Hospitality Management: Asset Management and Acquisition Report

VerifiedAdded on 2021/10/05

|29

|7081

|77

Report

AI Summary

This report provides a comprehensive analysis of asset management within the context of a hospitality business, specifically focusing on Café B. It examines various factors influencing asset acquisition, including inflation, post-tax returns, and effective annual rates, alongside mandatory acquisitions driven by revenue growth and operational objectives. The report delves into depreciation methods, recommending the straight-line method for its simplicity and suitability for small firms, while considering factors like asset cost, useful life, and salvage value. It details the selection of suppliers for assets such as impinger ovens and POS systems, evaluating criteria like cost, reputation, and after-sales services. Furthermore, the report recommends the implementation of the BMC asset management system for enhanced visibility, control, and compliance of IT assets. The report also covers financial aspects, including finance and leasing costs, setup costs, maintenance costs, and training costs. Finally, it addresses funding options for asset purchases, suggesting borrowing for POS systems and impinger ovens and the use of retained earnings for refurbishments.

Running head: HOSPITALITY MANAGEMENT

Hospitality management

Name of the student

Name of the university

Student ID

Author note

Hospitality management

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1HOSPITALITY MANAGEMENT

Table of Contents

Section 1 – acquisition of asset..................................................................................................3

Part 1......................................................................................................................................3

Part 2......................................................................................................................................3

Part 3......................................................................................................................................3

Part 4(a)(i)..............................................................................................................................5

Part 4(b)(i)..............................................................................................................................6

Part 4(b)(ii).............................................................................................................................6

Part 4(c)(i)..............................................................................................................................7

Part 5......................................................................................................................................7

Part 6(a)(i)..............................................................................................................................7

Part 6(a)(ii).............................................................................................................................7

Part 6(a)(iii)............................................................................................................................8

Part 6(a)(iv)............................................................................................................................8

Part 6(b)..................................................................................................................................8

Part 6(c)(i)..............................................................................................................................8

Part 6(c)(ii).............................................................................................................................9

Part 6(c)(iii)............................................................................................................................9

Part 6(d)(i)..............................................................................................................................9

Part 7......................................................................................................................................9

Section 2 – Asset management system (BMC asset management)..........................................10

Part 2(a)................................................................................................................................10

Part 2(b)................................................................................................................................10

Part 2(c)................................................................................................................................11

Part 3(a)(i)............................................................................................................................11

Table of Contents

Section 1 – acquisition of asset..................................................................................................3

Part 1......................................................................................................................................3

Part 2......................................................................................................................................3

Part 3......................................................................................................................................3

Part 4(a)(i)..............................................................................................................................5

Part 4(b)(i)..............................................................................................................................6

Part 4(b)(ii).............................................................................................................................6

Part 4(c)(i)..............................................................................................................................7

Part 5......................................................................................................................................7

Part 6(a)(i)..............................................................................................................................7

Part 6(a)(ii).............................................................................................................................7

Part 6(a)(iii)............................................................................................................................8

Part 6(a)(iv)............................................................................................................................8

Part 6(b)..................................................................................................................................8

Part 6(c)(i)..............................................................................................................................8

Part 6(c)(ii).............................................................................................................................9

Part 6(c)(iii)............................................................................................................................9

Part 6(d)(i)..............................................................................................................................9

Part 7......................................................................................................................................9

Section 2 – Asset management system (BMC asset management)..........................................10

Part 2(a)................................................................................................................................10

Part 2(b)................................................................................................................................10

Part 2(c)................................................................................................................................11

Part 3(a)(i)............................................................................................................................11

2HOSPITALITY MANAGEMENT

Part 3(b)................................................................................................................................11

Part 3(c)................................................................................................................................11

Part 3(d)(i)............................................................................................................................11

Part 3(d)(ii)...........................................................................................................................12

Part 4(a)................................................................................................................................12

Part 5(a)(i)............................................................................................................................12

Part 5(a)(ii)...........................................................................................................................13

Part 5(b)(i)............................................................................................................................13

Part 5(b)(ii)...........................................................................................................................13

Part (5)(c).............................................................................................................................13

Part 6(a)................................................................................................................................14

