Financial Management, Budgeting and Costing in Hospitality Report

VerifiedAdded on 2019/12/28

|14

|4158

|159

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins with an introduction to financial management and accounting, explaining the purposes of business accounting and the users of accounting reports. The report defines budgeting and its purpose, categorizes different types of costs, and explains the trial balance. It evaluates various sources of finance and delves into calculations, including room occupancy rates, depreciation, revenue percentages, break-even points, and profit analysis. The report then moves on to costing, with a detailed costing sheet for a recipe, and discusses the best ways for a restaurant to control its stock. Furthermore, it includes calculations for package deals, selling prices, and profit variance, concluding with recommendations and references. The report utilizes tables to present data such as depreciation calculations, revenue percentages, and break-even points to support the analysis. The report is a valuable resource for students studying finance and hospitality management.

Finance in Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................5

PART 1 ...........................................................................................................................................5

TASK A...........................................................................................................................................5

1. Purposes of business keeping accounts and users of accounting reports.................................5

2. Define budgeting and its purpose............................................................................................6

3. Categorization of fixed, variable and semi variable cost ........................................................6

4. Define trial balance and its purpose .......................................................................................7

5. (a & b) Evaluation of different sources of finance..................................................................7

TASK B CALCULATION AND DISCUSSION ...........................................................................8

1 . Evaluation of room occupancy rate .......................................................................................8

2. Calculating of Depreciation.....................................................................................................9

3. Calculating percentage of revenue ..........................................................................................9

4. Identification of breakeven point and profit..........................................................................10

5. Recommendation...................................................................................................................10

PART B..........................................................................................................................................11

TASK A. PREPARING A COSTING SHEET FOR THE RECIPE FOR FOUR PORTIONS OF

FLAMBÉED CHICKEN WITH ASPARAGUS IN A RESTAURANT......................................11

1. Calculate the recipe cost .......................................................................................................11

2. Calculating the cost per portion ............................................................................................11

3. Calculating and discus the selling price per portion to produce a 85% gross profit .............11

4. Calculating the quantity (all ingredient) required for 70 portions.........................................12

5. Discussing the best ways for a restaurant to control its stock................................................12

TASK B.........................................................................................................................................12

1. Calculating the total cost of package deal and cost per customer..........................................12

2. Calculating the selling price per seat if the mark up is to be 35%.........................................13

3. Identification of cost per customer if the break event sales point is set at 36 customers......13

4. Calculating profit for this package for 48 customers with given the break-even point is set at

36 customers and the profit mark-up is set at 35% ...................................................................13

5. Calculating profit variance ....................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................5

PART 1 ...........................................................................................................................................5

TASK A...........................................................................................................................................5

1. Purposes of business keeping accounts and users of accounting reports.................................5

2. Define budgeting and its purpose............................................................................................6

3. Categorization of fixed, variable and semi variable cost ........................................................6

4. Define trial balance and its purpose .......................................................................................7

5. (a & b) Evaluation of different sources of finance..................................................................7

TASK B CALCULATION AND DISCUSSION ...........................................................................8

1 . Evaluation of room occupancy rate .......................................................................................8

2. Calculating of Depreciation.....................................................................................................9

3. Calculating percentage of revenue ..........................................................................................9

4. Identification of breakeven point and profit..........................................................................10

5. Recommendation...................................................................................................................10

PART B..........................................................................................................................................11

TASK A. PREPARING A COSTING SHEET FOR THE RECIPE FOR FOUR PORTIONS OF

FLAMBÉED CHICKEN WITH ASPARAGUS IN A RESTAURANT......................................11

1. Calculate the recipe cost .......................................................................................................11

2. Calculating the cost per portion ............................................................................................11

3. Calculating and discus the selling price per portion to produce a 85% gross profit .............11

4. Calculating the quantity (all ingredient) required for 70 portions.........................................12

5. Discussing the best ways for a restaurant to control its stock................................................12

TASK B.........................................................................................................................................12

1. Calculating the total cost of package deal and cost per customer..........................................12

2. Calculating the selling price per seat if the mark up is to be 35%.........................................13

3. Identification of cost per customer if the break event sales point is set at 36 customers......13

4. Calculating profit for this package for 48 customers with given the break-even point is set at

36 customers and the profit mark-up is set at 35% ...................................................................13

5. Calculating profit variance ....................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INDEX OF TABLES

Table 1: Calculation of Depreciation...............................................................................................9

Table 2: Calculating percentage of revenue ....................................................................................9

Table 3: Computation of breakeven point ....................................................................................10

Table 4: Profit on sell of 290 hotdogs............................................................................................10

Table 5: Cost sheet ........................................................................................................................11

Table 6: Calculating the cost per portion.......................................................................................11

Table 7: Calculation of selling price to generate gross profit of 85%...........................................11

Table 8: Calculation of quantity of ingredients for 70 portion......................................................12

Table 9: Calculating the total cost of package deal.......................................................................12

Table 10: Cost per seat...................................................................................................................13

Table 11: Calculating the selling price per seat.............................................................................13

Table 12: Profit on the tour package of 48 people.........................................................................13

Table 13: Calculation of variance profit .....................................................................................14

Table 1: Calculation of Depreciation...............................................................................................9

Table 2: Calculating percentage of revenue ....................................................................................9

Table 3: Computation of breakeven point ....................................................................................10

Table 4: Profit on sell of 290 hotdogs............................................................................................10

Table 5: Cost sheet ........................................................................................................................11

Table 6: Calculating the cost per portion.......................................................................................11

Table 7: Calculation of selling price to generate gross profit of 85%...........................................11

Table 8: Calculation of quantity of ingredients for 70 portion......................................................12

Table 9: Calculating the total cost of package deal.......................................................................12

Table 10: Cost per seat...................................................................................................................13

Table 11: Calculating the selling price per seat.............................................................................13

Table 12: Profit on the tour package of 48 people.........................................................................13

Table 13: Calculation of variance profit .....................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the modern business era, financial management is termed as most crucial aspect of

business management that assists managers for carrying an appropriate financial planning.

Therefore, every organization develops various strategies for implementing an efficient plan to

manage wide range of monetary and non-monetary resources as per the requirement of various

strategic decisions (Bebbington, Unerman and O'Dwyer, 2014). But, the management of

financial resources assists managers in identifying requirement of sources of funds along with

their application in business management. In this process, the management of an organization

has to consider various other factors such as budget management, costing and selection of

appropriate sources of finance etc.

This report is going to analyze various elements of financial management with reference

to different operations of business associated with the hospitality industry. This investigation

also evaluates different tools of financial-management such as costing, budgetary control, ratio

analysis etc. These are playing important role in the decision making process.

