Sources of Finance and Financial Decisions: Home Textile Business

VerifiedAdded on 2019/12/18

|16

|4646

|158

Report

AI Summary

This report analyzes the financial aspects of establishing a home textile business. It begins by exploring various sources of finance, including internal and external options like personal savings, loans, and government incentives, along with their implications. The report then delves into the costs associated with these financing sources and emphasizes the importance of financial planning, covering topics like financial planning's significance, the users of financial information, and the impact of financing on financial statements. Furthermore, the report provides practical financial decision-making tools such as cash budgets, unit cost analysis for pricing, and investment project viability assessments using payback period, Net Present Value (NPV), and Internal Rate of Return (IRR) calculations. The report underscores the significance of financial management for the business's growth and profitability.

Managing Financial Resources & Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Managing financial resources, includes the management to finance in the business or from which

sources finance should be take so that it will financial for the organization. First thing an entrepreneur need

in the business is finance. An enterprise need a secure or adequate fund to start a business. In this case an

entrepreneur is thinking to establish a new business of home textile products. For the purpose of establishing

the business he will evaluate the market condition, financial sources available for business.

TASK 1

LO 1

1.1 Various sources of finance available for business

For starting or setting up the business an entrepreneur needs fund to start that business and for

meeting us the daily operations of a business. Finance is the major part of the business but selecting the

appropriate one is the main thing (Böhm, Eggert and Thiesbrummel, 2017). There are two sources from which

an entrepreneur can take finance they are internal sources of finances or external sources of finance.

Internal source of finance means entrepreneur personal finance that he is willing to invest in the business. It

includes

Personal saving-An entrepreneur can invest his personal savings in order to start the new business.

This in turn recognized as cheap source of finance because there is no obligation to pay back funfs.

Borrowing from friends-Friend and family who are supportive can provide finance to the

entrepreneur for setting up the new business. Such source of finance offers flexibility of re payment

and interest as compared to other alternatives available.

Credit card-This is the popular way of financing to start a new business. Working of credit cards be

like this, each month entrepreneur pay for expenses related to business on credit card. After 15 days

credit card statement is sent and the balance is paid by the business within credit free period (Cardin,

Jiang and Lim,2017). Effect to this business get access of free credit for 30-45 days.

External source of finance means taking finance from outside institutions. It includes the loan, leasing, or by

issuing the shares. Etc.

Loan capital- An entrepreneur can start venture by taking loan from financial institutions. Thus,

business entity can easily take loan on the behalf of collateral security and thereby would become

able to meet financial requirements.

Lease-Lease is the agreement between two persons where one party grant the right to use the assets

or services to other party for certain period. In other words, by taking fixed assets on lease business

unit can fulfil funding requirements significantly. Hence, in such case, firm only needs to pay rent in

against to using assets.

Loan from government- Sometimes many incentives or loans are given by government in order to

help the businessman in starting new business or expanding the existing business.

In order to set up the business of home textile product. Entrepreneur

has to make arrangement of finance through the internal or external sources. In this entrepreneur has only

£20,000 as an internal source of finance and entrepreneurs wants £250,000 in order to set up the business. So

Managing financial resources, includes the management to finance in the business or from which

sources finance should be take so that it will financial for the organization. First thing an entrepreneur need

in the business is finance. An enterprise need a secure or adequate fund to start a business. In this case an

entrepreneur is thinking to establish a new business of home textile products. For the purpose of establishing

the business he will evaluate the market condition, financial sources available for business.

TASK 1

LO 1

1.1 Various sources of finance available for business

For starting or setting up the business an entrepreneur needs fund to start that business and for

meeting us the daily operations of a business. Finance is the major part of the business but selecting the

appropriate one is the main thing (Böhm, Eggert and Thiesbrummel, 2017). There are two sources from which

an entrepreneur can take finance they are internal sources of finances or external sources of finance.

Internal source of finance means entrepreneur personal finance that he is willing to invest in the business. It

includes

Personal saving-An entrepreneur can invest his personal savings in order to start the new business.

This in turn recognized as cheap source of finance because there is no obligation to pay back funfs.

Borrowing from friends-Friend and family who are supportive can provide finance to the

entrepreneur for setting up the new business. Such source of finance offers flexibility of re payment

and interest as compared to other alternatives available.

Credit card-This is the popular way of financing to start a new business. Working of credit cards be

like this, each month entrepreneur pay for expenses related to business on credit card. After 15 days

credit card statement is sent and the balance is paid by the business within credit free period (Cardin,

Jiang and Lim,2017). Effect to this business get access of free credit for 30-45 days.

External source of finance means taking finance from outside institutions. It includes the loan, leasing, or by

issuing the shares. Etc.

Loan capital- An entrepreneur can start venture by taking loan from financial institutions. Thus,

business entity can easily take loan on the behalf of collateral security and thereby would become

able to meet financial requirements.

Lease-Lease is the agreement between two persons where one party grant the right to use the assets

or services to other party for certain period. In other words, by taking fixed assets on lease business

unit can fulfil funding requirements significantly. Hence, in such case, firm only needs to pay rent in

against to using assets.

Loan from government- Sometimes many incentives or loans are given by government in order to

help the businessman in starting new business or expanding the existing business.

In order to set up the business of home textile product. Entrepreneur

has to make arrangement of finance through the internal or external sources. In this entrepreneur has only

£20,000 as an internal source of finance and entrepreneurs wants £250,000 in order to set up the business. So

for the remaining fund he will go for the external sources of finance. Entrepreneur will either go for bank

loan, or will take finance on lease or will take from government.

1.2 Implication of different sources of finance

Sources Legal Financial Dilution of control Bankruptcy

1. Personal saving No implication No implication No implication No implication

2.Bank loan Documents are to be

submitted as a

security against

loan.

Interest will be as

per the loan.

Priority will be

given.

3.Share capital

4.Lease Agreement will be

made.

Financial

implication will be

as per the

agreement.

Priority will be

given.

1.3 Appropriate sources of finance for starting a business

For starting a business of home textile product's entrepreneur will compare all the sources of finance

and will choose the best source of finance. As entrepreneur will firstly opt for the internal sources of finance

but the entrepreneur has only £20,000 as an internal source of finance and rest of will be taken from external

source of finance that is £230,000. Entrepreneur will compare all the options on the bases of their legality

and financial implication.

In case of loan there is obligation of interest at the end of every month. Entrepreneur has to pay

interest at the end of every month but this is the easiest way to take finance and interest rate is also

minimum(Gianni, Gotzamani and Vouzas,2017). Lease will be depend upon the parties as what they have

decided in respect of interest or amount.

Borrowing from government is also the best way. As sometimes government offers incentive plan or

lower interest rates to the entrepreneur.

For setting up the business £230,000 will be taken from government institution as government is

giving various incentives plan for setting up the new business. And interest rates are also low as compared

to other.

