Finance in Hospitality Report

VerifiedAdded on 2019/12/03

|26

|7579

|138

Report

AI Summary

This report delves into the financial aspects of the hospitality industry, specifically focusing on a large restaurant chain. It examines various sources of funding, including debt, equity, and venture capital, weighing their advantages and disadvantages. The report then analyzes cost elements, gross profit percentage, and selling price, exploring methods for controlling stock and cash. Budgetary control processes are detailed, along with variance analysis between budgeted and actual performance, offering recommendations for improvement. The report also includes an analysis of financial statements, ratio analysis (gross profit, net profit, current, liquid, debtor, and creditor collection periods), and recommendations for enhancing business performance. Finally, it discusses fixed, variable, and semi-variable costs, and uses break-even calculations to inform short-term management decisions. The website provides this solved assignment and other past papers to help students.

FINANCE IN HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION....................................................................................................................... 1

TASK 1....................................................................................................................................... 1

1.1 Sources of funding available to business............................................................................ 1

1.2 Contribution made by various methods of generating income for a large chain of

restaurants............................................................................................................................... 2

TASK 2....................................................................................................................................... 2

2.1 Elements of cost, gross profit percentage and selling price ...............................................2

2.2 Evaluating methods of controlling stock and cash.............................................................3

TASK 3....................................................................................................................................... 4

3.3 Process and purpose of budgetary control .........................................................................4

3.4 Analyzing variance of budgeted performance from actual performance and

recommendations.................................................................................................................... 4

TASK 4 ...................................................................................................................................... 5

3.1 Source and structure of trial balance..................................................................................5

3.2 Adjustments in financial statements................................................................................... 6

4.1 & 4.2 Ratio analysis and recommendations.......................................................................8

TASK 5....................................................................................................................................... 9

5.1 Brief notes on fixed, variable and semi-variable costs......................................................9

5.3 Short term management decision based on break even calculation...................................12

CONCLUSION.......................................................................................................................... 12

REFERENCES ....................................................................................................................... 13

1

INTRODUCTION....................................................................................................................... 1

TASK 1....................................................................................................................................... 1

1.1 Sources of funding available to business............................................................................ 1

1.2 Contribution made by various methods of generating income for a large chain of

restaurants............................................................................................................................... 2

TASK 2....................................................................................................................................... 2

2.1 Elements of cost, gross profit percentage and selling price ...............................................2

2.2 Evaluating methods of controlling stock and cash.............................................................3

TASK 3....................................................................................................................................... 4

3.3 Process and purpose of budgetary control .........................................................................4

3.4 Analyzing variance of budgeted performance from actual performance and

recommendations.................................................................................................................... 4

TASK 4 ...................................................................................................................................... 5

3.1 Source and structure of trial balance..................................................................................5

3.2 Adjustments in financial statements................................................................................... 6

4.1 & 4.2 Ratio analysis and recommendations.......................................................................8

TASK 5....................................................................................................................................... 9

5.1 Brief notes on fixed, variable and semi-variable costs......................................................9

5.3 Short term management decision based on break even calculation...................................12

CONCLUSION.......................................................................................................................... 12

REFERENCES ....................................................................................................................... 13

1

INTRODUCTION

Finance plays a vital role in the growth of any organization. Along with this, companies

are also required to control their costs. This requires application of various techniques. In this

report, some of the techniques regarding cost evaluation are presented and probable reason for

variance in performance is also explained in detail. Further, ratio analysis is also done in order to

evaluate the business. After that, recommendations are made regarding improvement in business

performance. Along with these, adjustments are also made in P&L account and balance sheet of

the firm. Further, ways in which adjustments are made is also discussed in this report.

TASK 1

1.1

Finance plays a vital role in the growth of an organization. In today’s uncertain business

environment, it is difficult to raise entire amount from a single source of finance. Hence,

business firms collect a specific corpus from various sources of finance in the specific

proportion. Some sources though which Aquapet can raise funds are given below:

External sources

1 Debt/ long term loan – Aquapet can raise loan from banks or NBFC'S at fixed or floating

interest rates.

Advantage- The main advantage of debt is that in this source of finance ownership of owners of

the company does not get diluted. Hence, they are able to maintain full control on firm.

Disadvantages- It depends on the management of Aquapet only that at which interest rate, they

take loan. In past years, it has been seen that firms who raise loan at floating interest rate face a

lot of problems due to frequent change in the interest rates structure by the central bank and

fluctuation in currency in an international market (Mayer, Schoors and Yafeh, 2005). With

increase in interest rate and weakness in domestic currency debt payment liability on firms get

increased. Hence, it is recommended that firms must abstain from taking loan at floating interest

rate.

1 Venture capital- This is an alternative source of finance of equity. Under this system,

there is a firm that provides capital to its client firm and in return, it gets ownership in

2

Finance plays a vital role in the growth of any organization. Along with this, companies

are also required to control their costs. This requires application of various techniques. In this

report, some of the techniques regarding cost evaluation are presented and probable reason for

variance in performance is also explained in detail. Further, ratio analysis is also done in order to

evaluate the business. After that, recommendations are made regarding improvement in business

performance. Along with these, adjustments are also made in P&L account and balance sheet of

the firm. Further, ways in which adjustments are made is also discussed in this report.