PART 1

TASK A

1. Purposes of business keeping accounts and users of accounting reports

For keeping systematic record of wide range of financial transaction and business

operations, management of every organization formulates wide range of accounting statement.

Purpose of business keeping accounts

Different financial statements assist the managers for keeping wide range of financial

data with an appropriate manner (Oakshott, 2012). Therefore, management of hospitality

firm formulates income statements, balance sheet, cash flow statements.

These statements provide information about income and profitability of the business.

It also determines wide range of data about source of income along with activities that

influence expenditure of company through which management can address net profit of

the company. These statements assist in evaluation of financial position of company in the form of

debt-equity value, value of total assets along with current liquidity position of business

(Kim, Ham and Moon, 2012).

User of accounting reports

4

In the modern business era, financial management is termed as most crucial aspect of

business management that assists managers for carrying an appropriate financial planning.

Therefore, every organization develops various strategies for implementing an efficient plan to

manage wide range of monetary and non-monetary resources as per the requirement of various

strategic decisions (Bebbington, Unerman and O'Dwyer, 2014). But, the management of

financial resources assists managers in identifying requirement of sources of funds along with

their application in business management. In this process, the management of an organization

has to consider various other factors such as budget management, costing and selection of

appropriate sources of finance etc.

This report is going to analyze various elements of financial management with reference

to different operations of business associated with the hospitality industry. This investigation

also evaluates different tools of financial-management such as costing, budgetary control, ratio

analysis etc. These are playing important role in the decision making process.

PART 1

TASK A

1. Purposes of business keeping accounts and users of accounting reports

For keeping systematic record of wide range of financial transaction and business

operations, management of every organization formulates wide range of accounting statement.

Purpose of business keeping accounts

Different financial statements assist the managers for keeping wide range of financial

data with an appropriate manner (Oakshott, 2012). Therefore, management of hospitality

firm formulates income statements, balance sheet, cash flow statements.

These statements provide information about income and profitability of the business.

It also determines wide range of data about source of income along with activities that

influence expenditure of company through which management can address net profit of

the company. These statements assist in evaluation of financial position of company in the form of

debt-equity value, value of total assets along with current liquidity position of business

(Kim, Ham and Moon, 2012).

User of accounting reports

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

An organization operates business operations by assessing support to different individuals

or stakeholders. Therefore, different stakeholders such as management, employees, shareholder's,

suppliers, creditors, lenders like bank etc. examine wide range of financial data that have been

presented by different accounting statements (Ross, Westerfield and Jordan, 2008). On the basis

of financial information, different stakeholders are able to make appropriate decisions.

2. Define budgeting and its purpose

Budgetary control provides significant assistance in scheduling duties and strategies as

per the different business objectives. Budgeting is defined as the most important element of

financial management in which management develops activities and allocates appropriate funds

as per the last year performance. It plays important role for ensuring financial success of the

company (Lashley, 2007). By developing appropriate budgets related income and expenditures

of company, the management is able to take appropriate decision.

Purpose of Budgeting

This approach is very effective for forecasting future income and expenditure of the

company. On the basis of this information, managers are able to take appropriate

decisions as per the current business requirement.

This system provides significant support in order to monitor performance of business by

identifying deviations between budgeted figures and actual results (Voss, Johnston and

Armistead, 2006).

It also supports the management for taking appropriate business decision as per the

distinct requirement of business.

By considering data associated with the budget management of the company are able to

consider appropriate source of funds as per the distinct needs of business.

3. Categorization of fixed, variable and semi variable cost Fixed cost. It includes all expenditures that are not altered as a result of change in number

service user and production quantity. In the context of hospitality business, fixed cost is

related torent, salary of staff, cost of equipment such cleaning machines etc. Variable cost: Variable cost is directly correlated with the number of units produced by

the business (Elements of Cost, 2010). In the context of hospitality business, variable cost

is identified as catering cost which is taken by the restaurant on per customer. It also

includes cost of food material.

5

or stakeholders. Therefore, different stakeholders such as management, employees, shareholder's,

suppliers, creditors, lenders like bank etc. examine wide range of financial data that have been

presented by different accounting statements (Ross, Westerfield and Jordan, 2008). On the basis

of financial information, different stakeholders are able to make appropriate decisions.

2. Define budgeting and its purpose

Budgetary control provides significant assistance in scheduling duties and strategies as

per the different business objectives. Budgeting is defined as the most important element of

financial management in which management develops activities and allocates appropriate funds

as per the last year performance. It plays important role for ensuring financial success of the

company (Lashley, 2007). By developing appropriate budgets related income and expenditures

of company, the management is able to take appropriate decision.

Purpose of Budgeting

This approach is very effective for forecasting future income and expenditure of the

company. On the basis of this information, managers are able to take appropriate

decisions as per the current business requirement.

This system provides significant support in order to monitor performance of business by

identifying deviations between budgeted figures and actual results (Voss, Johnston and

Armistead, 2006).

It also supports the management for taking appropriate business decision as per the

distinct requirement of business.

By considering data associated with the budget management of the company are able to

consider appropriate source of funds as per the distinct needs of business.

3. Categorization of fixed, variable and semi variable cost Fixed cost. It includes all expenditures that are not altered as a result of change in number

service user and production quantity. In the context of hospitality business, fixed cost is

related torent, salary of staff, cost of equipment such cleaning machines etc. Variable cost: Variable cost is directly correlated with the number of units produced by

the business (Elements of Cost, 2010). In the context of hospitality business, variable cost

is identified as catering cost which is taken by the restaurant on per customer. It also

includes cost of food material.

5

Semi variable cost: These expenses are both variable and fixed cost. In this hospitality

business, electricity bill is considered as semi-variable cost. This is because some portion

electricity consumption remains fixed and some portion of electricity consumption

changes according to the number of users (Jerenz, 2008). Sometime salaries of employees

are also considered as semi-variable cost. This is because company makes extra payment

for overtime working during the peak season.

4. Define trial balance and its purpose

Trial balance is playing a significant role in business accounting process. It is developed

as per the results of ledger account. It provides significant assistance to accounting department

trial balance for checking accuracy level and issues among wide range of business transactions

(Bennouna and et.al, 2010). The format of the trial balance consists of two-column in which

debit balances are recorded in one column and all the credit balances are recorded in another.

Purpose of trial balance

It is considered as a working paper that accountants use as a basis in formulating other

financial statements.

Trial balance gives assurance about every debit entry recorded as per the corresponding

credit entry with reference to double entry concept of accounting.

