Holmes Institute HI6028 Taxation Law Assignment: Tax Law Analysis

VerifiedAdded on 2022/09/18

|11

|2573

|24

Homework Assignment

AI Summary

This assignment analyzes taxation law principles, focusing on GST and CGT, and their application in real-world scenarios. The first part of the assignment examines whether a taxpayer can claim an input tax credit under the GST Act, specifically considering the attribution of tax credits for the purchase of land and associated legal services. The second part assesses the tax implications of various transactions, including the sale of land, shares, stamps, and a grand piano, evaluating the applicability of CGT and relevant deductions, such as cost base calculations, capital gains, and losses. The analysis includes relevant case law and legislation to support the conclusions. The assignment aims to demonstrate an understanding of the Australian income tax system and the ability to apply tax principles to complex scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

Will the taxpayer be permitted to claim the input tax credit from the creditable

purchase under “subsection 29-10 (1) of the GSTR 1999”?

Rule:

The “GSTR Ruling of 2000/28” is mainly dealing with the attribution of the Goods

and Service Tax (GST) payable or the input tax credit under the “Goods and Service Tax Act

1999” originating from the sale of land under the standard agreement of the land (McCluskey

and Franzsen 2017). Attribution refers to the term that is used under the GST law for

describing the manner in which the account for the GST is payable on the assessable supplies

and tax credit for the creditable purchase. A taxpayer attributes all the input tax credit for the

creditable acquisition to the previous tax years where they deliver any kind of consideration

or the invoice that is issued relating to the purchase (Li and Stathis 2017). If the taxpayer

maintains his books for GST on the cash basis, the taxpayer attributes the GST payable on the

taxable supply for the tax year in which the considerations for the supply is obtained but only

up to the extent that the consideration is received during the tax period.

A taxpayer attributes the input tax credit to the tax year where the taxpayer provides

the consideration for the acquisition but only up to the degree that the taxpayer provided the

consideration during that tax period. Importantly, under the “subsection 29-10 (1)” the

taxpayers are allowed to claim the tax credit relating to the creditable transaction under the

standard contract of land that is attributable to the period of tax in which the taxpayers deliver

any kind of consideration for the purchase (Thuronyi and Brooks 2016). “Subsection 29-10”

also states that a taxpayer is permitted to claim the tax credit for the creditable transaction if

Answer to question 1:

Issues:

Will the taxpayer be permitted to claim the input tax credit from the creditable

purchase under “subsection 29-10 (1) of the GSTR 1999”?

Rule:

The “GSTR Ruling of 2000/28” is mainly dealing with the attribution of the Goods

and Service Tax (GST) payable or the input tax credit under the “Goods and Service Tax Act

1999” originating from the sale of land under the standard agreement of the land (McCluskey

and Franzsen 2017). Attribution refers to the term that is used under the GST law for

describing the manner in which the account for the GST is payable on the assessable supplies

and tax credit for the creditable purchase. A taxpayer attributes all the input tax credit for the

creditable acquisition to the previous tax years where they deliver any kind of consideration

or the invoice that is issued relating to the purchase (Li and Stathis 2017). If the taxpayer

maintains his books for GST on the cash basis, the taxpayer attributes the GST payable on the

taxable supply for the tax year in which the considerations for the supply is obtained but only

up to the extent that the consideration is received during the tax period.

A taxpayer attributes the input tax credit to the tax year where the taxpayer provides

the consideration for the acquisition but only up to the degree that the taxpayer provided the

consideration during that tax period. Importantly, under the “subsection 29-10 (1)” the

taxpayers are allowed to claim the tax credit relating to the creditable transaction under the

standard contract of land that is attributable to the period of tax in which the taxpayers deliver

any kind of consideration for the purchase (Thuronyi and Brooks 2016). “Subsection 29-10”

also states that a taxpayer is permitted to claim the tax credit for the creditable transaction if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

prior to they provide any form of consideration or issues the invoice associated to the

acquisition.

The taxpayers should denote that the tax treatment relating to the land and the

proceeds that are obtained from the sale of land is usually reliant on whether it is treated as

the capital asset or regarded as the subject of business or the commercial transaction

(Mangioni 2015). For CGT purpose, vacant land is usually viewed as the capital asset that are

subjected to the CGT. Nevertheless, if the land is transaction and it is undertaken as the part

of the business activity, the sales proceeds may be treated as the ordinary earnings and may

attract GST.

