HND Business - Unit 2: Managing Financial Resources and Decisions

VerifiedAdded on 2020/02/03

|20

|7638

|195

Report

AI Summary

This report, prepared for an HND in Business course, delves into the critical aspects of financial resource management. It begins by identifying and assessing various sources of finance, differentiating between unincorporated and incorporated businesses, and evaluating the implications of internal and external financing. The report then analyzes the costs associated with different financing options, emphasizing the importance of financial planning, including budgeting and the implications of inadequate financing and overtrading. Furthermore, it examines the information needed for financing decisions, considering the perspectives of partners, venture capitalists, and finance brokers. The analysis extends to the impact of financing choices on financial statements, followed by a detailed examination of cash budgets, unit cost calculations for pricing decisions, and the application of investment appraisal techniques. Finally, the report discusses the key components of financial statements, compares formats, and interprets financial statements using ratio analysis, offering a comprehensive overview of financial management principles and practices.

UNIT 2

MANAGING FINANCIAL RESOURCES

AND DECISIONS

NAME: GABOR FEHER

ID: 13825

COURSE: HND IN BUSINESS

TUTOR NAME: RANSFORD GREY

1

MANAGING FINANCIAL RESOURCES

AND DECISIONS

NAME: GABOR FEHER

ID: 13825

COURSE: HND IN BUSINESS

TUTOR NAME: RANSFORD GREY

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTENTS

INTRODUCTION …………………………………………………………………………………………. 3

TASK 1 ……………………………………………………………………………………………………… 3

1.1 Identify the sources of finance available to a.)unincorporated and b.) incorporated business

……………………………………………………………………………………………………………….. 3

1.2 Assess the implications for using a.) internal and b.) external sources of finance …………………. 4

1.3 Evaluate the most appropriate sources of finance for Clariton Antiques Ltd. …………………….. 7

TASK 2 ……………………………………………………………………………………………………… 8

2.1 Analyse the cost of the two sources of finance under consideration with reference to: a.) dividends, b.)

interest and c.) tax. …………………………………………………………………………………………. 8

2.2 Explain the importance of financial planning for Clariton Antiques Ltd. With reference to: a.)

budgeting, b.)implications of failure to finance adequately and c.) overtrading. ……………………… 8

2.3 Give an assessment of the information that will be needed to make decision on financing the takeover

by: a.) the partners, b.) venture capital [We Finance Limited] and c.) finance broker.

……………………………………………………………………………………………………………….. 9

2.4 Explain the impact on the financial statement if Clariton Antiques Ltd. Choose to go with: a.) venture

capitalist, b.) financial broker. ……………………………………………………………………………. 9

TASK 3 ……………………………………………………………………………………………………. 10

3.1 Prepare an analyses of the cash budget for Clariton Antiques and advice on decision that can be taken

to improve their financial position. ……………………………………………………………………… 10

3.2 Explain how unit costs will be calculated to make pricing decision giving suitable example. …… 11

3.3 Assess the viability of the projects using investment appraisal techniques and state whether the

options satisfy Peter’s criteria for investment. ………………………………………………………….. 12

TASK 4 …………………………………………………………………………………………………….. 13

4.1 Discuss the key components of financial statement. ………………………………………………… 13

4.2 Compare the format used by Clariton to presenting their financial statement with that of a sole trader

or partnership or both. …………………………………………………………………………………… 14

4.3 Interpret the recent financial statement of Clariton using appropriate ratios and making comparison

with the previous year. ……………………………………………………………………………………. 15

CONCLUSION …………………………………………………………………………………………… 16

REFERENCES ……………………………………………………………………………………………. 17

2

INTRODUCTION …………………………………………………………………………………………. 3

TASK 1 ……………………………………………………………………………………………………… 3

1.1 Identify the sources of finance available to a.)unincorporated and b.) incorporated business

……………………………………………………………………………………………………………….. 3

1.2 Assess the implications for using a.) internal and b.) external sources of finance …………………. 4

1.3 Evaluate the most appropriate sources of finance for Clariton Antiques Ltd. …………………….. 7

TASK 2 ……………………………………………………………………………………………………… 8

2.1 Analyse the cost of the two sources of finance under consideration with reference to: a.) dividends, b.)

interest and c.) tax. …………………………………………………………………………………………. 8

2.2 Explain the importance of financial planning for Clariton Antiques Ltd. With reference to: a.)

budgeting, b.)implications of failure to finance adequately and c.) overtrading. ……………………… 8

2.3 Give an assessment of the information that will be needed to make decision on financing the takeover

by: a.) the partners, b.) venture capital [We Finance Limited] and c.) finance broker.

……………………………………………………………………………………………………………….. 9

2.4 Explain the impact on the financial statement if Clariton Antiques Ltd. Choose to go with: a.) venture

capitalist, b.) financial broker. ……………………………………………………………………………. 9

TASK 3 ……………………………………………………………………………………………………. 10

3.1 Prepare an analyses of the cash budget for Clariton Antiques and advice on decision that can be taken

to improve their financial position. ……………………………………………………………………… 10

3.2 Explain how unit costs will be calculated to make pricing decision giving suitable example. …… 11

3.3 Assess the viability of the projects using investment appraisal techniques and state whether the

options satisfy Peter’s criteria for investment. ………………………………………………………….. 12

TASK 4 …………………………………………………………………………………………………….. 13

4.1 Discuss the key components of financial statement. ………………………………………………… 13

4.2 Compare the format used by Clariton to presenting their financial statement with that of a sole trader

or partnership or both. …………………………………………………………………………………… 14

4.3 Interpret the recent financial statement of Clariton using appropriate ratios and making comparison

with the previous year. ……………………………………………………………………………………. 15

CONCLUSION …………………………………………………………………………………………… 16

REFERENCES ……………………………………………………………………………………………. 17

2

INTRODUCTION

Finance is a fuel of business. Managing financial resources in terms of time efforts and money is a

crucial task for success and accomplishment of goals for the business. Every Business organisation whether

small or large, incorporated or unincorporated requires finance at every stage to excel. Finance can take the

business from ice cream's van to dragon den. Finance can be raised through various internal and external

sources of finance. Various sources comes with distinct risks and costs associated with it. In order to make

efficient choice of funds or source options should be critically evaluated on basis of length of available funds,

risk of control and costs involved in the same. Clarion Antiques being a partnership accommodating 4 partners

is an excelling firm and growing at good speed. However finance sources vary for partnership firm and

company, influenced by various factors. Financial planning including preparing budgets and capital budgeting

plays a major role in presenting a clear picture of the project and its future profitability. Budgeting gives a

portray of company's liquidity and cash status in future. Capital Budgeting techniques such as NPV, IRR and

payback period offers a comparison of various projects and their selection and rejection based on it.

