Finance in Hospitality Industry: Evaluating Funding and Profitability

VerifiedAdded on 2020/07/22

|14

|4434

|231

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins by exploring various sources of funding, both internal and external, relevant to a restaurant business, and then evaluates the impact of asset sales, subletting, and recipe sales on profitability and cash flow. The report delves into the elements of cost, profit margins, and pricing strategies, followed by an assessment of stock and cash control methods. Furthermore, it examines trial balance structures and the purpose of budgetary control, including variance analysis and recommendations for future management actions. The report underscores the importance of financial planning and control in maximizing business performance within the dynamic hospitality sector.

Finance in the

Hospitality Industry

Hospitality Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

PART A...........................................................................................................................................1

1.1 Review of source of funding:...........................................................................................1

1.2 Evaluate contribution of the sales of old oven and the sub-letting of unused spaces and

selling of recipes on business profitability and cash flow:.....................................................3

2.1 Elements of cost, profit percentages and selling prices for products and services offered by

a restaurant:............................................................................................................................3

2.2 Evaluation of methods of controlling stock and cash in the restaurant:...........................4

PART B............................................................................................................................................5

3.1: Assess the sources and structure of trail balance............................................................5

3.2 Evaluation of business account form................................................................................6

PART C............................................................................................................................................6

3.3 Process and purpose of budgetary control........................................................................6

3.4 Analysis of variance in budgeted and actual figures and suggestions for future

management action.................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

PART A...........................................................................................................................................1

1.1 Review of source of funding:...........................................................................................1

1.2 Evaluate contribution of the sales of old oven and the sub-letting of unused spaces and

selling of recipes on business profitability and cash flow:.....................................................3

2.1 Elements of cost, profit percentages and selling prices for products and services offered by

a restaurant:............................................................................................................................3

2.2 Evaluation of methods of controlling stock and cash in the restaurant:...........................4

PART B............................................................................................................................................5

3.1: Assess the sources and structure of trail balance............................................................5

3.2 Evaluation of business account form................................................................................6

PART C............................................................................................................................................6

3.3 Process and purpose of budgetary control........................................................................6

3.4 Analysis of variance in budgeted and actual figures and suggestions for future

management action.................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Nowadays, finance becomes the crucial parts for operating business in each sector

(Altinay, Paraskevas and Jang, 2015). Although, this can be said that each company needs to

know about the source of finance and pick the best among them. Under this report, various

financial raising tools are elaborated. There is huge importance of management of the finance in

organisations. It provides the opportunity regarding use best resources which helps in attaining

predetermined objectives. The hospitality sector is UK is on Boom right now. There are large

number of opportunities are available which to earn large number of profits. There are large

number of sources from which organisations raise their finance includes bank loan, hire

purchase, Factoring, venture capitalists etc.

In the present report explain about, different sources of funds, different factors which

helps in generation of income and major elements of cost, gross margin and selling prices. Also,

analysis of the methods which helps in controlling stock, sources of trial balance and purpose of

budgetary control.

TASK 1

PART A

1.1 Review of source of funding:

There is various source of finance which can be used by an enterprise while raising funds.

But mainly, internal and external sources are the most famous among all. These are required to

know about the various finance tools that may be used by the firm in internal and external

factors.

Internal sources of finance: This is the source which is related to the internal parts of

the organisation. In other words, these are the sources of finance for a business that are produced

by the business itself from its normal course of operations. The fund raised under this would take

from either owners capital, retained earnings or internal parts of the organisation. This is the

most usable form for raising capital by the finance manager in the firm. These internal sources

are defined in details:

Retained Earnings: This is the capital of the company which can be used by the firm for

meeting the financial needs of the company. Although, this can be said that the company

by using retained earnings accumulate various advantages such as, higher term finance,

1

Nowadays, finance becomes the crucial parts for operating business in each sector

(Altinay, Paraskevas and Jang, 2015). Although, this can be said that each company needs to

know about the source of finance and pick the best among them. Under this report, various

financial raising tools are elaborated. There is huge importance of management of the finance in

organisations. It provides the opportunity regarding use best resources which helps in attaining

predetermined objectives. The hospitality sector is UK is on Boom right now. There are large

number of opportunities are available which to earn large number of profits. There are large

number of sources from which organisations raise their finance includes bank loan, hire

purchase, Factoring, venture capitalists etc.

In the present report explain about, different sources of funds, different factors which

helps in generation of income and major elements of cost, gross margin and selling prices. Also,

analysis of the methods which helps in controlling stock, sources of trial balance and purpose of

budgetary control.

TASK 1

PART A

1.1 Review of source of funding:

There is various source of finance which can be used by an enterprise while raising funds.

But mainly, internal and external sources are the most famous among all. These are required to

know about the various finance tools that may be used by the firm in internal and external

factors.

