Marketing Management: Customer Perceived Value of Hong Leong Bank

VerifiedAdded on 2019/12/28

|13

|4513

|426

Report

AI Summary

This report delves into the concept of customer perceived value within the banking sector, emphasizing its significance in today's competitive market. It begins with a comprehensive introduction, defining key terms and outlining the importance of meeting and exceeding customer expectations, particularly in light of external factors like technological advancements and competitor actions. The report then examines the customer perceived value in the banking sector, using the Sanchez model to analyze the value proposition of Hong Leong Bank Berhad and its competitor, Public Bank Berhad. The analysis includes a detailed breakdown of perceived benefits (economic, emotional, social, and relationship) and sacrifices (price, time, effort, risk, and inconvenience). The report contrasts the value propositions of Hong Leong Bank and Public Bank, highlighting the key differences in their approaches to customer experience, competitive positioning, and benefits offered. Finally, it concludes with a discussion of the lessons learned from the module and a plan to implement the value chain to improve customer satisfaction and loyalty.

MARKETING

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MARKETING MANAGEMENT....................................................................................................1

1.0Introduction.................................................................................................................................3

Definitions...................................................................................................................................3

2.0Customer Perceive Value of Banking Sector..............................................................................3

Perceived Benefits.......................................................................................................................4

Economic Benefits...................................................................................................4

Emotional Benefits............................................................................................................5

Social Benefits...................................................................................................................5

Relationship Benefit..........................................................................................................5

Sacrifices.....................................................................................................................................6

Price, Time and Effort Sacrifices ......................................................................................6

Risk and Inconvenience.....................................................................................................6

2. Contrast the value proposition of Hong Leong Bank..............................................................6

3. Benchmark the two value propositions comparing and contrasting.......................................8

4. what had been learnt from the module....................................................................................8

5. Plan to implement the value chain..........................................................................................9

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

MARKETING MANAGEMENT....................................................................................................1

1.0Introduction.................................................................................................................................3

Definitions...................................................................................................................................3

2.0Customer Perceive Value of Banking Sector..............................................................................3

Perceived Benefits.......................................................................................................................4

Economic Benefits...................................................................................................4

Emotional Benefits............................................................................................................5

Social Benefits...................................................................................................................5

Relationship Benefit..........................................................................................................5

Sacrifices.....................................................................................................................................6

Price, Time and Effort Sacrifices ......................................................................................6

Risk and Inconvenience.....................................................................................................6

2. Contrast the value proposition of Hong Leong Bank..............................................................6

3. Benchmark the two value propositions comparing and contrasting.......................................8

4. what had been learnt from the module....................................................................................8

5. Plan to implement the value chain..........................................................................................9

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

Introduction

To meet the potential customer needs and keep the early adopters loyal by just meeting their

needs are insufficient nowadays. Because of the external factors that may disrupt the habits of

customers such as technology and competition, the customers are expecting more than their

expectations. Therefore, the use of the concept of perceived value has gradually become a

priority for business sustainability as well as the key of success in the high market competition

(Septa et al., 2016).

The purpose of this paper is to identify the customer perceived value in the banking sector using

Sanchez model to measure the value proposition of Hong Leong Bank Berhad and the leading

competitor, Public Bank Berhad according to the list of top banks in Malaysia relbanks (n.d.)

based on total assets. Through to end of this research, the new value of proposition will be

proposed to meet the value criteria of the customers and provided with the implementation plan.

Definitions

Author Model Definition

Woodruff (1997) Value Hierachy Model

He defined perceived value as “customer‟s perceived preference for an

evaluation of those product attributes, attribute performances, and

consequences arising from use that facilitate (or block) achieving the

customer‟s goals and purpose in use situations.

Holbrook and Hirschman (1982) Utilitarian and Hedonic Model

They had a notion that value should not only viewed from utilitarian

perspective in which the product is valued based on its performance or

functions, but also include the experiential perspective in

which the product is valued based on the experience or the feeling arouse

from consumption, including the symbolic

and hedonic aspect

Sheth et al (1991) Consumption Value Theory

They suggested five dimensions of value namely functional value which is

related to the utilitarian or functional purpose of the product, social value

which is related to the image obtained from the society, emotional value

which is related to the feeling arouse from using the product, epistemic value

which is related to the curiosity or desire for knowledge or novelty seeking,

and conditional value which is derived due to specific situation or

circumstances that faced by the consumers.

Holbrook (1996) Holbrook Typology of Consumer Value

His perceived value can be defined as “an interactive relativistic preference

experience.” By interactive He meant that value entails the relationship

between the customer and the product, it is comparative, subjective, and

specific to the context. He claimed that the customer perceived the value not

in the purchase stage however during the consumption stage.

(Source: Septa et al., 2016)

Customer Perceive Value of Banking Sector

In the recent years, the banking sector was changing remarkably due to several of external

factors. Karin (2011) has identified 5 notable factors below:

1) Competitors in the same industry such as foreign and local banks.

2) Competitors in different industry such as leasing and money lender companies.