Application:

The case study highlights that City Sky Co is the property investment company that

has recently bought a vacant piece of land for the purpose of building 15 apartments to sell.

The company also engaged in the service of local lawyer Maurice Blackburn for providing

the legal services needed for the development and paid $33,000 for the service. The land

bought by City Sky Co will be considered as the subject of business or commercial

transaction. The land transaction undertaken by the City Sky Co as the part of business

activity and any sales proceeds will be viewed as the ordinary returns for the company and

will be subjected to GST.

City Sky Co with respect to the “subsection 29-10 (1) of the GSTR 1999” will be

attributable for the tax credit for the current tax year since the transaction of purchase was

entered into by the company in consideration for the acquisition (McCluskey 2018).

However, City Sky Co will only be allowed to obtain the tax credit up to the extent of

consideration delivered by the company for the present tax period.

prior to they provide any form of consideration or issues the invoice associated to the

acquisition.

The taxpayers should denote that the tax treatment relating to the land and the

proceeds that are obtained from the sale of land is usually reliant on whether it is treated as

the capital asset or regarded as the subject of business or the commercial transaction

(Mangioni 2015). For CGT purpose, vacant land is usually viewed as the capital asset that are

subjected to the CGT. Nevertheless, if the land is transaction and it is undertaken as the part

of the business activity, the sales proceeds may be treated as the ordinary earnings and may

attract GST.

Application:

The case study highlights that City Sky Co is the property investment company that

has recently bought a vacant piece of land for the purpose of building 15 apartments to sell.

The company also engaged in the service of local lawyer Maurice Blackburn for providing

the legal services needed for the development and paid $33,000 for the service. The land

bought by City Sky Co will be considered as the subject of business or commercial

transaction. The land transaction undertaken by the City Sky Co as the part of business

activity and any sales proceeds will be viewed as the ordinary returns for the company and

will be subjected to GST.

City Sky Co with respect to the “subsection 29-10 (1) of the GSTR 1999” will be

attributable for the tax credit for the current tax year since the transaction of purchase was

entered into by the company in consideration for the acquisition (McCluskey 2018).

However, City Sky Co will only be allowed to obtain the tax credit up to the extent of

consideration delivered by the company for the present tax period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

As City Sky Co is registered for the GST, it is attributable to the tax credit for the

creditable purchase of vacant land in regard to the complete regular land deal for the tax year

in which the settlement occurred (Christians 2016). Furthermore, under the “subsection 29-

10 (1)”, City Sky Co is entitled to the tax credit for the creditable procurement under the

standard land agreement since it is attributable to the tax year in which the company provided

the consideration for the acquisition.

The company being registered for GST should include the GST in the price of land.

Subject to the normal rules of the GST, City Sky Co is allowed to claim the tax credit for the

amount of GST that is contained within in the price of vacant land of its business purchase.

As the business intends to build apartments and sell it, the company will be making a

taxable supply. This implies that City Sky Co is permitted to claim the GST credits or the

input tax credits during the tax period for all the considerations of the creditable acquisition

that is attributable for that period.

Conclusion:

The analysis performed above suggest that under the subsection 29-10 (1), City Sky

Co has attributed the input tax credit for the taxation period during which the company

provided its consideration for the creditable acquisition. However, it will only be allowed to

the tax credit till the extent it has provided consideration during that tax period.

Answer to question 2:

Sale of a block of land for $1,000,000:

A taxpayer is entitled to deduction for the certain outgoings that are occurred on the

investment property. However, there are certain categories of investment property expenses

that are non-permissible as deduction. This includes the acquisition and the disposal costs

As City Sky Co is registered for the GST, it is attributable to the tax credit for the

creditable purchase of vacant land in regard to the complete regular land deal for the tax year

in which the settlement occurred (Christians 2016). Furthermore, under the “subsection 29-

10 (1)”, City Sky Co is entitled to the tax credit for the creditable procurement under the

standard land agreement since it is attributable to the tax year in which the company provided

the consideration for the acquisition.

The company being registered for GST should include the GST in the price of land.

Subject to the normal rules of the GST, City Sky Co is allowed to claim the tax credit for the

amount of GST that is contained within in the price of vacant land of its business purchase.

