Holmes Institute HI6028 Taxation Law Assignment - T3 2019

VerifiedAdded on 2022/08/22

|11

|2600

|22

Homework Assignment

AI Summary

This taxation law assignment analyzes various aspects of Australian income tax, focusing on the taxation of an individual's income and capital gains. The assignment addresses the tax implications of salary, tips, gifts, and fringe benefits, applying relevant legislation such as the ITAA 1997 and FBTAA. It examines whether certain receipts, like tips and gifts, constitute assessable income, and differentiates between taxable and non-taxable income sources. Furthermore, the assignment delves into Capital Gains Tax (CGT), including pre-CGT assets, personal use assets, and small business concessions under Division 152. It also addresses the tax treatment of collectables and the application of CGT events. The assignment includes computations of assessable income and capital gains, providing a comprehensive understanding of the tax implications in various scenarios. The document also includes a reference list of the sources used.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................5

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................7

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................5

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................7

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

The “sec 6-5 ITA Act 1997” discusses whether the salary and other receipts the tax

payer should receive from her employer Crown Melbourne restaurant which attracts the tax

liability or not.

Rule:

The common concept of income on the basis of ordinary notion for an individual

taxpayer are described in the “sec 6-5 ITA Act 1997”. The receipts which a taxpayer earns

from their services and employment might be statutory and ordinarily assessable (Skapinker

2018). The payment which are recovered from voluntary payments are mainly rewarded for

their services and treated as ordinary earnings as ordinary employment incident takes place in

the situation. Any tips should be considered as third party gift and should be help as

voluntary payments as these are considered as paid for their services as described in “Peen v

Speiers & Pond Ltd (1908)”. It helps to establish a link between the services making it an

ordinary earnings.

Commision and services also considered as service and held as ordinary earnings.

This also includes wages, salaries bonuses fees for services. According to “Moorhouse v

Dooland (1995)” any earning of the taxpayer whether direct or indirect which is based on

their personal works can be considered as ordinary earnings (Tucker 2018). The “sec 6-5

ITAA 1997” describes the certainty of the receipts and works should be treated as ordinary

earnings or not.

Any gift or related thing should be treated as ordinary earnings which is not taxable.

“Scott v FCT (1996)” noticed that any unsolicited service which is prompted by the

Answer to question 1:

Issues:

The “sec 6-5 ITA Act 1997” discusses whether the salary and other receipts the tax

payer should receive from her employer Crown Melbourne restaurant which attracts the tax

liability or not.

Rule:

The common concept of income on the basis of ordinary notion for an individual

taxpayer are described in the “sec 6-5 ITA Act 1997”. The receipts which a taxpayer earns

from their services and employment might be statutory and ordinarily assessable (Skapinker

2018). The payment which are recovered from voluntary payments are mainly rewarded for

their services and treated as ordinary earnings as ordinary employment incident takes place in

the situation. Any tips should be considered as third party gift and should be help as

voluntary payments as these are considered as paid for their services as described in “Peen v

Speiers & Pond Ltd (1908)”. It helps to establish a link between the services making it an

ordinary earnings.

Commision and services also considered as service and held as ordinary earnings.

This also includes wages, salaries bonuses fees for services. According to “Moorhouse v

Dooland (1995)” any earning of the taxpayer whether direct or indirect which is based on

their personal works can be considered as ordinary earnings (Tucker 2018). The “sec 6-5

ITAA 1997” describes the certainty of the receipts and works should be treated as ordinary

earnings or not.

Any gift or related thing should be treated as ordinary earnings which is not taxable.

“Scott v FCT (1996)” noticed that any unsolicited service which is prompted by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

gratitude of certain services should be treated as non-taxable ordinary earnings (Walrut

2018). Other considerable factors are needed to be understood for this situation.