TASK 1

1.1

Finance plays a vital role in the growth of an organization. In today’s uncertain business

environment, it is difficult to raise entire amount from a single source of finance. Hence,

business firms collect a specific corpus from various sources of finance in the specific

proportion. Some sources though which Aquapet can raise funds are given below:

External sources

1 Debt/ long term loan – Aquapet can raise loan from banks or NBFC'S at fixed or floating

interest rates.

Advantage- The main advantage of debt is that in this source of finance ownership of owners of

the company does not get diluted. Hence, they are able to maintain full control on firm.

Disadvantages- It depends on the management of Aquapet only that at which interest rate, they

take loan. In past years, it has been seen that firms who raise loan at floating interest rate face a

lot of problems due to frequent change in the interest rates structure by the central bank and

fluctuation in currency in an international market (Mayer, Schoors and Yafeh, 2005). With

increase in interest rate and weakness in domestic currency debt payment liability on firms get

increased. Hence, it is recommended that firms must abstain from taking loan at floating interest

rate.

1 Venture capital- This is an alternative source of finance of equity. Under this system,

there is a firm that provides capital to its client firm and in return, it gets ownership in

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company’s stock. Hence, company does not need to resort to banks for financing their

operations. The other benefit that this source of finance gives is that it also gets legal entitle to

give guidance to the firm regarding business policy and strategy. The main disadvantage of

venture capital is that ownership of existing shareholders gets diluted in the firm. Hence,

decision making power of directors gets reduced. Thus, it is an inverse of debt as a source of

finance and due to this reason; it is quite popular in USA and Europe.

2 Equity- When firms wants to start any project they can approach primary market for

raising capital through IPO or FPO. The main advantage of this source of finance is that like

debt it is not necessary to pay dividend each and every year. But issue of shares dilutes control

of existing shareholders on the company. Hence, this source of finance has both positive and

negative points.

3 Private equity- If firm is not eligible to raise capital from stock market then it can

approach private equity firms for financing their business projects (Galia and Legros, 2004). The

main benefit of this source of finance is that at infant stage firm get a large amount of capital

that it cannot get from banks or NBFC'S. But in this source of finance company have to sell its

stack to private equity firms. Hence, control of existing shareholders on the company gets

reduced which is major disadvantage of this source of finance.

4 Short term loan- This loan is available from banks and NBFC'S for short duration say

one year. The main benefit of this source of finance is that firm can fulfill its working capital

requirements from this source of finance. The main disadvantage is that if loan is taken at

floating rate then finance burden on the company get increased.

5 Debentures- It is a written acknowledgment of debt taken by the company from the

public. In return firm pay interest to the debenture holders. In this source of finance it is

necessary to pay interest in specific time period . If financial condition is not good then payment

of interest may create problem for an organization. This is major limitation of this source of

finance. But control of existing shareholders does not get diluted in case of debentures. So, it has

both positive and negative points.

6 Consortium finance- Consortium finance is taken when single bank cannot finance

entire project and multiple banks are required to finance specific project which will be executed

in the domestic land. Like debenture in case of this source of finance it is necessary to pay

interest on time and this is major limitation of this source of finance. But in this case

3

operations. The other benefit that this source of finance gives is that it also gets legal entitle to

give guidance to the firm regarding business policy and strategy. The main disadvantage of

venture capital is that ownership of existing shareholders gets diluted in the firm. Hence,

decision making power of directors gets reduced. Thus, it is an inverse of debt as a source of

finance and due to this reason; it is quite popular in USA and Europe.

2 Equity- When firms wants to start any project they can approach primary market for

raising capital through IPO or FPO. The main advantage of this source of finance is that like

debt it is not necessary to pay dividend each and every year. But issue of shares dilutes control

of existing shareholders on the company. Hence, this source of finance has both positive and

negative points.

3 Private equity- If firm is not eligible to raise capital from stock market then it can

approach private equity firms for financing their business projects (Galia and Legros, 2004). The

main benefit of this source of finance is that at infant stage firm get a large amount of capital

that it cannot get from banks or NBFC'S. But in this source of finance company have to sell its

stack to private equity firms. Hence, control of existing shareholders on the company gets

reduced which is major disadvantage of this source of finance.

4 Short term loan- This loan is available from banks and NBFC'S for short duration say

one year. The main benefit of this source of finance is that firm can fulfill its working capital

requirements from this source of finance. The main disadvantage is that if loan is taken at

floating rate then finance burden on the company get increased.

5 Debentures- It is a written acknowledgment of debt taken by the company from the

public. In return firm pay interest to the debenture holders. In this source of finance it is

necessary to pay interest in specific time period . If financial condition is not good then payment

of interest may create problem for an organization. This is major limitation of this source of

finance. But control of existing shareholders does not get diluted in case of debentures. So, it has

both positive and negative points.

6 Consortium finance- Consortium finance is taken when single bank cannot finance

entire project and multiple banks are required to finance specific project which will be executed

in the domestic land. Like debenture in case of this source of finance it is necessary to pay

interest on time and this is major limitation of this source of finance. But in this case

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shareholders control on the company does not get diluted. Hence, this is major advantage of this

source of finance.