Trial balance helps the manager by ensuring them that the account balances are accurately

extracted from different accounting ledgers associated with different financial transactions

of hospitality business (O'Fallon and Rutherford, 2010).

It enhances accuracy of other financial statements.

5. (a & b) Evaluation of different sources of finance

Peter is planning to open a small fast food shop with a business partner that requires

capital of £ 9,000 Peter and his business partner have £6,500 for business. Therefore, Peter

should consider the below mentioned resources for funds:

Source of finance Advantages Disadvantages

Private lenders:

It includes individual finance,

finance companies, private

lenders etc.

In this, risk on

investment is mainly

taken by lenders.

Mr. Peter is not

High rate of interest increases

the cost of finance.

6

business, electricity bill is considered as semi-variable cost. This is because some portion

electricity consumption remains fixed and some portion of electricity consumption

changes according to the number of users (Jerenz, 2008). Sometime salaries of employees

are also considered as semi-variable cost. This is because company makes extra payment

for overtime working during the peak season.

4. Define trial balance and its purpose

Trial balance is playing a significant role in business accounting process. It is developed

as per the results of ledger account. It provides significant assistance to accounting department

trial balance for checking accuracy level and issues among wide range of business transactions

(Bennouna and et.al, 2010). The format of the trial balance consists of two-column in which

debit balances are recorded in one column and all the credit balances are recorded in another.

Purpose of trial balance

It is considered as a working paper that accountants use as a basis in formulating other

financial statements.

Trial balance gives assurance about every debit entry recorded as per the corresponding

credit entry with reference to double entry concept of accounting.

Trial balance helps the manager by ensuring them that the account balances are accurately

extracted from different accounting ledgers associated with different financial transactions

of hospitality business (O'Fallon and Rutherford, 2010).

It enhances accuracy of other financial statements.

5. (a & b) Evaluation of different sources of finance

Peter is planning to open a small fast food shop with a business partner that requires

capital of £ 9,000 Peter and his business partner have £6,500 for business. Therefore, Peter

should consider the below mentioned resources for funds:

Source of finance Advantages Disadvantages

Private lenders:

It includes individual finance,

finance companies, private

lenders etc.

In this, risk on

investment is mainly

taken by lenders.

Mr. Peter is not

High rate of interest increases

the cost of finance.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

required to mortgage

any property.

Bank Loans:

It is one of the most common

and quick way through which

management can assess funds

in the form of tools long term

loan, working capital,

overdraft etc (Financial

Management, 2015). As per

the requirement of business.

Quick method

Relationship with

banking organization

provides significant

assistance in the

funding decisions.

Bank loans are backed

by the property of

business entity

(Menifield, 2013).

Increase the chances of

bankruptcy.

TASK B CALCULATION AND DISCUSSION

1. Evaluation of room occupancy rate

a) The occupancy percentage in a five star hotel in London on 25th July 2013

Room occupancy percentage

Number of total rooms 368

Number of Rooms occupied 236

Room occupancy percentage

(Number of occupied room*100/ number

of total room) 64.13%

b) Discussing the performance of the hotel on 25th July 2013.

As per the case, it has been evaluated that hotel has normally kept 80% occupancy rate in

the summer. But, five star hotels have identified 64.13% occupancy percentage on 25th July 2013

which is very less as compared to normal 80%. Therefore, it can be stated that the performance

of hospitality firm is not good on particular date.

c) Suggestion for their performance improvement.

For improving performance of hotel, the management of hospitality firm should apply

some unique and aggressive marketing strategies through which company is able to attract

consumers towards different products and services of hotel organization. In addition to that

management needs to provide wide range of discount offers and services to attract new along

with existing consumers of company (Bennouna and et.al, 2010).

7

any property.

Bank Loans:

It is one of the most common

and quick way through which

management can assess funds

in the form of tools long term

loan, working capital,

overdraft etc (Financial

Management, 2015). As per

the requirement of business.

Quick method

Relationship with

banking organization

provides significant

assistance in the

funding decisions.

Bank loans are backed

by the property of

business entity

(Menifield, 2013).

Increase the chances of

bankruptcy.

TASK B CALCULATION AND DISCUSSION

1. Evaluation of room occupancy rate

a) The occupancy percentage in a five star hotel in London on 25th July 2013

Room occupancy percentage

Number of total rooms 368

Number of Rooms occupied 236

Room occupancy percentage

(Number of occupied room*100/ number

of total room) 64.13%

b) Discussing the performance of the hotel on 25th July 2013.

As per the case, it has been evaluated that hotel has normally kept 80% occupancy rate in

the summer. But, five star hotels have identified 64.13% occupancy percentage on 25th July 2013

which is very less as compared to normal 80%. Therefore, it can be stated that the performance

of hospitality firm is not good on particular date.

c) Suggestion for their performance improvement.

For improving performance of hotel, the management of hospitality firm should apply

some unique and aggressive marketing strategies through which company is able to attract

consumers towards different products and services of hotel organization. In addition to that

management needs to provide wide range of discount offers and services to attract new along

with existing consumers of company (Bennouna and et.al, 2010).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