Part 6(b)................................................................................................................................14

Part 7(a)................................................................................................................................14

Part 7(b)................................................................................................................................15

Part 7(c)................................................................................................................................15

Section 3 – Asset Replacement................................................................................................15

Part 1(a)(i)............................................................................................................................15

Part 1(b)(i)............................................................................................................................15

Part 1(c)(i)............................................................................................................................16

Part 1(c)(ii)...........................................................................................................................16

Part 1(c)(iii)..........................................................................................................................16

Part 2(a)................................................................................................................................16

Reference and bibliography.....................................................................................................17

Appendix..................................................................................................................................20

1. Contract agreement.......................................................................................................20

2. Loan agreement.............................................................................................................24

Part 3(b)................................................................................................................................11

Part 3(c)................................................................................................................................11

Part 3(d)(i)............................................................................................................................11

Part 3(d)(ii)...........................................................................................................................12

Part 4(a)................................................................................................................................12

Part 5(a)(i)............................................................................................................................12

Part 5(a)(ii)...........................................................................................................................13

Part 5(b)(i)............................................................................................................................13

Part 5(b)(ii)...........................................................................................................................13

Part (5)(c).............................................................................................................................13

Part 6(a)................................................................................................................................14

Part 6(b)................................................................................................................................14

Part 7(a)................................................................................................................................14

Part 7(b)................................................................................................................................15

Part 7(c)................................................................................................................................15

Section 3 – Asset Replacement................................................................................................15

Part 1(a)(i)............................................................................................................................15

Part 1(b)(i)............................................................................................................................15

Part 1(c)(i)............................................................................................................................16

Part 1(c)(ii)...........................................................................................................................16

Part 1(c)(iii)..........................................................................................................................16

Part 2(a)................................................................................................................................16

Reference and bibliography.....................................................................................................17

Appendix..................................................................................................................................20

1. Contract agreement.......................................................................................................20

2. Loan agreement.............................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3HOSPITALITY MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4HOSPITALITY MANAGEMENT

Section 1 – acquisition of asset

Part 1

Various particular factors are there those required to be considered while thinking if

acquiring Impinger Oven, Alfresco Dining area, iPad systems and paperless online booking

system. These factors are as follows –

Inflation – if the inflation rate of any country changed the purchasing power of the

people also changed. Hence, while considering acquiring of any asset effect of

inflations shall also be taken into consideration (Glasson and Gibbons 2015).

Post – tax return – after tax return is always lower as compared to pre-tax return.

Hence, Café B must consider regarding the possible return that may be created from

the asset. Hence, before taking final decision regarding investment post tax return

must be computed.

Effective annual rate – generally the nominal rate of return does not match with the

annual return rate owing to the compounding rate in the year. Hence, it must be

considered before considering the investment (Campbell, Jardine and McGlynn

2016).

Part 2

Mandatory acquisitions are taken into consideration with the concern of various

aspects like growth of revenue, capacity of production and margin of profit. It shall further be

considered that the acquisition shall be made in such manner that it shall fulfil the key

objectives of the entity. These key objectives are depending on the paperless system of

inventory control, POS ordering and enhancing the payment amount of dividend over the 5

years time period. Further, the asset management register shall also be taken into

consideration for details regarding the accounts payable, general ledger and system for

managing the assets (Garleanu and Pedersen 2018).