LO 2

2.1 Cost of financing resources

Loan capital- In case of borrowing from the bank, entrepreneur has to pay interest on the loan to the

bank. Interest rate of loan varies from bank to bank. Generally interest rates on loan are between 10-

15%. Interest on loan is paid monthly to the bankers.

loan, or will take finance on lease or will take from government.

1.2 Implication of different sources of finance

Sources Legal Financial Dilution of control Bankruptcy

1. Personal saving No implication No implication No implication No implication

2.Bank loan Documents are to be

submitted as a

security against

loan.

Interest will be as

per the loan.

Priority will be

given.

3.Share capital

4.Lease Agreement will be

made.

Financial

implication will be

as per the

agreement.

Priority will be

given.

1.3 Appropriate sources of finance for starting a business

For starting a business of home textile product's entrepreneur will compare all the sources of finance

and will choose the best source of finance. As entrepreneur will firstly opt for the internal sources of finance

but the entrepreneur has only £20,000 as an internal source of finance and rest of will be taken from external

source of finance that is £230,000. Entrepreneur will compare all the options on the bases of their legality

and financial implication.

In case of loan there is obligation of interest at the end of every month. Entrepreneur has to pay

interest at the end of every month but this is the easiest way to take finance and interest rate is also

minimum(Gianni, Gotzamani and Vouzas,2017). Lease will be depend upon the parties as what they have

decided in respect of interest or amount.

Borrowing from government is also the best way. As sometimes government offers incentive plan or

lower interest rates to the entrepreneur.

For setting up the business £230,000 will be taken from government institution as government is

giving various incentives plan for setting up the new business. And interest rates are also low as compared

to other.

LO 2

2.1 Cost of financing resources

Loan capital- In case of borrowing from the bank, entrepreneur has to pay interest on the loan to the

bank. Interest rate of loan varies from bank to bank. Generally interest rates on loan are between 10-

15%. Interest on loan is paid monthly to the bankers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lease- Lease is depend upon the agreement made between the parties. In this case leasee has to pay

rent to lessor (Grabher and König,2017) Rent is determined by the lessor on the bases of the time of

lease.

Loan from government-Cost of taking borrowing from government is low. in these loan rates are low

as compared to other institutions. Sometimes in order to promote the businessman government may

give incentives. Entrepreneur again has to pay to interest on loan. But the rates may differ.

Venture capital-Cost of hiring the venture capital is high as they take at least 40% venture in client

firm.

2.2 Importance of financial planning

Financial planning is the process of estimating the capital requirement of business. It relates to the

process of framing financial policies, investment and administration of funds of the enterprises. With the

help of financial policies' entrepreneur can make effective and adequate financial policies which will give

positive return to the business (Hisrich and Ramadani,2017). Importance of financial planning are:

Financial planning helps entrepreneur in getting adequate funds for setting up the business, and

ensure the consistency of goals by coordinating the objective of business with the financial

requirement.

With the help of proper financial planning proper utilization of fund can be done.

An entrepreneur can anticipate the future requirement.

Financial planning helps to reduce the uncertainties which can be obstacle to the growth of business.

This helps in ensuring stability and profitability.

Financial planning helps the entrepreneur in making right decision.

It ensures the balance between the outflow and inflow of the business.

It also supports the strategic growth of the organization, by evaluating the risk, estimates and

opportunities in the market.

All these importance’s of financial planning helps an entrepreneur in setting the business (Karakaya

and Karakaya, 2017). As with the help of this entrepreneur can anticipate the demand of home textile products

in the market. And accordingly entrepreneur will invest in the business.

2.3 Users of financial information

Financial information is useful for the person who wants to invest in the business. Various users of

financial information are internal users and external users.

Internal users are those users which are within the organization. It includes

Management- Management of the organization need financial information in order to know the

financial position of the organization and accordingly strategies will be planes.

Employees- Employees analysis the company profitability in order to expect the increment in there

salarie4s in future.

Owners- Owners are the person who run the business, they want financial information to check out

the growth and position of their organization.

External users are those users which are the outside the organization. They are

rent to lessor (Grabher and König,2017) Rent is determined by the lessor on the bases of the time of

lease.

Loan from government-Cost of taking borrowing from government is low. in these loan rates are low

as compared to other institutions. Sometimes in order to promote the businessman government may

give incentives. Entrepreneur again has to pay to interest on loan. But the rates may differ.

Venture capital-Cost of hiring the venture capital is high as they take at least 40% venture in client

firm.

2.2 Importance of financial planning

Financial planning is the process of estimating the capital requirement of business. It relates to the

process of framing financial policies, investment and administration of funds of the enterprises. With the

help of financial policies' entrepreneur can make effective and adequate financial policies which will give

positive return to the business (Hisrich and Ramadani,2017). Importance of financial planning are:

Financial planning helps entrepreneur in getting adequate funds for setting up the business, and

ensure the consistency of goals by coordinating the objective of business with the financial

requirement.

With the help of proper financial planning proper utilization of fund can be done.

An entrepreneur can anticipate the future requirement.

Financial planning helps to reduce the uncertainties which can be obstacle to the growth of business.

This helps in ensuring stability and profitability.

Financial planning helps the entrepreneur in making right decision.

It ensures the balance between the outflow and inflow of the business.

It also supports the strategic growth of the organization, by evaluating the risk, estimates and

opportunities in the market.

All these importance’s of financial planning helps an entrepreneur in setting the business (Karakaya

and Karakaya, 2017). As with the help of this entrepreneur can anticipate the demand of home textile products

in the market. And accordingly entrepreneur will invest in the business.

2.3 Users of financial information

Financial information is useful for the person who wants to invest in the business. Various users of

financial information are internal users and external users.

Internal users are those users which are within the organization. It includes

Management- Management of the organization need financial information in order to know the

financial position of the organization and accordingly strategies will be planes.

Employees- Employees analysis the company profitability in order to expect the increment in there

salarie4s in future.

Owners- Owners are the person who run the business, they want financial information to check out

the growth and position of their organization.

External users are those users which are the outside the organization. They are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creditors-They want the financial information to know the credit worthiness of the

organization .Terms of credit is decided on the bases of organization financial health.

Tax Authorities- For determining the creditability of tax of then organization.

Investors- Investors analysis the financial information to access the feasibility of investing in the

company. Investor wart higher return on their investment.

Customers- Uses the financial information to access the financial position of its supplier in order

to maintain the stability of supply.

Regulator Authorities- Check the financial information that organization has disclosed all the

information or not. Or the financial statements are made according to legal rules or not.

2.4 Impact of finance on financial statement

Financial statements are the record that outline the financial activity of the business.

Financing from different sources affect the balance sheet and profit and loss account of the business

(Kolokytha, de Oliveira Galvão and Teegavarapu, 2017).

Owners own fund- Owners own fund mean the personal fund which has invested by owner

in the business. Owners fund affect the balance sheet it is shown at right side of the balance

sheet under the heading owners’ equity.