Under “sec 66(1), FBTAA” the employees are not needed to pay tax as it is levied on

the employer named as Fringe benefit tax. This type of tax should be levied on the

endowment of benefits and should not be on the receiver of benefits. The legislation of FBT

applicable on non-cash benefits. So, it is important to understand whether the workers are

remunerated with non-cash benefits rather than salary or not (Pinto, Kendall and Sadiq 2018).

The “sec 23L ITAA 1936” defines that the fringe benefit will always treated as non-taxable

earning where the employer provides the employee with the same. The employer bears the

liability of paying tax of any benefits given to the employee. “Indooroopily Children’s

Service v FCT (2007)” noted that any applicable benefit should be provided to the employee

during the employment stage.

Any gifts received on the special occasions which includes cash gift from the relatives

will not be treated as taxable income as it is given out of love. The personal gifts are not

treated as taxable income for the recipient as described in “FCT v Hayes (1947)”.

Application:

In this situation, Emmi is the taxpayer who is working in Crown Melbourne restaurant

on a part time basis. A customer gives her a tip of $335 in the restaurant. As per “Peen v

Speiers & Pond Ltd (1908), tips received from customer should be treated as voluntary

payment as it was paid to Emmi for her level of service to the customer (Sadiq 2018). “sec 6-

5 ITAA 1997” states that any tips received by taxpayer links with the service and it will be

treated as ordinary earnings and is taxable under this section.

In another case, Emmi received $25,000 from her part time job in the restaurant.

“Moorhouse v Dooland (1955) describes this as ordinary earnings as this income is earned

gratitude of certain services should be treated as non-taxable ordinary earnings (Walrut

2018). Other considerable factors are needed to be understood for this situation.

Under “sec 66(1), FBTAA” the employees are not needed to pay tax as it is levied on

the employer named as Fringe benefit tax. This type of tax should be levied on the

endowment of benefits and should not be on the receiver of benefits. The legislation of FBT

applicable on non-cash benefits. So, it is important to understand whether the workers are

remunerated with non-cash benefits rather than salary or not (Pinto, Kendall and Sadiq 2018).

The “sec 23L ITAA 1936” defines that the fringe benefit will always treated as non-taxable

earning where the employer provides the employee with the same. The employer bears the

liability of paying tax of any benefits given to the employee. “Indooroopily Children’s

Service v FCT (2007)” noted that any applicable benefit should be provided to the employee

during the employment stage.

Any gifts received on the special occasions which includes cash gift from the relatives

will not be treated as taxable income as it is given out of love. The personal gifts are not

treated as taxable income for the recipient as described in “FCT v Hayes (1947)”.

Application:

In this situation, Emmi is the taxpayer who is working in Crown Melbourne restaurant

on a part time basis. A customer gives her a tip of $335 in the restaurant. As per “Peen v

Speiers & Pond Ltd (1908), tips received from customer should be treated as voluntary

payment as it was paid to Emmi for her level of service to the customer (Sadiq 2018). “sec 6-

5 ITAA 1997” states that any tips received by taxpayer links with the service and it will be

treated as ordinary earnings and is taxable under this section.

In another case, Emmi received $25,000 from her part time job in the restaurant.

“Moorhouse v Dooland (1955) describes this as ordinary earnings as this income is earned

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

by Emmi directily on the basis on her service which includes personal efforts. This tip is

included as ordinary earning under “sec 6-5 ITAA 1997” as it is related with her work.

On an occasion in the restaurant, a customer gifts Emmi with a luxury perfume worth

$250. This gift are to be treated as a gift and it is non-taxable ordinary pays as it is a

Christmas gift that is given to her on personal qualities as described by “Scott v FCT

(1966)”.

An employer provides Emmi with a monthly entertainment and meal in the restaurant.

This type of benefits should be treated as fringe benefit for the taxpayer as noted in the “sec

23L ITAA 1936”. As denoted by “FC of T v Indooroopily Children’s Service (2007)” a

clear work relation with the employment can be represented by this type of benefits (Bond

and Wright 2018). The tax payer, in such cases will not require to pay tax as noted in “sec

66(1), FBTAA”. However, the employer should be liable to pay fringe benefit tax for the

entertainment and meals given to the employee as described under “Sec 23L ITAA 1936”.

