Finance in Hospitality: Funding, Profitability, Stock & Cash Control

VerifiedAdded on 2024/05/29

|11

|3393

|384

Report

AI Summary

This report provides a comprehensive analysis of finance in the hospitality sector, focusing on various aspects critical for effective financial management. It begins by reviewing eight potential funding sources for a hospitality business, such as factoring, retained profits, sale of unused assets, owner financing, bank overdrafts, trade credit, business angels, and crowdfunding, evaluating their contributions to profitability and cash flow. The report then discusses the elements of cost, gross profit percentages, and selling prices for restaurant products and services, including direct and indirect materials, labor, and overhead expenses. Finally, it evaluates different methods for controlling stock and cash within a restaurant, emphasizing the importance of inventory management systems for effective stock control. This analysis offers valuable insights for hospitality businesses seeking to optimize their financial performance and ensure sustainable growth, with similar solved assignments available on Desklib.

Finance in Hospitality

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

1.1 Review of the sources of funding (8 sources) available to Paul................................................3

1.2 Evaluate the contribution that the sale of the old oven, the sub-letting of the unused space and

the selling of recipes for commission can make on the business’s profitability and cash flow......5

2.1 Discuss elements of cost, gross profit percentages and selling prices for products and services

offered by a restaurant.....................................................................................................................6

2.2 Evaluate methods of controlling stock and cash in the restaurant.............................................7

Reference list.................................................................................................................................10

2

Introduction......................................................................................................................................3

1.1 Review of the sources of funding (8 sources) available to Paul................................................3

1.2 Evaluate the contribution that the sale of the old oven, the sub-letting of the unused space and

the selling of recipes for commission can make on the business’s profitability and cash flow......5

2.1 Discuss elements of cost, gross profit percentages and selling prices for products and services

offered by a restaurant.....................................................................................................................6

2.2 Evaluate methods of controlling stock and cash in the restaurant.............................................7

Reference list.................................................................................................................................10

2

Introduction

Finance is a significant part of every business. It is important even for non-profit seeking

companies to manage its finances. Finance plays an important role in the field of hospitality as

well. Since there is a rapid growth in the sector of hospitality, the need of managing finances in

the sector is also increasing. This report contains the discussion of the various aspects of finance

within the sector of hospitality. The report comprises of different discussions on the eight

sources of finance that can be used in a hospitality organization and the contribution of different

sources of finance for measuring the cash flows and profitability of a hospitality organization. It

also contains evaluation of various elements of costs, gross profit and selling prices along with

evaluating different methods that can be used for controlling the cash and stock in hospitality

organizations.

1.1 Review of the sources of funding (8 sources) available to Paul

In order to fund the different activities and investments in a business, the business requires

seeking out for a wide range of sources from which it will be able to generate funds (Peirson

et

al., 2014). However, the sources are not always internally available in a company. Sources of

funding can be external as well. The internal sources from which Paul can be generating funds

for his restaurant business are the following -

Factoring - As stated by Tanrisever

et al. (2015), factoring can be referred to as the type

of debt financing used in a business in which funds are raised through selling of the

accounts receivables or the invoices of a company to factors, who are usually a third

party, at a certain rate of discount. In simple words, factoring is selling of debts to

agencies in exchange of money. The different invoices or the accounts receivables of

Paul’s restaurant can be sold off to third parties or agencies for generating funds for the

restaurant’s new energy efficient oven that is intended to be bought. Retained profit - According to Elsas

et al. (2014), retained profits refer to the amount of

money retained in a business after dividends have been paid off to the shareholders of the

company. This amount retained in the company can be used further as a fund for its

different operations. For example, the retained profit in the small restaurant in Redbridge

3

Finance is a significant part of every business. It is important even for non-profit seeking

companies to manage its finances. Finance plays an important role in the field of hospitality as

well. Since there is a rapid growth in the sector of hospitality, the need of managing finances in

the sector is also increasing. This report contains the discussion of the various aspects of finance

within the sector of hospitality. The report comprises of different discussions on the eight

sources of finance that can be used in a hospitality organization and the contribution of different

sources of finance for measuring the cash flows and profitability of a hospitality organization. It

also contains evaluation of various elements of costs, gross profit and selling prices along with

evaluating different methods that can be used for controlling the cash and stock in hospitality

organizations.