To meet the potential customer needs and keep the early adopters loyal by just meeting their

needs are insufficient nowadays. Because of the external factors that may disrupt the habits of

customers such as technology and competition, the customers are expecting more than their

expectations. Therefore, the use of the concept of perceived value has gradually become a

priority for business sustainability as well as the key of success in the high market competition

(Septa et al., 2016).

The purpose of this paper is to identify the customer perceived value in the banking sector using

Sanchez model to measure the value proposition of Hong Leong Bank Berhad and the leading

competitor, Public Bank Berhad according to the list of top banks in Malaysia relbanks (n.d.)

based on total assets. Through to end of this research, the new value of proposition will be

proposed to meet the value criteria of the customers and provided with the implementation plan.

Definitions

Author Model Definition

Woodruff (1997) Value Hierachy Model

He defined perceived value as “customer‟s perceived preference for an

evaluation of those product attributes, attribute performances, and

consequences arising from use that facilitate (or block) achieving the

customer‟s goals and purpose in use situations.

Holbrook and Hirschman (1982) Utilitarian and Hedonic Model

They had a notion that value should not only viewed from utilitarian

perspective in which the product is valued based on its performance or

functions, but also include the experiential perspective in

which the product is valued based on the experience or the feeling arouse

from consumption, including the symbolic

and hedonic aspect

Sheth et al (1991) Consumption Value Theory

They suggested five dimensions of value namely functional value which is

related to the utilitarian or functional purpose of the product, social value

which is related to the image obtained from the society, emotional value

which is related to the feeling arouse from using the product, epistemic value

which is related to the curiosity or desire for knowledge or novelty seeking,

and conditional value which is derived due to specific situation or

circumstances that faced by the consumers.

Holbrook (1996) Holbrook Typology of Consumer Value

His perceived value can be defined as “an interactive relativistic preference

experience.” By interactive He meant that value entails the relationship

between the customer and the product, it is comparative, subjective, and

specific to the context. He claimed that the customer perceived the value not

in the purchase stage however during the consumption stage.

(Source: Septa et al., 2016)

Customer Perceive Value of Banking Sector

In the recent years, the banking sector was changing remarkably due to several of external

factors. Karin (2011) has identified 5 notable factors below:

1) Competitors in the same industry such as foreign and local banks.

2) Competitors in different industry such as leasing and money lender companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) Change of IT technologies

4) Change of customer service channel

5) Marketing strategy development

Despite most of the banks have taken initiative in generating perceived value for the customers,

the customer’s dissatisfaction level was not improved (Johnston, 1997). (Juan et al., 2006)

highlighted that majority of the banks are defining the “customer value” as the value that the

customer generates for them, instead of the value that the Banks can offer their customers. Due

to this misperception, this paper will use Sanchez model to examine and analyze the customer

perceived value for banking sector. Since in the previous study such as Juan et al. (2006) was

using the Sanchez model to analyze the customer perceived value in banking sector, hence this is

the suitable model. According to Sanchez et al. (2006), there are two main components in

Sanchez model which are benefits and sacrifices. Table 1 below is showing the two main

components in banking sector:

Perceived Benefits Perceived Sacrifices

Economic Benefits

1)Lower financial cost

2)Higher return of investment

Price Sacrifice

1)Cost of travelling to branches

2)Cost of purchasing the smartphone

3)Cost of internet subscription

Emotional Benefits

1)Personalized and customised products

Time Sacrifice

1)Queue time

2)Processing time

Social Benefits

1)Service quality

2)Convenience

Effort Sacrifice

1)Adoption of new technology

Relationship Benefits

1)Service prior availing it

2)Post service

Risk

1)Wrongly made transactions due to no training is provided.

2)Transaction is unsuccessful due to poor connection.

Inconvenience

1)Website is not user-friendly

2)Limited of ATM

Table 1

Perceived Benefits

Economic Benefits

In the previous study, Reichheld (1993) highlighted that customers are exploring the lower

financial cost with more services by comparing the different banks in the market. Therefore,

customers are usually looking for more variety of customized products and personalized services

4) Change of customer service channel

5) Marketing strategy development

Despite most of the banks have taken initiative in generating perceived value for the customers,

the customer’s dissatisfaction level was not improved (Johnston, 1997). (Juan et al., 2006)

highlighted that majority of the banks are defining the “customer value” as the value that the

customer generates for them, instead of the value that the Banks can offer their customers. Due

to this misperception, this paper will use Sanchez model to examine and analyze the customer

perceived value for banking sector. Since in the previous study such as Juan et al. (2006) was

using the Sanchez model to analyze the customer perceived value in banking sector, hence this is

the suitable model. According to Sanchez et al. (2006), there are two main components in

Sanchez model which are benefits and sacrifices. Table 1 below is showing the two main

components in banking sector:

Perceived Benefits Perceived Sacrifices

Economic Benefits

1)Lower financial cost

2)Higher return of investment

Price Sacrifice

1)Cost of travelling to branches

2)Cost of purchasing the smartphone

3)Cost of internet subscription

Emotional Benefits

1)Personalized and customised products

Time Sacrifice

1)Queue time

2)Processing time

Social Benefits

1)Service quality

2)Convenience

Effort Sacrifice

1)Adoption of new technology

Relationship Benefits

1)Service prior availing it

2)Post service

Risk

1)Wrongly made transactions due to no training is provided.