Internal sources

Retained earnings- It is a portion of profit that remains after payment of expenses and

debt from company’s revenue (Irwin and Scott, 2011). This is the commonly used source of

finance among all categories of organizations whether they are sole trader, partnership or

company because organization is not liable to pay any sort of finance cost to any institute. This

source of finance does not have any limitation.

Equity, debt and consortium finance are three sources of finance that can be used in order

to finance entire finance requirements. In case of equity 60% stack remains with the company

owners and liability to pay fixed amount periodically also not created. But company power to

take decision get reduced. In case company failed to raise capital from equity then it can issue

capital from debt. But due to poor economic conditions banks are following a cautious approach

and they may deny from financing a project. Hence, consortium finance is suggested to the

mentioned firm in which multiple banks will collectively finance firm. This is selected because

in this source of finance owners will have full control of company and due to sharing of risk

banks will also prepared to finance company project easily.

1.2

There are many things that play an important role in generating revenue for the firm.

Some of them are given below:

1 Sales- Sales is an item in a company’s P&L account that represents money that a firm

earned from sales. For generating sales, large chain of restaurants need to put various sorts of

efforts. This is because; there are numerous hotels in London or in entire UK due to high

inbound tourism in the mentioned nation. As a result, there is a stiff competition among firms in

the relevant industry (Eriksson, Katila and Niskanen, 2009). Therefore, Aquapet requires

formulating and implementing some unique strategies in order to flourish its business in the

relevant industry.

2 Home delivery service- In today’s time period, people is busy and they find it difficult to

cook their food on time. As a result, home delivery service is increasing rapidly in London.

4

source of finance.

Internal sources

Retained earnings- It is a portion of profit that remains after payment of expenses and

debt from company’s revenue (Irwin and Scott, 2011). This is the commonly used source of

finance among all categories of organizations whether they are sole trader, partnership or

company because organization is not liable to pay any sort of finance cost to any institute. This

source of finance does not have any limitation.

Equity, debt and consortium finance are three sources of finance that can be used in order

to finance entire finance requirements. In case of equity 60% stack remains with the company

owners and liability to pay fixed amount periodically also not created. But company power to

take decision get reduced. In case company failed to raise capital from equity then it can issue

capital from debt. But due to poor economic conditions banks are following a cautious approach

and they may deny from financing a project. Hence, consortium finance is suggested to the

mentioned firm in which multiple banks will collectively finance firm. This is selected because

in this source of finance owners will have full control of company and due to sharing of risk

banks will also prepared to finance company project easily.

1.2

There are many things that play an important role in generating revenue for the firm.

Some of them are given below:

1 Sales- Sales is an item in a company’s P&L account that represents money that a firm

earned from sales. For generating sales, large chain of restaurants need to put various sorts of

efforts. This is because; there are numerous hotels in London or in entire UK due to high

inbound tourism in the mentioned nation. As a result, there is a stiff competition among firms in

the relevant industry (Eriksson, Katila and Niskanen, 2009). Therefore, Aquapet requires

formulating and implementing some unique strategies in order to flourish its business in the

relevant industry.

2 Home delivery service- In today’s time period, people is busy and they find it difficult to

cook their food on time. As a result, home delivery service is increasing rapidly in London.

4

Thus, Aquapet by entering in this segment of business can grow at a fast rate in hospitality

industry.

3 Renting place for an occasion- Aquapet can rent a place for specific occasions like

conference on business or social issues and marriage etc. By focusing on this segment, firm can

elevate its revenue (Atkinson, 2005). Normally, hotels charge a very high amount for such kind

of services and due to this reason, their profitability gets increased. Hence, Aquapet must pay

close attention on this segment of business.

Advantages

Only benefit that a restaurant can get from sale of unused asset is that it will not need to

go to bank for financing its operations. By selling assets firm operations will be financed

and it will not need to pay any sort of finance cost. So both have advantages and

disadvantage for Aquapet and it needs to follow cautious approach for making prudent

decision.

Adoption of this method will lead to saving in terms of finance cost. Hence, economies

of scale will be generated and that saved amount will be used for other productive

activity.

Disadvantages

Company may sell its assets to finance its operation due to lack of cash and poor

performance of restaurant. But if restaurant changed its policy and it starts earning profit

then in future it may face problems due to scarcity of resources. Hence, firm will again

need to purchase asset in order to met customer demand. This, this strategy is not good

for the firm.

In future price of these assets may increase and become costly to buy. Hence, sale of

asset may prove disadvantageous for the firm in long term.

In upcoming time period asset of price may increase at higher rate. Means that if these

asset are sold in future then good profit can be earned in comparison to profit that a firm

will earn if assets ares old on current date. Hence, decision to sell asset on current date

may prove disadvantageous for the firm.

5

industry.

3 Renting place for an occasion- Aquapet can rent a place for specific occasions like

conference on business or social issues and marriage etc. By focusing on this segment, firm can

elevate its revenue (Atkinson, 2005). Normally, hotels charge a very high amount for such kind

of services and due to this reason, their profitability gets increased. Hence, Aquapet must pay

close attention on this segment of business.