1.1 Review of the sources of funding (8 sources) available to Paul

In order to fund the different activities and investments in a business, the business requires

seeking out for a wide range of sources from which it will be able to generate funds (Peirson

et

al., 2014). However, the sources are not always internally available in a company. Sources of

funding can be external as well. The internal sources from which Paul can be generating funds

for his restaurant business are the following -

Factoring - As stated by Tanrisever

et al. (2015), factoring can be referred to as the type

of debt financing used in a business in which funds are raised through selling of the

accounts receivables or the invoices of a company to factors, who are usually a third

party, at a certain rate of discount. In simple words, factoring is selling of debts to

agencies in exchange of money. The different invoices or the accounts receivables of

Paul’s restaurant can be sold off to third parties or agencies for generating funds for the

restaurant’s new energy efficient oven that is intended to be bought. Retained profit - According to Elsas

et al. (2014), retained profits refer to the amount of

money retained in a business after dividends have been paid off to the shareholders of the

company. This amount retained in the company can be used further as a fund for its

different operations. For example, the retained profit in the small restaurant in Redbridge

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

owned by Paul can be used for funding its different types of operations such as the

purchase of the new energy efficient intergrated oven needed in the machine. Sale of unused assets - The unused assets of a business can also be utilized for generating

funds for a business. The sale of such assets helps in raising good amount of funds. Paul

can also be seeking for unused assets in his restaurant such as the old oven that is not

used anymore, which can act as a good source of fund for Paul for his restaurant business.

Owner financing - The funds invested or capital introduced by the owner of a business

himself or herself is also a good source of funding (Chen and Elston, 2013). The biggest

advantage of this investment is that the burden of repayment is absent in this source. Paul

can be investing additional capital into his restaurant business in order to generate funds

for the purchase of the new oven he intends to be purchasing for his restaurant.

On the other hand, the following are external sources from which Paul can be generating funds

for his restaurant business is the following -

Bank overdraft - According to Cowling

et al. (2016), bank overdrafts are the short-term

external source of funding in which bank allows a certain sum of money to its customers

and allows them to draw money in spite of having no funds in the account. It is an

agreement of loan in which banks extend credit to customers to certain maximum amount

called the overdraft limit. Paul can also be relying on bank overdraft over funding its new

oven. Trade credit - Purchasing goods and services from suppliers on credit is known as trade

credit (Carbo‐Valverde

et al., 2016). The credit agreement between a business and its

suppliers also acts as a source of funds for a business. Paul can also be negotiating with

its suppliers and agree to purchase inputs at trade credit. Business angels - Another external source of funding are the business angels. Business

angels are the wealthy entrepreneurial individuals or people who provide good amount of

funds and invest capital into businesses in exchange of the return of a proportion of

equity shares in the business (White and Dumay, 2017). Paul can also be seeking out for

business angels for funding his restaurant’s new oven, as business angels often take

personal risks in order to own shares of a growing business.

4

purchase of the new energy efficient intergrated oven needed in the machine. Sale of unused assets - The unused assets of a business can also be utilized for generating

funds for a business. The sale of such assets helps in raising good amount of funds. Paul

can also be seeking for unused assets in his restaurant such as the old oven that is not

used anymore, which can act as a good source of fund for Paul for his restaurant business.

Owner financing - The funds invested or capital introduced by the owner of a business

himself or herself is also a good source of funding (Chen and Elston, 2013). The biggest

advantage of this investment is that the burden of repayment is absent in this source. Paul

can be investing additional capital into his restaurant business in order to generate funds

for the purchase of the new oven he intends to be purchasing for his restaurant.