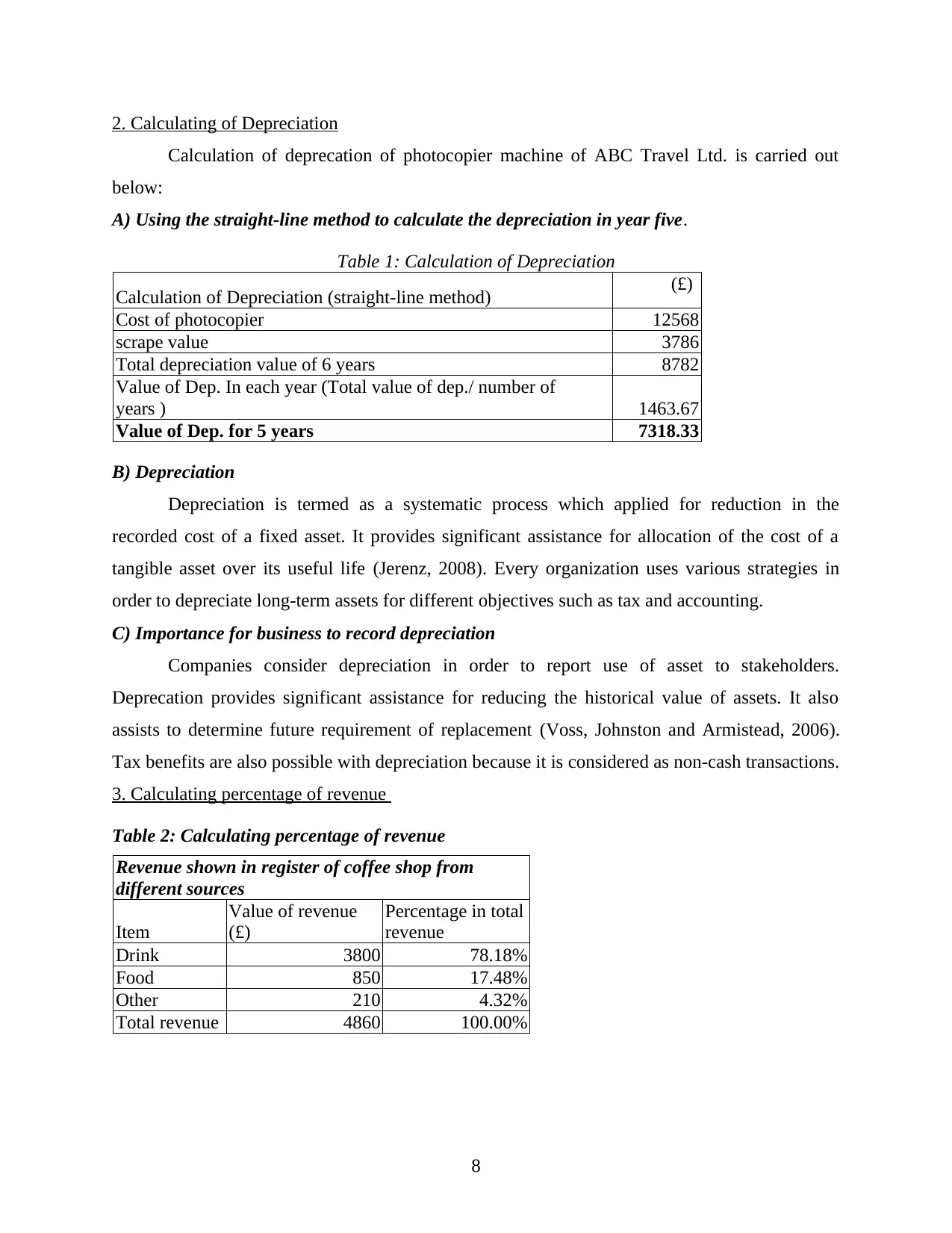

2. Calculating of Depreciation

Calculation of deprecation of photocopier machine of ABC Travel Ltd. is carried out

below:

A) Using the straight-line method to calculate the depreciation in year five.

Table 1: Calculation of Depreciation

Calculation of Depreciation (straight-line method) (£)

Cost of photocopier 12568

scrape value 3786

Total depreciation value of 6 years 8782

Value of Dep. In each year (Total value of dep./ number of

years ) 1463.67

Value of Dep. for 5 years 7318.33

B) Depreciation

Depreciation is termed as a systematic process which applied for reduction in the

recorded cost of a fixed asset. It provides significant assistance for allocation of the cost of a

tangible asset over its useful life (Jerenz, 2008). Every organization uses various strategies in

order to depreciate long-term assets for different objectives such as tax and accounting.

C) Importance for business to record depreciation

Companies consider depreciation in order to report use of asset to stakeholders.

Deprecation provides significant assistance for reducing the historical value of assets. It also

assists to determine future requirement of replacement (Voss, Johnston and Armistead, 2006).

Tax benefits are also possible with depreciation because it is considered as non-cash transactions.

3. Calculating percentage of revenue

Table 2: Calculating percentage of revenue

Revenue shown in register of coffee shop from

different sources

Item

Value of revenue

(£)

Percentage in total

revenue

Drink 3800 78.18%

Food 850 17.48%

Other 210 4.32%

Total revenue 4860 100.00%

8

Calculation of deprecation of photocopier machine of ABC Travel Ltd. is carried out

below:

A) Using the straight-line method to calculate the depreciation in year five.

Table 1: Calculation of Depreciation

Calculation of Depreciation (straight-line method) (£)

Cost of photocopier 12568

scrape value 3786

Total depreciation value of 6 years 8782

Value of Dep. In each year (Total value of dep./ number of

years ) 1463.67

Value of Dep. for 5 years 7318.33

B) Depreciation

Depreciation is termed as a systematic process which applied for reduction in the

recorded cost of a fixed asset. It provides significant assistance for allocation of the cost of a

tangible asset over its useful life (Jerenz, 2008). Every organization uses various strategies in

order to depreciate long-term assets for different objectives such as tax and accounting.

C) Importance for business to record depreciation

Companies consider depreciation in order to report use of asset to stakeholders.

Deprecation provides significant assistance for reducing the historical value of assets. It also

assists to determine future requirement of replacement (Voss, Johnston and Armistead, 2006).

Tax benefits are also possible with depreciation because it is considered as non-cash transactions.

3. Calculating percentage of revenue

Table 2: Calculating percentage of revenue

Revenue shown in register of coffee shop from

different sources

Item

Value of revenue

(£)