Internal sources of finance: This is the source which is related to the internal parts of

the organisation. In other words, these are the sources of finance for a business that are produced

by the business itself from its normal course of operations. The fund raised under this would take

from either owners capital, retained earnings or internal parts of the organisation. This is the

most usable form for raising capital by the finance manager in the firm. These internal sources

are defined in details:

Retained Earnings: This is the capital of the company which can be used by the firm for

meeting the financial needs of the company. Although, this can be said that the company

by using retained earnings accumulate various advantages such as, higher term finance,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

no dilution of control and ownership, cost efficiency. But, there are drawback too, as this

does not consider cost of equity capital much effective.

Sale of assets: This is also the another tool for internal source of finance. During selling

the business assets and cash generated is implemented internally for financing of capital

needs.

Bank overdraft: This is the overdraft which is simple mode of short term financing.

Businesses are required to need money for their routine needs which emerge due to a

time gap between their accumulation and payments. To satiate these requirements, bank

overdraft is the most effective tool in the short term source of capital of finance.

Trade credits: Trade credit is rendered to an organisation by their creditors/suppliers.

This enables an organisation to delays its payments by some period. The period of credit

based on credit terms between business and suppliers.

Factoring of debt: This is an arrangement whereby organisation sell out its account

receivables/ debtors during discount, in this arrangement, buyer who is known due to

known as the factor, gather finance from the debtors on behalf of organisation and

charges a premium for this service. This is debtor does not pay for any reason, factor

could get back to the organisation for the payment.

Fund from operations: It is effective source which include about raise the funds by the

management of restaurant through their own personal operations. Such sources are

considered as their own profits which are earn by restaurant through their different

functions. These funds are used by the management of restaurant regarding effective

operation of their day to day operations.

External source of finance: There are so many external sources of finance which

emerges from outsiders. Capital raised from public by exercising IPOs and FPOs and debentures.

These are some of the external factors which are elaborated in details:

Equity shares: This is the common source of finance as this is only exercised for big

tech organisation. Not entire organisation could apply this source as this is controlled by

the various legislations. A crucial feature of equity shares is the sharing ownership rights

and henceforth, current shareholder’s rights are diluted to few extents.

2

does not consider cost of equity capital much effective.

Sale of assets: This is also the another tool for internal source of finance. During selling

the business assets and cash generated is implemented internally for financing of capital

needs.

Bank overdraft: This is the overdraft which is simple mode of short term financing.

Businesses are required to need money for their routine needs which emerge due to a

time gap between their accumulation and payments. To satiate these requirements, bank

overdraft is the most effective tool in the short term source of capital of finance.

Trade credits: Trade credit is rendered to an organisation by their creditors/suppliers.

This enables an organisation to delays its payments by some period. The period of credit

based on credit terms between business and suppliers.

Factoring of debt: This is an arrangement whereby organisation sell out its account

receivables/ debtors during discount, in this arrangement, buyer who is known due to

known as the factor, gather finance from the debtors on behalf of organisation and

charges a premium for this service. This is debtor does not pay for any reason, factor

could get back to the organisation for the payment.

Fund from operations: It is effective source which include about raise the funds by the

management of restaurant through their own personal operations. Such sources are

considered as their own profits which are earn by restaurant through their different

functions. These funds are used by the management of restaurant regarding effective

operation of their day to day operations.

External source of finance: There are so many external sources of finance which

emerges from outsiders. Capital raised from public by exercising IPOs and FPOs and debentures.

These are some of the external factors which are elaborated in details:

Equity shares: This is the common source of finance as this is only exercised for big

tech organisation. Not entire organisation could apply this source as this is controlled by

the various legislations. A crucial feature of equity shares is the sharing ownership rights

and henceforth, current shareholder’s rights are diluted to few extents.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debentures: This is the most common means of capital which is used by the cited

organisation over the other means. Debt is assumed to be the most reasonable mode of

finance (Cobanoglu and et. al., 2011).

Preferred stock: This is the stock shares characteristics of both common equity stocks

and debts. They are known as the preferred as they got attention over common equity

shares in terms of payment of dividend and capital likewise during liquidation.

Venture capital: This is just like equity shares excepts which investors are a diverse set

of people. Most commonly known as the venture capitalists, they are generally investing

in a new organisation which at a beginning stage and do a rigorous assessment of an

organisation before going to invest. Venture capitalists exist the organisation once it

begins getting a quite valuation.

Under this, this has been observed that Mr. Paul would exercise internal source of finance in

order to raise funding for sustainable development.

1.2 Evaluate contribution of the sales of old oven and the sub-letting of unused spaces and

selling of recipes on business profitability and cash flow:

In improvement of the performance of their small restaurant Paul is decided to upgrade

their equipment’s and explore other methods of income which helps in improvement of their

profitability.

The old oven which is used in the restaurant is sold at value of £ 3000. To improve their

productivity and profitability they purchase new oven which helps in consumption of 30%

energy. To improve their profitability also rent their unused space to Costa Coffee. Another

method which is used by the management of restaurant is to share their recipes with other for

charge. The contribution of all these factors of the functioning of restaurant is defined below:

Productivity: The purchase of new oven helps in preparation of 3 meals at one time

which is 3 time more than the performance of old oven. This will help in improvement of

the productivity of restaurant. It also helps in improvement of the efficiency of staff

members also (Jang and Park, 2011).