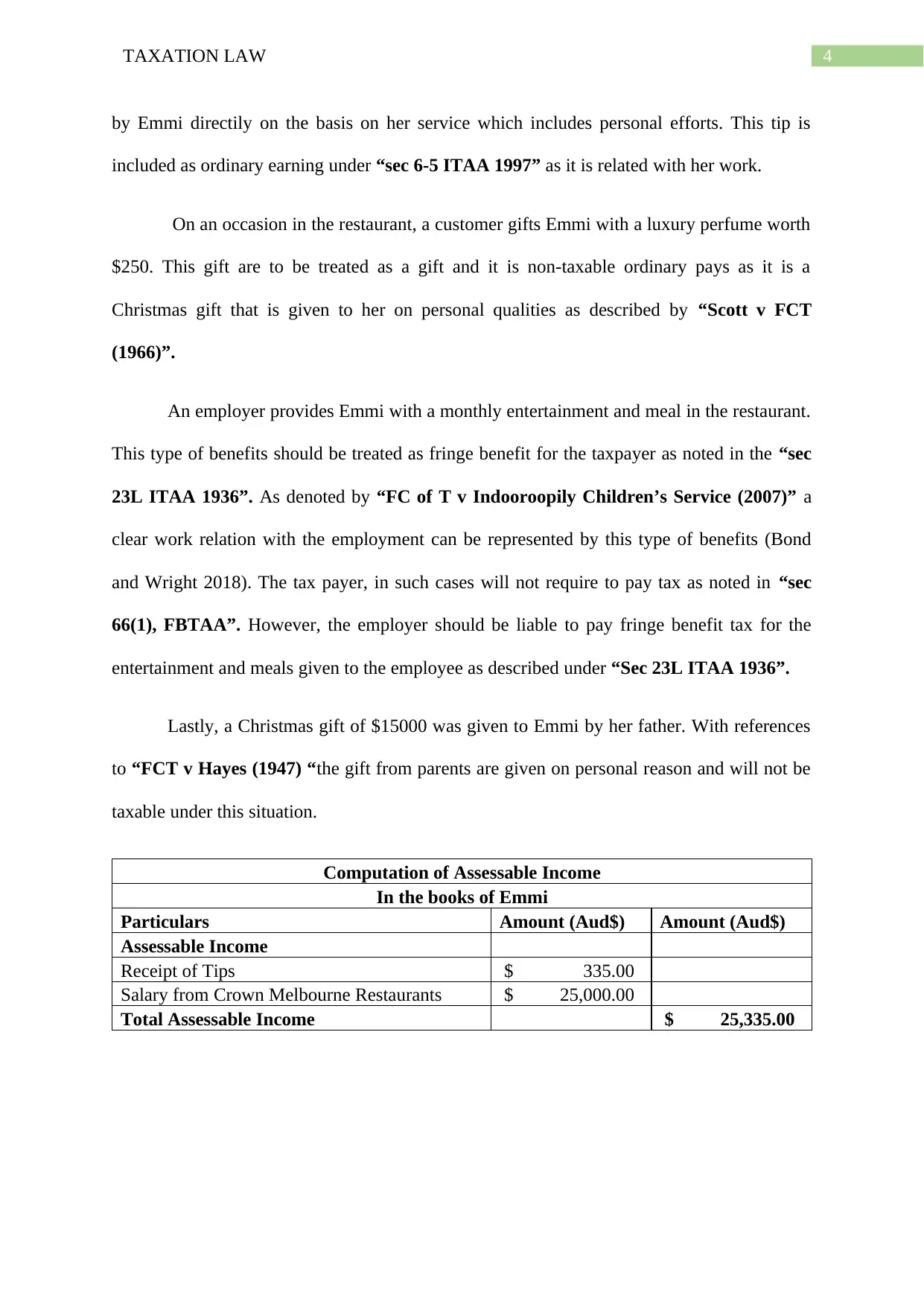

Lastly, a Christmas gift of $15000 was given to Emmi by her father. With references

to “FCT v Hayes (1947) “the gift from parents are given on personal reason and will not be

taxable under this situation.