Percentage in total

revenue

Drink 3800 78.18%

Food 850 17.48%

Other 210 4.32%

Total revenue 4860 100.00%

8

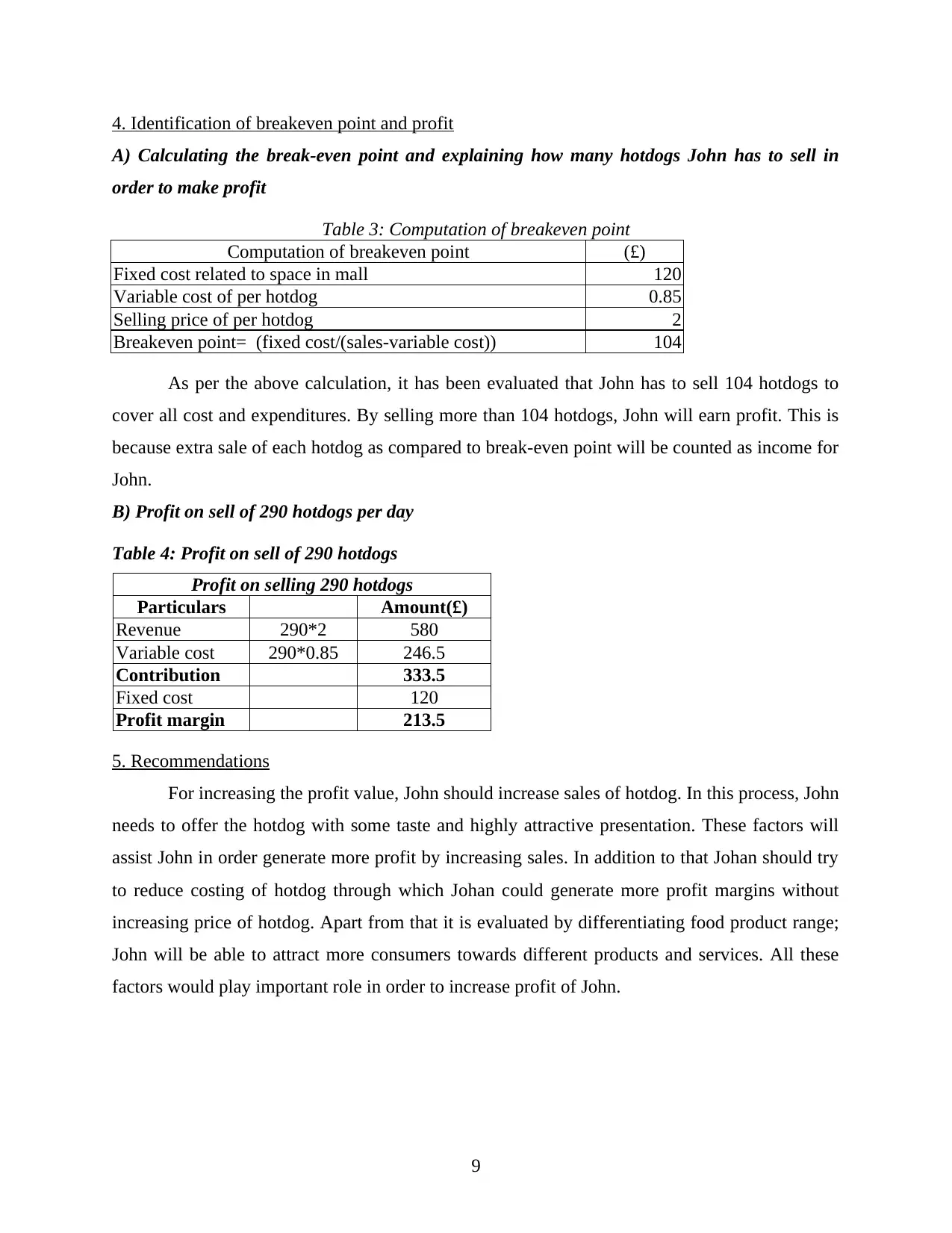

4. Identification of breakeven point and profit

A) Calculating the break-even point and explaining how many hotdogs John has to sell in

order to make profit

Table 3: Computation of breakeven point

Computation of breakeven point (£)

Fixed cost related to space in mall 120

Variable cost of per hotdog 0.85

Selling price of per hotdog 2

Breakeven point= (fixed cost/(sales-variable cost)) 104

As per the above calculation, it has been evaluated that John has to sell 104 hotdogs to

cover all cost and expenditures. By selling more than 104 hotdogs, John will earn profit. This is

because extra sale of each hotdog as compared to break-even point will be counted as income for

John.

B) Profit on sell of 290 hotdogs per day

Table 4: Profit on sell of 290 hotdogs

Profit on selling 290 hotdogs

Particulars Amount(£)

Revenue 290*2 580

Variable cost 290*0.85 246.5

Contribution 333.5

Fixed cost 120

Profit margin 213.5

5. Recommendations

For increasing the profit value, John should increase sales of hotdog. In this process, John

needs to offer the hotdog with some taste and highly attractive presentation. These factors will

assist John in order generate more profit by increasing sales. In addition to that Johan should try

to reduce costing of hotdog through which Johan could generate more profit margins without

increasing price of hotdog. Apart from that it is evaluated by differentiating food product range;

John will be able to attract more consumers towards different products and services. All these

factors would play important role in order to increase profit of John.

9

A) Calculating the break-even point and explaining how many hotdogs John has to sell in

order to make profit

Table 3: Computation of breakeven point

Computation of breakeven point (£)

Fixed cost related to space in mall 120

Variable cost of per hotdog 0.85

Selling price of per hotdog 2

Breakeven point= (fixed cost/(sales-variable cost)) 104

As per the above calculation, it has been evaluated that John has to sell 104 hotdogs to

cover all cost and expenditures. By selling more than 104 hotdogs, John will earn profit. This is

because extra sale of each hotdog as compared to break-even point will be counted as income for

John.

B) Profit on sell of 290 hotdogs per day

Table 4: Profit on sell of 290 hotdogs

Profit on selling 290 hotdogs

Particulars Amount(£)

Revenue 290*2 580

Variable cost 290*0.85 246.5

Contribution 333.5

Fixed cost 120

Profit margin 213.5

5. Recommendations

For increasing the profit value, John should increase sales of hotdog. In this process, John

needs to offer the hotdog with some taste and highly attractive presentation. These factors will

assist John in order generate more profit by increasing sales. In addition to that Johan should try

to reduce costing of hotdog through which Johan could generate more profit margins without

increasing price of hotdog. Apart from that it is evaluated by differentiating food product range;

John will be able to attract more consumers towards different products and services. All these

factors would play important role in order to increase profit of John.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