Loan from various institutions- If an entrepreneur is financing fund from loans than it will

affect both the balance sheet and profit and loss account of the business. As loan increase the

liability of business and shown under the heading the liabilities as a ”Long term liability”,

and the interest on loan will affect the profit of the business as it will deducted from profit of

the organization. It is shown on the left side as “To interest on loan” and will get deducted

from profits.

Share capital- If fund is accumulated through the issue of share capital than it will increase

the liability of the company and will be shown under the heading liabilities under the sub

heading share capital. Interest on shares paid to shareholder will affect the profit and loss

account as the interest will be deducted from the profit.

LO 3 Financial decision based on financial information

3.1 Cash budget of the Home textile products of the six months

organization .Terms of credit is decided on the bases of organization financial health.

Tax Authorities- For determining the creditability of tax of then organization.

Investors- Investors analysis the financial information to access the feasibility of investing in the

company. Investor wart higher return on their investment.

Customers- Uses the financial information to access the financial position of its supplier in order

to maintain the stability of supply.

Regulator Authorities- Check the financial information that organization has disclosed all the

information or not. Or the financial statements are made according to legal rules or not.

2.4 Impact of finance on financial statement

Financial statements are the record that outline the financial activity of the business.

Financing from different sources affect the balance sheet and profit and loss account of the business

(Kolokytha, de Oliveira Galvão and Teegavarapu, 2017).

Owners own fund- Owners own fund mean the personal fund which has invested by owner

in the business. Owners fund affect the balance sheet it is shown at right side of the balance

sheet under the heading owners’ equity.

Loan from various institutions- If an entrepreneur is financing fund from loans than it will

affect both the balance sheet and profit and loss account of the business. As loan increase the

liability of business and shown under the heading the liabilities as a ”Long term liability”,

and the interest on loan will affect the profit of the business as it will deducted from profit of

the organization. It is shown on the left side as “To interest on loan” and will get deducted

from profits.

Share capital- If fund is accumulated through the issue of share capital than it will increase

the liability of the company and will be shown under the heading liabilities under the sub

heading share capital. Interest on shares paid to shareholder will affect the profit and loss

account as the interest will be deducted from the profit.

LO 3 Financial decision based on financial information

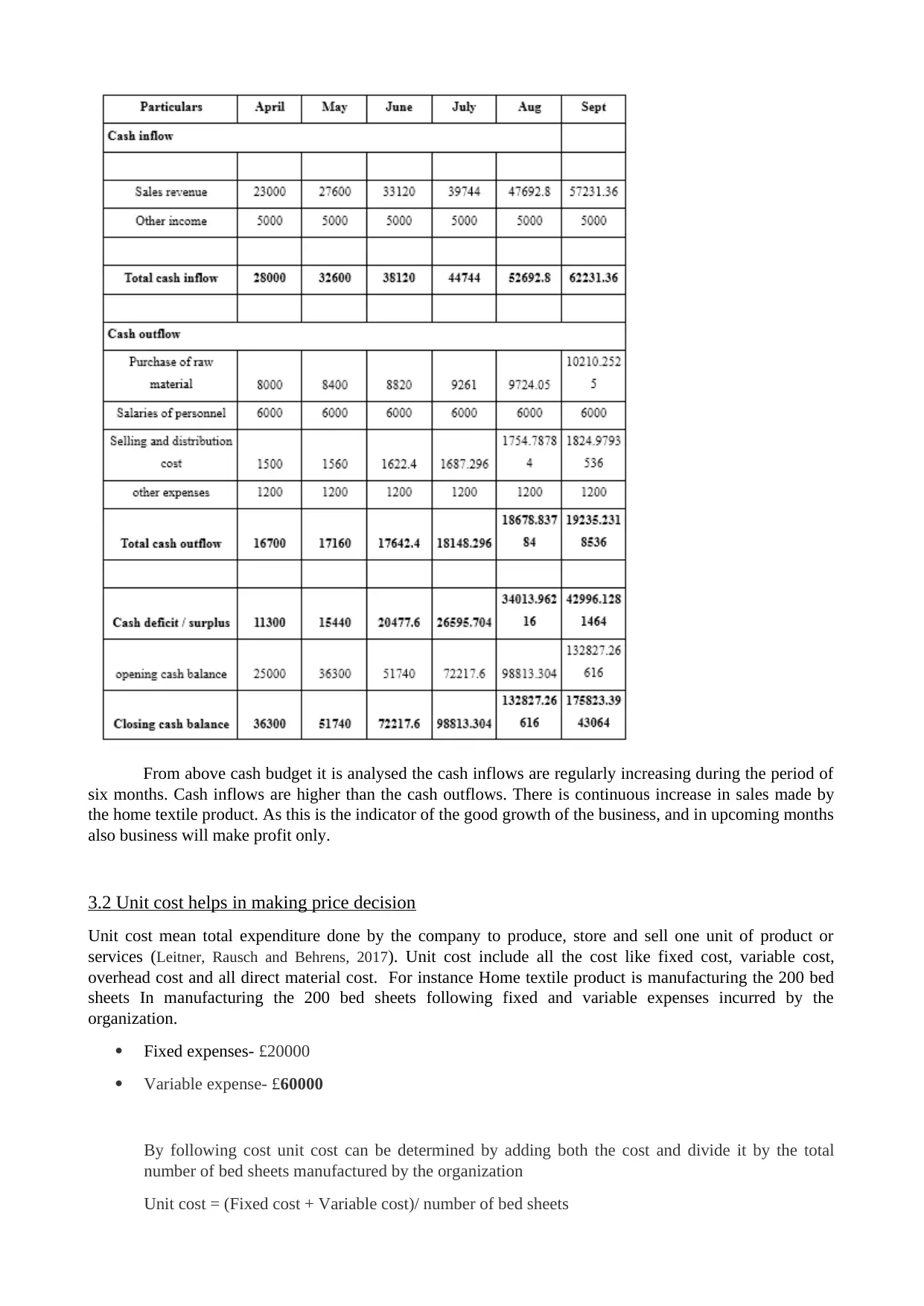

3.1 Cash budget of the Home textile products of the six months

From above cash budget it is analysed the cash inflows are regularly increasing during the period of

six months. Cash inflows are higher than the cash outflows. There is continuous increase in sales made by

the home textile product. As this is the indicator of the good growth of the business, and in upcoming months

also business will make profit only.

3.2 Unit cost helps in making price decision

Unit cost mean total expenditure done by the company to produce, store and sell one unit of product or

services (Leitner, Rausch and Behrens, 2017). Unit cost include all the cost like fixed cost, variable cost,

overhead cost and all direct material cost. For instance Home textile product is manufacturing the 200 bed

sheets In manufacturing the 200 bed sheets following fixed and variable expenses incurred by the

organization.

Fixed expenses- £20000

Variable expense- £60000

By following cost unit cost can be determined by adding both the cost and divide it by the total

number of bed sheets manufactured by the organization

Unit cost = (Fixed cost + Variable cost)/ number of bed sheets

six months. Cash inflows are higher than the cash outflows. There is continuous increase in sales made by

the home textile product. As this is the indicator of the good growth of the business, and in upcoming months

also business will make profit only.