As the business intends to build apartments and sell it, the company will be making a

taxable supply. This implies that City Sky Co is permitted to claim the GST credits or the

input tax credits during the tax period for all the considerations of the creditable acquisition

that is attributable for that period.

Conclusion:

The analysis performed above suggest that under the subsection 29-10 (1), City Sky

Co has attributed the input tax credit for the taxation period during which the company

provided its consideration for the creditable acquisition. However, it will only be allowed to

the tax credit till the extent it has provided consideration during that tax period.

Answer to question 2:

Sale of a block of land for $1,000,000:

A taxpayer is entitled to deduction for the certain outgoings that are occurred on the

investment property. However, there are certain categories of investment property expenses

that are non-permissible as deduction. This includes the acquisition and the disposal costs

5TAXATION LAW

occurred for the property (Oates and Schwab 2015). A taxpayer is not permitted to obtain

deduction for the cost of acquiring or selling the property. The examples of this outgoings

includes the purchase price of the property, stamp duty and other incidental costs.

Nevertheless, these costs may be treated as the cost base of the property for the CGT purpose.

A taxpayer may make the capital gains or loss when they dispose the property which

they have bought following 1985. The cost base and reduced cost base of the property

comprises of the amount that a taxpayer pay when they pay for the property along with the

certain type of incidental costs related with purchasing the property, acquiring, holding and

selling the property (Gitman, Juchau and Flanagan 2015). The cost base can be defined as the

total cost that are related with the CGT asset. “Sec 110-25(1), ITAA 1997” explains that the

cost base of items comprises of the five elements.

Emma here purchased a land for the investment purpose in 1991. The purchase price

of the land was $250,000 which also includes the certain incidental costs related to the

purchase of investment property. Emma while purchasing the property incurred stamp duty

and legal fees in purchase (Tran 2015). The stamp duty and legal fees should be classified

under “section 110-25 (1), ITAA 1997” as the incidental cost of acquisition of land under the

2nd Element of cost base item.

To fund the purchase Emma took loan and paid a total amount of interest amounting

to $32,000. The third element of the cost base or property includes the non-capital ownership

cost of assets that are acquired following 20 August 1991. This includes the interest, rates,

repairs and land tax. The interest on loan paid by Emma to fund the purchase of investment

property will be included into the cost base of land for CGT purpose as the non-capital cost

of ownership for the asset.

occurred for the property (Oates and Schwab 2015). A taxpayer is not permitted to obtain

deduction for the cost of acquiring or selling the property. The examples of this outgoings

includes the purchase price of the property, stamp duty and other incidental costs.

Nevertheless, these costs may be treated as the cost base of the property for the CGT purpose.

A taxpayer may make the capital gains or loss when they dispose the property which

they have bought following 1985. The cost base and reduced cost base of the property

comprises of the amount that a taxpayer pay when they pay for the property along with the

certain type of incidental costs related with purchasing the property, acquiring, holding and

selling the property (Gitman, Juchau and Flanagan 2015). The cost base can be defined as the

total cost that are related with the CGT asset. “Sec 110-25(1), ITAA 1997” explains that the

cost base of items comprises of the five elements.

Emma here purchased a land for the investment purpose in 1991. The purchase price

of the land was $250,000 which also includes the certain incidental costs related to the

purchase of investment property. Emma while purchasing the property incurred stamp duty

and legal fees in purchase (Tran 2015). The stamp duty and legal fees should be classified

under “section 110-25 (1), ITAA 1997” as the incidental cost of acquisition of land under the

2nd Element of cost base item.

To fund the purchase Emma took loan and paid a total amount of interest amounting

to $32,000. The third element of the cost base or property includes the non-capital ownership

cost of assets that are acquired following 20 August 1991. This includes the interest, rates,

repairs and land tax. The interest on loan paid by Emma to fund the purchase of investment

property will be included into the cost base of land for CGT purpose as the non-capital cost

of ownership for the asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

A dispute occurred in 2015 where Emma was required to pay the legal fees of $5000

in resolving the dispute. The fifth element of the cost of base item is usually concerned with

the capital expenses that are occurred in establishing, preserving and defending the title of the

assets (Freebairn 2016). The legal fees that is occurred by Emma for the disputed with

neighbour will form the part of the assets cost base. The legal fees are a capital expenditure

that is occurred in establishing, preserving and defending the title of asset by Emma.