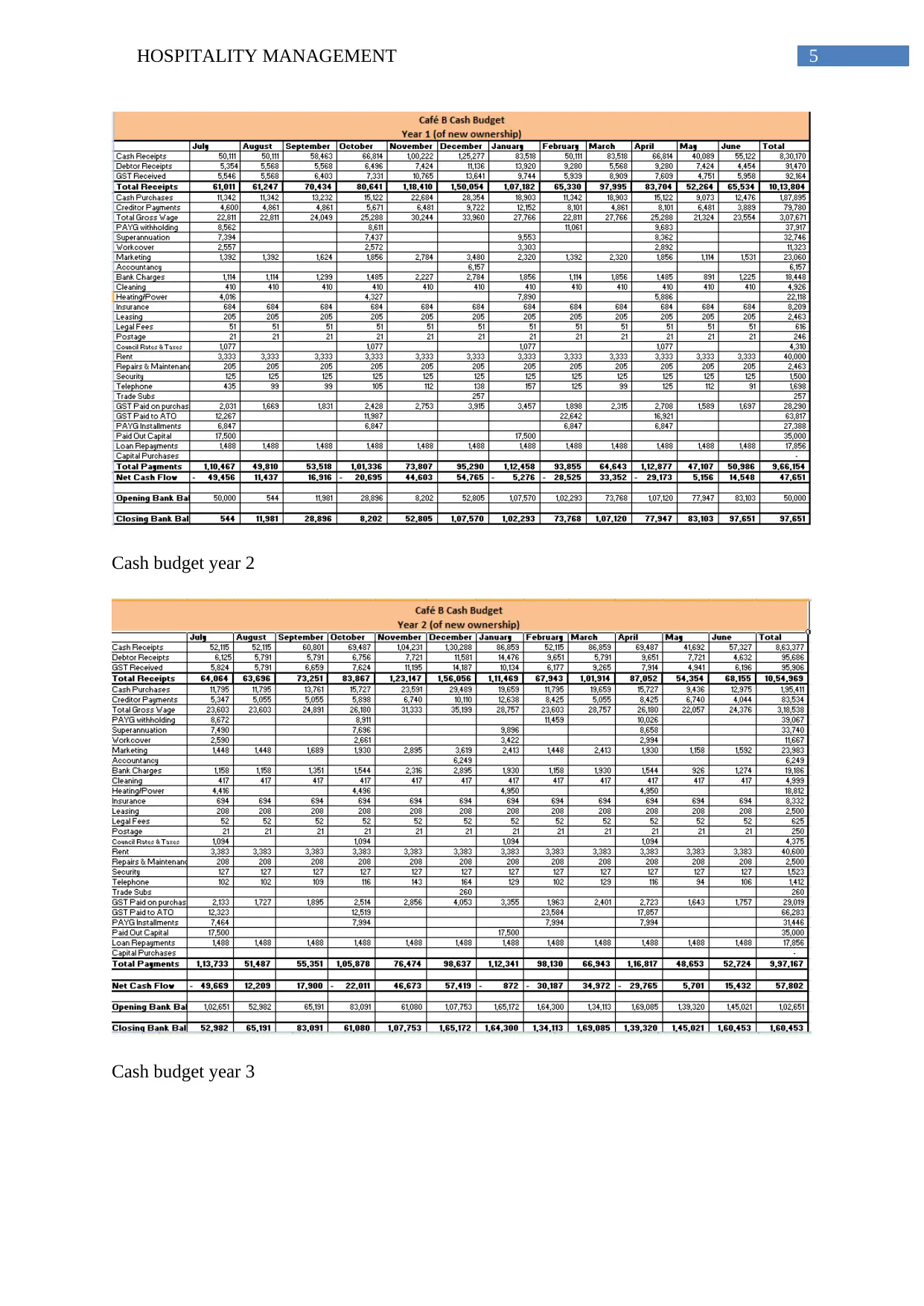

Part 3

Cash budget year 1

Section 1 – acquisition of asset

Part 1

Various particular factors are there those required to be considered while thinking if

acquiring Impinger Oven, Alfresco Dining area, iPad systems and paperless online booking

system. These factors are as follows –

Inflation – if the inflation rate of any country changed the purchasing power of the

people also changed. Hence, while considering acquiring of any asset effect of

inflations shall also be taken into consideration (Glasson and Gibbons 2015).

Post – tax return – after tax return is always lower as compared to pre-tax return.

Hence, Café B must consider regarding the possible return that may be created from

the asset. Hence, before taking final decision regarding investment post tax return

must be computed.

Effective annual rate – generally the nominal rate of return does not match with the

annual return rate owing to the compounding rate in the year. Hence, it must be

considered before considering the investment (Campbell, Jardine and McGlynn

2016).