2)Transaction is unsuccessful due to poor connection.

Inconvenience

1)Website is not user-friendly

2)Limited of ATM

Table 1

Perceived Benefits

Economic Benefits

In the previous study, Reichheld (1993) highlighted that customers are exploring the lower

financial cost with more services by comparing the different banks in the market. Therefore,

customers are usually looking for more variety of customized products and personalized services

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

at lower price (Anna, 2011). Customer satisfaction is achievable when customers are rewarded

through their cash flow is accelerated, increased in residual value of cash and decreased in

volatility of cash flow (Wang et. al., 2009). To increase the number of satisfied customers and

establish customer perceived value, the loyalty customers is important to act as a marketing

agent by spreading positive word-of-mouth (Reichheld and Sasser, 1990).

Emotional Benefits

There are several service channels provided by Bank such as ATM, telephone and internet in

order to satisfy customers with diverse intimacy preference. Majority of the customers are

expecting Bank is responsible to improve the quality of their lifestyle (Anna, 2011). Thus,

personalized service is highly demanded by the customers (Zineldin, 1995).

Social Benefits

Many studies have been conducted in the past to analyze the importance of service quality as

well as to enhance the customer loyalty (i.e. Ladhari et. al., 2011 and Robinson, 1999). Lee and

Sedigheh (2015) do believe that the increased of perceived value is followed by a higher service

quality. Perceived service quality, perceived value and customer satisfaction are the important

concepts in the retail banking industry despite these concepts are interlinked, intangible, complex

and relatively vague (Aleksandra and Boris, 2010).

Perceived convenience is one of the major factors that may influence the customer’s satisfaction

(Levesque & McDougall, 1996). Convenience has been defined by Lee and Sedigheh (2015)

that it is an ability to approach bank services through its location, operating hours, ATM

location, and the presence of a complete range of available services. Subsequently, Almossawi

(2001) affirmed that customers are highly concerned on bank’s location, the presence of 24-hour

ATM and parking availability in the bank premises.

Relationship Benefit

Empathetic service to customer is providing customer service with reliability and security which

will result to a higher perceived value (Lee and Sedigheh, 2015). For example, service before

availing it and post service. Service before availing it is demonstrating a concern about the

customer’s need on financial products or services. Furthermore, the post service is a service after

through their cash flow is accelerated, increased in residual value of cash and decreased in

volatility of cash flow (Wang et. al., 2009). To increase the number of satisfied customers and

establish customer perceived value, the loyalty customers is important to act as a marketing

agent by spreading positive word-of-mouth (Reichheld and Sasser, 1990).

Emotional Benefits

There are several service channels provided by Bank such as ATM, telephone and internet in

order to satisfy customers with diverse intimacy preference. Majority of the customers are

expecting Bank is responsible to improve the quality of their lifestyle (Anna, 2011). Thus,

personalized service is highly demanded by the customers (Zineldin, 1995).

Social Benefits

Many studies have been conducted in the past to analyze the importance of service quality as

well as to enhance the customer loyalty (i.e. Ladhari et. al., 2011 and Robinson, 1999). Lee and

Sedigheh (2015) do believe that the increased of perceived value is followed by a higher service

quality. Perceived service quality, perceived value and customer satisfaction are the important

concepts in the retail banking industry despite these concepts are interlinked, intangible, complex

and relatively vague (Aleksandra and Boris, 2010).

Perceived convenience is one of the major factors that may influence the customer’s satisfaction

(Levesque & McDougall, 1996). Convenience has been defined by Lee and Sedigheh (2015)

that it is an ability to approach bank services through its location, operating hours, ATM

location, and the presence of a complete range of available services. Subsequently, Almossawi

(2001) affirmed that customers are highly concerned on bank’s location, the presence of 24-hour

ATM and parking availability in the bank premises.

Relationship Benefit

Empathetic service to customer is providing customer service with reliability and security which

will result to a higher perceived value (Lee and Sedigheh, 2015). For example, service before

availing it and post service. Service before availing it is demonstrating a concern about the

customer’s need on financial products or services. Furthermore, the post service is a service after

sales to the customers about their concerns. Stone (2009) has emphasized that customers prefer

their queries are attended promptly and services are delivered timely.

Sacrifices

Price, Time and Effort Sacrifices

There are two broad types of customer perceived sacrifice: monetary costs and non-monetary

costs (De Ruyter et al., 1997). In the previous study, Sirohi et al. (1998) defined value-for-money

assessment as “what you get for what you pay”. Therefore, the perceived benefits are depending

on price paid. To maximize the perceived benefits, customers are willing to sacrifice additional

money to travel within a reasonable distance for better banking services, buying smartphone and

subscribe mobile internet to use banking services whenever wanted. Moreover, queue time and

processing time are common issue facing by customers in banking sector because majority of the

customer values their time is more important than dollar cost (Carothers and Adam, 1991). The

change of IT technology is providing the convenience to the customers to perform banking

transaction via internet, hence the effort in adoption of new technology is a sacrifice.