Computation of Assessable Income

In the books of Emmi

Particulars Amount (Aud$) Amount (Aud$)

Assessable Income

Receipt of Tips $ 335.00

Salary from Crown Melbourne Restaurants $ 25,000.00

Total Assessable Income $ 25,335.00

by Emmi directily on the basis on her service which includes personal efforts. This tip is

included as ordinary earning under “sec 6-5 ITAA 1997” as it is related with her work.

On an occasion in the restaurant, a customer gifts Emmi with a luxury perfume worth

$250. This gift are to be treated as a gift and it is non-taxable ordinary pays as it is a

Christmas gift that is given to her on personal qualities as described by “Scott v FCT

(1966)”.

An employer provides Emmi with a monthly entertainment and meal in the restaurant.

This type of benefits should be treated as fringe benefit for the taxpayer as noted in the “sec

23L ITAA 1936”. As denoted by “FC of T v Indooroopily Children’s Service (2007)” a

clear work relation with the employment can be represented by this type of benefits (Bond

and Wright 2018). The tax payer, in such cases will not require to pay tax as noted in “sec

66(1), FBTAA”. However, the employer should be liable to pay fringe benefit tax for the

entertainment and meals given to the employee as described under “Sec 23L ITAA 1936”.

Lastly, a Christmas gift of $15000 was given to Emmi by her father. With references

to “FCT v Hayes (1947) “the gift from parents are given on personal reason and will not be

taxable under this situation.

Computation of Assessable Income

In the books of Emmi

Particulars Amount (Aud$) Amount (Aud$)

Assessable Income

Receipt of Tips $ 335.00

Salary from Crown Melbourne Restaurants $ 25,000.00

Total Assessable Income $ 25,335.00

5TAXATION LAW

Conclusion:

As described under “sec 6-5 ITAA 1997” the income and receipt of $25000 received

from Crown Melbourne restaurants will be included in the taxable income of Emmi as it is

received from her employment and it is an ordinary income. Emmi will not require to pay any

tax for the entertainment and meals. This should be treated as fringe benefit. Any gifts

received by Emmi will not be taxable under ordinary income as it is purely voluntary and

based on her personal grounds.

Answer to question 2:

Answer A:

CGT has primary objective to recognize the CGT budget and its sale as soon as the

“CGT event A1” occurs. The assets which are purchased on or following 20th September

1985 is applied by CGT which is its basic feature (Slater and Bishop 2018). The assets which

are acquired before is referred as pre-CGT asset which is acquired by the taxpayer. This type

of assets are taxable for CGT purpose as described by ATO.

Any residency that are generating income should be taxable .The residency of Liu

should be exempted from tax as long as it is not used to produce any income and is the main

residence of the taxpayer as described under “sec 118-110 ITAA 1997”.

Liu, a taxpayer sold her house which she resided as her main residence from 1981.

She sold the house for $630,000 which she purchased for $55,000. In this case, the house of

the taxpayer should be levied from tax under “sec 118-110” as it was used as main residence

(Šinkūnienė 2015). This house is a pre-CGT asset as Liu purchased it before 20th September

1985 and the capital gains made from selling pre-CGT assets are exempted from tax.

Conclusion:

As described under “sec 6-5 ITAA 1997” the income and receipt of $25000 received

from Crown Melbourne restaurants will be included in the taxable income of Emmi as it is

received from her employment and it is an ordinary income. Emmi will not require to pay any

tax for the entertainment and meals. This should be treated as fringe benefit. Any gifts

received by Emmi will not be taxable under ordinary income as it is purely voluntary and

based on her personal grounds.