Part 2

Mandatory acquisitions are taken into consideration with the concern of various

aspects like growth of revenue, capacity of production and margin of profit. It shall further be

considered that the acquisition shall be made in such manner that it shall fulfil the key

objectives of the entity. These key objectives are depending on the paperless system of

inventory control, POS ordering and enhancing the payment amount of dividend over the 5

years time period. Further, the asset management register shall also be taken into

consideration for details regarding the accounts payable, general ledger and system for

managing the assets (Garleanu and Pedersen 2018).

Part 3

Cash budget year 1

5HOSPITALITY MANAGEMENT

Cash budget year 2

Cash budget year 3

Cash budget year 2

Cash budget year 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6HOSPITALITY MANAGEMENT

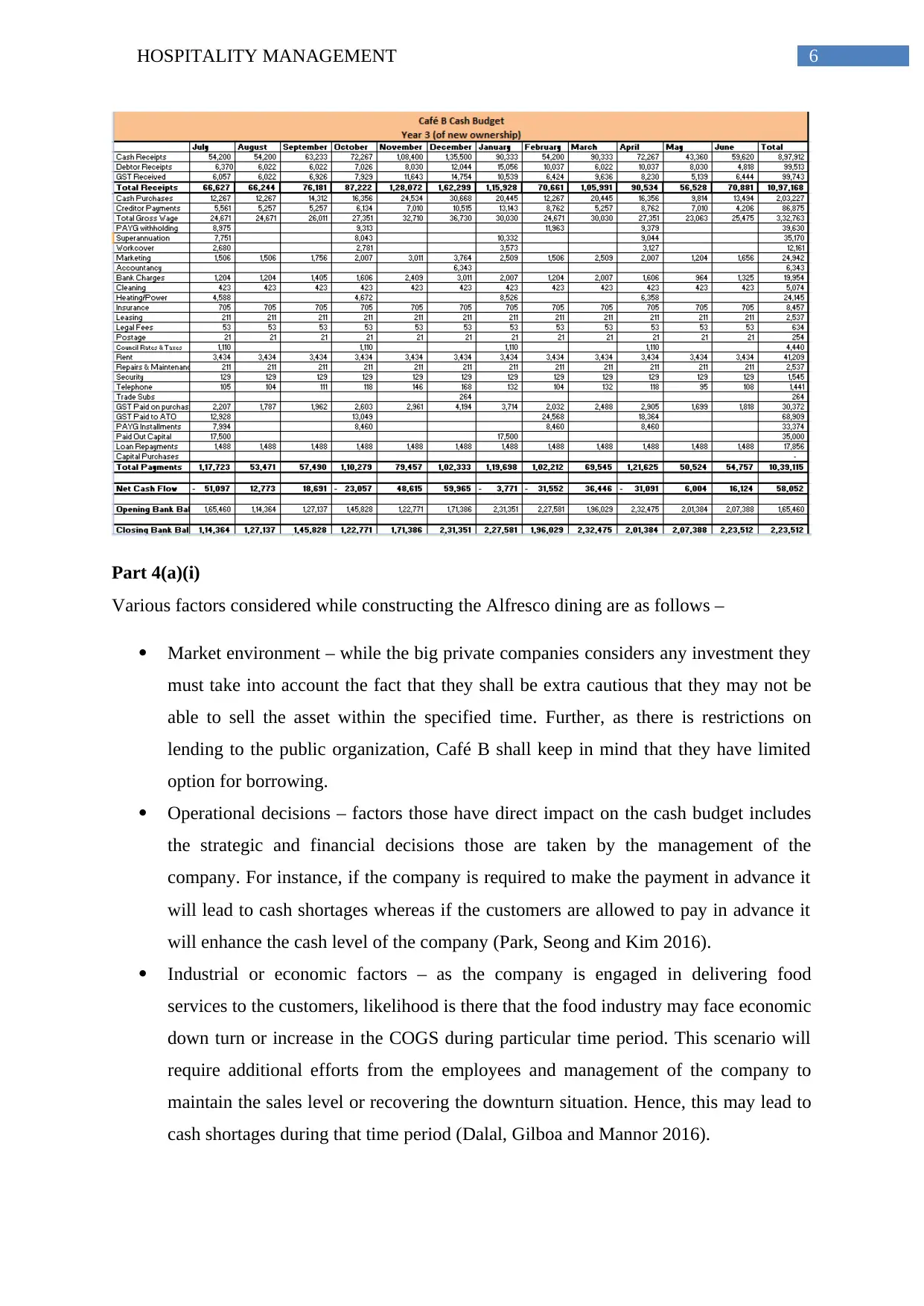

Part 4(a)(i)

