Financial Principles and Analysis Assignment: Hoosier Racing Company

VerifiedAdded on 2022/10/06

|9

|1899

|457

Report

AI Summary

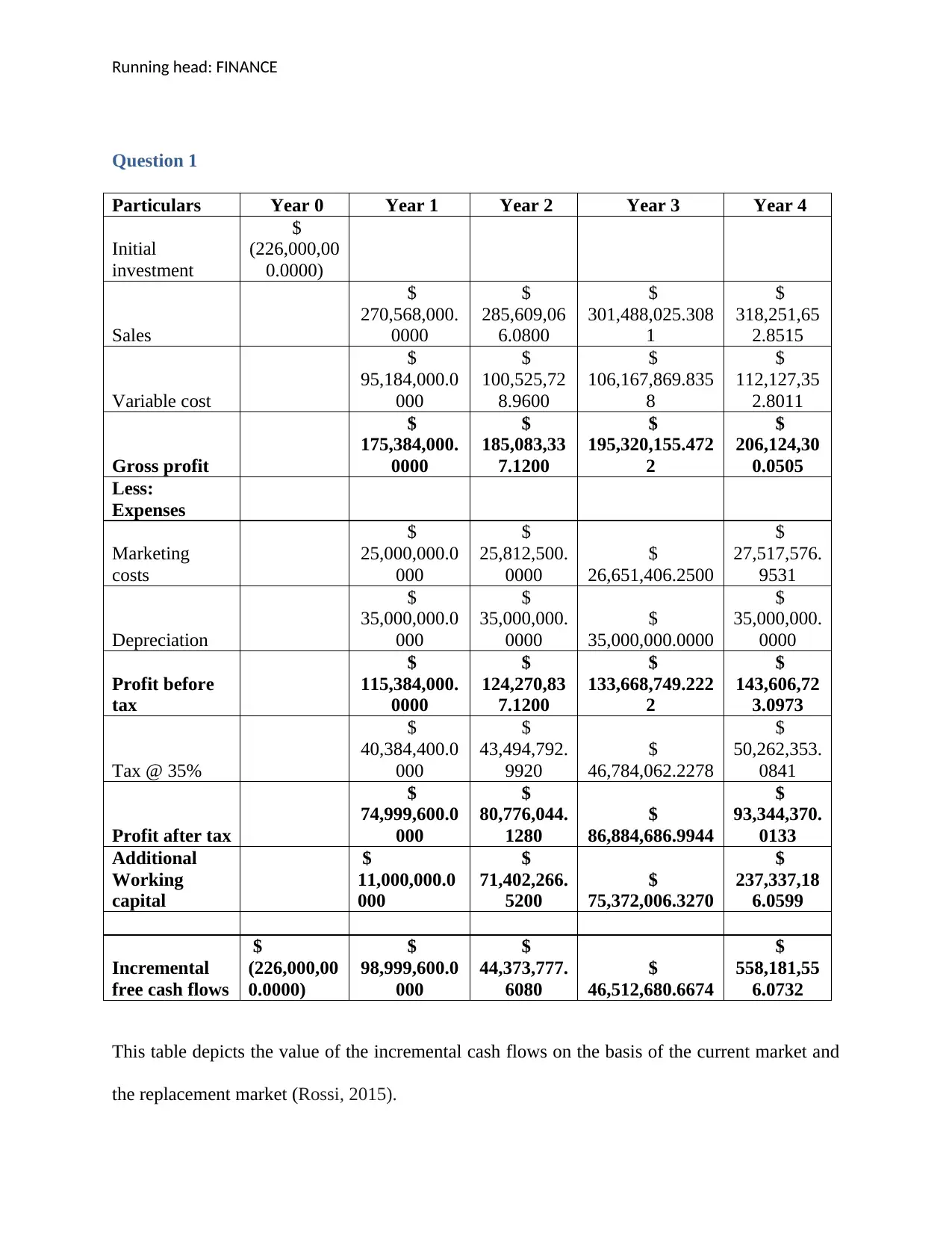

This report provides a comprehensive financial analysis of the Hoosier Racing Company, evaluating its investment decisions using various capital budgeting techniques. The analysis includes the calculation of incremental free cash flows, net present value (NPV), internal rate of return (IRR), payback period, discounted payback period, and profitability index (PI). The report examines the accounting treatment of depreciation and its impact on project feasibility. The study determines the feasibility of the project based on the calculated NPV, IRR, and payback periods. Furthermore, the report discusses mutually exclusive projects and their evaluation criteria, concluding with a recommendation on whether the project should be accepted based on the financial metrics. The report utilizes a discounting rate of 16% and provides detailed calculations and interpretations of each financial metric to assess the project's viability and profitability, considering the company's investment and return expectations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.