On the other hand, the following are external sources from which Paul can be generating funds

for his restaurant business is the following -

Bank overdraft - According to Cowling

et al. (2016), bank overdrafts are the short-term

external source of funding in which bank allows a certain sum of money to its customers

and allows them to draw money in spite of having no funds in the account. It is an

agreement of loan in which banks extend credit to customers to certain maximum amount

called the overdraft limit. Paul can also be relying on bank overdraft over funding its new

oven. Trade credit - Purchasing goods and services from suppliers on credit is known as trade

credit (Carbo‐Valverde

et al., 2016). The credit agreement between a business and its

suppliers also acts as a source of funds for a business. Paul can also be negotiating with

its suppliers and agree to purchase inputs at trade credit. Business angels - Another external source of funding are the business angels. Business

angels are the wealthy entrepreneurial individuals or people who provide good amount of

funds and invest capital into businesses in exchange of the return of a proportion of

equity shares in the business (White and Dumay, 2017). Paul can also be seeking out for

business angels for funding his restaurant’s new oven, as business angels often take

personal risks in order to own shares of a growing business.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Crowd funding - The practice of funding a venture through fund raising from a large

number of individuals who contribute relatively small amount of money through the

mode of internet is known as crowd funding (Kirby and Worner, 2014). Paul can also be

using the crowd funding as a source of fund for the new oven he intends to purchase for

the restaurant. The biggest advantage of crowd funding is that is a fast way for raising

finance without any upfront fees.

1.2 Evaluate the contribution that the sale of the old oven, the sub-letting of the unused space and

the selling of recipes for commission can make on the business’s profitability and cash flow

The current situation of the restaurant business of Paul has three main sources of income

available to it. All the three sources available to the business can be used for increasing the

profitability of the business along with adding to its cash flows. The following are the

contribution of the three sources of income available for Paul’s restaurant -

Sale of the old oven - The old oven of the restaurant can be sold off for £3000, which will

be helping the company in enhancing its cash flows. This amount can also be used for

generating funds for its new oven, as one fourth of the amount of the new oven can be

recovered from the sale of the old oven.

Sub-letting of the unused space - Sub-letting the unused space will be generating income

in a business at the end of every month. This will help in enhancing the restaurant’s cash

inflows and will be quite profitable as well for funding the purchase of its new oven.

Selling of recipes for commission - The selling of the recipes of dessert can also be

helping Paul’s restaurants in generating funds in the restaurant. The amount at which the

recipes will be sold has almost negligible cost of sales and thus the entire amount will be

the profits of the company. On the other hand, selling the recipes for commission will

also enhance the cash flows of the restaurant. The new oven intended to be purchased can

also be purchased using this commission.

5

Crowd funding - The practice of funding a venture through fund raising from a large

number of individuals who contribute relatively small amount of money through the

mode of internet is known as crowd funding (Kirby and Worner, 2014). Paul can also be

using the crowd funding as a source of fund for the new oven he intends to purchase for

the restaurant. The biggest advantage of crowd funding is that is a fast way for raising

finance without any upfront fees.

1.2 Evaluate the contribution that the sale of the old oven, the sub-letting of the unused space and

the selling of recipes for commission can make on the business’s profitability and cash flow

The current situation of the restaurant business of Paul has three main sources of income

available to it. All the three sources available to the business can be used for increasing the

profitability of the business along with adding to its cash flows. The following are the

contribution of the three sources of income available for Paul’s restaurant -

Sale of the old oven - The old oven of the restaurant can be sold off for £3000, which will

be helping the company in enhancing its cash flows. This amount can also be used for

generating funds for its new oven, as one fourth of the amount of the new oven can be

recovered from the sale of the old oven.

Sub-letting of the unused space - Sub-letting the unused space will be generating income

in a business at the end of every month. This will help in enhancing the restaurant’s cash

inflows and will be quite profitable as well for funding the purchase of its new oven.

Selling of recipes for commission - The selling of the recipes of dessert can also be

helping Paul’s restaurants in generating funds in the restaurant. The amount at which the

recipes will be sold has almost negligible cost of sales and thus the entire amount will be

the profits of the company. On the other hand, selling the recipes for commission will

also enhance the cash flows of the restaurant. The new oven intended to be purchased can

also be purchased using this commission.

5

2.1 Discuss elements of cost, gross profit percentages and selling prices for products and services

offered by a restaurant

In accountancy, cost can be defined as the cash amount or any amount that is equivalent to cash

is given up for an asset, including all kinds of costs needed to be spent for getting an asset in

place and making it ready to be used (Mishan, 2015). In order to ensure proper control of cost

and making effective managerial decisions on cost management, the different elements of cost

must be identified. There are three elements of costs, which are as follows -

Materials (Direct and indirect) - The costs spent by a company can be divided into two

categories - direct material and indirect material. Direct materials are the ones that can be

identified, conveniently measured as well as directly charged to products of a company.