Advantages

Only benefit that a restaurant can get from sale of unused asset is that it will not need to

go to bank for financing its operations. By selling assets firm operations will be financed

and it will not need to pay any sort of finance cost. So both have advantages and

disadvantage for Aquapet and it needs to follow cautious approach for making prudent

decision.

Adoption of this method will lead to saving in terms of finance cost. Hence, economies

of scale will be generated and that saved amount will be used for other productive

activity.

Disadvantages

Company may sell its assets to finance its operation due to lack of cash and poor

performance of restaurant. But if restaurant changed its policy and it starts earning profit

then in future it may face problems due to scarcity of resources. Hence, firm will again

need to purchase asset in order to met customer demand. This, this strategy is not good

for the firm.

In future price of these assets may increase and become costly to buy. Hence, sale of

asset may prove disadvantageous for the firm in long term.

In upcoming time period asset of price may increase at higher rate. Means that if these

asset are sold in future then good profit can be earned in comparison to profit that a firm

will earn if assets ares old on current date. Hence, decision to sell asset on current date

may prove disadvantageous for the firm.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2.1

Cost- It refers to the expenses that we incurred to produce goods and services. For

Aquapet, it includes carrier bags, food waste and staffing costs. On the other hand, indirect costs

include stationery, telephone expenses, security and electricity expenses. These costs are

combined to compute the cost of service for Aquapet. As mentioned in the case study, control of

stock and cash is an important factor for a business. Thus, management of Aquapet is required to

use its cash in an efficient and effective manner. On the other hand, it must also keep stiff

control on stock quantity in order to prevent the blockage of money in stock. It is clear that

enhancement in cost cannot be passed directly to the customers (Andreff, 2007). Hence, firm is

required to make its management very effective in order to reduce its service cost.

There are three elements of cost like material, labor and expenses. These costs are further

divided in to direct and indirect costs. Direct material, labor and expenses are those costs that are

directly related to production of goods and services.

Indirect cost- Indirect cost are those cost that are not related to production process. Employees

that are working in sales and administrative departments and expense regarding same are

example of indirect cost.

Indirect labor cost- It refers to those employees that are not involved in production

process. Cost incurred in respect to this employees is known as direct material cost.

Indirect material cost- It refers to material that are not used in production process. Cost

incurred in packaging is indirect material cost because it is not incurred during production

process.

Indirect expenses- These are those expenses that are not incurred in production process.

Cost of carriage is best example of indirect expenses.

Direct cost- Direct cost are those cost that are directly related to the production of goods and

services. Material used for production and employees working in plant as well as expenses

regarding same are example of direct cost. These costs are then considered to compute final

value of the product.

Direct labor- These are those employees that are directly involved in the production process.

With change in production level direct labor cost may also change.

6

2.1

Cost- It refers to the expenses that we incurred to produce goods and services. For

Aquapet, it includes carrier bags, food waste and staffing costs. On the other hand, indirect costs

include stationery, telephone expenses, security and electricity expenses. These costs are

combined to compute the cost of service for Aquapet. As mentioned in the case study, control of

stock and cash is an important factor for a business. Thus, management of Aquapet is required to

use its cash in an efficient and effective manner. On the other hand, it must also keep stiff

control on stock quantity in order to prevent the blockage of money in stock. It is clear that

enhancement in cost cannot be passed directly to the customers (Andreff, 2007). Hence, firm is

required to make its management very effective in order to reduce its service cost.

There are three elements of cost like material, labor and expenses. These costs are further

divided in to direct and indirect costs. Direct material, labor and expenses are those costs that are

directly related to production of goods and services.

Indirect cost- Indirect cost are those cost that are not related to production process. Employees

that are working in sales and administrative departments and expense regarding same are

example of indirect cost.

Indirect labor cost- It refers to those employees that are not involved in production

process. Cost incurred in respect to this employees is known as direct material cost.

Indirect material cost- It refers to material that are not used in production process. Cost

incurred in packaging is indirect material cost because it is not incurred during production

process.

Indirect expenses- These are those expenses that are not incurred in production process.

Cost of carriage is best example of indirect expenses.

Direct cost- Direct cost are those cost that are directly related to the production of goods and

services. Material used for production and employees working in plant as well as expenses

regarding same are example of direct cost. These costs are then considered to compute final

value of the product.

Direct labor- These are those employees that are directly involved in the production process.

With change in production level direct labor cost may also change.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material- It refers to material that is used in the production process. Cost incurred

to purchase direct material is treated as direct material cost. Like direct labor with change in

production direct material cost also get changed.

Direct expenses- Other expenses that are incurred in production process is known as

direct expenses. These may be electricity expenses.

Cost is also divided into fixed and variable cost and both affects cost of production of the

company.

Fixed cost- These are those costs that can not be change with change in production of goods and

services. Investment in plant and machinery is best example of fixed cost.

Variable cost- It is a cost that gt changed with change in level of production of goods and

services. Employee cost and raw material purchase amount are the best examples of variable

cost.

Effects of these costs and way to control

If production of the company declines and sale price remain constant then cost of production get

increased in cost of production and profitability of the firm get declined. Fixed cost cannot be

reduced but its elevation can be controlled. Best example of fixed cost is investment in building.