3.2 Unit cost helps in making price decision

Unit cost mean total expenditure done by the company to produce, store and sell one unit of product or

services (Leitner, Rausch and Behrens, 2017). Unit cost include all the cost like fixed cost, variable cost,

overhead cost and all direct material cost. For instance Home textile product is manufacturing the 200 bed

sheets In manufacturing the 200 bed sheets following fixed and variable expenses incurred by the

organization.

Fixed expenses- £20000

Variable expense- £60000

By following cost unit cost can be determined by adding both the cost and divide it by the total

number of bed sheets manufactured by the organization

Unit cost = (Fixed cost + Variable cost)/ number of bed sheets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= (20000+60000)/200

=£400

Further is the business wants to attain the margin of 20% through mark up pricing method than price

will be

Price per unit: 400 + (400*20%)

= 400 + 80

=£480

Hence from above calculation it is notice that in order to get the profit of £80 company has to

charge £480 from each individual.

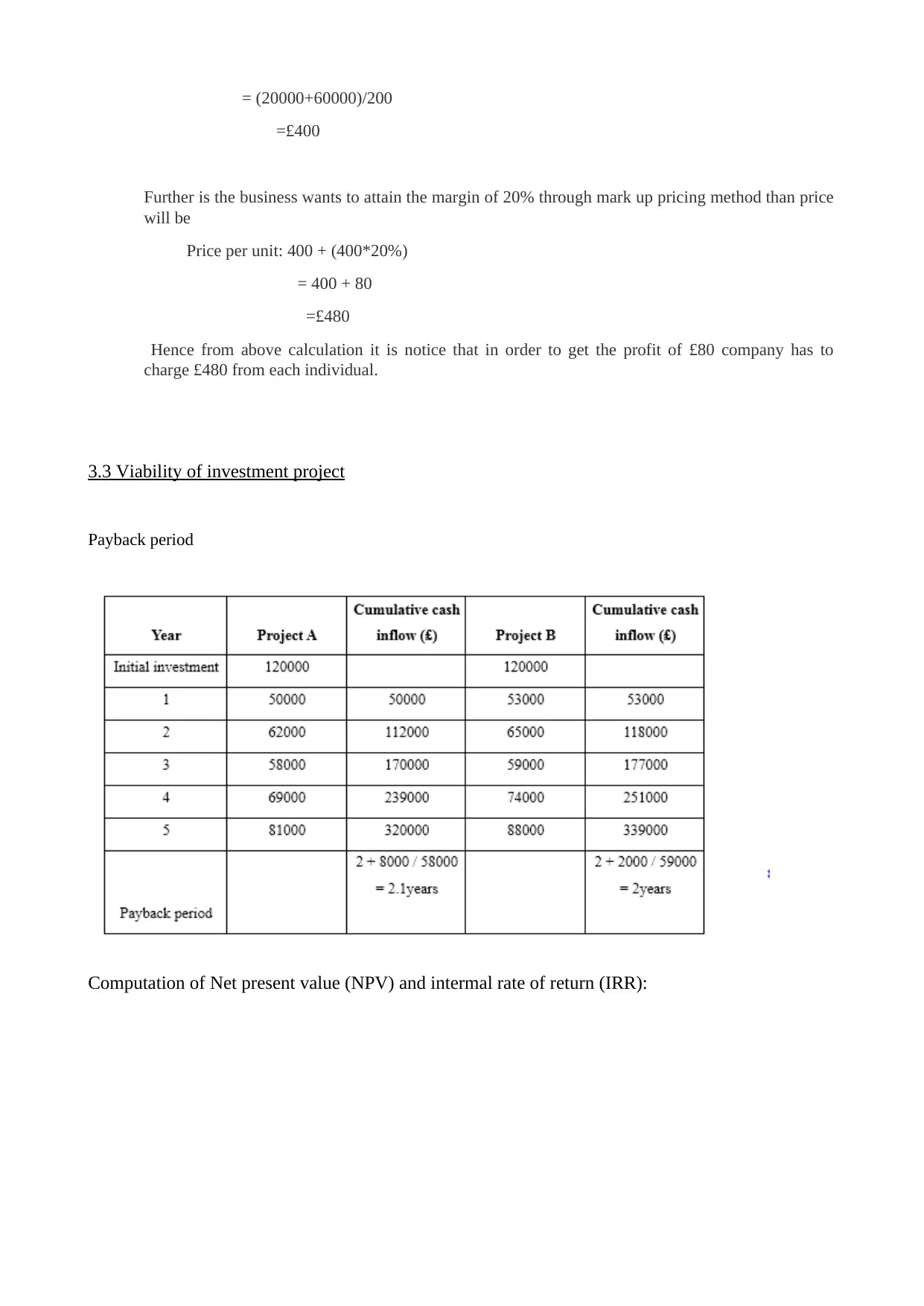

3.3 Viability of investment project

Payback period

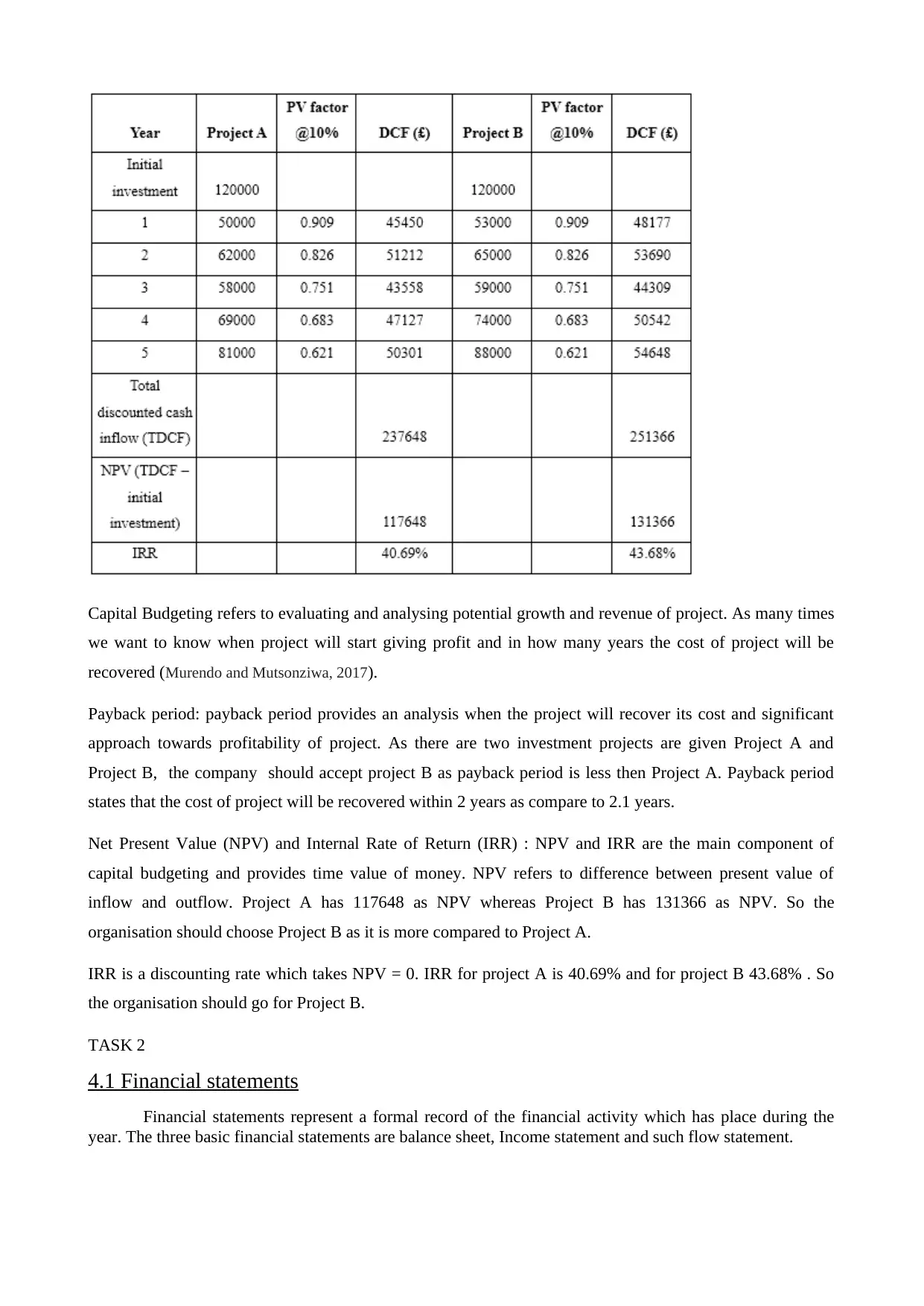

Computation of Net present value (NPV) and intermal rate of return (IRR):

=£400

Further is the business wants to attain the margin of 20% through mark up pricing method than price

will be

Price per unit: 400 + (400*20%)

= 400 + 80

=£480

Hence from above calculation it is notice that in order to get the profit of £80 company has to

charge £480 from each individual.

3.3 Viability of investment project

Payback period

Computation of Net present value (NPV) and intermal rate of return (IRR):

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Budgeting refers to evaluating and analysing potential growth and revenue of project. As many times

we want to know when project will start giving profit and in how many years the cost of project will be

recovered (Murendo and Mutsonziwa, 2017).

Payback period: payback period provides an analysis when the project will recover its cost and significant

approach towards profitability of project. As there are two investment projects are given Project A and

Project B, the company should accept project B as payback period is less then Project A. Payback period

states that the cost of project will be recovered within 2 years as compare to 2.1 years.

Net Present Value (NPV) and Internal Rate of Return (IRR) : NPV and IRR are the main component of

capital budgeting and provides time value of money. NPV refers to difference between present value of

inflow and outflow. Project A has 117648 as NPV whereas Project B has 131366 as NPV. So the

organisation should choose Project B as it is more compared to Project A.

IRR is a discounting rate which takes NPV = 0. IRR for project A is 40.69% and for project B 43.68% . So

the organisation should go for Project B.

TASK 2

4.1 Financial statements

Financial statements represent a formal record of the financial activity which has place during the

year. The three basic financial statements are balance sheet, Income statement and such flow statement.

we want to know when project will start giving profit and in how many years the cost of project will be

recovered (Murendo and Mutsonziwa, 2017).

Payback period: payback period provides an analysis when the project will recover its cost and significant

approach towards profitability of project. As there are two investment projects are given Project A and