For example, the costs spent in a restaurant for different input materials such as tables,

chairs, knives, cutlery, fruits, vegetables, etc. are its direct material costs. On the other

hand, the indirect material costs are the costs spent by a company on material, which

cannot be directly traced into cost units. For example, the postage expenses, the printing

costs, the stationery expenses, etc. are indirect material costs of a restaurant.

Labor (Direct and indirect) - The labor costs of a company can also be segregated into

direct and indirect. Direct labor costs refer to the labor expended in a company for

alteration of the condition and composition of the products of the company. On the other

hand, indirect labor costs are the costs spent on labor, which cannot be directly charged to

the products that are manufactured in the company. For example, the wages of the chef

and waiters of a restaurant are its direct labor cost while the feeds paid to the manager of

the restaurant are the indirect labor costs.

Overheads expenses (direct and indirect) - The overheads spent by a company can be

defined as the aggregate of the indirect labor, indirect materials and other indirect

expenses of a company. These expenses made by a company are not directly attributable

to cost units. For example, a restaurant business spends various expenses for

bookkeeping, insurance, cleaning, legal fees, advertising, etc. However, none of these

costs is attributable to any cost unit and thus considered as indirect overhead expenses of

the restaurant. On the other hand, the overhead expenses spent in a restaurant such as

excise duty and royalty are its direct overhead expenses.

6

offered by a restaurant

In accountancy, cost can be defined as the cash amount or any amount that is equivalent to cash

is given up for an asset, including all kinds of costs needed to be spent for getting an asset in

place and making it ready to be used (Mishan, 2015). In order to ensure proper control of cost

and making effective managerial decisions on cost management, the different elements of cost

must be identified. There are three elements of costs, which are as follows -

Materials (Direct and indirect) - The costs spent by a company can be divided into two

categories - direct material and indirect material. Direct materials are the ones that can be

identified, conveniently measured as well as directly charged to products of a company.

For example, the costs spent in a restaurant for different input materials such as tables,

chairs, knives, cutlery, fruits, vegetables, etc. are its direct material costs. On the other

hand, the indirect material costs are the costs spent by a company on material, which

cannot be directly traced into cost units. For example, the postage expenses, the printing

costs, the stationery expenses, etc. are indirect material costs of a restaurant.

Labor (Direct and indirect) - The labor costs of a company can also be segregated into

direct and indirect. Direct labor costs refer to the labor expended in a company for

alteration of the condition and composition of the products of the company. On the other

hand, indirect labor costs are the costs spent on labor, which cannot be directly charged to

the products that are manufactured in the company. For example, the wages of the chef

and waiters of a restaurant are its direct labor cost while the feeds paid to the manager of

the restaurant are the indirect labor costs.

Overheads expenses (direct and indirect) - The overheads spent by a company can be

defined as the aggregate of the indirect labor, indirect materials and other indirect

expenses of a company. These expenses made by a company are not directly attributable

to cost units. For example, a restaurant business spends various expenses for

bookkeeping, insurance, cleaning, legal fees, advertising, etc. However, none of these

costs is attributable to any cost unit and thus considered as indirect overhead expenses of

the restaurant. On the other hand, the overhead expenses spent in a restaurant such as

excise duty and royalty are its direct overhead expenses.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to Kjaer (2016), the gross profit percentage or margin is a financial metric that

assesses a firm’s financial stability and health through revealing the proportion of money left in

the firm after accounting for the cost of sales of the firm. The following is the formula of

deriving gross profit margin -

[Sales Revenue – COGS] * 100 / Sales Revenue

Thus, there are two basic elements of the gross profit percentage. The first element is the sales

revenue while the second element is the cost of goods sold. For a restaurant, the sales revenue

refers to the amount of money generated from rendering the different products and services of

the restaurant. On the other hand, cost of goods sold in a restaurant refers to the costs spent in the

restaurant for providing its customers with those products and services.