TASK 1

1.1

Finance being one of the major functions of the organisation. It is a crucial business decision to be taken on

from where to raise the funds to fulfil the business requirement. Also feasibility of various sources depends

upon the type of business such as incorporated or unincorporated. (Caglayan and Demir, 2014).

a.) Unincorporated business/sole traders and partnership: this the business where individual comes together

to perform the operation to earn profits. This does not have its own legal entity. Therefore all the risks and

liabilities of business belong wholly to the persons and individuals who are owner of the business(Bishop,

2015). These firms can raise finance from undermentioned sources:

Venture Capital / New Partner: Unincorporated firms who are not legally registered as a separate

entity can raise funds in form of investments from venture capitalist who are interested in the idea of

business. Venture capitalist are individuals or group of individuals who have surplus funds and want to

invest them in some profitable business to multiply the savings. These are risk takers and by investing in

business reap profits therefrom. Also capital of the business can be raised by admitting a new partner

who in turn will bring cash as charge against goodwill and finance into the business in return of sharing

profits.

Bank Loans: Raising of funds by receiving a bank loan is also a good option available with the

business. Long term loans can be raised from banks or financial institution. Loans involve interest cost

and scheduled repayments at particular intervals. However loans affect the financial risk and liquidity of

the business.

3

Finance is a fuel of business. Managing financial resources in terms of time efforts and money is a

crucial task for success and accomplishment of goals for the business. Every Business organisation whether

small or large, incorporated or unincorporated requires finance at every stage to excel. Finance can take the

business from ice cream's van to dragon den. Finance can be raised through various internal and external

sources of finance. Various sources comes with distinct risks and costs associated with it. In order to make

efficient choice of funds or source options should be critically evaluated on basis of length of available funds,

risk of control and costs involved in the same. Clarion Antiques being a partnership accommodating 4 partners

is an excelling firm and growing at good speed. However finance sources vary for partnership firm and

company, influenced by various factors. Financial planning including preparing budgets and capital budgeting

plays a major role in presenting a clear picture of the project and its future profitability. Budgeting gives a

portray of company's liquidity and cash status in future. Capital Budgeting techniques such as NPV, IRR and

payback period offers a comparison of various projects and their selection and rejection based on it.

TASK 1

1.1

Finance being one of the major functions of the organisation. It is a crucial business decision to be taken on

from where to raise the funds to fulfil the business requirement. Also feasibility of various sources depends

upon the type of business such as incorporated or unincorporated. (Caglayan and Demir, 2014).

a.) Unincorporated business/sole traders and partnership: this the business where individual comes together

to perform the operation to earn profits. This does not have its own legal entity. Therefore all the risks and

liabilities of business belong wholly to the persons and individuals who are owner of the business(Bishop,

2015). These firms can raise finance from undermentioned sources:

Venture Capital / New Partner: Unincorporated firms who are not legally registered as a separate

entity can raise funds in form of investments from venture capitalist who are interested in the idea of

business. Venture capitalist are individuals or group of individuals who have surplus funds and want to

invest them in some profitable business to multiply the savings. These are risk takers and by investing in

business reap profits therefrom. Also capital of the business can be raised by admitting a new partner

who in turn will bring cash as charge against goodwill and finance into the business in return of sharing

profits.

Bank Loans: Raising of funds by receiving a bank loan is also a good option available with the

business. Long term loans can be raised from banks or financial institution. Loans involve interest cost

and scheduled repayments at particular intervals. However loans affect the financial risk and liquidity of

the business.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings: Business can use the undistributed parts of profits retained by owners in the

business and this is best internal source as does not involve any cost and scheduled repayments.

Reduction in Working Capital Cycle: Short terms funds can be raised by reducing the working capital

cycle in terms of reducing the credit period extended to debtors or better stock selling activities for

improving liquidity.

b.) Incorporated Business/ Private or Public Limited Companies: It is the form of business that have their

individual legal status. All the risks and liabilities associated of the business are only responsibility of the

business and business and owners have separate legal entity. Some of the following sources of incorporated

business are as follows.

Issuing Share capital: can raise funds by issuing share capital to the public and receiving funds on the

same. Equity shares are financial instruments which transfers the ownership of the business to the

shareholder and appropriation of profits against them. Shareholders have right over the profits of the

business and business distribute the profits in the form of dividends.

Issuing bonds or debentures: can raise funds against floating debt instruments such as debentures or

bonds in the market and receiving debt against the same from public. Debentures are financial debt

instrument that acknowledges the company against debt provided by the debenture holder.

Retained earnings: it is that part of profits which are not distributed as dividends to the shareholders

and instead plough back into the business to multiply the amount by using as source of finance. It does

not involve any financial costs or risk associated with them.

Raising loans from Banks or Financial Institution: can raise funds by applying and receiving loans

from Banks and financial institution for longer period of time. However loans have fixed rescheduled

payment of interest and principal which affects the liquidity of the company. Dividends which are

appropriation of profits.

4

business and this is best internal source as does not involve any cost and scheduled repayments.

Reduction in Working Capital Cycle: Short terms funds can be raised by reducing the working capital

cycle in terms of reducing the credit period extended to debtors or better stock selling activities for

improving liquidity.

b.) Incorporated Business/ Private or Public Limited Companies: It is the form of business that have their

individual legal status. All the risks and liabilities associated of the business are only responsibility of the

business and business and owners have separate legal entity. Some of the following sources of incorporated

business are as follows.

Issuing Share capital: can raise funds by issuing share capital to the public and receiving funds on the

same. Equity shares are financial instruments which transfers the ownership of the business to the

shareholder and appropriation of profits against them. Shareholders have right over the profits of the

business and business distribute the profits in the form of dividends.

Issuing bonds or debentures: can raise funds against floating debt instruments such as debentures or

bonds in the market and receiving debt against the same from public. Debentures are financial debt

instrument that acknowledges the company against debt provided by the debenture holder.

Retained earnings: it is that part of profits which are not distributed as dividends to the shareholders

and instead plough back into the business to multiply the amount by using as source of finance. It does

not involve any financial costs or risk associated with them.

Raising loans from Banks or Financial Institution: can raise funds by applying and receiving loans

from Banks and financial institution for longer period of time. However loans have fixed rescheduled

payment of interest and principal which affects the liquidity of the company. Dividends which are