Various factors considered while constructing the Alfresco dining are as follows –

Market environment – while the big private companies considers any investment they

must take into account the fact that they shall be extra cautious that they may not be

able to sell the asset within the specified time. Further, as there is restrictions on

lending to the public organization, Café B shall keep in mind that they have limited

option for borrowing.

Operational decisions – factors those have direct impact on the cash budget includes

the strategic and financial decisions those are taken by the management of the

company. For instance, if the company is required to make the payment in advance it

will lead to cash shortages whereas if the customers are allowed to pay in advance it

will enhance the cash level of the company (Park, Seong and Kim 2016).

Industrial or economic factors – as the company is engaged in delivering food

services to the customers, likelihood is there that the food industry may face economic

down turn or increase in the COGS during particular time period. This scenario will

require additional efforts from the employees and management of the company to

maintain the sales level or recovering the downturn situation. Hence, this may lead to

cash shortages during that time period (Dalal, Gilboa and Mannor 2016).

Part 4(a)(i)

Various factors considered while constructing the Alfresco dining are as follows –

Market environment – while the big private companies considers any investment they

must take into account the fact that they shall be extra cautious that they may not be

able to sell the asset within the specified time. Further, as there is restrictions on

lending to the public organization, Café B shall keep in mind that they have limited

option for borrowing.

Operational decisions – factors those have direct impact on the cash budget includes

the strategic and financial decisions those are taken by the management of the

company. For instance, if the company is required to make the payment in advance it

will lead to cash shortages whereas if the customers are allowed to pay in advance it

will enhance the cash level of the company (Park, Seong and Kim 2016).

Industrial or economic factors – as the company is engaged in delivering food

services to the customers, likelihood is there that the food industry may face economic

down turn or increase in the COGS during particular time period. This scenario will

require additional efforts from the employees and management of the company to

maintain the sales level or recovering the downturn situation. Hence, this may lead to

cash shortages during that time period (Dalal, Gilboa and Mannor 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7HOSPITALITY MANAGEMENT

Part 4(b)(i)

It is recommended that for all the 3 assets classified by Café B it shall use straight line

method for charging depreciation on those assets. Under this method, the carrying value of

the asset is reduced gradually over the term of useful life of the asset. This method is used

where any particular pattern of using the asset is not identified and this method is considered

as the easiest method of charging depreciation as it results into less number of calculation

errors. As per this method the asset’s initial cost is determined and its estimated salvage

value is deducted from it (Del Giudice, Manganelli and De Paola 2016). Thereafter the useful

life of the asset is determined and the initial cost reduced by salvage value is divided by the

useful life to get the amount of depreciation. This method of charging depreciation is

recommended due to the below mentioned reasons –

Simplicity – it is the simplest method of charging depreciation as the calculation

method is very simple and even an ordinary person also can understand the

calculation

Appropriate for small firms – this method is most appropriate for the small firms as it

is simple, easy and suitable to the size of the firm (Cheng and Wei 2017)

Comparison – as amount of depreciation charged remain same all over the useful life

of the asset, profit comparison for different years is easier through this method.

Suitability – this method is suitable for those assets which can be used consistently

over the useful life of the assets and where the useful life can be reliable estimated.