The selling price of a restaurant also comprises of certain elements (Danzigert

et al., 2014). The

elements are as follows -

Direct cost - The selling price offered to customers by a restaurant involves three types of

direct costs, which are direct material, direct labor and direct expenses.

Share of overheads - The overheads that are involved in the selling prices offered by a

restaurant are the production overheads, the administrative overheads and the selling and

distribution overheads.

Profit - Profit is the third and the last element in the selling prices of a company. The

products and services sold by a restaurant are sold after adding a certain amount of

increment. This amount is the profit of the restaurant.

2.2 Evaluate methods of controlling stock and cash in the restaurant

Controlling cash and stock is necessary for every business. Hospitality organizations also require

controlling cash and stock. The inventory management system helps a company in effective

stock control (McCullough and Blomgren, 2014). The following are the methods of stock control

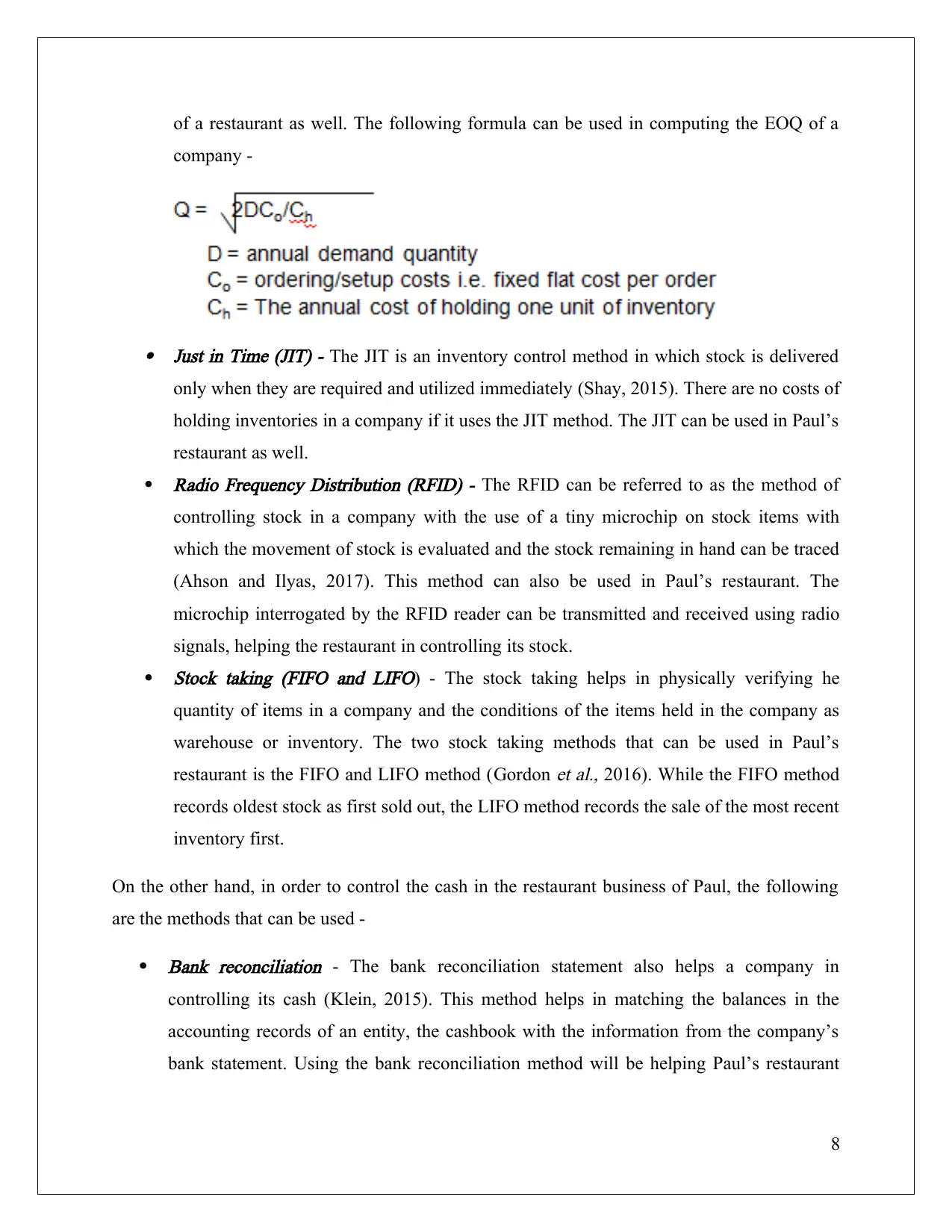

and inventory management that can be used in the restaurant business of Paul - Economic Order Quantity (EOQ) - The economic order quantity or the EOQ method