Its cost cannot be reduced but traction in this cost can be prevented. On other hand variable cost

can be reduced or controlled by adopting cost control techniques. Employee cost is variable cost

and it can be reduced by the company at any time by following employee lay off approach.

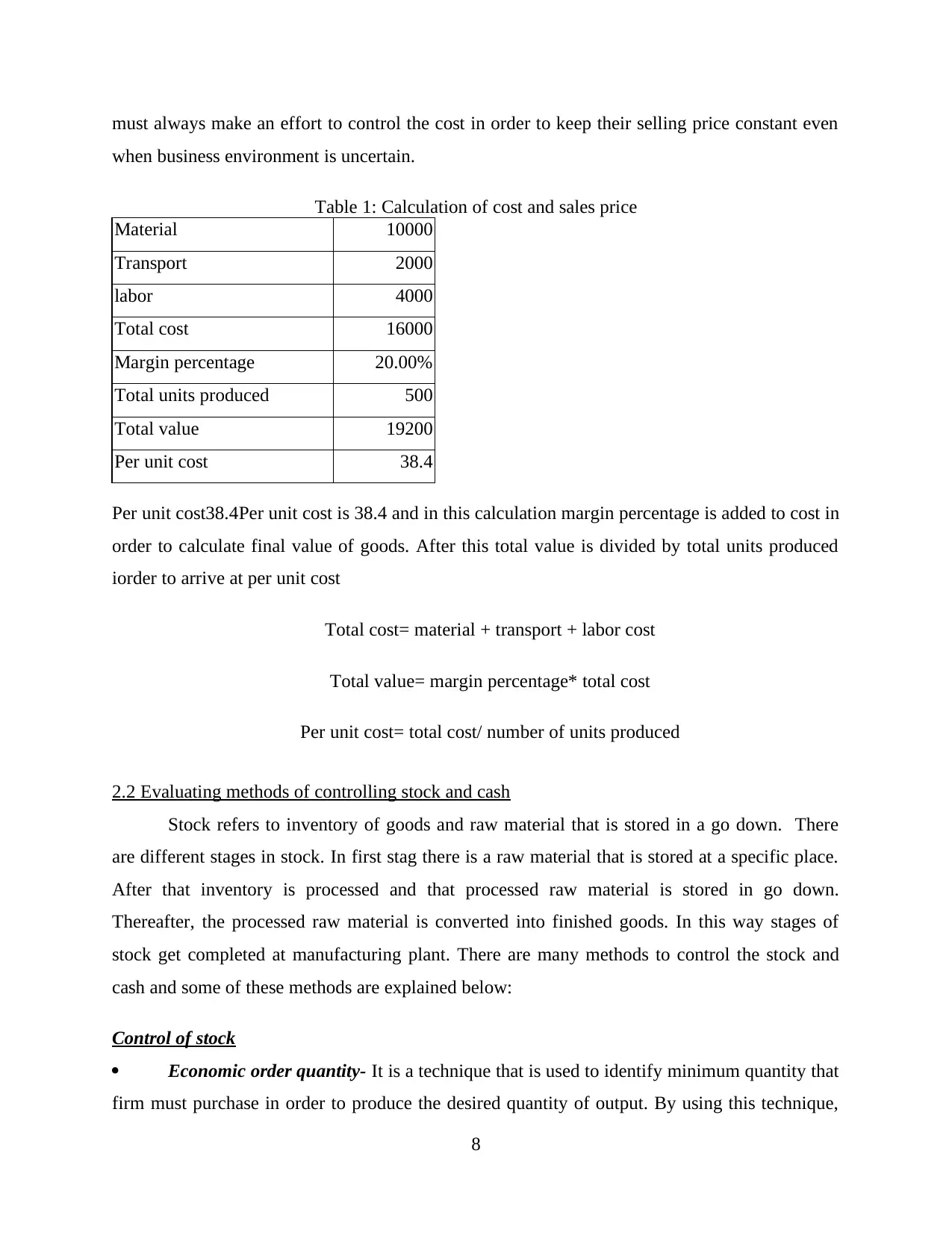

Gross profit- Gross profit percentage is calculated by dividing gross profit by net sales

multiplied by hundred. Hence, gross profit and net sales are two main components which are

used while calculating the gross profit percentage. This percentage when compared with the

previous quarter percentage indicates that whether firm successfully controls its cost or not. But

this is only possible to find out only when sales price remains static.

Gross profit percentage= gross profit/ net sales*100

= (19200-16000)/19200*100= 16.66%

Selling price- Sales price is calculated by using the cost of production plus margin on

sales. Thus, cost of goods sold and margin percentage are two components of computing sales

price. Firms by looking at surrounding business conditions determine margin percentage for

sales (Brealey, 2012). With decline in sales margin, percentage also gets changed. Hence, firms

7

to purchase direct material is treated as direct material cost. Like direct labor with change in

production direct material cost also get changed.

Direct expenses- Other expenses that are incurred in production process is known as

direct expenses. These may be electricity expenses.

Cost is also divided into fixed and variable cost and both affects cost of production of the

company.