Part 4(b)(ii)

Factors taken into consideration while selecting the straight line method for charging

depreciation are as follows –

Cost of asset

Useful life estimated for the asset

Estimated salvage value of asset

Obsolescence shall be considered while determining the useful life of the asset

Maintenance of capital

Managerial decision

Suitability to the organization

Part 4(b)(i)

It is recommended that for all the 3 assets classified by Café B it shall use straight line

method for charging depreciation on those assets. Under this method, the carrying value of

the asset is reduced gradually over the term of useful life of the asset. This method is used

where any particular pattern of using the asset is not identified and this method is considered

as the easiest method of charging depreciation as it results into less number of calculation

errors. As per this method the asset’s initial cost is determined and its estimated salvage

value is deducted from it (Del Giudice, Manganelli and De Paola 2016). Thereafter the useful

life of the asset is determined and the initial cost reduced by salvage value is divided by the

useful life to get the amount of depreciation. This method of charging depreciation is

recommended due to the below mentioned reasons –

Simplicity – it is the simplest method of charging depreciation as the calculation

method is very simple and even an ordinary person also can understand the

calculation

Appropriate for small firms – this method is most appropriate for the small firms as it

is simple, easy and suitable to the size of the firm (Cheng and Wei 2017)

Comparison – as amount of depreciation charged remain same all over the useful life

of the asset, profit comparison for different years is easier through this method.

Suitability – this method is suitable for those assets which can be used consistently

over the useful life of the assets and where the useful life can be reliable estimated.

Part 4(b)(ii)

Factors taken into consideration while selecting the straight line method for charging

depreciation are as follows –

Cost of asset

Useful life estimated for the asset

Estimated salvage value of asset

Obsolescence shall be considered while determining the useful life of the asset

Maintenance of capital

Managerial decision

Suitability to the organization

8HOSPITALITY MANAGEMENT

Part 4(c)(i)

Café B shall made all the acquisitions during December that is before the end of the

1st year as the company will be able to generate most amount of sales during that month.

Further, owing to sufficiency of cash acquisition of the asset will not have any adverse impact

on company’s cash status (Komljenovic et al. 2016).

Part 5

Various steps have been taken into consideration for improving the services and food

products provided by Café B. for assuring the quality of food, the company decided to

purchase the products from the reputed suppliers in the market. Further, for providing the

seating arrangements under the open air it has increased the patronage and considered

refurbishing of the dining space. As wide numbers of suppliers are there in the market

bargaining power of the purchasers are high and hence, Café B can purchase the product at

comparatively lower price if proper research is carried out in the market. This will further

enable the company to achieve 4% annual growth for revenue.

Café B is required to purchase 3 POS systems and 10 impinger oven to achieve its

business objectives. It will further enable the company to expand the capacity of pizza

production through producing 60 pizzas additionally per hour. Further the company will

consider the environment friendly equipment those will also ensure the sustainability aspect

of environment. The same aspects will be considered while implementing the POS systems

that will also enhance the operational efficiency of the company.

Part 6(a)(i)

Finance cost is the cost of borrowing the funds. It includes the interest charges and

other charges those are involved in borrowing the amount for purchasing the asset. On the

other hand, leasing costs states all the capital costs and amount spend for improvements of

the capital, painting, equipment, partitioning, decorating. Leasing will enable Café B to

control the asset as per the agreed terms with payment of instalments and the rates that will

cover the interest and depreciation charges to cover the capital cost (Ang 2014). However,

leasing cost will not be applicable for Café B as it will purchase all the assets instead of

taking it for lease.

Part 6(a)(ii)

Set up cost is the cost associated with the set up of piece of the production equipment.

Set up cost includes cost of setting up the mechanic, scheduling cost, cost of keeping the

Part 4(c)(i)

Café B shall made all the acquisitions during December that is before the end of the

1st year as the company will be able to generate most amount of sales during that month.

Further, owing to sufficiency of cash acquisition of the asset will not have any adverse impact

on company’s cash status (Komljenovic et al. 2016).

Part 5

Various steps have been taken into consideration for improving the services and food

products provided by Café B. for assuring the quality of food, the company decided to

purchase the products from the reputed suppliers in the market. Further, for providing the

seating arrangements under the open air it has increased the patronage and considered

refurbishing of the dining space. As wide numbers of suppliers are there in the market

bargaining power of the purchasers are high and hence, Café B can purchase the product at

comparatively lower price if proper research is carried out in the market. This will further

enable the company to achieve 4% annual growth for revenue.

Café B is required to purchase 3 POS systems and 10 impinger oven to achieve its

business objectives. It will further enable the company to expand the capacity of pizza

production through producing 60 pizzas additionally per hour. Further the company will

consider the environment friendly equipment those will also ensure the sustainability aspect

of environment. The same aspects will be considered while implementing the POS systems

that will also enhance the operational efficiency of the company.