refers to the order quantity, which minimizes a company’s inventory ordering costs as

well as inventory holding costs (Chen

et al., 2014). This method can be applied in case

7

assesses a firm’s financial stability and health through revealing the proportion of money left in

the firm after accounting for the cost of sales of the firm. The following is the formula of

deriving gross profit margin -

[Sales Revenue – COGS] * 100 / Sales Revenue

Thus, there are two basic elements of the gross profit percentage. The first element is the sales

revenue while the second element is the cost of goods sold. For a restaurant, the sales revenue

refers to the amount of money generated from rendering the different products and services of

the restaurant. On the other hand, cost of goods sold in a restaurant refers to the costs spent in the

restaurant for providing its customers with those products and services.

The selling price of a restaurant also comprises of certain elements (Danzigert

et al., 2014). The

elements are as follows -

Direct cost - The selling price offered to customers by a restaurant involves three types of

direct costs, which are direct material, direct labor and direct expenses.

Share of overheads - The overheads that are involved in the selling prices offered by a

restaurant are the production overheads, the administrative overheads and the selling and

distribution overheads.

Profit - Profit is the third and the last element in the selling prices of a company. The

products and services sold by a restaurant are sold after adding a certain amount of

increment. This amount is the profit of the restaurant.

2.2 Evaluate methods of controlling stock and cash in the restaurant

Controlling cash and stock is necessary for every business. Hospitality organizations also require

controlling cash and stock. The inventory management system helps a company in effective

stock control (McCullough and Blomgren, 2014). The following are the methods of stock control

and inventory management that can be used in the restaurant business of Paul - Economic Order Quantity (EOQ) - The economic order quantity or the EOQ method

refers to the order quantity, which minimizes a company’s inventory ordering costs as

well as inventory holding costs (Chen

et al., 2014). This method can be applied in case

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of a restaurant as well. The following formula can be used in computing the EOQ of a

company -

Just in Time (JIT) - The JIT is an inventory control method in which stock is delivered

only when they are required and utilized immediately (Shay, 2015). There are no costs of

holding inventories in a company if it uses the JIT method. The JIT can be used in Paul’s

restaurant as well.

Radio Frequency Distribution (RFID) - The RFID can be referred to as the method of

controlling stock in a company with the use of a tiny microchip on stock items with

which the movement of stock is evaluated and the stock remaining in hand can be traced

(Ahson and Ilyas, 2017). This method can also be used in Paul’s restaurant. The

microchip interrogated by the RFID reader can be transmitted and received using radio

signals, helping the restaurant in controlling its stock.

Stock taking (FIFO and LIFO) - The stock taking helps in physically verifying he

quantity of items in a company and the conditions of the items held in the company as

warehouse or inventory. The two stock taking methods that can be used in Paul’s

restaurant is the FIFO and LIFO method (Gordon

et al., 2016). While the FIFO method

records oldest stock as first sold out, the LIFO method records the sale of the most recent

inventory first.

On the other hand, in order to control the cash in the restaurant business of Paul, the following

are the methods that can be used -

Bank reconciliation - The bank reconciliation statement also helps a company in

controlling its cash (Klein, 2015). This method helps in matching the balances in the

accounting records of an entity, the cashbook with the information from the company’s

bank statement. Using the bank reconciliation method will be helping Paul’s restaurant

8

company -

Just in Time (JIT) - The JIT is an inventory control method in which stock is delivered

only when they are required and utilized immediately (Shay, 2015). There are no costs of

holding inventories in a company if it uses the JIT method. The JIT can be used in Paul’s

restaurant as well.