Profitability: Another three majors which are taken by management is selling of unused

space to Costa Coffee which helps in earning large number of income in form of rent.

Also saving of 30% energy by use of new oven helps in reduction of their electricity bills.

They also share their new recipes to the different restaurants which are operating in local

3

organisation over the other means. Debt is assumed to be the most reasonable mode of

finance (Cobanoglu and et. al., 2011).

Preferred stock: This is the stock shares characteristics of both common equity stocks

and debts. They are known as the preferred as they got attention over common equity

shares in terms of payment of dividend and capital likewise during liquidation.

Venture capital: This is just like equity shares excepts which investors are a diverse set

of people. Most commonly known as the venture capitalists, they are generally investing

in a new organisation which at a beginning stage and do a rigorous assessment of an

organisation before going to invest. Venture capitalists exist the organisation once it

begins getting a quite valuation.

Under this, this has been observed that Mr. Paul would exercise internal source of finance in

order to raise funding for sustainable development.

1.2 Evaluate contribution of the sales of old oven and the sub-letting of unused spaces and

selling of recipes on business profitability and cash flow:

In improvement of the performance of their small restaurant Paul is decided to upgrade

their equipment’s and explore other methods of income which helps in improvement of their

profitability.

The old oven which is used in the restaurant is sold at value of £ 3000. To improve their

productivity and profitability they purchase new oven which helps in consumption of 30%

energy. To improve their profitability also rent their unused space to Costa Coffee. Another

method which is used by the management of restaurant is to share their recipes with other for

charge. The contribution of all these factors of the functioning of restaurant is defined below:

Productivity: The purchase of new oven helps in preparation of 3 meals at one time

which is 3 time more than the performance of old oven. This will help in improvement of

the productivity of restaurant. It also helps in improvement of the efficiency of staff

members also (Jang and Park, 2011).

Profitability: Another three majors which are taken by management is selling of unused

space to Costa Coffee which helps in earning large number of income in form of rent.

Also saving of 30% energy by use of new oven helps in reduction of their electricity bills.

They also share their new recipes to the different restaurants which are operating in local

3

region. It helps in earning profits in form of commission from others. This will also

contribute in improvement of their brand image also.

Sales of old oven

In the present case study, observed that Paul doesn't need old oven to perform their

business activities. The residual value of such old oven is £3000. It is the duty of the

management is to sell at higher prices and earns profit. This will helps to improve their cash-

flows and performance of day to day functions.

Sub-letting of unused space

It is observed in case study 2 that Paul has free space in basement. Costa cafe approach

the management of Paul restaurant is to take their basement on rental basis to provide their

functions. It helps Paul to generate extra income in the form of rent.

Selling of recipes for commission

It is another source which helps to generate income through selling of their recipes. It is

observed that Paul has 20 years of experience in restaurant line which helps to provide new

dishes to their customers. In this regard, Paul introduce new book which has 20 recipes. This

recipe book is sold by Paul on commission basis which is used by the other restaurant owners to

provide such dishes to their customers. It helps the Paul to earn extra income in form of

commission and attracts large number of customers.

2.1 Elements of cost, profit percentages and selling prices for products and services offered by a

restaurant:

It is important for business to analyse the component of expenses which are incurred in

business activities. It indicates the monetary value which is required to be taken in the books of

company so that the manager can easily identify the exact cost incurred in the manufacturing

process. The cost incurred in producing quality goods are related with:

Material cost: It includes cost such as Raw material, finished goods which is used in

producing final products to the customers.

Labour cost: It includes the cost which is incurred in making payment to the staff

members and employees which are indulge in operating business operations.

Direct expenses: It includes the cost which are incurred in hiring or purchasing

equipment’s and technologies used in manufacturing food products

4

contribute in improvement of their brand image also.

Sales of old oven

In the present case study, observed that Paul doesn't need old oven to perform their

business activities. The residual value of such old oven is £3000. It is the duty of the

management is to sell at higher prices and earns profit. This will helps to improve their cash-

flows and performance of day to day functions.

Sub-letting of unused space

It is observed in case study 2 that Paul has free space in basement. Costa cafe approach

the management of Paul restaurant is to take their basement on rental basis to provide their

functions. It helps Paul to generate extra income in the form of rent.

Selling of recipes for commission

It is another source which helps to generate income through selling of their recipes. It is

observed that Paul has 20 years of experience in restaurant line which helps to provide new

dishes to their customers. In this regard, Paul introduce new book which has 20 recipes. This

recipe book is sold by Paul on commission basis which is used by the other restaurant owners to

provide such dishes to their customers. It helps the Paul to earn extra income in form of

commission and attracts large number of customers.

2.1 Elements of cost, profit percentages and selling prices for products and services offered by a

restaurant:

It is important for business to analyse the component of expenses which are incurred in

business activities. It indicates the monetary value which is required to be taken in the books of

company so that the manager can easily identify the exact cost incurred in the manufacturing

process. The cost incurred in producing quality goods are related with:

Material cost: It includes cost such as Raw material, finished goods which is used in

producing final products to the customers.