Risk and Inconvenience

Titrade et al., (2008) have identified the transaction risk of internet banking and generally, this

risk arises from fraudulent activity and processing errors which customers may potentially facing

these issues. Subsequently, customers may face some challenges despite various service channels

are provided and the common channels are internet banking and Automated Teller Machine

(ATM). For security reason and capacity issue, the service availability of these channels may be

limited.

2. Contrast the value proposition of Hong Leong Bank.

Customer value proposition is an sum of the total of the benefits which an company

promises the customers that will receive in the return of the customers with the payment. A

customer value chain is an proposition is an business or the marketing statement that it is

describes the why of the customers that should use the services. It is important as it gives the

reasons to the customers to why they have to use the products and that can make the Hong Leong

Bank to make differentiate from there competitors. They requires some of the things in the

company as(Chan, Heand Wang., 2012). Hong Leong Bank is providing their customer the

their queries are attended promptly and services are delivered timely.

Sacrifices

Price, Time and Effort Sacrifices

There are two broad types of customer perceived sacrifice: monetary costs and non-monetary

costs (De Ruyter et al., 1997). In the previous study, Sirohi et al. (1998) defined value-for-money

assessment as “what you get for what you pay”. Therefore, the perceived benefits are depending

on price paid. To maximize the perceived benefits, customers are willing to sacrifice additional

money to travel within a reasonable distance for better banking services, buying smartphone and

subscribe mobile internet to use banking services whenever wanted. Moreover, queue time and

processing time are common issue facing by customers in banking sector because majority of the

customer values their time is more important than dollar cost (Carothers and Adam, 1991). The

change of IT technology is providing the convenience to the customers to perform banking

transaction via internet, hence the effort in adoption of new technology is a sacrifice.

Risk and Inconvenience

Titrade et al., (2008) have identified the transaction risk of internet banking and generally, this

risk arises from fraudulent activity and processing errors which customers may potentially facing

these issues. Subsequently, customers may face some challenges despite various service channels

are provided and the common channels are internet banking and Automated Teller Machine

(ATM). For security reason and capacity issue, the service availability of these channels may be

limited.

2. Contrast the value proposition of Hong Leong Bank.

Customer value proposition is an sum of the total of the benefits which an company

promises the customers that will receive in the return of the customers with the payment. A

customer value chain is an proposition is an business or the marketing statement that it is

describes the why of the customers that should use the services. It is important as it gives the

reasons to the customers to why they have to use the products and that can make the Hong Leong

Bank to make differentiate from there competitors. They requires some of the things in the

company as(Chan, Heand Wang., 2012). Hong Leong Bank is providing their customer the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quality, they provides the best quality services to there customers at the reasonable and

affordable prices. Which can make them think about t use the services of the company as it

attract more them there competitors as they provides the best services to their customers in the

affordable prices and easily.

The entrepreneurship is to make the management vision to be achieved the entrepreneur

tries to do the best and required things in the organisation has to do the better things in the

organisation which will make them get achievement in their business. Hong Leong Bank

provides various incentive plans for the customer beneficial point of view so that more customers

get attracted towards their company and get familiarise with the Hong leong Bank. They use to

make and create new innovations where ever they are required and when ever they have to do it.

They want to make their bank the number one bank in their country and outside of that so they

can get more attraction of the peoples of the place as they are required to help them in achieving

the growth and popularity among the all of them(Chaston., 2014). Human resource plays an

important role in any of the organisation as it helps the organisation to achieve the growth and

success because they have to make the possible effects to make attract the people towards there

organisation so they can make then use their services and they can get most of the attraction of

the people. And this bank has the best skill and knowledge human resource working with their

organisation, they select the people according to the knowledge and the proper skill as it will

make people to attract more and so that they can provide the best services to customers according

to the customer’s needs and wants(Goworekand McGoldrick., 2015). The best thing is that they

all have the unity among them as they use to do all things in an proper manner and with all of

them together and they use to help one another in all the situations and makes them different too.

There is a friendly and healthy working environment in the Hong Leong Bank this helps in

working more effectively and freely for the employees. They always try to make improvements

in their operational activities which they do and they use to make it better day by day to make the

customers happy with their performance and it can make trust on the bank and they will like to

get connected with them only. And they even take care of the social responsibilities and they

respects that and try their maximum to make the society get benefit and can be happy with their

services. As it can help them to achieve a great trust from peoples living in the society and that

will help them to solve many of the problems(Huttand Speh., 2012). And they use to create the

affordable prices. Which can make them think about t use the services of the company as it

attract more them there competitors as they provides the best services to their customers in the

affordable prices and easily.

The entrepreneurship is to make the management vision to be achieved the entrepreneur

tries to do the best and required things in the organisation has to do the better things in the

organisation which will make them get achievement in their business. Hong Leong Bank

provides various incentive plans for the customer beneficial point of view so that more customers

get attracted towards their company and get familiarise with the Hong leong Bank. They use to

make and create new innovations where ever they are required and when ever they have to do it.