Radio Frequency Distribution (RFID) - The RFID can be referred to as the method of

controlling stock in a company with the use of a tiny microchip on stock items with

which the movement of stock is evaluated and the stock remaining in hand can be traced

(Ahson and Ilyas, 2017). This method can also be used in Paul’s restaurant. The

microchip interrogated by the RFID reader can be transmitted and received using radio

signals, helping the restaurant in controlling its stock.

Stock taking (FIFO and LIFO) - The stock taking helps in physically verifying he

quantity of items in a company and the conditions of the items held in the company as

warehouse or inventory. The two stock taking methods that can be used in Paul’s

restaurant is the FIFO and LIFO method (Gordon

et al., 2016). While the FIFO method

records oldest stock as first sold out, the LIFO method records the sale of the most recent

inventory first.

On the other hand, in order to control the cash in the restaurant business of Paul, the following

are the methods that can be used -

Bank reconciliation - The bank reconciliation statement also helps a company in

controlling its cash (Klein, 2015). This method helps in matching the balances in the

accounting records of an entity, the cashbook with the information from the company’s

bank statement. Using the bank reconciliation method will be helping Paul’s restaurant

8

for ascertaining the frauds or the mishandling of cash that has taken place in the

restaurant.

Dual cash control - The establishment of cash handling policies in a business helps it in

reviewing the cash transactions made in the business (Zhao

et al., 2015). The policy of

dual cash control is one of the most effective cash handling policies. It helps in creating

an extra security layer in the cash management of a company, which its employees are

unaware. The risks of frauds taking place in the restaurant of Paul will be reduced due to

dual cash control, leading to decrease in its errors and increase in availability of backup.

Implementation of cctv cameras - Implementing cctvs within the office premises of a

business helps in cash control as well. Implementing cctvs in Paul’s restaurant will be

helpful for tracking the behaviour and movements of the staff working in the restaurant,

which help in detecting the cash mishandling or frauds taking place in the restaurant.

Proper bookkeeping records - The cash related problems in a company could also be

reduced with the help of maintaining proper bookkeeping records (Milanovic and

Trajkovic10, 2017). Ensuring the proper maintenance of bookkeeping records can be

useful for controlling the cash of Paul’s restaurant as well.

9

restaurant.

Dual cash control - The establishment of cash handling policies in a business helps it in

reviewing the cash transactions made in the business (Zhao

et al., 2015). The policy of

dual cash control is one of the most effective cash handling policies. It helps in creating

an extra security layer in the cash management of a company, which its employees are

unaware. The risks of frauds taking place in the restaurant of Paul will be reduced due to

dual cash control, leading to decrease in its errors and increase in availability of backup.

Implementation of cctv cameras - Implementing cctvs within the office premises of a

business helps in cash control as well. Implementing cctvs in Paul’s restaurant will be

helpful for tracking the behaviour and movements of the staff working in the restaurant,

which help in detecting the cash mishandling or frauds taking place in the restaurant.

Proper bookkeeping records - The cash related problems in a company could also be

reduced with the help of maintaining proper bookkeeping records (Milanovic and

Trajkovic10, 2017). Ensuring the proper maintenance of bookkeeping records can be

useful for controlling the cash of Paul’s restaurant as well.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference list

Ahson, S.A. and Ilyas, M., 2017.

RFID handbook: applications, technology, security, and

privacy. CRC press.

Carbo‐Valverde, S., Rodríguez‐Fernandez, F. and Udell, G.F., 2016. Trade credit, the financial

crisis, and SME access to finance.

Journal of Money, Credit and Banking,

48(1), pp.113-143.

Chen, S.C., Cárdenas-Barron, L.E. and Teng, J.T., 2014. Retailer’s economic order quantity

when the supplier offers conditionally permissible delay in payments link to order

quantity.

International Journal of Production Economics,

155, pp.284-291.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis.

International Journal of Entrepreneurial Behavior & Research,

22(6),

pp.903-932.

Danziger, S., Hadar, L. and Morwitz, V.G., 2014.Retailer pricing strategy and consumer choice

under price uncertainty.Journal of Consumer Research, 41(3), pp.761-774.

Elsas, R., Flannery, M.J. and Garfinkel, J.A., 2014. Financing major investments: information

about capital structure decisions.

Review of Finance,

18(4), pp.1341-1386.

Gordon, E.A., Raedy, J.S. and Sannella, A.J., 2016.