Labour cost: It includes the cost which is incurred in making payment to the staff

members and employees which are indulge in operating business operations.

Direct expenses: It includes the cost which are incurred in hiring or purchasing

equipment’s and technologies used in manufacturing food products

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consumables: These are the main cost component involved in the final products. This

involves process of delivering final product to the customers, For example Foods and Beverages

Overheads: Such cost are incurred for indirect materials, indirect labour and other

indirect cost. Generally, such cost is not identified specifically with the final product or service.

Example of such are electricity cost, stationary cost

Gross margin %: This will provides the information regarding the profit margin which

Paul wants to earn from their services of dinning in their restaurant. This identification of the

profit margin helps the management to determine their selling prices regarding their different

services.

Selling price: It is the amount which is decided by Paul to charge from their customers

on use of their different services. The formula which helps in determination of the selling price is

defined below:

Selling price (per unit): cost per unit + (Cost PU * gross margin %)

2.2 Evaluation of methods of controlling stock and cash in the restaurant:

There are various methods through which hotel can control stock and are able to designed

an effective system in order to decide what, when and how much to order. Such an effective

system of controlling stock are as follows:

Just in time (JIT): Through such methods the manager can bale reduce inventory cost by

ordering stock from suppliers whenever they required. It helps in saving cost of storing such

inventories which are not yet required in production process.

Computerised stock control system: Through such method, the manager can easily

monitor, trigger order when the re-order level is reached. It can help in getting a stock valuation

more quickly and are able to find out that how well a particular item of inventory is moving.

RFID inventory management: Through such system, the manager can prevent situation

of over-stocking or under-stocking of product used in production process. It can help stocks

which has limited shelf life to maintain their quality so that they can bring useful outcome to

them.

Inventory turnover Ratio: It is effective tool which helps in determination of the time

period about how quickly inventory is used by organisation. This ratio represents that higher the

5

involves process of delivering final product to the customers, For example Foods and Beverages

Overheads: Such cost are incurred for indirect materials, indirect labour and other

indirect cost. Generally, such cost is not identified specifically with the final product or service.

Example of such are electricity cost, stationary cost

Gross margin %: This will provides the information regarding the profit margin which

Paul wants to earn from their services of dinning in their restaurant. This identification of the

profit margin helps the management to determine their selling prices regarding their different

services.

Selling price: It is the amount which is decided by Paul to charge from their customers

on use of their different services. The formula which helps in determination of the selling price is

defined below:

Selling price (per unit): cost per unit + (Cost PU * gross margin %)

2.2 Evaluation of methods of controlling stock and cash in the restaurant:

There are various methods through which hotel can control stock and are able to designed

an effective system in order to decide what, when and how much to order. Such an effective

system of controlling stock are as follows:

Just in time (JIT): Through such methods the manager can bale reduce inventory cost by

ordering stock from suppliers whenever they required. It helps in saving cost of storing such

inventories which are not yet required in production process.

Computerised stock control system: Through such method, the manager can easily

monitor, trigger order when the re-order level is reached. It can help in getting a stock valuation

more quickly and are able to find out that how well a particular item of inventory is moving.

RFID inventory management: Through such system, the manager can prevent situation

of over-stocking or under-stocking of product used in production process. It can help stocks

which has limited shelf life to maintain their quality so that they can bring useful outcome to

them.

Inventory turnover Ratio: It is effective tool which helps in determination of the time

period about how quickly inventory is used by organisation. This ratio represents that higher the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ratio, shorter is the life of inventory. It shows that higher the sales volume with lower profit

margin.

Inventory control software: With the help of such system, the manager can easily

identify and tract the stock levels. It helps manager in getting knowledge about the level of stock

that the stock items are falling below mentioned points or not. so that they can place reorders

through economic order quantity (Rogerson, 2013).

Maintaining perpetual inventory system: It is effective method which is used by the

management of Paul's restaurant to keep effective track over the stocks and raw materials. This

system is also known as automatic inventory system. ERP and WMS are two effective

technologies which provides optimum solution regarding maintenance of level of inventories.

Preparation of inventory budgets: Regarding effective allocation of resources to the

different departments of Paul's restaurant need to prepare inventory budgets in advance. The

budgets should includes the information regarding total cost which is incurred by organisation in

keeping of the adequate amount of stock. This cost includes about material, fixed, carrying,

logistics, redistribution costs etc.

Establishment of Annual stock policies: It is the duty of the management of Paul's

restaurant is to implement the effective policies which provides direction to the manager is to

follow such guidelines regarding performance of their functions. This policy includes the

information regarding maximum and minimum level of stock which is need to maintain in

restaurant. The different benefits which are gathered by restaurant through application of such

policies are optimizing re-order levels, safety stock levels etc.