Part 6(a)(i)

Finance cost is the cost of borrowing the funds. It includes the interest charges and

other charges those are involved in borrowing the amount for purchasing the asset. On the

other hand, leasing costs states all the capital costs and amount spend for improvements of

the capital, painting, equipment, partitioning, decorating. Leasing will enable Café B to

control the asset as per the agreed terms with payment of instalments and the rates that will

cover the interest and depreciation charges to cover the capital cost (Ang 2014). However,

leasing cost will not be applicable for Café B as it will purchase all the assets instead of

taking it for lease.

Part 6(a)(ii)

Set up cost is the cost associated with the set up of piece of the production equipment.

Set up cost includes cost of setting up the mechanic, scheduling cost, cost of keeping the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9HOSPITALITY MANAGEMENT

record and testing of 1st few units of the output. From the given scenario it can be stated that

Café B will incur $ 45,000 for setting up for modifications of the floor plans.

Part 6(a)(iii)

Maintenance cost is the cost that is incurred for keeping the asset in god working

order. While purchasing the asset apart from purchasing cost the purchaser shall also consider

the maintenance cost of the asset. From the given scenario it can be stated that Café B will

require incurring $ 205 per month for as maintenance cost.

Part 6(a)(iv)

Training costs for the staffs is incurred to provide training to the employees to use any

new asset smoothly. From the given scenario it can be stated that Café B will require

incurring $ 2,000 for providing training to the staffs.

Part 6(b)

POS used as the synonym for point of sale. POS transactions take place among the

merchant and customers whenever the service or product is purchased through common use

of POS systems for completing transaction. Merchants generally use the POS system for

completing the sales transaction. It includes both POS software as well as POS hardware for

creating POS machine to process the payment and transactions. Under POS system cash

registers are not evolved and it lacks various various features and functions of the modern

day POS system. Cash register can be considered as the solution for POS system technically

(Lam, Lee and Tsai 2018). However, it can be used for enhancing the staff’s efficiency

regarding customer solution. Further, it will improve the efficiency and will minimize the

human errors apart from increasing the sales level.

Part 6(c)(i)

Asset acquisition Names of the suppliers

Refurbishment of dining area Kitchen Equipment Australia

West Coast Office Equipment

Impinger Oven BTU

Sydney Fire Bricks

POS systems Retail Express

Maplewave

record and testing of 1st few units of the output. From the given scenario it can be stated that

Café B will incur $ 45,000 for setting up for modifications of the floor plans.

Part 6(a)(iii)

Maintenance cost is the cost that is incurred for keeping the asset in god working

order. While purchasing the asset apart from purchasing cost the purchaser shall also consider

the maintenance cost of the asset. From the given scenario it can be stated that Café B will

require incurring $ 205 per month for as maintenance cost.

Part 6(a)(iv)

Training costs for the staffs is incurred to provide training to the employees to use any

new asset smoothly. From the given scenario it can be stated that Café B will require

incurring $ 2,000 for providing training to the staffs.

Part 6(b)

POS used as the synonym for point of sale. POS transactions take place among the

merchant and customers whenever the service or product is purchased through common use

of POS systems for completing transaction. Merchants generally use the POS system for

completing the sales transaction. It includes both POS software as well as POS hardware for

creating POS machine to process the payment and transactions. Under POS system cash

registers are not evolved and it lacks various various features and functions of the modern

day POS system. Cash register can be considered as the solution for POS system technically

(Lam, Lee and Tsai 2018). However, it can be used for enhancing the staff’s efficiency

regarding customer solution. Further, it will improve the efficiency and will minimize the

human errors apart from increasing the sales level.