Project B, the company should accept project B as payback period is less then Project A. Payback period

states that the cost of project will be recovered within 2 years as compare to 2.1 years.

Net Present Value (NPV) and Internal Rate of Return (IRR) : NPV and IRR are the main component of

capital budgeting and provides time value of money. NPV refers to difference between present value of

inflow and outflow. Project A has 117648 as NPV whereas Project B has 131366 as NPV. So the

organisation should choose Project B as it is more compared to Project A.

IRR is a discounting rate which takes NPV = 0. IRR for project A is 40.69% and for project B 43.68% . So

the organisation should go for Project B.

TASK 2

4.1 Financial statements

Financial statements represent a formal record of the financial activity which has place during the

year. The three basic financial statements are balance sheet, Income statement and such flow statement.

Balance sheet –Balance sheet is the statement of assets, liabilities and capital of business. Balance

sheet gives the idea to investors about the company owns and owes. Balance sheet work on basic

formulae that is Assets = Liabilities + Equity.

Balance sheet contain three element assets liabilities and equity. Asserts are the properties invested in the

business to be used in the operation of business. Such as cash, inventory, building etc. Liabilities are the

legal obligation on the organization such as loans. Equity are the cash or non-cash items invested by the

owner or investors.

Uses of balance sheet

Balance sheet helps us in determine the working capital of the business. Working capital is the

difference between the current asset and current liability.

Balance sheet helps the organisation or investors to know the net worth of the business. Net worth

defines the true value of an entity.

Balance sheet helps to company in sustain future needs. By seeing the balance sheet an entrepreneurs

can sustain the future needs.

Income statement – It is also known as the profit and loss account of the organization as it shows the

revenues and expenses made by the organization during the year. Income statement include the sales,

gross profit, other general and administration expenses or any income.

For obtaining the net profit firstly gross profit will be ascertained. After gross profit all the expense

will be deducted and all the income will be added in gross profit in order to get the net profit of the

firm.

Cash flow statement- Cash flow statement shows the inflow and outflow of the cash during a

particular period of time (Nizamidou and Vouzas, 2017). Cash flow activity involves cash generated

from operating activities, cash generated from investing activities and cash from financing activities.

Cash from operating activities include the cash generated from sales and purchases made by the

organization. Cash from investing activities include the cash inflows and outflows made by

investment made by the organization like investment purchase, sell of investment. Cash from

financing activities includes cash inflow and outflow from the selling and purchasing of shares,

dividend paid etc.

All these financial statements are seen by the lender, investor, creditor in order to know th position

of the organization. As balance sheet gives the idea regarding worth of the organization, profit and

loss account shows the profit or loss made by the organization or cash flow statement shows the

balance of cash with the organization for used in the daily operations.