Fixed cost- These are those costs that can not be change with change in production of goods and

services. Investment in plant and machinery is best example of fixed cost.

Variable cost- It is a cost that gt changed with change in level of production of goods and

services. Employee cost and raw material purchase amount are the best examples of variable

cost.

Effects of these costs and way to control

If production of the company declines and sale price remain constant then cost of production get

increased in cost of production and profitability of the firm get declined. Fixed cost cannot be

reduced but its elevation can be controlled. Best example of fixed cost is investment in building.

Its cost cannot be reduced but traction in this cost can be prevented. On other hand variable cost

can be reduced or controlled by adopting cost control techniques. Employee cost is variable cost

and it can be reduced by the company at any time by following employee lay off approach.

Gross profit- Gross profit percentage is calculated by dividing gross profit by net sales

multiplied by hundred. Hence, gross profit and net sales are two main components which are

used while calculating the gross profit percentage. This percentage when compared with the

previous quarter percentage indicates that whether firm successfully controls its cost or not. But

this is only possible to find out only when sales price remains static.

Gross profit percentage= gross profit/ net sales*100

= (19200-16000)/19200*100= 16.66%

Selling price- Sales price is calculated by using the cost of production plus margin on

sales. Thus, cost of goods sold and margin percentage are two components of computing sales

price. Firms by looking at surrounding business conditions determine margin percentage for

sales (Brealey, 2012). With decline in sales margin, percentage also gets changed. Hence, firms

7

must always make an effort to control the cost in order to keep their selling price constant even

when business environment is uncertain.

Table 1: Calculation of cost and sales price

Material 10000

Transport 2000

labor 4000

Total cost 16000

Margin percentage 20.00%

Total units produced 500

Total value 19200

Per unit cost 38.4

Per unit cost38.4Per unit cost is 38.4 and in this calculation margin percentage is added to cost in

order to calculate final value of goods. After this total value is divided by total units produced

iorder to arrive at per unit cost

Total cost= material + transport + labor cost

Total value= margin percentage* total cost

Per unit cost= total cost/ number of units produced

2.2 Evaluating methods of controlling stock and cash

Stock refers to inventory of goods and raw material that is stored in a go down. There

are different stages in stock. In first stag there is a raw material that is stored at a specific place.

After that inventory is processed and that processed raw material is stored in go down.

Thereafter, the processed raw material is converted into finished goods. In this way stages of

stock get completed at manufacturing plant. There are many methods to control the stock and

cash and some of these methods are explained below:

Control of stock

Economic order quantity- It is a technique that is used to identify minimum quantity that

firm must purchase in order to produce the desired quantity of output. By using this technique,

8

when business environment is uncertain.

Table 1: Calculation of cost and sales price

Material 10000

Transport 2000

labor 4000

Total cost 16000

Margin percentage 20.00%

Total units produced 500

Total value 19200

Per unit cost 38.4

Per unit cost38.4Per unit cost is 38.4 and in this calculation margin percentage is added to cost in

order to calculate final value of goods. After this total value is divided by total units produced

iorder to arrive at per unit cost

Total cost= material + transport + labor cost

Total value= margin percentage* total cost

Per unit cost= total cost/ number of units produced

2.2 Evaluating methods of controlling stock and cash

Stock refers to inventory of goods and raw material that is stored in a go down. There

are different stages in stock. In first stag there is a raw material that is stored at a specific place.

After that inventory is processed and that processed raw material is stored in go down.

Thereafter, the processed raw material is converted into finished goods. In this way stages of

stock get completed at manufacturing plant. There are many methods to control the stock and

cash and some of these methods are explained below:

Control of stock

Economic order quantity- It is a technique that is used to identify minimum quantity that

firm must purchase in order to produce the desired quantity of output. By using this technique,

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company abstains from employing unnecessary amount on the purchase of raw material.

Moreover, cash is also not blocked on unused inventory. Thus, this technique also helps in

managing cash in an appropriate manner.

EOQ= ?2SD/PI

Where

SD= set up cost

D= Demand rate

P= production cost

I= Interest rate

Minimum quantity- By using old data, Aquapet can identify minimum quantity of raw

material that it mostly consumes in specific duration say month or quarter (Petersen, 2009). By

following this technique, firm can manage its cash in a proper manner and also prevents the

blockage of cash in unused stock.

Just in time- It is a technique that is used to control stock. As per this technique raw

material are purchased to meet actual demand. As a result good control is maintained on stock

and amount is prevented from being locked in unused inventory.

Recorder point (ROP) - This method is used for system controlled process and is also

used for controlling manual as well as visual environment. Due to this reason this technique is

widely used by organizations at the manufacturing facility.

LIFO- LIFO means last in first out and it says that units that are produced at end must be

sold first so that its value does not deteriorate.

FIFO – This concept state that inventory of units that is produced first must be sold first.

Hence, inventory that remains at the end of a year is sod at the end of the year.

ANTIPATORY- It is a technique that is used to forecast inventory that will be required in

future. In this way this technique helps in controlling stock in upcoming time period.

RESPONSE- It is a system that is used to control stock when business situation gets

changed. With change in condition by using this system new inventory control targets are

determined.