Answer to question 2:

Answer A:

CGT has primary objective to recognize the CGT budget and its sale as soon as the

“CGT event A1” occurs. The assets which are purchased on or following 20th September

1985 is applied by CGT which is its basic feature (Slater and Bishop 2018). The assets which

are acquired before is referred as pre-CGT asset which is acquired by the taxpayer. This type

of assets are taxable for CGT purpose as described by ATO.

Any residency that are generating income should be taxable .The residency of Liu

should be exempted from tax as long as it is not used to produce any income and is the main

residence of the taxpayer as described under “sec 118-110 ITAA 1997”.

Liu, a taxpayer sold her house which she resided as her main residence from 1981.

She sold the house for $630,000 which she purchased for $55,000. In this case, the house of

the taxpayer should be levied from tax under “sec 118-110” as it was used as main residence

(Šinkūnienė 2015). This house is a pre-CGT asset as Liu purchased it before 20th September

1985 and the capital gains made from selling pre-CGT assets are exempted from tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer B:

CGT event must be on application on any type of capital gains. As described under

“sec 104-10 (1) ITAA 1997” on the basis of “CGT Event A1” deals with any asset inclined

by the tax payer. The “Subdivision 108-C” acts with the assets which are used personally.

According to the “sec 108-20 (2) & (3) ITAA 1997”, any asset which is held by the taxpayer

for the purpose of personal use are known as personal use asset (Rohatgi 2015). Certain

examples of personal use assets can be boats, household premises and motor vehicles or any

items that is used by the taxpayer for personal use. Any amount of capital loss on the use of

personal asset are exempted under “sec-108-20 (1) ITAA 1997”.

Liu purchased a car in the year 2011 for $37,000 which she sold for $8,000 in the

present year. Car is used in personal purpose therefore it is a personal asset which goes under

“sec-108-20 (2) & (3) ITAA 1997”. The sale of car resulted in a capital loss by Liu which is

resulted in “CGT Event A1” under “sec-104-10 (1) ITAA 1997 and classified as the loss

from use of personal asset which is levied under “sec-108-20 (1) ITAA 1997”.

Answer C:

“Division 152 of the ITAA 1997” provides the small businesses with some concession

thereby assisting them to get relief from capital gains (Hildreth 2019). The basic concessions

given by this division are given below

1. When the age of taxpayer is above 55 years, a “15-year exemption” are given from

capital gains when selling the asset held for more than 15 years.

2. 50% reduction are given in capital gains to the qualifying taxpayer in this section.

They can reduce their capital gains by 50% by following the deduction (Miller and

Oats 2016).

Answer B:

CGT event must be on application on any type of capital gains. As described under

“sec 104-10 (1) ITAA 1997” on the basis of “CGT Event A1” deals with any asset inclined

by the tax payer. The “Subdivision 108-C” acts with the assets which are used personally.

According to the “sec 108-20 (2) & (3) ITAA 1997”, any asset which is held by the taxpayer

for the purpose of personal use are known as personal use asset (Rohatgi 2015). Certain

examples of personal use assets can be boats, household premises and motor vehicles or any

items that is used by the taxpayer for personal use. Any amount of capital loss on the use of

personal asset are exempted under “sec-108-20 (1) ITAA 1997”.

Liu purchased a car in the year 2011 for $37,000 which she sold for $8,000 in the

present year. Car is used in personal purpose therefore it is a personal asset which goes under

“sec-108-20 (2) & (3) ITAA 1997”. The sale of car resulted in a capital loss by Liu which is

resulted in “CGT Event A1” under “sec-104-10 (1) ITAA 1997 and classified as the loss

from use of personal asset which is levied under “sec-108-20 (1) ITAA 1997”.

Answer C:

“Division 152 of the ITAA 1997” provides the small businesses with some concession

thereby assisting them to get relief from capital gains (Hildreth 2019). The basic concessions

given by this division are given below

1. When the age of taxpayer is above 55 years, a “15-year exemption” are given from

capital gains when selling the asset held for more than 15 years.

2. 50% reduction are given in capital gains to the qualifying taxpayer in this section.