PART B

3.1: Assess the sources and structure of trail balance

In every financial statement the main factors are to record every information in their

respective format. For this purpose, they need to make use of data according to their time of

occurrence. In accounting terms, the main sources of trail balance are taken form journal leger

accounts. In their every transaction which is been first done by the company is recorded under

this statement. It consists of lists of accounts that are needed at the time of preparing trial balance

at a specific period of time. This has been seen that most of the accountant use to consider this

process as the initial step in financial statement for Olakunle. This must ensure that every

particular debit side balance must be equal to their credit total (Shaw, Bailey and Williams,

6

margin.

Inventory control software: With the help of such system, the manager can easily

identify and tract the stock levels. It helps manager in getting knowledge about the level of stock

that the stock items are falling below mentioned points or not. so that they can place reorders

through economic order quantity (Rogerson, 2013).

Maintaining perpetual inventory system: It is effective method which is used by the

management of Paul's restaurant to keep effective track over the stocks and raw materials. This

system is also known as automatic inventory system. ERP and WMS are two effective

technologies which provides optimum solution regarding maintenance of level of inventories.

Preparation of inventory budgets: Regarding effective allocation of resources to the

different departments of Paul's restaurant need to prepare inventory budgets in advance. The

budgets should includes the information regarding total cost which is incurred by organisation in

keeping of the adequate amount of stock. This cost includes about material, fixed, carrying,

logistics, redistribution costs etc.

Establishment of Annual stock policies: It is the duty of the management of Paul's

restaurant is to implement the effective policies which provides direction to the manager is to

follow such guidelines regarding performance of their functions. This policy includes the

information regarding maximum and minimum level of stock which is need to maintain in

restaurant. The different benefits which are gathered by restaurant through application of such

policies are optimizing re-order levels, safety stock levels etc.

PART B

3.1: Assess the sources and structure of trail balance

In every financial statement the main factors are to record every information in their

respective format. For this purpose, they need to make use of data according to their time of

occurrence. In accounting terms, the main sources of trail balance are taken form journal leger

accounts. In their every transaction which is been first done by the company is recorded under

this statement. It consists of lists of accounts that are needed at the time of preparing trial balance

at a specific period of time. This has been seen that most of the accountant use to consider this

process as the initial step in financial statement for Olakunle. This must ensure that every

particular debit side balance must be equal to their credit total (Shaw, Bailey and Williams,

6

2011). There are various financial operations those are primary base of financial decision. Every

adjustment is recorded into the trail balance because of they are said to be primary part of the

company. It would be guided as accountant to do proper rectification in order to analyse errors

that are arises in an activity.