Control of cash

9

Moreover, cash is also not blocked on unused inventory. Thus, this technique also helps in

managing cash in an appropriate manner.

EOQ= ?2SD/PI

Where

SD= set up cost

D= Demand rate

P= production cost

I= Interest rate

Minimum quantity- By using old data, Aquapet can identify minimum quantity of raw

material that it mostly consumes in specific duration say month or quarter (Petersen, 2009). By

following this technique, firm can manage its cash in a proper manner and also prevents the

blockage of cash in unused stock.

Just in time- It is a technique that is used to control stock. As per this technique raw

material are purchased to meet actual demand. As a result good control is maintained on stock

and amount is prevented from being locked in unused inventory.

Recorder point (ROP) - This method is used for system controlled process and is also

used for controlling manual as well as visual environment. Due to this reason this technique is

widely used by organizations at the manufacturing facility.

LIFO- LIFO means last in first out and it says that units that are produced at end must be

sold first so that its value does not deteriorate.

FIFO – This concept state that inventory of units that is produced first must be sold first.

Hence, inventory that remains at the end of a year is sod at the end of the year.

ANTIPATORY- It is a technique that is used to forecast inventory that will be required in

future. In this way this technique helps in controlling stock in upcoming time period.

RESPONSE- It is a system that is used to control stock when business situation gets

changed. With change in condition by using this system new inventory control targets are

determined.

Control of cash

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There is a lots of importance of cash and by using this business in run smoothly even

business conditions are uncertain. For controlling cash, firm can use cash management strategy

under which it will control cash inflow and outflow. With respect to this, Aquapet can centralize

its payment system and on the other hand, it can decentralize its receipt system. Along with this,

firm will make all payments by cheques. By doing all these efforts, firm can control its cash

outflow or can extend the time for cash outflow (Ross, Westerfield and Jordan, 2008). However,

due to decentralization in receipt system, cash inflow intensity will get increased. In this way,

firm will be able to control the cash in a proper manner.

There is system under which company maintains its own cash book in which entries of

receipts and payment is made. This book is compared with bank pass book in order to make sure

that any sort of wrong entry is not made in banks pass book and company managed book. In