They can reduce their capital gains by 50% by following the deduction (Miller and

Oats 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

3. “Retirement concessions” allows to neglect the capital gains from CGT asset valued

up to $500,000 providing the proceeds that are used in retirement concession.

4. “Roll-over relief” allows the taxpayers to defer the capital gain when purchasing any

replacement asset.

When a business is ceased permanently, “CGT event C1” happens to the business

goodwill. Business goodwill comes up when the business ends their operation due to loss or

destruction of their business (Whittington 2015). Business goodwill can also come up when

the business in closed permanently.

Liu, who was running a photography business, retires from it and sells it for $125,000. It

includes photography equipment worth $53,000 and goodwill worth $50.000. Retirement

concession are eligible for Liu as her capital gains are below $500,000. Liu can also obtain a

15 year exemption as she is aged 65 years for her business goodwill and equipment as the

statutory limit for this exemption is 55 years.

Answer D:

During the year, Liu also sold her furniture worth $4,800 and each of her furniture is

costs less than $2,000. Any capital gain from the sale of asset should be ignored if the value

of the asset is less than $10,000 as noted under “sec 118-10 ITAA 1997”.

Answer E:

Any asset taken for private purpose and enjoyment should be treated as collectables

under “Subdivision 108-B” (Coleman et al. 2018). This can include any jewellery, painting,

stamps and coins. Any assets or collectables which cost less than $500 should be ignored

under “sec 118-10(1)”.

3. “Retirement concessions” allows to neglect the capital gains from CGT asset valued

up to $500,000 providing the proceeds that are used in retirement concession.

4. “Roll-over relief” allows the taxpayers to defer the capital gain when purchasing any

replacement asset.

When a business is ceased permanently, “CGT event C1” happens to the business

goodwill. Business goodwill comes up when the business ends their operation due to loss or

destruction of their business (Whittington 2015). Business goodwill can also come up when

the business in closed permanently.

Liu, who was running a photography business, retires from it and sells it for $125,000. It

includes photography equipment worth $53,000 and goodwill worth $50.000. Retirement

concession are eligible for Liu as her capital gains are below $500,000. Liu can also obtain a

15 year exemption as she is aged 65 years for her business goodwill and equipment as the

statutory limit for this exemption is 55 years.

Answer D:

During the year, Liu also sold her furniture worth $4,800 and each of her furniture is

costs less than $2,000. Any capital gain from the sale of asset should be ignored if the value

of the asset is less than $10,000 as noted under “sec 118-10 ITAA 1997”.

Answer E:

Any asset taken for private purpose and enjoyment should be treated as collectables

under “Subdivision 108-B” (Coleman et al. 2018). This can include any jewellery, painting,

stamps and coins. Any assets or collectables which cost less than $500 should be ignored

under “sec 118-10(1)”.

8TAXATION LAW

Liu sold all of her paintings for $28,000 which has cost base less than $500. This

paintings are stated as collectable under “sec 108-10 (2) & (3) ITAA 1997” (Woellner et al.

2016). With reference to “sec 119-10 (1)” are levied from tax as most of her paintings costs

less than $500. One of Liu’s painting costs $1,000 which she sold for $8,000. The painting

will be taxable under “sec 102-5 ITAA 1997”.

Computation of Capital Gains

Particulars Amount ($)

Net capital gain on disposal of painting

CGT event A1 (“Sec 104-10 (1))”

Sales Proceeds 8,000

Element 1- Cost of Acquisition (“Sec 110-25 (1), ITAA 1997”)

Cost base 1,000

Gross capital gain (proceeds less cost base) 7,000

50% CGT Discount 3,500

Taxable Capital Gains 3,500

Liu sold all of her paintings for $28,000 which has cost base less than $500. This

paintings are stated as collectable under “sec 108-10 (2) & (3) ITAA 1997” (Woellner et al.

2016). With reference to “sec 119-10 (1)” are levied from tax as most of her paintings costs

less than $500. One of Liu’s painting costs $1,000 which she sold for $8,000. The painting

will be taxable under “sec 102-5 ITAA 1997”.