appropriation of profits.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

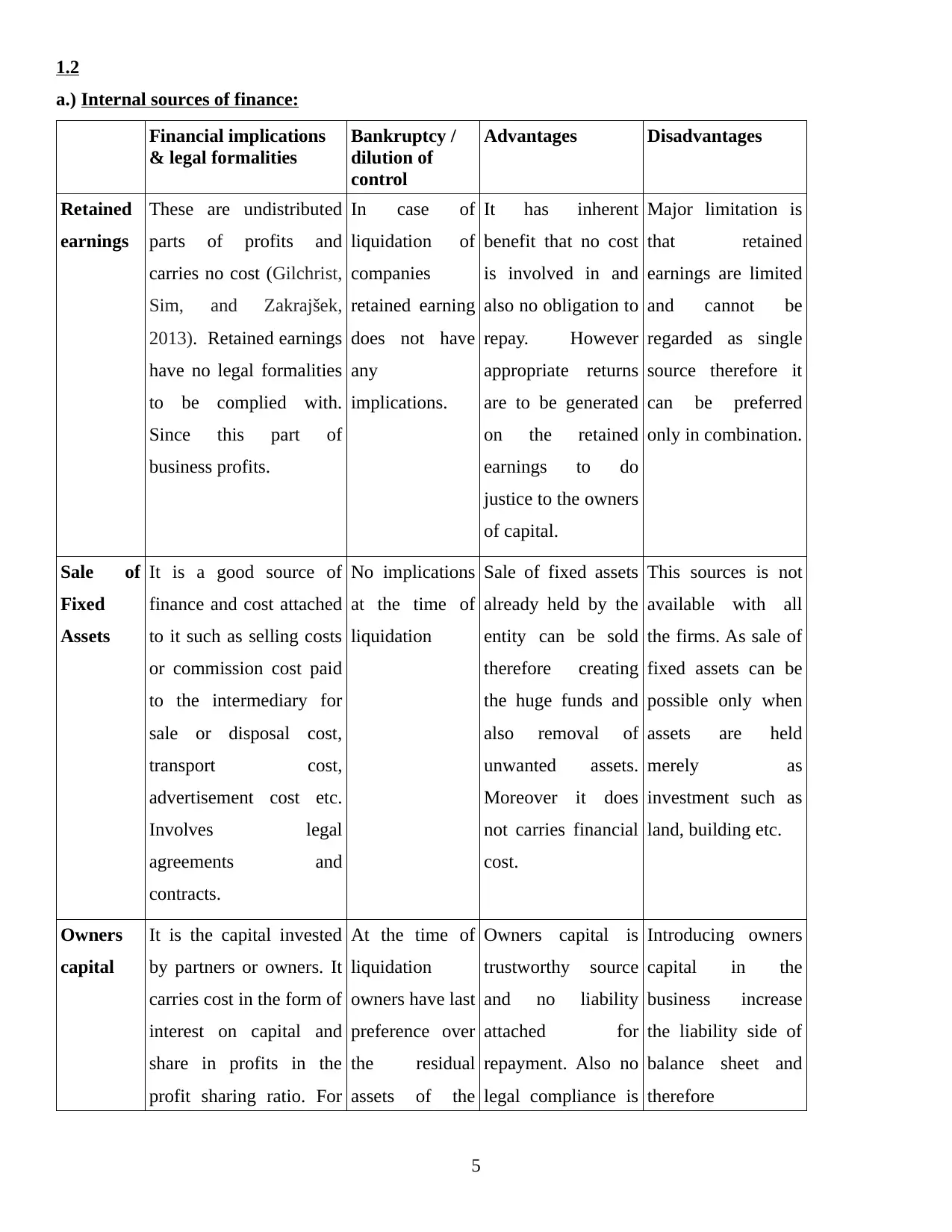

1.2

a.) Internal sources of finance:

Financial implications

& legal formalities

Bankruptcy /

dilution of

control

Advantages Disadvantages

Retained

earnings

These are undistributed

parts of profits and

carries no cost (Gilchrist,

Sim, and Zakrajšek,

2013). Retained earnings

have no legal formalities

to be complied with.

Since this part of

business profits.

In case of

liquidation of

companies

retained earning

does not have

any

implications.

It has inherent

benefit that no cost

is involved in and

also no obligation to

repay. However

appropriate returns

are to be generated

on the retained

earnings to do

justice to the owners

of capital.

Major limitation is

that retained

earnings are limited

and cannot be

regarded as single

source therefore it

can be preferred

only in combination.

Sale of

Fixed

Assets

It is a good source of

finance and cost attached

to it such as selling costs

or commission cost paid

to the intermediary for

sale or disposal cost,

transport cost,

advertisement cost etc.

Involves legal

agreements and

contracts.

No implications

at the time of

liquidation

Sale of fixed assets

already held by the

entity can be sold

therefore creating

the huge funds and

also removal of

unwanted assets.

Moreover it does

not carries financial

cost.

This sources is not

available with all

the firms. As sale of

fixed assets can be

possible only when

assets are held

merely as

investment such as

land, building etc.

Owners

capital

It is the capital invested

by partners or owners. It

carries cost in the form of

interest on capital and

share in profits in the

profit sharing ratio. For

At the time of

liquidation

owners have last

preference over

the residual

assets of the

Owners capital is

trustworthy source

and no liability

attached for

repayment. Also no

legal compliance is

Introducing owners

capital in the

business increase

the liability side of

balance sheet and

therefore

5

a.) Internal sources of finance:

Financial implications

& legal formalities

Bankruptcy /

dilution of

control

Advantages Disadvantages

Retained

earnings

These are undistributed

parts of profits and

carries no cost (Gilchrist,

Sim, and Zakrajšek,

2013). Retained earnings

have no legal formalities

to be complied with.

Since this part of

business profits.

In case of

liquidation of

companies

retained earning

does not have

any

implications.

It has inherent

benefit that no cost

is involved in and

also no obligation to

repay. However

appropriate returns

are to be generated

on the retained

earnings to do

justice to the owners

of capital.

Major limitation is

that retained

earnings are limited

and cannot be

regarded as single

source therefore it

can be preferred

only in combination.

Sale of

Fixed

Assets

It is a good source of

finance and cost attached

to it such as selling costs

or commission cost paid

to the intermediary for

sale or disposal cost,

transport cost,

advertisement cost etc.

Involves legal

agreements and

contracts.

No implications

at the time of

liquidation

Sale of fixed assets

already held by the

entity can be sold

therefore creating

the huge funds and

also removal of

unwanted assets.

Moreover it does

not carries financial

cost.

This sources is not

available with all

the firms. As sale of

fixed assets can be

possible only when

assets are held

merely as

investment such as

land, building etc.

Owners

capital

It is the capital invested

by partners or owners. It

carries cost in the form of

interest on capital and

share in profits in the

profit sharing ratio. For

At the time of

liquidation

owners have last

preference over

the residual

assets of the

Owners capital is

trustworthy source

and no liability

attached for

repayment. Also no

legal compliance is

Introducing owners

capital in the

business increase

the liability side of

balance sheet and

therefore

5

raising owners capital

internally there are no

such legal formalities.

However deed or

agreement is entered for

the provision of profit

sharing ratios or interest

in capital.

firm. If more

partners are

admitted into

firm for the

funds in form of

capital it dilutes

the control of

existing partner.

required and interest

on capital is a tax

deductible expense.

unbalancing the

debt equity ratio.

Further amount is

not sufficient

generally to support

big projects.