They want to make their bank the number one bank in their country and outside of that so they

can get more attraction of the peoples of the place as they are required to help them in achieving

the growth and popularity among the all of them(Chaston., 2014). Human resource plays an

important role in any of the organisation as it helps the organisation to achieve the growth and

success because they have to make the possible effects to make attract the people towards there

organisation so they can make then use their services and they can get most of the attraction of

the people. And this bank has the best skill and knowledge human resource working with their

organisation, they select the people according to the knowledge and the proper skill as it will

make people to attract more and so that they can provide the best services to customers according

to the customer’s needs and wants(Goworekand McGoldrick., 2015). The best thing is that they

all have the unity among them as they use to do all things in an proper manner and with all of

them together and they use to help one another in all the situations and makes them different too.

There is a friendly and healthy working environment in the Hong Leong Bank this helps in

working more effectively and freely for the employees. They always try to make improvements

in their operational activities which they do and they use to make it better day by day to make the

customers happy with their performance and it can make trust on the bank and they will like to

get connected with them only. And they even take care of the social responsibilities and they

respects that and try their maximum to make the society get benefit and can be happy with their

services. As it can help them to achieve a great trust from peoples living in the society and that

will help them to solve many of the problems(Huttand Speh., 2012). And they use to create the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

wealth for the society for their betterment as the society can make use of it and can get many of

the good things in their society.

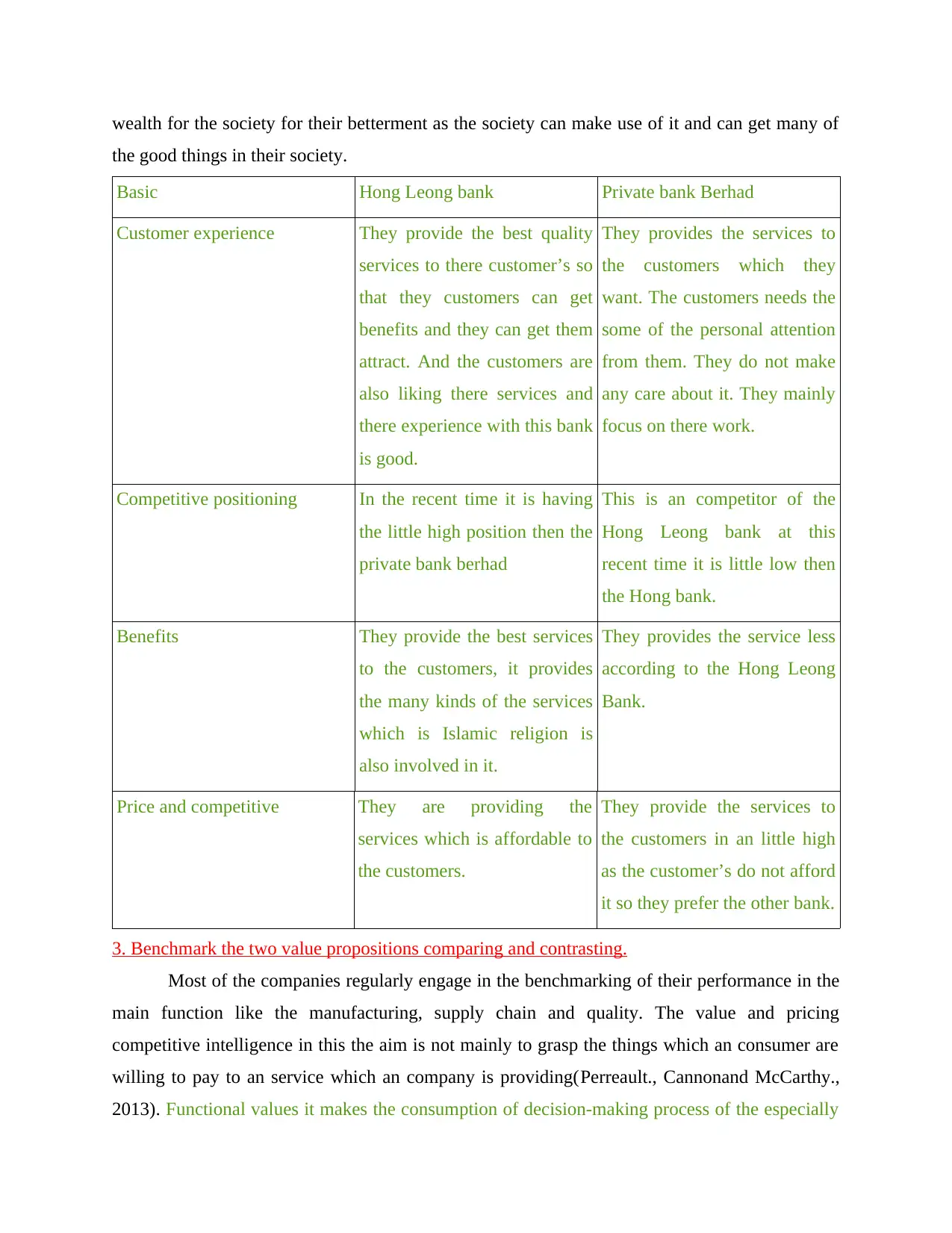

Basic Hong Leong bank Private bank Berhad

Customer experience They provide the best quality

services to there customer’s so

that they customers can get

benefits and they can get them

attract. And the customers are

also liking there services and

there experience with this bank

is good.