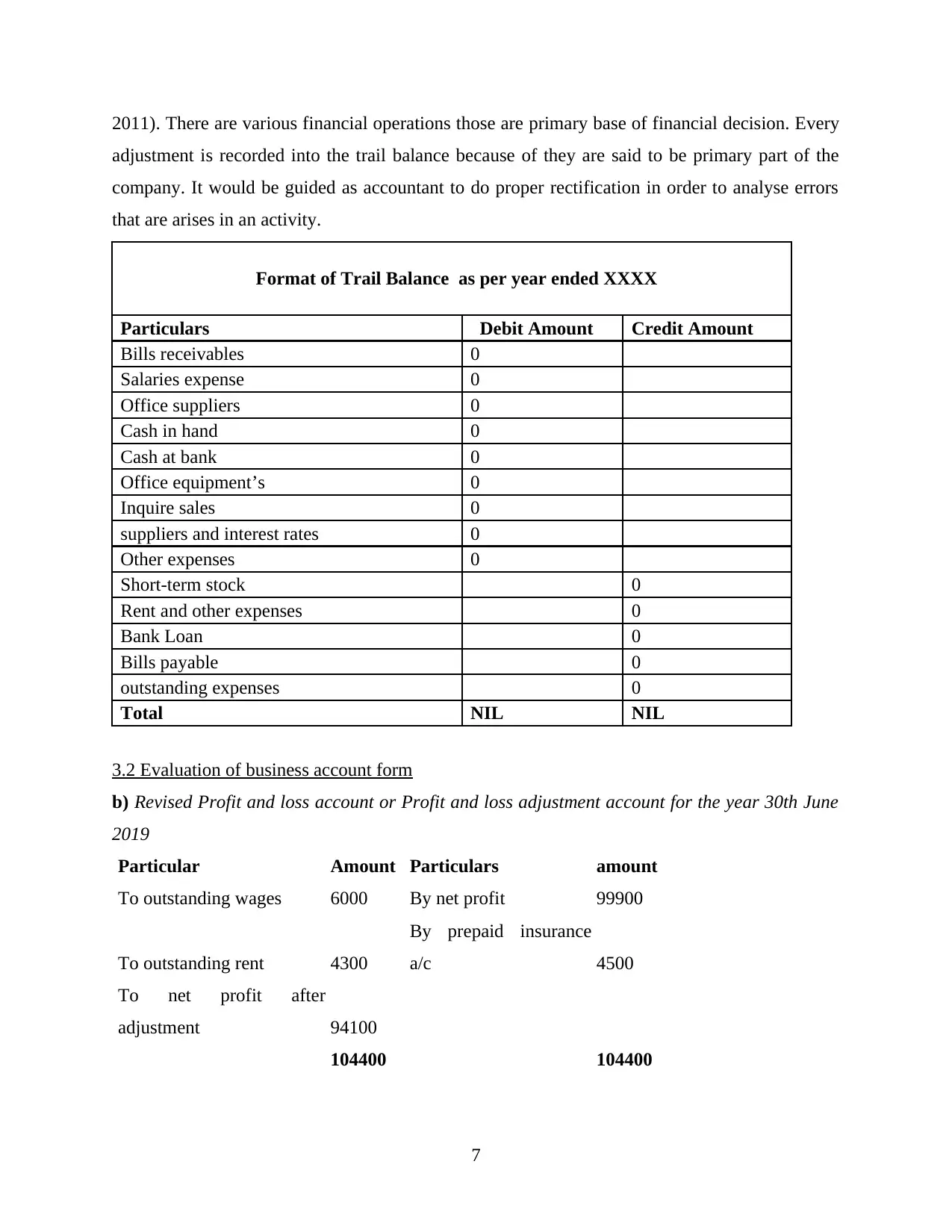

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Bills receivables 0

Salaries expense 0

Office suppliers 0

Cash in hand 0

Cash at bank 0

Office equipment’s 0

Inquire sales 0

suppliers and interest rates 0

Other expenses 0

Short-term stock 0

Rent and other expenses 0

Bank Loan 0

Bills payable 0

outstanding expenses 0

Total NIL NIL

3.2 Evaluation of business account form

b) Revised Profit and loss account or Profit and loss adjustment account for the year 30th June

2019

Particular Amount Particulars amount

To outstanding wages 6000 By net profit 99900

To outstanding rent 4300

By prepaid insurance

a/c 4500

To net profit after

adjustment 94100

104400 104400

7

adjustment is recorded into the trail balance because of they are said to be primary part of the

company. It would be guided as accountant to do proper rectification in order to analyse errors

that are arises in an activity.

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Bills receivables 0

Salaries expense 0

Office suppliers 0

Cash in hand 0

Cash at bank 0

Office equipment’s 0

Inquire sales 0

suppliers and interest rates 0

Other expenses 0

Short-term stock 0

Rent and other expenses 0

Bank Loan 0

Bills payable 0

outstanding expenses 0

Total NIL NIL

3.2 Evaluation of business account form

b) Revised Profit and loss account or Profit and loss adjustment account for the year 30th June