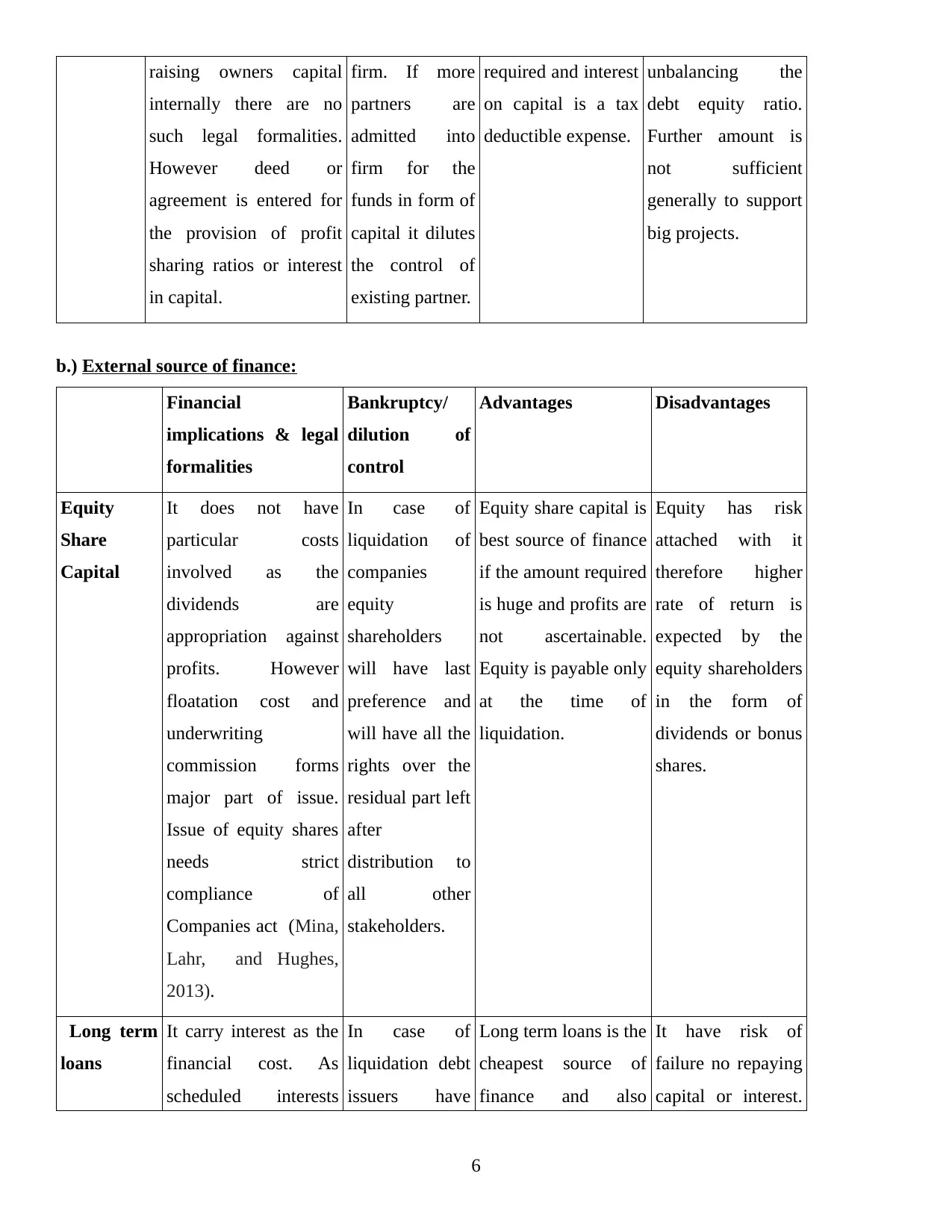

b.) External source of finance:

Financial

implications & legal

formalities

Bankruptcy/

dilution of

control

Advantages Disadvantages

Equity

Share

Capital

It does not have

particular costs

involved as the

dividends are

appropriation against

profits. However

floatation cost and

underwriting

commission forms

major part of issue.

Issue of equity shares

needs strict

compliance of

Companies act (Mina,

Lahr, and Hughes,

2013).

In case of

liquidation of

companies

equity

shareholders

will have last

preference and

will have all the

rights over the

residual part left

after

distribution to

all other

stakeholders.

Equity share capital is

best source of finance

if the amount required

is huge and profits are

not ascertainable.

Equity is payable only

at the time of

liquidation.

Equity has risk

attached with it

therefore higher

rate of return is

expected by the

equity shareholders

in the form of

dividends or bonus

shares.

Long term

loans

It carry interest as the

financial cost. As

scheduled interests

In case of

liquidation debt

issuers have

Long term loans is the

cheapest source of

finance and also

It have risk of

failure no repaying

capital or interest.

6

internally there are no

such legal formalities.

However deed or

agreement is entered for

the provision of profit

sharing ratios or interest

in capital.

firm. If more

partners are

admitted into

firm for the

funds in form of

capital it dilutes

the control of

existing partner.

required and interest

on capital is a tax

deductible expense.

unbalancing the

debt equity ratio.

Further amount is

not sufficient

generally to support

big projects.

b.) External source of finance:

Financial

implications & legal

formalities

Bankruptcy/

dilution of

control

Advantages Disadvantages

Equity

Share

Capital

It does not have

particular costs

involved as the

dividends are

appropriation against

profits. However

floatation cost and

underwriting

commission forms

major part of issue.

Issue of equity shares

needs strict

compliance of

Companies act (Mina,

Lahr, and Hughes,

2013).

In case of

liquidation of

companies

equity

shareholders

will have last

preference and

will have all the

rights over the

residual part left

after

distribution to

all other

stakeholders.

Equity share capital is

best source of finance

if the amount required

is huge and profits are

not ascertainable.

Equity is payable only

at the time of

liquidation.

Equity has risk

attached with it

therefore higher

rate of return is

expected by the

equity shareholders

in the form of

dividends or bonus

shares.

Long term

loans

It carry interest as the

financial cost. As

scheduled interests

In case of

liquidation debt

issuers have

Long term loans is the

cheapest source of

finance and also

It have risk of

failure no repaying

capital or interest.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and capital repayments

are fixed it affects for

firm liquidity

first preference

over the assets

of the business.

provides tax benefit

on the interest

payments.

Scheduled

repayment affects

the liquidity

adversely.

Hiring and

Leasing

These have attached

cost in the form of

hiring and lease

rentals payable in

instalments. The legal

contracts entered by

the agency and client

for hiring the asset or

leasing.

In case of

liquidation

hiring and

leasing rentals

will be paid

with high

priority.

Leasing or hiring the

asset avoids huge

spending on the fixed

assets which requires

huge cost. Lease

rentals are tax

deductible.

Hiring and leasing

are costly and

depreciation is not

allowed. Further

Lease rental

payments at fixed

intervals affects the

cash flows of the

company.

Overdraft It has interest as its

financial cost. It is

payable for the

duration of drawing

overdraft. It is based

on relationship and

past records of

customer with bank.

In case of

liquidation

overdraft will

be paid at

preference.

Overdraft is a cheap

source of finance and

satisfies the urgent

financial requirement.

It is for short term

and also affects the

reputation of

company in eyes of

banks and further

once taken cannot

be drawn time and

again.