They provides the services to

the customers which they

want. The customers needs the

some of the personal attention

from them. They do not make

any care about it. They mainly

focus on there work.

Competitive positioning In the recent time it is having

the little high position then the

private bank berhad

This is an competitor of the

Hong Leong bank at this

recent time it is little low then

the Hong bank.

Benefits They provide the best services

to the customers, it provides

the many kinds of the services

which is Islamic religion is

also involved in it.

They provides the service less

according to the Hong Leong

Bank.

Price and competitive They are providing the

services which is affordable to

the customers.

They provide the services to

the customers in an little high

as the customer’s do not afford

it so they prefer the other bank.

3. Benchmark the two value propositions comparing and contrasting.

Most of the companies regularly engage in the benchmarking of their performance in the

main function like the manufacturing, supply chain and quality. The value and pricing

competitive intelligence in this the aim is not mainly to grasp the things which an consumer are

willing to pay to an service which an company is providing(Perreault., Cannonand McCarthy.,

2013). Functional values it makes the consumption of decision-making process of the especially

the good things in their society.

Basic Hong Leong bank Private bank Berhad

Customer experience They provide the best quality

services to there customer’s so

that they customers can get

benefits and they can get them

attract. And the customers are

also liking there services and

there experience with this bank

is good.

They provides the services to

the customers which they

want. The customers needs the

some of the personal attention

from them. They do not make

any care about it. They mainly

focus on there work.

Competitive positioning In the recent time it is having

the little high position then the

private bank berhad

This is an competitor of the

Hong Leong bank at this

recent time it is little low then

the Hong bank.

Benefits They provide the best services

to the customers, it provides

the many kinds of the services

which is Islamic religion is

also involved in it.

They provides the service less

according to the Hong Leong

Bank.

Price and competitive They are providing the

services which is affordable to

the customers.

They provide the services to

the customers in an little high

as the customer’s do not afford

it so they prefer the other bank.

3. Benchmark the two value propositions comparing and contrasting.

Most of the companies regularly engage in the benchmarking of their performance in the

main function like the manufacturing, supply chain and quality. The value and pricing

competitive intelligence in this the aim is not mainly to grasp the things which an consumer are

willing to pay to an service which an company is providing(Perreault., Cannonand McCarthy.,

2013). Functional values it makes the consumption of decision-making process of the especially

in some of the items. The social value of the products and the services which are been obtained

from the associations in positive or negative way. Emotional value- there are many different

kinds of the products and the services which are related with the emotions. And many of them

had been made the widespread of the feelings in the advertisement and all the organisation use

this. Epistemic value is an wish to know something different.

In value and pricing management practices benchmarking an getting an better or an

optimal price for particular services at most of the time can be achieved with the sufficient of the

market research and the analysis. This can help the company to get achieve the possible and the

aim which they have to do. Hong Leong Bank provides to their customers an best possible

services so that they can get the best services from them then the other banks and they can get

attracted by them in an proper and good way(Shaniand Chalasani., 2013).

Hong Leong Bank provides various alternative services and beneficial schemes to the

customers for gaining more attention of customers towards their bank. They also provide them

the services in an proper manner which will make them use the services to their bank in an easy

way so they would not face any such problems and as well as they could get attract more. They

try to give their customers the best quality of the services. And they follow the rules and

regulations of the and take cares of the societies responsibilities and make them fulfil it in an

proper way so that they can make the many things better in the society and can get the things

better for them and the society. This can help them to get the peoples trust on there company and

they will make efforts to use the services of the company. Hong Long Bank basically aims for

providing their best services to their customers and providing the customer satisfaction fully. The

comparison of Hong Long Bank and public bank because it is a strong group with the assets of

more than RM 140 billion as well as having a more comprehensive portfolio of the products and

services which is to be serve to the community. They have to expand the distribution network for

the convenience of the consumers with more than approx. 300 branches. Along with this they

focuses on the individual person or the consumers and on the basis of that they can make the

merger as well as integration which helps them in doing the acquisition of assets and liabilities.

4. what had been learnt from the module.

The people who are smart and wise they use to learn from the experience of the others. In

creating of the bridge in the gap between the My din value and the CPV towards the bank. As the

bank is providing the services to the customer in an best possible way and they are giving the

from the associations in positive or negative way. Emotional value- there are many different

kinds of the products and the services which are related with the emotions. And many of them

had been made the widespread of the feelings in the advertisement and all the organisation use

this. Epistemic value is an wish to know something different.