2019

Particular Amount Particulars amount

To outstanding wages 6000 By net profit 99900

To outstanding rent 4300

By prepaid insurance

a/c 4500

To net profit after

adjustment 94100

104400 104400

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

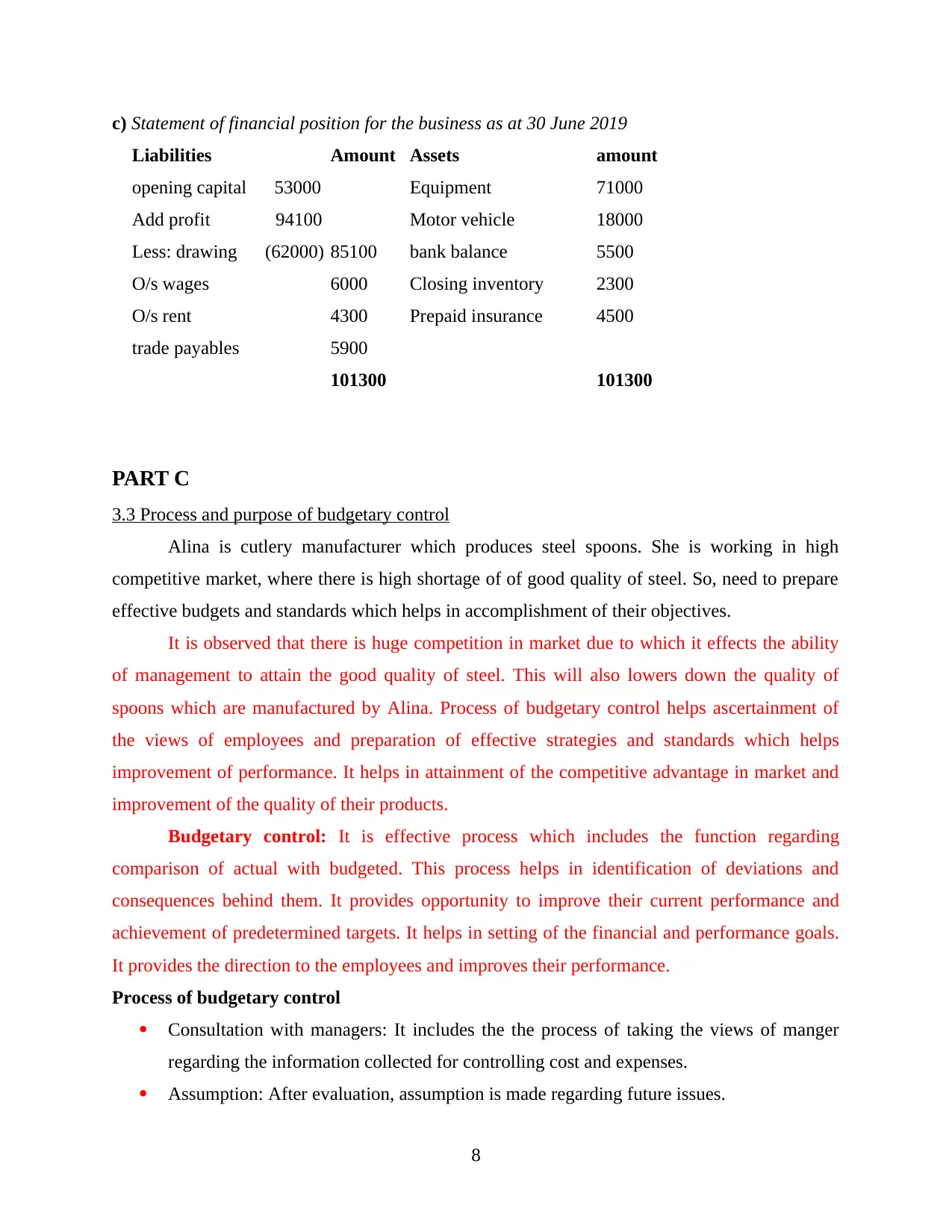

c) Statement of financial position for the business as at 30 June 2019

Liabilities Amount Assets amount

opening capital 53000 Equipment 71000

Add profit 94100 Motor vehicle 18000

Less: drawing (62000) 85100 bank balance 5500

O/s wages 6000 Closing inventory 2300

O/s rent 4300 Prepaid insurance 4500

trade payables 5900

101300 101300

PART C

3.3 Process and purpose of budgetary control

Alina is cutlery manufacturer which produces steel spoons. She is working in high

competitive market, where there is high shortage of of good quality of steel. So, need to prepare

effective budgets and standards which helps in accomplishment of their objectives.

It is observed that there is huge competition in market due to which it effects the ability

of management to attain the good quality of steel. This will also lowers down the quality of

spoons which are manufactured by Alina. Process of budgetary control helps ascertainment of

the views of employees and preparation of effective strategies and standards which helps

improvement of performance. It helps in attainment of the competitive advantage in market and

improvement of the quality of their products.

Budgetary control: It is effective process which includes the function regarding

comparison of actual with budgeted. This process helps in identification of deviations and

consequences behind them. It provides opportunity to improve their current performance and

achievement of predetermined targets. It helps in setting of the financial and performance goals.

It provides the direction to the employees and improves their performance.

Process of budgetary control

Consultation with managers: It includes the the process of taking the views of manger

regarding the information collected for controlling cost and expenses.

Assumption: After evaluation, assumption is made regarding future issues.

8

Liabilities Amount Assets amount

opening capital 53000 Equipment 71000

Add profit 94100 Motor vehicle 18000

Less: drawing (62000) 85100 bank balance 5500

O/s wages 6000 Closing inventory 2300

O/s rent 4300 Prepaid insurance 4500

trade payables 5900

101300 101300

PART C

3.3 Process and purpose of budgetary control

Alina is cutlery manufacturer which produces steel spoons. She is working in high

competitive market, where there is high shortage of of good quality of steel. So, need to prepare

effective budgets and standards which helps in accomplishment of their objectives.

It is observed that there is huge competition in market due to which it effects the ability

of management to attain the good quality of steel. This will also lowers down the quality of

spoons which are manufactured by Alina. Process of budgetary control helps ascertainment of

the views of employees and preparation of effective strategies and standards which helps

improvement of performance. It helps in attainment of the competitive advantage in market and

improvement of the quality of their products.

Budgetary control: It is effective process which includes the function regarding

comparison of actual with budgeted. This process helps in identification of deviations and

consequences behind them. It provides opportunity to improve their current performance and

achievement of predetermined targets. It helps in setting of the financial and performance goals.

It provides the direction to the employees and improves their performance.

Process of budgetary control

Consultation with managers: It includes the the process of taking the views of manger

regarding the information collected for controlling cost and expenses.

Assumption: After evaluation, assumption is made regarding future issues.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preparation of budgets: Preparation of budgets for each and every department. It helps in

defining their goals and objectives. It is the duty of all the employees is to adhere such

standards and improve their performances.

Measurement: Process of measuring actual information with budgeted. It helps in

ascertaining deviations in performance. Through ascertainment of the deviations and their

consequences different strategies and policies are prepared which helps in

accomplishment of goals. (O’Neill and Carlbäck, 2011).

Review analysis: Function of reviewing all the activities which are performed earlier. It

helps in attaining right direction. The process of review helps in effective monitoring

upon overall functions. It helps in attainment of the sustainability in their operations and

accomplishment of their goals.