Governmen

t grants

It carries no financial

cost as they are the

financial assistance

from the government

to promote business. It

has specific conditions

to be fulfilled for

receiving the grant.

No effect at the

time of

liquidation.

Government projects

are of great help to

finance huge projects.

Government grants

are attached with

complex conditions

which are to

strictly complied.

1.3

Clariton is a partnership firm however thinking of conversion into Public Limited Company. If examine

7

are fixed it affects for

firm liquidity

first preference

over the assets

of the business.

provides tax benefit

on the interest

payments.

Scheduled

repayment affects

the liquidity

adversely.

Hiring and

Leasing

These have attached

cost in the form of

hiring and lease

rentals payable in

instalments. The legal

contracts entered by

the agency and client

for hiring the asset or

leasing.

In case of

liquidation

hiring and

leasing rentals

will be paid

with high

priority.

Leasing or hiring the

asset avoids huge

spending on the fixed

assets which requires

huge cost. Lease

rentals are tax

deductible.

Hiring and leasing

are costly and

depreciation is not

allowed. Further

Lease rental

payments at fixed

intervals affects the

cash flows of the

company.

Overdraft It has interest as its

financial cost. It is

payable for the

duration of drawing

overdraft. It is based

on relationship and

past records of

customer with bank.

In case of

liquidation

overdraft will

be paid at

preference.

Overdraft is a cheap

source of finance and

satisfies the urgent

financial requirement.

It is for short term

and also affects the

reputation of

company in eyes of

banks and further

once taken cannot

be drawn time and

again.

Governmen

t grants

It carries no financial

cost as they are the

financial assistance

from the government

to promote business. It

has specific conditions

to be fulfilled for

receiving the grant.

No effect at the

time of

liquidation.

Government projects

are of great help to

finance huge projects.

Government grants

are attached with

complex conditions

which are to

strictly complied.

1.3

Clariton is a partnership firm however thinking of conversion into Public Limited Company. If examine

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the possible internal source can be seen that none of them good enough. The Retained earnings: no cost but the

amount is too low for the investment. The Owners capital: is also low because of only two owner and no

vendible fixed assets as well. If examine the external sources can be seen that the Government grants here is not

an option, the Overdraft: is good for short term goal and urgent cases with limited amount. Hiring and Leasing:

is can good for buying assets but not good for increase capital and cash flow. Therefore, best sources of finance

available for Clariton is selling shares and raising the finance. The required amount be obtained and the

liquidity is provided. The next best alternative for raising funds are long-term borrowings from the bank.

Since the Clariton is operating from quite a long time they don't have issue regarding liquidity therefore can

easily pay of the scheduled repayments on time.

TASK 2

2.1

As stated the most appropriate sources of finance for the company are Issue of Equity Shares or

borrowing funds from bank. Both these sources allow long term funds and amount involved may be large.

Therefore for major financial decision such as expansion or in terms of product diversification these sources

should be preferred.

In raising finance, clariton is face with the choice of debt finance vs equity finance . debt finance refers

to the borrow cost, this normally cheaper, the major cost to debt financing is interest , this normally refer to as

the after tax interest (1-t), this is because interest on business borrowings exempt from tax, this makes

borrowing cheaper for business purposes, in the case of clariton.

a) Dividend: It is the cost which is attached with venture capitalist source of finance. As per the case “

We Finance limited” is the venture capitalist and entity wants 20% stake in the business against its investments.

It is kind of equity financing in which Clariton will have to pay dividend of 20% to the investor and capitalist

will get rights to influence decisions of cited firm. Every year 20% dividend will increase economic burden on

the entity and it will reduce profit as well.

(Cost of Equity = (Next Year's Annual Dividend / Current SHARE Price) + Dividend Growth Rate)

For instance:

Cost of equity=(25/60)+3%

Cost of equity=3.4%

b) Interest: It is associated with the bank loan and kind of debt financing. As if Clariton takes loan from

financial institutes then it will have to pay interest on it. Bank charges 2% annual interest and 1% brokerage

charged by broker, that would increase cost of the cited firm. For instance; Clariton is taking loan of 5,00,000

then cost of interest would be calculated as below:

=500000*2%+1%*500000

8

amount is too low for the investment. The Owners capital: is also low because of only two owner and no

vendible fixed assets as well. If examine the external sources can be seen that the Government grants here is not

an option, the Overdraft: is good for short term goal and urgent cases with limited amount. Hiring and Leasing:

is can good for buying assets but not good for increase capital and cash flow. Therefore, best sources of finance

available for Clariton is selling shares and raising the finance. The required amount be obtained and the

liquidity is provided. The next best alternative for raising funds are long-term borrowings from the bank.

Since the Clariton is operating from quite a long time they don't have issue regarding liquidity therefore can

easily pay of the scheduled repayments on time.

TASK 2

2.1

As stated the most appropriate sources of finance for the company are Issue of Equity Shares or

borrowing funds from bank. Both these sources allow long term funds and amount involved may be large.

Therefore for major financial decision such as expansion or in terms of product diversification these sources

should be preferred.

In raising finance, clariton is face with the choice of debt finance vs equity finance . debt finance refers

to the borrow cost, this normally cheaper, the major cost to debt financing is interest , this normally refer to as

the after tax interest (1-t), this is because interest on business borrowings exempt from tax, this makes

borrowing cheaper for business purposes, in the case of clariton.

a) Dividend: It is the cost which is attached with venture capitalist source of finance. As per the case “

We Finance limited” is the venture capitalist and entity wants 20% stake in the business against its investments.

It is kind of equity financing in which Clariton will have to pay dividend of 20% to the investor and capitalist

will get rights to influence decisions of cited firm. Every year 20% dividend will increase economic burden on

the entity and it will reduce profit as well.

(Cost of Equity = (Next Year's Annual Dividend / Current SHARE Price) + Dividend Growth Rate)

For instance:

Cost of equity=(25/60)+3%

Cost of equity=3.4%

b) Interest: It is associated with the bank loan and kind of debt financing. As if Clariton takes loan from

financial institutes then it will have to pay interest on it. Bank charges 2% annual interest and 1% brokerage

charged by broker, that would increase cost of the cited firm. For instance; Clariton is taking loan of 5,00,000

then cost of interest would be calculated as below:

=500000*2%+1%*500000

8

=10000+5000

=15000 cost of interest would have to be beard by Clariton if it goes with bank loan.

c) Tax: It is another cost of source of finance in which cited firm will have to pay corporate tax on its

income. For instance currently tax is 30% then cost of tax would be:

=2%*(1-0.2)*£5,00,000

= £7000 +1% of £500000 admin fees

=£7000+£5000

=12000 would be cost of tax which has to be beard by Clariton antiques Ltd.