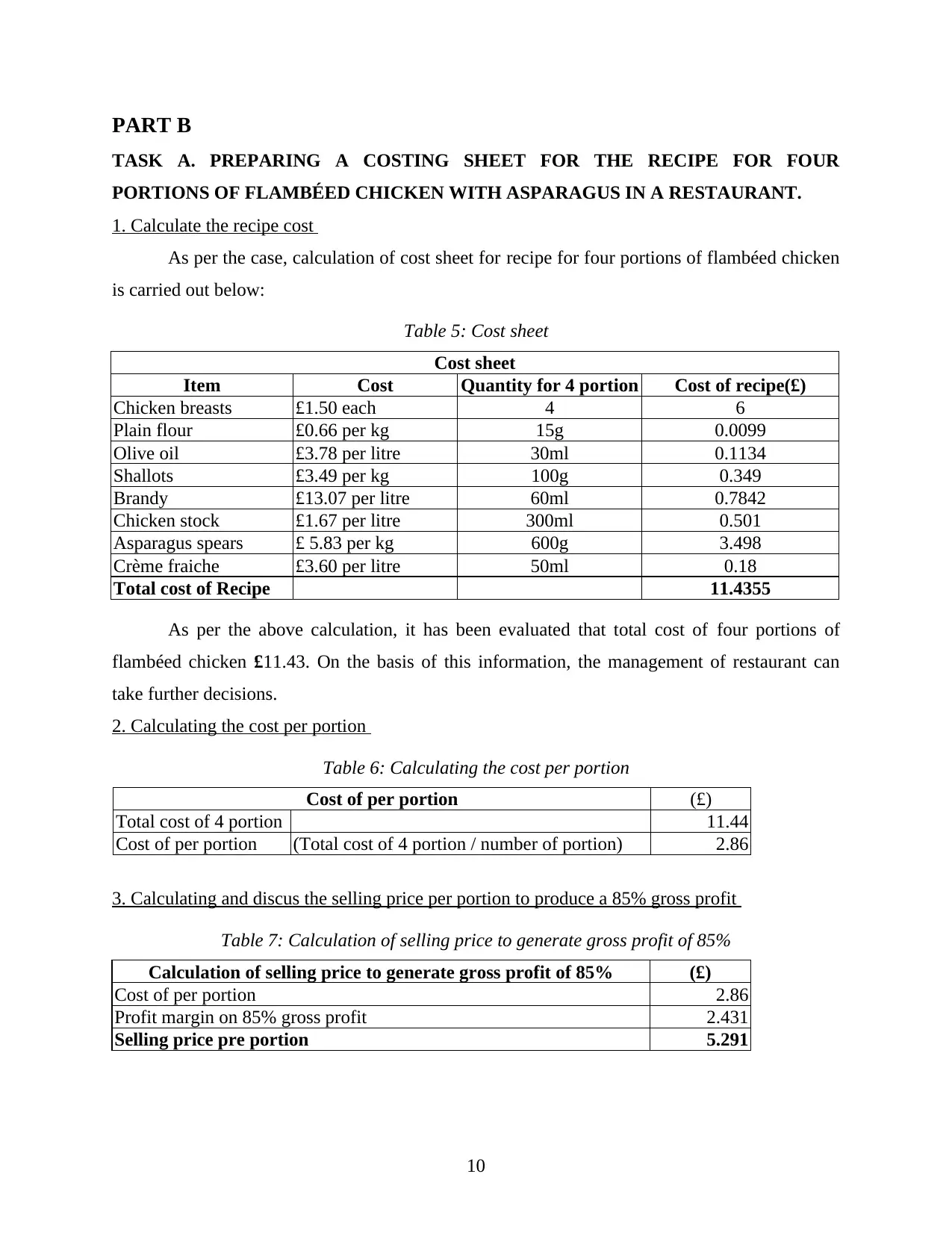

PART B

TASK A. PREPARING A COSTING SHEET FOR THE RECIPE FOR FOUR

PORTIONS OF FLAMBÉED CHICKEN WITH ASPARAGUS IN A RESTAURANT.

1. Calculate the recipe cost

As per the case, calculation of cost sheet for recipe for four portions of flambéed chicken

is carried out below:

Table 5: Cost sheet

Cost sheet

Item Cost Quantity for 4 portion Cost of recipe(£)

Chicken breasts £1.50 each 4 6

Plain flour £0.66 per kg 15g 0.0099

Olive oil £3.78 per litre 30ml 0.1134

Shallots £3.49 per kg 100g 0.349

Brandy £13.07 per litre 60ml 0.7842

Chicken stock £1.67 per litre 300ml 0.501

Asparagus spears £ 5.83 per kg 600g 3.498

Crème fraiche £3.60 per litre 50ml 0.18

Total cost of Recipe 11.4355

As per the above calculation, it has been evaluated that total cost of four portions of

flambéed chicken £11.43. On the basis of this information, the management of restaurant can

take further decisions.

2. Calculating the cost per portion

Table 6: Calculating the cost per portion

Cost of per portion (£)

Total cost of 4 portion 11.44

Cost of per portion (Total cost of 4 portion / number of portion) 2.86

3. Calculating and discus the selling price per portion to produce a 85% gross profit

Table 7: Calculation of selling price to generate gross profit of 85%

Calculation of selling price to generate gross profit of 85% (£)

Cost of per portion 2.86

Profit margin on 85% gross profit 2.431

Selling price pre portion 5.291

10

TASK A. PREPARING A COSTING SHEET FOR THE RECIPE FOR FOUR

PORTIONS OF FLAMBÉED CHICKEN WITH ASPARAGUS IN A RESTAURANT.

1. Calculate the recipe cost

As per the case, calculation of cost sheet for recipe for four portions of flambéed chicken

is carried out below:

Table 5: Cost sheet

Cost sheet

Item Cost Quantity for 4 portion Cost of recipe(£)

Chicken breasts £1.50 each 4 6

Plain flour £0.66 per kg 15g 0.0099

Olive oil £3.78 per litre 30ml 0.1134

Shallots £3.49 per kg 100g 0.349

Brandy £13.07 per litre 60ml 0.7842

Chicken stock £1.67 per litre 300ml 0.501

Asparagus spears £ 5.83 per kg 600g 3.498

Crème fraiche £3.60 per litre 50ml 0.18

Total cost of Recipe 11.4355

As per the above calculation, it has been evaluated that total cost of four portions of

flambéed chicken £11.43. On the basis of this information, the management of restaurant can

take further decisions.

2. Calculating the cost per portion

Table 6: Calculating the cost per portion

Cost of per portion (£)

Total cost of 4 portion 11.44

Cost of per portion (Total cost of 4 portion / number of portion) 2.86

3. Calculating and discus the selling price per portion to produce a 85% gross profit

Table 7: Calculation of selling price to generate gross profit of 85%

Calculation of selling price to generate gross profit of 85% (£)