Intermediate Accounting. Pearson.

Kirby, E. and Worner, S., 2014. Crowd-funding: An infant industry growing fast. IOSCO,

Madrid.

Kjaer, H., EPISTA SOFTWARE A/S, 2016. Electronic mathematical model builder.U.S. Patent

9,465,787.

Klein, R., 2015. How to avoid or minimize fraud exposures.

The CPA Journal,

85(3), p.6.

McCullough, K. and Blomgren, S., 2014.

Inventory management system. U.S. Patent

Application 13/958,179.

10

Ahson, S.A. and Ilyas, M., 2017.

RFID handbook: applications, technology, security, and

privacy. CRC press.

Carbo‐Valverde, S., Rodríguez‐Fernandez, F. and Udell, G.F., 2016. Trade credit, the financial

crisis, and SME access to finance.

Journal of Money, Credit and Banking,

48(1), pp.113-143.

Chen, S.C., Cárdenas-Barron, L.E. and Teng, J.T., 2014. Retailer’s economic order quantity

when the supplier offers conditionally permissible delay in payments link to order

quantity.

International Journal of Production Economics,

155, pp.284-291.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis.

International Journal of Entrepreneurial Behavior & Research,

22(6),

pp.903-932.

Danziger, S., Hadar, L. and Morwitz, V.G., 2014.Retailer pricing strategy and consumer choice

under price uncertainty.Journal of Consumer Research, 41(3), pp.761-774.

Elsas, R., Flannery, M.J. and Garfinkel, J.A., 2014. Financing major investments: information

about capital structure decisions.

Review of Finance,

18(4), pp.1341-1386.

Gordon, E.A., Raedy, J.S. and Sannella, A.J., 2016.

Intermediate Accounting. Pearson.

Kirby, E. and Worner, S., 2014. Crowd-funding: An infant industry growing fast. IOSCO,

Madrid.

Kjaer, H., EPISTA SOFTWARE A/S, 2016. Electronic mathematical model builder.U.S. Patent

9,465,787.

Klein, R., 2015. How to avoid or minimize fraud exposures.

The CPA Journal,

85(3), p.6.

McCullough, K. and Blomgren, S., 2014.

Inventory management system. U.S. Patent

Application 13/958,179.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Milanovic, F. and Trajkovic10, M., 2017. POSSIBILITIES OF MONITORING THE

MAINTENANCE IN THE ACCOUNTING RECORDS.

FINANCE, BANKING AND

INSURANCE, p.88.

Mishan, E.J., 2015.

Elements of Cost-Benefit Analysis (Routledge Revivals). Routledge.

Peirson, G., Brown, R., Easton, S. and Howard, P., 2014.Business finance.McGraw-Hill

Education Australia.

Shay, K., 2015.

Just in time (Vol. 1). Ocean View Books.

Tanrisever, F., Cetinay, H., Reindorp, M. and Fransoo, J., 2015. Reverse factoring for SME

finance.

White, B.A. and Dumay, J., 2017. Business angels: a research review and new agenda. Venture

Capital, 19(3), pp.183-216.

Zhao, F., Dash Wu, D., Liang, L. and Dolgui, A., 2015. Cash flow risk in dual-channel supply

chain.

International Journal of Production Research,

53(12), pp.3678-3691.

11

MAINTENANCE IN THE ACCOUNTING RECORDS.

FINANCE, BANKING AND

INSURANCE, p.88.

Mishan, E.J., 2015.

Elements of Cost-Benefit Analysis (Routledge Revivals). Routledge.

Peirson, G., Brown, R., Easton, S. and Howard, P., 2014.Business finance.McGraw-Hill

Education Australia.

Shay, K., 2015.

Just in time (Vol. 1). Ocean View Books.

Tanrisever, F., Cetinay, H., Reindorp, M. and Fransoo, J., 2015. Reverse factoring for SME

finance.

White, B.A. and Dumay, J., 2017. Business angels: a research review and new agenda. Venture

Capital, 19(3), pp.183-216.

Zhao, F., Dash Wu, D., Liang, L. and Dolgui, A., 2015. Cash flow risk in dual-channel supply

chain.

International Journal of Production Research,

53(12), pp.3678-3691.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.