Before putting the property for sale in the market Emma occurred a sum of $27,500

for removing the pine trees which were on the land. Under “sec 110-25(1)”, the sum of

$27,500 occurred by Emma should be regarded as the capital enhancement cost under 5th

Element of cost base item that is mainly occurred in increasing the value of land.

The above stated costs forms the part of the cost base items of property for CGT

purpose and it is included in computing the capital gains tax for Emma.

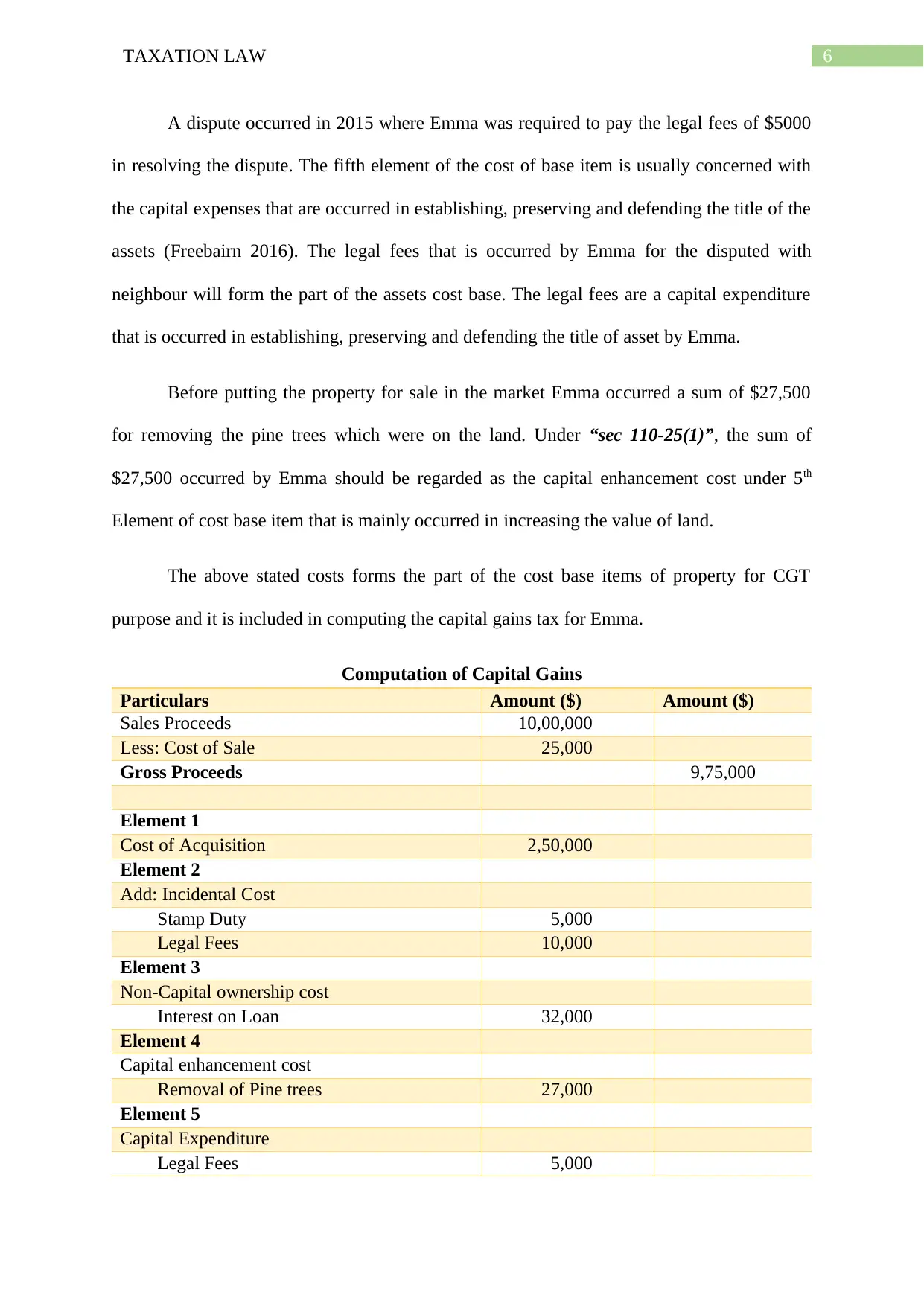

Computation of Capital Gains

Particulars Amount ($) Amount ($)