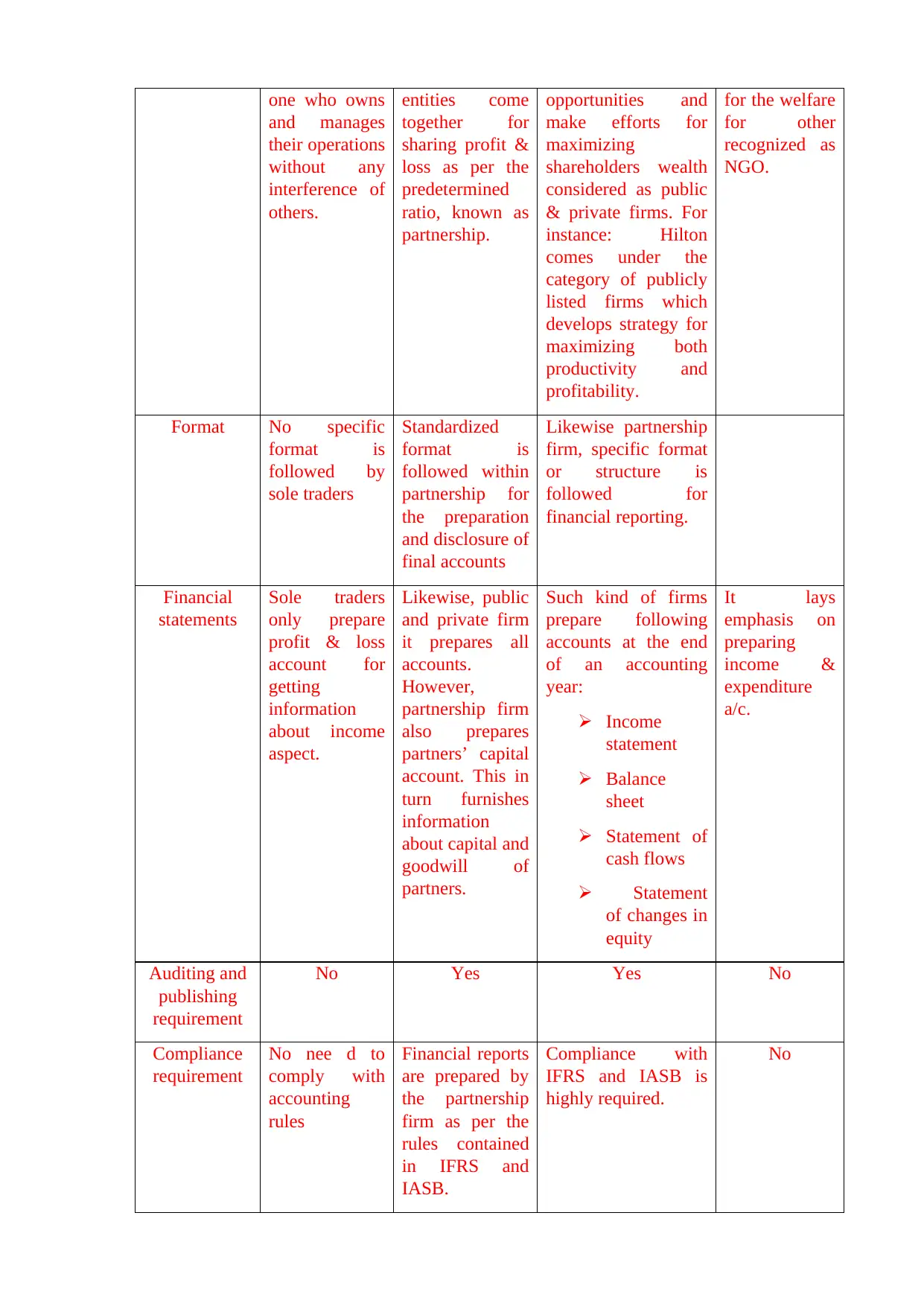

4.2 Comparison of financial statements

Basis of

difference

Sole trader Partnership

firm

Public and private

firm

Non-profit

making

organization

Meaning Sole traders

implies for the

Firm in which

two or more

Firms which create

employment

Organization

which works

sheet gives the idea to investors about the company owns and owes. Balance sheet work on basic

formulae that is Assets = Liabilities + Equity.

Balance sheet contain three element assets liabilities and equity. Asserts are the properties invested in the

business to be used in the operation of business. Such as cash, inventory, building etc. Liabilities are the

legal obligation on the organization such as loans. Equity are the cash or non-cash items invested by the

owner or investors.

Uses of balance sheet

Balance sheet helps us in determine the working capital of the business. Working capital is the

difference between the current asset and current liability.

Balance sheet helps the organisation or investors to know the net worth of the business. Net worth

defines the true value of an entity.

Balance sheet helps to company in sustain future needs. By seeing the balance sheet an entrepreneurs

can sustain the future needs.

Income statement – It is also known as the profit and loss account of the organization as it shows the

revenues and expenses made by the organization during the year. Income statement include the sales,

gross profit, other general and administration expenses or any income.

For obtaining the net profit firstly gross profit will be ascertained. After gross profit all the expense

will be deducted and all the income will be added in gross profit in order to get the net profit of the

firm.

Cash flow statement- Cash flow statement shows the inflow and outflow of the cash during a

particular period of time (Nizamidou and Vouzas, 2017). Cash flow activity involves cash generated

from operating activities, cash generated from investing activities and cash from financing activities.

Cash from operating activities include the cash generated from sales and purchases made by the

organization. Cash from investing activities include the cash inflows and outflows made by

investment made by the organization like investment purchase, sell of investment. Cash from

financing activities includes cash inflow and outflow from the selling and purchasing of shares,

dividend paid etc.

All these financial statements are seen by the lender, investor, creditor in order to know th position

of the organization. As balance sheet gives the idea regarding worth of the organization, profit and

loss account shows the profit or loss made by the organization or cash flow statement shows the

balance of cash with the organization for used in the daily operations.

4.2 Comparison of financial statements

Basis of

difference

Sole trader Partnership

firm

Public and private

firm

Non-profit

making

organization

Meaning Sole traders

implies for the

Firm in which

two or more

Firms which create

employment

Organization

which works

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

one who owns

and manages

their operations

without any

interference of

others.

entities come

together for

sharing profit &

loss as per the

predetermined

ratio, known as

partnership.

opportunities and

make efforts for

maximizing

shareholders wealth

considered as public

& private firms. For

instance: Hilton

comes under the

category of publicly

listed firms which

develops strategy for

maximizing both

productivity and

profitability.

for the welfare

for other

recognized as

NGO.

Format No specific

format is

followed by

sole traders

Standardized

format is

followed within

partnership for

the preparation

and disclosure of

final accounts

Likewise partnership

firm, specific format

or structure is

followed for

financial reporting.

Financial

statements

Sole traders

only prepare

profit & loss

account for

getting

information

about income

aspect.

Likewise, public

and private firm

it prepares all

accounts.

However,

partnership firm

also prepares

partners’ capital

account. This in

turn furnishes

information

about capital and

goodwill of

partners.

Such kind of firms

prepare following

accounts at the end

of an accounting

year:

Income

statement

Balance

sheet

Statement of

cash flows

Statement

of changes in

equity

It lays

emphasis on

preparing

income &

expenditure

a/c.

Auditing and

publishing

requirement

No Yes Yes No

Compliance

requirement

No nee d to

comply with

accounting

rules

Financial reports

are prepared by

the partnership

firm as per the

rules contained

in IFRS and

IASB.