Loans from Bank: it is a long term obligations for the business to be repaid in fixed repayment

schedule agreed between the parties. Clariton if took loan from banks at 2% interest rate for the term of

10 years it will be liable to pay 1% broker fee. Also interest paid is tax deductible for the business and

tax benefit is generated by business on the same. But interest is charge against profits unlike dividends

which are appropriation of profits. It implies that company will have to pay interest on loans.

THE COST OF EQUITY FINANCE REFERS TO THE RETURN INVESTORS WILL NEED

FROM INVESTING IN THEBUSINESS , THIS IS SIMPLE SENSE REFERES TO DIVIDEND ,

TO MEASURE THIS THERE ARE DIFFERENT MODELS USE , THE MOST COMMON IS

THE DIVIDEND GROWTH MODEL (Cost of Equity = (Next Year's Annual Dividend /

Current SHARE Price) + Dividend Growth Rate) , THIS MODEL CALCULATES THE COST

OF EQUITY BY ASSUMING THAT DIVIDEND WILL GROW AT A CONSTANT RATE , THIS

BECAUSE INVESTORS WILL REQUIRE THEIR INVESTMENT TO GROW OVER TIME .

Equity Share Capital: Finance can be raised by issuing equity shares to the public. We Finance is

providing 5 Million towards 20% ownership in the business. Owners of the equity shares becomes the

owners of the company and has rights over the assets and residual profits of the company.

Dividends are distributed to the shareholders as return to their investment. Dividends are appropriation

of profits which implies that if profits are earned by the company, dividends will be declared otherwise

not. Company do not to pay tax on dividends. Therefore We Finance invest for 20% ownership in the

business it will be paid dividends out of the profits earned by Clariton.

◦ From the above discussion it can be said that all financial sources have some cost so organizations

need to select most appropriate source which has less cost and can give long term benefit to the

entity.

2.2

Financial planning is a major function of the business organisation to manage its functions smoothly

and in orderly manner. FINANCIAL PLANNING HAS MANY POSITIVE EFFECTS ON A BUSINESS , AS

9

=15000 cost of interest would have to be beard by Clariton if it goes with bank loan.

c) Tax: It is another cost of source of finance in which cited firm will have to pay corporate tax on its

income. For instance currently tax is 30% then cost of tax would be:

=2%*(1-0.2)*£5,00,000

= £7000 +1% of £500000 admin fees

=£7000+£5000

=12000 would be cost of tax which has to be beard by Clariton antiques Ltd.

Loans from Bank: it is a long term obligations for the business to be repaid in fixed repayment

schedule agreed between the parties. Clariton if took loan from banks at 2% interest rate for the term of

10 years it will be liable to pay 1% broker fee. Also interest paid is tax deductible for the business and

tax benefit is generated by business on the same. But interest is charge against profits unlike dividends

which are appropriation of profits. It implies that company will have to pay interest on loans.

THE COST OF EQUITY FINANCE REFERS TO THE RETURN INVESTORS WILL NEED

FROM INVESTING IN THEBUSINESS , THIS IS SIMPLE SENSE REFERES TO DIVIDEND ,

TO MEASURE THIS THERE ARE DIFFERENT MODELS USE , THE MOST COMMON IS

THE DIVIDEND GROWTH MODEL (Cost of Equity = (Next Year's Annual Dividend /

Current SHARE Price) + Dividend Growth Rate) , THIS MODEL CALCULATES THE COST

OF EQUITY BY ASSUMING THAT DIVIDEND WILL GROW AT A CONSTANT RATE , THIS

BECAUSE INVESTORS WILL REQUIRE THEIR INVESTMENT TO GROW OVER TIME .

Equity Share Capital: Finance can be raised by issuing equity shares to the public. We Finance is

providing 5 Million towards 20% ownership in the business. Owners of the equity shares becomes the

owners of the company and has rights over the assets and residual profits of the company.

Dividends are distributed to the shareholders as return to their investment. Dividends are appropriation

of profits which implies that if profits are earned by the company, dividends will be declared otherwise

not. Company do not to pay tax on dividends. Therefore We Finance invest for 20% ownership in the

business it will be paid dividends out of the profits earned by Clariton.

◦ From the above discussion it can be said that all financial sources have some cost so organizations

need to select most appropriate source which has less cost and can give long term benefit to the

entity.

2.2

Financial planning is a major function of the business organisation to manage its functions smoothly

and in orderly manner. FINANCIAL PLANNING HAS MANY POSITIVE EFFECTS ON A BUSINESS , AS

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART OF FINANCIAL PLANNING THE BUSINESS WILL CARRY ON BUDGETTING :-

a.) Budgeting is detailed plan to forecast expenses and incomes to be incurred in future (Board, 2015).

Budgeting is an important functions incorporated in financial planning which will assist Clariton in depicting

the expected future inflows and outflows or sales and revenue and all other financial aspects which helps the

organisation to determine the future surplus and deficit. Further Clariton is planning to open a new branch

which will have projected sales and related expenses which are to be considered in budgeting. Financial

planning is very important and supports firm in preparing budget by this way issues related to inadequacy of

funds can be minimized. It gives positive results to entities by this way unnecessary expenditures can be

minimized and firm can achieve its economic goal.

b.) Implications of failure to finance adequately: Financial Planning helps in allocating the financial and non-

financial resources effectively and efficiently for proper utilisation. It will help Clariton to focus on availability

of cash and effective utilisation of all the hard and soft assets of the business in form of intellectual property

rights or human resources. (Babajana, and Phillips, 2015) Through focussed and concentrated efforts, failure of

inadequate finance can be detected and actions can be taken to improve the situation and reverse the decision at

the initial stage of branch opening.

c.) Overtrading refers to trade affected over and above the budgeted or planned. In case of it Clariton will have

to allocate the resources effectively and convert the threat of over trading into opportunity of making higher

profits. Overtrading can be effectively managed by financial planning. Overtrading generally leads to excessive

trade payables or trade receivables therefore causing crunch of working capital (Hope, and Fraser, 2013). This

situation can be handled by financial planning of transactions and setting appropriate limits for all the

operations and functions.

2.3

a.) The Partners: In order to finance the takeover decision if the partners are approached by business it

will be a favourable decision. Partners of Clariton can finance the decision by bringing into additional capital

for long terms and utilising their personal savings, without much procedural delay and implications. Partners

can easily pinch in the capital into the business and interest on capital is to be paid on the same (Hull, 2014).

For making effective financial decisions partners need information like profitability ratio, assets value, total

liabilities, sales revenues, total employees and customers in the firm etc. By getting all these details they will

get to know the real position of the firm and accordingly then will make plan and will invest their own capital in

the business.

b.) Venture Capitalist (We Finance Limited): Venture capitalist are risk takers and always ready to

invest in innovative projects therefore venture capitalist can aid the takeover by providing financial assistance

against the share in ownership and profits in the Clariton (Ozmel, Robinson, and Stuart, 2013). Venture

10

a.) Budgeting is detailed plan to forecast expenses and incomes to be incurred in future (Board, 2015).