Sales Proceeds 10,00,000

Less: Cost of Sale 25,000

Gross Proceeds 9,75,000

Element 1

Cost of Acquisition 2,50,000

Element 2

Add: Incidental Cost

Stamp Duty 5,000

Legal Fees 10,000

Element 3

Non-Capital ownership cost

Interest on Loan 32,000

Element 4

Capital enhancement cost

Removal of Pine trees 27,000

Element 5

Capital Expenditure

Legal Fees 5,000

A dispute occurred in 2015 where Emma was required to pay the legal fees of $5000

in resolving the dispute. The fifth element of the cost of base item is usually concerned with

the capital expenses that are occurred in establishing, preserving and defending the title of the

assets (Freebairn 2016). The legal fees that is occurred by Emma for the disputed with

neighbour will form the part of the assets cost base. The legal fees are a capital expenditure

that is occurred in establishing, preserving and defending the title of asset by Emma.

Before putting the property for sale in the market Emma occurred a sum of $27,500

for removing the pine trees which were on the land. Under “sec 110-25(1)”, the sum of

$27,500 occurred by Emma should be regarded as the capital enhancement cost under 5th

Element of cost base item that is mainly occurred in increasing the value of land.

The above stated costs forms the part of the cost base items of property for CGT

purpose and it is included in computing the capital gains tax for Emma.

Computation of Capital Gains

Particulars Amount ($) Amount ($)

Sales Proceeds 10,00,000

Less: Cost of Sale 25,000

Gross Proceeds 9,75,000

Element 1

Cost of Acquisition 2,50,000

Element 2

Add: Incidental Cost

Stamp Duty 5,000

Legal Fees 10,000

Element 3

Non-Capital ownership cost

Interest on Loan 32,000

Element 4

Capital enhancement cost

Removal of Pine trees 27,000

Element 5

Capital Expenditure

Legal Fees 5,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Total Cost Base 3,29,000

Capital Gains 6,46,000

50% CGT Discount 3,23,000

Net Capital Gains 3,23,000

Sale of Emma’s 1000 shares in Rio Tinto:

A person may make capital gains or capital loss when they sell the rental property that

they have purchased following 20th September 1985. The regimes of the capital gains tax

(CGT) began on 20th September 1985. Accordingly, “sec 100-25 (1) of the ITAA 1997”

restricts the assets to which the provision of CGT is applied for the assets purchased on or

following 20 September 1985 (Burkhauser, Hahn and Wilkins 2015). Assets that are

purchased before the 20th September 1985 are classified as the pre-CGT asset and the gains

made from that asset is not taxed under the CGT regime.

Emma here purchased 1000 shares in Rio Tinto for $3.5 in 1982. The shares were

eventually sold by Emma for $50.85. The shares will be classified as the pre-CGT asset

because they were purchased before the introduction of the CGT regime. As only real gains

are taxed under the regime of CGT, the gains made from the sale of Rio Tinto will be

excluded from CGT.

Sale of Stamp:

As per “sec 108-10 (2) of the ITAA 1997”, collectable is referred as the items that are

used or kept by taxpayer for private enjoyment (Evans, Minas and Lim 2015). Collectables

generally includes the following

a. Antiques

b. Works of art

Total Cost Base 3,29,000

Capital Gains 6,46,000

50% CGT Discount 3,23,000

Net Capital Gains 3,23,000

Sale of Emma’s 1000 shares in Rio Tinto:

A person may make capital gains or capital loss when they sell the rental property that

they have purchased following 20th September 1985. The regimes of the capital gains tax

(CGT) began on 20th September 1985. Accordingly, “sec 100-25 (1) of the ITAA 1997”

restricts the assets to which the provision of CGT is applied for the assets purchased on or

following 20 September 1985 (Burkhauser, Hahn and Wilkins 2015). Assets that are

purchased before the 20th September 1985 are classified as the pre-CGT asset and the gains

made from that asset is not taxed under the CGT regime.