Cost of per portion 2.86

Profit margin on 85% gross profit 2.431

Selling price pre portion 5.291

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

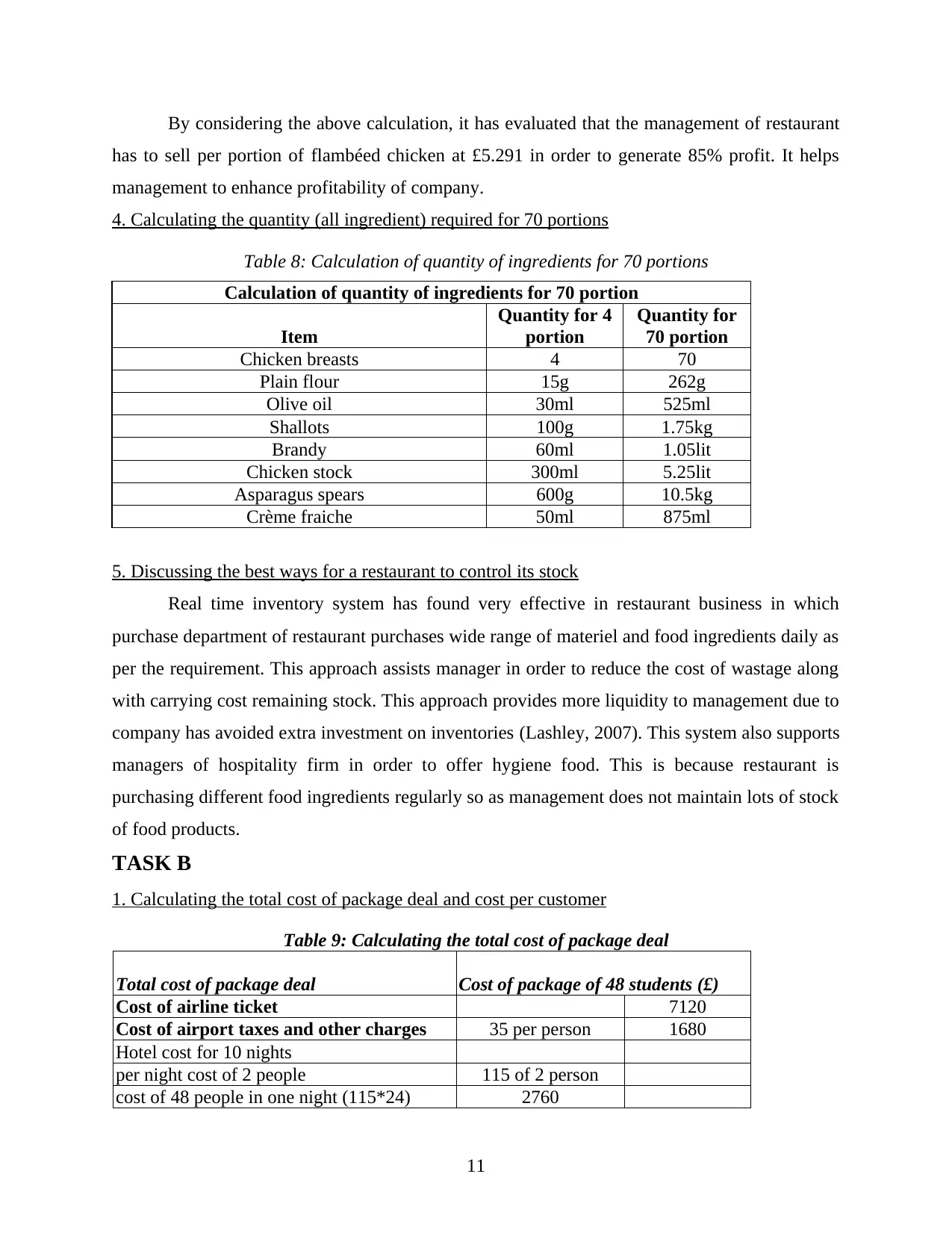

By considering the above calculation, it has evaluated that the management of restaurant

has to sell per portion of flambéed chicken at £5.291 in order to generate 85% profit. It helps

management to enhance profitability of company.

4. Calculating the quantity (all ingredient) required for 70 portions

Table 8: Calculation of quantity of ingredients for 70 portions

Calculation of quantity of ingredients for 70 portion

Item

Quantity for 4

portion

Quantity for

70 portion

Chicken breasts 4 70

Plain flour 15g 262g

Olive oil 30ml 525ml

Shallots 100g 1.75kg

Brandy 60ml 1.05lit

Chicken stock 300ml 5.25lit

Asparagus spears 600g 10.5kg

Crème fraiche 50ml 875ml

5. Discussing the best ways for a restaurant to control its stock

Real time inventory system has found very effective in restaurant business in which

purchase department of restaurant purchases wide range of materiel and food ingredients daily as

per the requirement. This approach assists manager in order to reduce the cost of wastage along

with carrying cost remaining stock. This approach provides more liquidity to management due to

company has avoided extra investment on inventories (Lashley, 2007). This system also supports

managers of hospitality firm in order to offer hygiene food. This is because restaurant is

purchasing different food ingredients regularly so as management does not maintain lots of stock

of food products.

TASK B

1. Calculating the total cost of package deal and cost per customer

Table 9: Calculating the total cost of package deal

Total cost of package deal Cost of package of 48 students (£)

Cost of airline ticket 7120

Cost of airport taxes and other charges 35 per person 1680

Hotel cost for 10 nights

per night cost of 2 people 115 of 2 person

cost of 48 people in one night (115*24) 2760

11

has to sell per portion of flambéed chicken at £5.291 in order to generate 85% profit. It helps

management to enhance profitability of company.

4. Calculating the quantity (all ingredient) required for 70 portions

Table 8: Calculation of quantity of ingredients for 70 portions

Calculation of quantity of ingredients for 70 portion

Item

Quantity for 4

portion

Quantity for

70 portion

Chicken breasts 4 70

Plain flour 15g 262g

Olive oil 30ml 525ml

Shallots 100g 1.75kg

Brandy 60ml 1.05lit

Chicken stock 300ml 5.25lit

Asparagus spears 600g 10.5kg

Crème fraiche 50ml 875ml

5. Discussing the best ways for a restaurant to control its stock

Real time inventory system has found very effective in restaurant business in which

purchase department of restaurant purchases wide range of materiel and food ingredients daily as

per the requirement. This approach assists manager in order to reduce the cost of wastage along

with carrying cost remaining stock. This approach provides more liquidity to management due to

company has avoided extra investment on inventories (Lashley, 2007). This system also supports

managers of hospitality firm in order to offer hygiene food. This is because restaurant is

purchasing different food ingredients regularly so as management does not maintain lots of stock

of food products.