Budgeting is an important functions incorporated in financial planning which will assist Clariton in depicting

the expected future inflows and outflows or sales and revenue and all other financial aspects which helps the

organisation to determine the future surplus and deficit. Further Clariton is planning to open a new branch

which will have projected sales and related expenses which are to be considered in budgeting. Financial

planning is very important and supports firm in preparing budget by this way issues related to inadequacy of

funds can be minimized. It gives positive results to entities by this way unnecessary expenditures can be

minimized and firm can achieve its economic goal.

b.) Implications of failure to finance adequately: Financial Planning helps in allocating the financial and non-

financial resources effectively and efficiently for proper utilisation. It will help Clariton to focus on availability

of cash and effective utilisation of all the hard and soft assets of the business in form of intellectual property

rights or human resources. (Babajana, and Phillips, 2015) Through focussed and concentrated efforts, failure of

inadequate finance can be detected and actions can be taken to improve the situation and reverse the decision at

the initial stage of branch opening.

c.) Overtrading refers to trade affected over and above the budgeted or planned. In case of it Clariton will have

to allocate the resources effectively and convert the threat of over trading into opportunity of making higher

profits. Overtrading can be effectively managed by financial planning. Overtrading generally leads to excessive

trade payables or trade receivables therefore causing crunch of working capital (Hope, and Fraser, 2013). This

situation can be handled by financial planning of transactions and setting appropriate limits for all the

operations and functions.

2.3

a.) The Partners: In order to finance the takeover decision if the partners are approached by business it

will be a favourable decision. Partners of Clariton can finance the decision by bringing into additional capital

for long terms and utilising their personal savings, without much procedural delay and implications. Partners

can easily pinch in the capital into the business and interest on capital is to be paid on the same (Hull, 2014).

For making effective financial decisions partners need information like profitability ratio, assets value, total

liabilities, sales revenues, total employees and customers in the firm etc. By getting all these details they will

get to know the real position of the firm and accordingly then will make plan and will invest their own capital in

the business.

b.) Venture Capitalist (We Finance Limited): Venture capitalist are risk takers and always ready to

invest in innovative projects therefore venture capitalist can aid the takeover by providing financial assistance

against the share in ownership and profits in the Clariton (Ozmel, Robinson, and Stuart, 2013). Venture

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capitalist receive dividends and control over the working of the business as proposed share is 20 % which is

substantial enough to have influence on decisions of the company. Also venture capitalist will charge sitting fees

for participating in Board Meetings. Venture capitalist need information related to profit history, solvency ratio,

future income, dividend policy, cash management strategies etc. BY this way they can assume returns on their

investment. It will help them in taking better decision and they will be able to get high revenues on their

invested amount.

c.) Finance Broker: Finance Brokers are the persons who organise finance for the company financial

requirements. Once the agreement is done with financial broker company Clariton is not required to worry

about legal and procedural compliances. Everything will be taken care by financial Brokers. Finance Brokers

charge handsome amount of commission for delivering such services. In case of Clariton it is charging 1% as

broker fee for arranging loans at the rate of 2% for ten years. Further due to high competition in financial sector

Clariton will have bargaining powers to renegotiate the quotes offered. Brokers need information related to

assets and liabilities of the firm, solvency ratio, repay capacity, market worthiness, interest bearing capacity,

creditability of each partners, profitability ratio etc. By this way they will be able to make good decision.

2.4

Various financial decisions has distinct impact on the financial statements of the company. Some of them

are illustrated below:

a.) Venture capitalist (We Finance Limited): If funds are raised from Venture capitalist it will affect the

Financial Statement in a substantial manner. Share capital of the Clariton will increase therefore affecting the

Liabilities side of the Position statement of the company (Paeglis and Veeren, 2013). Venture capitalist will

earn dividends which will be affect for income of Clariton. Since it is acquiring 20% ownership it will

charge sitting fees which will be shown in Income Statement of Clariton.

b.) Finance Broker: it arranging loan at 2% for ten years. Loan will be reflected in the liabilities side of the

Position Statement of Clariton and interest thereupon as a charge against profits in the Income Statement of

Clariton. Also commission of 1% charged by finance broker will have to be reflected in Income Statement.

Commission and interest will reduce the profits of the Clariton.