Computation of Capital Gains

Particulars Amount ($)

Net capital gain on disposal of painting

CGT event A1 (“Sec 104-10 (1))”

Sales Proceeds 8,000

Element 1- Cost of Acquisition (“Sec 110-25 (1), ITAA 1997”)

Cost base 1,000

Gross capital gain (proceeds less cost base) 7,000

50% CGT Discount 3,500

Taxable Capital Gains 3,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Bond, D. and Wright, A., 2018. A Snapshot of the Australian Taxpayer. Australian

Accounting Review, 28(4), pp.598–615.

Coleman, C., Hanegbi, R., Hart, G., Jogarajan, S., Krever, R., McLaren, J., Obst, W. and

Sadiq, K., 2018. Principles of taxation law. THE AUSTRALIAN TAFE TEACHER.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Pinto, D., Kendall, K. and Sadiq, K., 2018. Fundamental tax legislation 2018 Twenty-sixth.,

Rohatgi, R., 2015. Basic international taxation (Vol. 1). Richmond Law & Tax.

Sadiq, K. et al., 2018. Principles of taxation law 2018 11th ed.,

Šinkūnienė, K., 2015. Taxation principles in tax culture: theoretical and practical

aspects. Organizacijų vadyba: sisteminiai tyrimai, (35), pp.177-192.

Skapinker, D, 2018. Property: 2018 NSW contract for sale and purchase of land and the 'GST

at settlement' measure. LSJ: Law Society of NSW Journal, (45), pp.76–79.

Slater, T. and Bishop, E., 2018. Taxation of Settlements, Judgments and Awards. Australian

Law Journal, 92(8), pp.602–618.

Tucker, J, 2018. Tax changes for developers of new residential property. BULLETIN (LAW

SOCIETY OF S.A.), 40(2), p.41.

Walrut, B, 2018. Tax files: New surcharge duty on foreign acquisitions. Bulletin (Law

Society of South Australia), 40(1), pp.43–45.

References:

Bond, D. and Wright, A., 2018. A Snapshot of the Australian Taxpayer. Australian

Accounting Review, 28(4), pp.598–615.

Coleman, C., Hanegbi, R., Hart, G., Jogarajan, S., Krever, R., McLaren, J., Obst, W. and

Sadiq, K., 2018. Principles of taxation law. THE AUSTRALIAN TAFE TEACHER.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Pinto, D., Kendall, K. and Sadiq, K., 2018. Fundamental tax legislation 2018 Twenty-sixth.,

Rohatgi, R., 2015. Basic international taxation (Vol. 1). Richmond Law & Tax.

Sadiq, K. et al., 2018. Principles of taxation law 2018 11th ed.,

Šinkūnienė, K., 2015. Taxation principles in tax culture: theoretical and practical

aspects. Organizacijų vadyba: sisteminiai tyrimai, (35), pp.177-192.

Skapinker, D, 2018. Property: 2018 NSW contract for sale and purchase of land and the 'GST

at settlement' measure. LSJ: Law Society of NSW Journal, (45), pp.76–79.

Slater, T. and Bishop, E., 2018. Taxation of Settlements, Judgments and Awards. Australian

Law Journal, 92(8), pp.602–618.

Tucker, J, 2018. Tax changes for developers of new residential property. BULLETIN (LAW

SOCIETY OF S.A.), 40(2), p.41.

Walrut, B, 2018. Tax files: New surcharge duty on foreign acquisitions. Bulletin (Law

Society of South Australia), 40(1), pp.43–45.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Whittington, G., 2015. Tax policy and accounting standards. Taxation: Critical Perspectives

on the World Economy, 2, p.394.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian taxation

law. CCH Australia.

Whittington, G., 2015. Tax policy and accounting standards. Taxation: Critical Perspectives

on the World Economy, 2, p.394.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian taxation

law. CCH Australia.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.