Purpose of budgetary control

It helps in communication of ideas and plans to every employee. It brings awareness

regarding functions which they have to perform.

Budgetary control contributes in maintenance of coordination among the different

activities of the employees.

Another purpose of budgetary control is to establishment of effective systems of control.

It also helps in motivating of the employees to perform better and optimum utilisation of

resources.

Coordination: Through implementation of master budget in budgetary control process

helps in achievement of effective coordination among the functions which are provided

by departments. It helps the management to make the plans by thinking of organisation as

a whole group.

Increase in efficiency: Alina is faced the issues regarding the quality of their products and

high competitiveness in market. Determination of the standards regarding different

activities like production, sales, costs and overheads after consideration of the internal

and external factors helps in improvement of the efficiency. It brings an obligation upon

the departments is to follow such standards to attain efficiency over the use of men,

material, method and money.

Financial planning: The budgets which are prepared by Alina is expressed in financial

terms. Such budgets provides the information regarding estimated expenditures and

9

defining their goals and objectives. It is the duty of all the employees is to adhere such

standards and improve their performances.

Measurement: Process of measuring actual information with budgeted. It helps in

ascertaining deviations in performance. Through ascertainment of the deviations and their

consequences different strategies and policies are prepared which helps in

accomplishment of goals. (O’Neill and Carlbäck, 2011).

Review analysis: Function of reviewing all the activities which are performed earlier. It

helps in attaining right direction. The process of review helps in effective monitoring

upon overall functions. It helps in attainment of the sustainability in their operations and

accomplishment of their goals.

Purpose of budgetary control

It helps in communication of ideas and plans to every employee. It brings awareness

regarding functions which they have to perform.

Budgetary control contributes in maintenance of coordination among the different

activities of the employees.

Another purpose of budgetary control is to establishment of effective systems of control.

It also helps in motivating of the employees to perform better and optimum utilisation of

resources.

Coordination: Through implementation of master budget in budgetary control process

helps in achievement of effective coordination among the functions which are provided

by departments. It helps the management to make the plans by thinking of organisation as

a whole group.

Increase in efficiency: Alina is faced the issues regarding the quality of their products and

high competitiveness in market. Determination of the standards regarding different

activities like production, sales, costs and overheads after consideration of the internal

and external factors helps in improvement of the efficiency. It brings an obligation upon

the departments is to follow such standards to attain efficiency over the use of men,

material, method and money.

Financial planning: The budgets which are prepared by Alina is expressed in financial

terms. Such budgets provides the information regarding estimated expenditures and

9

revenues. It helps in effective management of cash flow. Through this process working

capital requirements are fulfilled and helps in effective performance of day to day

functions.

Motivating employees: Budgetary control process helps in appraisal of the actual

performance of employees. On the basis of this information incentives are paid by the

management to employees. There is hue importance of this system regarding motivation

of employees and improves their passion.

3.4 Analysis of variance in budgeted and actual figures and suggestions for future management

action

Alina observed that to improve their performance need to prepare budgets which helps in

establishment of targets which are achieved by employees through their performances in future.

The table which shows the budgeted and actual figures is presented below:

Particulars Budget Actual Variance

units sold 100000 70000 30000

Materials 15000 22500 7500

Direct

Labour 22500 24375 1875

As per above table, the budgeted figures which are given by the manager regarding units

sold is 100000 but in actual the employees of company not able to meet the standards and only

70000 units are sold in market. The variance is of 30000 units from budgeted. It means less sales

and profitability.

Similarly, there is also difference shown in between the budgeted and actual of material

and labour. The variance which is analysed between both are 7500 and 1875. This shows the

higher amount of expenses are incurred (Phelan, Mejia and Hertzman, 2013).

Suggestions

Use of appropriate communication channels which helps in effective disbursement of

roles and responsibilities to achieve lasting improvements.

10

capital requirements are fulfilled and helps in effective performance of day to day

functions.

Motivating employees: Budgetary control process helps in appraisal of the actual

performance of employees. On the basis of this information incentives are paid by the

management to employees. There is hue importance of this system regarding motivation

of employees and improves their passion.

3.4 Analysis of variance in budgeted and actual figures and suggestions for future management

action

Alina observed that to improve their performance need to prepare budgets which helps in

establishment of targets which are achieved by employees through their performances in future.

The table which shows the budgeted and actual figures is presented below:

Particulars Budget Actual Variance

units sold 100000 70000 30000

Materials 15000 22500 7500

Direct

Labour 22500 24375 1875

As per above table, the budgeted figures which are given by the manager regarding units

sold is 100000 but in actual the employees of company not able to meet the standards and only

70000 units are sold in market. The variance is of 30000 units from budgeted. It means less sales

and profitability.

Similarly, there is also difference shown in between the budgeted and actual of material

and labour. The variance which is analysed between both are 7500 and 1875. This shows the

higher amount of expenses are incurred (Phelan, Mejia and Hertzman, 2013).

Suggestions

Use of appropriate communication channels which helps in effective disbursement of

roles and responsibilities to achieve lasting improvements.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.