Compliance with

IFRS and IASB is

highly required.

No

and manages

their operations

without any

interference of

others.

entities come

together for

sharing profit &

loss as per the

predetermined

ratio, known as

partnership.

opportunities and

make efforts for

maximizing

shareholders wealth

considered as public

& private firms. For

instance: Hilton

comes under the

category of publicly

listed firms which

develops strategy for

maximizing both

productivity and

profitability.

for the welfare

for other

recognized as

NGO.

Format No specific

format is

followed by

sole traders

Standardized

format is

followed within

partnership for

the preparation

and disclosure of

final accounts

Likewise partnership

firm, specific format

or structure is

followed for

financial reporting.

Financial

statements

Sole traders

only prepare

profit & loss

account for

getting

information

about income

aspect.

Likewise, public

and private firm

it prepares all

accounts.

However,

partnership firm

also prepares

partners’ capital

account. This in

turn furnishes

information

about capital and

goodwill of

partners.

Such kind of firms

prepare following

accounts at the end

of an accounting

year:

Income

statement

Balance

sheet

Statement of

cash flows

Statement

of changes in

equity

It lays

emphasis on

preparing

income &

expenditure

a/c.

Auditing and

publishing

requirement

No Yes Yes No

Compliance

requirement

No nee d to

comply with

accounting

rules

Financial reports

are prepared by

the partnership

firm as per the

rules contained

in IFRS and

IASB.

Compliance with

IFRS and IASB is

highly required.

No

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

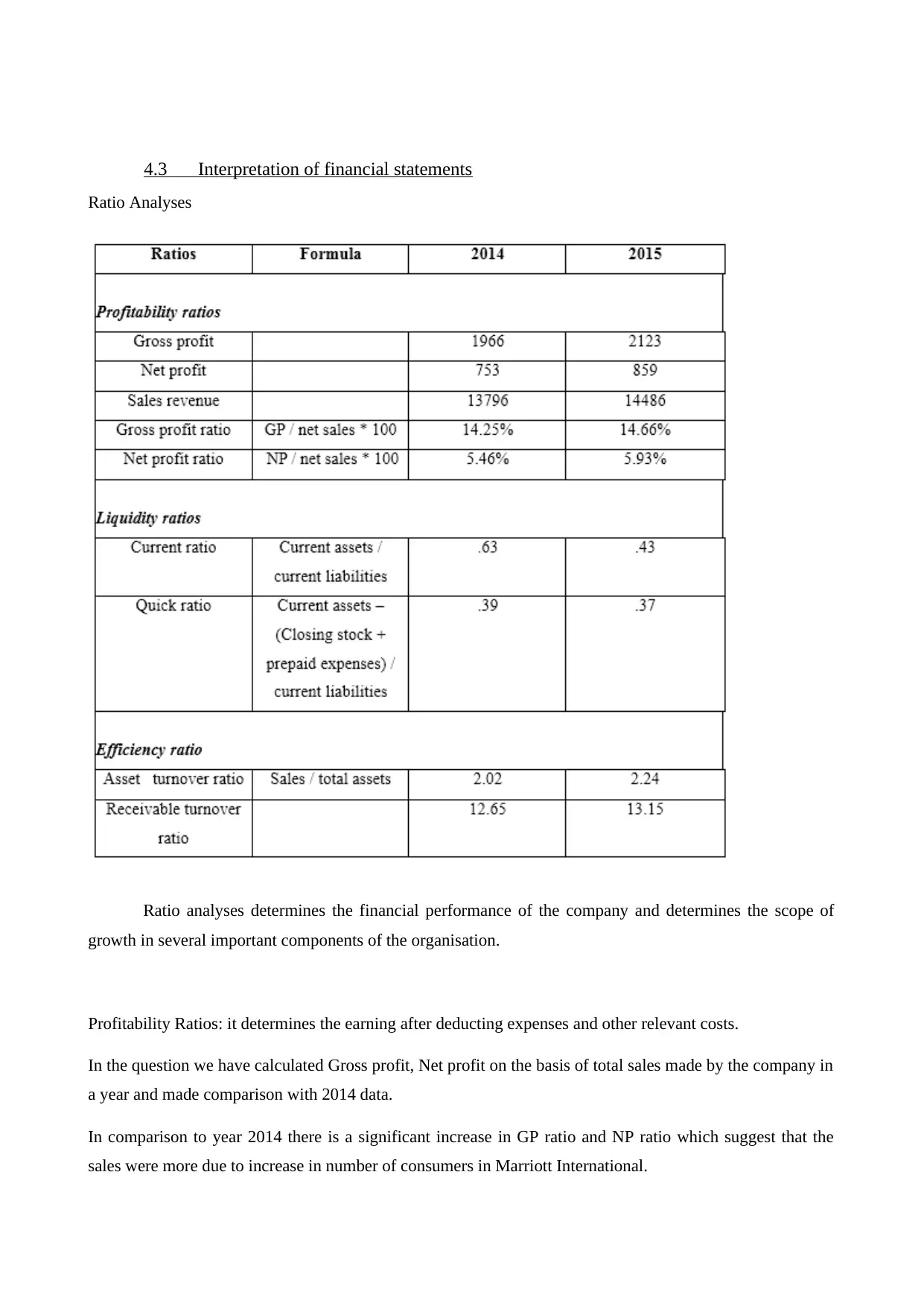

4.3 Interpretation of financial statements

Ratio Analyses

Ratio analyses determines the financial performance of the company and determines the scope of

growth in several important components of the organisation.

Profitability Ratios: it determines the earning after deducting expenses and other relevant costs.

In the question we have calculated Gross profit, Net profit on the basis of total sales made by the company in

a year and made comparison with 2014 data.

In comparison to year 2014 there is a significant increase in GP ratio and NP ratio which suggest that the

sales were more due to increase in number of consumers in Marriott International.

Ratio Analyses

Ratio analyses determines the financial performance of the company and determines the scope of

growth in several important components of the organisation.

Profitability Ratios: it determines the earning after deducting expenses and other relevant costs.

In the question we have calculated Gross profit, Net profit on the basis of total sales made by the company in

a year and made comparison with 2014 data.

In comparison to year 2014 there is a significant increase in GP ratio and NP ratio which suggest that the

sales were more due to increase in number of consumers in Marriott International.