TASK B

1. Calculating the total cost of package deal and cost per customer

Table 9: Calculating the total cost of package deal

Total cost of package deal Cost of package of 48 students (£)

Cost of airline ticket 7120

Cost of airport taxes and other charges 35 per person 1680

Hotel cost for 10 nights

per night cost of 2 people 115 of 2 person

cost of 48 people in one night (115*24) 2760

11

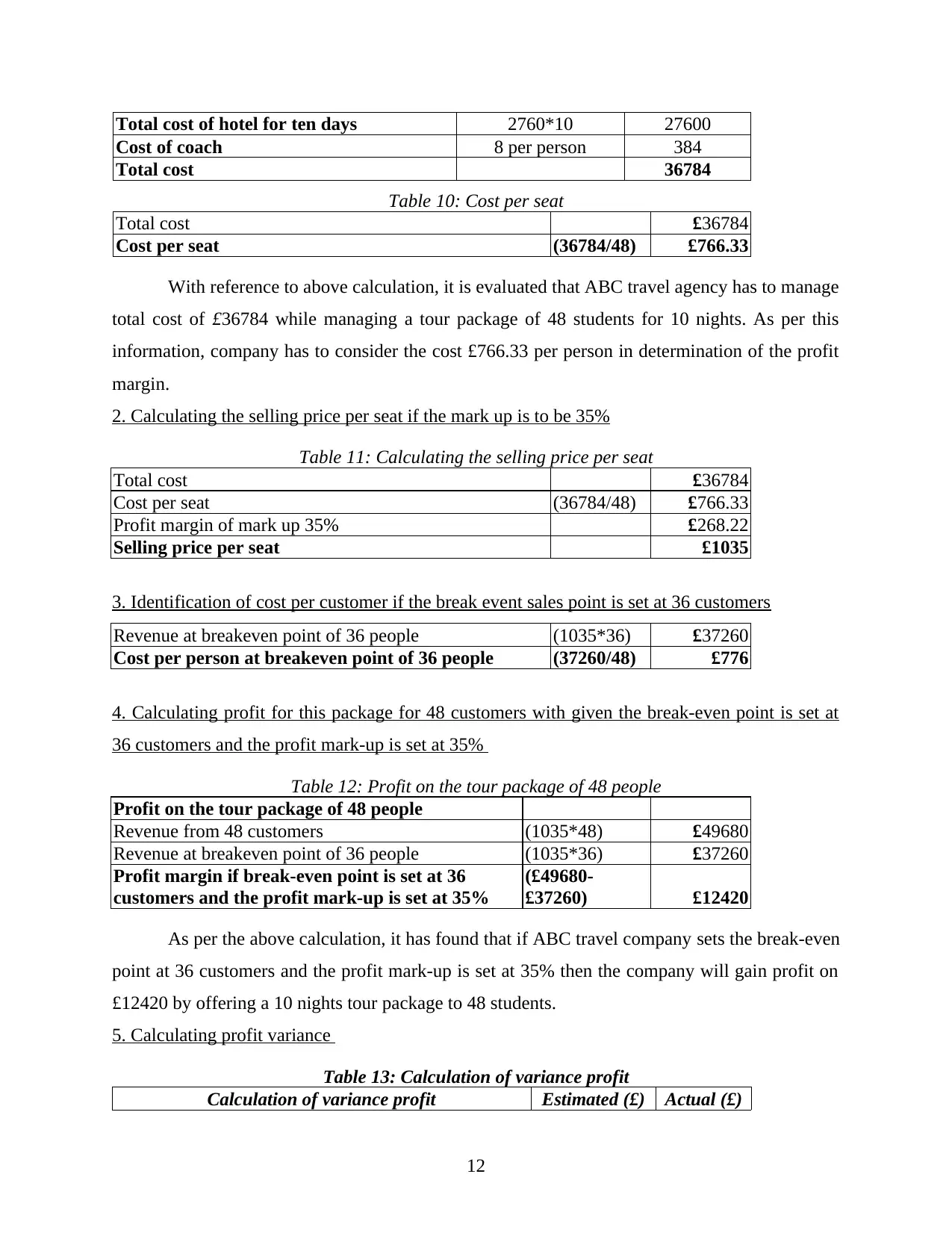

Total cost of hotel for ten days 2760*10 27600

Cost of coach 8 per person 384

Total cost 36784

Table 10: Cost per seat

Total cost £36784

Cost per seat (36784/48) £766.33

With reference to above calculation, it is evaluated that ABC travel agency has to manage

total cost of £36784 while managing a tour package of 48 students for 10 nights. As per this

information, company has to consider the cost £766.33 per person in determination of the profit

margin.

2. Calculating the selling price per seat if the mark up is to be 35%

Table 11: Calculating the selling price per seat

Total cost £36784

Cost per seat (36784/48) £766.33

Profit margin of mark up 35% £268.22

Selling price per seat £1035

3. Identification of cost per customer if the break event sales point is set at 36 customers

Revenue at breakeven point of 36 people (1035*36) £37260

Cost per person at breakeven point of 36 people (37260/48) £776

4. Calculating profit for this package for 48 customers with given the break-even point is set at

36 customers and the profit mark-up is set at 35%

Table 12: Profit on the tour package of 48 people

Profit on the tour package of 48 people

Revenue from 48 customers (1035*48) £49680

Revenue at breakeven point of 36 people (1035*36) £37260

Profit margin if break-even point is set at 36

customers and the profit mark-up is set at 35%

(£49680-

£37260) £12420

As per the above calculation, it has found that if ABC travel company sets the break-even

point at 36 customers and the profit mark-up is set at 35% then the company will gain profit on

£12420 by offering a 10 nights tour package to 48 students.

5. Calculating profit variance

Table 13: Calculation of variance profit

Calculation of variance profit Estimated (£) Actual (£)

12

Cost of coach 8 per person 384

Total cost 36784

Table 10: Cost per seat

Total cost £36784

Cost per seat (36784/48) £766.33

With reference to above calculation, it is evaluated that ABC travel agency has to manage

total cost of £36784 while managing a tour package of 48 students for 10 nights. As per this

information, company has to consider the cost £766.33 per person in determination of the profit

margin.

2. Calculating the selling price per seat if the mark up is to be 35%

Table 11: Calculating the selling price per seat

Total cost £36784

Cost per seat (36784/48) £766.33

Profit margin of mark up 35% £268.22

Selling price per seat £1035

3. Identification of cost per customer if the break event sales point is set at 36 customers

Revenue at breakeven point of 36 people (1035*36) £37260

Cost per person at breakeven point of 36 people (37260/48) £776

4. Calculating profit for this package for 48 customers with given the break-even point is set at

36 customers and the profit mark-up is set at 35%

Table 12: Profit on the tour package of 48 people

Profit on the tour package of 48 people

Revenue from 48 customers (1035*48) £49680

Revenue at breakeven point of 36 people (1035*36) £37260

Profit margin if break-even point is set at 36

customers and the profit mark-up is set at 35%

(£49680-

£37260) £12420

As per the above calculation, it has found that if ABC travel company sets the break-even

point at 36 customers and the profit mark-up is set at 35% then the company will gain profit on

£12420 by offering a 10 nights tour package to 48 students.

5. Calculating profit variance

Table 13: Calculation of variance profit

Calculation of variance profit Estimated (£) Actual (£)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.