In value and pricing management practices benchmarking an getting an better or an

optimal price for particular services at most of the time can be achieved with the sufficient of the

market research and the analysis. This can help the company to get achieve the possible and the

aim which they have to do. Hong Leong Bank provides to their customers an best possible

services so that they can get the best services from them then the other banks and they can get

attracted by them in an proper and good way(Shaniand Chalasani., 2013).

Hong Leong Bank provides various alternative services and beneficial schemes to the

customers for gaining more attention of customers towards their bank. They also provide them

the services in an proper manner which will make them use the services to their bank in an easy

way so they would not face any such problems and as well as they could get attract more. They

try to give their customers the best quality of the services. And they follow the rules and

regulations of the and take cares of the societies responsibilities and make them fulfil it in an

proper way so that they can make the many things better in the society and can get the things

better for them and the society. This can help them to get the peoples trust on there company and

they will make efforts to use the services of the company. Hong Long Bank basically aims for

providing their best services to their customers and providing the customer satisfaction fully. The

comparison of Hong Long Bank and public bank because it is a strong group with the assets of

more than RM 140 billion as well as having a more comprehensive portfolio of the products and

services which is to be serve to the community. They have to expand the distribution network for

the convenience of the consumers with more than approx. 300 branches. Along with this they

focuses on the individual person or the consumers and on the basis of that they can make the

merger as well as integration which helps them in doing the acquisition of assets and liabilities.

4. what had been learnt from the module.

The people who are smart and wise they use to learn from the experience of the others. In

creating of the bridge in the gap between the My din value and the CPV towards the bank. As the

bank is providing the services to the customer in an best possible way and they are giving the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

services in the affordable prices as the customers can try to use it if they can pay that much of the

amount(Wilsonand Gilligan., 2012). In an new perceived value it is been analysed that if the

people will get the services in an premium price then they will make effort to buy it as they can

get attracted by the amount so they will be in an high quantity. Hong Leong Bank provides their

services at an affordable prices that attain more people to buy frequently and leads to beneficial

for the bank to attract more people and increase in bank services providing.

Implementation of the plan is important as it will after the plan is been made in the

organisation so that they can get the benefits according to the which the plan is been made. For

implementing the plans in the organisation they have to follow the 4 Ps in the organisation. Four

Ps are:

Products- There are the products which they have to give to there customer’s so that they

can get the benefits of the products and the services of the organisation.

Price- in this they have to plan the price according to the products and from the other

resources.

Place- they have to plan the place where they can sell there products. The place should be

perfect so that they can sell more products.

Promotion- in this the company use to choose the channel from which they have to

promote there product and services to there customer’s.

5. Plan to implement the value chain.

Implementing the plan is based on the two way, internally and externally and both has to

be followed and they have to make the required changes in the both of the following things has it

can make the proper plans in the organisation and that can make the people do the things ion the

better way in the bank(Marketing mix modelling.2016). They have to implement the new plans

which will help in getting new things and new ideas to fulfil the customer needs and wants. Hong

Leong Bank leads to innovations in their working plans and leads to updates in the working by

adopting new technologies for the bank. This influence to efficiency in the bank working.

CONCLUSION

From the above report it is been analysed that the marketing management is necessary in

the organisation as it helps the bank in getting the important strategies to plan and to implement

that in the organisation.

amount(Wilsonand Gilligan., 2012). In an new perceived value it is been analysed that if the

people will get the services in an premium price then they will make effort to buy it as they can

get attracted by the amount so they will be in an high quantity. Hong Leong Bank provides their

services at an affordable prices that attain more people to buy frequently and leads to beneficial

for the bank to attract more people and increase in bank services providing.

Implementation of the plan is important as it will after the plan is been made in the

organisation so that they can get the benefits according to the which the plan is been made. For

implementing the plans in the organisation they have to follow the 4 Ps in the organisation. Four

Ps are:

Products- There are the products which they have to give to there customer’s so that they

can get the benefits of the products and the services of the organisation.

Price- in this they have to plan the price according to the products and from the other

resources.

Place- they have to plan the place where they can sell there products. The place should be

perfect so that they can sell more products.

Promotion- in this the company use to choose the channel from which they have to

promote there product and services to there customer’s.

5. Plan to implement the value chain.

Implementing the plan is based on the two way, internally and externally and both has to

be followed and they have to make the required changes in the both of the following things has it

can make the proper plans in the organisation and that can make the people do the things ion the

better way in the bank(Marketing mix modelling.2016). They have to implement the new plans

which will help in getting new things and new ideas to fulfil the customer needs and wants. Hong

Leong Bank leads to innovations in their working plans and leads to updates in the working by

adopting new technologies for the bank. This influence to efficiency in the bank working.

CONCLUSION

From the above report it is been analysed that the marketing management is necessary in

the organisation as it helps the bank in getting the important strategies to plan and to implement

that in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Agnihotri, R and et.al., 2016. Social media: Influencing customer satisfaction in B2B sales.

Industrial Marketing Management. 53. pp.172-180.

Baker, M.J and Saren, M. eds., 2016. Marketing theory: a student text. Sage.

Baker, M.J and Saren, M. eds., 2016. Marketing theory: a student text. Sage.