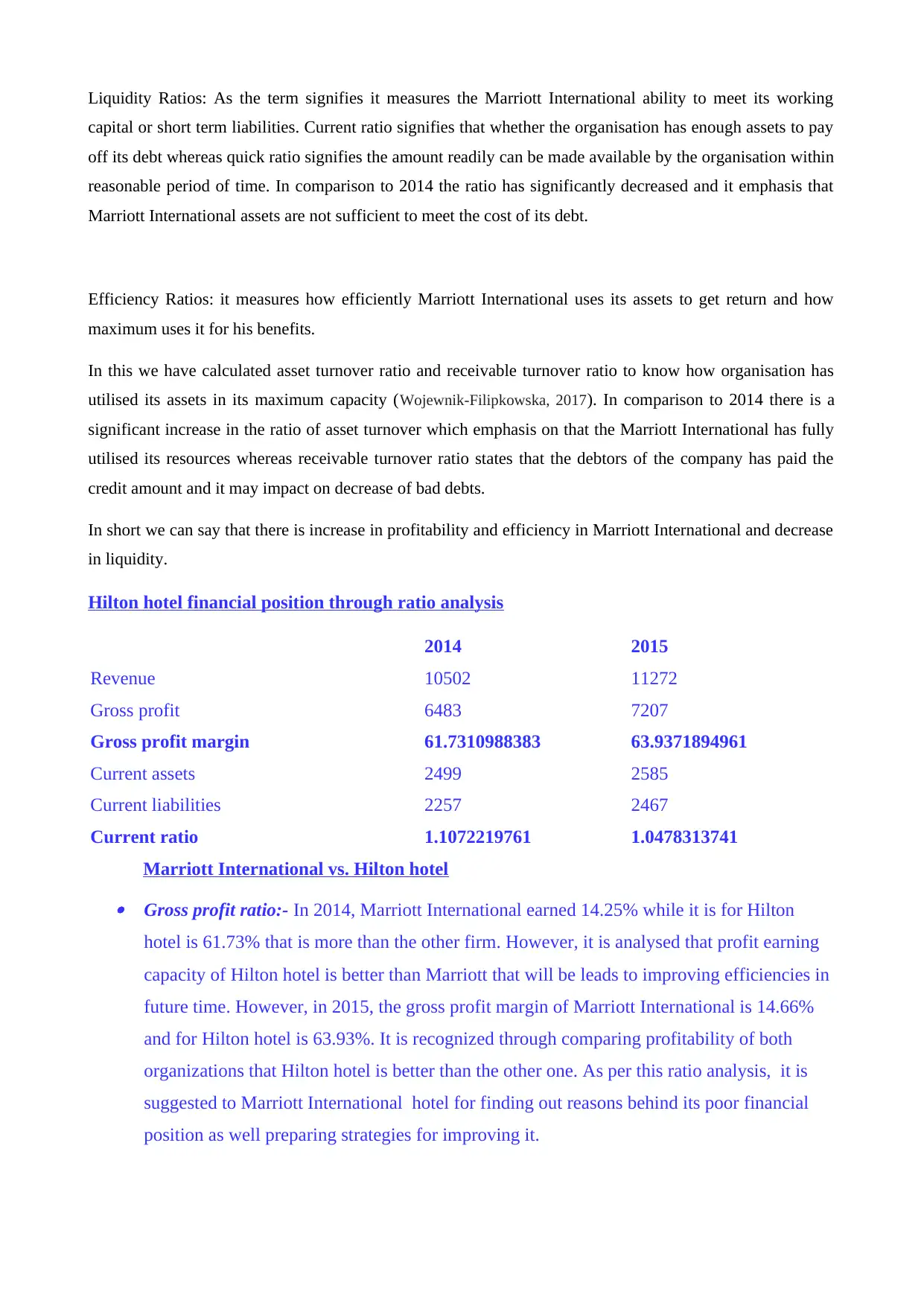

Liquidity Ratios: As the term signifies it measures the Marriott International ability to meet its working

capital or short term liabilities. Current ratio signifies that whether the organisation has enough assets to pay

off its debt whereas quick ratio signifies the amount readily can be made available by the organisation within

reasonable period of time. In comparison to 2014 the ratio has significantly decreased and it emphasis that

Marriott International assets are not sufficient to meet the cost of its debt.

Efficiency Ratios: it measures how efficiently Marriott International uses its assets to get return and how

maximum uses it for his benefits.

In this we have calculated asset turnover ratio and receivable turnover ratio to know how organisation has

utilised its assets in its maximum capacity (Wojewnik-Filipkowska, 2017). In comparison to 2014 there is a

significant increase in the ratio of asset turnover which emphasis on that the Marriott International has fully

utilised its resources whereas receivable turnover ratio states that the debtors of the company has paid the

credit amount and it may impact on decrease of bad debts.

In short we can say that there is increase in profitability and efficiency in Marriott International and decrease

in liquidity.

Hilton hotel financial position through ratio analysis

2014 2015

Revenue 10502 11272

Gross profit 6483 7207

Gross profit margin 61.7310988383 63.9371894961

Current assets 2499 2585

Current liabilities 2257 2467

Current ratio 1.1072219761 1.0478313741

Marriott International vs. Hilton hotel

Gross profit ratio:- In 2014, Marriott International earned 14.25% while it is for Hilton

hotel is 61.73% that is more than the other firm. However, it is analysed that profit earning

capacity of Hilton hotel is better than Marriott that will be leads to improving efficiencies in

future time. However, in 2015, the gross profit margin of Marriott International is 14.66%

and for Hilton hotel is 63.93%. It is recognized through comparing profitability of both

organizations that Hilton hotel is better than the other one. As per this ratio analysis, it is

suggested to Marriott International hotel for finding out reasons behind its poor financial

position as well preparing strategies for improving it.

capital or short term liabilities. Current ratio signifies that whether the organisation has enough assets to pay

off its debt whereas quick ratio signifies the amount readily can be made available by the organisation within

reasonable period of time. In comparison to 2014 the ratio has significantly decreased and it emphasis that

Marriott International assets are not sufficient to meet the cost of its debt.

Efficiency Ratios: it measures how efficiently Marriott International uses its assets to get return and how

maximum uses it for his benefits.

In this we have calculated asset turnover ratio and receivable turnover ratio to know how organisation has

utilised its assets in its maximum capacity (Wojewnik-Filipkowska, 2017). In comparison to 2014 there is a

significant increase in the ratio of asset turnover which emphasis on that the Marriott International has fully

utilised its resources whereas receivable turnover ratio states that the debtors of the company has paid the

credit amount and it may impact on decrease of bad debts.

In short we can say that there is increase in profitability and efficiency in Marriott International and decrease

in liquidity.

Hilton hotel financial position through ratio analysis

2014 2015

Revenue 10502 11272

Gross profit 6483 7207

Gross profit margin 61.7310988383 63.9371894961

Current assets 2499 2585

Current liabilities 2257 2467

Current ratio 1.1072219761 1.0478313741

Marriott International vs. Hilton hotel

Gross profit ratio:- In 2014, Marriott International earned 14.25% while it is for Hilton

hotel is 61.73% that is more than the other firm. However, it is analysed that profit earning

capacity of Hilton hotel is better than Marriott that will be leads to improving efficiencies in

future time. However, in 2015, the gross profit margin of Marriott International is 14.66%

and for Hilton hotel is 63.93%. It is recognized through comparing profitability of both

organizations that Hilton hotel is better than the other one. As per this ratio analysis, it is

suggested to Marriott International hotel for finding out reasons behind its poor financial

position as well preparing strategies for improving it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.