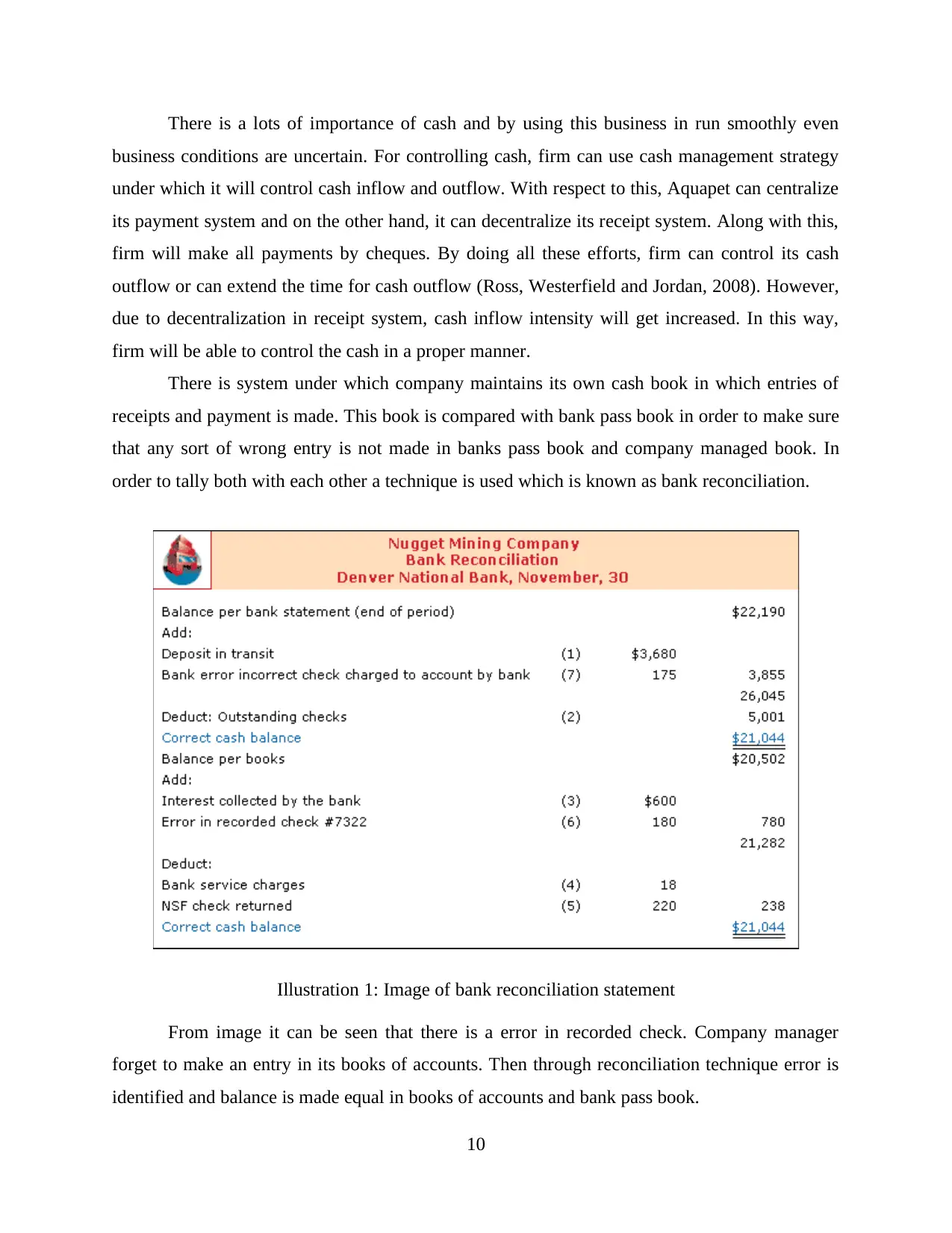

order to tally both with each other a technique is used which is known as bank reconciliation.

Illustration 1: Image of bank reconciliation statement

From image it can be seen that there is a error in recorded check. Company manager

forget to make an entry in its books of accounts. Then through reconciliation technique error is

identified and balance is made equal in books of accounts and bank pass book.

10

business conditions are uncertain. For controlling cash, firm can use cash management strategy

under which it will control cash inflow and outflow. With respect to this, Aquapet can centralize

its payment system and on the other hand, it can decentralize its receipt system. Along with this,

firm will make all payments by cheques. By doing all these efforts, firm can control its cash

outflow or can extend the time for cash outflow (Ross, Westerfield and Jordan, 2008). However,

due to decentralization in receipt system, cash inflow intensity will get increased. In this way,

firm will be able to control the cash in a proper manner.

There is system under which company maintains its own cash book in which entries of

receipts and payment is made. This book is compared with bank pass book in order to make sure

that any sort of wrong entry is not made in banks pass book and company managed book. In

order to tally both with each other a technique is used which is known as bank reconciliation.

Illustration 1: Image of bank reconciliation statement

From image it can be seen that there is a error in recorded check. Company manager

forget to make an entry in its books of accounts. Then through reconciliation technique error is

identified and balance is made equal in books of accounts and bank pass book.

10

TASK 3

3.3 Process and purpose of budgetary control

Process of budgetary control

Determine standard- This is the first stage in budgetary control process and in this step,

standards are determined for the cost and revenue. These standards are further used to identify

whether the firm gives good or poor performance (Allen, Qian and Qian, 2005).

Measuring performance- This is the second step and under this stage, performance of

the firm is measured in terms of value.

Comparison of actual performance with determined standards- In the third stage, after

measurement of performance, comparison of same is done with standards in order to identify

positive and negative points of company with respect to budget for specific quarter.

Identify variance/evalauting- By making comparison; managers identify the areas where

company gives a good and poor performance. If variance is positive then it is considered to be

good from company’s point of view (Knudtzon and Schmidling, 2006). But if variance is

negative then firm takes corrective actions in order to ensure that same mistakes will never get

repeated in the upcoming time period.

Corrective action/controlling- After identification of negative factors, managers carries

out discussion with their subordinates. On the basis of discussion, they find out ways that can be

adopted in order to avoid occurrence of such a poor performance again.

The main purpose of budgetary control is to motivate managers to control cost. This is done by

setting targets related to expenses in a budget. The other main purpose of budgetary control is to

ensure that expenses will remain in line that is determined in a budget. In this regard managers

start evaluation process under which actual results are compared with determine standards in

order to check that results are in line to expectation or not.

Budgetary control cycle

Responsibility- In this stage responsibilities of managers and employees are determined who will

play a key role in cost control. Responsibilities indicate expectation of top management from

managers. Hence, managers must makes an attempt to control cost.

11

3.3 Process and purpose of budgetary control

Process of budgetary control

Determine standard- This is the first stage in budgetary control process and in this step,

standards are determined for the cost and revenue. These standards are further used to identify

whether the firm gives good or poor performance (Allen, Qian and Qian, 2005).

Measuring performance- This is the second step and under this stage, performance of

the firm is measured in terms of value.

Comparison of actual performance with determined standards- In the third stage, after

measurement of performance, comparison of same is done with standards in order to identify

positive and negative points of company with respect to budget for specific quarter.

Identify variance/evalauting- By making comparison; managers identify the areas where

company gives a good and poor performance. If variance is positive then it is considered to be

good from company’s point of view (Knudtzon and Schmidling, 2006). But if variance is

negative then firm takes corrective actions in order to ensure that same mistakes will never get

repeated in the upcoming time period.

Corrective action/controlling- After identification of negative factors, managers carries

out discussion with their subordinates. On the basis of discussion, they find out ways that can be

adopted in order to avoid occurrence of such a poor performance again.

The main purpose of budgetary control is to motivate managers to control cost. This is done by

setting targets related to expenses in a budget. The other main purpose of budgetary control is to

ensure that expenses will remain in line that is determined in a budget. In this regard managers

start evaluation process under which actual results are compared with determine standards in

order to check that results are in line to expectation or not.

Budgetary control cycle

Responsibility- In this stage responsibilities of managers and employees are determined who will

play a key role in cost control. Responsibilities indicate expectation of top management from

managers. Hence, managers must makes an attempt to control cost.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.