Ball, D and et.al., 2012. International business. McGraw-Hill Higher Education.

Carraher, S.M and Paridon, T.J., 2015. Entrepreneurship journal rankings across the discipline.

Journal of Small Business Strategy. 19(2). pp.89-98.

Chan, H.K., He, H and Wang, W.Y., 2012. Green marketing and its impact on supply chain

management in industrial markets. Industrial Marketing Management. 41(4). pp.557-

562.

Chaston, I., 2014. Small business marketing. Palgrave Macmillan.

Goworek, H and McGoldrick, P., 2015. Retail Marketing Management: Principles and Practice.

Pearson Higher Ed.

Hutt, M.D and Speh, T.W., 2012. Business marketing management: B2B. Cengage Learning.

Mullins, J., Walker, O.C and Boyd Jr, H.W., 2012. Marketing management: A strategic

decision-making approach. McGraw-Hill Higher Education.

Mullins, J., Walker, O.C and Boyd Jr, H.W., 2012. Marketing management: A strategic

decision-making approach. McGraw-Hill Higher Education.

Peñaloza, L., Toulouse, N and Visconti, L.M. eds., 2013. Marketing management: A cultural

perspective. Routledge.

Perreault Jr, W., Cannon, J and McCarthy, E.J., 2013. Basic marketing. McGraw-Hill Higher

Education.

Shani, D and Chalasani, S., 2013. Exploiting niches using relationship marketing. Journal of

Services Marketing.

Wilson, R.M and Gilligan, C., 2012. Strategic marketing management. Routledge.

Online

Marketing mix modelling.2016.Available through

<https://analyticpartners.com/services/marketing-mix-modeling/>.Accessed on 5th May

2017.

Marketing Strategy.2016.Available through

<https://www.marketingdonut.co.uk/marketing/marketing-strategy>.Accessed on 5th

May 2017.

Aleksandra Pisnik Korda and Boris Snoj. (2010). Development, Validity and Reliability of

Perceived Service Quality in Retail Banking and its Relationship With Perceived Value

and Customer Satisfaction. Managing Global Transitions, Vol 8, No 2.

Anna Omarini. (2011). Retail banking: the challenge of getting customer intimate. Banks and

Bank Systems, Volume 6, Issue 3.

Becker, Gary S. (1965), Theory of the Allocation of Time. Economic Journal, 75 (September),

493-517.

Books and journals

Agnihotri, R and et.al., 2016. Social media: Influencing customer satisfaction in B2B sales.

Industrial Marketing Management. 53. pp.172-180.

Baker, M.J and Saren, M. eds., 2016. Marketing theory: a student text. Sage.

Baker, M.J and Saren, M. eds., 2016. Marketing theory: a student text. Sage.

Ball, D and et.al., 2012. International business. McGraw-Hill Higher Education.

Carraher, S.M and Paridon, T.J., 2015. Entrepreneurship journal rankings across the discipline.

Journal of Small Business Strategy. 19(2). pp.89-98.

Chan, H.K., He, H and Wang, W.Y., 2012. Green marketing and its impact on supply chain

management in industrial markets. Industrial Marketing Management. 41(4). pp.557-

562.

Chaston, I., 2014. Small business marketing. Palgrave Macmillan.

Goworek, H and McGoldrick, P., 2015. Retail Marketing Management: Principles and Practice.

Pearson Higher Ed.

Hutt, M.D and Speh, T.W., 2012. Business marketing management: B2B. Cengage Learning.

Mullins, J., Walker, O.C and Boyd Jr, H.W., 2012. Marketing management: A strategic

decision-making approach. McGraw-Hill Higher Education.

Mullins, J., Walker, O.C and Boyd Jr, H.W., 2012. Marketing management: A strategic

decision-making approach. McGraw-Hill Higher Education.

Peñaloza, L., Toulouse, N and Visconti, L.M. eds., 2013. Marketing management: A cultural

perspective. Routledge.

Perreault Jr, W., Cannon, J and McCarthy, E.J., 2013. Basic marketing. McGraw-Hill Higher

Education.

Shani, D and Chalasani, S., 2013. Exploiting niches using relationship marketing. Journal of

Services Marketing.

Wilson, R.M and Gilligan, C., 2012. Strategic marketing management. Routledge.

Online

Marketing mix modelling.2016.Available through

<https://analyticpartners.com/services/marketing-mix-modeling/>.Accessed on 5th May

2017.

Marketing Strategy.2016.Available through

<https://www.marketingdonut.co.uk/marketing/marketing-strategy>.Accessed on 5th

May 2017.

Aleksandra Pisnik Korda and Boris Snoj. (2010). Development, Validity and Reliability of

Perceived Service Quality in Retail Banking and its Relationship With Perceived Value

and Customer Satisfaction. Managing Global Transitions, Vol 8, No 2.

Anna Omarini. (2011). Retail banking: the challenge of getting customer intimate. Banks and

Bank Systems, Volume 6, Issue 3.

Becker, Gary S. (1965), Theory of the Allocation of Time. Economic Journal, 75 (September),

493-517.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.