Part 6(c)(i)

Asset acquisition Names of the suppliers

Refurbishment of dining area Kitchen Equipment Australia

West Coast Office Equipment

Impinger Oven BTU

Sydney Fire Bricks

POS systems Retail Express

Maplewave

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10HOSPITALITY MANAGEMENT

Part 6(c)(ii)

Asset acquisition Names of the suppliers price quotation

Refurbishment of dining area Kitchen Equipment Australia $ 45,000

West Coast Office Equipment $ 42,000

Impinger Oven BTU $ 113,000

Sydney Fire Bricks $ 108,000

POS systems Retail Express $ 32,000

Maplewave $ 34,000

Part 6(c)(iii)

While selecting a particular supplier, Café B carried out sufficient research in the

market. On the basis of the market research particular supplier has been selected for all the

above mentioned 3 items on the below mentioned criteria –

Cost of the product

Reputation of the company

Delivery period

Past experience, if any

After sales services

Technical support provided by the company (Naude and Martin 2018).

Part 6(d)(i)

For purchasing the POS systems and Impinger oven Café B can raise the required

fund through borrowing as raising through equity is not available at this moment and if

compared, borrowing is cheaper against equity. Another advantage of raising through

borrowing is that it is deductible under tax whereas equity is not eligible for deduction

(Medina et al. 2017). On the other hand, for the purpose of refurbishment the company can

use its retained earnings available with it.

Part 7

Follow the appendix

Part 6(c)(ii)

Asset acquisition Names of the suppliers price quotation

Refurbishment of dining area Kitchen Equipment Australia $ 45,000

West Coast Office Equipment $ 42,000

Impinger Oven BTU $ 113,000

Sydney Fire Bricks $ 108,000

POS systems Retail Express $ 32,000

Maplewave $ 34,000

Part 6(c)(iii)

While selecting a particular supplier, Café B carried out sufficient research in the

market. On the basis of the market research particular supplier has been selected for all the

above mentioned 3 items on the below mentioned criteria –

Cost of the product

Reputation of the company

Delivery period

Past experience, if any

After sales services

Technical support provided by the company (Naude and Martin 2018).

Part 6(d)(i)

For purchasing the POS systems and Impinger oven Café B can raise the required

fund through borrowing as raising through equity is not available at this moment and if

compared, borrowing is cheaper against equity. Another advantage of raising through

borrowing is that it is deductible under tax whereas equity is not eligible for deduction

(Medina et al. 2017). On the other hand, for the purpose of refurbishment the company can

use its retained earnings available with it.

Part 7

Follow the appendix

11HOSPITALITY MANAGEMENT

Section 2 – Asset management system (BMC asset management)

It is recommended that Café B shall use BMC asset management system for

managing their asset. It will assist in gaining the visibility, control and compliance of the IT

assets for revealing true value they deliver. It is considered as the delightful solution based on

cloud for managing the asset. It can be used by small scale companies and it can work on

computer as well as mobile platforms. Payment for the software can be made yearly or

monthly basis and it supports various languages including English (Bmc.com 2018).

Part 2(a)

BMC asset management provides complete management for the lifecycle of the asset

from purchase to end of its life with details of deployment, depreciation, ownership, context,

state and operation (Council 2016). Further, it has space for general data collection that can

be used by Café B to generate all required data associated with the asset.

Part 2(b)

Financial data section under BMC asset management has space for complete

depreciation schedule linked with the asset. It has various depreciation options like written

down value method, straight line method, and useful life period, salvage value and amount of

depreciation. This space can be used by Café B for detail presentation of depreciation.

Section 2 – Asset management system (BMC asset management)

It is recommended that Café B shall use BMC asset management system for

managing their asset. It will assist in gaining the visibility, control and compliance of the IT

assets for revealing true value they deliver. It is considered as the delightful solution based on

cloud for managing the asset. It can be used by small scale companies and it can work on

computer as well as mobile platforms. Payment for the software can be made yearly or

monthly basis and it supports various languages including English (Bmc.com 2018).

Part 2(a)

BMC asset management provides complete management for the lifecycle of the asset

from purchase to end of its life with details of deployment, depreciation, ownership, context,

state and operation (Council 2016). Further, it has space for general data collection that can

be used by Café B to generate all required data associated with the asset.

Part 2(b)

Financial data section under BMC asset management has space for complete

depreciation schedule linked with the asset. It has various depreciation options like written

down value method, straight line method, and useful life period, salvage value and amount of

depreciation. This space can be used by Café B for detail presentation of depreciation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.