Emma here purchased 1000 shares in Rio Tinto for $3.5 in 1982. The shares were

eventually sold by Emma for $50.85. The shares will be classified as the pre-CGT asset

because they were purchased before the introduction of the CGT regime. As only real gains

are taxed under the regime of CGT, the gains made from the sale of Rio Tinto will be

excluded from CGT.

Sale of Stamp:

As per “sec 108-10 (2) of the ITAA 1997”, collectable is referred as the items that are

used or kept by taxpayer for private enjoyment (Evans, Minas and Lim 2015). Collectables

generally includes the following

a. Antiques

b. Works of art

8TAXATION LAW

c. Rare stamps

d. Jewellery

e. Manuscripts

Capital loss that is suffered by the taxpayers from the sale of collectables is only

allowed for offset when a capital gain from the collectables are made.

In the same way, Emma sold the collection of stamps purchased from the private

collector in 2015 for 60,000. Emma could only fetch $50,000 from the sales. Accordingly,

under “sec 108-10 (2)”, Emma’s collection of stamps has been classified as the collectable’s.

As the sale of stamps has resulted in capital loss, Emma can either quarantined the capital

loss or is she is allowed offset the loss from the other collectables. As no other capital gains

has been reported by Emma from the collectables, she can carry forward it to subsequent

years.

Sale of grand piano for $30,000:

“Section 108-20 ITAA 1997” defines the personal use asset. These assets are treated

as the CGT assets apart from the collectables which is mainly used or kept by the taxpayer

for their own enjoyment and usage (Li and Stathis 2017). The examples of this assets

includes the race horses, furniture, electrical items and household items. Notably under “sec

108-20 (1) ITAA 1997”, taxpayers are required to simply ignore the capital loss that arise

from the sale of the personal use asset.

A grand piano was initially bought by Emma for $80,000 but was sold for $80,000 in

2020. As understood, the piano ought to be treated as the personal use asset under “sec 108-

20, ITAA 1997”. The capital loss that Emma has occurred from the disposal of a grand piano

will be simply ignored under the “sec 108-20 (1), ITAA 1997”.

c. Rare stamps

d. Jewellery

e. Manuscripts

Capital loss that is suffered by the taxpayers from the sale of collectables is only

allowed for offset when a capital gain from the collectables are made.

In the same way, Emma sold the collection of stamps purchased from the private

collector in 2015 for 60,000. Emma could only fetch $50,000 from the sales. Accordingly,

under “sec 108-10 (2)”, Emma’s collection of stamps has been classified as the collectable’s.

As the sale of stamps has resulted in capital loss, Emma can either quarantined the capital

loss or is she is allowed offset the loss from the other collectables. As no other capital gains

has been reported by Emma from the collectables, she can carry forward it to subsequent

years.

Sale of grand piano for $30,000:

“Section 108-20 ITAA 1997” defines the personal use asset. These assets are treated

as the CGT assets apart from the collectables which is mainly used or kept by the taxpayer

for their own enjoyment and usage (Li and Stathis 2017). The examples of this assets

includes the race horses, furniture, electrical items and household items. Notably under “sec

108-20 (1) ITAA 1997”, taxpayers are required to simply ignore the capital loss that arise

from the sale of the personal use asset.

A grand piano was initially bought by Emma for $80,000 but was sold for $80,000 in

2020. As understood, the piano ought to be treated as the personal use asset under “sec 108-

20, ITAA 1997”. The capital loss that Emma has occurred from the disposal of a grand piano

will be simply ignored under the “sec 108-20 (1), ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Christians, A., 2016. BEPS and the new international tax order. BYU L. Rev., p.1603.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Li, H. and Stathis, P., 2017. Determinants of capital structure in Australia: an analysis of

important factors. Managerial Finance, 43(8), pp.881-897.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Oates, W.E. and Schwab, R.M., 2015. The window tax: A case study in excess

burden. Journal of Economic Perspectives, 29(1), pp.163-80.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, p.569.

References:

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Christians, A., 2016. BEPS and the new international tax order. BYU L. Rev., p.1603.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Li, H. and Stathis, P., 2017. Determinants of capital structure in Australia: an analysis of

important factors. Managerial Finance, 43(8), pp.881-897.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Oates, W.E. and Schwab, R.M., 2015. The window tax: A case study in excess

burden. Journal of Economic Perspectives, 29(1), pp.163-80.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, p.569.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.