TASK 3

3.1

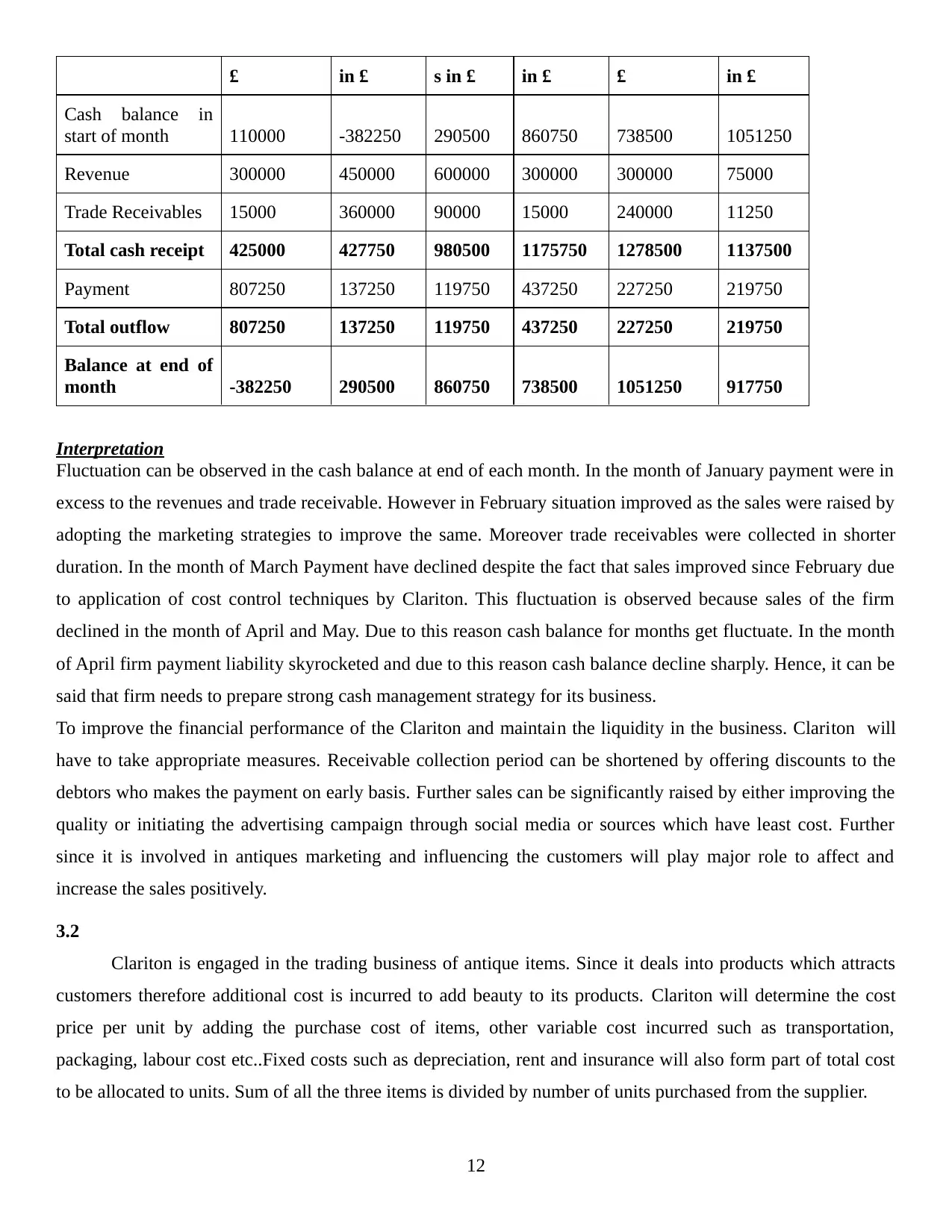

Table 1: Cash budget from January to July

Particulars January February March April May June

Amounts in Amounts Amount Amounts Amounts in Amounts

11

substantial enough to have influence on decisions of the company. Also venture capitalist will charge sitting fees

for participating in Board Meetings. Venture capitalist need information related to profit history, solvency ratio,

future income, dividend policy, cash management strategies etc. BY this way they can assume returns on their

investment. It will help them in taking better decision and they will be able to get high revenues on their

invested amount.

c.) Finance Broker: Finance Brokers are the persons who organise finance for the company financial

requirements. Once the agreement is done with financial broker company Clariton is not required to worry

about legal and procedural compliances. Everything will be taken care by financial Brokers. Finance Brokers

charge handsome amount of commission for delivering such services. In case of Clariton it is charging 1% as

broker fee for arranging loans at the rate of 2% for ten years. Further due to high competition in financial sector

Clariton will have bargaining powers to renegotiate the quotes offered. Brokers need information related to

assets and liabilities of the firm, solvency ratio, repay capacity, market worthiness, interest bearing capacity,

creditability of each partners, profitability ratio etc. By this way they will be able to make good decision.

2.4

Various financial decisions has distinct impact on the financial statements of the company. Some of them

are illustrated below:

a.) Venture capitalist (We Finance Limited): If funds are raised from Venture capitalist it will affect the

Financial Statement in a substantial manner. Share capital of the Clariton will increase therefore affecting the

Liabilities side of the Position statement of the company (Paeglis and Veeren, 2013). Venture capitalist will

earn dividends which will be affect for income of Clariton. Since it is acquiring 20% ownership it will

charge sitting fees which will be shown in Income Statement of Clariton.

b.) Finance Broker: it arranging loan at 2% for ten years. Loan will be reflected in the liabilities side of the

Position Statement of Clariton and interest thereupon as a charge against profits in the Income Statement of

Clariton. Also commission of 1% charged by finance broker will have to be reflected in Income Statement.

Commission and interest will reduce the profits of the Clariton.

TASK 3

3.1

Table 1: Cash budget from January to July

Particulars January February March April May June

Amounts in Amounts Amount Amounts Amounts in Amounts

11

£ in £ s in £ in £ £ in £

Cash balance in

start of month 110000 -382250 290500 860750 738500 1051250

Revenue 300000 450000 600000 300000 300000 75000

Trade Receivables 15000 360000 90000 15000 240000 11250

Total cash receipt 425000 427750 980500 1175750 1278500 1137500

Payment 807250 137250 119750 437250 227250 219750

Total outflow 807250 137250 119750 437250 227250 219750

Balance at end of

month -382250 290500 860750 738500 1051250 917750

Interpretation

Fluctuation can be observed in the cash balance at end of each month. In the month of January payment were in

excess to the revenues and trade receivable. However in February situation improved as the sales were raised by

adopting the marketing strategies to improve the same. Moreover trade receivables were collected in shorter

duration. In the month of March Payment have declined despite the fact that sales improved since February due

to application of cost control techniques by Clariton. This fluctuation is observed because sales of the firm

declined in the month of April and May. Due to this reason cash balance for months get fluctuate. In the month

of April firm payment liability skyrocketed and due to this reason cash balance decline sharply. Hence, it can be

said that firm needs to prepare strong cash management strategy for its business.

To improve the financial performance of the Clariton and maintain the liquidity in the business. Clariton will

have to take appropriate measures. Receivable collection period can be shortened by offering discounts to the

debtors who makes the payment on early basis. Further sales can be significantly raised by either improving the

quality or initiating the advertising campaign through social media or sources which have least cost. Further

since it is involved in antiques marketing and influencing the customers will play major role to affect and

increase the sales positively.

3.2

Clariton is engaged in the trading business of antique items. Since it deals into products which attracts

customers therefore additional cost is incurred to add beauty to its products. Clariton will determine the cost

price per unit by adding the purchase cost of items, other variable cost incurred such as transportation,

packaging, labour cost etc..Fixed costs such as depreciation, rent and insurance will also form part of total cost

to be allocated to units. Sum of all the three items is divided by number of units purchased from the supplier.

12

Cash balance in

start of month 110000 -382250 290500 860750 738500 1051250

Revenue 300000 450000 600000 300000 300000 75000

Trade Receivables 15000 360000 90000 15000 240000 11250

Total cash receipt 425000 427750 980500 1175750 1278500 1137500

Payment 807250 137250 119750 437250 227250 219750

Total outflow 807250 137250 119750 437250 227250 219750

Balance at end of

month -382250 290500 860750 738500 1051250 917750

Interpretation

Fluctuation can be observed in the cash balance at end of each month. In the month of January payment were in

excess to the revenues and trade receivable. However in February situation improved as the sales were raised by

adopting the marketing strategies to improve the same. Moreover trade receivables were collected in shorter

duration. In the month of March Payment have declined despite the fact that sales improved since February due

to application of cost control techniques by Clariton. This fluctuation is observed because sales of the firm

declined in the month of April and May. Due to this reason cash balance for months get fluctuate. In the month

of April firm payment liability skyrocketed and due to this reason cash balance decline sharply. Hence, it can be

said that firm needs to prepare strong cash management strategy for its business.

To improve the financial performance of the Clariton and maintain the liquidity in the business. Clariton will

have to take appropriate measures. Receivable collection period can be shortened by offering discounts to the

debtors who makes the payment on early basis. Further sales can be significantly raised by either improving the

quality or initiating the advertising campaign through social media or sources which have least cost. Further

since it is involved in antiques marketing and influencing the customers will play major role to affect and

increase the sales positively.

3.2

Clariton is engaged in the trading business of antique items. Since it deals into products which attracts

customers therefore additional cost is incurred to add beauty to its products. Clariton will determine the cost

price per unit by adding the purchase cost of items, other variable cost incurred such as transportation,

packaging, labour cost etc..Fixed costs such as depreciation, rent and insurance will also form part of total cost

to be allocated to units. Sum of all the three items is divided by number of units purchased from the supplier.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.