develop trial balance by using the balance off rules to match the figures

The trial balance is one the tool used under the double entry bookkeeping system

which considers all the general ledger account balance used in an entity. The fraud can easily

be detected by using this account as all the figures will get matched to ensure the off by

showing zero balance at the end of the trial balance to know the total debit and credit

balances occurred in the business concern of an entity the mismatched figures will show

alarming situation for an entity to keep a track on the activities of an entity to rectify the same

within a given time limit. There are two kinds of trial balance which consist of normal trial

balance which involves the consideration of all the general accounts used by an entity in its

daily routine books of accounts and adjusted trial balance will focus on all the adjustments

takes places in the firm by including the suspense account, selling of a particular asset or any

changes takes places in the company’s books of accounts after finalization of

the pervious trial balance which should be modified as according to the current change.

The purpose of the trial balance is to match all the balancing figures of all the

accounts mentioned in the general accounts with the balance amount stated in the business

vouchers to know the discrepancy done by an accountant whether intentionally or done by

mistake (Trial balance, 2017). Aim and purpose of this trial balance are to develop the

standard financial statements such as profit and loss accounts, balance sheet and cash flow

statements which are regarded as the best suitable statements to know the financial

performance of an entity. Trial balance will also highlight the proper posting of all the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.